|

市场调查报告书

商品编码

2019203

印表机市场机会、成长要素、产业趋势分析及2026-2035年预测。Printer Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

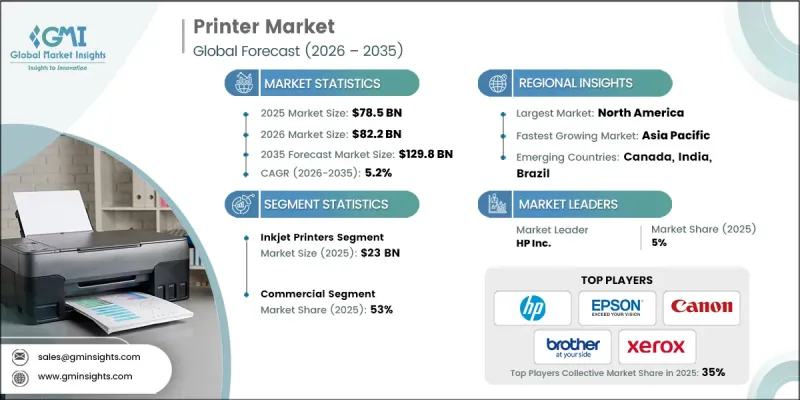

2025年全球印表机市场价值为785亿美元,预计到2035年将以5.2%的复合年增长率成长至1,298亿美元。

印表机不再只是创建文件的工具;它们被视为具备物联网连接、云端服务以及与智慧型设备相容性的智慧工具。企业可以从中受益,例如优化列印操作、降低成本和增强安全性;而消费者则可以享受便利性、即时墨水余量检查和自动化工作流程解决方案。基于云端的列印和资料传输功能可保护敏感讯息,并确保只有授权负责人才能存取文件。这些智慧功能提高了整体效率,使印表机成为企业和住宅环境中不可或缺的合作伙伴,同时协助数位转型和流程优化。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测期 | 2026-2035 |

| 初始市场规模 | 785亿美元 |

| 预测金额 | 1298亿美元 |

| 复合年增长率 | 5.2% |

喷墨印表机目前占29.4%的市场份额,预计2025年市场规模将达到230亿美元。其多功能性使其适用于从住宅文件和照片列印到商业用途的各种应用,并拥有广泛的使用者群体。喷墨印表机凭藉其高品质的彩色输出、经济高效的运作以及灵活的设计特性(例如独立墨盒和紧凑的机壳),对家庭用户和商业用户都极具吸引力。

预计到2025年,商用印表机市场规模将达到416亿美元,市占率将达53%。商用印表机是推动市场成长的主要动力,这主要得益于办公室、教育机构和零售商等场所的大批量列印需求。可靠性、多功能性、高速输出和强大的安全功能正日益受到企业的青睐。

美国印表机市场占72%的份额,预计到2025年将达到169亿美元。强大的技术基础设施、数位印刷的广泛应用以及注重安全性和託管列印服务的高级产品的部署,正在巩固北美市场的主导地位。资料保护方面的监管要求进一步加速了安全性、云端连线列印系统的普及。

目录

第一章:调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 每个阶段增加的价值

- 影响价值链的因素

- 影响产业的因素

- 促进因素

- 对环保和永续印刷解决方案的需求日益增长

- 智慧印刷技术的进步

- 数位化进程的推进以及对託管列印服务的关注

- 产业潜在风险与挑战

- 高阶商用车型的初始成本相对较高。

- 快速过渡到无纸化社会

- 机会

- 3D列印应用领域的拓展

- 智慧功能整合(物联网、云端连线)

- 促进因素

- 成长潜力分析

- 未来市场趋势

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 价格分析(基于初步调查)

- 对过去价格趋势的分析(基于初步研究)

- 根据业务类型分類的定价策略(高端/价值/成本加成)(基于初步调查)

- 监理情势

- 标准和合规要求

- 区域法规结构

- 认证标准

- 波特五力分析

- PESTEL 分析

- 贸易数据分析(基于初步调查)

- 进出口数量和价值趋势(基于初步调查)

- 主要贸易走廊及关税影响(基于初步调查)

- 人工智慧和生成式人工智慧对市场的影响

- 人工智慧驱动的列印管理和预测性维护

- 针对特定领域的生成式人工智慧应用案例和实施蓝图

- 风险、限制和监管考量

- 基础设施和实施情况(基于初步调查)

- 按地区和购买者群体分類的采用率和渗透率(基于初步调查)

- 基础设施投资的可扩展性限制和趋势(基于初步调查)

第四章 竞争情势

- 介绍

- 企业市占率分析

- 按地区

- 企业矩阵分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 主要进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 业务拓展计划

第五章 市场估计与预测:依类型划分,2022-2035年

- 喷墨印表机

- 雷射印表机

- 点阵印表机

- 3D印表机

- 胶印机

- 柔版印刷

- 其他的

第六章 市场估计与预测:依功能划分,2022-2035年

- 单功能印表机

- 多功能设备

第七章 市场估计与预测:以连结方式划分,2022-2035年

- 有线

- 无线

第八章 市场估计与预测:依价格划分,2022-2035年

- 低的

- 中等的

- 高的

第九章 市场估价与预测:依最终用户划分,2022-2035年

- 工业的

- 住宅

- 商业的

- 公司总部

- 卫生保健

- 教育

- 饭店业

- 其他(活动策划公司等)

第十章 市场估价与预测:依销售管道划分,2022-2035年

- 在线的

- 电子商务

- 企业网站

- 离线

- 量贩店

- 品牌自营店

- 其他的

第十一章 市场估价与预测:按地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第十二章:公司简介

- HP Inc.

- Epson

- Canon Inc.

- Brother Industries

- Xerox Holdings

- Ricoh Company

- Konica Minolta

- Kyocera Corporation

- Lexmark International

- Stratasys Ltd.

- 3D Systems

- Sharp Corporation

- Fujifilm Holdings

- Roland DG

- Toshiba

The Global Printer Market was valued at USD 78.5 billion in 2025 and is estimated to grow at a CAGR of 5.2% to reach USD 129.8 billion by 2035.

Printers are no longer seen merely as devices for producing documents but as intelligent tools integrated with IoT connectivity, cloud services, and smart device compatibility. Businesses benefit from optimized printing operations, reduced costs, and enhanced security, while consumers enjoy convenience, real-time ink monitoring, and automated workflow solutions. Cloud-based printing and data transmission features safeguard sensitive information, ensuring only authorized personnel can access documents. These smart functionalities improve overall efficiency, positioning printers as essential partners in both professional and residential environments while supporting digital adoption and process optimization.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $78.5 Billion |

| Forecast Value | $129.8 Billion |

| CAGR | 5.2% |

The inkjet printers segment held a 29.4% share, generating USD 23 billion in 2025. Their versatility caters to multiple applications, from residential document and photo printing to commercial needs, making them a popular choice across diverse user segments. Inkjet printers provide high-quality color output, cost-efficient operation, and flexible designs, including individual ink cartridges and compact form factors, appealing to both households and businesses.

The commercial segment generated USD 41.6 billion in 2025, representing 53% share. Commercial printers dominate due to high-volume demands from offices, educational institutions, and retail operations. Reliability, multifunction capabilities, high-speed output, and robust security features drive preference among organizations.

U.S. Printer Market accounted for 72% share, generating USD 16.9 billion in 2025. Strong technology infrastructure, digital printing adoption, and a premium product focus on security and managed print services reinforce North America's leadership. Regulatory requirements for data protection further accelerate the adoption of secure, cloud-connected printing systems.

Key players in the Global Printer Market include HP Inc., Epson, Canon Inc., Brother Industries, Xerox Holdings, Ricoh Company, Konica Minolta, Kyocera Corporation, Lexmark International, Stratasys Ltd., 3D Systems, Sharp Corporation, Fujifilm Holdings, Roland DG, and Toshiba. Companies strengthen their market presence by introducing smart, IoT-enabled printers with cloud integration and advanced security. They expand product portfolios to cater to commercial and residential users, emphasizing multifunctionality, high-speed performance, and energy efficiency. Strategic partnerships with IT service providers and retail networks enhance visibility and distribution. Investment in R&D drives innovation in ink technologies, automated workflows, and cost-effective solutions. Aggressive marketing campaigns, competitive pricing strategies, and after-sales support help retain customer loyalty while enabling entry into emerging markets. This multifaceted approach reinforces brand credibility and fortifies market foothold.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Functionality

- 2.2.4 Connectivity

- 2.2.5 Price

- 2.2.6 End User

- 2.2.7 Distribution Channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for eco-friendly & sustainable printing solutions

- 3.2.1.2 Technological advancements in "Smart" printing

- 3.2.1.3 Growing digitalization & focus on managed print services

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High initial cost of premium commercial models

- 3.2.2.2 Rapid shift toward paperless operations

- 3.2.3 Opportunities

- 3.2.3.1 Expansion of 3D printing applications

- 3.2.3.2 Integration of smart features (IoT, cloud connectivity)

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Pricing Analysis (Driven by Primary Research)

- 3.6.1 Historical Price Trend Analysis (Driven by Primary Research)

- 3.6.2 Pricing Strategy by Player Type (Premium / Value / Cost-Plus) (Driven by Primary Research)

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Trade Data Analysis (Driven by Primary Research)

- 3.10.1 Import/Export Volume & Value Trends (Driven by Primary Research)

- 3.10.2 Key Trade Corridors & Tariff Impact (Driven by Primary Research)

- 3.11 Impact of AI & Generative AI on the Market

- 3.11.1 AI-Driven Print Management & Predictive Maintenance

- 3.11.2 GenAI Use Cases & Adoption Roadmap by Segment

- 3.11.3 Risks, Limitations & Regulatory Considerations

- 3.12 Infrastructure & Deployment Landscape (Driven by Primary Research)

- 3.12.1 Deployment Penetration by Region & Buyer Segment (Driven by Primary Research)

- 3.12.2 Scalability Constraints & Infrastructure Investment Trends (Driven by Primary Research)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2022 - 2035 (USD Billion) (Thousand units)

- 5.1 Key trends

- 5.2 Inkjet printers

- 5.3 Laser printers

- 5.4 Dot matrix printers

- 5.5 3D printers

- 5.6 Offset printers

- 5.7 Flexographic

- 5.8 Others

Chapter 6 Market Estimates and Forecast, By Functionality, 2022 - 2035 (USD Billion) (Thousand units)

- 6.1 Key trends

- 6.2 Single function printers

- 6.3 Multifunction printers

Chapter 7 Market Estimates and Forecast, By Connectivity, 2022 - 2035 (USD Billion) (Thousand units)

- 7.1 Key trends

- 7.2 Corded

- 7.3 Cordless

Chapter 8 Market Estimates and Forecast, By Price, 2022 - 2035 (USD Billion) (Thousand units)

- 8.1 Key trends

- 8.2 Low

- 8.3 Medium

- 8.4 High

Chapter 9 Market Estimates and Forecast, By End User, 2022 - 2035 (USD Billion) (Thousand units)

- 9.1 Key trends

- 9.2 Industrial

- 9.3 Residential

- 9.4 Commercial

- 9.4.1 Corporate offices

- 9.4.2 Healthcare

- 9.4.3 Educational

- 9.4.4 Hospitality

- 9.4.5 others (events planners etc.)

Chapter 10 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion) (Thousand units)

- 10.1 Key trends

- 10.2 Online

- 10.2.1 E-commerce

- 10.2.2 Company website

- 10.3 Offline

- 10.3.1 Electronics Stores

- 10.3.2 Brand Stores

- 10.3.3 Others

Chapter 11 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion) (Thousand Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 Japan

- 11.4.3 India

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 Middle East and Africa

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 HP Inc.

- 12.2 Epson

- 12.3 Canon Inc.

- 12.4 Brother Industries

- 12.5 Xerox Holdings

- 12.6 Ricoh Company

- 12.7 Konica Minolta

- 12.8 Kyocera Corporation

- 12.9 Lexmark International

- 12.10 Stratasys Ltd.

- 12.11 3D Systems

- 12.12 Sharp Corporation

- 12.13 Fujifilm Holdings

- 12.14 Roland DG

- 12.15 Toshiba

单功能印表机市场商机、成长要素、产业趋势分析及2026-2035年预测。

单功能印表机市场商机、成长要素、产业趋势分析及2026-2035年预测。 直接薄膜印刷市场:按类型、薄膜、分销管道和应用划分-2026-2032年全球市场预测

直接薄膜印刷市场:按类型、薄膜、分销管道和应用划分-2026-2032年全球市场预测 印表机市场规模、份额、成长率和全球产业分析:按类型、应用和地区分類的洞察,2026-2034 年预测

印表机市场规模、份额、成长率和全球产业分析:按类型、应用和地区分類的洞察,2026-2034 年预测 DTF印表机:全球市占率和排名、总销售额和需求预测(2026-2032年)单标籤印表机市场:依印表机类型、技术、标籤材料、最终用户和销售管道,全球预测,2026-2032年航空公司登机证与行李标籤印表机市场:依印表机类型、技术、连接方式、应用程式、最终用户、通路划分,全球预测(2026-2032年)软指示牌印表机市场:依产品类型、墨水类型、速度等级、应用、最终用户、通路划分,全球预测,2026-2032年

DTF印表机:全球市占率和排名、总销售额和需求预测(2026-2032年)单标籤印表机市场:依印表机类型、技术、标籤材料、最终用户和销售管道,全球预测,2026-2032年航空公司登机证与行李标籤印表机市场:依印表机类型、技术、连接方式、应用程式、最终用户、通路划分,全球预测(2026-2032年)软指示牌印表机市场:依产品类型、墨水类型、速度等级、应用、最终用户、通路划分,全球预测,2026-2032年 印表机市场规模、份额、趋势和预测(按印表机类型、技术类型、印表机介面、最终用户和地区划分),2026-2034年日本印表机市场报告:按印表机类型、技术类型、印表机介面、最终用户和地区划分(2026-2034年)

印表机市场规模、份额、趋势和预测(按印表机类型、技术类型、印表机介面、最终用户和地区划分),2026-2034年日本印表机市场报告:按印表机类型、技术类型、印表机介面、最终用户和地区划分(2026-2034年) 印表机市场 - 全球产业规模、份额、趋势、机会和预测(按印表机类型、技术类型、印表机介面、输出类型、最终用户应用、地区和竞争格局划分),2021-2031年

印表机市场 - 全球产业规模、份额、趋势、机会和预测(按印表机类型、技术类型、印表机介面、输出类型、最终用户应用、地区和竞争格局划分),2021-2031年