|

市场调查报告书

商品编码

2019212

无线印表机市场商机、成长要素、产业趋势分析及2026-2035年预测。Wireless Printer Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

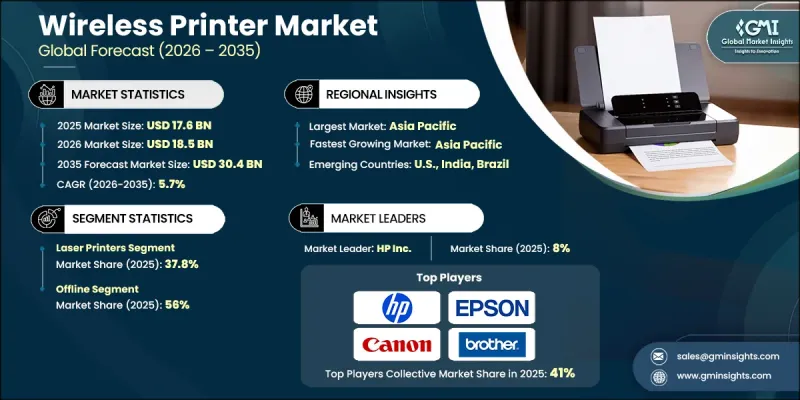

预计到 2025 年,全球无线印表机市场规模将达到 176 亿美元,并以 5.7% 的复合年增长率成长,到 2035 年将达到 304 亿美元。

市场成长的驱动力在于连接性、行动整合和成像技术的持续创新。领先的印表机製造商正在将高速 Wi-Fi 6/7、低功耗蓝牙和 NFC 整合到其喷墨、雷射和热敏产品中,从而在商用和工业应用中实现无线操作和高速资料传输。产业重组,包括併购以及与软体和云端解决方案供应商的合作,也在推动市场扩张。这些合作关係为企业级无线列印和託管列印服务提供了支援。从传统的有线列印转向云端按需数位解决方案正在改变企业的营运方式,而人工智慧驱动的列印管理、多装置同步和混合云端列印正在重新定义工作流程的效率和可自订性,从而满足高印量办公环境和工业列印的需求。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测期 | 2026-2035 |

| 上市时的市场规模 | 176亿美元 |

| 预测金额 | 304亿美元 |

| 复合年增长率 | 5.7% |

到2025年,雷射印表机市场占有率将达到37.8%。雷射印表机凭藉其高速列印、在大规模办公室和企业营运中的成本效益以及强大的无线安全协议,持续保持主导地位,成为高印量企业的理想之选。此外,雷射印表机还能与行动和云端解决方案集成,进一步增强了其对寻求可靠高效列印解决方案的企业的吸引力。

线下销售通路占56%,市场规模达98亿美元。线下通路表现依然强劲,尤其是在商业和企业环境中,这得益于现场演示、专业安装服务以及订阅式墨水和碳粉填充计划等优势。此外,客户更倾向于离线购买,因为他们可以立即获得产品和个人化支持,从而提升整体购买体验。

预计到2025年,美国无线印表机市占率将达到80.5%。该地区正受益于混合办公模式、云端整合办公室基础设施和行动优先列印解决方案的日益普及。企业办公室、教育机构和医疗机构对无线印表机的日益青睐,以及其对云端列印、行动装置连接和安全远端管理的支持,正在推动该地区强劲的需求,并巩固美国作为无线印表机普及领先市场中心的地位。

目录

第一章:调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 每个阶段增加的价值

- 影响价值链的因素

- 影响产业的因素

- 促进因素

- 劳动力短缺加剧和製造业回流

- 人工智慧、衍生设计和软体集成

- IT/OT在印刷作业中的集成

- 产业潜在风险与挑战

- 高整合复杂性

- 资料隐私和网路安全

- 机会

- Printing-as-a-Service(PaaS)

- 印刷电子和智慧包装的成长

- 促进因素

- 成长潜力分析

- 未来市场趋势

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 价格分析(基于初步调查)

- 对过去价格趋势的分析(基于初步研究)

- 根据业务类型分類的定价策略(高端/价值/成本加成)(基于初步调查)

- 专利趋势(基于初步调查)

- 无线技术专利(Wi-Fi、蓝牙、NFC)

- 与印刷安全和加密相关的专利

- 与云端列印基础设施相关的专利

- 与多功能设备整合相关的专利

- 监理情势

- 标准和合规要求

- 区域法规结构

- 认证标准

- 波特五力分析

- PESTEL 分析

- 贸易数据分析(基于初步调查)

- 进出口数量和价值趋势(基于初步调查)

- 主要贸易走廊及关税影响(基于初步调查)

- 人工智慧和生成式人工智慧对市场的影响

- 人工智慧驱动的列印管理和预测性维护

- 针对特定领域的生成式人工智慧应用案例和实施蓝图

- 风险、限制和监管考量

- 基础设施和实施情况(基于初步调查)

- 按地区和购买者群体分類的采用率和渗透率(基于初步调查)

- 基础设施投资的可扩展性限制和趋势(基于初步调查)

第四章 竞争情势

- 介绍

- 企业市占率分析

- 按地区

- 企业矩阵分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 主要进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 业务拓展计划

第五章 市场估算与预测:依产品类型划分,2022-2035年

- 喷墨印表机

- 雷射印表机

- 3D印表机

- 其他(热感式印表机、热昇华印表机、可携式/行动印表机等)

第六章 市场估计与预测:依功能划分,2022-2035年

- 单功能印表机

- 多功能印表机

第七章 市场估计与预测:以连结方式划分,2022-2035年

- Wi-Fi

- Bluetooth

- 云端列印

- 其他(近距离场通讯 (NFC) 相容印表机、AirPrint 等)

第八章 市场估计与预测:依应用领域划分,2022-2035年

- 住宅

- 商业的

- 公司总部

- 卫生保健

- 教育

- 饭店业

- 政府

- 其他(旅馆业、活动策划公司等)

- 工业的

第九章 市场估计与预测:依价格划分,2022-2035年

- 低的

- 中等的

- 高的

第十章 市场估价与预测:依通路划分,2022-2035年

- 在线的

- 电子商务网站

- 公司经营的网站

- 离线

- 量贩店

- 品牌自营店

- 其他(百货公司)

第十一章 市场估价与预测:按地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第十二章:公司简介

- Brother USA

- Canon

- Dell

- Epson

- HP

- Fujifilm

- Konica Minolta

- Kyocera

- Lexmark

- Oki

- Ricoh

- Roland

- Sharp

- Toshiba

- Xerox

The Global Wireless Printer Market was valued at USD 17.6 billion in 2025 and is estimated to grow at a CAGR of 5.7% to reach USD 30.4 billion by 2035.

The market's growth is fueled by continuous innovation in connectivity, mobile integration, and imaging technologies. Leading printer manufacturers are incorporating high-speed Wi-Fi 6/7, Bluetooth Low Energy, and NFC into their inkjet, laser, and thermal products, enabling cable-free operation and fast data transfer for professional and industrial applications. Market expansion is also driven by industry consolidation, including mergers, acquisitions, and partnerships with software and cloud solution providers. These collaborations support enterprise-class wireless printing and managed print services. The shift from traditional cabled printing to cloud-enabled and on-demand digital solutions is reshaping operations, while AI-driven print management, multi-device synchronization, and hybrid cloud printing are redefining workflow efficiency and customization, catering to both high-volume office settings and industrial printing needs.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $17.6 Billion |

| Forecast Value | $30.4 Billion |

| CAGR | 5.7% |

In 2025, the laser printers segment accounted for a 37.8% share. Laser printers continue to lead because they offer high-speed printing, cost efficiency for large-scale office and enterprise operations, and robust wireless security protocols, making them the preferred choice for organizations handling high-volume printing tasks. Their ability to integrate with mobile and cloud-based solutions further strengthens their appeal among businesses seeking reliable and efficient printing solutions.

The offline sales segment held 56% share, valued at USD 9.8 billion. Offline channels continue to perform strongly, particularly in commercial and enterprise settings, due to the availability of hands-on demonstrations, professional installation services, and subscription-based ink and toner replenishment programs. Customers also favor offline purchases for immediate product access and personalized support, which enhances the overall buying experience.

United States Wireless Printer Market accounted for 80.5% share in 2025. The region benefits from widespread adoption of hybrid work models, cloud-integrated office infrastructure, and mobile-first printing solutions. Corporate offices, educational institutions, and healthcare facilities are increasingly deploying wireless printers that support cloud printing, mobile device connectivity, and secure remote management, driving strong regional demand and solidifying the U.S. as a key market hub for wireless printer adoption.

Key players in the Global Wireless Printer Market include Canon, HP, Lexmark, Fujifilm, Ricoh, Brother USA, Dell, Epson, Konica Minolta, Kyocera, Oki, Roland, Sharp, Toshiba, and Xerox. Companies in the Wireless Printer Market are strengthening their positions by investing heavily in R&D to integrate advanced connectivity, mobile solutions, and AI-enabled print management. Strategic partnerships with cloud service providers, mergers, and acquisitions help expand product portfolios and enterprise-grade managed printing services. OEMs are focusing on customer experience through subscription-based ink services, hybrid cloud integration, and multi-device compatibility. Innovation in wireless security, high-speed printing, and scalable solutions ensures a competitive edge, while direct-to-consumer and professional installation services improve brand visibility and market penetration.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product Type

- 2.2.3 Functionality

- 2.2.4 Connectivity

- 2.2.5 Price

- 2.2.6 Application

- 2.2.7 Distribution Channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising Labor Shortages & Manufacturing Reshoring

- 3.2.1.2 AI, Generative Design & Software Integration

- 3.2.1.3 IT/OT Convergence in Printing Operations

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High Integration Complexity

- 3.2.2.2 Data Privacy & Cybersecurity

- 3.2.3 Opportunities

- 3.2.3.1 Printing-as-a-Service (PaaS)

- 3.2.3.2 Growth in Printed Electronics & Smart Packaging

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Pricing Analysis (Driven by Primary Research)

- 3.6.1 Historical Price Trend Analysis (Driven by Primary Research)

- 3.6.2 Pricing Strategy by Player Type (Premium / Value / Cost-Plus) (Driven by Primary Research)

- 3.7 Patent Landscape (Driven by Primary Research)

- 3.7.1 Wireless Technology Patents (Wi-Fi, Bluetooth, NFC)

- 3.7.2 Print Security & Encryption Patents

- 3.7.3 Cloud Printing Infrastructure Patents

- 3.7.4 Multi-Function Device Integration Patents

- 3.8 Regulatory landscape

- 3.8.1 Standards and compliance requirements

- 3.8.2 Regional regulatory frameworks

- 3.8.3 Certification standards

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

- 3.11 Trade Data Analysis (Driven by Primary Research)

- 3.11.1 Import/Export Volume & Value Trends (Driven by Primary Research)

- 3.11.2 Key Trade Corridors & Tariff Impact (Driven by Primary Research)

- 3.12 Impact of AI & Generative AI on the Market

- 3.12.1 AI-Driven Print Management & Predictive Maintenance

- 3.12.2 GenAI Use Cases & Adoption Roadmap by Segment

- 3.12.3 Risks, Limitations & Regulatory Considerations

- 3.13 Infrastructure & Deployment Landscape (Driven by Primary Research)

- 3.13.1 Deployment Penetration by Region & Buyer Segment (Driven by Primary Research)

- 3.13.2 Scalability Constraints & Infrastructure Investment Trends (Driven by Primary Research)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product type, 2022 - 2035 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Inkjet printer

- 5.3 Laser printer

- 5.4 3D printer

- 5.5 Others (Thermal printer, Dye-sublimation printer, Portable/Mobile printer, etc.)

Chapter 6 Market Estimates & Forecast, By Functionality, 2022 - 2035 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Single-function printer

- 6.3 Multi-function printer

Chapter 7 Market Estimates & Forecast, By Connectivity, 2022 - 2035 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Wi-Fi

- 7.3 Bluetooth

- 7.4 Cloud printing

- 7.5 Others (Near Field Communication (NFC) Enabled printer, AirPrint, etc.)

Chapter 8 Market Estimates & Forecast, By Application, 2022 - 2035 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Residential

- 8.3 Commercial

- 8.3.1 Corporate offices

- 8.3.2 Healthcare

- 8.3.3 Educational

- 8.3.4 Hospitality

- 8.3.5 Government

- 8.3.6 Others (Hospitality, Events planners etc.)

- 8.4 Industrial

Chapter 9 Market Estimates & Forecast, By Price, 2022 - 2035 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Low

- 9.3 Medium

- 9.4 High

Chapter 10 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035 (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 Online

- 10.2.1 E-commerce website

- 10.2.2 Company owned website

- 10.3 Offline

- 10.3.1 Electronics stores

- 10.3.2 Brand stores

- 10.3.3 Others (department stores)

Chapter 11 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion) (Thousand Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 Japan

- 11.4.3 India

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 Middle East and Africa

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Brother USA

- 12.2 Canon

- 12.3 Dell

- 12.4 Epson

- 12.5 HP

- 12.6 Fujifilm

- 12.7 Konica Minolta

- 12.8 Kyocera

- 12.9 Lexmark

- 12.10 Oki

- 12.11 Ricoh

- 12.12 Roland

- 12.13 Sharp

- 12.14 Toshiba

- 12.15 Xerox