|

市场调查报告书

商品编码

2019154

自修復聚合物市场商机、成长要素、产业趋势分析及2026-2035年预测。Self-repairing Polymers Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

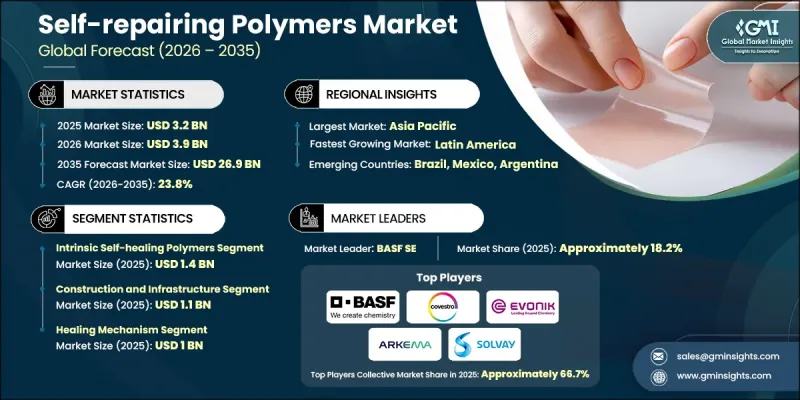

全球自修復聚合物市场预计到 2025 年价值 32 亿美元,预计到 2035 年将达到 269 亿美元,复合年增长率为 23.8%。

随着材料科学领域对耐久性、延长产品寿命和持续性能的要求日益提高,自修復聚合物市场呈现强劲的成长动能。这些先进聚合物旨在损伤后恢復其机械、化学和功能特性,从而减少维修和材料更换的频率。此领域的研究主要集中在「内在体系」(依赖聚合物结构内部的可逆键结)和「外在体系」(包含修復剂)两方面。聚合物化学、奈米技术和仿生材料设计的不断进步,正在拓展这些材料的应用范围,使其能够应用于要求更高的领域。在材料失效可能导致高成本和安全风险的领域,自修復聚合物的应用日益广泛,这推动了市场成长。自修復聚合物有助于延长各行业的产品寿命并提高可靠性。持续的创新旨在提高修復速度、一致性和结构完整性。人们对永续材料解决方案的日益关注以及对循环经济原则的日益重视,进一步推动了对自修復聚合物的需求,这有助于减少废弃物并提高资源利用效率。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测期 | 2026-2035 |

| 上市时的市场规模 | 32亿美元 |

| 预测金额 | 269亿美元 |

| 复合年增长率 | 23.8% |

预计到2025年,本征自修復聚合物市场规模将达14亿美元,并在2026年至2035年间以23%的复合年增长率成长。该市场占据重要地位,原因在于其能够透过嵌入聚合物基体内部的可逆键结机制来修復损伤。这些材料无需外部试剂即可进行多次修復循环,从而保持结构完整性和长期性能。它们能够从微损伤中恢復,使其成为即使在反覆应力条件下也需要保持稳定功能的应用的理想选择。这种可靠性,加上低维护成本和轻量化结构等特性,持续吸引业界的浓厚兴趣。

预计到2025年,修復机制市场规模将达到10亿美元,占市场份额的30.7%,并将在2035年之前以22.4%的复合年增长率成长。修復机制的类型在决定材料从损伤中恢復的有效性、修復过程的频率以及材料长期稳定性方面起着至关重要的作用。虽然修復效率、恢復速度和环境耐受性等因素会影响整体性能,但背后的修復机制仍然是决定材料在各种使用条件和应用中性能的关键因素。

预计到2025年,北美自修復聚合物市场规模将达到8.685亿美元。该地区受益于完善的研究生态系统、先进材料的早期应用以及在高科技产业的广泛应用。美国凭藉着强大的研究机构网络、专业製造商和创新主导产业,正引领区域发展。加拿大则透过持续推动以永续材料和基础设施为重点的研究倡议,为区域发展做出贡献,从而支持整体市场扩张。

目录

第一章:调查方法

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 每个阶段增加的价值

- 影响价值链的因素

- 中断

- 影响产业的因素

- 促进因素

- 产业潜在风险与挑战

- 市场机会

- 成长潜力分析

- 监理情势

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特五力分析

- PESTEL 分析

- 价格趋势

- 按地区

- 副产品

- 未来市场趋势

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 专利趋势

- 贸易统计

- 主要进口国

- 主要出口国

- 永续性和环境方面

- 永续倡议

- 减少废弃物策略

- 生产中的能源效率

- 环保意识的倡议

- 关于碳足迹的考量

第四章 竞争情势

- 介绍

- 企业市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 按地区

- 企业矩阵分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 主要进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 业务拓展计划

第五章 市场估计与预测:依类型划分,2022-2035年

- 本征自修復聚合物

- 基于可逆共用价键

- 基于超分子交互作用

- 形状记忆聚合物

- 其他的

- 外源性自修復聚合物

- 微胶囊系统

- 血管网路系统

- 超细纤维增强

- 其他的

- 混合式自癒系统

- 内在系统与外在系统的结合

- 多机制系统

- 其他的

第六章 市场估计与预测:依应用领域划分,2022-2035年

- 建筑和基础设施

- 自癒混凝土

- 保护涂层

- 密封剂和黏合剂

- 其他的

- 汽车和航太

- 结构部件

- 涂料和油漆

- 室内使用

- 其他的

- 电子与能源

- 电池零件

- 软性电子产品

- 太阳能板

- 其他的

- 生医医疗保健

- 组织工程

- 药物输送系统

- 医疗设备

- 其他的

- 消费品

- 包装

- 保护膜

- 纤维

- 其他的

- 其他的

第七章 市场估计与预测:依性能特征划分,2022-2035年

- 修復机制

- 热启用

- 光激活

- pH响应性

- 机械激活

- 其他的

- 维修效率

- 高效率(>80%)

- 中等效率(50-80%)

- 效率低(<50%)

- 疗癒时间

- 快速癒合(不到1小时)

- 中等癒合速度(1-24小时)

- 癒合速度慢(超过24小时)

- 环境稳定性

- 耐热性

- 化学耐受性

- 抗紫外线

- 其他的

第八章 市场估计与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿拉伯聯合大公国

- 其他中东和非洲地区

第九章:公司简介

- BASF SE

- Arkema

- Covestro AG

- Evonik Industries AG

- The Dow Chemical Company

- Sika AG

- Solvay SA

- Toray Industries, Inc.

- NEI Corporation

The Global Self-Repairing Polymers Market was valued at USD 3.2 billion in 2025 and is estimated to grow at a CAGR of 23.8% to reach USD 26.9 billion by 2035.

The self-repairing polymers market is gaining strong momentum as material science increasingly emphasizes durability, extended product life, and sustained performance. These advanced polymers are engineered to restore their mechanical, chemical, and functional properties after damage, reducing the frequency of repairs and material replacement. Research in this field is focused on both intrinsic systems, which rely on reversible bonding within the polymer structure, and extrinsic systems that incorporate embedded healing agents. Continuous advancements in polymer chemistry, nanotechnology, and bio-inspired material design are expanding the scope of these materials across demanding applications. Market growth is being driven by rising adoption in sectors where material failure can result in high costs or safety risks. Self-repairing polymers contribute to longer product lifecycles and improved reliability across various industries. Ongoing innovation is aimed at enhancing healing speed, consistency, and structural integrity. Increasing awareness of sustainable material solutions and the growing focus on circular economy principles are further supporting the demand for self-repairing polymers, as they help reduce waste and improve resource efficiency.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $3.2 Billion |

| Forecast Value | $26.9 Billion |

| CAGR | 23.8% |

The intrinsic self-healing polymers segment accounted for USD 1.4 billion in 2025 and is projected to grow at a CAGR of 23% from 2026 to 2035. This segment holds a prominent position due to its ability to repair damage through reversible bonding mechanisms embedded within the polymer matrix. These materials can undergo multiple healing cycles without requiring external agents, preserving their structural integrity and long-term performance. Their capability to recover from micro-level damage makes them highly suitable for applications requiring consistent functionality under repeated stress conditions. This reliability, combined with reduced maintenance needs and lightweight characteristics, continues to drive strong interest from industrial sectors.

The healing mechanism segment reached USD 1 billion in 2025, accounting for 30.7% share, and is anticipated to grow at a CAGR of 22.4% through 2035. The type of healing mechanism plays a critical role in determining how effectively a material can recover from damage, how frequently the healing process can occur, and how stable the material remains over time. Factors such as healing efficiency, recovery speed, and environmental resistance influence overall performance; however, the underlying healing mechanism remains the key factor shaping material behavior across different operating conditions and applications.

North America Self-Repairing Polymers Market was valued at USD 868.5 million in 2025. The region benefits from a well-established research ecosystem, early adoption of advanced materials, and broad application across high-technology industries. The United States leads regional development, supported by a strong network of research institutions, specialized manufacturers, and innovation-driven industries. Canada contributes to regional progress through continued advancements in sustainable materials and infrastructure-focused research initiatives, supporting the overall expansion of the market.

Key companies operating in the Global Self-Repairing Polymers Market include Covestro AG, Arkema, BASF SE, Evonik Industries AG, The Dow Chemical Company, Solvay S.A., Sika AG, Toray Industries, Inc., and NEI Corporation. Companies in the self-repairing polymers market are strengthening their competitive position through continuous innovation, strategic collaborations, and expansion into high-growth application areas. They are investing heavily in research and development to improve the healing efficiency, durability, and environmental performance of advanced polymer systems. Partnerships with end-use industries are enabling the development of customized solutions tailored to specific performance requirements. Manufacturers are also focusing on scaling production capabilities and optimizing supply chains to meet increasing demand efficiently. In addition, companies are exploring sustainable material innovations and integrating advanced technologies such as nanomaterials to enhance product functionality, while expanding their presence in emerging markets to capture new growth opportunities.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Application

- 2.2.4 Performance Characteristics

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and Environmental Aspects

- 3.12.1 Sustainable Practices

- 3.12.2 Waste Reduction Strategies

- 3.12.3 Energy Efficiency in Production

- 3.12.4 Eco-friendly Initiatives

- 3.13 Carbon Footprint Considerations

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Type, 2022- 2035 (USD Billion, Kilo Tons)

- 5.1 Key trends

- 5.2 Intrinsic Self-healing Polymers

- 5.2.1 Reversible Covalent Bond-based

- 5.2.2 Supramolecular Interaction-based

- 5.2.3 Shape Memory Polymers

- 5.2.4 Others

- 5.3 Extrinsic Self-healing Polymers

- 5.3.1 Microcapsule-based Systems

- 5.3.2 Vascular Network Systems

- 5.3.3 Microfiber Reinforcement

- 5.3.4 Others

- 5.4 Hybrid Self-healing Systems

- 5.4.1 Combined Intrinsic-Extrinsic Systems

- 5.4.2 Multi-mechanism Systems

- 5.4.3 Others

Chapter 6 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Billion, Kilo Tons)

- 6.1 Key trends

- 6.2 Construction and Infrastructure

- 6.2.1 Self-healing Concrete

- 6.2.2 Protective Coatings

- 6.2.3 Sealants and Adhesives

- 6.2.4 Others

- 6.3 Automotive and Aerospace

- 6.3.1 Structural Components

- 6.3.2 Coatings and Paints

- 6.3.3 Interior Applications

- 6.3.4 Others

- 6.4 Electronics and Energy

- 6.4.1 Battery Components

- 6.4.2 Flexible Electronics

- 6.4.3 Solar Panels

- 6.4.4 Others

- 6.5 Biomedical and Healthcare

- 6.5.1 Tissue Engineering

- 6.5.2 Drug Delivery Systems

- 6.5.3 Medical Devices

- 6.5.4 Others

- 6.6 Consumer Products

- 6.6.1 Packaging

- 6.6.2 Protective Films

- 6.6.3 Textiles

- 6.6.4 Others

- 6.7 Others

Chapter 7 Market Estimates and Forecast, By Performance Characteristics, 2022 - 2035 (USD Billion, Kilo Tons)

- 7.1 Key trends

- 7.2 Healing Mechanism

- 7.2.1 Thermally Activated

- 7.2.2 Light-activated

- 7.2.3 pH-responsive

- 7.2.4 Mechanically Activated

- 7.2.5 Others

- 7.3 Healing Efficiency

- 7.3.1 High Efficiency (>80%)

- 7.3.2 Medium Efficiency (50-80%)

- 7.3.3 Low Efficiency (<50%)

- 7.4 Healing Time

- 7.4.1 Rapid Healing (<1 hour)

- 7.4.2 Moderate Healing (1-24 hours)

- 7.4.3 Slow Healing (>24 hours)

- 7.5 Environmental Stability

- 7.5.1 Temperature Resistant

- 7.5.2 Chemical Resistant

- 7.5.3 UV Resistant

- 7.5.4 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion, Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East & Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East & Africa

Chapter 9 Company Profiles

- 9.1 BASF SE

- 9.2 Arkema

- 9.3 Covestro AG

- 9.4 Evonik Industries AG

- 9.5 The Dow Chemical Company

- 9.6 Sika AG

- 9.7 Solvay S.A.

- 9.8 Toray Industries, Inc.

- 9.9 NEI Corporation