|

市场调查报告书

商品编码

1388498

仓库自动化市场(物流自动化):到2028年将达到440亿美元-按技术、按行业、按地区划分国家(第四版)Warehouse Automation Market (Logistics Automation) Worth $44 Billion by 2028 - By Technology (AGV/AMR, ASRS, Conveyors, Sortation, Order Picking, AIDC, Palletizing and WMS/WES/WCS), By Industry, By Region & Country - 4th Edition |

||||||

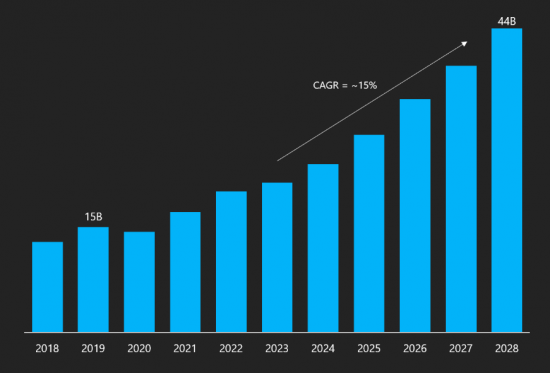

全球仓库自动化市场预计到 2028 年将达到 440 亿美元大关,2023 年至 2028 年复合年增长率为 15%。

当然,推动仓库自动化的运动早在 COVID-19 之前就已如火如荼地展开,但全球大流行迫使企业将其仓库自动化策略转变为维持行业所必需的策略。我们一直在被迫将类别从 "没什么好失去的" 改为 "必须拥有" 的类别。 从COVID-19 大流行中学到的教训之一是,我们需要以长远的眼光看待并透过关注各种大趋势(老化、全球化、健康与安全、流动性、绿色物流、自动化等)来应对任何挑战。全球化、城市化、个人化、数位化等比以往任何时候都需要更多地考虑和强调。

2021年,仓库自动化公司订单量庞大,但由于供应链限制,收入成长有限。 结果,该行业最终在 2022 年出现了创纪录的积压,而由于经济放缓和宏观不确定性,积压在 2023 年有所下降。 进入2024年,企业重新开始接受订单,但由于消费者支出疲软、通膨高企和地缘政治紧张局势,零售商对资本投资仍持谨慎态度。

由于劳动成本上升以及电子商务、零售和 3PL 物流领域消费者需求的若干结构性趋势,我们认为仓库自动化市场存在重大的长期成长机会。 儘管由于2023 年经济放缓,零售和电子商务将出现暂时收缩,但2023 年人们对仓库自动化的兴趣将会很高,这将从2024 年起转化为这些系统整合商和製造商的新订单和收入。

仓库自动化市场报告亮点

- 仓库自动化设备的供应商和行业顾问正在看到数据分析、5G、数位服务和后电晕时代的新趋势,这些趋势是由不断变化的人口结构、不断增长的电子商务渗透率以及工业物联网的兴起,随着自动化操作需求的增加,我们预计长期销售成长将在10%左右。

- 竞争格局:物料搬运设备领域约有15家主要公司可以提供全面的自动化仓库解决方案,年收入超过10亿美元,收入在2亿美元至1美元之间亿,有15至20家中型企业。 许多新创公司在AMR、基于立方体的ASRS、拣选机器人、微型履行、自主服务提供者等新类别中不断涌现,但排名前10 位的大型参与者(Dematic、Daifuku、SSI Schaefer、Honeywell Intelligerated、Knapp、 Toyota Advance) Logistics、Muratec、Beumer Group、Fortna 和 Witron)占据了超过 50% 的市场份额。 近年来,Symbotic 作为新玩家崛起,挑战美国的老牌玩家。

- 服务(MRO 和数位)的重要性日益增加:随着自动化仓库解决方案安装基础的成长,公司预期服务和维护收入将会增加。 到 2028 年,预计将带来 110 亿美元的机遇,占整个市场(包括数位服务)的近 25%。

- 商业模式也随着最终用户对高资本支出的即时痛点而改变。 由于 RaaS(机器人即服务)的灵活性、可扩展性以及比传统机器人程式更低的入门成本,越来越多的公司开始转向 RaaS。 拣选即服务业务模式通常每次拣选的成本在 6 美分到 10 美分之间,而 AMR 即服务通常按月租赁(取决于合约期限)每个机器人。价格从每月750 美元到每月数千美元不等。

- 产业整合:过去五年,物料搬运设备供应商之间的整合不断加强。 这是因为传统公司发现收购新技术领导者是应对不断变化的市场趋势和定位自己的更有吸引力的方式。

您需要了解的事实

- 过去十年,全球电子商务销售额的复合年增长率为 20%,预计到 2021 年全球将达到约 5 兆美元,到 2027 年将增长到超过 8 兆美元。网路零售额占零售总额的比重预计将从2%上升到19%,到2030年将达到25%以上。

- Amazon Robotics 使用超过 750,000 个自主移动机器人来实现其配送中心的自动化,比 2015 年底的 30,000 个增长了 25 倍。 亚马逊一直在迎头赶上,以匹配供需。 配送成本占销售额的百分比将从 2020 年的约 15% 上升到 2022 年的 16-17%。 亚马逊创建了一项名为 AIIF 的 10 亿美元风险投资计划,以促进和支持客户履行、物流和供应链方面的创新。

- 沃尔玛宣布与 Symbotic 合作,重新构想该零售商的区域配送网路。 Symbotic 于 2017 年在佛罗里达州布鲁克斯维尔的沃尔玛配送中心首次安装了该系统。 此后,两家公司共同努力优化该系统。 2021 年 7 月,沃尔玛宣布与 Symbotic 合作,在其区域网路中实施其高科技自动化系统,并计划在其 42 个 RDC 中的 25 个实施该技术。 2022 年 5 月,两家公司扩大了商业协议,在未来几年内将 Symbotic 的机器人和软体自动化平台引入沃尔玛的所有 42 个区域配送中心。

- 欧洲领先的线上时尚和生活方式平台 Zalando 在波兰开设了第三个营运中心。 波兰的两个履行中心将为 Zalando 不断增长的客户群提供服务,一个物流站点将负责 Zalando Lounge 的送货。

- 在黑色星期五、网路星期一、亚马逊 Prime 会员日、感恩节和光棍节等主要购物节日前后出现劳动力需求高峰期间,仓库劳动力短缺也是一个问题。 仓库必须在高峰时段僱用临时工,以满足客户的交货时程。 供应链机器人公司菜鸟在中国最大的机器人操作仓库中安装了 700 多台机器人来处理 "双十一" 订单。

- 阿里巴巴历史上首次拒绝公布 2022 年销售数据,称销售额将与 2021 年 "处于同一水平" 。 阿里巴巴的竞争对手中国第二大零售商京东也首次没有公布销售数据,儘管该公司称这些数据 "创纪录" 。 2022年全平台双十一销售额在1,300亿美元至1,500亿美元之间,较2021年成长3%至13%。 分析师预计 2023 年双十一的成长将处于低个位数。

亚马逊开始竞相实现仓库和供应链自动化

机器人和自动化正迅速成为电子商务的关键成功因素,并将对物流世界产生巨大影响。 从自主移动机器人和自动化仓储系统,到追踪技术和先进的供应链软体,一切都是为了更快、更安全、更无错误的物流,更快的上市时间,以及最终更快、更安全、更少的错误。免费物流。它改变了游戏规则,使消费者能够降低成本。

亚马逊一直是仓库自动化产业诞生的主要推手。 2005 年,亚马逊推出了 Prime,这是一项针对约 100 万种产品的快速会员计画。 Amazon Prime 目前拥有超过1 亿会员,为超过3000 万件商品提供免费无限制送货服务,为超过100 万件商品提供免费当日送货服务,并在特定城市为数万件商品提供服务。我们在1-2 小时内送达。 Prime 最终透过规模和自动化证明了永续发展,使亚马逊占据了美国电子商务市场 35% 以上的份额。 现在它已成为线上零售业事实上的基准,将消费者对配送性能的期望设定到非常高的水平。

零售商在线上营运的一大优势是能够将非常大的库存文件保存在一个地方并将其分发到世界各地。 这使得零售商能够库存比每家商店库存更多的产品 (SKU),而不会产生库存风险。 聚合网站的成功清楚地表明,增加产品选择可以增加长期销售量。 仓库自动化使零售商能够处理比以往更多的库存,从而推动成长。

如果不利用机器人和自动化技术的尖端进步,亚马逊 Prime 就不可能实现,该公司已将其转变为可持续竞争优势的来源。 2012年,亚马逊以7.75亿美元收购了Kiva Systems。 Kiva Systems(现称为 Amazon Robotics)率先使用自主移动机器人实现仓库自动化,并引入了革命性的订单处理方法。 Kiva 机器人由最先进的控制软体控制,可在仓库中自主移动,动态移动装有订购产品的货架并进行包装以履行订单。 Amazon Robotics 目前拥有超过 75 万个自主移动机器人,实现其配送中心的自动化,比 2015 年底的 30,000 个增加了 25 倍多。

自2015年以来,Kiva技术仅限于亚马逊的仓库,因此许多公司争先恐后地填补空白,各种自主的移动机器人系统现在已经普遍存在。 该行业仍处于起步阶段,老牌企业包括最近被中国消费电子巨头美的收购的 KUKA 子公司 Swisslog 和同样被日本欧姆龙收购的 Adept,以及 Fetch Robotics 和 Universal Robotics 等美国公司。从联合创始人发起的丹麦移动工业机器人(MiR),到总部位于新加坡、在印度拥有客户的GreyOrange,再到中国海康威视子公司Hikrobot Technologies 等众多新创公司。

亚马逊斥资 140 亿美元收购 Whole Foods Markets,对电子商务和物流业影响深远,意味着网上杂货购物即将迎来黄金时段。这也预示着。 我们相信此次收购是美国线上杂货市场的决定性事件。 该市场仍处于起步阶段,仅占美国 6,750 亿美元食品杂货市场的 2%,占较发达的英国市场的 6% 左右。 克罗格与艾伯森的合併可能会成为零售自动化领域的下一个游戏规则改变者。 近年来,像 Ocado 这样的纯线上杂货服务已经测试并证明了具有非常高自动化强度的商业模式,但规模相对有限。 另一方面,传统杂货零售商却一直在与最后一英里的物流噩梦作斗争。 杂货的拣选和运输面临冷炼等物流挑战。

订单拣选对机器人来说仍然是一个挑战

亚马逊评论说,商业上可行的自动拣选仍然是一个 "艰鉅的挑战" 。

一款能够实现自动订单拣选的机器人已经发布。 大多数机器人供应商和仓库自动化公司都会生产各种订单拣选机器人。 这些订单拣选机器人从托盘上 "拣选" 包裹,将其放入纸箱或盒子中,然后将其放在传送带系统上以进行进一步交付。

有些公司,例如 IAM Robotics,使用 Fanuc 的带有手臂的自主移动采摘机器人 "Swift" 。 这些机器人通常被归类为协作机器人(cobots),它们从货架上挑选物品的能力通常与自动引导车辆有关,该车辆将它们从货架运输到仓库的包装和运输部分。 2020年,Ocado同意以2.62亿美元收购旧金山机器人公司Kindred Systems,以2,500万美元收购拉斯维加斯Haddington Dynamics,以加强其拣选和包装能力。 另外,Ocado Group 于 2023 年从 Shopify 收购了 6 River Robotics,这是一家针对物流和非食品零售领域的协作 AMR 履行解决方案提供商。

到 2028 年,仓库自动化市场的最大部分将是电子商务,其次是杂货市场

电商和杂货对仓库自动化设备的需求最高,到2028年成长率将超过10%。 电子商务的成长也推动了印度、印尼、拉丁美洲以及中欧和东欧等历史上此类解决方案渗透率很低的地区对自动化解决方案的需求。 在新兴国家,现代仓库空间的需求量很大。

亚太地区将成为最大的仓库自动化市场,其中印度由于其在电子商务方面的巨大潜力,预计将呈现全球最高的成长。 印度的 GreyOrange 和 Addverb Technologies 等区域新创公司表明,更在地化的解决方案也在电子商务企业中获得了认可。

美国目前是最大的仓库自动化市场,鑑于全自动化仓库仅占美国仓库总面积的不到5%,预计将继续保持领先地位。 更快的履约率、劳动力短缺以及仓库员工的更高工资预计将推动自动化技术的采用。 在电子商务的显着成长以及京东等公司的大量 SKU 处理和运输的推动下,中国排名第二,仅次于美国。

目前,10家主要公司占据了50%以上的市场份额,但预计未来还会出现更多併购。

本报告分析了全球仓库自动化市场,包括市场的基本结构和驱动因素、技术和解决方案概述以及近期趋势、主要公司和主要产品概况、行业最新趋势以及未来的成长。我们目前正在调查前景。

本报告的内容

-

包含

- 500+ 页和 290+ 图表的市场报告:7 个主要产业和 10 个技术

- 仓库自动化市场由下而上分析:20多个国家和地区

- 对生态系中 700 家公司的详细分析:包含 140 多家公司的公司简介

- 与整个价值链中 100+ 个主要产业利害关係人进行焦点小组讨论,收集原始资讯以验证分析。

- 包含资料透视模型和 350 多个市场表的 Excel 文件,包括截至 2028 年的未来预测

- 两场分析师会议,用于进一步集思广益

- 投资详情:包括超过 150 笔 併购交易和超过 750 笔 融资交易。

- LogisticsIQ (TM) 独特的市场地图(15+ 类别/650+ 公司)

目录

第 1 章仓库自动化

- 仓库营运结构

- 自动化对于降低营运成本和取得市场成功至关重要

第 2 章仓库自动化技术细分

- 仓库管理系统 (WMS)、仓库执行系统 (WES) 仓库控制系统 (WCS)

- 自动识别和资料撷取 (AIDC)

- 输送机、分类、高架系统

- 自主导引车 (AGV)/自主移动机器人 (AMR)

- 自动储存与检索系统 (AS/RS) 或託盘架

- 码垛/卸垛系统

- 订单拣选

第 3 章仓库自动化的商业模式、推动因素与趋势

- 商业模式

- 仓库自动化的经济学

- 产业驱动因素

- 宏观成长的驱动因素

- 整合与併购 (M&A)

- Modex 2022:概述

第 4 章新型冠状病毒感染 (COVID-19) 的传播:对仓库自动化的影响

- 即时与短期影响

- 新冠肺炎 (COVID-19) 疫情后的新趋势

第 5 章仓库自动化的驱动因素与趋势

- 市场成长

- 电子商务:仓库自动化的最大成长动力

- 超快速配送服务:对进一步自动化的需求

- 机器人与自动化:订单处理的关键成功因素

- 线上杂货可能是仓库自动化的下一个颠覆者和主要候选者

- 订单拣选:对机器人来说仍然是一个挑战

- 仓库空间供应限制

- 开发商在部分市场测试多层仓库

- 仓库自动化面临的挑战

- 前期投资成本

- 灵活性

- 创新

第 6 章仓库自动化市场:依技术

- 输送机/分类系统

- 架空系统

- 龙门机器人

- 自动储存与检索系统(AS/RS)

- 码垛/卸垛系统

- 自动识别和资料撷取 (AIDC)

- 自主导引车 (AGV)/自主移动机器人 (AMR)

- 订单拣选

- 使用语音技术进行优化

- 仓库中的语音辨识技术

- 分析的优点

- 机器人拣选达到转折点

- 合作

- WMS□WES□WCS

- MRO 服务

第 7 章仓库自动化市场:依最终使用者产业划分

- 电子商务

- 杂货店

- 服装

- 食品/饮料

- 杂货

- 邮政/包裹

- 批发

- 其他(製药/生命科学、金属/采矿、化学品等)

第 8 章仓库自动化市占率:依国家

- 北美

- 美国

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 荷兰

- 北欧国家

- 欧洲其他地区

- 亚太地区

- 中国

- 日本

- 韩国

- 印度

- 澳大利亚

- 印尼

- 泰国

- 菲律宾

- 越南

- 马来西亚

- 新加坡

- 中东/非洲

- 沙乌地阿拉伯

- 阿拉伯联合大公国

- 其他海湾合作委员会 (GCC) 国家

- 土耳其

- 南非

- 其他中东/非洲

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地区

第 9 章仓库自动化开发:主要客户

- Amazon

- JD.com

- Walmart

- Tesco

- Kroger

- Ocado

- ASOS

- Zalando

第 10 章竞争态势

- 主要公司及其能力

- 仓库设备提供者

- 仓库管理软体供应商

- AIDC 提供者

- 市占率分析

- 主要公司和主要趋势

- 仓库管理系统(WMS)

- 物料搬运系统

- 自动导引车 (AGV)/自主移动机器人 (AMR)

- AIDC(自动识别/资料收集)

- 最后一哩配送

- 单件拣选机器人

- ASP(自主服务提供者)

- 仓库无人机

- 人工智慧 (AI)

- 物联网分析

- 区块链

- 5G技术

- 微履行

- 3PL(第三方物流)

第 11 章新兴科技

- 仓库无人机

- 针对特定产业的解决方案

- 地下物流

第 12 章研究方法

第 13 章公司简介

- Daifuku

- Dematic (KION Group)

- SSI-Schaefer

- Vanderlande (Toyota Advanced Logistics)

- Swisslog (KUKA)

- Knapp AG

- Murata Machinery Ltd.

- Elettric 80

- Beumer Group

- Witron Logistik + Informatik

- TGW Logistics

- Grenzebach GmbH

- FIVES Group

- Honeywell Intelligrated

- Bastian Solutions (Toyota Advanced Logistics)

- Wayzim Technology

- Material Handling System - MHS (FORTNA)

- Jungheinrich AG

- LODIGE Industries

- ViaStore Systems (Toyota Advanced Logistics)

- Interlake Macalux

- Kardex

- AutoStore

- DMW&H

- Westfalia

- Dambach AG

- PSB intralogistics GmbH

- SIASUN Robot Automation Co., Ltd.

- KPI Integrated Solutions

- SAVOYE

- OPEX Corporation

- System Logistics (Krones Group)

- Addverb Technologies

- Lodamaster Group

- GUDEL

第 14 章 AGV/AMR:主要公司

- Geek+

- Quicktron (Flashhold)

- ForwardX Robotics

- Huaxiao Precision (Suzhou) Co., Ltd. - (CSG Huaxiao)

- GreyOrange

- HIKROBOT (HIKVISION)

- Mobile Industrial Robots - MiR (Teradyne)

- inVia Robotics

- 6 River Systems (Ocado Group)

- Fetch Robotics (Zebra Technologies)

- John Bean Technologies (JBT Corporation)

- JATEN

- IAM Robotics

- Locus Robotics

- Vecna Robotics

- BALYO

- SEEGRID

- Waypoint Robotics (Locus Robotics)

- Tompkins Robotics

- Scallog

- OTTO Motors (Clearpath Robotics)

- GIDEON Brothers

- Magazino GmbH

- NextShift Robotics (JASCI Robotics)

- AutoGuide Mobile Robots (MiR, Teradyne)

- EiraTech Robotics

- Aethon (ST Engineering)

- Prime Robotics (BLEUM)

- HAI Robotics

- Bionic HIVE

- Oppent

- PAL Robotics

- Matthews Automation Solutions (Matthews International)

- GUOZI Robotics

- CAJA Robotics

- Omron (Adept Technology)

- Guidance Automation (Matthews International)

- Syrius Robotics

- MALU Innovation

- Eurotec (Lowpad)

- DS Automotion GmbH (SSI Schaefer)

- Rocla (Mitsubishi Logisnext Europe Oy)

- Neobotix

- Transbotics (SCOTT Group)

- ek-robotics (EK Automation)

- OCEANEERING MOBILE ROBOTICS

- Wellwit Robotics

- Logistic-Jet

- Mushiny

- TUNKERS Maschinenbau GmbH

- CPM - Dürr Group

- Shanghai Seer Intelligent Technology Corporation (SEER)

- FlexQube

- Continental Mobile Robots

- IDEALworks GmbH

第 15 章自主服务提供者 (ASP)

- Brain Corporation

- Bluebotics (Zapi Group)

- Kollmorgen (Altra Industrial Motion Corp)

- Autonomous Solutions, Inc. (ASI)

- MOVEL AI

- MOV AI

- FREEDOM ROBOTICS

- ROBOMINDS

- PERCEPTIN

- Hangzhou Coevolution Technology Co., Ltd.

- FORT Robotics

- Romb Technologies

第16章机器视觉成像

- Basler AG

- Keyence

- Omron Microscan Systems

- Cognex

第 17 章消毒机器人

- UVD Robotics (Blue Ocean Robotics)

- Sarcos Robotics

- Techmetics Robotics

- Wellwit Disinfection Robotics

第 18 章零售机器人

- Bossa Nova Robotics

- Simbe Robotics

- Badger Technologies

- Lowe's - LoweBot (Powered by Fellow AI)

第 19 章室内外送机器人

- Bear Robotics

- Keenon Robotics

- Relay Robotics (Savioke Inc.)

- Rice Robotics

第 20 章安检机器人

- Cobalt Robotics

- Knightscope Robotics

- OTSAW Digital

- SMP Robotics

第 21 章远端控制/智真机器人

- Diligent Robotics

- Ohmni Labs

- AVA Robotics

- GoBe Robotics (Blue Ocean Robotics)

第 22 章 清洁机器人

- Softbank Robotics

- Avidbots

- Gaussian Robotics

- LionsBot

第 23 章医院支援机器人

- Revotonix L.L.C

- Jetbrain

第 24 章农业机器人

- Bogaerts

- Harvest Automation

第 25 章电池/充电器

- LG Chem (LG Energy Solutions)

- Crown Equipment Corporation

- East Penn Manufacturing

- EnerSys

- Conductix-Wampfler

第 26 章主要组成部分

- Advance Motion Control

- Kollmorgen

- Energid (Teradyne)

- Harmonic Drive System

- Murrelektronik

第 27 章 拣货机器人

- Berkshire Grey

- Righthand Robotics

- KINDRED (Ocado Group)

- OSARO

- Plus One Robotics

第 28 章仓库管理系统供应商

- Blue Yonder (JDA)

- Infor (Koch Industries)

- Oracle

- SAP

- Manhattan Associates

- Introduction

- General Information

- Solutions

- Manhattan SCALE (TM) WMS

- HighJump (Körber AG)

第 29 章 AIDC(自动辨识/资料撷取)

- Zebra Technologies

- Honeywell AIDC

- Data Logic

- SATO

- SICK AG

第 30 章 仓库无人机

- Eyesee (HARDIS Group)

- UVL ROBOTICS

- AirMap (DroneUp)

第 31 章送货机器人

- Starship Technologies

- NURO AI

- Tele Retail

- Kiwibot

- Robby Technologies

LogisticsIQ's latest market research study "Warehouse Automation Market By Technology (AGV/AMR, ASRS, Conveyors, Sortation, Order Picking, Automatic Identification and Data Capture, Palletizing & Depalletizing, Gantry Robots, Overhead Systems, MRO Services and WMS/WES/WCS), By Industry (E-commerce, General Merchandise, Grocery, Apparel, Food & Beverage, Pharma, 3PL), By Geography - Global Forecast to 2028", estimates that the Global Warehouse Automation Market will reach the milestone of $44 Billion by 2028, at a CAGR of 15% between 2023 and 2028.

Our 4th edition of this market study is having a detailed market analysis of more than 700+ players (part of our exclusive Market Map), 10 solutions, 7 industries and 30 countries along with more than 500 pages, 350+ Market Tables, 290+ Exhibits and 140+ Company Profiles. Analysis is validated through 100+ in-depth interviews across the value chain with components and technology providers, system integrators & manufacturers, software and services providers, and end-user industry verticals. Market size tables are also available in a pivot-ready excel format. It is a best reference to analyze the market attractiveness, to identify the partner, customer or supplier, to check the competitive landscape, to benchmark the new technologies and to select the right the geography & industry vertical for your products and services.

Of course, the push to automate the warehouses was in full force before the Covid-19 but global pandemic forced the companies to change their strategy w.r.t warehouse automation from "good to have" category to "must to have" if they have to sustain in this industry. One of the learnings from the COVID-19 pandemic is that mega-trends like aging population, globalization, health & safety, mobility, green logistics, autonomous world, urbanization, individualization and digitization need to be given more consideration and weight than in the past with a long-term vision so that we are ready with any challenge.

Year 2021 witnessed a huge order intake for warehouse automation companies but revenue growth was limited due to supply chain constraints. As a result, industry entered in 2022 with a record order backlog which got reduced in 2023 due to slowdown and macro uncertainties in 2023. Entering 2024, companies have started receiving the orders once again but retailers are still cautious about capital expenditure due to low consumer spending, high inflation, and geopolitical tension.

We see substantial growth opportunities in long term for the warehouse automation market space owing to high labor cost and several structural trends in consumer demand within eCommerce, retailing and 3PL logistics. Despite of the temporary reduction in retail and e-commerce caused by slowdown in 2023, we have observed a high interest towards warehouse automation in 2023 which may convert into new orders and revenues of these system integrators and manufacturers in 2024 onwards.

Post pandemic, most important and emerging trends have been eGrocery Growth, Micro-Fulfillment Centers, Automated Picking, Mixed Pallets Automation, Mobiile Manipulators, and Automated Cold Storages. Huge investment in start-ups such as Symbotic, Takeoff Technologies, Geek+, Fabric, Attabotics, Exotec Solutions, Hai Robotics, Addverb Technologies, and Dexterity are witnessing this growth along with presence of existing big players like Dematic, Honeywell intelligrated, SSI Schafer, Knapp, Daifuku, Muratec, AutoStore, and Toyota Advance Logistics. Retailers such as Walmart, Kroger, Coop, Target, Woolworths, Amazon, Ocado, Meijer, Carrefour, H-E-B, Albertsons, and Ahold Delhaize have already started adopting and implementing these new technologies during pandemic. Apart this, piece picking players such as Righthand Robotics, Nimble, Fizyr, Kindred, Covariant, OSARO, Plus One Robotics, Berkshire Grey, and AWL have established a new attractive capability for order picking in ecommerce fulfillment as picking is least automated process in existing warehouses.

- Automation is must for customer fulfilment: Meeting customer demands within e-commerce requires increased adoption of warehouse automation solutions to keep costs and operational complexity in check. Online retailing is fundamentally a logistics business driven by margin improvement from cost reduction in inventory management, order fulfilment and delivery capabilities.

- Scalable solutions enable Double-digit growth in e-commerce and online grocery sales is driving players to expand capacity to deliver required volumes. Warehouse automation solutions are built for scale and can deliver higher output and more accurate order fulfilment than a manual setup at lower operating costs and can increase the customer satisfaction as well as improve margins by reducing the delivery time as well as cutting down on the cost of wrong orders.

- Online Grocery Retail: Online grocery retail is the perfect use-case owing to the high-volume, low-margin nature of the business and the constraints involved in storing and delivering "fresh" products that typically involve temperature controlled supply chains. Building and delivering orders that meet increasing customer demands as well as can compete with the produce available in brick and mortar grocery stores in terms of freshness and prices, puts a huge pressure on the already thin margins in the grocery retail business. Warehouse Automation is a perfect solution for this model, as the order picking and fulfillment process can be made more cost-efficient enabling the retailer to compete on prices as well as offer same-day delivery. Micro-Fulfillment and Last Mile Delivery are going to drive this market further in next 5 years.

- Efficiency: The spatial savings from reduced warehouse footprints can be up to 85% and reductions in operational costs of up to 65%. Space savings are achieved primarily through storing SKUs higher and denser, and reductions in operational costs are resulting from decreased demand for manual labour.

KEY FINDINGS

Adoption of warehouse automation technologies is on the rise due to labor shortage, eCommerce penetration, and change in consumer behavior.

- US, Germany and China are the key market: United States, China and Germany are the largest markets with more than 50% share for Warehouse Automation both with regards to demand as well as the presence of OEMs and System Integrators. Europe is a big hub for OEMs, with strong presence in Germany, Italy, France, Netherlands, and Spain. Western Europe is a big market accounting ~30% of the overall global market. Most of the fastest growing markets are concentrated in APAC, mainly in South Asia (India) and South-East Asia. Middle East is another exciting opportunity and is well suited in terms of geography with European players looking to expand their offerings in the region. Latin America is still under-penetrated with regards to automation; however, things are set to change and market is set to observe a high growth in Brazil and Mexico. Within Europe, Central and Eastern Europe is a fast-growing region, with Poland and Czech Republic emerging as logistics hub and showing good growth prospects.

- Online Grocery becoming the top attraction for warehouse automation: The Grocery industry is one of the most challenging and attractive industries from a logistics perspective. Grocery distributors ship high cubic volumes of merchandise to retail stores with frequent deliveries to ensure product freshness. Grocery distribution center operations are amongst the most labour intensive of any industry. Higher automation driven by online grocery, micro-fulfillment centers (MFC) and ultrafast deliveries is going to be biggest opportunity in next 5 years led by different type of solution providers as AutoStore, Ocado, Takeoff Technologies, Exotec, Fabric, Symbotic, Attabotics, OPEX, , Geek+, and Urbx Logistics. It will witness an opportunity of more than $7B by 2028 with 18% growth rate. We have already witnessed many partnerships in last 2-3 years such as Ocado and Kroger in USA, Takeoff Technologies and Majid Al Futtaim in Middle East, Walmart and Symbotic in USA, Ocado and Coles in Australia, and Freshippo (Alibaba Group) in China.

- AGV/AMR will remain the key technology to adopt: AGV and AMR market is expected to be biggest market in 2028 with a CAGR of ~30%. AMR (without any external support of optical tape, sensor or vision) is going to be main contributor in the warehouses due to high demand in e-commerce sector and its flexibility to deploy the robot without any major change in the existing warehouse infrastructure. However, it is a bit slow in terms of pick rate per hour as compared to ASRS but is preferred in small and medium warehouses due to lower cost and quick deployment. It is expected that AGVs/AMRs are going to have more than 20% market share by 2028 in this market led by players like Seegrid, Balyo, Hai Robotics, Geek+, GreyOrange, HikRobot, Quicktron, Locus Robotics, Fetch Robotics (Zebra), 6 River Systems (Ocado), Teradyne (MiR, AutoGuide Mobile Robots), Rocla, JBT, ek-robotics, Omron, Rockwell Automation (Clearpath Robotics, OTTO Motors) etc.

- Picking systems are still largely manual: The order picking process can be done manually or can be automated. Manual picking is preferred when there is a wide variety of SKUs (for example online grocery shopping) to pick from. The order picking is the most labour intense part of the warehouse/DC and ideal for automation, however automation becomes increasingly challenging as the number of SKUs goes up. Barcode scanning can minimize errors but RFID (radio frequency) is quicker and more accurate for product identification. Manual pickers can still be tasked with picking individual items; however, automated storage and retrieval systems can bring the goods to the picker, and order picking robots can improve this further, thereby cutting down on a lot of manual labour and costs. Technologies like pick-to-light or pick-to-voice can also increase the efficiency of the human worker even if the task is not truly automated. Apart this, piece picking robots are the latest pick by fulfillment center for ecommerce delivered by Righthand Robotics, Berkshire Grey, Osaro, Covariant, Kindred AI, Plus One Robotics, Fizyr, Dexterity, Pickr AI etc.

Highlights of Warehouse Automation Market Report

- Warehouse Automation equipment suppliers and industry consultants expect broadly mid-teen% sales growth in long term driven by demographic changes, increased penetration in e-commerce and the advent of the Industrial IoT, that will drive demand for data analytics, 5G, digital services and automated operations in post-pandemic era.

- Competitive landscape - There are around 15 big players having annual revenue of more than $1B and 15-20 medium-size companies with revenue between $200M and $1B operating in the material handling equipment space capable of delivering comprehensive automated warehouse solutions. Top-10 large companies (including Dematic, Daifuku, SSI Schaefer, Honeywell Intelligrated, Knapp, Toyota Advance Logistics, Muratec, Beumer Group, Fortna, Witron) are capturing more than 50% of market share although lots of start-ups are emerging in new categories like AMRs, Cube based ASRS, Picking Robots, Micro-Fulfillment, Autonomy Service Providers etc. Symbotic has emerged as a new player in last couple of years to compete with stablished players in USA.

- Services, both MRO and Digital, importance is increasing - Over the time as the installed base of automated warehouse solutions grows, industry players expect an increase in revenues from services and maintenance, which would have a positive impact on profitability as the service business typically has 15-20% operating margins, versus 3-5% margins for new equipment. It is expected to be ~$11B opportunity by 2028 including digital services which is almost 25% of total market.

- Business models are also changing considering the real time pain points of end-users for high capex. Businesses are increasingly intrigued with RaaS (Robotics As a Service) because of its flexibility, scalability, and lower cost of entry than traditional robotics programs. The business model for pick-as-a-service is usually on a per-pick basis, ranging from 6 cents to 10 cents per pick, while AMR-as-a-service is usually leased on a monthly basis, from US$750 per robot per month to several thousands of dollars per month, depending on the commitment period.

- Industry Consolidation - The past 5 years have seen an increase in consolidation amongst material handling equipment providers as traditional players see acquisition of new technology leaders as an increasingly attractive way of positioning themselves in response to changing market trends. Acquisitions like Rockwell Automation (Clearpath Robotics, OTTO Motors), Jungheinrich (Magazino), SSI Schafer (DS Automotion), Zebra (Fetch Robotics, Matrox), ABB (ASTI), Toyota (Vanderlande, Bastian Solutions, ViaStore), Murata Machinery (Cimcorp), Locus Robotics (Waypoint), Hitachi (JR Automation), KPI Solutions (Kuecker Logistics Group, Pulse Integration, QC Software), Ocado (6 River Systems, Kindred, Haddington Dynamics), Element Logic (SDI), Honeywell (Intelligrated, Transnorm), Körber (Cohesio Group, Siemens Logistics, HighJump), Teradyne (MiR, Energid, AutoGuide Mobile Robots), Jungheinrich (Arculus), KION (Dematic), KUKA (Swisslog) are just some of the examples of this consolidation.

Facts to Know

- Global e-Commerce sales have grown at a CAGR of 20% over the last decade, reaching almost $5 trillion worldwide in 2021, and expected to grow to more than $8 trillion by 2027. The share of online retail sales has gone from 2% of total to 19%, and is further expected to reach >25% by 2030.

- Amazon Robotics automates the company's fulfillment centers using more than 750,000 autonomous mobile robots, 25x growth from 30,000 at the end of 2015. Amazon had been playing catchup to match supply with demand - fulfillment costs as a percentage of net sales climbed from ~15% in 2020 to 16-17% in 2022. Company has created a $1 billion venture investment program called the Amazon Industrial Innovation Fund (AIIF) to spur and support innovation in customer fulfillment, logistics, and the supply chain.

- Walmart announced has partnered with Symbotic to reimagine the retailer's regional distribution network. Symbotic first implemented its system in Walmart's Brooksville, Florida distribution center in 2017. Since that time, the companies have worked together to optimize the system. In July 2021, Walmart announced its partnership with Symbotic to implement their high-tech automation system in the regional network and planned to implement this technology in 25 of their 42 RDCs. In May 2022, both expanded commercial agreements to implement Symbotic's robotics and software automation platform in all 42 of Walmart's regional distribution centers over the coming years.

- Zalando, Europe's leading online platform for fashion and lifestyle, has opened its third fulfillment center in Poland. The ramp up marks an important milestone in Zalando's logistics network expansion with two Polish fulfillment centers serving Zalando's growing customer base and one logistics site taking care of Zalando Lounge deliveries.

- Warehouse labour shortages are also an issue with peak labour demands occurring around major shopping holidays viz. Black Friday, Cyber Monday, Amazon Prime day, Thanksgiving Day and Singles Day. Warehouses have to hire temporary labour around these peak times to meet the customer delivery schedules. Supply chain robotics company Cainiao had installed 700+ robots at China's largest robot-run warehouse to process orders on Singles Day.

- 2022 was the first year in Singles' Day history Alibaba declined to release its sales data, with the company simply stating sales were "in line" with those of 2021. Alibaba rival JD.com (China's second-largest retailer) also declined to release sales numbers for the first time-although they called their sales "record-setting". Singles' Day 2022 sales volume across all platforms was between $130 and $150 billion, an increase of between 3% and 13% from 2021. Analysts are expecting low-single-digit% growth for 2023 Singles' Day.

Amazon kicked off the arm race to automate warehouses & supply chains

Robotics & automation is rapidly becoming a key success factor in eCommerce and is about to make a very large impact on the world of logistics. From autonomous mobile robots and automatic storage systems to track & trace technologies and advanced supply chain software, it is a game changer enabling increasingly speedy, safe and error-free distribution, shorter time to market and ultimately lower costs to businesses and consumers.

Amazon was a major driving force behind the birth of the warehouse automation industry. In 2005, Amazon introduced Prime, its express shipping membership program for about a million products. Today Amazon has more than a 100 million Prime members using its fast, free, unlimited shipping on more than 30 million items, free same-day delivery on more than a million items, and even one-and-two-hour delivery on tens of thousands of items in certain cities. Prime has eventually proved sustainable with scale and automation, and has enabled Amazon to grab more than 35% share of the US eCommerce market. It is now the de facto benchmark in the online retail industry, setting consumers' expectations in terms of shipping performance at a very high level.

A massive advantage of online operations for retailers is that a very large stock file can be held in one location and distributed globally. This allows retailers to stock many more products (SKUs) than are available in each individual store without the same associated inventory risk. The success of aggregation websites shows clearly that a larger choice of products drives sales growth over time. Automation of warehouses allows retailer to handle ever larger volumes and ranges of stock, which in turn drives growth.

Amazon Prime would not be viable without leveraging cutting-edge advances in Robotics & Automation technology, which the company has turned into a source of sustainable competitive advantage. In 2012, Amazon acquired Kiva Systems in a $775m deal. Kiva Systems, now known as Amazon Robotics, pioneered the use of autonomous mobile robots for warehouse automation, introducing a revolutionary approach to order fulfilment. Kiva robots navigate autonomously around the warehouse, moving dynamically-stored shelves of ordered items to packers to fulfil orders, controlled by cutting edge control software. Today Amazon Robotics automates the company's fulfilment centers using more than 750,000 autonomous mobile robots, up more than 25x from 30,000 at the end of 2015.

With Kiva technology confined to Amazon warehouses since 2015, many companies have scrambled to fill the void and we are now seeing a proliferation of mobile robotic systems with various degrees of autonomy. The industry is still in its infancy, with competitors ranging from established players such as Swisslog, a subsidiary of KUKA recently acquired by Chinese electrical appliance giant Midea, and Adept, also acquired by Omron of Japan, to a multitude of startups such as Fetch Robotics in the US, Mobile Industrial Robots (MiR) in Denmark, which was started by a co-founder of Universal Robotics, Singapore based GreyOrange with customers in India, as well as Hikrobot Technologies, a subsidiary of Hikvision in China.

Amazon acquired Whole Foods Markets in a $14bn deal with wide ranging implications for the e-commerce and logistics industries and a sign that online grocery shopping may be ready for prime time. We think the deal marked a seminal moment in the US online grocery market, which remains in its infancy, at only 2% of the $675bn US grocery market and around 6% in the more developed UK market. The merger between Kroger and Albertsons could be another game changer in retail automation. In recent years, a number of online-only grocery services such as Ocado have tested and proven the business model, with very high automation intensity but relatively limited scale. Meanwhile, traditional grocery retailers have struggled with the last-mile logistics nightmare. Given the additional logistical challenges presented by grocery picking and shipping such as cold chain.

Order Picking remains a Robotic Challenge

Order picking in warehouses still remains a largely manual process, with Amazon commenting that commercially viable automated picking remains a "difficult challenge".

There have been launches of robots that enable automated order picking. Most of the robot vendors, as well as some of the warehouse automation players themselves, produce some variety of order picking robots. These order picker robots 'pick' the parcels off the pallet and place them into cartons or boxes, which go onto the conveyor system for further delivery.

Initially picking robots were being produced that are capable of picking objects off the shelf (which is a more subtle process), such as IAM Robotics which uses an autonomous mobile picking robot called Swift which has a Fanuc arm. These robots are often classified as collaborative robots (cobots), and the shelf-picking function often comes on top of being an automated guided vehicle, which transports objects from the shelf to the packaging and shipping corner of the warehouse. In 2020, Ocado agreed to buy San Francisco-headquartered robotics firm Kindred Systems for $262 million and Las Vegas firm Haddington Dynamics for $25 million to enhance its picking and packing capabilities. Apart this, Ocado Group acquired 6 River Robotics, a collaborative AMR fulfillment solutions provider to the logistics and non-grocery retail sectors, from Shopify in 2023.

Warehouse robots are typically used for:

- 1. De-palletizing/palletizing: De-palletizing robots strip a pallet of products coming into a warehouse. In the simplest cases this can be all the same product (say from a single manufacturer), but may also contain mixed products. De-palletizing robots are typically standard industrial robots with a dedicated tool mounted, often using a vacuum enabled grip to remove packages from the pallet. Palletizing robots re-pack the pallet for onward shipment.

- 2. Order picking: A picking arm can be mounted to a standard industrial robot/cobot. As highlighted by DHL, a standard industrial robot from the major supplier has none of the five senses when it comes out the box, meaning the sensing/machine vision, software and dexterous tool are crucial add-ons.

- 3. Goods-to-person movement through AGVs: Autonomous Guided Vehicles are typically used for goods-to-person movement.

eCommerce to be the biggest segment in the Warehouse Automation Market by 2028, followed by Grocery

eCommerce and Grocery will have the largest demand for warehouse automation equipment, growing in high-teen% through 2028. The growth of eCommerce is also driving the demand for automation solutions from geographies such as India, Indonesia, Latin America, Central & Eastern Europe, where historically there is a very low penetration of such solutions. In emerging economies, there is a high demand for modern warehouse space.

APAC will be the largest market for warehouse automation, with India demonstrating highest growth globally, in the backdrop of its huge potential in eCommerce. Regional upstarts such as GreyOrange and Addverb Technologies in India, point towards more localized solutions gaining traction with eCommerce players as well.

United States is currently the largest market for warehouse automation and is expected to maintain its leadership given the fact that fully automated warehouses account for less than 5% of the total warehouse area in US. We expect this to change substantially during our forecast period, as faster fulfillment, and shortage of labour, as well as high wages for warehouse staff), drive more adoption of automation technologies. China will play a close second to US, driven by the tremendous growth in eCommerce and the large amount SKUs being handled and shipped by players such as JD.com.

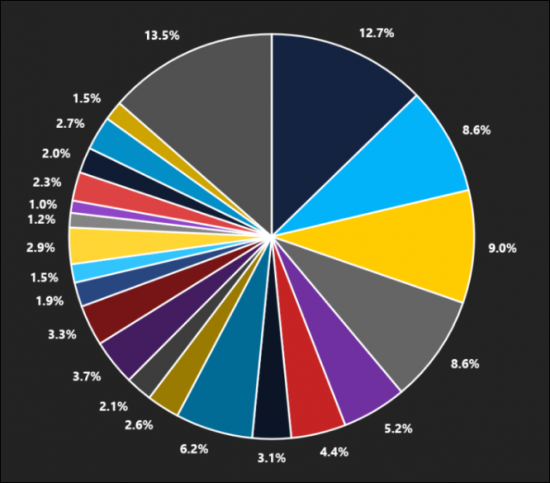

Top 10 players account for >50% of the market share* currently, market to witness more M&As in the future

Warehouse Automation Market Share

Key Players Analyzed

- Material Handling Equipment: Dematic, Daifuku, SSI Schafer, Honeywell Intelligrated, Murata Machinery, FIVES, Körber, Savoye, Witron, Beumer Group, Swisslog, TGW, Interlake Mecalux, Knapp, OPEX Corporation, Westfalia, Vanderlande, MHS Global, Bastian Solutions, SIASUN, KPI Solutions, Lodige, Kardex, Jungheinrich, Dambach, PSB Intralogistics, Gudel, Symbotic

- AGV/AMR: Geek+, Quicktron (Flashhold), Amazon Robotics (Kiva System), Grey Orange, HikRobots, MiR, inVia Robotics, Guidance Automation, IAM Robotics, EiraTech Robotics, Aethon, 6 River Systems (Shopify), Caja System, Cobalt , Sherpa (Norcan), Syrius Robotics, Locus Robotics, Matthews Automation Solutions, Waypoint Robotics, iFuture Robotics , SMP Robotics, Milvus Robotics, ALOG Tech, Vecna Robotics, Fetch Robotics, Tompkins Robotics, Scallog, MegVII, Malu Innovation, EuroTec (Lowpad), Cohesio Group (Korber), OTTO Motors (Clearpath Robotics), BLEUM, Ubiquity Robotics, Neobotix, IQ Robotics, Next Shift Robotics, KnightScope, Magazino, Intelligent Robots, Yandex, Savioke, Gideon Brothers, The Hi-Tech Robotic Systemz Ltd., ForwardX , Omron Adept, Milrem Robotics, Cainiao, Cohesio, DS Automation, Ro-ber, Rocla AGV, Active Space Automation, AgiLox, John Bean Technologies Corporation (JBT), AGVE Group, EK Automation, Transbotics (SCOTT), ESTI Mobile Robotics, America in Motion (AIM), Kivnon, Oceaneering AGV, Casun, Savant Automation, AGV International, Creform, PAL Robotics, Pulse Integration

- Warehouse Management System (WMS): AFS Technologies, Aptean, Consafe Logistics, DataByte, Davanti, Deposco, DSI, Ehrhardt + Partner Group, EVS, Generix Group, HAL, Hardis Group, HighJump, inconso, Infor, Iptor, Blue Yonder, Made4net, Manhattan Associates, Mantis, Mecalux Software, Microlistics, Oracle, Reply, SAP, Softeon, SSI SCHÄFER IT, Synergy Logistics, Tecsys, Tradelink, TTX, Vinculum, vTradEx, Savant Software, envista, Fishbowl

- Micro-Fulfillment: Takeoff Technologies, Fabric, Dematic, Knapp, Murata Machinery, Alert Innovation, Opex Corporation, Attabotics, Autostore, Exotec, Swisslog, Clevron, i-collector, Storojet, Konecranes, Ocado Technology, Pulse Integration, Geek+, Hai Robotics, Urbx Logistics, Nano Fulfillment

- Piece Picking Robots: Righthand Robotics, Kindred AI, Knapp, Universal Robotics, Berkshire Grey, Plus One Robotics, XYZ Robotics, Swisslog, Grey Orange, OSARO, Dematic, Nimble, Fizyr

- Last Mile Delivery: Myrmex Robotics, Cleveron, Starship Robots, Nuro, Refraction AI, LogiNext, PostMates, Bringg, Matternet, what3words, Deliv, Roadie, Routific, Gatik AI, iMile, Robby Technologies, Marble.io, BoxBot

- Automatic Identification and Data Capture (AIDC): Zebra Technologies, Datalogic, Cognex, SATO, Honeywell AIDC, SICK, BLUEBIRD, DENSO, Panasonic, Toshiba TEC, TSC, CASIO, SNBC, AVERY DENNISON, NCR, Scan Source, Newland America, CAB, EPSON, Unitech, M3 Mobile

- Autonomy Service Providers (ASP): Covariant AI, Brain Corp, Balyo, Mov AI, Amazon Canvas, WIBOTIC, Realtime Robotics, Seegrid, Kollmorgen, Oceaneering, MEGVII, MOVEL AI, PerceptIn, RoboCV, Robominds, SlamTec, Freedom Robotics, Humatics, Clearpath Robotics, Bluebotics, ASI, Exyn Technologies, BITO Robotics, Vecna Robotics, Robust AI, Stanley Innovation, Southie Autonomy

- Warehouse Drones: PINC Solutions, Drone Delivery Canada, Dronescan, Eyesee Drone, Infinium Robotics, Matternet, Workhorse Group, Skycart, Skysense, Zipline, Flirtey, Flytrex, Altitude Angel, Airmap, H3 Dynamics, Edronic, Cheetah Logistics Technology, Multirotor, Skyward.io, Unify, Sensefly, Volocopter GmbH, Ehang, Uber

What will you get in this report?

- 500+ Pages and 290+ Exhibits Market Report for 7 major Industry Verticals and 10 Technologies

- A bottom-up analysis of Warehouse Automation market for 20+ countries and regions

- In-depth analysis of 700 companies in the ecosystem with more than 140 company profiles

- Focus Group Discussion with 100+ key industry stakeholders across the value chain to collect the first-hand information to validate our analysis

- Excel file with a pivot modelling and 350+ market tables including forecast till 2028

- 2 Analyst Sessions to brainstorm further

- Investment details with 150+ M&A and 750+ funding deals

- LogisticsIQ™ Exclusive Market Map (650+ Players across 15+ categories)

Table of Contents

1. Warehouse Automation

- 1.1. Anatomy of warehouse operations

- 1.2. Automation lowers operating costs and is critical to achieving market success

2. Warehouse Automation Technology Breakdown

- 2.1. Warehouse Management System (WMS) , Warehouse Execution Systems (WES) and Warehouse control systems (WCS)

- 2.1.1. Warehouse Management System (WMS)

- 2.1.2. Warehouse Control System (WCS)

- 2.1.3. Warehouse Execution System (WES)

- 2.2. Automatic Identification and Data Capture

- 2.3. Conveyors, Sorting and Overhead Systems

- 2.4. Autonomous Guided Vehicles (AGVs) and Autonomous Mobile Robots (AMRs)

- 2.5. Automated Storage and Retrieval System (AS/RS) or Pallet Rack

- 2.6. Palletizing/Depalletizing Systems

- 2.7. Order Picking

- 2.7.1. Currently available technologies are capable of delivering fully automated picking solutions

- 2.7.2. Small-Scale Automation Solutions Exist but are Unlikely to Provide Sustainable Profits

3. Warehouse Automation Business Model, Drivers and Trends

- 3.1. Business Model

- 3.1.1. Robotics as a Service (RaaS)

- 3.2. Economics of Warehouse Automation

- 3.2.1. Critical factors impacting ROI

- 3.3. Industry growth drivers

- 3.4. Macro growth drivers

- 3.5. Consolidation & M&A

- 3.6. Modex 2022

- 3.6.1. 2022 MHI Innovation Award winners

- 3.6.2. Highlights

4. COVID-19 pandemic - Impact on warehouse automation

- 4.1. Immediate and short-term Impact

- 4.1.1. Logistics Automation - Crisis or Opportunity

- 4.2. Emerging Trends after COVID-19

- 4.2.1. E-Grocery

- 4.2.2. Urban Warehouses and Micro-Fulfilment

- 4.2.3. Investment Growth

5. Warehouse automation drivers and trends

- 5.1. Market Growth

- 5.2. e-Commerce is the biggest growth driver for Warehouse Automation

- 5.3. Ultrafast Delivery Services are demanding more automation

- 5.4. Robotics & Automation: Key success factors for order fulfilment

- 5.5. Online grocery is set to be the next disruption and may be the prime candidate for warehouse automation

- 5.6. Order Picking Remains a Robotic Challenge

- 5.7. Supply for Warehouse space is constrained

- 5.7.1. Developers Testing Multi-storey Warehouses in Select Markets

- 5.8. Challenges to Warehouse Automation

- 5.8.1. Upfront Investment Costs

- 5.8.2. Flexibility

- 5.9. Innovation

6. Warehouse Automation Market, by Technology

- 6.1. Conveyors and Sortation Systems

- 6.2. Overhead Systems

- 6.2.1. Gantry Robots

- 6.3. Automated Storage and Retrieval System (AS/RS)

- 6.4. Palletizing/De-palletizing Systems

- 6.5. Automatic Identification and Data Capture

- 6.5.1. From bar-codes to image reading

- 6.5.2. The rise of Android

- 6.5.3. Growing popularity of wearables

- 6.6. Autonomous Guided Vehicles (AGV) & Autonomous Mobile Robots (AMR)

- 6.7. Order Picking

- 6.7.1. Optimization with Voice Technology

- 6.7.2. Voice recognition technology in the warehouse

- 6.7.3. Analytics advantages

- 6.7.4. Robotic Piece Picking Hits Tipping Point

- 6.7.5. Collaboration

- 6.8. WMS, WES, WCS

- 6.9. MRO services

7. Warehouse Automation Market, by End-user Industry

- 7.1. E-Commerce

- 7.2. Grocery

- 7.2.1. Key players and major developments

- 7.2.2. Reasons to Automate

- 7.2.3. Reasons Not to Automate

- 7.3. Apparel

- 7.3.1. Key players and major developments

- 7.4. Food and Beverage

- 7.4.1. Key players and major developments

- 7.4.2. Post Pandemic Effects

- 7.5. General Merchandise

- 7.5.1. Key players and major developments

- 7.6. Post & Parcel

- 7.6.1. Key players and major developments

- 7.6.2. Redesign Sorting Centres for More Efficient Robotic Sorting

- 7.6.3. Up-front Cost Makes Implementation Expensive and Results in Low Adoption

- 7.7. Wholesale

- 7.8. Others (incl. Pharma & Lifesciences, Metals & Mining, Chemicals)

8. Warehouse Automation Market Share, by country

- 8.1. North America

- 8.1.1. US

- 8.1.2. Canada

- 8.2. Europe

- 8.2.1. UK

- 8.2.2. Germany

- 8.2.3. France

- 8.2.4. Italy

- 8.2.5. Spain

- 8.2.6. Netherlands

- 8.2.7. Nordics

- 8.2.8. Rest of Europe

- 8.3. Asia-Pacific

- 8.3.1. China

- 8.3.2. Japan

- 8.3.3. South Korea

- 8.3.5. India

- 8.3.6. Australia

- 8.3.7. Indonesia

- 8.3.8. Thailand

- 8.3.9. Philippines

- 8.3.10. Vietnam

- 8.3.11. Malaysia

- 8.3.12. Singapore

- 8.4. Middle East & Africa

- 8.4.1. Middle East: Key players and Developments

- 8.4.2. Saudi Arabia

- 8.4.3. UAE

- 8.4.4. Rest of GCC

- 8.4.5. Turkey

- 8.4.6. South Africa

- 8.4.7. Rest of Middle East & Africa

- 8.5. Latin America

- 8.5.1. Automation in Latin America

- 8.5.2. Logistics Is Still the Main Bottleneck in Brazil

- 8.5.3. Omni-Channel rather than Pure-play online strategy is more common amongst eCommerce players

- 8.5.4. Brazil

- 8.5.5. Mexico

- 8.5.6. Argentina

- 8.5.7. Rest of Latin America

9. Warehouse Automation Developments - Major Customers

- 9.1. Amazon

- 9.1.1. The Expanding (Accelerating) Role of Robot-Enabled Fulfilment

- 9.1.2. The Benefits of Automation/Robotics

- 9.1.3. Amazon Industrial Innovation Fund

- 9.1.4. There Is Still More Room for Improvement

- 9.1.5. Automation Beyond Amazon's Traditional Retail Operations

- 9.1.6. Amazon - Last Mile Delivery (Scout and Prime Air Drone)

- 9.1.7. Amazon Small Delivery Hubs - Urban Warehouses

- 9.1.8. Expansion Plan

- 9.2. JD.com

- 9.2.1. Warehouse Automaton

- 9.2.2. Delivery Drones

- 9.2.3. Autonomous Delivery Robots

- 9.3. Walmart

- 9.3.1. Alphabot Micro-Fulfilment Centre

- 9.3.2. Walmart Consolidation centres

- 9.3.3. Last Mile Delivery

- 9.4. Tesco

- 9.5. Kroger

- 9.6. Ocado

- 9.6.1. Ocado Smart Platform (OSP)

- 9.6.2. Ocado is distributing and licensing its technology to other retailers

- 9.7. ASOS

- 9.8. Zalando

10. Competitive Landscape

- 10.1. Key Players and their capabilities

- 10.1.1. Warehouse Equipment Providers

- 10.1.2. Warehouse Management Software Providers

- 10.1.3. AIDC Providers

- 10.2. Market Share Analysis

- 10.3. Major Players & Key Developments

- 10.3.1. Warehouse Management System (WMS)

- 10.3.2. Material Handling System

- 10.3.3. Automated Guided Vehicles (AGV) & Automated Mobile Robots (AMR)

- 10.3.4. Automatic Identification & Data Capture (AIDC)

- 10.3.5. Last Mile Delivery

- 10.3.6. Piece Picking Robots

- 10.3.7. Autonomy Service Providers (ASP)

- 10.3.8. Warehouse Drones

- 10.3.9. Artificial Intelligence (AI)

- 10.3.10. IoT Analytics

- 10.3.11. Blockchain

- 10.3.12. 5G Technology

- 10.3.13. Micro-Fulfilment

- 10.3.14. Third-Party Logistics (3PL)

11. Emerging Technologies

- 11.1. Warehouse Drones

- 11.2. Vertical Solutions

- 11.3. Underground Logistics

12. Research Methodology

13. Company Profiles

- 13.1. Daifuku

- 13.1.1. Introduction

- 13.1.2. General Information

- 13.1.3. Financial Results by reportable segments for FY2022 (In Billion Yen)

- 13.1.4. Daifuku Sales by Industry (In Billion Yen)

- 13.1.5. Business Plan - Value Transformation 2023

- 13.1.6. The Innovation Center

- 13.1.7. Geographical Presence

- 13.1.8. Major Development & News

- 13.1.9. Product Portfolio By Industry

- 13.1.10. Product Portfolio By Function

- 13.1.11. Industries & Solutions Offered

- 13.1.12. Successful Case Studies (Customer List)

- 13.2. Dematic (KION Group)

- 13.2.1. Introduction

- 13.2.2. General Information

- 13.2.3. Major Developments & News

- 13.2.4. Micro-Fulfillment Center (MFC)

- 13.2.5. Latest Developments

- 13.2.6. Recent Win & Projects

- 13.2.7. Timeline for revenue recognition

- 13.2.8. Product Portfolio

- 13.2.9. Successful Case Studies (Customer List)

- 13.2.10. Industries & Solutions Offered

- 13.3. SSI-Schaefer

- 13.3.1. Introduction

- 13.3.2. General Information

- 13.3.3. System & Solutions

- 13.3.4. Major Development & News

- 13.3.5. Solutions By Industry

- 13.3.6. Product & Software Solutions

- 13.3.7. Successful Case Studies (Customer List)

- 13.4. Vanderlande (Toyota Advanced Logistics)

- 13.4.1. Introduction

- 13.4.2. General Information

- 13.4.3. History

- 13.4.4. Major Acquisitions by Vanderlande in the past

- 13.4.5. Key Investment - Smart Robotics

- 13.4.6. Major Development & News

- 13.4.7. Products & Segments

- 13.4.8. Successful Case Studies (Customer List)

- 13.5. Swisslog (KUKA)

- 13.5.1. Introduction

- 13.5.2. General Information

- 13.5.3. History

- 13.5.4. Major Development & News

- 13.5.5. Logistics Automation - Offering by Industries

- 13.5.6. Logistics Automation - Offering by Products & Systems

- 13.5.7. Successful Case Studies (Customer List)

- 13.6. Knapp AG

- 13.6.1. Introduction

- 13.6.2. General Information

- 13.6.3. Major Development & News

- 13.6.4. Technologies by Products

- 13.6.5. Successful Case Studies (Customer List)

- 13.6.6. History

- 13.7. Murata Machinery Ltd.

- 13.7.1. Introduction

- 13.7.2. General Information

- 13.7.3. Major Development & News

- 13.7.4. Logistics & Automation - Solutions by Technology

- 13.7.5. Markets & Industries Served

- 13.7.6. Successful Case Studies (Customer List)

- 13.7.7. History and Developments

- 13.8. Elettric 80

- 13.8.1. Introduction

- 13.8.2. General Information

- 13.8.3. Industries, Products & Successful Client Base

- 13.8.4. Major Development & News

- 13.9. Beumer Group

- 13.9.1. Introduction

- 13.9.2. General Information

- 13.9.3. Major Development & News

- 13.9.4. Focused Solutions

- 13.9.5. Products by Technology

- 13.9.6. Successful Case Studies (Customer List)

- 13.9.7. Solutions by Industry

- 13.10. Witron Logistik + Informatik

- 13.10.1. Introduction

- 13.10.2. General Information

- 13.10.3. Major Development & News

- 13.10.4. Storage System, Warehouse Technology & System Type

- 13.10.5. Solutions by Industry

- 13.10.6. Industries and Case studies (Successful Clients)

- 13.11. TGW Logistics

- 13.11.1. Introduction

- 13.11.2. General Information

- 13.11.3. Products Offering

- 13.11.4. Solutions & Services

- 13.11.5. Major Development & News

- 13.11.6. Successful Case Studies (Customer List)

- 13.11.7. History & Developments

- 13.12. Grenzebach GmbH

- 13.12.1. Introduction

- 13.12.2. General Information

- 13.12.3. History

- 13.12.4. Major Development & News

- 13.12.5. Products & Markets

- 13.12.6. Transport and Handling Solutions

- 13.13. FIVES Group

- 13.13.1. Introduction

- 13.13.2. History

- 13.13.3. General Information

- 13.13.4. Major Development & News

- 13.13.5. Solutions By Industry

- 13.14. Honeywell Intelligrated

- 13.14.1. Introduction

- 13.14.2. General Information

- 13.14.3. History

- 13.14.4. Major Development & News

- 13.14.5. Solutions by Technology/Product

- 13.14.6. Industries & Solutions Offered

- 13.14.7. Successful Case Studies (Customer List)

- 13.15. Bastian Solutions (Toyota Advanced Logistics)

- 13.15.1. Introduction

- 13.15.2. General Information

- 13.15.3. Major Development & News

- 13.15.4. Solutions by Function

- 13.15.5. Solutions by Technology

- 13.15.6. Industries and Case studies (Successful Clients)

- 13.15.7. History

- 13.16. Wayzim Technology

- 13.16.1. Wayzim - Industrial Deployment

- 13.16.2. Innovative Technologies

- 13.16.3. Major Milestones & News

- 13.16.4. Product Portfolio By Industry

- 13.16.5. Product Portfolio by Function

- 13.16.6. Case Studies and Successful Clients

- 13.17. Material Handling System - MHS (FORTNA)

- 13.18. Jungheinrich AG

- 13.19. LODIGE Industries

- 13.20. ViaStore Systems (Toyota Advanced Logistics)

- 13.21. Interlake Macalux

- 13.22. Kardex

- 13.23. AutoStore

- 13.24. DMW&H

- 13.25. Westfalia

- 13.26. Dambach AG

- 13.27. PSB intralogistics GmbH

- 13.28. SIASUN Robot Automation Co., Ltd.

- 13.29. KPI Integrated Solutions

- 13.30. SAVOYE

- 13.31. OPEX Corporation

- 13.32. System Logistics (Krones Group)

- 13.33. Addverb Technologies

- 13.34. Lodamaster Group

- 13.35. GUDEL

14. AGV & AMR - Key Players

- 14.1. Geek+

- 14.2. Quicktron (Flashhold)

- 14.3. ForwardX Robotics

- 14.4. Huaxiao Precision (Suzhou) Co., Ltd. - (CSG Huaxiao)

- 14.5. GreyOrange

- 14.6. HIKROBOT (HIKVISION)

- 14.7. Mobile Industrial Robots - MiR (Teradyne)

- 14.8. inVia Robotics

- 14.9. 6 River Systems (Ocado Group)

- 14.10. Fetch Robotics (Zebra Technologies)

- 14.11. John Bean Technologies (JBT Corporation)

- 14.12. JATEN

- 14.13. IAM Robotics

- 14.14. Locus Robotics

- 14.15. Vecna Robotics

- 14.16. BALYO

- 14.17. SEEGRID

- 14.18. Waypoint Robotics (Locus Robotics)

- 14.19. Tompkins Robotics

- 14.20. Scallog

- 14.21. OTTO Motors (Clearpath Robotics)

- 14.22. GIDEON Brothers

- 14.23. Magazino GmbH

- 14.24. NextShift Robotics (JASCI Robotics)

- 14.25. AutoGuide Mobile Robots (MiR, Teradyne)

- 14.26. EiraTech Robotics

- 14.27. Aethon (ST Engineering)

- 14.28. Prime Robotics (BLEUM)

- 14.29. HAI Robotics

- 14.30. Bionic HIVE

- 14.31. Oppent

- 14.32. PAL Robotics

- 14.33. Matthews Automation Solutions (Matthews International)

- 14.34. GUOZI Robotics

- 14.35. CAJA Robotics

- 14.36. Omron (Adept Technology)

- 14.37. Guidance Automation (Matthews International)

- 14.38. Syrius Robotics

- 14.39. MALU Innovation

- 14.40. Eurotec (Lowpad)

- 14.41. DS Automotion GmbH (SSI Schaefer)

- 14.42. Rocla (Mitsubishi Logisnext Europe Oy)

- 14.43. Neobotix

- 14.44. Transbotics (SCOTT Group)

- 14.45. ek-robotics (EK Automation)

- 14.46. OCEANEERING MOBILE ROBOTICS

- 14.47. Wellwit Robotics

- 14.48. Logistic-Jet

- 14.49. Mushiny

- 14.50. TUNKERS Maschinenbau GmbH

- 14.51. CPM - Dürr Group

- 14.52. Shanghai Seer Intelligent Technology Corporation (SEER)

- 14.53. FlexQube

- 14.54. Continental Mobile Robots

- 14.55. IDEALworks GmbH

15. Autonomy Service Providers (ASP)

- 15.1. Brain Corporation

- 15.2. Bluebotics (Zapi Group)

- 15.3. Kollmorgen (Altra Industrial Motion Corp)

- 15.4. Autonomous Solutions, Inc. (ASI)

- 15.5. MOVEL AI

- 15.6. MOV AI

- 15.7. FREEDOM ROBOTICS

- 15.8. ROBOMINDS

- 15.9. PERCEPTIN

- 15.10. Hangzhou Coevolution Technology Co., Ltd.

- 15.11. FORT Robotics

- 15.12. Romb Technologies

16. Machine Vision & Imaging

- 16.1. Basler AG

- 16.2. Keyence

- 16.3. Omron Microscan Systems

- 16.4. Cognex

17. Disinfection Robots

- 17.1. UVD Robotics (Blue Ocean Robotics)

- 17.2. Sarcos Robotics

- 17.3. Techmetics Robotics

- 17.4. Wellwit Disinfection Robotics

18. Retail Robots

- 18.1. Bossa Nova Robotics

- 18.2. Simbe Robotics

- 18.3. Badger Technologies

- 18.4. Lowe's - LoweBot (Powered by Fellow AI)

19. Indoor Delivery Robots

- 19.1. Bear Robotics

- 19.2. Keenon Robotics

- 19.3. Relay Robotics (Savioke Inc.)

- 19.4. Rice Robotics

20. Security and Inspection Robots

- 20.1. Cobalt Robotics

- 20.2. Knightscope Robotics

- 20.3. OTSAW Digital

- 20.4. SMP Robotics

21. Tele-operated / Telepresence Robots

- 21.1. Diligent Robotics

- 21.2. Ohmni Labs

- 21.3. AVA Robotics

- 21.4. GoBe Robotics (Blue Ocean Robotics)

22. Cleaning Robots

- 22.1. Softbank Robotics

- 22.2. Avidbots

- 22.3. Gaussian Robotics

- 22.4. LionsBot

23. Hospital Support Robots

- 23.1. Revotonix L.L.C

- 23.2. Jetbrain

24. Agriculture Robots

- 24.1. Bogaerts

- 24.2. Harvest Automation

25. Battery & Chargers

- 25.1. LG Chem (LG Energy Solutions)

- 25.2. Crown Equipment Corporation

- 25.3. East Penn Manufacturing

- 25.4. EnerSys

- 25.5. Conductix-Wampfler

26. Key Components

- 26.1. Advance Motion Control

- 26.2. Kollmorgen

- 26.3. Energid (Teradyne)

- 26.4. Harmonic Drive System

- 26.5. Murrelektronik

27. Piece Picking Robots

- 27.1. Berkshire Grey

- 27.2. Righthand Robotics

- 27.3. KINDRED (Ocado Group)

- 27.4. OSARO

- 27.5. Plus One Robotics

28. Warehouse Management System Providers

- 28.1. Blue Yonder (JDA)

- 28.1.1. Introduction

- 28.1.2. General Information

- 28.1.3. Company Acquisitions

- 28.1.4. Intelligent Fulfillment™ WMS

- 28.2. Infor (Koch Industries)

- 28.2.1. Introduction

- 28.2.2. General Information:

- 28.2.3. History & Developments:

- 28.2.4. CloudSuite™ WMS

- 28.3. Oracle

- 28.3.1. Introduction

- 28.3.2. General Information

- 28.3.3. Products & Solutions

- 28.3.4. Oracle Warehouse Management Cloud (WMS)

- 28.4. SAP

- 28.4.1. Introduction

- 28.4.2. General Information

- 28.4.3. Portfolio

- 28.4.4. SAP Extended Warehouse Management (SAP EWM)

- 28.5. Manhattan Associates

- 28.5.1. Introduction

- 28.5.2. General Information

- 28.5.3. Solutions

- 28.5.4. Manhattan SCALE™ WMS

- 28.6. HighJump (Körber AG)

- 28.6.1. Introduction

- 28.6.2. General Information

- 28.6.3. Körber Logistics System

- 28.6.4. HighJump WMS

29. Automatic Identification and Data Capture (AIDC)

- 29.1. Zebra Technologies

- 29.1.1. Introduction

- 29.1.2. General Information

- 29.1.3. Recent Acquisitions

- 29.1.4. Warehouse Solutions

- 29.1.5. Products & Industries

- 29.2. Honeywell AIDC

- 29.2.1. Introduction

- 29.2.2. General Information

- 29.2.3. Products & Solutions

- 29.2.4. Transportation & Logistics Solutions

- 29.3. Data Logic

- 29.3.1. Introduction

- 29.3.2. General Information

- 29.3.3. Industries Targeted

- 29.3.4. Products and Systems Offered

- 29.4. SATO

- 29.4.1. Introduction

- 29.4.2. General Information

- 29.4.3. History

- 29.4.4. Industries Targeted

- 29.4.5. Hand Labeling Systems

- 29.4.6. Software

- 29.5. SICK AG

- 29.5.1. Introduction

- 29.5.2. General Information

- 29.5.3. History

- 29.5.4. Product Portfolio

- 29.5.5. Industries Targeted

30. Warehouse Drones

- 30.1. Eyesee (HARDIS Group)

- 30.2. UVL ROBOTICS

- 30.3. AirMap (DroneUp)

31. Delivery Robots

- 31.1. Starship Technologies

- 31.2. NURO AI

- 31.3. Tele Retail

- 31.4. Kiwibot

- 31.5. Robby Technologies

LIST OF EXHIBITS

- EXHIBIT 1: Systems and technologies making up Warehouse automation

- EXHIBIT 2: Process steps inside a warehouse

- EXHIBIT 3: Warehouse automation - Digitalization and Automation

- EXHIBIT 4: Barcodes optimize the identification of pallets

- EXHIBIT 5: Wearable Devices in Warehouses

- EXHIBIT 6: Main causes of error in behind order fulfillment

- EXHIBIT 7: Conveyor and Sortation

- EXHIBIT 8: Mixed Case Palletising Robot

- EXHIBIT 9: Illustration of AS/RS for Pallets with Loading Docks and Conveyor System

- EXHIBIT 10: Swisslog Shuttle AS/RS for Order Picking

- EXHIBIT 11: A Glimpse of Körber's stacker crane

- EXHIBIT 12: Liberty Research Mixed Case Palletising with Picking Robot

- EXHIBIT 13: Warehouse split case labour hours, by function

- EXHIBIT 14: Overview of Order Picking Systems by Category

- EXHIBIT 15: Classification of Automated Order Picking Systems by Number of SKUs and Throughput

- EXHIBIT 16: Pick-to-light solutions are very useful for pharmaceutical companies

- EXHIBIT 17: Autonomous Picking Robots from Fetch

- EXHIBIT 18: AGVs from Amazon Robotics (formerly KIVA)

- EXHIBIT 19: Material Handling and Warehouse Automation Value Chain

- EXHIBIT 20: Overview of Automated Warehouse System Supply Chain with Key Players

- EXHIBIT 21: Number of RaaS companies by market segment

- EXHIBIT 22: RaaS for warehouse automation

- EXHIBIT 23: Four levels of Warehouse Automation defined

- EXHIBIT 24: Major M&A since 2012

- EXHIBIT 25: Automated Warehouse - Future Look

- EXHIBIT 26: U.S. online Spend by credit card

- EXHIBIT 27: Change in willingness to invest in warehouse automation post covid-19

- EXHIBIT 28: Change in willingness to invest in warehouse automation post covid-19

- EXHIBIT 29: Online Grocery Shoppers by Retailers (2019 vs 2020)

- EXHIBIT 30: Consumers who bought the online grocery in 2018-19 and expected to buy in 2020-21

- EXHIBIT 31: Inventory Carrying Costs

- EXHIBIT 32: Investments in Warehouse Logistics startups is increasing

- EXHIBIT 33: Micro-Fulfillment Technologies

- EXHIBIT 34: Top Robotics & Automation Investment in 2021

- EXHIBIT 35: Warehouse automation market will grow ~2x to ~$44 billion by 2028

- EXHIBIT 36: eCommerce adoption continues unabated, however growth is stagnating

- EXHIBIT 37: CBRE - Logistics Property Sector Performance Drivers

- EXHIBIT 38: Ultrafast Delivery Services - Race to begin

- EXHIBIT 39: Ultrafast Delivery Services in USA

- EXHIBIT 40: Online Aggregation Model

- EXHIBIT 41: Illustration of Product Range by Retailer: U.K. Clothing

- Exhibit 42: Fetch Robotics' Fetch and Freight

- Exhibit 43: Adept's Lynx

- EXHIBIT 44: Geekplus's Mobile Robot

- EXHIBIT 45: Mobile Industrial Robots (MIR)'S MIR200

- EXHIBIT 46: Hikrobotics' Qianmo Smart Warehouse Robot

- EXHIBIT 47: Quicktron Robot

- EXHIBIT 48: Zebra Technologies' hand-free scanning, wearable computer and voice-directed picking solution

- EXHIBIT 49: CONVEYORS

- EXHIBIT 50: SWISSLOG HIGH-DENSITY AUTOSTORE

- EXHIBIT 51: Online grocery penetration is increasing in major global economies; however, the pace of growth has slowed down

- EXHIBIT 52: Palletizing Robot

- EXHIBIT 53: Picking Robot

- EXHIBIT 54: AGV

- EXHIBIT 55: Some of the Warehouse Automation Robot Players Outside Palletizing

- EXHIBIT 56: Modern Supply Chain

- EXHIBIT 57: 100 Largest U.S. Warehouse Deals by Industry

- EXHIBIT 58: E-Commerce sales and Additional Expected Annual warehouse demand

- EXHIBIT 59: Multi-storey development and population density by Metro

- EXHIBIT 60: Georgetown Crossroads - the first multi-storey warehouse in US

- EXHIBIT 61: eCommerce requires a larger building footprint

- EXHIBIT 62: Cost Breakdown of 10,000 Pallet AS/RS (Million Euros)

- EXHIBIT 63: Warehouse Automation Market to grow almost 2x at ~15% CAGR...

- EXHIBIT 64: ...with AGV/AMR and MRO services making up for the biggest share of the market...

- EXHIBIT 65: ...and eCommerce accounting for the highest demand

- EXHIBIT 66: Warehouse Automation Market By Equipment, Software & Services ($Million)

- EXHIBIT 67: Conveyors and sortation equipment is the basic building block of automated warehouse, to remain a large opportunity, albeit a moderate growth rate

- EXHIBIT 68: Challenges in e-Commerce to maintain competitiveness

- EXHIBIT 69: Online fast fashion is driving the adoption of Overhead conveyor systems

- EXHIBIT 70: Gantry Robots - Best combination of payload, flexibility and stroke

- EXHIBIT 71: AS/RS solutions are being preferred for higher accuracy and faster fulfiment of orders

- EXHIBIT 72: Palletising and De-palletising systems are needed for large warehouses

- EXHIBIT 73: Coordinated by intelligent software, ergonomic palletizing operations can address variability in SKUs and volume

- EXHIBIT 74: Palletizing is largely automated in production facilities, but the latest technologies can also handle a dynamic warehousing environment

- EXHIBIT 75: AIDC solutions to grow as well, driven in large by higher penetration in warehouse workers

- EXHIBIT 76: Traceability of ones and zeroes is great, but the latest scanners can capture image-based data about the quality of the product and the process.

- EXHIBIT 77: Solutions that are intuitive and familiar will improve onboarding and retention-both of which are critical in a tight labor market.

- EXHIBIT 78: Laser/image-based scanners are the window to real-time operations to Industry 4.0

- EXHIBIT 79: AGV and AMR is the fastest growing segment, and is necessary for fully autmated warehouses

- EXHIBIT 80: Order picking technologies are seeing higher adoption as picking accuracy becomes critical

- EXHIBIT 81: Voice based picking systems are a system's window to real-time operations and a door to Industry 4.0

- EXHIBIT 82: Analytics can spot patterns that help an organization fine tune the use of voice directed work.

- EXHIBIT 83: Voice technology being deployed for other tasks as well

- EXHIBIT 84: Robotic Piece Picking in action

- EXHIBIT 85: Robots can be pre-programmed or use AI to recognize object orientation for right pick

- EXHIBIT 86: Grippers and suction-based technologies have the most deployments

- EXHIBIT 87: Warehouse Automation Software to be a $3b+ opportunity

- EXHIBIT 88: WMS, WES and WCS are converging

- EXHIBIT 89: MRO services form the second biggest share, and essential to business model and sustainable margins

- EXHIBIT 90: One year maintenance contracts are quite common

- EXHIBIT 91: Maintenance requires training of new staff as well as maintaining an inventory of spare parts

- EXHIBIT 92: Suppliers should be brought in every six to 12 months to ensure maintenance is adequate

- EXHIBIT 93: COVID-19 - Industries hit by crisis as compared to MIA average

- EXHIBIT 94: Warehouse Automation Market By End-User Industry ($Million)

- EXHIBIT 95: eCommerce is the largest segment in Warehouse Automation, growing at high single digit YoY

- EXHIBIT 96: Global eCommerce sales will be $8 trillion by 2027, 23% of all global retail sales

- EXHIBIT 97: Sales of shopping events, broken down by avg. sales per day in USD Billion

- EXHIBIT 98: Online Grocery adoption increased due to COVID-19; higher automation is necessary for fulfilment

- EXHIBIT 99: US online grocery will be $250B market by 2025

- EXHIBIT 100: Online grocery in top 10 economies will reach $1.4b by 2028

- EXHIBIT 101: High volume, high SKUs and high cost of returns pushing apparel players to automate operations

- EXHIBIT 102: Ecommerce Penetration Rate in Fashion and Apparel Market

- EXHIBIT 103: H&M continues to invest in automated online warehouses to provide next day delivery

- EXHIBIT 104: Automation in F&B is driven by higher focus on safety regulations & improving operating margins

- EXHIBIT 105: Coca-Cola, Northmead, Australia

- EXHIBIT 106: General Merchandise presents a significant opportunity however, adoption is slow

- EXHIBIT 107: Post and Parcel is slow to adopt automation in sorting centers, limited by the ROI benefits

- EXHIBIT 108: Seegrid Tugger at Pennwood Place

- EXHIBIT 109: Wholesale distribution of goods is a slow growth segment as demand for faster delivery is limited

- EXHIBIT 110: Others segment has niche end-markets and growth is expected to remain stagnant

- EXHIBIT 111: APAC will account for the largest demand for warehouse automation equipment, while US will be the single largest country

- EXHIBIT 112: Warehouse Automation Market By Country ($Million)

- EXHIBIT 113: North America Warehouse Automation Market Size in US$ Million

- EXHIBIT 114: US Warehouse Automation Market Size in US$ Million

- EXHIBIT 115: Top U.S. players for Retail Ecommerce Sales (%) in 2021

- EXHIBIT 116: Warehouse Automation Market in United States By Equipment ($Million)

- EXHIBIT 117: Warehouse Automation Market By End-Use Industry ($Million)

- EXHIBIT 118: Investment Deals in USA for 2021

- EXHIBIT 119: Canada Warehouse Automation Market Size in US$ Million

- EXHIBIT 120: Warehouse Automation Market In Canada By Equipment ($Million)

- EXHIBIT 121: Warehouse Automation Market in Canada By End-Use Industry ($Million)

- EXHIBIT 122: Investment Deals in Canada for 2021

- EXHIBIT 123: Western Europe Warehouse Automation Market Size in US$ Million

- EXHIBIT 124: Central & Eastern Europe Warehouse Automation Market Size in US$ Million

- EXHIBIT 125: UK Online Market Share of Top-5 Players

- EXHIBIT 126: UK Warehouse Automation Market Size (2016-2026) in US$ Million

- EXHIBIT 127: Investment Deals in Canada for 2021

- EXHIBIT 128: Asda's AutoStore Installation (Supplied by Swisslog) in Lutterworth

- EXHIBIT 129: Warehouse Automation Market in United Kingdom By Equipment ($Million)

- EXHIBIT 130: Warehouse Automation Market in United Kingdom By End-Use Industry ($Million)

- EXHIBIT 131: Germany Warehouse Automation Market Size in US$ Million

- EXHIBIT 132: Warehouse Automation Market in Germany By Equipment ($Million)

- EXHIBIT 133: Warehouse Automation Market in Germany By End-Use Industry ($Million)

- EXHIBIT 134: Investment Deals in Germany for 2021

- EXHIBIT 135: France Warehouse Automation Market Size in US$ Million

- EXHIBIT 136: Investment Deals in France for 2020-21

- EXHIBIT 137: Online grocery in France will be a $48bn market by 2027

- EXHIBIT 138: Warehouse Automation Market in France By Equipment ($Million)

- EXHIBIT 139: Casino has partnered with Ocado to develop automated CFC

- EXHIBIT 140: Warehouse Automation Market in France By End-Use Industry ($Million)

- EXHIBIT 141: Italy Warehouse Automation Market Size in US$ Million

- EXHIBIT 142: Warehouse Automation Market in Italy By Equipment ($Million)

- EXHIBIT 143: Warehouse Automation Market in Italy By End-Use Industry ($Million)

- EXHIBIT 144: Spain Warehouse Automation Market Size in US$ Million

- EXHIBIT 145: Warehouse Automation Market in Spain, By Equipment ($Million)

- EXHIBIT 146: Warehouse Automation Market in Spain, By End-Use Industry ($Million)

- EXHIBIT 147: Netherlands Warehouse Automation Market Size in US$ Million: Driven by Grocery & Retail

- EXHIBIT 148: Warehouse Automation Market in Netherlands, By Equipment ($Million)

- EXHIBIT 149: Warehouse Automation Market in Netherlands, By End-Use Industry ($Million)

- EXHIBIT 150: Parcel lockers in the Nordics

- EXHIBIT 151: Nordics Warehouse Automation Market Size in US$ Million

- EXHIBIT 152: SOK/ Inex Oy automated warehouse

- EXHIBIT 153: Warehouse Automation Market in Nordics By Equipment ($Million)

- EXHIBIT 154: Warehouse Automation Market in Nordics By End-Use Industry ($Million)

- EXHIBIT 155: Rest of Western Europe Warehouse Automation Market Size in US$ Million

- EXHIBIT 156: Warehouse Automation Market in Rest of Western Europe By Equipment ($Million)

- EXHIBIT 157: Warehouse Automation Market in Rest of Western Europe By End-Use Industry ($Million)

- EXHIBIT 158: Warehouse Automation Market in Rest of Central and Eastern Europe By Equipment ($Million)

- EXHIBIT 159: Warehouse Automation Market in Rest of Central and Eastern Europe By End-Use Industry ($Million)

- EXHIBIT 160: Asia-Pacific Warehouse Automation Market Size in US$ Million

- EXHIBIT 161: China eCommerce is booming, but distribution and logistics is lagging

- EXHIBIT 162: China Warehouse Automation Market Size in US$ Million

- EXHIBIT 163: Automated warehouses cost more than 15x traditional warehouse

- EXHIBIT 164: Warehouse Automation Market in China By Equipment ($Million)

- EXHIBIT 165: Warehouse Automation Market in China By End-Use Industry ($Million)

- EXHIBIT 166: Investment Deals in China for 2021

- EXHIBIT 167: Japan Warehouse Automation Market Size in US$ Million

- EXHIBIT 168: Warehouse Automation Market in Japan By Equipment ($Million)

- EXHIBIT 169: Warehouse Automation Market in Japan By End-Use Industry ($Million)

- EXHIBIT 170: South Korea Warehouse Automation Market Size in US$ Million

- EXHIBIT 171: Warehouse Automation Market in South Korea By ($Million)

- EXHIBIT 172: Warehouse Automation Market in South Korea By ($Million)

- EXHIBIT 173: India Warehouse Automation Market Size in US$ Million

- EXHIBIT 174: Demand for warehouse space is being driven by eCommerce

- EXHIBIT 175: Sorter Robot

- EXHIBIT 176: Addverb Technologies Portfolio

- EXHIBIT 177: Warehouse Automation Market in India By Equipment ($Million)

- EXHIBIT 178: Warehouse Automation Market in India By End-Use Industry ($Million)

- EXHIBIT 179: Australia Warehouse Automation Market Size in US$ Million

- EXHIBIT 180: Warehouse Automation Market in Australia By Equipment ($Million)

- EXHIBIT 181: Warehouse Automation Market in Australia By End-Use Industry ($Million)

- EXHIBIT 182: Indonesia Warehouse Automation Market Size in US$ Million

- EXHIBIT 183: The South-east Asian eCommerce market is booming

- EXHIBIT 184: Warehouse Automation Market in Indonesia by Equipment ($Million)

- EXHIBIT 185: Warehouse Automation Market in Indonesia By End-Use Industry ($Million)

- EXHIBIT 186: Thailand Warehouse Automation Market Size in US$ Million

- EXHIBIT 187: Warehouse Automation Market in Thailand By Equipment ($Million)

- EXHIBIT 188: Warehouse Automation Market in Thailand By Equipment ($Million)

- EXHIBIT 189: Philippines Warehouse Automation Market Size in US$ Million

- EXHIBIT 190: Warehouse Automation Market in Philippines By Equipment ($Million)

- EXHIBIT 191: Warehouse Automation Market in Philippines By End-Use Industry ($Million)

- EXHIBIT 192: Vietnam Warehouse Automation Market Size in US$ Million

- EXHIBIT 193: Warehouse Automation Market in Vietnam By Equipment ($Million)

- EXHIBIT 194: Warehouse Automation Market in Vietnam By End-Use Industry ($Million)

- EXHIBIT 195: Malaysia Warehouse Automation Market Size in US$ Million

- EXHIBIT 196: Warehouse Automation Market in Malaysia By Equipment ($Million)

- EXHIBIT 197: Warehouse Automation Market in Malaysia By End-Use Industry ($Million)

- EXHIBIT 198: Singapore Warehouse Automation Market (US$ Million)

- EXHIBIT 199: Warehouse Automation Market in Singapore By Equipment ($Million)

- EXHIBIT 200: Warehouse Automation Market in Singapore By End-Use Industry ($Million)

- EXHIBIT 201: Middle-East Warehouse Automation Market was $0.7B in 2021 and to be 3x $2.1B in 2027E

- EXHIBIT 202: Retail Strategy for eCommerce in Middle East

- EXHIBIT 203: Middle East Retail Ecosystem

- EXHIBIT 204: Saudi Arabia Warehouse Automation Market Size in US$ Million

- EXHIBIT 205: Warehouse Automation Market in Saudi Arabia By Equipment ($Million)

- EXHIBIT 206: Warehouse Automation Market in Saudi Arabia By End-Use Industry ($Million)

- EXHIBIT 207: UAE Warehouse Automation Market Size in US$ Million

- EXHIBIT 208: Warehouse Automation Market in UAE By Equipment ($Million)

- EXHIBIT 209: Warehouse Automation Market in UAE By End-Use Industry ($Million)

- EXHIBIT 210: Rest of GCC Warehouse Automation Market Size in US$ Million

- EXHIBIT 211: Warehouse Automation Market in Rest of GCC By Equipment ($Million)

- EXHIBIT 212: Warehouse Automation Market in Rest of GCC By End-Use Industry ($Million)

- EXHIBIT 213: Turkey Warehouse Automation Market Size in US$ Million