|

市场调查报告书

商品编码

2019247

心血管医疗设备市场:商机、成长要素、产业趋势分析及2026-2035年预测Cardiovascular Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

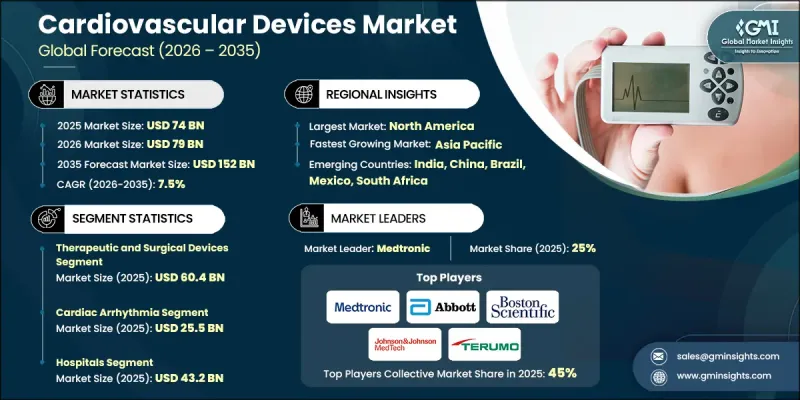

预计到 2025 年,全球心血管器材市场价值将达到 740 亿美元,并预计以 7.5% 的复合年增长率成长,到 2035 年达到 1,520 亿美元。

心血管疾病盛行率上升、全球人口老化、政府医疗保健政策加强以及对微创治疗需求不断增长,是推动心血管医疗器材市场扩张的主要因素。心血管医疗设备包括植入式、体外和诊断系统,用于监测、辅助或恢復心臟和血管功能。它们有助于检测异常情况、改善血液循环、调节心率、增强血流并支持长期疾病管理。器械技术的进步、小型化、创新材料和数位化整合提高了临床准确性、安全性和易用性。先进支架、电生理解决方案和成像工具等创新技术能够实现更早期的检测和更有效的治疗,从而推动了医生对这些技术的采用。微创手术,包括经导管心臟瓣膜置换术术和机器人辅助手术系统,减轻了手术负担、缩短了住院时间并降低了治疗成本,促使医院和心臟中心优先采用最先进的精准导向器械。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测期 | 2026-2035 |

| 上市时的市场规模 | 740亿美元 |

| 预测金额 | 1520亿美元 |

| 复合年增长率 | 7.5% |

预计到2025年,治疗和外科医疗设备市场规模将达到604亿美元。这个市场涵盖了重要的心血管器械,例如导管、冠状动脉介入治疗器械、心臟节律管理系统、结构性心臟疾病器械和手术器械。这些器械在恢復或替代心臟功能方面发挥着至关重要的作用,是介入性心臟病学和心臟外科的核心。该市场透过提供治疗紧急或危及生命的心臟疾病所需的根治性疗法来推动市场成长。持续的产品创新,包括微创导管、新一代支架、更先进的心律不整管理器械和耐用型人工心臟瓣膜,正在改善治疗效果、缩短住院时间并扩大其在高风险患者中的应用范围。

预计到2025年,心律不整市场规模将达255亿美元。专为心律不整治疗而设计的设备占据了市场的大部分份额,这主要得益于心房颤动、心搏过速和心搏过缓等心律不整盛行率的不断上升。与生活方式相关的风险因素,例如老化、肥胖、高血压和糖尿病,以及对持续监测需求的日益增长,都在推动市场的持续成长。心律不整检测和治疗技术的进步,包括先进的监测系统和植入式设备,正在巩固该领域的市场地位,并支持其长期成长。

到2025年,北美循环系统器材市场将占据全球41.8%的份额。该地区因久坐不动的生活方式、肥胖和高血压而导致的高疾病负担,推动了对先进诊断和治疗解决方案的强劲需求。医院和专科医疗中心正越来越多地采用微创心臟器械,例如支架、起搏器、去心房颤动和监测系统,以治疗日益增多的患者。心血管疾病(CVD)相关住院人数的增加,加速了创新介入器材的应用,而心臟器材的持续改善也与该地区的医疗保健需求和监管标准相契合。

目录

第一章:调查方法

- 研究途径

- 品质改进计划

- GMI人工智慧政策和资料完整性倡议

- 资讯来源一致性协议

- GMI人工智慧政策和资料完整性倡议

- 调查过程和可靠性评分

- 调查过程的组成部分

- 评分组成部分

- 数据收集

- 主要来源部分列表

- 资料探勘资讯来源

- 付费资讯来源

- 区域资讯来源

- 付费资讯来源

- 基本估算和计算方法

- 每种方法中基准年的计算

- 预测模型

- 量化市场影响分析

- 生长参数对预测的数学影响

- 量化市场影响分析

- 关于调查透明度的补充信息

- 资讯来源归属框架

- 品质保证指标

- 对信任的承诺

第二章执行摘要

第三章业界考察

- 生态系分析

- 影响产业的因素

- 促进因素

- 患有心血管疾病的患者人数正在增加。

- 老年人口增加

- 政府主导的措施增加

- 心血管器械的技术进步

- 对微创手术的需求日益增长

- 产业潜在风险与挑战

- 心血管手术风险较高

- 严格的法规环境

- 市场机会

- 人工智慧在心血管疾病领域的应用日益广泛

- 促进因素

- 成长潜力分析

- 监理情势(基于初步调查)

- 技术趋势(基于初步调查)

- 当前技术趋势

- 用于即时心血管诊断的先进成像和感测系统

- 用于自动检测和风险分层的AI整合式心血管设备

- 新兴技术

- 用于下一代心血管植入和支架的生物工程和自适应材料

- 用于动态心血管评估的超高速 3D 视觉化数位双胞胎技术

- 当前技术趋势

- 未来市场趋势(基于初步研究)

- 2025年价格分析

- 人工智慧和生成式人工智慧对市场的影响

- 波特五力分析

- PESTEL 分析

第四章 竞争情势

- 介绍

- 企业市占率分析

- 世界

- 北美洲

- 欧洲

- 亚太地区

- 企业矩阵分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 主要进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 业务拓展计划

第五章 市场估计与预测:依类型划分,2022-2035年

- 诊断和监测设备

- 心电图系统

- 动态心电图和心臟事件记录器

- 远端心电图监测设备

- 心臟诊断超音波设备

- 其他诊断和监测设备

- 治疗及外科器械

- 导管

- 电生理消融导管

- 电生理诊断及标测导管

- 介入导管

- 冠状动脉介入装置

- 药物释放型支架

- 裸金属支架

- 生物可吸收支架

- PTCA球囊

- 动脉粥状硬化斑块切除术装置

- 导管导引线

- 栓塞预防装置

- 其他冠状动脉介入装置

- 心臟节律管理(CRM)设备

- 起搏器

- 植入式心臟整流去颤器

- 心臟再同步治疗装置

- 植物型循环记录器

- 其他心臟节律管理装置

- 结构性心臟装置

- 左心耳封堵装置

- 心臟瓣膜

- 心臟外科手术器械

- 冠状动脉绕道手术手术(CABG)手术器械

- 其他心臟外科器械

- 心室辅助装置

- 导管

第六章 市场估计与预测:依应用领域划分,2022-2035年

- 冠状动脉疾病

- 心律不整

- 心臟衰竭

- 其他用途

第七章 市场估计与预测:依最终用途划分,2022-2035年

- 医院

- 门诊手术中心

- 心臟中心

- 其他最终用户

第八章 市场估计与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第九章:公司简介

- Abbott Laboratories

- AngioDynamics

- Biotronik

- Boston Scientific

- Johnson &Johnson MedTech

- Koninklijke Philips

- Medtronic

- Meril Life Sciences

- MicroPort Scientific

- Olympus

- Penumbra

- Relisys Medical Devices

- Sahajanand Medical Technologies

- Terumo

- Translumina Therapeutics

The Global Cardiovascular Devices Market was valued at USD 74 billion in 2025 and is estimated to grow at a CAGR of 7.5% to reach USD 152 billion by 2035.

The expansion is fueled by the rising prevalence of cardiovascular diseases, an aging global population, increased government healthcare initiatives, and growing demand for minimally invasive interventions. Cardiovascular devices include implantable, external, and diagnostic systems that monitor, support, or restore heart and vascular function. They help detect irregularities, improve circulation, regulate heart rhythms, enhance blood flow, and assist in long-term disease management. Advancements in device technology, miniaturization, innovative materials, and digital integration have improved clinical precision, safety, and usability. Innovations like advanced stents, electrophysiology solutions, and imaging tools enable earlier detection and more effective treatment, encouraging physician adoption. Minimally invasive procedures, including transcatheter heart valves and robotic-assisted systems, reduce surgical trauma, shorten hospital stays, and lower treatment costs, prompting hospitals and cardiology centers to prioritize cutting-edge, precision-guided devices.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $74 Billion |

| Forecast Value | $152 Billion |

| CAGR | 7.5% |

The therapeutic and surgical devices segment reached USD 60.4 billion in 2025. This segment encompasses essential cardiovascular tools such as catheters, coronary intervention devices, cardiac rhythm management systems, structural heart devices, and surgical instruments. These devices play a critical role in restoring or replacing heart function and are central to interventional cardiology and cardiac surgery. The segment dominates due to its provision of definitive treatments, often necessary for urgent or life-threatening cardiac conditions. Continuous product innovations, including minimally invasive catheters, next-generation stents, smarter rhythm management devices, and durable heart valves, enhance procedural outcomes, reduce hospital stays, and expand eligibility for high-risk patients.

The cardiac arrhythmia segment generated USD 25.5 billion in 2025. Arrhythmia-focused devices hold a major share because of the increasing prevalence of irregular heart rhythms such as atrial fibrillation, tachycardia, and bradycardia. Aging populations, lifestyle-related risk factors like obesity, hypertension, and diabetes, and the rising need for continuous monitoring drive sustained demand. Technological progress in arrhythmia detection and therapy, including advanced monitoring systems and implantable devices, strengthens the segment's market position and supports long-term growth.

North America Cardiovascular Devices Market accounted for 41.8% share in 2025. The region's high disease burden, driven by sedentary lifestyles, obesity, and hypertension, fuels strong demand for advanced diagnostic and therapeutic solutions. Hospitals and specialty centers increasingly adopt minimally invasive cardiac devices, such as stents, pacemakers, defibrillators, and monitoring systems, to treat a growing patient population. Rising CVD-related hospitalizations accelerate the adoption of innovative interventional devices, while continuous improvements in cardiology equipment align with the region's healthcare needs and regulatory standards.

Key players in the Global Cardiovascular Devices Market include Abbott Laboratories, Boston Scientific, Biotronik, Johnson & Johnson MedTech, Terumo, AngioDynamics, Olympus, Medtronic, Meril Life Sciences, Penumbra, Sahajanand Medical Technologies, Koninklijke Philips, Translumina Therapeutics, Relisys Medical Devices, and MicroPort Scientific. Companies in the Global Cardiovascular Devices Market strengthen their position by prioritizing innovation and expanding their product portfolios to include advanced, minimally invasive, and digitally integrated devices. Firms invest heavily in R&D to develop next-generation stents, rhythm management systems, structural heart devices, and robotic-assisted technologies. Strategic partnerships with hospitals and research institutions accelerate clinical adoption and market penetration. Global expansion into emerging markets and targeted collaborations with distributors ensure wider geographic reach. Companies also focus on regulatory compliance, quality assurance, and physician training programs to build trust and drive adoption.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Device type trends

- 2.2.2 Application trends

- 2.2.3 End use trends

- 2.2.4 Regional trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing number of patients suffering from cardiovascular diseases

- 3.2.1.2 Expanding geriatric population

- 3.2.1.3 Rising government initiatives

- 3.2.1.4 Technological advancements in cardiovascular devices

- 3.2.1.5 Rising demand for minimally invasive procedures

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High risk associated with cardiac procedures

- 3.2.2.2 Stringent regulatory scenario

- 3.2.3 Market opportunities

- 3.2.3.1 Increasing applications of AI in cardiovascular diseases

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape (Driven by primary research)

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Technology landscape (Driven by primary research)

- 3.5.1 Current technological trends

- 3.5.1.1 Advanced imaging and sensing systems for real-time cardiovascular diagnostics

- 3.5.1.2 AI-integrated cardiovascular devices for automated detection and risk stratification

- 3.5.2 Emerging technologies

- 3.5.2.1 Bioengineered and adaptive materials for next-generation cardiovascular implants and stents

- 3.5.2.2 Ultra-high-speed 3D visualization and digital twin technologies for dynamic cardiovascular assessment

- 3.5.1 Current technological trends

- 3.6 Future market trends (Driven by primary research)

- 3.7 Pricing analysis, 2025

- 3.8 Impact of AI and Generative AI on the market

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Global

- 4.2.2 North America

- 4.2.3 Europe

- 4.2.4 Asia Pacific

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Diagnostic and monitoring devices

- 5.2.1 Electrocardiogram systems

- 5.2.2 Holter and event monitors

- 5.2.3 Remote cardiac monitoring devices

- 5.2.4 Cardiac diagnostic ultrasound

- 5.2.5 Other diagnostic and monitoring devices

- 5.3 Therapeutic and surgical devices

- 5.3.1 Catheters

- 5.3.1.1 Electrophysiology ablation catheters

- 5.3.1.2 Electrophysiology diagnostic and mapping catheters

- 5.3.1.3 Interventional catheters

- 5.3.2 Coronary intervention devices

- 5.3.2.1 Drug eluting stents

- 5.3.2.2 Bare metal stents

- 5.3.2.3 Bioresorbable scaffolds

- 5.3.2.4 PTCA balloons

- 5.3.2.5 Atherectomy devices

- 5.3.2.6 Guidewires

- 5.3.2.7 Embolic protection devices

- 5.3.2.8 Other coronary intervention devices

- 5.3.3 Cardiac rhythm management (CRM) devices

- 5.3.3.1 Pacemakers

- 5.3.3.2 Implantable cardioverter defibrillators

- 5.3.3.3 Cardiac resynchronization therapy devices

- 5.3.3.4 Implantable loop recorders

- 5.3.3.5 Other cardiac rhythm management devices

- 5.3.4 Structural heart devices

- 5.3.4.1 LAA closure devices

- 5.3.4.2 Heart valves

- 5.3.5 Cardiac surgery devices

- 5.3.5.1 Coronary artery bypass graft (CABG) surgical tools

- 5.3.5.2 Other cardiac surgical devices

- 5.3.6 Ventricular assist devices

- 5.3.1 Catheters

Chapter 6 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Coronary artery disease

- 6.3 Cardiac arrhythmia

- 6.4 Heart failure

- 6.5 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgical centers

- 7.4 Cardiac centers

- 7.5 Other end users

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Abbott Laboratories

- 9.2 AngioDynamics

- 9.3 Biotronik

- 9.4 Boston Scientific

- 9.5 Johnson & Johnson MedTech

- 9.6 Koninklijke Philips

- 9.7 Medtronic

- 9.8 Meril Life Sciences

- 9.9 MicroPort Scientific

- 9.10 Olympus

- 9.11 Penumbra

- 9.12 Relisys Medical Devices

- 9.13 Sahajanand Medical Technologies

- 9.14 Terumo

- 9.15 Translumina Therapeutics

心血管医疗设备市场:2026-2032年全球市场预测(按器材类型、手术类型、入路方式、应用和最终用户划分)

心血管医疗设备市场:2026-2032年全球市场预测(按器材类型、手术类型、入路方式、应用和最终用户划分) 心血管领域的合作研究与授权协议(2016-2026 年)

心血管领域的合作研究与授权协议(2016-2026 年) 2026年全球心血管基因检测市场报告心血管器材疲劳测试仪市场(依最终用户、应用、硬体、测试模式、测试类型和软体划分),全球预测,2026-2032年2026年全球比索洛尔市场报告2026年全球心血管器材市场报告2026年全球房间隔分流装置市场报告

2026年全球心血管基因检测市场报告心血管器材疲劳测试仪市场(依最终用户、应用、硬体、测试模式、测试类型和软体划分),全球预测,2026-2032年2026年全球比索洛尔市场报告2026年全球心血管器材市场报告2026年全球房间隔分流装置市场报告 基于半导体的血栓监测器市场分析及预测(至2035年):按类型、产品类型、技术、应用、最终用户、组件、製程、材料类型、设备、安装类型划分

基于半导体的血栓监测器市场分析及预测(至2035年):按类型、产品类型、技术、应用、最终用户、组件、製程、材料类型、设备、安装类型划分 全球心血管器材市场规模、份额、趋势和成长分析报告(2026-2034)全球心血管器材市场:依器材类型、应用、最终用户和地区划分 - 市场规模、产业动态、机会分析和预测(2026-2035 年)

全球心血管器材市场规模、份额、趋势和成长分析报告(2026-2034)全球心血管器材市场:依器材类型、应用、最终用户和地区划分 - 市场规模、产业动态、机会分析和预测(2026-2035 年)