|

市场调查报告书

商品编码

2019158

智慧水錶市场机会、成长要素、产业趋势分析及2026-2035年预测Smart Water Meter Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

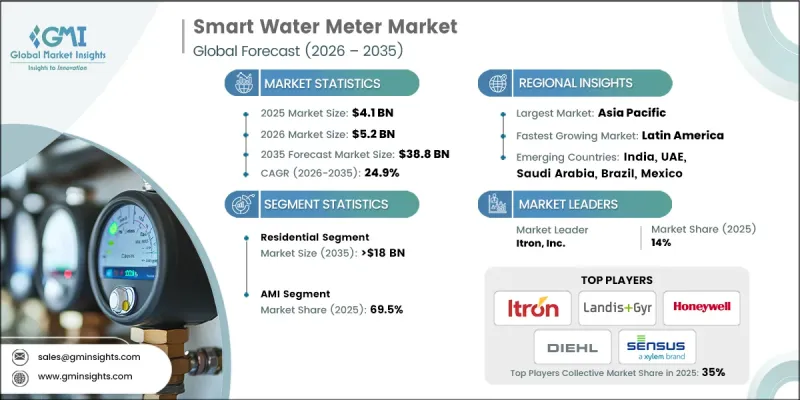

全球智慧水錶市场预计到 2025 年将价值 41 亿美元,并将以 24.9% 的复合年增长率成长,到 2035 年达到 388 亿美元。

这一快速增长是由技术的快速发展、节水措施的不断加强、监管要求以及对更高效水资源管理系统的需求所驱动的。世界各地的供水事业和城市都在部署智慧水錶,以优化供水、减少浪费并提高营运效率。对精确、即时用水监测的需求是成长要素,因为传统水錶通常依赖耗时且容易出错的人工抄表。整合物联网技术的智慧水錶能够实现远端监控、自动计费和即时数据采集,从而提高效率和服务品质。政府推行的节水和漏水侦测政策及奖励计画进一步加速了智慧水錶的普及,尤其是在缺水地区。此外,不断加强的数位化建设和永续性目标,尤其是在水利基础设施现代化至关重要的新兴经济体,也为市场成长提供了支持。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测期 | 2026-2035 |

| 初始市场规模 | 41亿美元 |

| 预测金额 | 388亿美元 |

| 复合年增长率 | 24.9% |

预计到2035年,住宅市场规模将达到180亿美元,这主要得益于消费者对智慧电錶的日益普及,以支持更高效的水和能源管理、更精准的计费以及可再生能源的併网。家用智慧电錶透过实现精准的用量追踪、帮助消费者管理用电量以及与智慧家居系统无缝集成,正在推动市场成长。

具备双向通讯功能的先进计量基础设施 (AMI) 预计将超越自动抄表 (AMR) 系统,并在 2025 年占据 69.5% 的市场份额。 AMI 使公共产业能够收集即时数据、远端系统管理水錶、快速检测洩漏并迅速回应异常。与智慧电网和数位化水资源管理解决方案的整合进一步巩固了其优势,使其成为高效公共产业营运的最佳技术。

预计2025年,美国智慧水錶市场规模将达7.04亿美元。在美国,由于人口成长、基础设施老化以及气候变迁的影响,多个地区的水资源短缺问题日益严峻。美国公共产业正在扩大智慧水錶的部署,以即时监测用水量、识别洩漏并检测异常用水模式,旨在节约用水并提高营运效率。

目录

第一章:调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 监理情势

- 区域价格趋势分析(以美元计)

- 影响产业的因素

- 促进因素

- 产业潜在风险与挑战

- 成长潜力分析

- 波特五力分析

- PESTEL 分析

- 新机会与趋势

- 数位化和物联网集成

- 进入新兴市场

- 投资分析及未来展望

第四章 竞争情势

- 介绍

- 企业市占率分析:按地区划分

- 北美洲

- 欧洲

- 亚太地区

- 中东和非洲

- 拉丁美洲

- 策略倡议

- 竞争标竿分析图

- 战略仪錶板

- 创新与科技趋势

第五章 市场规模及预测:依应用领域划分,2022-2035年

- 住宅

- 商业的

- 公共产业

- AMI

- AMR

第六章 市场规模与预测:依产品划分,2022-2035年

- 热水錶

- 冷水錶

第七章 市场规模及预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 瑞典

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 澳洲

- 中东和非洲

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 南非

- 埃及

- 拉丁美洲

- 巴西

- 阿根廷

第八章:公司简介

- ABB

- Apator SA

- Arad Group:

- Badger Meter, Inc.

- BMETERS Srl

- Diehl Stiftung & Co. KG

- Honeywell International Inc.

- Itron Inc.

- Kamstrup

- Landis+Gyr

- Neptune Technology Group Inc.

- Ningbo Water Meter Co., Ltd.

- Schneider Electric

- Siemens

- Sontex SA

- Xylem(Sensus)

- ZENNER International GmbH & Co. KG

- Suez

- Baylan Water Meters

- BOVE Technology

The Global Smart Water Meter Market was valued at USD 4.1 billion in 2025 and is estimated to grow at a CAGR of 24.9% to reach USD 38.8 billion by 2035.

The surge is driven by rapid technological advancements, increasing water conservation initiatives, regulatory mandates, and the need for more efficient water management systems. Utilities and cities worldwide are adopting smart water meters to optimize water distribution, minimize wastage, and enhance operational efficiency. The demand for accurate, real-time monitoring of water consumption is a key growth factor, as conventional meters often rely on manual readings that are time-consuming and prone to errors. Smart meters integrated with IoT technology provide remote monitoring, automated billing, and real-time data collection, boosting efficiency and service quality. Government policies and incentive programs promoting water conservation and leakage detection, particularly in water-stressed regions, are further accelerating adoption. The market is also supported by growing digitalization efforts and sustainability goals, especially in emerging economies where water infrastructure modernization is critical.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $4.1 Billion |

| Forecast Value | $38.8 Billion |

| CAGR | 24.9% |

The residential segment is expected to reach USD 18 billion by 2035, driven by rising consumer adoption of smart meters to improve water and energy management, enable accurate billing, and support renewable energy integration. Smart meters in homes provide precise usage insights, empower consumers to manage consumption, and integrate seamlessly with home automation systems, contributing to market growth.

The AMI (Advanced Metering Infrastructure) segment captured 69.5% share in 2025, leading over AMR (Automatic Meter Reading) systems due to its two-way communication capabilities. AMI enables utilities to collect real-time data, remotely manage meters, detect leaks promptly, and respond faster to anomalies. Its integration with smart grids and digital water management solutions further reinforces its dominance, making it the preferred technology for efficient utility operations.

U.S. Smart Water Meter Market was valued at USD 704 million in 2025. The country faces rising water scarcity across several regions, influenced by population growth, aging infrastructure, and climate variability. Utilities in the U.S. are increasingly deploying smart meters to monitor consumption in real-time, identify leaks, and detect abnormal usage patterns, enhancing water conservation and operational efficiency.

Key players in the Global Smart Water Meter Market include Landis + Gyr, Diehl Stiftung, Itron, Inc., Honeywell International, and Xylem (Sensus). Companies in the Smart Water Meter Market are strengthening their presence through continuous innovation in IoT-enabled metering solutions and real-time analytics. They are focusing on strategic collaborations with utilities, governments, and technology providers to expand deployment and offer integrated water management systems. R&D investments drive the development of highly accurate, low-maintenance, and energy-efficient meters. Businesses are also leveraging data-driven services, remote diagnostics, and predictive maintenance to enhance customer value and operational reliability. Regional expansion, participation in government incentive programs, and sustainable product development are additional strategies to solidify their market foothold and capture a larger share of the rapidly growing smart water meter industry.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Price trend analysis, by region (USD/Unit)

- 3.4 Industry impact forces

- 3.4.1 Growth drivers

- 3.4.2 Industry pitfalls & challenges

- 3.5 Growth potential analysis

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

- 3.7.1 Political factors

- 3.7.2 Economic factors

- 3.7.3 Social factors

- 3.7.4 Technological factors

- 3.7.5 Legal factors

- 3.7.6 Environmental factors

- 3.8 Emerging opportunities & trends

- 3.8.1 Digitalization & IoT integration

- 3.8.2 Emerging market penetration

- 3.9 Investment analysis & future outlook

Chapter 4 Competitive Landscape, 2026

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Strategic initiatives

- 4.4 Competitive benchmarking depictions

- 4.5 Strategy dashboard

- 4.6 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Application, 2022 - 2035 (USD Million & '000 Units)

- 5.1 Key trends

- 5.2 Residential

- 5.3 Commercial

- 5.4 Utility

- 5.5 Market Size and Forecast, By Technology, 2022 - 2035 (USD Million & '000 Units)

- 5.6 Key trends

- 5.7 AMI

- 5.8 AMR

Chapter 6 Market Size and Forecast, By Product, 2022 - 2035 (USD Million & '000 Units)

- 6.1 Key trends

- 6.2 Hot water meter

- 6.3 Cold water meter

Chapter 7 Market Size and Forecast, By Region, 2022 - 2035 (USD Million & '000 Units)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.2.3 Mexico

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Italy

- 7.3.5 Sweden

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Japan

- 7.4.3 India

- 7.4.4 South Korea

- 7.4.5 Australia

- 7.5 Middle East & Africa

- 7.5.1 UAE

- 7.5.2 Saudi Arabia

- 7.5.3 South Africa

- 7.5.4 Egypt

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Argentina

Chapter 8 Company Profiles

- 8.1 ABB

- 8.2 Apator S.A.

- 8.3 Arad Group:

- 8.4 Badger Meter, Inc.

- 8.5 BMETERS S.r.l

- 8.6 Diehl Stiftung & Co. KG

- 8.7 Honeywell International Inc.

- 8.8 Itron Inc.

- 8.9 Kamstrup

- 8.10 Landis+Gyr

- 8.11 Neptune Technology Group Inc.

- 8.12 Ningbo Water Meter Co., Ltd.

- 8.13 Schneider Electric

- 8.14 Siemens

- 8.15 Sontex SA

- 8.16 Xylem (Sensus)

- 8.17 ZENNER International GmbH & Co. KG

- 8.18 Suez

- 8.19 Baylan Water Meters

- 8.20 BOVE Technology

智慧水錶市场:按组件、技术、通讯技术、最终用户和安装类型划分-2026-2032年全球市场预测预付式智慧水錶市场:按组件、水錶类型、技术、部署模式、最终用户和分销管道划分——2026-2032年全球预测

智慧水錶市场:按组件、技术、通讯技术、最终用户和安装类型划分-2026-2032年全球市场预测预付式智慧水錶市场:按组件、水錶类型、技术、部署模式、最终用户和分销管道划分——2026-2032年全球预测 2026年全球智慧水錶市场报告智慧超音波水錶市场:按安装方式、类型、连接方式、水錶尺寸、最终用户和应用划分——全球预测,2026-2032年磁感应脉衝智慧水錶市场按最终用户、技术、通讯方式、应用、安装类型、连接类型、收费方式和材料分類的全球预测(2026-2032年)

2026年全球智慧水錶市场报告智慧超音波水錶市场:按安装方式、类型、连接方式、水錶尺寸、最终用户和应用划分——全球预测,2026-2032年磁感应脉衝智慧水錶市场按最终用户、技术、通讯方式、应用、安装类型、连接类型、收费方式和材料分類的全球预测(2026-2032年) 中东和非洲(MEA)智慧水錶解决方案市场成长机会:预测至2032年全球智慧水錶市场规模、份额、趋势和成长分析报告(2026-2034年)智慧饮水机市场按产品类型、技术、水类型、材料、容量、电源、最终用途和分销管道划分 - 2025-2030 年全球预测

中东和非洲(MEA)智慧水錶解决方案市场成长机会:预测至2032年全球智慧水錶市场规模、份额、趋势和成长分析报告(2026-2034年)智慧饮水机市场按产品类型、技术、水类型、材料、容量、电源、最终用途和分销管道划分 - 2025-2030 年全球预测 AMI 水錶的全球市场全球AMI智慧水錶市场

AMI 水錶的全球市场全球AMI智慧水錶市场