|

市场调查报告书

商品编码

2019059

静脉输液市场商机、成长要素、产业趋势分析及2026-2035年预测。Intravenous Solutions Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

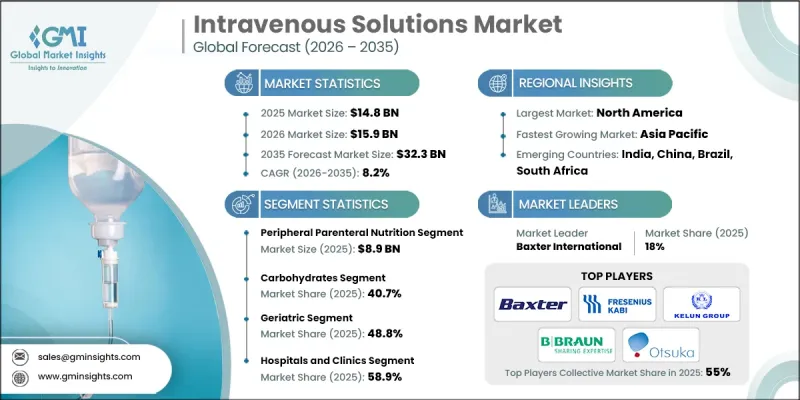

预计到 2025 年,全球静脉输液市场价值将达到 148 亿美元,并有望以 8.2% 的复合年增长率成长,到 2035 年达到 323 亿美元。

新兴国家和已开发国家营养不良盛行率的上升以及对专业营养支持需求的增加,推动了该市场的成长。静脉输液,包括肠外营养(PN),在直接向血液中输送必需营养素、体液和电解质方面发挥着至关重要的作用,尤其适用于无法口服或吸收营养的患者。医护人员也更倾向于使用预混即用型静脉输液,这类输液能够提高病患安全性和操作效率,同时最大限度地降低污染和配製错误的风险,从而进一步刺激了市场需求。此外,製剂技术的进步以及人们对及时营养干预重要性的认识不断提高,也促使医院和诊所在新生儿护理、重症监护、肿瘤科和慢性病管理等领域更多地采用静脉输液。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测期 | 2026-2035 |

| 上市时的市场规模 | 148亿美元 |

| 预测金额 | 323亿美元 |

| 复合年增长率 | 8.2% |

预计到2025年,周边静脉营养(PPN)市场规模将达89亿美元。 PPN广泛用于需要短期营养支持的患者,透过週边静脉输注胺基酸、葡萄糖和脂质等必需巨量营养素。这种疗法有助于恢復营养平衡,防止营养素进一步流失,并改善口服或肠内摄取受限患者的营养缺乏。临床研究表明,及时给予PPN可改善患者的预后和满意度。 PPN的精确配方可确保患者以正确的比例获得必需的微量营养素和宏量营养素,从而降低併发症风险,并在康復期间维持代谢稳定。医院越来越依赖PPN製剂,将其作为一种安全有效的营养支持方式,用于重症监护和外科手术环境。

预计到2025年,碳水化合物类产品将占据40.7%的市场份额,成为重要的市场贡献因素。葡萄糖类静脉输液为无法透过口服或经肠营养获得足够热量的患者提供必需的能量。这些输液能够满足细胞能量需求,防止瘦体重流失,并维持重症患者和营养不良患者的代谢平衡。富含碳水化合物的静脉输液在加护病房、外科病房和新生儿护理中尤其重要,因为这些科室能量需求高,及时的营养支持至关重要。医护人员更倾向于使用含葡萄糖的输液,因为可以根据每位患者的个别需求进行精准输注,这已成为现代肠外营养治疗中不可或缺的一部分。

预计到2025年,北美静脉输液市场将占据最大的市场份额。这主要得益于先进的医疗基础设施、大量的手术以及在各种医疗机构中广泛应用肠外营养和静脉输液疗法。美国和加拿大的医院、诊所、门诊中心以及不断扩展的家庭医疗保健服务,都在持续推动静脉输液的需求。该地区受益于由美国FDA和加拿大卫生署主导的健全法规结构,该框架对无菌、标籤、品管和GMP(良好生产规范)合规性实施严格的标准。这些法规确保了病患安全、产品品质稳定以及可靠的供应链。此外,医院采用先进技术、完善的临床方案以及即用型预混合料静脉输液,正在提高营运效率,最大限度地减少临床错误,并进一步巩固北美在静脉输液市场的主导地位。

目录

第一章:调查方法

- 研究途径

- 品质改进计划

- GMI人工智慧政策和资料完整性倡议

- 资讯来源一致性协议

- GMI人工智慧政策和资料完整性倡议

- 调查过程和可靠性评分

- 调查过程的组成部分

- 评分组成部分

- 数据收集

- 主要来源部分列表

- 资料探勘资讯来源

- 付费资讯来源

- 区域资讯来源

- 付费资讯来源

- 基本估算和计算方法

- 每种方法中基准年的计算

- 预测模型

- 量化市场影响分析

- 生长参数对预测的数学影响

- 量化市场影响分析

- 关于调查透明度的补充信息

- 资讯来源归属框架

- 品质保证指标

- 对信任的承诺

第二章执行摘要

第三章业界考察

- 生态系分析

- 影响产业的因素

- 促进因素

- 营养不良病例增加

- 早产发生率高

- 胃肠道疾病、神经系统疾病和癌症等疾病的发生率增加。

- 手术数量增加

- 产业潜在风险与挑战

- 严格的规章制度和品质要求

- 市场机会

- 居家和门诊静脉输液护理正成为日益增长的趋势。

- 促进因素

- 成长潜力分析

- 监理情势

- 北美洲

- 欧洲

- 亚太地区

- 技术趋势(基于初步调查)

- 目前技术

- 即用型 (RTU)预混合料溶液

- 个人化静脉营养配方

- 新兴技术

- 过渡到口服补液疗法

- 多腔袋和自复合袋

- 目前技术

- 未来市场趋势(基于初步研究)

- 专利分析(基于初步研究)

- 人工智慧和生成式人工智慧对市场的影响(基于初步研究)

- 波特五力分析

- PESTEL 分析

第四章 竞争情势

- 介绍

- 企业市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 企业矩阵分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 主要进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 业务拓展计划

第五章 市场估计与预测:依类型划分,2022-2035年

- 全静脉营养

- 周边静脉营养

第六章 市场估计与预测:依组成划分,2022-2035年

- 碳水化合物

- 维生素和矿物质

- 单剂量胺基酸

- 肠外脂肪乳剂

- 其他作品

第七章 市场估计与预测:依年龄组别划分,2022-2035年

- 儿童

- 成人

- 老年人

第八章 市场估计与预测:依应用领域划分,2022-2035年

- 营养支持

- 输血

- 体液和电解质平衡

- 其他用途

第九章 市场估计与预测:依最终用途划分,2022-2035年

- 医院和诊所

- 门诊手术中心

- 居家照护设施

第十章 市场估价与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第十一章:公司简介

- Aculife Healthcare

- AdvaCare Pharma

- Albert David

- Amanta Healthcare

- Axa Parenterals

- B. Braun Melsungen

- Baxter International

- CSL

- Fresenius Kabi

- Grifols

- Haisco Pharmaceutical Group

- ICU Medical

- JW Life Science

- Kelun Industry Group

- Otsuka Pharmaceutical

The Global Intravenous Solutions Market was valued at USD 14.8 billion in 2025 and is estimated to grow at a CAGR of 8.2% to reach USD 32.3 billion by 2035.

The market growth is fueled by the rising prevalence of malnutrition and an increasing need for specialized nutrition support across both emerging and developed regions. Intravenous solutions, including parenteral nutrition (PN), play a critical role in delivering essential nutrients, hydration, and electrolytes directly into the bloodstream, particularly for patients who cannot ingest or absorb nutrients orally. The demand is also driven by healthcare providers' preference for pre-mixed, ready-to-use IV solutions, which minimize the risks of contamination and preparation errors while enhancing patient safety and operational efficiency. In addition, advancements in formulation technology and increasing awareness of the importance of timely nutritional intervention have encouraged hospitals and clinics to adopt IV solutions for neonatal, critical care, oncology, and chronic disease management.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $14.8 Billion |

| Forecast Value | $32.3 Billion |

| CAGR | 8.2% |

The peripheral parenteral nutrition (PPN) segment generated USD 8.9 billion in 2025. PPN is widely used for patients requiring short-term nutritional support, delivering vital macronutrients like amino acids, dextrose, and lipids through peripheral veins. The solution helps restore nutrient balance, prevent further nutritional depletion, and correct deficiencies in patients with limited oral or enteral intake. Clinical studies indicate that the timely administration of PPN improves patient outcomes and satisfaction. The precise formulation of PPN ensures that patients receive the necessary micromolecules and macromolecules in the right proportion, reducing the risk of complications and supporting metabolic stability during recovery periods. Hospitals increasingly rely on PPN solutions as a safe, efficient method to maintain nutritional support in critical care and surgical settings.

The carbohydrates segment accounted for 40.7% share in 2025, establishing the segment as a key contributor. Dextrose-based IV solutions provide essential energy for patients who cannot obtain adequate calories orally or through enteral feeding. These solutions support cellular energy requirements, prevent the breakdown of lean body mass, and maintain metabolic balance in critically ill and malnourished patients. The use of carbohydrate-enriched IV fluids is particularly critical in intensive care units, surgical wards, and neonatal care, where energy demands are high and timely nutrient delivery is essential. Clinicians favor dextrose-containing solutions because they can be accurately dosed to meet individual patient needs, making them indispensable in modern parenteral nutrition therapy.

North America Intravenous Solutions Market held the largest market share in 2025, driven by advanced healthcare infrastructure, high surgical procedure volumes, and widespread use of parenteral nutrition and IV fluid therapy across multiple care settings. Hospitals, clinics, ambulatory centers, and expanding home healthcare services in the U.S. and Canada have created sustained demand for intravenous solutions. The region benefits from a strong regulatory framework, led by the U.S. FDA and Health Canada, which enforces rigorous standards for sterility, labeling, quality control, and GMP compliance. These regulations ensure patient safety, consistent product quality, and reliable supply chains. Additionally, technological adoption in hospitals, advanced clinical protocols, and integration of ready-to-use pre-mixed IV solutions enhance operational efficiency and minimize clinical errors, further consolidating North America's dominance in the intravenous solutions market.

Key players operating in the Global Intravenous Solutions Market include Baxter International, B. Braun Melsungen, Fresenius Kabi, Grifols, ICU Medical, AdvaCare Pharma, JW Life Science, Otsuka Pharmaceutical, Aculife Healthcare, Amanta Healthcare, Albert David, Axa Parenterals, and Haisco Pharmaceutical Group. Companies in the Intravenous Solutions Market strengthen their presence by focusing on developing pre-mixed, ready-to-use formulations that reduce contamination risk and enhance operational efficiency. They invest in advanced manufacturing technologies to improve sterility, stability, and shelf life. Strategic collaborations with hospitals, clinics, and home healthcare providers help expand distribution networks and increase product adoption. Market leaders also prioritize regulatory compliance, leveraging certifications from U.S. FDA, Health Canada, and other authorities to build trust and maintain quality standards. Additionally, companies emphasize product innovation, offering customized nutrient compositions tailored for neonatal, critical care, and oncology patients.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.3 Type trends

- 2.4 Compositions trends

- 2.5 Age group trends

- 2.6 Application trends

- 2.7 End use trends

- 2.8 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing cases of malnutrition

- 3.2.1.2 High prevalence of pre-term births

- 3.2.1.3 Increasing prevalence of diseases, such as gastrointestinal disorder, neurological diseases, and cancer

- 3.2.1.4 Increasing number of surgical procedures

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Stringent regulatory and quality requirements

- 3.2.3 Market opportunity

- 3.2.3.1 Rising shift toward home-based and outpatient infusion care

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technological landscape (Driven by Primary Research)

- 3.5.1 Current technologies

- 3.5.1.1 Ready-to-use (RTU) premixed solutions

- 3.5.1.2 Personalized IV nutrition formulations

- 3.5.2 Emerging technologies

- 3.5.2.1 Shift toward oral rehydration therapy

- 3.5.2.2 Multi-chamber and self-compounding bags

- 3.5.1 Current technologies

- 3.6 Future market trends (Driven by Primary Research)

- 3.7 Patent analysis (Driven by Primary Research)

- 3.8 Impact of AI and generative AI on the market (Driven by Primary Research)

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2022 - 2035 ($ Mn and Units)

- 5.1 Key trends

- 5.2 Total parenteral nutrition

- 5.3 Peripheral parenteral nutrition

Chapter 6 Market Estimates and Forecast, By Composition, 2022 - 2035 ($ Mn and Units)

- 6.1 Key trends

- 6.2 Carbohydrates

- 6.3 Vitamins and minerals

- 6.4 Single-dose amino acids

- 6.5 Parenteral lipid emulsion

- 6.6 Other compositions

Chapter 7 Market Estimates and Forecast, By Age Group, 2022 - 2035 ($ Mn and Units)

- 7.1 Key trends

- 7.2 Pediatric

- 7.3 Adults

- 7.4 Geriatric

Chapter 8 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Nutritional support

- 8.3 Blood transfusion

- 8.4 Fluid and electrolyte balance

- 8.5 Other applications

Chapter 9 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 Hospitals and clinics

- 9.3 Ambulatory surgery centers

- 9.4 Home care settings

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn and Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Aculife Healthcare

- 11.2 AdvaCare Pharma

- 11.3 Albert David

- 11.4 Amanta Healthcare

- 11.5 Axa Parenterals

- 11.6 B. Braun Melsungen

- 11.7 Baxter International

- 11.8 CSL

- 11.9 Fresenius Kabi

- 11.10 Grifols

- 11.11 Haisco Pharmaceutical Group

- 11.12 ICU Medical

- 11.13 JW Life Science

- 11.14 Kelun Industry Group

- 11.15 Otsuka Pharmaceutical

静脉注射市场:按产品类型、包装类型、分销管道、应用和最终用户分類的全球市场预测 – 2026-2032 年

静脉注射市场:按产品类型、包装类型、分销管道、应用和最终用户分類的全球市场预测 – 2026-2032 年 静脉输液市场规模、份额、趋势和预测:按类型、营养成分和地区划分,2026-2034年

静脉输液市场规模、份额、趋势和预测:按类型、营养成分和地区划分,2026-2034年 全球静脉输液市场规模、份额、趋势和成长分析报告(2026-2034年)日本静脉输液市场规模、份额、趋势和预测:按类型、营养成分和地区划分,2026-2034年

全球静脉输液市场规模、份额、趋势和成长分析报告(2026-2034年)日本静脉输液市场规模、份额、趋势和预测:按类型、营养成分和地区划分,2026-2034年 静脉输液市场规模、份额和成长分析(按产品、营养成分和地区划分)—产业预测(2026-2033 年)

静脉输液市场规模、份额和成长分析(按产品、营养成分和地区划分)—产业预测(2026-2033 年) 静脉输液市场规模、份额和趋势分析报告:按类型、营养成分、最终用途、地区和细分市场预测(2026-2033 年)

静脉输液市场规模、份额和趋势分析报告:按类型、营养成分、最终用途、地区和细分市场预测(2026-2033 年) Ringer's Solution:2025-2031年全球市占率与排名、总收入与需求预测

Ringer's Solution:2025-2031年全球市占率与排名、总收入与需求预测 全球药用级氯化钾市场:依通路、应用和地区(~2035年)

全球药用级氯化钾市场:依通路、应用和地区(~2035年) 静脉输液市场:市场规模、份额、前景、按解决方案、输液袋类型、应用、最终用户和地区分類的机会分析,2025 年至 2032 年美国静脉注射注射液市场规模、份额、趋势分析报告:按产品、营养、最终用途、细分市场预测,2025-2030 年

静脉输液市场:市场规模、份额、前景、按解决方案、输液袋类型、应用、最终用户和地区分類的机会分析,2025 年至 2032 年美国静脉注射注射液市场规模、份额、趋势分析报告:按产品、营养、最终用途、细分市场预测,2025-2030 年