|

市场调查报告书

商品编码

2019232

硅胶薄膜市场机会、成长要素、产业趋势分析及2026-2035年预测Silicone Film Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

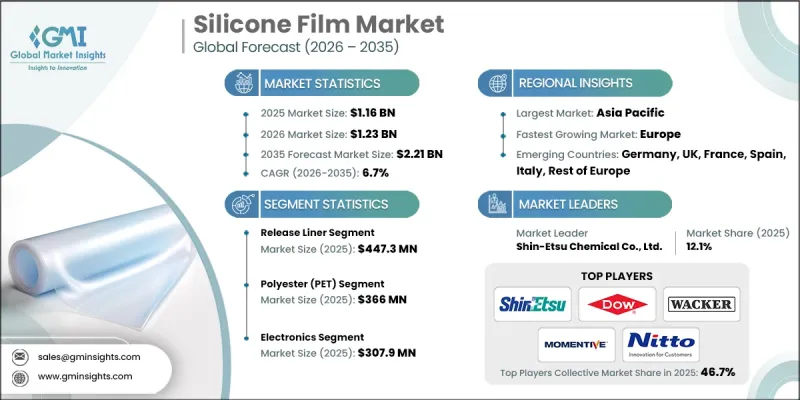

预计到 2025 年,全球硅胶薄膜市场价值将达到 11.6 亿美元,年复合成长率为 6.7%,到 2035 年将达到 22.1 亿美元。

硅胶薄膜是由硅酮聚合物经压延、挤出和涂覆等製程製成的薄而柔韧的片材,其特征是表面光滑、厚度均匀。这些薄膜即使在极端温度和各种环境条件下也能保持稳定的性能,因此备受青睐。为了满足特定应用的需求,可提供多种厚度、固化类型和表面处理方式的硅胶薄膜。硅胶薄膜不发生化学反应且性质惰性,适用于对安全性和材料可靠性要求较高的受控环境。近年来,技术进步主要集中在改进製造流程、定製配方和增强产品功能方面。涂覆和固化技术的创新使得在保持柔软性的同时,能够更好地控制黏着性、表面纹理和机械强度,从而拓展了材料在先进技术领域的应用范围。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测期 | 2026-2035 |

| 上市时的市场规模 | 11.6亿美元 |

| 预测金额 | 22.1亿美元 |

| 复合年增长率 | 6.7% |

预计到2025年,离型纸市场规模将达到4.473亿美元。由于其可控的释放性能、均匀的表面和尺寸稳定性对于精密应用至关重要,该品类将持续成长。製造商正在不断改进涂层和配方,以满足不断变化的工业搬运和加工需求。

到2025年,电子产业市场规模将达到3.079亿美元。由于电子产品、医疗设备和医疗保健设备的需求不断增长,硅胶薄膜正推动市场成长。硅胶薄膜具有绝缘、保护和表面控制功能,同时也能确保热稳定性和运作可靠性。随着现代设备日益复杂,对符合严格加工和性能标准的材料的需求也持续增长。

预计北美硅胶薄膜市场将从2025年的3.776亿美元显着成长至2035年的7.302亿美元。该地区的需求主要受强劲的电子、医疗保健和汽车行业驱动,这些行业需要符合严格监管标准的高性能材料。美国市场也受惠于先进的製造能力和强大的医疗设备生产基地,这些产业涵盖众多领域,特别注重材料的防护、绝缘和脱模性能。

目录

第一章:调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 每个阶段增加的价值

- 影响价值链的因素

- 中断

- 影响产业的因素

- 促进因素

- 电子医疗设备需求的不断增长对硅胶稳定性提出了更高的要求。

- 始终偏爱兼具耐热性和柔软性的材质。

- 在工业流程和防护应用中广泛应用

- 陷阱与挑战

- 生产成本上升正在影响定价和利润率。

- 原材料供应波动会影响生产稳定性。

- 机会

- 根据特定应用性能要求客製化薄膜。

- 新兴领域对硅薄膜的日益重视

- 促进因素

- 成长潜力分析

- 监理情势

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特五力分析

- PESTEL 分析

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 按类型

- 未来市场趋势

- 专利趋势

- 贸易统计(HS编码)

- 主要进口国

- 主要出口国

- 永续性和环境方面

- 永续倡议

- 减少废弃物策略

- 生产中的能源效率

- 环保意识的倡议

- 考虑碳足迹

第四章 竞争情势

- 介绍

- 企业市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 按地区

- 企业矩阵分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 主要进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 业务拓展计划

第五章 市场估计与预测:依类型划分,2022-2035年

- 发布文件

- 涂层膜

- 橡胶膜

- 其他的

第六章 市场估算与预测:依薄膜基材划分,2022-2035年

- 聚酯(PET)

- 聚酰亚胺(PI)

- 聚乙烯(PE)

- 其他的

第七章 市场估计与预测:依最终用途产业划分,2022-2035年

- 电子学

- 医疗保健

- 包装

- 车

- 消费品

- 其他的

第八章 市场估计与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿拉伯聯合大公国

- 其他中东和非洲地区

第九章:公司简介

- 3M Company

- Dow Inc.

- Elkem ASA

- Mitsubishi Chemical Corporation

- Momentive Performance Materials Inc.

- Nitto Denko Corporation

- Polyplex Corporation Limited

- Rogers Corporation

- Saint-Gobain Performance Plastics

- Shin-Etsu Chemical Co., Ltd.

- Silex Silicones Ltd.

- Wacker Chemie AG

The Global Silicone Film Market was valued at USD 1.16 billion in 2025 and is estimated to grow at a CAGR of 6.7% to reach USD 2.21 billion by 2035.

Silicone films are thin, flexible sheets produced from silicone polymers using calendaring, extrusion, and coating techniques, resulting in smooth surfaces and uniform thickness. These films are prized for their ability to maintain consistent performance under extreme temperatures and varying environmental conditions. They are available in multiple thicknesses, curing types, and surface finishes to meet application-specific needs. Non-reactive and chemically inert, silicone films are suitable for controlled environments requiring high safety and material reliability. Recent technological advancements focus on improved manufacturing methods, custom formulations, and enhanced product functionality. Innovations in coating and curing techniques have allowed better control over adhesion, surface texture, and mechanical strength while preserving flexibility, extending the material's usability in advanced technical applications.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.16 Billion |

| Forecast Value | $2.21 Billion |

| CAGR | 6.7% |

The release liner segment reached USD 447.3 million in 2025. This category continues to expand due to its controlled release properties, uniform surface, and dimensional stability, which are essential for precision applications. Manufacturers are refining coatings and formulations to meet evolving industrial handling and processing requirements.

The electronics segment accounted for USD 307.9 million in 2025. Rising demand in electronics, medical devices, and healthcare equipment drives growth, as silicone films provide insulation, protection, and surface control while ensuring thermal stability and operational reliability. The need for materials that meet strict processing and performance standards continues to rise alongside the complexity of modern devices.

North America Silicone Film Market is expected to grow significantly, rising from USD 377.6 million in 2025 to USD 730.2 million by 2035. The region's demand stems from robust electronics, healthcare, and automotive sectors, which require high-performance materials that comply with stringent regulatory standards. The U.S. market is further strengthened by advanced manufacturing capabilities and a strong medical device production base that emphasizes protective, insulating, and release functionalities across multiple industries.

Key players operating in the Global Silicone Film Market include 3M Company, Momentive Performance Materials Inc., Mitsubishi Chemical Corporation, Elkem ASA, Dow Inc., Nitto Denko Corporation, Rogers Corporation, Shin-Etsu Chemical Co., Ltd., Silex Silicones Ltd., Saint-Gobain Performance Plastics, and Polyplex Corporation Limited. Companies in the Global Silicone Film Market are strengthening their presence through multiple strategies. They invest in research and development to improve mechanical strength, thermal stability, and flexibility while expanding product customization. Collaboration with electronics, automotive, and healthcare manufacturers ensures solutions meet industry-specific requirements. Firms are adopting advanced coating and curing technologies to enhance surface uniformity, adhesion, and durability. Expanding global manufacturing capacities and supply networks helps capture emerging markets. Additionally, companies focus on sustainability, producing eco-friendly silicone formulations and reducing energy consumption during production.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Type

- 2.2.2 Film Base

- 2.2.3 End Use Industry

- 2.2.4 Regional

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Expanding electronics healthcare demand requires stable silicone performance

- 3.2.1.2 Preference for materials offering thermal resistance flexibility consistently

- 3.2.1.3 Wider adoption in industrial processing and protective applications

- 3.2.2 Pitfalls/challenge

- 3.2.2.1 Higher production costs influencing pricing and profitability margins

- 3.2.2.2 Volatility in raw material supply affecting production stability

- 3.2.3 Opportunities

- 3.2.3.1 Customization of films for application specific performance requirements

- 3.2.3.2 Growing evaluation of silicone films in emerging sectors

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By type

- 3.9 Future market trends

- 3.10 Patent landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2022-2035 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Release liner

- 5.3 Coated films

- 5.4 Rubber films

- 5.5 Others

Chapter 6 Market Estimates and Forecast, By Film Base, 2022-2035 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Polyester (PET)

- 6.3 Polyimide (PI)

- 6.4 Polyethylene (PE)

- 6.5 Others

Chapter 7 Market Estimates and Forecast, By End Use Industry, 2022-2035 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Electronics

- 7.3 Medical and healthcare

- 7.4 Packaging

- 7.5 Automotive

- 7.6 Consumer goods

- 7.7 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 3M Company

- 9.2 Dow Inc.

- 9.3 Elkem ASA

- 9.4 Mitsubishi Chemical Corporation

- 9.5 Momentive Performance Materials Inc.

- 9.6 Nitto Denko Corporation

- 9.7 Polyplex Corporation Limited

- 9.8 Rogers Corporation

- 9.9 Saint-Gobain Performance Plastics

- 9.10 Shin-Etsu Chemical Co., Ltd.

- 9.11 Silex Silicones Ltd.

- 9.12 Wacker Chemie AG