|

市场调查报告书

商品编码

1413837

农业技术即服务市场:按技术、服务类型和应用划分 - 2024-2030 年全球预测Agriculture Technology-as-a-Service Market by Technology (Data Analytics & Intelligence, Guidance Technology, Sensing Technology), Service Type (Equipment-as-a-Service (EaaS), Software-as-a-Service (SaaS)), Application - Global Forecast 2024-2030 |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

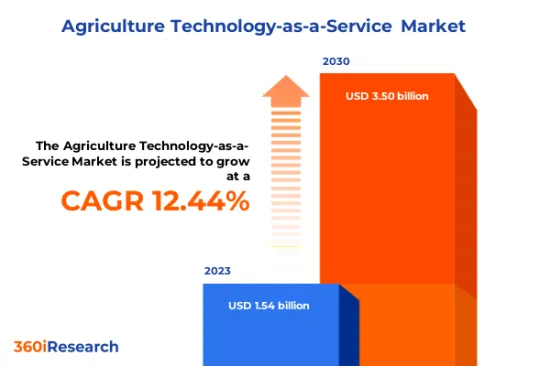

农业技术即服务市场规模预计2023年为15.4亿美元,2024年达到17.2亿美元,预计2030年将达到35亿美元,复合年增长率为12.44%。

农业技术即服务的全球市场

| 主要市场统计 | |

|---|---|

| 基准年[2023] | 15.4亿美元 |

| 预测年份 [2024] | 17.2亿美元 |

| 预测年份 [2030] | 35亿美元 |

| 复合年增长率(%) | 12.44% |

农业技术即服务(ATaaS) 市场涉及利用先进技术向农民和农业部门的其他相关人员提供基于订阅、计量收费或基于绩效的农业创新。解决方案。这些服务通常包括资料分析、精密农业工具、云端基础的监控系统以及各种软体解决方案,以协助农场管理、作物健康监测和产量优化。 ATaaS 可应用于农业的多个子区隔,包括作物监测、牲畜管理、设备租赁和农业金融服务。农民正在利用这些技术来提高田间活动的准确性、动物健康和运作效率。这些服务的主要最终用户是农民、农学家、作物顾问和农业公司。此外,政府机构和研究机构可以使用 ATaaS 来改善保护工作并促进永续农业。生物技术和供应链营业单位等产业也受惠于这些服务。 ATaaS 市场的成长受到精密农业需求增加、提高作物产量的需求增加、水等自然资源稀缺性以及农业营运中越来越多地采用物联网和人工智慧等因素的影响。这些技术增强了决策能力,降低了技术的初始资本投资,并降低了农民的风险。然而,ATaaS 解决方案面临一定的挑战和限制,例如资料管理高成本、小农的技术无知以及对资料隐私和安全的担忧。此外,对网路连线的依赖和技术中断的不可预测性等因素也可能阻碍市场成长。同时,区块链的可追溯性、机器人自动化和农业预测分析等新趋势为 ATaaS 市场提供了新的机会。此外,垂直农业和都市农业的兴起为空间有限地区的技术服务开闢了新途径。

区域洞察

在先进技术基础设施和主要行业参与者的支持下,北美农业技术即服务(ATaaS) 市场正在显着成长。美国和加拿大处于采用数位农业的前沿,利用物联网、人工智慧和云端运算等技术来优化农场运作。在南美洲,随着农民寻求提高作物产量和减少环境影响,对 ATaaS 的需求不断增长。越来越多的新兴企业和合作伙伴正在推动农业实践的创新,其中巴西和阿根廷等国家处于领先地位。用于作物监测和农场管理服务的卫星影像、无人机和遥感技术的整合正在推动 ATaaS 市场的发展。在欧洲,优先考虑永续性和可追溯性的严格法律规范正在强烈影响消费者的需求。欧盟 (EU)通用农业政策 (CAP) 支持整合技术,促进智慧、有弹性和多样化的农业系统。投资和研究主要集中在作物监测和管理系统上,卫星影像在精密农业中的使用正在显着增加。在中东,ATaaS 市场处于相对早期阶段,但正在兴起,主要是由优化用水和加强粮食安全的需求所推动的。在气候干旱、水资源稀缺的背景下,ATaaS供应商专注于智慧灌溉系统、水耕和土壤感测技术,以促进高效农业。在非洲,儘管受到经济限制,人们对行动技术的兴趣日益浓厚,以改善农业流程和加强价值链。亚太地区的 ATaaS 市场显示出巨大的成长前景,其中中国、印度和澳洲等国家贡献显着。采用行动技术、遥感和地理资讯系统(GIS)进行即时监测和决策正在改变农业面貌。尤其是印度,农业技术新兴企业数量激增,为小农提供负担得起且可扩展的服务,使先进技术的取得更加民主化。

FPNV定位矩阵

FPNV 定位矩阵对于评估农业技术即服务市场至关重要。我们检视与业务策略和产品满意度相关的关键指标,以对供应商进行全面评估。这种深入的分析使用户能够根据自己的要求做出明智的决策。根据评估,供应商被分为四个成功程度不同的像限:前沿(F)、探路者(P)、利基(N)和重要(V)。

市场占有率分析

市场占有率分析是一种综合工具,可以对农业技术即服务市场中供应商的现状进行深入而深入的研究。全面比较和分析供应商在整体收益、基本客群和其他关键指标方面的贡献,以便更好地了解公司的绩效及其在争夺市场占有率时面临的挑战。此外,该分析还提供了对该行业竞争特征的宝贵考察,包括在研究基准年观察到的累积、分散主导地位和合併特征等因素。这种详细程度的提高使供应商能够做出更明智的决策并制定有效的策略,从而在市场上获得竞争优势。

本报告在以下方面提供了宝贵的见解:

1-市场渗透率:提供有关主要企业所服务的市场的全面资讯。

2-市场开拓:我们深入研究利润丰厚的新兴市场,并分析它们在成熟细分市场中的渗透率。

3- 市场多元化:提供有关新产品发布、开拓地区、最新发展和投资的详细资讯。

4-竞争力评估与资讯:对主要企业的市场占有率、策略、产品、认证、监管状况、专利状况、製造能力等进行全面评估。

5- 产品开发与创新:提供对未来技术、研发活动和突破性产品开发的见解。

本报告解决了以下关键问题:

1-农业技术即服务市场的市场规模与预测为何?

2-在农业技术即服务市场的预测期内,需要考虑投资哪些产品、细分市场、应用和领域?

3-农业技术即即服务市场的技术趋势和法律规范是什么?

4-农业技术即服务市场中主要供应商的市场占有率是多少?

5-进入农业技术即服务市场的适当型态和策略手段是什么?

目录

第一章 前言

第二章调查方法

第三章执行摘要

第四章市场概况

第五章市场洞察

- 市场动态

- 促进因素

- 更多采用现代农业技术

- 强调永续农业实践

- 资料驱动的见解在农业中变得越来越重要

- 抑制因素

- 高成本和连接问题

- 机会

- 人工智慧与物联网融合

- 客製化服务渗透率提高

- 任务

- 与资料外洩和资料安全相关的担忧

- 促进因素

- 市场区隔分析

- 技术:农业领域对资料分析和情报的偏好日益增长

- 服务类型:在农场管理软体中越来越多地使用软体即服务 (SaaS)

- 应用:增加农业技术即服务(ATaaS) 在土壤管理与测试的应用

- 市场趋势分析

- 高通膨的累积效应

- 波特五力分析

- 价值炼和关键路径分析

- 法律规范

第六章 农业技术即服务市场:依技术分类

- 资料分析与情报

- 感应技术

- 感测技术

- 可变速率应用技术

第七章 农业技术即服务市场:依服务类型

- Equipment-as-a-Service(EaaS)

- 软体即服务 (SaaS)

第八章农业技术即服务市场:依应用分类

- 作物健康监测

- 智慧灌溉

- 土壤管理和测试

- 产量绘图和监控

第九章美洲农业技术即服务市场

- 阿根廷

- 巴西

- 加拿大

- 墨西哥

- 美国

第十章亚太农业技术即服务市场

- 澳洲

- 中国

- 印度

- 印尼

- 日本

- 马来西亚

- 菲律宾

- 新加坡

- 韩国

- 台湾

- 泰国

- 越南

第十一章欧洲、中东和非洲的农业技术即服务市场

- 丹麦

- 埃及

- 芬兰

- 法国

- 德国

- 以色列

- 义大利

- 荷兰

- 奈及利亚

- 挪威

- 波兰

- 卡达

- 俄罗斯

- 沙乌地阿拉伯

- 南非

- 西班牙

- 瑞典

- 瑞士

- 土耳其

- 阿拉伯聯合大公国

- 英国

第十二章竞争形势

- FPNV定位矩阵

- 市场占有率分析:按主要企业划分

- 主要企业竞争情境分析

- 併购

- 新产品发布和功能增强

- 投资、资金筹措

第13章竞争产品组合

- 主要公司简介

- 365FarmNet GmbH

- Accenture PLC

- AG Leader Technology

- AGCO Corporation

- AgEagle Aerial Systems Inc.

- AgJunction, Inc. by Kubota Corp.

- AgriData Incorporated

- AGRIVI doo

- Aker Technologies by IntelinAir, Inc.

- ATMOS UAV

- Corteva Agriscience

- Cropin Technology Solutions Pvt Ltd

- Deere & Company

- Delair SAS

- Dickey-John Corporation

- DroneDeploy, Inc.

- Farmers Edge Precision Consulting Inc.

- Hexagon AB

- Kubota Corporation

- Lockheed Martin Corporation

- Microdrones GmbH by mdGroup GmbH

- Nileworks Inc.

- Parrot Drone SAS

- PrecisionHawk, Inc.

- Prospera Technologies Ltd. by Valmont Industries, Inc.

- Raven Industries, Inc. by CNH Industrial NV

- SZ DJI Technology Co., Ltd.

- Teejet Technologies

- Topcon Positioning Systems

- Yamaha Motor Co., Ltd.

- 主要产品系列

第十四章附录

- 讨论指南

- 关于许可证和定价

[190 Pages Report] The Agriculture Technology-as-a-Service Market size was estimated at USD 1.54 billion in 2023 and expected to reach USD 1.72 billion in 2024, at a CAGR 12.44% to reach USD 3.50 billion by 2030.

Global Agriculture Technology-as-a-Service Market

| KEY MARKET STATISTICS | |

|---|---|

| Base Year [2023] | USD 1.54 billion |

| Estimated Year [2024] | USD 1.72 billion |

| Forecast Year [2030] | USD 3.50 billion |

| CAGR (%) | 12.44% |

The Agriculture Technology-as-a-Service (ATaaS) market encompasses services and solutions that leverage advanced technologies to offer subscription-based, pay-as-you-go, or performance-based agricultural innovations to farmers and other stakeholders in the agricultural sector. These services typically include data analysis, precision farming tools, cloud-based monitoring systems, and various software solutions aiding in farm management, crop health monitoring, and yield optimization. ATaaS can be applied to multiple sub-segments of agriculture, including crop monitoring, livestock management, equipment leasing, and agricultural financial services. Farmers use these technologies to enhance field activity accuracy, livestock health, and operational efficiency. The primary end-users of such services are farmers, agronomists, crop consultants, and agricultural enterprises. Additionally, government bodies and research institutions can employ ATaaS to improve conservation practices and foster sustainable farming. Industries such as biotechnology and supply chain entities also benefit from these services. The growth of the ATaaS market is influenced by factors including the increasing demand for precision agriculture, the growing need for enhanced crop yields, the scarcity of natural resources such as water, and the rise in adoption of IoT and AI in farming practices. These technologies offer enhanced decision-making capabilities, lower initial capital investment in technology, and reduced risk for farmers. However, ATaaS solutions face certain challenges and limitations, such as the high cost of data management, technological ignorance amongst small-scale farmers, and concerns over data privacy and security. Moreover, factors such as dependency on internet connectivity and the unpredictability of technological disruptions can hinder market growth. On the other hand, emerging trends such as blockchain for traceability, robotic automation, and predictive analytics in farming practices provide new opportunities in the ATaaS market. Additionally, the rise of vertical farming and urban agriculture is opening up new avenues for technology services in regions with space constraints.

Regional Insights

The Agriculture Technology-as-a-Service (ATaaS) market in North America is experiencing significant growth, aided by advanced technological infrastructure and the presence of major industry players. The United States and Canada are at the forefront of the adoption of digital agriculture, leveraging technologies such as IoT, AI, and cloud computing to optimize farming practices. In South America, the demand for ATaaS is expanding as farmers seek to improve crop yields and reduce environmental impact. Countries such as Brazil and Argentina are at the forefront, with a growing number of startups and partnerships fostering innovation in agricultural practices. The integration of satellite imagery, drones, and remote sensing technology for crop monitoring and farm management services is propelling the ATaaS market. In Europe, consumer demand is strongly influenced by the stringent regulatory framework prioritizing sustainability and traceability. The European Union's Common Agricultural Policy (CAP) supports the integration of technology to promote smart, resilient, and diversified agricultural systems. Investment and research are focused on crop monitoring and management systems, with a remarkable increase in satellite imagery usage for precision farming. The Middle East exhibits a relatively nascent yet budding ATaaS market, driven primarily by the need to optimize water usage and enhance food security. With arid climates and scarce water resources, ATaaS providers focus on smart irrigation systems, hydroponics, and soil sensing technologies to facilitate efficient agriculture. In Africa, despite economic constraints, there is a growing interest in mobile technologies for enhancing agricultural processes and strengthening the value chain. The APAC region demonstrates remarkable growth prospects in the ATaaS market, with countries such as China, India, and Australia contributing significantly. The adoption of mobile technologies, remote sensing, and geographic information systems (GIS) for real-time monitoring and decision-making is transforming the agricultural landscape. In particular, India is witnessing a surge in agri-tech startups providing affordable and scalable services to smallholder farms, thus democratizing access to advanced technologies.

FPNV Positioning Matrix

The FPNV Positioning Matrix is pivotal in evaluating the Agriculture Technology-as-a-Service Market. It offers a comprehensive assessment of vendors, examining key metrics related to Business Strategy and Product Satisfaction. This in-depth analysis empowers users to make well-informed decisions aligned with their requirements. Based on the evaluation, the vendors are then categorized into four distinct quadrants representing varying levels of success: Forefront (F), Pathfinder (P), Niche (N), or Vital (V).

Market Share Analysis

The Market Share Analysis is a comprehensive tool that provides an insightful and in-depth examination of the current state of vendors in the Agriculture Technology-as-a-Service Market. By meticulously comparing and analyzing vendor contributions in terms of overall revenue, customer base, and other key metrics, we can offer companies a greater understanding of their performance and the challenges they face when competing for market share. Additionally, this analysis provides valuable insights into the competitive nature of the sector, including factors such as accumulation, fragmentation dominance, and amalgamation traits observed over the base year period studied. With this expanded level of detail, vendors can make more informed decisions and devise effective strategies to gain a competitive edge in the market.

Key Company Profiles

The report delves into recent significant developments in the Agriculture Technology-as-a-Service Market, highlighting leading vendors and their innovative profiles. These include 365FarmNet GmbH, Accenture PLC, AG Leader Technology, AGCO Corporation, AgEagle Aerial Systems Inc., AgJunction, Inc. by Kubota Corp., AgriData Incorporated, AGRIVI d.o.o., Aker Technologies by IntelinAir, Inc., ATMOS UAV, Corteva Agriscience, Cropin Technology Solutions Pvt Ltd, Deere & Company, Delair SAS, Dickey-John Corporation, DroneDeploy, Inc., Farmers Edge Precision Consulting Inc., Hexagon AB, Kubota Corporation, Lockheed Martin Corporation, Microdrones GmbH by mdGroup GmbH, Nileworks Inc., Parrot Drone S.A.S, PrecisionHawk, Inc., Prospera Technologies Ltd. by Valmont Industries, Inc., Raven Industries, Inc. by CNH Industrial N.V., SZ DJI Technology Co., Ltd., Teejet Technologies, Topcon Positioning Systems, and Yamaha Motor Co., Ltd..

Market Segmentation & Coverage

This research report categorizes the Agriculture Technology-as-a-Service Market to forecast the revenues and analyze trends in each of the following sub-markets:

- Technology

- Data Analytics & Intelligence

- Guidance Technology

- Sensing Technology

- Variable Rate Application Technology

- Service Type

- Equipment-as-a-Service (EaaS)

- Software-as-a-Service (SaaS)

- Application

- Crop Health Monitoring

- Smart Irrigation

- Soil Management & Testing

- Yield Mapping & Monitoring

- Region

- Americas

- Argentina

- Brazil

- Canada

- Mexico

- United States

- California

- Florida

- Illinois

- New York

- Ohio

- Pennsylvania

- Texas

- Asia-Pacific

- Australia

- China

- India

- Indonesia

- Japan

- Malaysia

- Philippines

- Singapore

- South Korea

- Taiwan

- Thailand

- Vietnam

- Europe, Middle East & Africa

- Denmark

- Egypt

- Finland

- France

- Germany

- Israel

- Italy

- Netherlands

- Nigeria

- Norway

- Poland

- Qatar

- Russia

- Saudi Arabia

- South Africa

- Spain

- Sweden

- Switzerland

- Turkey

- United Arab Emirates

- United Kingdom

- Americas

The report offers valuable insights on the following aspects:

1. Market Penetration: It presents comprehensive information on the market provided by key players.

2. Market Development: It delves deep into lucrative emerging markets and analyzes the penetration across mature market segments.

3. Market Diversification: It provides detailed information on new product launches, untapped geographic regions, recent developments, and investments.

4. Competitive Assessment & Intelligence: It conducts an exhaustive assessment of market shares, strategies, products, certifications, regulatory approvals, patent landscape, and manufacturing capabilities of the leading players.

5. Product Development & Innovation: It offers intelligent insights on future technologies, R&D activities, and breakthrough product developments.

The report addresses key questions such as:

1. What is the market size and forecast of the Agriculture Technology-as-a-Service Market?

2. Which products, segments, applications, and areas should one consider investing in over the forecast period in the Agriculture Technology-as-a-Service Market?

3. What are the technology trends and regulatory frameworks in the Agriculture Technology-as-a-Service Market?

4. What is the market share of the leading vendors in the Agriculture Technology-as-a-Service Market?

5. Which modes and strategic moves are suitable for entering the Agriculture Technology-as-a-Service Market?

Table of Contents

1. Preface

- 1.1. Objectives of the Study

- 1.2. Market Segmentation & Coverage

- 1.3. Years Considered for the Study

- 1.4. Currency & Pricing

- 1.5. Language

- 1.6. Limitations

- 1.7. Assumptions

- 1.8. Stakeholders

2. Research Methodology

- 2.1. Define: Research Objective

- 2.2. Determine: Research Design

- 2.3. Prepare: Research Instrument

- 2.4. Collect: Data Source

- 2.5. Analyze: Data Interpretation

- 2.6. Formulate: Data Verification

- 2.7. Publish: Research Report

- 2.8. Repeat: Report Update

3. Executive Summary

4. Market Overview

- 4.1. Introduction

- 4.2. Agriculture Technology-as-a-Service Market, by Region

5. Market Insights

- 5.1. Market Dynamics

- 5.1.1. Drivers

- 5.1.1.1. Increasing adoption of modern farming technologies

- 5.1.1.2. Emphasis on sustainable agriculture practices

- 5.1.1.3. Growing importance of data-driven insights in agriculture

- 5.1.2. Restraints

- 5.1.2.1. High cost and connectivity issues

- 5.1.3. Opportunities

- 5.1.3.1. Integration with artificial intelligence and IoT

- 5.1.3.2. Increasing penetration of customized services

- 5.1.4. Challenges

- 5.1.4.1. Concerns associated with data breach and data security

- 5.1.1. Drivers

- 5.2. Market Segmentation Analysis

- 5.2.1. Technology: Rising preference for data analytics & intelligence in agriculture sector

- 5.2.2. Service Type: Increasing usage of Software-as-a-Service (SaaS) in farm management software

- 5.2.3. Application: Growing application of Agriculture Technology-as-a-Service (ATaaS) for soil management & testing

- 5.3. Market Trend Analysis

- 5.4. Cumulative Impact of High Inflation

- 5.5. Porter's Five Forces Analysis

- 5.5.1. Threat of New Entrants

- 5.5.2. Threat of Substitutes

- 5.5.3. Bargaining Power of Customers

- 5.5.4. Bargaining Power of Suppliers

- 5.5.5. Industry Rivalry

- 5.6. Value Chain & Critical Path Analysis

- 5.7. Regulatory Framework

6. Agriculture Technology-as-a-Service Market, by Technology

- 6.1. Introduction

- 6.2. Data Analytics & Intelligence

- 6.3. Guidance Technology

- 6.4. Sensing Technology

- 6.5. Variable Rate Application Technology

7. Agriculture Technology-as-a-Service Market, by Service Type

- 7.1. Introduction

- 7.2. Equipment-as-a-Service (EaaS)

- 7.3. Software-as-a-Service (SaaS)

8. Agriculture Technology-as-a-Service Market, by Application

- 8.1. Introduction

- 8.2. Crop Health Monitoring

- 8.3. Smart Irrigation

- 8.4. Soil Management & Testing

- 8.5. Yield Mapping & Monitoring

9. Americas Agriculture Technology-as-a-Service Market

- 9.1. Introduction

- 9.2. Argentina

- 9.3. Brazil

- 9.4. Canada

- 9.5. Mexico

- 9.6. United States

10. Asia-Pacific Agriculture Technology-as-a-Service Market

- 10.1. Introduction

- 10.2. Australia

- 10.3. China

- 10.4. India

- 10.5. Indonesia

- 10.6. Japan

- 10.7. Malaysia

- 10.8. Philippines

- 10.9. Singapore

- 10.10. South Korea

- 10.11. Taiwan

- 10.12. Thailand

- 10.13. Vietnam

11. Europe, Middle East & Africa Agriculture Technology-as-a-Service Market

- 11.1. Introduction

- 11.2. Denmark

- 11.3. Egypt

- 11.4. Finland

- 11.5. France

- 11.6. Germany

- 11.7. Israel

- 11.8. Italy

- 11.9. Netherlands

- 11.10. Nigeria

- 11.11. Norway

- 11.12. Poland

- 11.13. Qatar

- 11.14. Russia

- 11.15. Saudi Arabia

- 11.16. South Africa

- 11.17. Spain

- 11.18. Sweden

- 11.19. Switzerland

- 11.20. Turkey

- 11.21. United Arab Emirates

- 11.22. United Kingdom

12. Competitive Landscape

- 12.1. FPNV Positioning Matrix

- 12.2. Market Share Analysis, By Key Player

- 12.3. Competitive Scenario Analysis, By Key Player

- 12.3.1. Merger & Acquisition

- 12.3.1.1. AGCO Acquires FarmFacts GmbH & Launches AGCO Ventures

- 12.3.1.2. Intelinair to Acquire Aker Technologies

- 12.3.2. New Product Launch & Enhancement

- 12.3.2.1. EOSDA Enters France With Its Crop Monitoring Platform

- 12.3.3. Investment & Funding

- 12.3.3.1. Terramera spinout enrichAg officially launches with $6m from At One Ventures

- 12.3.1. Merger & Acquisition

13. Competitive Portfolio

- 13.1. Key Company Profiles

- 13.1.1. 365FarmNet GmbH

- 13.1.2. Accenture PLC

- 13.1.3. AG Leader Technology

- 13.1.4. AGCO Corporation

- 13.1.5. AgEagle Aerial Systems Inc.

- 13.1.6. AgJunction, Inc. by Kubota Corp.

- 13.1.7. AgriData Incorporated

- 13.1.8. AGRIVI d.o.o.

- 13.1.9. Aker Technologies by IntelinAir, Inc.

- 13.1.10. ATMOS UAV

- 13.1.11. Corteva Agriscience

- 13.1.12. Cropin Technology Solutions Pvt Ltd

- 13.1.13. Deere & Company

- 13.1.14. Delair SAS

- 13.1.15. Dickey-John Corporation

- 13.1.16. DroneDeploy, Inc.

- 13.1.17. Farmers Edge Precision Consulting Inc.

- 13.1.18. Hexagon AB

- 13.1.19. Kubota Corporation

- 13.1.20. Lockheed Martin Corporation

- 13.1.21. Microdrones GmbH by mdGroup GmbH

- 13.1.22. Nileworks Inc.

- 13.1.23. Parrot Drone S.A.S

- 13.1.24. PrecisionHawk, Inc.

- 13.1.25. Prospera Technologies Ltd. by Valmont Industries, Inc.

- 13.1.26. Raven Industries, Inc. by CNH Industrial N.V.

- 13.1.27. SZ DJI Technology Co., Ltd.

- 13.1.28. Teejet Technologies

- 13.1.29. Topcon Positioning Systems

- 13.1.30. Yamaha Motor Co., Ltd.

- 13.2. Key Product Portfolio

14. Appendix

- 14.1. Discussion Guide

- 14.2. License & Pricing

LIST OF FIGURES

- FIGURE 1. AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET RESEARCH PROCESS

- FIGURE 2. AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, 2023 VS 2030

- FIGURE 3. AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, 2018-2030 (USD MILLION)

- FIGURE 4. AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY REGION, 2023 VS 2030 (%)

- FIGURE 5. AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY REGION, 2023 VS 2024 VS 2030 (USD MILLION)

- FIGURE 6. AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET DYNAMICS

- FIGURE 7. AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY TECHNOLOGY, 2023 VS 2030 (%)

- FIGURE 8. AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY TECHNOLOGY, 2023 VS 2024 VS 2030 (USD MILLION)

- FIGURE 9. AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY SERVICE TYPE, 2023 VS 2030 (%)

- FIGURE 10. AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY SERVICE TYPE, 2023 VS 2024 VS 2030 (USD MILLION)

- FIGURE 11. AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY APPLICATION, 2023 VS 2030 (%)

- FIGURE 12. AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY APPLICATION, 2023 VS 2024 VS 2030 (USD MILLION)

- FIGURE 13. AMERICAS AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY COUNTRY, 2023 VS 2030 (%)

- FIGURE 14. AMERICAS AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY COUNTRY, 2023 VS 2024 VS 2030 (USD MILLION)

- FIGURE 15. UNITED STATES AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY STATE, 2023 VS 2030 (%)

- FIGURE 16. UNITED STATES AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY STATE, 2023 VS 2024 VS 2030 (USD MILLION)

- FIGURE 17. ASIA-PACIFIC AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY COUNTRY, 2023 VS 2030 (%)

- FIGURE 18. ASIA-PACIFIC AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY COUNTRY, 2023 VS 2024 VS 2030 (USD MILLION)

- FIGURE 19. EUROPE, MIDDLE EAST & AFRICA AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY COUNTRY, 2023 VS 2030 (%)

- FIGURE 20. EUROPE, MIDDLE EAST & AFRICA AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY COUNTRY, 2023 VS 2024 VS 2030 (USD MILLION)

- FIGURE 21. AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET, FPNV POSITIONING MATRIX, 2023

- FIGURE 22. AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SHARE, BY KEY PLAYER, 2023

LIST OF TABLES

- TABLE 1. AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SEGMENTATION & COVERAGE

- TABLE 2. UNITED STATES DOLLAR EXCHANGE RATE, 2018-2023

- TABLE 3. AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, 2018-2030 (USD MILLION)

- TABLE 4. GLOBAL AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY REGION, 2018-2030 (USD MILLION)

- TABLE 5. AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY TECHNOLOGY, 2018-2030 (USD MILLION)

- TABLE 6. AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY DATA ANALYTICS & INTELLIGENCE, BY REGION, 2018-2030 (USD MILLION)

- TABLE 7. AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY GUIDANCE TECHNOLOGY, BY REGION, 2018-2030 (USD MILLION)

- TABLE 8. AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY SENSING TECHNOLOGY, BY REGION, 2018-2030 (USD MILLION)

- TABLE 9. AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY VARIABLE RATE APPLICATION TECHNOLOGY, BY REGION, 2018-2030 (USD MILLION)

- TABLE 10. AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY SERVICE TYPE, 2018-2030 (USD MILLION)

- TABLE 11. AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY EQUIPMENT-AS-A-SERVICE (EAAS), BY REGION, 2018-2030 (USD MILLION)

- TABLE 12. AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY SOFTWARE-AS-A-SERVICE (SAAS), BY REGION, 2018-2030 (USD MILLION)

- TABLE 13. AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 14. AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY CROP HEALTH MONITORING, BY REGION, 2018-2030 (USD MILLION)

- TABLE 15. AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY SMART IRRIGATION, BY REGION, 2018-2030 (USD MILLION)

- TABLE 16. AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY SOIL MANAGEMENT & TESTING, BY REGION, 2018-2030 (USD MILLION)

- TABLE 17. AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY YIELD MAPPING & MONITORING, BY REGION, 2018-2030 (USD MILLION)

- TABLE 18. AMERICAS AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY TECHNOLOGY, 2018-2030 (USD MILLION)

- TABLE 19. AMERICAS AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY SERVICE TYPE, 2018-2030 (USD MILLION)

- TABLE 20. AMERICAS AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 21. AMERICAS AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY COUNTRY, 2018-2030 (USD MILLION)

- TABLE 22. ARGENTINA AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY TECHNOLOGY, 2018-2030 (USD MILLION)

- TABLE 23. ARGENTINA AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY SERVICE TYPE, 2018-2030 (USD MILLION)

- TABLE 24. ARGENTINA AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 25. BRAZIL AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY TECHNOLOGY, 2018-2030 (USD MILLION)

- TABLE 26. BRAZIL AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY SERVICE TYPE, 2018-2030 (USD MILLION)

- TABLE 27. BRAZIL AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 28. CANADA AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY TECHNOLOGY, 2018-2030 (USD MILLION)

- TABLE 29. CANADA AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY SERVICE TYPE, 2018-2030 (USD MILLION)

- TABLE 30. CANADA AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 31. MEXICO AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY TECHNOLOGY, 2018-2030 (USD MILLION)

- TABLE 32. MEXICO AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY SERVICE TYPE, 2018-2030 (USD MILLION)

- TABLE 33. MEXICO AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 34. UNITED STATES AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY TECHNOLOGY, 2018-2030 (USD MILLION)

- TABLE 35. UNITED STATES AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY SERVICE TYPE, 2018-2030 (USD MILLION)

- TABLE 36. UNITED STATES AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 37. UNITED STATES AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY STATE, 2018-2030 (USD MILLION)

- TABLE 38. ASIA-PACIFIC AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY TECHNOLOGY, 2018-2030 (USD MILLION)

- TABLE 39. ASIA-PACIFIC AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY SERVICE TYPE, 2018-2030 (USD MILLION)

- TABLE 40. ASIA-PACIFIC AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 41. ASIA-PACIFIC AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY COUNTRY, 2018-2030 (USD MILLION)

- TABLE 42. AUSTRALIA AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY TECHNOLOGY, 2018-2030 (USD MILLION)

- TABLE 43. AUSTRALIA AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY SERVICE TYPE, 2018-2030 (USD MILLION)

- TABLE 44. AUSTRALIA AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 45. CHINA AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY TECHNOLOGY, 2018-2030 (USD MILLION)

- TABLE 46. CHINA AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY SERVICE TYPE, 2018-2030 (USD MILLION)

- TABLE 47. CHINA AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 48. INDIA AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY TECHNOLOGY, 2018-2030 (USD MILLION)

- TABLE 49. INDIA AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY SERVICE TYPE, 2018-2030 (USD MILLION)

- TABLE 50. INDIA AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 51. INDONESIA AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY TECHNOLOGY, 2018-2030 (USD MILLION)

- TABLE 52. INDONESIA AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY SERVICE TYPE, 2018-2030 (USD MILLION)

- TABLE 53. INDONESIA AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 54. JAPAN AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY TECHNOLOGY, 2018-2030 (USD MILLION)

- TABLE 55. JAPAN AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY SERVICE TYPE, 2018-2030 (USD MILLION)

- TABLE 56. JAPAN AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 57. MALAYSIA AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY TECHNOLOGY, 2018-2030 (USD MILLION)

- TABLE 58. MALAYSIA AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY SERVICE TYPE, 2018-2030 (USD MILLION)

- TABLE 59. MALAYSIA AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 60. PHILIPPINES AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY TECHNOLOGY, 2018-2030 (USD MILLION)

- TABLE 61. PHILIPPINES AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY SERVICE TYPE, 2018-2030 (USD MILLION)

- TABLE 62. PHILIPPINES AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 63. SINGAPORE AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY TECHNOLOGY, 2018-2030 (USD MILLION)

- TABLE 64. SINGAPORE AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY SERVICE TYPE, 2018-2030 (USD MILLION)

- TABLE 65. SINGAPORE AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 66. SOUTH KOREA AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY TECHNOLOGY, 2018-2030 (USD MILLION)

- TABLE 67. SOUTH KOREA AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY SERVICE TYPE, 2018-2030 (USD MILLION)

- TABLE 68. SOUTH KOREA AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 69. TAIWAN AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY TECHNOLOGY, 2018-2030 (USD MILLION)

- TABLE 70. TAIWAN AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY SERVICE TYPE, 2018-2030 (USD MILLION)

- TABLE 71. TAIWAN AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 72. THAILAND AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY TECHNOLOGY, 2018-2030 (USD MILLION)

- TABLE 73. THAILAND AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY SERVICE TYPE, 2018-2030 (USD MILLION)

- TABLE 74. THAILAND AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 75. VIETNAM AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY TECHNOLOGY, 2018-2030 (USD MILLION)

- TABLE 76. VIETNAM AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY SERVICE TYPE, 2018-2030 (USD MILLION)

- TABLE 77. VIETNAM AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 78. EUROPE, MIDDLE EAST & AFRICA AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY TECHNOLOGY, 2018-2030 (USD MILLION)

- TABLE 79. EUROPE, MIDDLE EAST & AFRICA AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY SERVICE TYPE, 2018-2030 (USD MILLION)

- TABLE 80. EUROPE, MIDDLE EAST & AFRICA AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 81. EUROPE, MIDDLE EAST & AFRICA AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY COUNTRY, 2018-2030 (USD MILLION)

- TABLE 82. DENMARK AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY TECHNOLOGY, 2018-2030 (USD MILLION)

- TABLE 83. DENMARK AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY SERVICE TYPE, 2018-2030 (USD MILLION)

- TABLE 84. DENMARK AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 85. EGYPT AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY TECHNOLOGY, 2018-2030 (USD MILLION)

- TABLE 86. EGYPT AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY SERVICE TYPE, 2018-2030 (USD MILLION)

- TABLE 87. EGYPT AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 88. FINLAND AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY TECHNOLOGY, 2018-2030 (USD MILLION)

- TABLE 89. FINLAND AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY SERVICE TYPE, 2018-2030 (USD MILLION)

- TABLE 90. FINLAND AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 91. FRANCE AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY TECHNOLOGY, 2018-2030 (USD MILLION)

- TABLE 92. FRANCE AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY SERVICE TYPE, 2018-2030 (USD MILLION)

- TABLE 93. FRANCE AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 94. GERMANY AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY TECHNOLOGY, 2018-2030 (USD MILLION)

- TABLE 95. GERMANY AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY SERVICE TYPE, 2018-2030 (USD MILLION)

- TABLE 96. GERMANY AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 97. ISRAEL AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY TECHNOLOGY, 2018-2030 (USD MILLION)

- TABLE 98. ISRAEL AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY SERVICE TYPE, 2018-2030 (USD MILLION)

- TABLE 99. ISRAEL AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 100. ITALY AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY TECHNOLOGY, 2018-2030 (USD MILLION)

- TABLE 101. ITALY AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY SERVICE TYPE, 2018-2030 (USD MILLION)

- TABLE 102. ITALY AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 103. NETHERLANDS AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY TECHNOLOGY, 2018-2030 (USD MILLION)

- TABLE 104. NETHERLANDS AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY SERVICE TYPE, 2018-2030 (USD MILLION)

- TABLE 105. NETHERLANDS AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 106. NIGERIA AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY TECHNOLOGY, 2018-2030 (USD MILLION)

- TABLE 107. NIGERIA AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY SERVICE TYPE, 2018-2030 (USD MILLION)

- TABLE 108. NIGERIA AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 109. NORWAY AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY TECHNOLOGY, 2018-2030 (USD MILLION)

- TABLE 110. NORWAY AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY SERVICE TYPE, 2018-2030 (USD MILLION)

- TABLE 111. NORWAY AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 112. POLAND AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY TECHNOLOGY, 2018-2030 (USD MILLION)

- TABLE 113. POLAND AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY SERVICE TYPE, 2018-2030 (USD MILLION)

- TABLE 114. POLAND AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 115. QATAR AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY TECHNOLOGY, 2018-2030 (USD MILLION)

- TABLE 116. QATAR AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY SERVICE TYPE, 2018-2030 (USD MILLION)

- TABLE 117. QATAR AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 118. RUSSIA AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY TECHNOLOGY, 2018-2030 (USD MILLION)

- TABLE 119. RUSSIA AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY SERVICE TYPE, 2018-2030 (USD MILLION)

- TABLE 120. RUSSIA AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 121. SAUDI ARABIA AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY TECHNOLOGY, 2018-2030 (USD MILLION)

- TABLE 122. SAUDI ARABIA AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY SERVICE TYPE, 2018-2030 (USD MILLION)

- TABLE 123. SAUDI ARABIA AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 124. SOUTH AFRICA AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY TECHNOLOGY, 2018-2030 (USD MILLION)

- TABLE 125. SOUTH AFRICA AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY SERVICE TYPE, 2018-2030 (USD MILLION)

- TABLE 126. SOUTH AFRICA AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 127. SPAIN AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY TECHNOLOGY, 2018-2030 (USD MILLION)

- TABLE 128. SPAIN AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY SERVICE TYPE, 2018-2030 (USD MILLION)

- TABLE 129. SPAIN AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 130. SWEDEN AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY TECHNOLOGY, 2018-2030 (USD MILLION)

- TABLE 131. SWEDEN AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY SERVICE TYPE, 2018-2030 (USD MILLION)

- TABLE 132. SWEDEN AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 133. SWITZERLAND AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY TECHNOLOGY, 2018-2030 (USD MILLION)

- TABLE 134. SWITZERLAND AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY SERVICE TYPE, 2018-2030 (USD MILLION)

- TABLE 135. SWITZERLAND AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 136. TURKEY AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY TECHNOLOGY, 2018-2030 (USD MILLION)

- TABLE 137. TURKEY AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY SERVICE TYPE, 2018-2030 (USD MILLION)

- TABLE 138. TURKEY AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 139. UNITED ARAB EMIRATES AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY TECHNOLOGY, 2018-2030 (USD MILLION)

- TABLE 140. UNITED ARAB EMIRATES AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY SERVICE TYPE, 2018-2030 (USD MILLION)

- TABLE 141. UNITED ARAB EMIRATES AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 142. UNITED KINGDOM AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY TECHNOLOGY, 2018-2030 (USD MILLION)

- TABLE 143. UNITED KINGDOM AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY SERVICE TYPE, 2018-2030 (USD MILLION)

- TABLE 144. UNITED KINGDOM AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 145. AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET, FPNV POSITIONING MATRIX, 2023

- TABLE 146. AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET SHARE, BY KEY PLAYER, 2023

- TABLE 147. AGRICULTURE TECHNOLOGY-AS-A-SERVICE MARKET LICENSE & PRICING

2024-2032 年按服务类型(软体即服务、设备即服务)、技术、定价、应用和地区分類的农业技术即服务市场报告

2024-2032 年按服务类型(软体即服务、设备即服务)、技术、定价、应用和地区分類的农业技术即服务市场报告 全球农业即服务市场研究报告 - 2024 年至 2032 年产业分析、规模、份额、成长、趋势与预测

全球农业即服务市场研究报告 - 2024 年至 2032 年产业分析、规模、份额、成长、趋势与预测 全球农业技术即服务市场 - 2023-2030 年

全球农业技术即服务市场 - 2023-2030 年 农业即服务市场:按流程、交付模式和最终用户 - 俄罗斯-乌克兰衝突、高累积的累积影响 - 2023-2030 年全球预测

农业即服务市场:按流程、交付模式和最终用户 - 俄罗斯-乌克兰衝突、高累积的累积影响 - 2023-2030 年全球预测 ATaaS (Agriculture Technology-as-a-Service) 的全球市场 (2022-2027年):各产品、用途、地区/国家分析、预测

ATaaS (Agriculture Technology-as-a-Service) 的全球市场 (2022-2027年):各产品、用途、地区/国家分析、预测 按服务类型、交付模式和最终用户划分的农业即服务市场:2021-2031 年全球机遇分析和行业预测

按服务类型、交付模式和最终用户划分的农业即服务市场:2021-2031 年全球机遇分析和行业预测 农业即服务市场规模、份额和趋势分析报告:按服务类型(农场管理解决方案、生产协助)、按交付模式(即付即用、订阅)、按最终用户、按地区、细分预测、 2022- 2030

农业即服务市场规模、份额和趋势分析报告:按服务类型(农场管理解决方案、生产协助)、按交付模式(即付即用、订阅)、按最终用户、按地区、细分预测、 2022- 2030