|

市场调查报告书

商品编码

1927588

全球手术机器人市场按产品、应用、最终用户和地区划分-预测至2030年Surgical Robots Market By Product (Instruments & Accessories, Robotic Systems (Laparoscopy, Orthopedic), Services), Application (Urological Surgery, Orthopedic Surgery), End User (Hospitals, Clinics, Ambulatory Surgery Centers) - Global Forecast to 2030 |

||||||

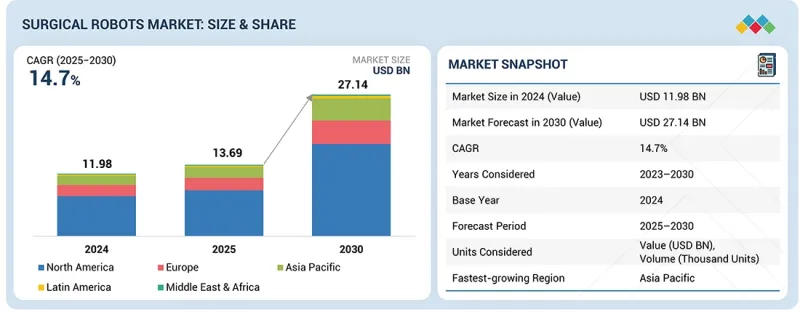

全球手术机器人市场预计将从 2025 年的 136.9 亿美元成长到 2030 年的 271.4 亿美元,预测期内复合年增长率为 14.7%。

| 调查范围 | |

|---|---|

| 调查期 | 2023-2030 |

| 基准年 | 2024 |

| 预测期 | 2025-2030 |

| 目标单元 | 金额(十亿美元) |

| 部分 | 按产品/服务、按应用、按最终用户、按地区 |

| 目标区域 | 北美、欧洲、亚太地区及其他地区 |

随着医疗机构越来越多地采用机器人辅助系统来提高手术精度、改善患者预后并支持微创手术,手术机器人市场正经历显着成长。对更快康復时间、更少併发症和更短住院时间的需求不断增长,促使医院在多个专科领域投资机器人技术。持续的技术进步,包括更先进的成像技术、人工智慧驱动的导航以及更紧凑的机器人平台,正在拓展机器人手术的临床应用。同时,不断扩大的外科医生培训计画、完善的报销体係以及意识提升也在加速机器人手术的普及。这些因素共同推动市场发展,并扩大了机器人辅助手术在全球的应用范围。

手术机器人器械及配件在手术机器人市场中占据最大份额,因为这些组件是所有机器人手术的必备要素,能够产生稳定且持续的需求。虽然机器人系统本身需要初始资本投资,但器械和其他耗材,例如缝合器、剪刀、抓钳和能量器械等,在使用一定次数后需要更换,从而确保了系统的持续利用和收入。此外,视觉工具、连接埠和套管针等配件对于系统功能至关重要,也需要频繁补充。随着机器人手术数量的增加和医院机器人专案的扩展,器械及配件的消耗量也相应增长,使其成为整体市场收入的最大贡献者。

由于医院和诊所作为主要的手术中心,拥有部署必要的设施、资金和训练有素的人员来实施机器人技术的能力,因此它们在手术机器人市场中主导。这些机构正在投资机器人技术,以提高手术精确度、改善患者预后并简化临床工作流程。微创手术的优惠报销政策也推动了机器人系统的应用。此外,大多数外科医生都在医院环境中接受过机器人手术培训,从而提高了机器人手术的使用率。随着患者对先进的微创治疗的需求日益增长,医院和诊所仍然是市场上最大、最具影响力的终端用户。

美国预计将成为北美手术机器人市场中复合年增长率最高的国家,这主要得益于其对先进医疗技术的重视、机器人手术项目的快速扩张以及对医院基础设施的持续投入。美国拥有训练有素的外科医生人才储备、广泛的临床研究活动以及患者对微创手术的高需求,所有这些因素都在加速机器人平台的普及应用。有利的医疗保险政策、主要机器人手术设备製造商的强大影响力以及持续的产品创新也进一步推动了市场成长。此外,与该地区其他国家相比,美国医疗保健系统对改善病患预后、缩短住院时间和提高手术精准度的重视,也进一步加速了手术机器人在美国的应用。

手术机器人市场的主要企业有:Intuitive Surgical(美国)、Stryker(美国)、Medtronic(爱尔兰)、Smith+Nephew(英国)、Zimmer Biomet(美国)、Asensus Surgical(美国)、Siemens Healthineers(德国)、CMR Surgical(英国)、Johnson & Johnson(美国)和Renishaw Plclc(英国)。

研究范围:

本报告旨在分析手术机器人市场,并根据产品、应用、最终用户、地区等各种细分市场估算市场规模和未来成长潜力。该报告还提供了主要企业的竞争分析,以及公司简介、服务产品、近期发展和关键市场策略。

购买本报告的理由

本报告提供手术机器人市场整体收入最准确的估计值,有助于市场领导和新参与企业。它帮助相关人员了解竞争格局,并提供有价值的见解,以帮助他们优化业务定位并制定合适的打入市场策略。此外,它还透过提供有关关键市场驱动因素、限制、挑战和机会的信息,帮助他们了解市场趋势。

本报告深入分析了以下内容:

- 对关键驱动因素(机器人辅助手术的优势、技术进步、报销的改善、手术机器人的日益普及以及医疗机器人研究资金的增加)、限制因素(机器人系统高成本)、机会(手术机器人在门诊手术中心 (ASC) 的渗透率不断提高以及新兴市场的增长机会)和挑战(手术错误)进行分析。

- 市场渗透率:该报告详细介绍了全球手术机器人市场主要参与者提供的产品,涵盖了按产品类型、应用、最终用户和地区分類的各个细分市场。

- 产品增强与创新:全面详细资讯全球外科手术机器人市场的新产品发布与预测趋势。

- 市场开发:按产品、应用、最终用户和地区,提供对盈利且不断增长的市场的深入见解和分析。

- 市场多元化:提供有关全球手术机器人市场的新产品发布、市场扩张、当前进展和投资的全面资讯。

- 竞争格局分析:对全球手术机器人市场主要竞争对手的市场份额、成长计画、产品供应和生产能力进行详细评估。

目录

第一章 引言

第二章执行摘要

第三章 市场概览

- 司机

- 抑制因素

- 机会

- 任务

- 未满足的需求和閒置频段

- 相互关联的市场与跨产业机会

- 一级/二级/三级公司的策略性倡议

第四章 产业趋势

- 波特五力分析

- 宏观经济展望

- 供应链分析

- 价值链分析

- 生态系分析

- 定价分析

- 贸易数据分析

- 2025-2026 年主要会议和活动

- 影响客户业务的趋势/颠覆性因素

- 投资和资金筹措方案

- 案例研究分析

- 2025年美国关税对外科机器人市场的影响

第五章:技术进步、人工智慧的影响、专利、创新与未来应用

- 关键新兴技术

- 技术/产品蓝图

- 专利分析

- 手术机器人的未来应用

- 人工智慧/生成式人工智慧对外科手术机器人市场的影响

第六章 监理环境

- 地方法规和合规性

- 认证、标籤和环境标准

第七章:顾客状况与购买行为

- 决策流程

- 主要相关人员和采购评估标准

- 招募障碍和内部挑战

- 终端用户产业未满足的需求

- 市场盈利

8. 手术机器人市场(依产品/服务分类)

- 医疗设备及配件

- 机器人系统

- 服务

第九章 手术机器人市场(依应用领域划分)

- 一般外科

- 妇科手术

- 整形外科

- 泌尿系统手术

- 神经外科

- 显微外科手术

- 耳鼻喉科手术

- 其他的

第十章 手术机器人市场(依最终用户划分)

- 医院和诊所

- 门诊手术中心

第十一章 各地区手术机器人市场

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 其他的

- 亚太地区

- 日本

- 中国

- 印度

- 澳洲

- 韩国

- 其他的

- 拉丁美洲

- 巴西

- 墨西哥

- 其他的

- 中东和非洲

- 海湾合作委员会国家

- 其他的

第十二章 竞争格局

- 主要参与企业的策略/优势

- 2020-2024年收入分析

- 2024年市占率分析

- 公司估值矩阵:主要参与企业,2024 年

- 公司估值矩阵:Start-Ups/中小企业,2024 年

- 估值和财务指标

- 品牌/产品对比

- 竞争场景

第十三章:公司简介

- 主要参与企业

- INTUITIVE SURGICAL OPERATIONS, INC.

- STRYKER

- ZIMMER BIOMET

- MEDTRONIC

- SMITH+NEPHEW

- ASENSUS SURGICAL US, INC.

- SIEMENS HEALTHINEERS AG

- RENISHAW PLC

- GLOBUS MEDICAL

- JOHNSON & JOHNSON

- CMR SURGICAL LTD.

- THINK SURGICAL, INC.

- CORIN GROUP

- MICROSURE

- AVATERAMEDICAL GMBH

- MEDICAL MICROINSTRUMENTS, INC.

- MEDICAROID CORPORATION

- BRAINLAB SE

- ECENTIAL ROBOTICS

- SS INNOVATIONS INTERNATIONAL, INC.

- 其他公司

- MONTERIS

- MOMENTIS INNOVATIVE SURGERY

- TINAVI MEDICAL TECHNOLOGIES CO., LTD.

- DISTALMOTION SA

- NOVUS SAGLIK URUNLERI AR-GE DANISMANLIK(NOVUS ARGE)

第十四章调查方法

第十五章附录

The global surgical robots market is projected to reach USD 27.14 billion by 2030 from USD 13.69 billion in 2025, at a CAGR of 14.7% during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2023-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD billion) |

| Segments | Product, Application, End User, and Region |

| Regions covered | North America, Europe, APAC, RoW |

The surgical robots market is experiencing strong growth as healthcare providers increasingly adopt robotic-assisted systems to enhance surgical precision, improve patient outcomes, and support minimally invasive procedures. The rising demand for faster recovery, reduced complications, and shorter hospital stays is driving hospitals to invest in robotics across multiple specialties. Continuous technological advancements, such as improved imaging, AI-driven guidance, and more compact robotic platforms, are expanding the clinical applications of robotic surgery. At the same time, the growth of surgeon training programs, supportive reimbursement structures, and increased patient awareness are accelerating adoption. Together, these factors are pushing the market forward and broadening the global footprint of robotic-assisted surgery.

"By offering, the instruments & accessories segment held the largest market share in 2024."

The instruments & accessories segment accounts for the largest share of the surgical robots market because these components are required for every robotic procedure, creating steady and recurring demand. While robotic systems are a one-time capital investment, instruments such as staplers, scissors, graspers, energy devices, and other consumables must be replaced after a limited number of uses, ensuring continuous utilization and revenue. Accessories, such as vision tools, ports, and trocars, are also essential for system functionality and require frequent replenishment. As robotic procedure volumes continue to rise and hospitals expand their robotic programs, the consumption of instruments and accessories grows proportionally, making this segment the most significant contributor to overall market revenue.

"By end user, the hospitals & clinics segment accounted for the largest market share in 2024."

Hospitals & clinics dominate the surgical robots market because they are the primary locations where surgeries are performed and have the necessary facilities, financial resources, and trained personnel to adopt robotic technologies. These institutions invest in robotics to improve surgical precision, enhance patient outcomes, and streamline clinical workflows. Favorable reimbursement policies for minimally invasive procedures further support their adoption of robotic systems. Additionally, most surgeons undergo robotic training within hospital environments, which increases utilization. With growing patient expectations for advanced, minimally invasive care, hospitals & clinics continue to be the largest and most influential end users in the market.

"The US is expected to grow at the highest CAGR during the forecast period."

The US is expected to grow at the highest CAGR within the North American surgical robots market due to its strong focus on adopting advanced medical technologies, rapid expansion of robotic-assisted surgical programs, and continuous investments in hospital infrastructure. The country benefits from a large base of trained surgeons, extensive clinical research activity, and high patient demand for minimally invasive procedures, all of which accelerate the uptake of robotic platforms. Favorable reimbursement policies, a strong presence of leading robotic surgery manufacturers, and ongoing product innovations further support growth. Additionally, the US healthcare system's emphasis on improving patient outcomes, reducing hospital stays, and enhancing surgical precision continues to drive faster adoption of surgical robots compared to other countries in the region.

A breakdown of the primary participants (supply side) for the surgical robots market referred to in this report is provided below:

- By Company Type: Tier 1 (35%), Tier 2 (40%), and Tier 3 (25%)

- By Designation: C-level Executives (45%), Director-level Executives (35%), and Others (20%)

- By Region: North America (27%), Europe (25%), Asia Pacific (30%), Latin America (8%), and the Middle East & Africa (10%)

Prominent players in the surgical robots market are Intuitive Surgical (US), Stryker (US), Medtronic (Ireland), Smith+Nephew (UK), Zimmer Biomet (US), Asensus Surgical (US), Siemens Healthineers (Germany), CMR Surgical (UK), Johnson & Johnson (US), and Renishaw Plc (UK).

Research Coverage:

The report analyzes the surgical robots market and aims at estimating the market size and future growth potential of this market based on various segments such as offering, application, end user, and region. The report also includes a competitive analysis of the key players in this market along with their company profiles, service offerings, recent developments, and key market strategies.

Reasons to Buy the Report

The report will help market leaders/new entrants in this market with information on the closest approximations of the revenue numbers for the overall surgical robots market. This report will help stakeholders understand the competitive landscape and gain valuable insights to better position their businesses and plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market, providing them with information on key market drivers, restraints, challenges, and opportunities.

This report provides insights into the following pointers:

- Analysis of key drivers (advantages of robot-assisted surgery, technological advancements, improving reimbursement scenario, increasing adoption of surgical robots, and increasing funding for medical robot research), restraints (high cost of robotic systems), opportunities (increasing penetration of surgical robots in ASCs and growth opportunities in emerging markets), and challenges (surgical errors).

- Market Penetration: It includes extensive information on products offered by the major players in the global surgical robots market. The report includes various segments by offering, application, end user, and region.

- Product Enhancement/Innovation: Comprehensive details about new product launches and anticipated trends in the global surgical robots market.

- Market Development: Thorough knowledge and analysis of the profitable rising markets by offering, application, end user, and region.

- Market Diversification: Comprehensive information about newly launched products, expanding markets, current advancements, and investments in the global surgical robots market.

- Competitive Assessment: Thorough evaluation of the market shares, growth plans, offerings of products, and capacities of the major competitors in the global surgical robots market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION & REGIONAL SCOPE

- 1.3.2 INCLUSIONS & EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.4 STAKEHOLDERS

- 1.5 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS & MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: INSIGHTS & DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING MARKET GROWTH

- 2.4 HIGH-GROWTH SEGMENTS & EMERGING FRONTIERS

- 2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 MARKET OVERVIEW

- 3.1 INTRODUCTION

- 3.1.1 DRIVERS

- 3.1.1.1 Advantages of robot-assisted minimally invasive surgeries

- 3.1.1.2 Technological advancements in surgical robots

- 3.1.1.3 Improving reimbursement scenario for surgical robots

- 3.1.1.4 Increasing adoption of surgical robots in modern surgeries

- 3.1.1.5 Increasing funding for medical robot research

- 3.1.2 RESTRAINTS

- 3.1.2.1 High cost of robotic systems

- 3.1.3 OPPORTUNITIES

- 3.1.3.1 Increasing penetration of surgical robots in outpatient settings

- 3.1.3.2 High growth opportunities in emerging economies

- 3.1.4 CHALLENGES

- 3.1.4.1 Rising number of surgical errors in global healthcare systems

- 3.1.1 DRIVERS

- 3.2 UNMET NEEDS & WHITE SPACES

- 3.2.1 UNMET NEEDS IN SURGICAL ROBOTS MARKET

- 3.2.2 WHITE SPACE OPPORTUNITIES

- 3.3 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 3.3.1 INTERCONNECTED MARKETS

- 3.3.2 CROSS-SECTOR OPPORTUNITIES

- 3.4 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

4 INDUSTRY TRENDS

- 4.1 PORTER'S FIVE FORCES ANALYSIS

- 4.1.1 THREAT OF NEW ENTRANTS

- 4.1.2 THREAT OF SUBSTITUTES

- 4.1.3 BARGAINING POWER OF SUPPLIERS

- 4.1.4 BARGAINING POWER OF BUYERS

- 4.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 4.2 MACROECONOMIC OUTLOOK

- 4.2.1 INTRODUCTION

- 4.2.2 GDP TRENDS AND FORECAST

- 4.2.3 TRENDS IN GLOBAL MINIMALLY INVASIVE SURGICAL INSTRUMENTS INDUSTRY

- 4.2.4 TRENDS IN GLOBAL MEDICAL ROBOTS INDUSTRY

- 4.3 SUPPLY CHAIN ANALYSIS

- 4.4 VALUE CHAIN ANALYSIS

- 4.5 ECOSYSTEM ANALYSIS

- 4.6 PRICING ANALYSIS

- 4.6.1 AVERAGE SELLING PRICE OF SURGICAL ROBOTIC APPLICATIONS, BY KEY PLAYER, 2024

- 4.6.2 AVERAGE SELLING PRICE TREND OF SURGICAL ROBOTS, BY REGION, 2022-2024

- 4.7 TRADE DATA ANALYSIS

- 4.7.1 IMPORT DATA FOR HS CODE 901890

- 4.7.2 EXPORT DATA FOR HS CODE 901890

- 4.8 KEY CONFERENCES AND EVENTS, 2025-2026

- 4.9 TRENDS/DISRUPTIONS IMPACTING CUSTOMER'S BUSINESS

- 4.10 INVESTMENT AND FUNDING SCENARIO

- 4.11 CASE STUDY ANALYSIS

- 4.11.1 REVOLUTIONISING FUTURE OF SURGERY WITH HIGH-PRECISION ROBOTS

- 4.11.2 HUNJAN HOSPITAL DEPLOYS ORTHOPEDIC SURGICAL ROBOT FOR KNEE REPLACEMENT SURGERY

- 4.11.3 BIONAUT LABS CREATES REMOTE-CONTROLLED MICRO-ROBOTS TO TARGET BRAIN DISEASES

- 4.12 IMPACT OF 2025 US TARIFF ON SURGICAL ROBOTS MARKET

- 4.12.1 KEY TARIFF RATES

- 4.12.2 PRICE IMPACT ANALYSIS

- 4.12.3 IMPACT ON COUNTRY/REGION

- 4.12.3.1 North America

- 4.12.3.1.1 US

- 4.12.3.2 Europe

- 4.12.3.3 Asia Pacific

- 4.12.3.1 North America

- 4.12.4 IMPACT ON END-USE INDUSTRIES

5 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 5.1 KEY EMERGING TECHNOLOGIES

- 5.1.1 ROBOTIC ARMS AND INSTRUMENTS

- 5.1.2 ARTIFICIAL INTELLIGENCE (AI) AND MACHINE LEARNING (ML)

- 5.1.3 TELEPRESENCE

- 5.1.4 5G TECHNOLOGY

- 5.1.5 COMPLEMENTARY TECHNOLOGIES

- 5.1.5.1 Augmented reality (AR) and virtual reality (VR)

- 5.1.5.2 3D printing

- 5.2 TECHNOLOGY/PRODUCT ROADMAP

- 5.2.1 SHORT-TERM (2025-2027) | FOUNDATION & EARLY COMMERCIALIZATION

- 5.2.2 MID-TERM (2027-2030) | EXPANSION & STANDARDIZATION

- 5.2.3 LONG-TERM (2030-2035+) | MASS COMMERCIALIZATION & DISRUPTION

- 5.3 PATENT ANALYSIS

- 5.4 FUTURE APPLICATIONS OF SURGICAL ROBOTS

- 5.5 IMPACT OF AI/GEN AI ON SURGICAL ROBOTS MARKET

- 5.5.1 TOP USE CASES AND MARKET POTENTIAL

- 5.5.2 BEST PRACTICES IN SURGICAL ROBOTS PROCESSING

- 5.5.3 CASE STUDIES OF AI IMPLEMENTATION

- 5.5.4 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 5.5.5 CLIENTS' READINESS TO ADOPT GENERATIVE AI

6 REGULATORY LANDSCAPE

- 6.1 REGIONAL REGULATIONS AND COMPLIANCE

- 6.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 6.1.2 REGULATORY FRAMEWORK

- 6.1.2.1 North America

- 6.1.2.1.1 US

- 6.1.2.2 Europe

- 6.1.2.3 Asia Pacific

- 6.1.2.3.1 Japan

- 6.1.2.3.2 China

- 6.1.2.3.3 India

- 6.1.2.1 North America

- 6.1.3 INDUSTRY STANDARDS

- 6.2 CERTIFICATIONS, LABELING, AND ECO-STANDARDS

7 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 7.1 DECISION-MAKING PROCESS

- 7.2 KEY STAKEHOLDERS & BUYING EVALUATION CRITERIA

- 7.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 7.2.2 KEY BUYING CRITERIA

- 7.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 7.4 UNMET NEEDS FROM END-USE INDUSTRIES

- 7.5 MARKET PROFITABILITY

- 7.5.1 REVENUE POTENTIAL

- 7.5.2 COST DYNAMICS

- 7.5.3 MARGIN OPPORTUNITIES IN KEY APPLICATIONS

8 SURGICAL ROBOTS MARKET, BY OFFERING

- 8.1 INTRODUCTION

- 8.2 INSTRUMENTS & ACCESSORIES

- 8.2.1 NEED FOR RECURRENT PURCHASE OF INSTRUMENTS & ACCESSORIES TO DRIVE MARKET GROWTH

- 8.3 ROBOTIC SYSTEMS

- 8.3.1 LAPAROSCOPIC ROBOTIC SYSTEMS

- 8.3.1.1 Growing popularity of laparoscopic robotic surgeries to drive market

- 8.3.2 ORTHOPEDIC ROBOTIC SYSTEMS

- 8.3.2.1 Rising number of market players offering orthopedic robots to support market growth

- 8.3.3 NEUROSURGICAL ROBOTIC SYSTEMS

- 8.3.3.1 Better reproducibility, higher accuracy, and greater precision in long, narrow surgical corridors to support market growth

- 8.3.4 OTHER ROBOTIC SYSTEMS

- 8.3.1 LAPAROSCOPIC ROBOTIC SYSTEMS

- 8.4 SERVICES

- 8.4.1 ONGOING NEED FOR SERVICE CONTRACTS FOR FUNDAMENTAL OPERATIONS TO PROPEL MARKET GROWTH

9 SURGICAL ROBOTS MARKET, BY APPLICATION

- 9.1 INTRODUCTION

- 9.2 GENERAL SURGERY

- 9.2.1 GROWING PREFERENCE FOR ROBOT-ASSISTED GENERAL SURGICAL PROCEDURES TO DRIVE MARKET

- 9.3 GYNECOLOGICAL SURGERY

- 9.3.1 RISING NUMBER OF HYSTERECTOMIES TO INCREASE DEMAND FOR SURGICAL ROBOTS

- 9.4 ORTHOPEDIC SURGERY

- 9.4.1 GROWING PREFERENCE FOR KNEE RECONSTRUCTION PROCEDURES TO SUPPORT MARKET GROWTH

- 9.5 UROLOGICAL SURGERY

- 9.5.1 RISING PREVALENCE OF UROLOGICAL DISEASES TO FUEL DEMAND FOR SURGICAL ROBOTS

- 9.6 NEUROSURGERY

- 9.6.1 INCREASING USE OF ROBOTIC TECHNOLOGIES IN NEUROSURGICAL PROCEDURES TO DRIVE MARKET

- 9.7 MICROSURGERY

- 9.7.1 RISING INTERSECTION OF MINIMALLY INVASIVE SURGERY AND SURGICAL ROBOTS TO SUPPORT MARKET GROWTH

- 9.8 OTOLOGICAL SURGERY

- 9.8.1 RISING PREVALENCE OF EAR-RELATED DISORDERS TO SPUR MARKET GROWTH

- 9.9 OTHER APPLICATIONS

10 SURGICAL ROBOTS MARKET, BY END USER

- 10.1 INTRODUCTION

- 10.2 HOSPITALS & CLINICS

- 10.2.1 INCREASING ROBOTIC-ASSISTED SURGERIES TO PROPEL MARKET GROWTH

- 10.3 AMBULATORY SURGERY CENTERS

- 10.3.1 GROWING PATIENT PREFERENCE FOR COST-EFFECTIVE TREATMENTS TO DRIVE MARKET GROWTH

11 SURGICAL ROBOTS MARKET, BY REGION

- 11.1 INTRODUCTION

- 11.2 NORTH AMERICA

- 11.2.1 US

- 11.2.1.1 US to dominate North American surgical robots market during study period

- 11.2.2 CANADA

- 11.2.2.1 Increased adoption of surgical robots for gynecological surgeries and cancerous tumor removal to drive market

- 11.2.1 US

- 11.3 EUROPE

- 11.3.1 GERMANY

- 11.3.1.1 Favorable healthcare initiatives and large pool of stroke patients to spur market growth

- 11.3.2 UK

- 11.3.2.1 Rising investments in surgical robots to propel market growth

- 11.3.3 FRANCE

- 11.3.3.1 Favorable investments and high demand for surgical robotic systems to boost market growth

- 11.3.4 SPAIN

- 11.3.4.1 Increasing number of robotic-assisted surgical procedures and initiatives to fuel growth

- 11.3.5 ITALY

- 11.3.5.1 Increasing number of robotic surgical procedures to propel market growth

- 11.3.6 REST OF EUROPE

- 11.3.1 GERMANY

- 11.4 ASIA PACIFIC

- 11.4.1 JAPAN

- 11.4.1.1 Favorable government initiatives to support adoption of surgical robots

- 11.4.2 CHINA

- 11.4.2.1 Favorable government initiatives to boost market growth

- 11.4.3 INDIA

- 11.4.3.1 Rapid developments in healthcare infrastructure to support market growth

- 11.4.4 AUSTRALIA

- 11.4.4.1 Increasing implementation and development of s urgical robotic training programs to fuel market growth

- 11.4.5 SOUTH KOREA

- 11.4.5.1 Increasing installation of surgical robots and growing government investments to ensure steady market growth

- 11.4.6 REST OF ASIA PACIFIC

- 11.4.1 JAPAN

- 11.5 LATIN AMERICA

- 11.5.1 BRAZIL

- 11.5.1.1 Rising incidence of target diseases and growing healthcare expenditure to drive market

- 11.5.2 MEXICO

- 11.5.2.1 Growing emphasis on surgical robotics in healthcare to support market growth

- 11.5.3 REST OF LATIN AMERICA

- 11.5.1 BRAZIL

- 11.6 MIDDLE EAST & AFRICA

- 11.6.1 GCC COUNTRIES

- 11.6.1.1 Robust healthcare industry and favorable government strategies to drive market

- 11.6.2 REST OF MIDDLE EAST & AFRICA

- 11.6.1 GCC COUNTRIES

12 COMPETITIVE LANDSCAPE

- 12.1 INTRODUCTION

- 12.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 12.2.1 OVERVIEW OF STRATEGIES ADOPTED BY PLAYERS IN SURGICAL ROBOTS MARKET

- 12.3 REVENUE ANALYSIS, 2020-2024

- 12.4 MARKET SHARE ANALYSIS, 2024

- 12.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 12.5.1 STARS

- 12.5.2 EMERGING LEADERS

- 12.5.3 PERVASIVE PLAYERS

- 12.5.4 PARTICIPANTS

- 12.5.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 12.5.5.1 Company footprint

- 12.5.5.2 Region footprint

- 12.5.5.3 Offering footprint

- 12.5.5.4 Application footprint

- 12.5.5.5 End-user footprint

- 12.6 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 12.6.1 PROGRESSIVE COMPANIES

- 12.6.2 DYNAMIC COMPANIES

- 12.6.3 STARTING BLOCKS

- 12.6.4 RESPONSIVE COMPANIES

- 12.6.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 12.6.5.1 Detailed list of key startups/SMEs

- 12.6.5.2 Competitive benchmarking of key startups/SMEs

- 12.7 COMPANY VALUATION & FINANCIAL METRICS

- 12.7.1 FINANCIAL METRICS

- 12.7.2 COMPANY VALUATION

- 12.8 BRAND/PRODUCT COMPARISON

- 12.9 COMPETITIVE SCENARIO

- 12.9.1 PRODUCT/SERVICE LAUNCHES AND APPROVALS

- 12.9.2 DEALS

- 12.9.3 EXPANSIONS

13 COMPANY PROFILES

- 13.1 KEY PLAYERS

- 13.1.1 INTUITIVE SURGICAL OPERATIONS, INC.

- 13.1.1.1 Business overview

- 13.1.1.2 Products/Services/Solutions offered

- 13.1.1.3 Recent developments

- 13.1.1.3.1 Product approvals

- 13.1.1.3.2 Deals

- 13.1.1.4 MnM view

- 13.1.1.4.1 Right to win

- 13.1.1.4.2 Strategic choices

- 13.1.1.4.3 Weaknesses & competitive threats

- 13.1.2 STRYKER

- 13.1.2.1 Business overview

- 13.1.2.2 Products/Services/Solutions offered

- 13.1.2.3 Recent developments

- 13.1.2.3.1 Product launches

- 13.1.2.3.2 Deals

- 13.1.2.3.3 Expansions

- 13.1.2.4 MnM view

- 13.1.2.4.1 Right to win

- 13.1.2.4.2 Strategic choices

- 13.1.2.4.3 Weaknesses & competitive threats

- 13.1.3 ZIMMER BIOMET

- 13.1.3.1 Business overview

- 13.1.3.2 Products/Services/Solutions offered

- 13.1.3.3 Recent developments

- 13.1.3.3.1 Product approvals

- 13.1.3.3.2 Deals

- 13.1.3.3.3 Other developments

- 13.1.3.4 MnM view

- 13.1.3.4.1 Right to win

- 13.1.3.4.2 Strategic choices

- 13.1.3.4.3 Weaknesses & competitive threats

- 13.1.4 MEDTRONIC

- 13.1.4.1 Business overview

- 13.1.4.2 Products/Services/Solutions offered

- 13.1.4.3 Recent developments

- 13.1.4.3.1 Product approvals

- 13.1.4.3.2 Deals

- 13.1.4.3.3 Expansions

- 13.1.4.4 MnM view

- 13.1.4.4.1 Right to win

- 13.1.4.4.2 Strategic choices

- 13.1.4.4.3 Weaknesses & competitive threats

- 13.1.5 SMITH+NEPHEW

- 13.1.5.1 Business overview

- 13.1.5.2 Products/Services/Solutions offered

- 13.1.5.3 Recent developments

- 13.1.5.3.1 Product & service launches and enhancements

- 13.1.5.4 MnM view

- 13.1.5.4.1 Right to win

- 13.1.5.4.2 Strategic choices

- 13.1.5.4.3 Weaknesses & competitive threats

- 13.1.6 ASENSUS SURGICAL US, INC.

- 13.1.6.1 Business overview

- 13.1.6.2 Products/Services/Solutions offered

- 13.1.6.3 Recent developments

- 13.1.6.3.1 Product approvals

- 13.1.6.3.2 Deals

- 13.1.7 SIEMENS HEALTHINEERS AG

- 13.1.7.1 Business overview

- 13.1.7.2 Products/Services/Solutions offered

- 13.1.7.3 Recent developments

- 13.1.7.3.1 Deals

- 13.1.8 RENISHAW PLC

- 13.1.8.1 Business overview

- 13.1.8.2 Products/Services/Solutions offered

- 13.1.8.3 Recent developments

- 13.1.8.3.1 Product approvals

- 13.1.9 GLOBUS MEDICAL

- 13.1.9.1 Business overview

- 13.1.9.2 Products/Services/Solutions offered

- 13.1.9.3 Recent developments

- 13.1.9.3.1 Product approvals

- 13.1.10 JOHNSON & JOHNSON

- 13.1.10.1 Business overview

- 13.1.10.2 Products/Services/Solutions offered

- 13.1.10.3 Recent developments

- 13.1.10.3.1 Product approvals

- 13.1.11 CMR SURGICAL LTD.

- 13.1.11.1 Business overview

- 13.1.11.2 Products/Services/Solutions offered

- 13.1.11.3 Recent developments

- 13.1.11.3.1 Product approvals

- 13.1.11.3.2 Deals

- 13.1.11.3.3 Expansions

- 13.1.11.3.4 Other developments

- 13.1.12 THINK SURGICAL, INC.

- 13.1.12.1 Business overview

- 13.1.12.2 Products/Services/Solutions offered

- 13.1.12.3 Recent developments

- 13.1.12.3.1 Product approvals

- 13.1.12.3.2 Deals

- 13.1.13 CORIN GROUP

- 13.1.13.1 Business overview

- 13.1.13.2 Products/Services/Solutions offered

- 13.1.13.3 Recent developments

- 13.1.13.3.1 Product launches & approvals

- 13.1.14 MICROSURE

- 13.1.14.1 Business overview

- 13.1.14.2 Products/Services/Solutions offered

- 13.1.14.3 Recent developments

- 13.1.14.3.1 Other developments

- 13.1.15 AVATERAMEDICAL GMBH

- 13.1.15.1 Business overview

- 13.1.15.2 Products/Services/Solutions offered

- 13.1.16 MEDICAL MICROINSTRUMENTS, INC.

- 13.1.16.1 Business overview

- 13.1.16.2 Products/Services/Solutions offered

- 13.1.16.3 Recent developments

- 13.1.16.3.1 Product approvals

- 13.1.16.3.2 Deals

- 13.1.16.3.3 Other developments

- 13.1.17 MEDICAROID CORPORATION

- 13.1.17.1 Business overview

- 13.1.17.2 Products/Services/Solutions offered

- 13.1.17.3 Recent developments

- 13.1.17.3.1 Product approvals

- 13.1.17.3.2 Deals

- 13.1.18 BRAINLAB SE

- 13.1.18.1 Business overview

- 13.1.18.2 Products/Services/Solutions offered

- 13.1.18.3 Recent developments

- 13.1.18.3.1 Product approvals

- 13.1.18.3.2 Deals

- 13.1.19 ECENTIAL ROBOTICS

- 13.1.19.1 Business overview

- 13.1.19.2 Products/Services/Solutions offered

- 13.1.19.3 Recent developments

- 13.1.19.3.1 Product approvals

- 13.1.19.3.2 Deals

- 13.1.20 SS INNOVATIONS INTERNATIONAL, INC.

- 13.1.20.1 Business overview

- 13.1.20.2 Products/Services/Solutions offered

- 13.1.20.3 Products/Services/Solutions in pipeline

- 13.1.20.4 Recent developments

- 13.1.20.4.1 Product launches and approvals

- 13.1.20.5 MnM view

- 13.1.20.5.1 Right to win

- 13.1.20.5.2 Strategic choices

- 13.1.20.5.3 Weaknesses & competitive threats

- 13.1.1 INTUITIVE SURGICAL OPERATIONS, INC.

- 13.2 OTHER PLAYERS

- 13.2.1 MONTERIS

- 13.2.2 MOMENTIS INNOVATIVE SURGERY

- 13.2.3 TINAVI MEDICAL TECHNOLOGIES CO., LTD.

- 13.2.4 DISTALMOTION SA

- 13.2.5 NOVUS SAGLIK URUNLERI AR-GE DANISMANLIK (NOVUS ARGE)

14 RESEARCH METHODOLOGY

- 14.1 RESEARCH DATA

- 14.1.1 SECONDARY DATA

- 14.1.1.1 Key sources of secondary data

- 14.1.1.2 Key data from secondary sources

- 14.1.2 PRIMARY DATA

- 14.1.2.1 Key objectives of primary research

- 14.1.2.2 Key data from primary sources

- 14.1.2.3 Key industry insights

- 14.1.1 SECONDARY DATA

- 14.2 MARKET SIZE ESTIMATION

- 14.2.1 BOTTOM-UP APPROACH

- 14.2.2 TOP-DOWN APPROACH

- 14.2.3 BASE NUMBER ESTIMATION

- 14.2.3.1 Supply-side analysis (revenue share analysis)

- 14.2.3.2 Company presentations and primary interviews

- 14.3 MARKET FORECAST APPROACH

- 14.4 DATA TRIANGULATION

- 14.5 STUDY ASSUMPTIONS

- 14.5.1 MARKET SHARE ASSUMPTIONS

- 14.5.2 RESEARCH ASSUMPTIONS

- 14.6 FACTOR ANALYSIS

- 14.7 RISK ANALYSIS

- 14.8 RESEARCH LIMITATIONS

15 APPENDIX

- 15.1 DISCUSSION GUIDE

- 15.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 15.3 CUSTOMIZATION OPTIONS

- 15.4 RELATED REPORTS

- 15.5 AUTHOR DETAILS

List of Tables

- TABLE 1 SURGICAL ROBOTS MARKET: INCLUSIONS & EXCLUSIONS

- TABLE 2 STANDARD CURRENCY CONVERSION RATES

- TABLE 3 SURGICAL ROBOTS MARKET: CURRENT UNMET NEEDS

- TABLE 4 SURGICAL ROBOTS MARKET: PORTER'S FIVE FORCES

- TABLE 5 GDP PERCENTAGE CHANGE, BY COUNTRY, 2021-2030

- TABLE 6 AVERAGE SELLING PRICE OF SURGICAL ROBOTIC APPLICATIONS, BY KEY PLAYER, 2024 (USD MILLION)

- TABLE 7 AVERAGE PRICING TREND OF SURGICAL ROBOTS, BY REGION, 2022-2024 (USD MILLION)

- TABLE 8 IMPORT DATA FOR HS CODE 901890, BY COUNTRY, 2020-2024 (USD THOUSAND)

- TABLE 9 EXPORT DATA FOR HS CODE 901890, BY COUNTRY, 2020-2024 (USD THOUSAND)

- TABLE 10 LIST OF KEY CONFERENCES AND EVENTS IN SURGICAL ROBOTS MARKET, JANUARY 2025-DECEMBER 2026

- TABLE 11 CASE STUDY 1: REVOLUTIONISING FUTURE OF SURGERY WITH HIGH-PRECISION ROBOTS

- TABLE 12 CASE STUDY 2: HUNJAN HOSPITAL DEPLOYS ORTHOPEDIC SURGICAL ROBOT FOR KNEE REPLACEMENT SURGERY

- TABLE 13 CASE STUDY 3: BIONAUT LABS CREATES REMOTE-CONTROLLED MICRO-ROBOTS TO TARGET BRAIN DISEASES

- TABLE 14 US ADJUSTED RECIPROCAL TARIFF RATES

- TABLE 15 KEY PRODUCT-RELATED TARIFF EFFECTIVE FOR SURGICAL ROBOTS

- TABLE 16 LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 17 US FDA: MEDICAL DEVICE CLASSIFICATION

- TABLE 18 US: MEDICAL DEVICE REGULATORY APPROVAL PROCESS

- TABLE 19 JAPAN: MEDICAL DEVICE CLASSIFICATION UNDER PMDA

- TABLE 20 CHINA: CLASSIFICATION OF MEDICAL DEVICES

- TABLE 21 GLOBAL STANDARDS IN SURGICAL ROBOTS MARKET

- TABLE 22 CERTIFICATIONS, LABELING, AND ECO-STANDARDS IN SURGICAL ROBOTS MARKET

- TABLE 23 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR KEY END USERS

- TABLE 24 KEY BUYING CRITERIA FOR KEY TWO END USERS

- TABLE 25 UNMET NEEDS FROM END-USE INDUSTRIES IN SURGICAL ROBOTS MARKET

- TABLE 26 SURGICAL ROBOTS MARKET, BY OFFERING, 2023-2030 (USD MILLION)

- TABLE 27 SURGICAL ROBOTS MARKET, BY REGION, 2023-2030 (MILLION UNITS)

- TABLE 28 SURGICAL ROBOT INSTRUMENTS & ACCESSORIES MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 29 SURGICAL ROBOTIC SYSTEMS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 30 SURGICAL ROBOTIC SYSTEMS MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 31 LAPAROSCOPIC ROBOTIC SYSTEMS MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 32 ORTHOPEDIC ROBOTIC SYSTEMS MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 33 NEUROSURGICAL ROBOTIC SYSTEMS MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 34 OTHER ROBOTIC SYSTEMS MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 35 SURGICAL ROBOT SERVICES MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 36 SURGICAL ROBOTS MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 37 SURGICAL ROBOTS MARKET FOR GENERAL SURGERY, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 38 SURGICAL ROBOTS MARKET FOR GYNECOLOGICAL SURGERY, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 39 SURGICAL ROBOTS MARKET FOR ORTHOPEDIC SURGERY, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 40 SURGICAL ROBOTS MARKET FOR UROLOGICAL SURGERY, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 41 SURGICAL ROBOTS MARKET FOR NEUROSURGERY, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 42 SURGICAL ROBOTS MARKET FOR MICROSURGERY, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 43 SURGICAL ROBOTS MARKET FOR OTOLOGICAL SURGERY, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 44 SURGICAL ROBOTS MARKET FOR OTHER APPLICATIONS, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 45 SURGICAL ROBOTS MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 46 SURGICAL ROBOTS MARKET FOR HOSPITALS & CLINICS, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 47 SURGICAL ROBOTS MARKET FOR AMBULATORY SURGERY CENTERS, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 48 SURGICAL ROBOTS MARKET, BY REGION, 2023-2030 (USD MILLION)

- TABLE 49 NORTH AMERICA: SURGICAL ROBOTS MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 50 NORTH AMERICA: SURGICAL ROBOTS MARKET, BY OFFERING, 2023-2030 (USD MILLION)

- TABLE 51 NORTH AMERICA: SURGICAL ROBOTIC SYSTEMS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 52 NORTH AMERICA: SURGICAL ROBOTS MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 53 NORTH AMERICA: SURGICAL ROBOTS MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 54 US: SURGICAL ROBOTS MARKET, BY OFFERING, 2023-2030 (USD MILLION)

- TABLE 55 US: SURGICAL ROBOTIC SYSTEMS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 56 US: SURGICAL ROBOTS MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 57 US: SURGICAL ROBOTS MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 58 CANADA: SURGICAL ROBOTS MARKET, BY OFFERING, 2023-2030 (USD MILLION)

- TABLE 59 CANADA: SURGICAL ROBOTIC SYSTEMS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 60 CANADA: SURGICAL ROBOTS MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 61 CANADA: SURGICAL ROBOTS MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 62 EUROPE: SURGICAL ROBOTS MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 63 EUROPE: SURGICAL ROBOTS MARKET, BY OFFERING, 2023-2030 (USD MILLION)

- TABLE 64 EUROPE: SURGICAL ROBOTIC SYSTEMS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 65 EUROPE: SURGICAL ROBOTS MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 66 EUROPE: SURGICAL ROBOTS MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 67 GERMANY: SURGICAL ROBOTS MARKET, BY OFFERING,

023-2030 (USD MILLION)

- TABLE 68 GERMANY: SURGICAL ROBOTIC SYSTEMS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 69 GERMANY: SURGICAL ROBOTS MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 70 GERMANY: SURGICAL ROBOTS MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 71 UK: SURGICAL ROBOTS MARKET, BY OFFERING, 2023-2030 (USD MILLION)

- TABLE 72 UK: SURGICAL ROBOTIC SYSTEMS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 73 UK: SURGICAL ROBOTS MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 74 UK: SURGICAL ROBOTS MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 75 FRANCE: SURGICAL ROBOTS MARKET, BY OFFERING, 2023-2030 (USD MILLION)

- TABLE 76 FRANCE: SURGICAL ROBOTIC SYSTEMS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 77 FRANCE: SURGICAL ROBOTS MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 78 FRANCE: SURGICAL ROBOTS MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 79 SPAIN: SURGICAL ROBOTS MARKET, BY OFFERING, 2023-2030 (USD MILLION)

- TABLE 80 SPAIN: SURGICAL ROBOTIC SYSTEMS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 81 SPAIN: SURGICAL ROBOTS MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 82 SPAIN: SURGICAL ROBOTS MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 83 ITALY: SURGICAL ROBOTS MARKET, BY OFFERING, 2023-2030 (USD MILLION)

- TABLE 84 ITALY: SURGICAL ROBOTIC SYSTEMS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 85 ITALY: SURGICAL ROBOTS MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 86 ITALY: SURGICAL ROBOTS MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 87 REST OF EUROPE: SURGICAL ROBOTS MARKET, BY OFFERING, 2023-2030 (USD MILLION)

- TABLE 88 REST OF EUROPE: SURGICAL ROBOTIC SYSTEMS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 89 REST OF EUROPE: SURGICAL ROBOTS MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 90 REST OF EUROPE: SURGICAL ROBOTS MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 91 ASIA PACIFIC: SURGICAL ROBOTS MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 92 ASIA PACIFIC: SURGICAL ROBOTS MARKET, BY OFFERING, 2023-2030 (USD MILLION)

- TABLE 93 ASIA PACIFIC: SURGICAL ROBOTIC SYSTEMS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 94 ASIA PACIFIC: SURGICAL ROBOTS MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 95 ASIA PACIFIC: SURGICAL ROBOTS MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 96 JAPAN: SURGICAL ROBOTS MARKET, BY OFFERING, 2023-2030 (USD MILLION)

- TABLE 97 JAPAN: SURGICAL ROBOTIC SYSTEMS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 98 JAPAN: SURGICAL ROBOTS MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 99 JAPAN: SURGICAL ROBOTS MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 100 CHINA: SURGICAL ROBOTS MARKET, BY OFFERING, 2023-2030 (USD MILLION)

- TABLE 101 CHINA: SURGICAL ROBOTIC SYSTEMS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 102 CHINA: SURGICAL ROBOTS MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 103 CHINA: SURGICAL ROBOTS MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 104 INDIA: SURGICAL ROBOTS MARKET, BY OFFERING, 2023-2030 (USD MILLION)

- TABLE 105 INDIA: SURGICAL ROBOTIC SYSTEMS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 106 INDIA: SURGICAL ROBOTS MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 107 INDIA: SURGICAL ROBOTS MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 108 AUSTRALIA: SURGICAL ROBOTS MARKET, BY OFFERING, 2023-2030 (USD MILLION)

- TABLE 109 AUSTRALIA: SURGICAL ROBOTIC SYSTEMS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 110 AUSTRALIA: SURGICAL ROBOTS MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 111 AUSTRALIA: SURGICAL ROBOTS MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 112 SOUTH KOREA: SURGICAL ROBOTS MARKET, BY OFFERING, 2023-2030 (USD MILLION)

- TABLE 113 SOUTH KOREA: SURGICAL ROBOTIC SYSTEMS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 114 SOUTH KOREA: SURGICAL ROBOTS MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 115 SOUTH KOREA: SURGICAL ROBOTS MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 116 REST OF ASIA PACIFIC: SURGICAL ROBOTS MARKET, BY OFFERING, 2023-2030 (USD MILLION)

- TABLE 117 REST OF ASIA PACIFIC: SURGICAL ROBOTIC SYSTEMS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 118 REST OF ASIA PACIFIC: SURGICAL ROBOTS MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 119 REST OF ASIA PACIFIC: SURGICAL ROBOTS MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 120 LATIN AMERICA: SURGICAL ROBOTS MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 121 LATIN AMERICA: SURGICAL ROBOTS MARKET, BY OFFERING, 2023-2030 (USD MILLION)

- TABLE 122 LATIN AMERICA: SURGICAL ROBOTIC SYSTEMS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 123 LATIN AMERICA: SURGICAL ROBOTS MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 124 LATIN AMERICA: SURGICAL ROBOTS MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 125 BRAZIL: SURGICAL ROBOTS MARKET, BY OFFERING, 2023-2030 (USD MILLION)

- TABLE 126 BRAZIL: SURGICAL ROBOTIC SYSTEMS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 127 BRAZIL: SURGICAL ROBOTS MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 128 BRAZIL: SURGICAL ROBOTS MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 129 MEXICO: SURGICAL ROBOTS MARKET, BY OFFERING, 2023-2030 (USD MILLION)

- TABLE 130 MEXICO: SURGICAL ROBOTIC SYSTEMS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 131 MEXICO: SURGICAL ROBOTS MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 132 MEXICO: SURGICAL ROBOTS MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 133 REST OF LATIN AMERICA: SURGICAL ROBOTS MARKET, BY OFFERING, 2023-2030 (USD MILLION)

- TABLE 134 REST OF LATIN AMERICA: SURGICAL ROBOTIC SYSTEMS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 135 REST OF LATIN AMERICA: SURGICAL ROBOTS MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 136 REST OF LATIN AMERICA: SURGICAL ROBOTS MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 137 MIDDLE EAST & AFRICA: SURGICAL ROBOTS MARKET, BY REGION, 2023-2030 (USD MILLION)

- TABLE 138 MIDDLE EAST & AFRICA: SURGICAL ROBOTS MARKET, BY OFFERING, 2023-2030 (USD MILLION)

- TABLE 139 MIDDLE EAST & AFRICA: SURGICAL ROBOTIC SYSTEMS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 140 MIDDLE EAST & AFRICA: SURGICAL ROBOTS MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 141 MIDDLE EAST & AFRICA: SURGICAL ROBOTS MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 142 GCC COUNTRIES: SURGICAL ROBOTS MARKET, BY OFFERING, 2023-2030 (USD MILLION)

- TABLE 143 GCC COUNTRIES: SURGICAL ROBOTIC SYSTEMS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 144 GCC COUNTRIES: SURGICAL ROBOTS MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 145 GCC COUNTRIES: SURGICAL ROBOTS MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 146 REST OF MIDDLE EAST & AFRICA: SURGICAL ROBOTS MARKET, BY OFFERING, 2023-2030 (USD MILLION)

- TABLE 147 REST OF MIDDLE EAST & AFRICA: SURGICAL ROBOTIC SYSTEMS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 148 REST OF MIDDLE EAST & AFRICA: SURGICAL ROBOTS MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 149 REST OF MIDDLE EAST & AFRICA: SURGICAL ROBOTS MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 150 KEY STRATEGIES DEPLOYED BY MAJOR PLAYERS IN SURGICAL ROBOTS MARKET, JANUARY 2021-DECEMBER 2025

- TABLE 151 SURGICAL ROBOTS MARKET: DEGREE OF COMPETITION

- TABLE 152 SURGICAL ROBOTS MARKET: REGION FOOTPRINT

- TABLE 153 SURGICAL ROBOTS MARKET: OFFERING FOOTPRINT

- TABLE 154 SURGICAL ROBOTS MARKET: APPLICATION FOOTPRINT

- TABLE 155 SURGICAL ROBOTS MARKET: END-USER FOOTPRINT

- TABLE 156 SURGICAL ROBOTS MARKET: DETAILED LIST OF KEY STARTUPS/SME PLAYERS

- TABLE 157 SURGICAL ROBOTS MARKET: COMPETITIVE BENCHMARKING OF KEY STARTUPS/SME PLAYERS, BY ROBOTIC SYSTEM TYPE AND REGION

- TABLE 158 SURGICAL ROBOTS MARKET: PRODUCT/SERVICE LAUNCHES AND APPROVALS, JANUARY 2021-DECEMBER 2025

- TABLE 159 SURGICAL ROBOTS MARKET: DEALS, JANUARY 2021-DECEMBER 2025

- TABLE 160 SURGICAL ROBOTS MARKET: EXPANSIONS, JANUARY 2021-DECEMBER 2025

- TABLE 161 INTUITIVE SURGICAL OPERATIONS, INC.: COMPANY OVERVIEW

- TABLE 162 INTUITIVE SURGICAL OPERATIONS, INC.: PRODUCTS/SERVICES/SOLUTIONS OFFERED

- TABLE 163 INTUITIVE SURGICALOPERATIONS, INC.: PRODUCT APPROVALS, JANUARY 2021-DECEMBER 2025

- TABLE 164 INTUITIVE SURGICAL OPERATIONS, INC.: DEALS, JANUARY 2021-DECEMBER 2025

- TABLE 165 STRYKER: COMPANY OVERVIEW

- TABLE 166 STRYKER: PRODUCTS/SERVICES/SOLUTIONS OFFERED

- TABLE 167 STRYKER: PRODUCT LAUNCHES, JANUARY 2021-DECEMBER 2025

- TABLE 168 STRYKER: DEALS, JANUARY 2021-DECEMBER 2025

- TABLE 169 STRYKER: EXPANSIONS, JANUARY 2021-DECEMBER 2025

- TABLE 170 ZIMMER BIOMET: COMPANY OVERVIEW

- TABLE 171 ZIMMER BIOMET: PRODUCTS/SERVICES/SOLUTIONS OFFERED

- TABLE 172 ZIMMER BIOMET: PRODUCT APPROVALS, JANUARY 2021-DECEMBER 2025

- TABLE 173 ZIMMER BIOMET: DEALS, JANUARY 2021-DECEMBER 2025

- TABLE 174 ZIMMER BIOMET: OTHER DEVELOPMENTS, JANUARY 2021-DECEMBER 2025

- TABLE 175 MEDTRONIC: COMPANY OVERVIEW

- TABLE 176 MEDTRONIC: PRODUCTS/SERVICES/SOLUTIONS OFFERED

- TABLE 177 MEDTRONIC: PRODUCT APPROVALS, JANUARY 2021-DECEMBER 2025

- TABLE 178 MEDTRONIC: DEALS, JANUARY 2021-DECEMBER 2025

- TABLE 179 MEDTRONIC: EXPANSIONS, JANUARY 2021-DECEMBER 2025

- TABLE 180 SMITH+NEPHEW: COMPANY OVERVIEW

- TABLE 181 SMITH+NEPHEW: PRODUCTS/SERVICES/SOLUTIONS OFFERED

- TABLE 182 SMITH+NEPHEW: PRODUCT & SERVICE LAUNCHES AND ENHANCEMENTS, JANUARY 2021-DECEMBER 2025

- TABLE 183 ASENSUS SURGICAL US, INC.: COMPANY OVERVIEW

- TABLE 184 ASENSUS SURGICAL US, INC.: PRODUCTS/SERVICES/SOLUTIONS OFFERED

- TABLE 185 ASENSUS SURGICAL US, INC.: PRODUCT APPROVALS, JANUARY 2021-DECEMBER 2025

- TABLE 186 ASENSUS SURGICAL US, INC.: DEALS, JANUARY 2021-DECEMBER 2025

- TABLE 187 SIEMENS HEALTHINEERS AG: COMPANY OVERVIEW

- TABLE 188 SIEMENS HEALTHINEERS AG: PRODUCTS/SERVICES/SOLUTIONS OFFERED

- TABLE 189 SIEMENS HEALTHINEERS AG: DEALS, JANUARY 2021-DECEMBER 2025

- TABLE 190 RENISHAW PLC: COMPANY OVERVIEW

- TABLE 191 RENISHAW PLC: PRODUCTS/SERVICES/SOLUTIONS OFFERED

- TABLE 192 RENISHAW PLC: PRODUCT APPROVALS, JANUARY 2021-DECEMBER 2025

- TABLE 193 GLOBUS MEDICAL: COMPANY OVERVIEW

- TABLE 194 GLOBUS MEDICAL: PRODUCTS/SERVICES/SOLUTIONS OFFERED

- TABLE 195 GLOBUS MEDICAL: PRODUCT APPROVALS, JANUARY 2021-DECEMBER 2025

- TABLE 196 JOHNSON & JOHNSON: COMPANY OVERVIEW

- TABLE 197 JOHNSON & JOHNSON: PRODUCTS/SERVICES/SOLUTIONS OFFERED

- TABLE 198 JOHNSON & JOHNSON: PRODUCT APPROVALS, JANUARY 2021-DECEMBER 2025

- TABLE 199 CMR SURGICAL LTD.: COMPANY OVERVIEW

- TABLE 200 CMR SURGICAL LTD.: PRODUCTS/SERVICES/SOLUTIONS OFFERED

- TABLE 201 CMR SURGICAL LTD.: PRODUCT APPROVALS, JANUARY 2021-DECEMBER 2025

- TABLE 202 CMR SURGICAL LTD.: DEALS, JANUARY 2021-DECEMBER 2025

- TABLE 203 CMR SURGICAL LTD.: EXPANSIONS, JANUARY 2021-DECEMBER 2025

- TABLE 204 CMR SURGICAL LTD.: OTHER DEVELOPMENTS, JANUARY 2021-DECEMBER 2025

- TABLE 205 THINK SURGICAL, INC.: COMPANY OVERVIEW

- TABLE 206 THINK SURGICAL, INC.: PRODUCTS/SERVICES/SOLUTIONS OFFERED

- TABLE 207 THINK SURGICAL, INC.: PRODUCT APPROVALS, JANUARY 2021-DECEMBER 2025

- TABLE 208 THINK SURGICAL, INC.: DEALS, JANUARY 2021-DECEMBER 2025

- TABLE 209 CORIN GROUP: COMPANY OVERVIEW

- TABLE 210 CORIN GROUP: PRODUCTS/SERVICES/SOLUTIONS OFFERED

- TABLE 211 CORIN GROUP: PRODUCT LAUNCHES & APPROVALS, JANUARY 2021-DECEMBER 2025

- TABLE 212 MICROSURE: COMPANY OVERVIEW

- TABLE 213 MICROSURE: PRODUCTS/SERVICES/SOLUTIONS OFFERED

- TABLE 214 MICROSURE: OTHER DEVELOPMENTS, JANUARY 2021-DECEMBER 2025

- TABLE 215 AVATERAMEDICAL GMBH: COMPANY OVERVIEW

- TABLE 216 AVATERAMEDICAL GMBH: PRODUCTS/SERVICES/SOLUTIONS OFFERED

- TABLE 217 MEDICAL MICROINSTRUMENTS, INC.: COMPANY OVERVIEW

- TABLE 218 MEDICAL MICROINSTRUMENTS, INC.: PRODUCTS/SERVICES/SOLUTIONS OFFERED

- TABLE 219 MEDICAL MICROINSTRUMENTS, INC.: PRODUCT APPROVALS, JANUARY 2021-DECEMBER 2025

- TABLE 220 MEDICAL MICROINSTRUMENTS, INC.: DEALS, JANUARY 2021-DECEMBER 2025

- TABLE 221 MEDICAL MICROINSTRUMENTS, INC.: OTHER DEVELOPMENTS, JANUARY 2021-DECEMBER 2025

- TABLE 222 MEDICAROID CORPORATION: COMPANY OVERVIEW

- TABLE 223 MEDICAROID CORPORATION: PRODUCTS/SERVICES/SOLUTIONS OFFERED

- TABLE 224 MEDICAROID CORPORATION: PRODUCT APPROVALS, JANUARY 2021-DECEMBER 2025

- TABLE 225 MEDICAROID CORPORATION: DEALS, JANUARY 2021-DECEMBER 2025

- TABLE 226 BRAINLAB SE: COMPANY OVERVIEW

- TABLE 227 BRAINLAB SE: PRODUCTS/SERVICES/SOLUTIONS OFFERED

- TABLE 228 BRAINLAB SE: PRODUCT APPROVALS, JANUARY 2021-DECEMBER 2025

- TABLE 229 BRAINLAB SE: DEALS, JANUARY 2021-DECEMBER 2025

- TABLE 230 ECENTIAL ROBOTICS: COMPANY OVERVIEW

- TABLE 231 ECENTIAL ROBOTICS: PRODUCTS/SERVICES/SOLUTIONS OFFERED

- TABLE 232 ECENTIAL ROBOTICS: PRODUCT APPROVALS, JANUARY 2021-DECEMBER 2025

- TABLE 233 ECENTIAL ROBOTICS: DEALS, JANUARY 2021-DECEMBER 2025

- TABLE 234 SS INNOVATIONS INTERNATIONAL, INC.: COMPANY OVERVIEW

- TABLE 235 SS INNOVATIONS INTERNATIONAL, INC.: PRODUCTS/SERVICES/SOLUTIONS OFFERED

- TABLE 236 SS INNOVATIONS INTERNATIONAL, INC.: PRODUCTS/SERVICES/SOLUTIONS IN PIPELINE

- TABLE 237 SS INNOVATIONS INTERNATIONAL, INC.: PRODUCT LAUNCHES AND APPROVALS, JANUARY 2022-DECEMBER 2025

- TABLE 238 MONTERIS: COMPANY OVERVIEW

- TABLE 239 MOMENTIS INNOVATIVE SURGERY: COMPANY OVERVIEW

- TABLE 240 TINAVI MEDICAL TECHNOLOGIES CO., LTD.: COMPANY OVERVIEW

- TABLE 241 DISTALMOTION SA: COMPANY OVERVIEW

- TABLE 242 NOVUS SAGLIK URUNLERI AR-GE DANISMANLIK (NOVUS ARGE): COMPANY OVERVIEW

- TABLE 243 SURGICAL ROBOTS MARKET: RESEARCH ASSUMPTIONS

- TABLE 244 SURGICAL ROBOTS MARKET: RISK ANALYSIS

List of Figures

- FIGURE 1 SURGICAL ROBOTS MARKET SEGMENTATION & REGIONAL SCOPE

- FIGURE 2 SURGICAL ROBOTS MARKET: YEARS CONSIDERED

- FIGURE 3 KEY INSIGHTS & MARKET HIGHLIGHTS

- FIGURE 4 SURGICAL ROBOTS MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- FIGURE 5 MAJOR STRATEGIES ADOPTED BY KEY PLAYERS IN SURGICAL ROBOTS MARKET

- FIGURE 6 DISRUPTIVE TRENDS IMPACTING GROWTH OF SURGICAL ROBOTS MARKET

- FIGURE 7 HIGH-GROWTH SEGMENTS & EMERGING FRONTIERS IN SURGICAL ROBOTS MARKET (2024)

- FIGURE 8 ASIA PACIFIC TO REGISTER HIGHEST GROWTH DURING FORECAST PERIOD

- FIGURE 9 SURGICAL ROBOTS MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

- FIGURE 10 SURGICAL ROBOTS MARKET: PORTER'S FIVE FORCES ANALYSIS

- FIGURE 11 SURGICAL ROBOTS MARKET: SUPPLY CHAIN ANALYSIS

- FIGURE 12 SURGICAL ROBOTS MARKET: VALUE CHAIN ANALYSIS

- FIGURE 13 SURGICAL ROBOTS MARKET: ECOSYSTEM ANALYSIS

- FIGURE 14 TRENDS/DISRUPTIONS IMPACTING CUSTOMER'S BUSINESS IN SURGICAL ROBOTS MARKET

- FIGURE 15 INVESTMENT/VENTURE CAPITAL SCENARIO IN SURGICAL ROBOTS MARKET, 2020-2023 (USD BILLION)

- FIGURE 16 TOP PATENT APPLICANTS/OWNERS (COMPANIES/INSTITUTES) FOR SURGICAL ROBOTS MARKET (JANUARY 2015-OCTOBER 2025)

- FIGURE 17 TOP PATENT APPLICANT COUNTRIES FOR SURGICAL ROBOTS (JANUARY 2014-DECEMBER 2024)

- FIGURE 18 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR KEY END USERS

- FIGURE 19 KEY BUYING CRITERIA FOR TOP TWO END USERS

- FIGURE 20 SURGICAL ROBOTS MARKET: GEOGRAPHIC SNAPSHOT

- FIGURE 21 NORTH AMERICA: SURGICAL ROBOTS MARKET SNAPSHOT

- FIGURE 22 ASIA PACIFIC: SURGICAL ROBOTS MARKET SNAPSHOT

- FIGURE 23 REVENUE SHARE ANALYSIS OF KEY PLAYERS IN SURGICAL ROBOTS MARKET (2020-2024)

- FIGURE 24 MARKET SHARE ANALYSIS OF KEY PLAYERS IN SURGICAL ROBOTS MARKET (2024)

- FIGURE 25 SURGICAL ROBOTS MARKET: COMPANY EVALUATION MATRIX (KEY PLAYERS), 2024

- FIGURE 26 SURGICAL ROBOTS MARKET: COMPANY FOOTPRINT

- FIGURE 27 SURGICAL ROBOTS MARKET: COMPANY EVALUATION MATRIX (STARTUPS/SMES), 2024

- FIGURE 28 EV/EBITDA OF KEY VENDORS

- FIGURE 29 YEAR-TO-DATE (YTD) PRICE TOTAL RETURN AND 5-YEAR STOCK BETA OF KEY VENDORS

- FIGURE 30 SURGICAL ROBOTS MARKET: BRAND/PRODUCT COMPARATIVE ANALYSIS

- FIGURE 31 INTUITIVE SURGICAL OPERATIONS, INC.: COMPANY SNAPSHOT

- FIGURE 32 STRYKER: COMPANY SNAPSHOT

- FIGURE 33 ZIMMER BIOMET: COMPANY SNAPSHOT

- FIGURE 34 MEDTRONIC: COMPANY SNAPSHOT

- FIGURE 35 SMITH+NEPHEW: COMPANY SNAPSHOT

- FIGURE 36 SIEMENS HEALTHINEERS AG: COMPANY SNAPSHOT

- FIGURE 37 RENISHAW PLC: COMPANY SNAPSHOT

- FIGURE 38 GLOBUS MEDICAL: COMPANY SNAPSHOT

- FIGURE 39 JOHNSON & JOHNSON: COMPANY SNAPSHOT

- FIGURE 40 SS INNOVATIONS INTERNATIONAL, INC.: COMPANY SNAPSHOT

- FIGURE 41 SURGICAL ROBOTS MARKET: RESEARCH DESIGN

- FIGURE 42 SURGICAL ROBOTS MARKET: KEY DATA FROM SECONDARY SOURCES

- FIGURE 43 SURGICAL ROBOTS MARKET: KEY PRIMARY SOURCES (BY COMPANY TYPE, DESIGNATION, AND REGION)

- FIGURE 44 SURGICAL ROBOTS MARKET: KEY DATA FROM PRIMARY SOURCES

- FIGURE 45 SURGICAL ROBOTS MARKET: KEY INDUSTRY INSIGHTS

- FIGURE 46 SURGICAL ROBOTS MARKET: BOTTOM-UP APPROACH

- FIGURE 47 SURGICAL ROBOTS MARKET: TOP-DOWN APPROACH

- FIGURE 48 SUPPLY-SIDE SURGICAL ROBOTS MARKET SIZE ESTIMATION: REVENUE SHARE ANALYSIS

- FIGURE 49 SURGICAL ROBOTS MARKET: REVENUE SHARE ANALYSIS ILLUSTRATION FOR STRYKER

- FIGURE 50 SUPPLY-SIDE SURGICAL ROBOTS MARKET ESTIMATION (2024)

- FIGURE 51 SURGICAL ROBOTS MARKET: CAGR PROJECTIONS (SUPPLY-SIDE ANALYSIS)

- FIGURE 52 SURGICAL ROBOTS MARKET: DATA TRIANGULATION METHODOLOGY

- FIGURE 53 SURGICAL ROBOTS MARKET: FACTOR ANALYSIS

2026年下一代手术机器人全球市场报告2026年全球单孔手术平台市场报告2026年全球復健用外骨骼步行器市场报告2026年全球机器人眼科手术市场报告2026年全球自主手术机器人市场报告

2026年下一代手术机器人全球市场报告2026年全球单孔手术平台市场报告2026年全球復健用外骨骼步行器市场报告2026年全球机器人眼科手术市场报告2026年全球自主手术机器人市场报告 手术机器人市场-全球产业规模、份额、趋势、机会和预测:按组件、控制机制、应用、最终用户、地区和竞争格局划分,2021-2031年

手术机器人市场-全球产业规模、份额、趋势、机会和预测:按组件、控制机制、应用、最终用户、地区和竞争格局划分,2021-2031年 多臂腹腔镜手术机器人市场按组件、连接埠类型、应用和最终用户划分 - 全球预测 2026-2032手术机器人市场按组件、应用和最终用户划分 - 全球预测 2026-2032 年

多臂腹腔镜手术机器人市场按组件、连接埠类型、应用和最终用户划分 - 全球预测 2026-2032手术机器人市场按组件、应用和最终用户划分 - 全球预测 2026-2032 年 手术机器人市场-2026-2031年预测

手术机器人市场-2026-2031年预测 日本手术机器人市场报告:按产品、应用、最终用户和地区划分(2026-2034年)

日本手术机器人市场报告:按产品、应用、最终用户和地区划分(2026-2034年)