|

市场调查报告书

商品编码

1787258

全球腰果壳油市场(依应用、产品类型、萃取製程、等级及地区)预测至2030年Cashew Nutshell Liquid Market by Product, Application, Region - Global Forecast to 2030 |

||||||

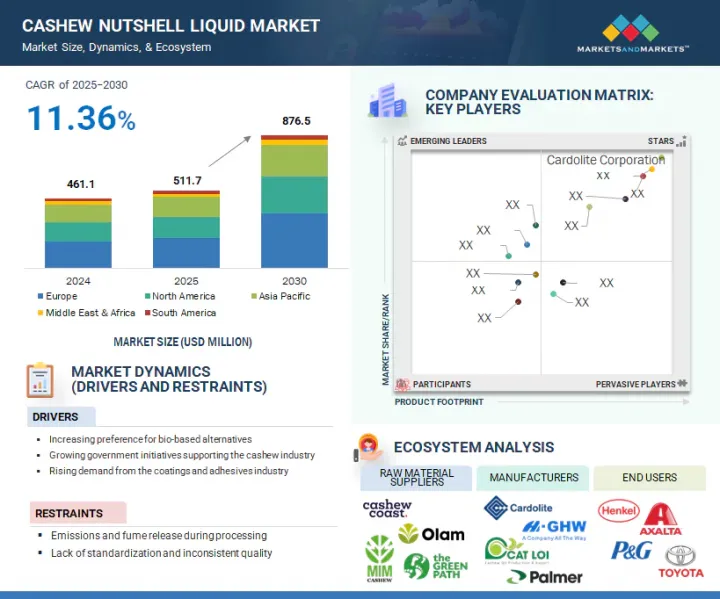

预计2025年至2030年腰果壳液市场将以11.36%的速度成长,2030年全球腰果壳液市场规模将达到8.765亿美元。

| 调查范围 | |

|---|---|

| 调查年份 | 2020-2030 |

| 基准年 | 2024 |

| 预测期 | 2025-2030 |

| 目标单位 | 金额(百万美元)和数量(千吨) |

| 部分 | 按应用、产品类型、提取工艺、等级和地区 |

| 目标区域 | 亚太地区、欧洲、北美、中东和非洲、南美 |

腰果壳油在黏合剂、涂料、泡沫、隔热材料、界面活性剂和层压材料等应用领域需求旺盛,其中被覆剂将占据最大份额,到2024年将达到1.3亿美元,其次是黏合剂,将达到1.13亿美元。腰果壳油(CNSL)环保、可再生,具有较高的热稳定性和化学稳定性,并且与多种聚合物和树脂相容——这些是腰果壳油基被覆剂和黏合剂的关键特性,这些特性将决定其市场需求。

腰果壳油中的酚类化合物可提高黏合强度和耐久性,使其成为汽车、建筑和电子行业的理想选择。此外,环境问题和日益增长的石油基化学品监管压力,促使製造商更偏好腰果壳油等生物基产品。永续且经济高效的材料在工业和消费产品配方中也越来越受欢迎,进一步促进了市场成长。

按产品类型划分,酚甲醛 (PF) 树脂将在 2024 年占据腰果壳油 (CNSL) 市场的最大份额,价值 7,630 万美元;紧随其后的是环氧改质剂和树脂及固化剂,价值分别为 7,620 万美元和 7,590 万美元。腰果壳油 (CNSL) 的反应性酚醛结构可用于多种产品类型,使其成为树脂和塑胶配方中强大且灵活的化学中间体。

从电子到汽车再到建筑等製造业,对高性能、耐热和永续材料的需求日益增长,这加速了基于腰果壳油(CNSL)的PF和环氧树脂的使用。尤其是腰果壳油(CNSL)固化剂,由于其低毒性和生物分解性,作为传统胺基体系的安全替代品,正日益受到欢迎。对多元醇和NCO封闭剂以及摩擦材料的需求也在增长,这些材料在煞车片、离合器和聚氨酯泡棉中发挥关键作用。随着人们对使用生物基原料生产高性能产品的兴趣日益浓厚,腰果壳油(CNSL)产品为现有原料提供了完美的绿色替代品,并满足了全球对永续性的需求。

欧洲市场是最重要的区域性腰果壳油市场,这主要得益于严格的环境政策、成熟的生产设施以及对生物基化学品的积极追求。该地区对腰果壳油的需求持续稳定,尤其是在汽车、建筑和电子行业中,对被覆剂、黏合剂、环氧系统和摩擦材料等应用的需求尤其突出。欧盟的绿色新政和循环经济倡议正在用腰果壳油等可再生资源取代对石油基原料的依赖。

在德国、法国和荷兰,製造商正在利用腰果壳油(CNSL)中的可再生酚类成分,生产不含甲醛且挥发性有机化合物 (VOC) 含量低的环保树脂、涂料和隔热材料。此外,腰果壳油在汽车摩擦材料(煞车皮、离合器片等)的应用,也与欧洲的汽车创新趋势和二氧化碳排放政策相符。

本报告研究了全球腰果壳液市场,并总结了应用、产品类型、提取流程、等级和地区的趋势,以及参与市场的公司概况。

目录

第一章 引言

第二章调查方法

第三章执行摘要

第四章重要考察

第五章市场概述

- 介绍

- 市场动态

- 波特五力分析

- 主要相关人员和采购标准

- 总体经济指标

第六章 产业趋势

- 供应链分析

- 定价分析

- 影响客户业务的趋势/中断

- 生态系分析

- 技术分析

- 案例研究分析

- 贸易分析

- 监管状况

- 2025-2026年主要会议和活动

- 投资金筹措场景

- 专利分析

- 2025年美国关税的影响—概述

- 人工智慧/生成式人工智慧对腰果壳油市场的影响

第七章 腰果壳油(CNSL)市场(依应用)

- 介绍

- 胶水

- 被覆剂

- 发泡材和隔热材料

- 层压板

- 摩擦衬片

- 个人护理

- 燃料

- 其他的

第 8 章 腰果壳油(CNSL)市场(依产品类型)

- 介绍

- 酚醛树脂(PF)

- 环氧改质剂和树脂

- 环氧固化剂

- 界面活性剂

- 多元醇和NCO阻断剂

- 摩擦材料

- 其他的

9. 腰果壳油(CNSL)市场(依萃取製程)

- 介绍

- 机械萃取工艺

- 溶剂萃取工艺

- 化学萃取工艺

第 10 章 腰果壳油(CNSL)市场(依等级)

- 介绍

- 主要特点

第 11 章 腰果壳油 (CNSL) 市场(按地区)

- 介绍

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 印尼

- 越南

- 北美洲

- 美国

- 墨西哥

- 加拿大

- 欧洲

- 德国

- 法国

- 英国

- 义大利

- 荷兰

- 南美洲

- 巴西

- 中东和非洲

- 海湾合作委员会国家

- 南非

第十二章竞争格局

- 介绍

- 主要参与企业的策略/优势

- 2024年市场占有率分析

- 2020年至2024年五大公司收益分析

- 公司估值矩阵:2024 年关键参与企业

- 公司估值矩阵:Start-Ups/中小企业,2024 年

- 品牌/产品比较分析

- 估值和财务指标

- 竞争场景

第十三章:公司简介

- 主要参与企业

- CARDOLITE CORPORATION

- GHW(VIETNAM)CO., LTD

- PALMER INTERNATIONAL

- LC BUFFALO CO. LTD.

- CAT LOI CASHEW OIL PRODUCTION & EXPORT JOINT STOCK COMPANY(CAT LOI)

- ZHEJIANG WANSHENG CO., LTD.

- CASHEW CHEM INDIA

- SRI DEVI GROUP

- ADMARK POLYCOATS PVT. LTD.

- GOLDEN CASHEW PRODUCTS PVT. LTD.

- 其他公司

- PALADIN PAINTS & CHEMICALS PVT. LTD

- SATYA CASHEW CHEMICALS PRIVATE LIMITED

- K2P CHEMICALS

- ZANTYE AGRO INDUSTRIES

- SON CHAU CO.,LTD

- SHIVAM CASHEW INDUSTRY

- HUNG LOC PHAT CASHEW OIL CO. LTD.

- KUMARASAMY INDUSTRIES

- MIRAE GREEN CHEMICAL CO., LTD.

- VIKO BIOFUEL COMPANY LIMITED

- THINH DAI CHEMICAL

- PT COMEXTRA MAJORA

- CUONG THINH CASHEW OIL PRODUCTION COMPANY LIMITED

- CNSL INDUSTRIAL CO., LTD.

- TAN LOC CASHEW OIL PRODUCTION COMPANY LIMITED

第14章:相邻市场与相关市场

- 介绍

- 限制

- 耐腐蚀树脂市场

- 耐腐蚀树脂市场(按地区)

第十五章 附录

The CNSL market is expected to grow at a rate of 11.36% between 2025 and 2030, projected to be USD 876.5 million globally by 2030.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2020-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD Million) and Volume (Kiloton) |

| Segments | Product Type, Application, and Region |

| Regions covered | Asia Pacific, Europe, North America, Middle East & Africa, and South America |

It is gaining high demand in the following applications, i.e., adhesives, coatings, foams, insulation, surfactants, and laminates. Of these, coatings had the highest share of USD 130.0 million in 2024 and that of the adhesives was USD 113.0 million. Its eco-friendly, renewable character, high thermal and chemical stability, compatibility with numerous polymers and resins are the main qualities of CNSL-based coatings and adhesives which predetermine their demand in the market.

The phenolic compounds present in CNSL enhance the outcomes of better bonding strength and durability, which makes it ideal in the automotive, construction, and electronics sectors. Besides, environmental issues and increased regulatory pressure of petroleum-based chemicals have started changing preferences among manufacturers to bio-based products like CNSL. The growth is also devoid of the fact that sustainable and cost-effective materials are gaining positive affinities in the industrial and consumer product formulations.

"Phenol formaldehyde resins and epoxy systems were leading product types in the CNSL market, 2024"

Phenol Formaldehyde (PF) resins have the largest share of CNSL market by product type valued at USD 76.3 million in 2024 and are closely followed by epoxy modifiers & resins and curing agents with a value of USD 76.2 million and USD 75.9 million, respectively. There are such product types which can take advantage of CNSL reactive phenolic structure, so that it could be used as a strong and flexible chemical intermediating in resin and plastic compounding.

The escalating need for high performance, heat-resistant and sustainable materials in the manufacturing industries starting with electronics to automotive industries then to construction industries is boosting the use of the CNSL-derived PF and epoxy systems. Specifically, CNSL-based curing agents are picking up popularity as they have the advantage of low toxicity and biodegradability, and thus, they can substitute the traditional amine-based systems offering a safer option. Also, polyols & NCO blocking agents and friction materials are experiencing high demand because they are important in brake linings, clutches, and polyurethane foams. With the growing interest of industries in the use of bio-based feedstocks as raw materials in making high-performance products, CNSL-based products come as perfect green alternatives to existing raw materials which meet the demands of sustainability that the world is gearing toward.

"Europe dominated the global CNSL market in 2024, driven by sustainable regulations and industrial innovation"

The European market is the most significant regional CNSL market. This is principally because of its strict policies on environment, the already developed manufacturing facilities and its active pursuit of bio-based chemicals. Consistency has been witnessed in the demand for the region in applications, such as coatings, adhesives, epoxy systems, and friction materials, especially in automotive, construction, and electronic industries. Green Deal and circular economy indicators in the EU with reliance on petroleum-based raw materials have been replaced by renewable sources such as CNSL.

In Germany, France, and the Netherlands, manufacturers are also taking advantage of the renewability of the phenolic content in CNSL to compile resins, coatings, and insulation materials that are free of formaldehyde and low in volatile organic compounds (VOCs), as well as environmentally harmless. In addition to this, the use of CNSL in automotive friction materials (such as brake pads, clutch plates) also suits well the trend of automotive innovations in Europe and its policy toward carbon emission reductions.

In-depth interviews have been conducted with chief executive officers (CEOs), Directors, and other executives from various key organizations operating in the CNSL marketplace.

- By Company Type: Tier 1 - 55%, Tier 2 - 25%, and Tier 3 - 20%

- By Designation: Directors - 50%, Managers - 30%, and Others - 20%

- By Region: North America - 40%, Europe - 35%, Asia Pacific - 20%, Rest of the World - 5%

The key players profiled in the report include Cardolite Corporation (US), GHW (Vietnam) Co. Ltd., Palmer International (US), LC Buffalo Co.Ltd. (Vietnam), Cat Loi Cashew Oil Production & Export Joint Stock Company (Vietnam), Senese (Poland), Zhejiang Wansheng Co., Ltd. (China), Cashew Chem India (India), Sri Devi Group (India), and ADMARK Polycoats Pvt. Ltd. (India).

Research Coverage

This report segments the market for CNSL based on product type, application, and region and provides estimations of value (USD Million) for the overall market size across various regions. A detailed analysis of key industry players has been conducted to provide insights into their business overviews, services, and key strategies, associated with the market for CNSL.

Reasons to Buy this Report

This research report is focused on various levels of analyses - industry analysis (industry trends), market share analysis of top players, and company profiles, which together provide an overall view of the competitive landscape, emerging and high-growth segments of the CNSL market; high-growth regions; and market drivers, restraints, and opportunities.

The report provides insights into the following points:

- Market Penetration: Comprehensive information on CNSL offered by top players in the global market.

- Analysis of key drivers: (Increasing preference for bio-based alternatives, growing government initiatives supporting the cashew industry) restraints (Emissions and fume release during processing, lack of standardization and inconsistent quality) opportunities (CNSL biofuel blends for marine fuel) and challenges (availability of substitutes) influencing the growth of CNSL market.

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product & service launches in the CNSL market.

- Market Development: Comprehensive information about lucrative emerging markets - the report analyzes the markets for CNSL across regions.

- Market Diversification: Exhaustive information about new products, untapped regions, and recent developments in the global CNSL market.

- Competitive Assessment: In-depth assessment of market shares, strategies, products, and manufacturing capabilities of leading players in the CNSL market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 MARKET DEFINITION AND INCLUSIONS, BY PRODUCT TYPE

- 1.3.4 MARKET DEFINITION AND INCLUSIONS, BY APPLICATION

- 1.3.5 YEARS CONSIDERED

- 1.3.6 CURRENCY CONSIDERED

- 1.3.7 UNITS CONSIDERED

- 1.4 STAKEHOLDERS

- 1.5 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY DATA

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Key primary participants

- 2.1.2.2 Key industry insights

- 2.1.2.3 Breakdown of interviews with experts

- 2.2 MARKET SIZE ESTIMATION

- 2.2.1 BOTTOM-UP APPROACH

- 2.2.2 TOP-DOWN APPROACH

- 2.3 DATA TRIANGULATION

- 2.4 GROWTH FORECAST

- 2.4.1 SUPPLY-SIDE ANALYSIS

- 2.4.2 DEMAND-SIDE ANALYSIS

- 2.5 ASSUMPTIONS

- 2.6 LIMITATIONS

- 2.7 RISK ASSESSMENT

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN CNSL MARKET

- 4.2 CNSL MARKET, BY REGION

- 4.3 ASIA PACIFIC: CNSL MARKET, BY APPLICATION AND COUNTRY

- 4.4 CNSL MARKET, BY APPLICATION AND REGION

- 4.5 CNSL MARKET, BY KEY COUNTRIES

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Increasing preference for bio-based alternatives

- 5.2.1.2 Growing government initiatives supporting cashew industry

- 5.2.1.3 Rising demand from coatings and adhesives industries

- 5.2.2 RESTRAINTS

- 5.2.2.1 Emissions and fume release during processing

- 5.2.2.2 Lack of standardization and inconsistent quality

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 CNSL biofuel blends for marine fuel

- 5.2.3.2 R&D in CNSL applications accelerating commercial adoption

- 5.2.4 CHALLENGES

- 5.2.4.1 Availability of substitutes

- 5.2.1 DRIVERS

- 5.3 PORTER'S FIVE FORCES ANALYSIS

- 5.3.1 INTENSITY OF COMPETITIVE RIVALRY

- 5.3.2 BARGAINING POWER OF BUYERS

- 5.3.3 BARGAINING POWER OF SUPPLIERS

- 5.3.4 THREAT OF SUBSTITUTES

- 5.3.5 THREAT OF NEW ENTRANTS

- 5.4 KEY STAKEHOLDERS AND BUYING CRITERIA

- 5.4.1 BUYING CRITERIA

- 5.5 MACROECONOMIC INDICATORS

- 5.5.1 GDP TRENDS AND FORECAST FOR MAJOR ECONOMIES, 2021-2030

6 INDUSTRY TRENDS

- 6.1 SUPPLY CHAIN ANALYSIS

- 6.1.1 RAW MATERIAL SUPPLIERS

- 6.1.2 MANUFACTURERS

- 6.1.3 DISTRIBUTION NETWORKS

- 6.1.4 END-USE INDUSTRIES

- 6.2 PRICING ANALYSIS

- 6.2.1 AVERAGE SELLING PRICE OF CNSL OFFERED BY KEY PLAYERS, BY APPLICATION, 2024

- 6.2.2 AVERAGE SELLING PRICE TREND OF CNSL, BY REGION, 2022-2030

- 6.3 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 6.4 ECOSYSTEM ANALYSIS

- 6.5 TECHNOLOGY ANALYSIS

- 6.5.1 KEY TECHNOLOGIES

- 6.5.1.1 Cardanol-derived epoxy compounds and modifiers

- 6.5.1.2 CNSL-based polyols for polyurethane systems

- 6.5.1.3 Integrated extraction, refinement, and blending technology for CNSL-based marine fuels

- 6.5.2 COMPLEMENTARY TECHNOLOGIES

- 6.5.2.1 Bio-based epoxy resins from glycerol and sugar derivatives

- 6.5.2.2 Advanced extraction and catalytic processing

- 6.5.1 KEY TECHNOLOGIES

- 6.6 CASE STUDY ANALYSIS

- 6.6.1 CNSL BIOFUEL'S ROLE IN DECARBONIZING MARINE TRANSPORT

- 6.6.2 REPLACING VOC-HEAVY EPOXIES WITH CNSL-BASED PHENALKAMINES

- 6.7 TRADE ANALYSIS

- 6.7.1 IMPORT SCENARIO (HS CODE 1302)

- 6.7.2 EXPORT SCENARIO (HS CODE 1302)

- 6.8 REGULATORY LANDSCAPE

- 6.8.1 GLOBAL: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 6.8.2 REGULATORY FRAMEWORK

- 6.8.2.1 REACH Regulation (European Union)

- 6.8.2.2 Circular Economy Action Plan (European Union)

- 6.8.2.3 Clean Air Act (US)

- 6.8.2.4 TSCA (Toxic Substances Control Act) (US)

- 6.8.2.5 ISO 9001 and ISO 14001 Standards (Global)

- 6.9 KEY CONFERENCES AND EVENTS, 2025-2026

- 6.10 INVESTMENT AND FUNDING SCENARIO

- 6.11 PATENT ANALYSIS

- 6.11.1 APPROACH

- 6.11.2 DOCUMENT TYPES

- 6.11.3 TOP APPLICANTS

- 6.11.4 JURISDICTION ANALYSIS

- 6.12 IMPACT OF 2025 US TARIFF - OVERVIEW

- 6.12.1 INTRODUCTION

- 6.12.2 KEY TARIFF RATES

- 6.12.3 PRICE IMPACT ANALYSIS

- 6.12.4 IMPACT ON COUNTRY/REGION

- 6.12.4.1 US

- 6.12.4.2 Europe

- 6.12.4.3 Asia Pacific

- 6.12.5 IMPACT ON APPLICATION SECTORS

- 6.13 IMPACT OF AI/GEN AI ON CNSL MARKET

7 CASHEW NUTSHELL LIQUID MARKET, BY APPLICATION

- 7.1 INTRODUCTION

- 7.2 ADHESIVES

- 7.2.1 WATER, CHEMICAL, THERMAL, SHOCK RESISTANCE, AND EXCELLENT MECHANICAL PROPERTIES TO BOOST GROWTH

- 7.3 COATINGS

- 7.3.1 HIGH DEMAND FOR ANTI-CORROSIVE PROTECTIVE COATINGS TO DRIVE MARKET

- 7.4 FOAMS & INSULATION

- 7.4.1 EXCELLENT PROCESSING, DIMENSIONAL STABILITY, AND UNIFORM STRUCTURE TO FUEL GROWTH

- 7.5 LAMINATES

- 7.5.1 SUPERIOR MOISTURE RESISTANCE AND HIGHER FLEXIBILITY TO PROPEL MARKET

- 7.6 FRICTION LININGS

- 7.6.1 NEED TO INCREASE FRICTION, REDUCE ROTOR WEAR, AND CONTROL NOISE TO BOOST MARKET

- 7.7 PERSONAL CARE

- 7.7.1 INCREASING DISPOSABLE INCOME TO DRIVE DEMAND

- 7.8 FUELS

- 7.8.1 ENHANCED FUEL STABILITY, REDUCED ENGINE WEAR, AND IMPROVED COMBUSTION EFFICIENCY TO BOOST GROWTH

- 7.9 OTHER APPLICATIONS

8 CASHEW NUTSHELL LIQUID MARKET, BY PRODUCT TYPE

- 8.1 INTRODUCTION

- 8.2 PHENOL FORMALDEHYDE (PF) RESINS

- 8.2.1 GROWING CONSUMER AND INDUSTRY PREFERENCE FOR GREEN CHEMISTRY AND REDUCED ENVIRONMENTAL IMPACT TO FUEL ADOPTION

- 8.3 EPOXY MODIFIERS & RESINS

- 8.3.1 EXCELLENT WATER RESISTANCE AND HIGHER FLEXIBILITY TO SUPPORT MARKET GROWTH

- 8.4 EPOXY CURING AGENTS

- 8.4.1 DEMAND FOR INDUSTRIAL, MARINE, PROTECTIVE COATINGS, TRANSPORTATION, AND FLOORING APPLICATIONS TO DRIVE MARKET

- 8.5 SURFACTANTS

- 8.5.1 GROWING DEMAND IN PERSONAL CARE FOR SAFETY TO BOOST MARKET GROWTH

- 8.6 POLYOLS & NCO BLOCKING AGENTS

- 8.6.1 IMPROVED PERFORMANCE AND DESIRED PROPERTIES OF END-USE PRODUCTS TO FUEL GROWTH

- 8.7 FRICTION MATERIALS

- 8.7.1 INCREASING DEMAND IN AUTOMOTIVE INDUSTRY TO BOOST MARKET

- 8.8 OTHER PRODUCT TYPES

9 CASHEW NUTSHELL LIQUID (CNSL) MARKET, BY EXTRACTION PROCESS

- 9.1 INTRODUCTION

- 9.1.1 MECHANICAL EXTRACTION PROCESS

- 9.1.2 SOLVENT EXTRACTION PROCESS

- 9.1.3 CHEMICAL EXTRACTION PROCESS

10 CASHEW NUTSHELL LIQUID (CNSL) MARKET, BY GRADE

- 10.1 INTRODUCTION

- 10.1.1 KEY CHARACTERISTICS

- 10.1.1.1 Raw CNSL

- 10.1.1.2 Degummed CNSL

- 10.1.1.3 Refined CNSL

- 10.1.1.4 Distilled CNSL

- 10.1.1 KEY CHARACTERISTICS

11 CASHEW NUTSHELL LIQUID (CNSL) MARKET, BY REGION

- 11.1 INTRODUCTION

- 11.2 ASIA PACIFIC

- 11.2.1 CHINA

- 11.2.1.1 Growing demand for processed and semi-processed CNSL products to drive market

- 11.2.2 INDIA

- 11.2.2.1 Rising middle-class population, rapid urbanization, and continuous influx of multinational companies to boost market

- 11.2.3 JAPAN

- 11.2.3.1 Demand from automobile industry to fuel market

- 11.2.4 SOUTH KOREA

- 11.2.4.1 Increasing demand for bio-based products from electronic and automotive industries to support growth

- 11.2.5 INDONESIA

- 11.2.5.1 Rapid industrialization and rising consumer spending to propel market

- 11.2.6 VIETNAM

- 11.2.6.1 Significant global exports to propel growth

- 11.2.1 CHINA

- 11.3 NORTH AMERICA

- 11.3.1 US

- 11.3.1.1 Rising environmental concerns and regulations to meet zero-emission norms to boost growth

- 11.3.2 MEXICO

- 11.3.2.1 Rising demand for coatings and adhesives to influence market growth

- 11.3.3 CANADA

- 11.3.3.1 Growing environmental concerns over petroleum-based products to support market growth

- 11.3.1 US

- 11.4 EUROPE

- 11.4.1 GERMANY

- 11.4.1.1 Growing developments and investments in chemical industry and exports to drive growth

- 11.4.2 FRANCE

- 11.4.2.1 Increasing investments in renewable energy sector to boost market

- 11.4.3 UK

- 11.4.3.1 Stringent environmental standards to drive market growth

- 11.4.4 ITALY

- 11.4.4.1 Growing automotive sector to drive market

- 11.4.5 NETHERLANDS

- 11.4.5.1 Demand in coatings, electrical and electronics, and construction to boost market

- 11.4.1 GERMANY

- 11.5 SOUTH AMERICA

- 11.5.1 BRAZIL

- 11.5.1.1 Strong export activity and industrial growth to drive market

- 11.5.1 BRAZIL

- 11.6 MIDDLE EAST & AFRICA

- 11.6.1 GCC COUNTRIES

- 11.6.1.1 UAE

- 11.6.1.1.1 Infrastructural projects to provide growth opportunities

- 11.6.1.2 Saudi Arabia

- 11.6.1.2.1 Rising demand from infrastructure, transportation, and manufacturing sectors to boost market

- 11.6.1.1 UAE

- 11.6.2 SOUTH AFRICA

- 11.6.2.1 Private sector investments to fuel market growth

- 11.6.1 GCC COUNTRIES

12 COMPETITIVE LANDSCAPE

- 12.1 INTRODUCTION

- 12.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 12.3 MARKET SHARE ANALYSIS, 2024

- 12.4 REVENUE ANALYSIS OF TOP FIVE PLAYERS, 2020-2024

- 12.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 12.5.1 STARS

- 12.5.2 EMERGING LEADERS

- 12.5.3 PERVASIVE PLAYERS

- 12.5.4 PARTICIPANTS

- 12.5.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 12.5.5.1 Company footprint

- 12.5.5.2 Region footprint

- 12.5.5.3 Product type footprint

- 12.5.5.4 Application footprint

- 12.6 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 12.6.1 PROGRESSIVE COMPANIES

- 12.6.2 RESPONSIVE COMPANIES

- 12.6.3 DYNAMIC COMPANIES

- 12.6.4 STARTING BLOCKS

- 12.6.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 12.6.5.1 Detailed list of key startups/SMES

- 12.6.5.2 Competitive benchmarking of key startups/SMEs

- 12.7 BRAND/PRODUCT COMPARISON ANALYSIS

- 12.8 COMPANY VALUATION AND FINANCIAL METRICS

- 12.9 COMPETITIVE SCENARIO

- 12.9.1 DEALS

- 12.9.2 EXPANSIONS

13 COMPANY PROFILES

- 13.1 KEY PLAYERS

- 13.1.1 CARDOLITE CORPORATION

- 13.1.1.1 Business overview

- 13.1.1.2 Products/Solutions/Services offered

- 13.1.1.3 MnM view

- 13.1.1.3.1 Right to win

- 13.1.1.3.2 Strategic choices

- 13.1.1.3.3 Weaknesses and competitive threats

- 13.1.2 GHW (VIETNAM) CO., LTD

- 13.1.2.1 Business overview

- 13.1.2.2 Products/Solutions/Services offered

- 13.1.2.3 MnM view

- 13.1.2.3.1 Right to win

- 13.1.2.3.2 Strategic choices

- 13.1.2.3.3 Weaknesses and competitive threats

- 13.1.3 PALMER INTERNATIONAL

- 13.1.3.1 Business overview

- 13.1.3.2 Products/Solutions/Services offered

- 13.1.3.3 Recent developments

- 13.1.3.3.1 Deals

- 13.1.3.3.2 Expansions

- 13.1.3.4 MnM view

- 13.1.3.4.1 Right to win

- 13.1.3.4.2 Strategic choices

- 13.1.3.4.3 Weaknesses and competitive threats

- 13.1.4 LC BUFFALO CO. LTD.

- 13.1.4.1 Products/Solutions/Services offered

- 13.1.4.2 MnM view

- 13.1.4.2.1 Right to win

- 13.1.4.2.2 Strategic choices

- 13.1.4.2.3 Weaknesses and competitive threats

- 13.1.5 CAT LOI CASHEW OIL PRODUCTION & EXPORT JOINT STOCK COMPANY (CAT LOI)

- 13.1.5.1 Business overview

- 13.1.5.2 Products/Solutions/Services offered

- 13.1.5.3 MnM view

- 13.1.5.3.1 Right to win

- 13.1.5.3.2 Strategic choices

- 13.1.5.3.3 Weaknesses and competitive threats

- 13.1.6 ZHEJIANG WANSHENG CO., LTD.

- 13.1.6.1 Business overview

- 13.1.6.2 Products/Solutions/Services offered

- 13.1.7 CASHEW CHEM INDIA

- 13.1.7.1 Business overview

- 13.1.7.2 Products/Solutions/Services offered

- 13.1.8 SRI DEVI GROUP

- 13.1.8.1 Business overview

- 13.1.8.2 Products/Solutions/Services offered

- 13.1.9 ADMARK POLYCOATS PVT. LTD.

- 13.1.9.1 Business overview

- 13.1.9.2 Products/Solutions/Services offered

- 13.1.10 GOLDEN CASHEW PRODUCTS PVT. LTD.

- 13.1.10.1 Business overview

- 13.1.10.2 Products/Solutions/Services offered

- 13.1.1 CARDOLITE CORPORATION

- 13.2 OTHER PLAYERS

- 13.2.1 PALADIN PAINTS & CHEMICALS PVT. LTD

- 13.2.2 SATYA CASHEW CHEMICALS PRIVATE LIMITED

- 13.2.3 K2P CHEMICALS

- 13.2.4 ZANTYE AGRO INDUSTRIES

- 13.2.5 SON CHAU CO.,LTD

- 13.2.6 SHIVAM CASHEW INDUSTRY

- 13.2.7 HUNG LOC PHAT CASHEW OIL CO. LTD.

- 13.2.8 KUMARASAMY INDUSTRIES

- 13.2.9 MIRAE GREEN CHEMICAL CO., LTD.

- 13.2.10 VIKO BIOFUEL COMPANY LIMITED

- 13.2.11 THINH DAI CHEMICAL

- 13.2.12 PT COMEXTRA MAJORA

- 13.2.13 CUONG THINH CASHEW OIL PRODUCTION COMPANY LIMITED

- 13.2.14 CNSL INDUSTRIAL CO., LTD.

- 13.2.15 TAN LOC CASHEW OIL PRODUCTION COMPANY LIMITED

14 ADJACENT & RELATED MARKETS

- 14.1 INTRODUCTION

- 14.2 LIMITATIONS

- 14.3 COATING RESINS MARKET

- 14.3.1 MARKET DEFINITION

- 14.3.2 MARKET OVERVIEW

- 14.4 COATING RESINS MARKET, BY REGION

- 14.4.1 ASIA PACIFIC

- 14.4.2 NORTH AMERICA

- 14.4.3 EUROPE

- 14.4.4 MIDDLE EAST & AFRICA

- 14.4.5 SOUTH AMERICA

15 APPENDIX

- 15.1 DISCUSSION GUIDE

- 15.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 15.3 CUSTOMIZATION OPTIONS

- 15.4 RELATED REPORTS

- 15.5 AUTHOR DETAILS

List of Tables

- TABLE 1 CNSL MARKET: RISK ASSESSMENT

- TABLE 2 ANALYSIS OF IMPACT OF PORTER'S FIVE FORCES ON CNSL MARKET

- TABLE 3 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP THREE APPLICATIONS (%)

- TABLE 4 KEY BUYING CRITERIA FOR TOP THREE APPLICATIONS

- TABLE 5 GDP TRENDS AND FORECAST OF MAJOR ECONOMIES, 2021-2030 (USD BILLION)

- TABLE 6 AVERAGE SELLING PRICE OF CNSL OFFERED BY KEY PLAYERS, BY APPLICATION, 2024 (USD/KG)

- TABLE 7 AVERAGE SELLING PRICE TREND OF CNSL, BY REGION, 2022-2030 (USD/KG)

- TABLE 8 ROLES OF COMPANIES IN CNSL ECOSYSTEM

- TABLE 9 IMPORT DATA FOR HS CODE 1302-COMPLIANT PRODUCTS, BY REGION, 2020-2024 (USD MILLION)

- TABLE 10 EXPORT DATA FOR HS CODE 1302-COMPLIANT PRODUCTS, BY REGION, 2020-2024 (USD MILLION)

- TABLE 11 NORTH AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 12 EUROPE: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 13 ASIA PACIFIC: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 14 MIDDLE EAST & AFRICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 15 SOUTH AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 16 CNSL MARKET: DETAILED LIST OF CONFERENCES AND EVENTS, 2025-2026

- TABLE 17 CNSL MARKET: FUNDING/INVESTMENT SCENARIO, 2020-2025

- TABLE 18 PATENT STATUS: PATENT APPLICATIONS, GRANTED PATENTS, AND OTHER PATENTS, 2014-2024

- TABLE 19 LIST OF MAJOR PATENTS RELATED TO CNSL, 2014-2024

- TABLE 20 US-ADJUSTED RECIPROCAL TARIFF RATES

- TABLE 21 CNSL MARKET, BY APPLICATION, 2020-2024 (KILOTON)

- TABLE 22 CNSL MARKET, BY APPLICATION, 2025-2030 (KILOTON)

- TABLE 23 CNSL MARKET, BY APPLICATION, 2020-2024 (USD MILLION)

- TABLE 24 CNSL MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 25 ADHESIVES: CNSL MARKET, BY REGION, 2020-2024 (KILOTON)

- TABLE 26 ADHESIVES: CNSL MARKET, BY REGION, 2025-2030 (KILOTON)

- TABLE 27 ADHESIVES: CNSL MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 28 ADHESIVES: CNSL MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 29 COATINGS: CNSL MARKET, BY REGION, 2020-2024 (KILOTON)

- TABLE 30 COATINGS: CNSL MARKET, BY REGION, 2025-2030 (KILOTON)

- TABLE 31 COATINGS: CNSL MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 32 COATINGS: CNSL MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 33 FOAMS & INSULATION: CNSL MARKET, BY REGION, 2020-2024 (KILOTON)

- TABLE 34 FOAMS & INSULATION: CNSL MARKET, BY REGION, 2025-2030 (KILOTON)

- TABLE 35 FOAMS & INSULATION: CNSL MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 36 FOAMS & INSULATION: CNSL MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 37 LAMINATES: CNSL MARKET, BY REGION, 2020-2024 (KILOTON)

- TABLE 38 LAMINATES: CNSL MARKET, BY REGION, 2025-2030 (KILOTON)

- TABLE 39 LAMINATES: CNSL MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 40 LAMINATES: CNSL MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 41 FRICTION LININGS: CNSL MARKET, BY REGION, 2020-2024 (KILOTON)

- TABLE 42 FRICTION LININGS: CNSL MARKET, BY REGION, 2025-2030 (KILOTON)

- TABLE 43 FRICTION LININGS: CNSL MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 44 FRICTION LININGS: CNSL MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 45 PERSONAL CARE: CNSL MARKET, BY REGION, 2020-2024 (KILOTON)

- TABLE 46 PERSONAL CARE: CNSL MARKET, BY REGION, 2025-2030 (KILOTON)

- TABLE 47 PERSONAL CARE: CNSL MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 48 PERSONAL CARE: CNSL MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 49 FUELS: CNSL MARKET, BY REGION, 2020-2024 (KILOTON)

- TABLE 50 FUELS: CNSL MARKET, BY REGION, 2025-2030 (KILOTON)

- TABLE 51 FUELS: CNSL MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 52 FUELS: CNSL MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 53 OTHER APPLICATIONS: CNSL MARKET, BY REGION, 2020-2024 (KILOTON)

- TABLE 54 OTHER APPLICATIONS: CNSL MARKET, BY REGION, 2025-2030 (KILOTON)

- TABLE 55 OTHER APPLICATIONS: CNSL MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 56 OTHER APPLICATIONS: CNSL MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 57 CNSL MARKET, BY PRODUCT TYPE, 2020-2024 (KILOTON)

- TABLE 58 CNSL MARKET, BY PRODUCT TYPE, 2025-2030 (KILOTON)

- TABLE 59 CNSL MARKET, BY PRODUCT TYPE, 2020-2024 (USD MILLION)

- TABLE 60 CNSL MARKET, BY PRODUCT TYPE, 2025-2030 (USD MILLION)

- TABLE 61 PHENOL FORMALDEHYDE (PF) RESINS: CNSL MARKET, BY REGION, 2020-2024 (KILOTON)

- TABLE 62 PHENOL FORMALDEHYDE (PF) RESINS: CNSL MARKET, BY REGION, 2025-2030 (KILOTON)

- TABLE 63 PHENOL FORMALDEHYDE (PF) RESINS: CNSL MARKET, BY REGION, 2020-2024, MARKET, BY REGION (USD MILLION)

- TABLE 64 PHENOL FORMALDEHYDE (PF) RESINS: CNSL MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 65 EPOXY MODIFIERS & RESINS: CNSL MARKET, BY REGION, 2020-2024 (KILOTON)

- TABLE 66 EPOXY MODIFIERS & RESINS: CNSL MARKET, BY REGION, 2025-2030 (KILOTON)

- TABLE 67 EPOXY MODIFIERS & RESINS: CNSL MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 68 EPOXY MODIFIERS & RESINS: CNSL MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 69 EPOXY CURING AGENTS: CNSL MARKET, BY REGION, 2020-2024 (KILOTON)

- TABLE 70 EPOXY CURING AGENTS: CNSL MARKET, BY REGION, 2025-2030 (KILOTON)

- TABLE 71 EPOXY CURING AGENTS: CNSL MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 72 EPOXY CURING AGENTS: CNSL MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 73 SURFACTANTS: CNSL MARKET, BY REGION, 2020-2024 (KILOTON)

- TABLE 74 SURFACTANTS: CNSL MARKET, BY REGION, 2025-2030 (KILOTON)

- TABLE 75 SURFACTANTS: CNSL MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 76 SURFACTANTS: CNSL MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 77 POLYOLS & NCO BLOCKING AGENTS: CNSL MARKET, BY REGION, 2020-2024 (KILOTON)

- TABLE 78 POLYOLS & NCO BLOCKING AGENTS: CNSL MARKET, BY REGION, 2025-2030 (KILOTON)

- TABLE 79 POLYOLS & NCO BLOCKING AGENTS: CNSL MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 80 POLYOLS & NCO BLOCKING AGENTS: CNSL MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 81 FRICTION MATERIALS: CNSL MARKET, BY REGION, 2020-2024 (KILOTON)

- TABLE 82 FRICTION MATERIALS: CNSL MARKET, BY REGION, 2025-2030 (KILOTON)

- TABLE 83 FRICTION MATERIALS: CNSL MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 84 FRICTION MATERIALS: CNSL MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 85 OTHER PRODUCT TYPES: CNSL MARKET, BY REGION, 2020-2024 (KILOTON)

- TABLE 86 OTHER PRODUCT TYPES: CNSL MARKET, BY REGION, 2025-2030 (KILOTON)

- TABLE 87 OTHER PRODUCT TYPES: CNSL MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 88 OTHER PRODUCT TYPES: CNSL MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 89 KEY CHARACTERISTICS OF DIFFERENT GRADES WITH PRIMARY APPLICATIONS

- TABLE 90 CNSL MARKET, BY REGION, 2020-2024 (KILOTON)

- TABLE 91 CNSL MARKET, BY REGION, 2025-2030 (KILOTON)

- TABLE 92 CNSL MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 93 CNSL MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 94 ASIA PACIFIC: CNSL MARKET, BY APPLICATION, 2020-2024 (KILOTON)

- TABLE 95 ASIA PACIFIC: CNSL MARKET, BY APPLICATION, 2025-2030 (KILOTON)

- TABLE 96 ASIA PACIFIC: CNSL MARKET, BY APPLICATION, 2020-2024 (USD MILLION)

- TABLE 97 ASIA PACIFIC: CNSL MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 98 ASIA PACIFIC: CNSL MARKET, BY PRODUCT TYPE, 2020-2024 (KILOTON)

- TABLE 99 ASIA PACIFIC: CNSL MARKET, BY PRODUCT TYPE, 2025-2030 (KILOTON)

- TABLE 100 ASIA PACIFIC: CNSL MARKET, BY PRODUCT TYPE, 2020-2024 (USD MILLION)

- TABLE 101 ASIA PACIFIC: CNSL MARKET, BY PRODUCT TYPE, 2025-2030 (USD MILLION)

- TABLE 102 ASIA PACIFIC: CNSL MARKET, BY COUNTRY, 2020-2024 (KILOTON)

- TABLE 103 ASIA PACIFIC: CNSL MARKET, BY COUNTRY, 2025-2030 (KILOTON)

- TABLE 104 ASIA PACIFIC: CNSL MARKET, BY COUNTRY, 2020-2024 (USD MILLION)

- TABLE 105 ASIA PACIFIC: CNSL MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 106 CHINA: CNSL MARKET, BY APPLICATION, 2020-2024 (KILOTON)

- TABLE 107 CHINA: CNSL MARKET, BY APPLICATION, 2025-2030 (KILOTON)

- TABLE 108 CHINA: CNSL MARKET, BY APPLICATION, 2020-2024 (USD MILLION)

- TABLE 109 CHINA: CNSL MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 110 INDIA: CNSL MARKET, BY APPLICATION, 2020-2024 (KILOTON)

- TABLE 111 INDIA: CNSL MARKET, BY APPLICATION, 2025-2030 (KILOTON)

- TABLE 112 INDIA: CNSL MARKET, BY APPLICATION, 2020-2024 (USD MILLION)

- TABLE 113 INDIA: CNSL MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 114 JAPAN: CNSL MARKET, BY APPLICATION, 2020-2024 (KILOTON)

- TABLE 115 JAPAN: CNSL MARKET, BY APPLICATION, 2025-2030 (KILOTON)

- TABLE 116 JAPAN: CNSL MARKET, BY APPLICATION, 2020-2024 (USD MILLION)

- TABLE 117 JAPAN: CNSL MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 118 SOUTH KOREA: CNSL MARKET, BY APPLICATION, 2020-2024 (KILOTON)

- TABLE 119 SOUTH KOREA: CNSL MARKET, BY APPLICATION, 2025-2030 (KILOTON)

- TABLE 120 SOUTH KOREA: CNSL MARKET, BY APPLICATION, 2020-2024 (USD MILLION)

- TABLE 121 SOUTH KOREA: CNSL MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 122 INDONESIA: CNSL MARKET, BY APPLICATION, 2020-2024 (KILOTON)

- TABLE 123 INDONESIA: CNSL MARKET, BY APPLICATION, 2025-2030 (KILOTON)

- TABLE 124 INDONESIA: CNSL MARKET, BY APPLICATION, 2020-2024 (USD MILLION)

- TABLE 125 INDONESIA: CNSL MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 126 VIETNAM: CNSL MARKET, BY APPLICATION, 2020-2024 (KILOTON)

- TABLE 127 VIETNAM: CNSL MARKET, BY APPLICATION, 2025-2030 (KILOTON)

- TABLE 128 VIETNAM: CNSL MARKET, BY APPLICATION, 2020-2024 (USD MILLION)

- TABLE 129 VIETNAM: CNSL MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 130 NORTH AMERICA: CNSL MARKET, BY APPLICATION, 2020-2024 (KILOTON)

- TABLE 131 NORTH AMERICA: CNSL MARKET, BY APPLICATION, 2025-2030 (KILOTON)

- TABLE 132 NORTH AMERICA: CNSL MARKET, BY APPLICATION, 2020-2024 (USD MILLION)

- TABLE 133 NORTH AMERICA: CNSL MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 134 NORTH AMERICA: CNSL MARKET, BY PRODUCT TYPE, 2020-2024 (KILOTON)

- TABLE 135 NORTH AMERICA: CNSL MARKET, BY PRODUCT TYPE, 2025-2030 (KILOTON)

- TABLE 136 NORTH AMERICA: CNSL MARKET, BY PRODUCT TYPE, 2020-2024 (USD MILLION)

- TABLE 137 NORTH AMERICA: CNSL MARKET, BY PRODUCT TYPE, 2025-2030 (USD MILLION)

- TABLE 138 NORTH AMERICA: CNSL MARKET, BY COUNTRY, 2020-2024 (KILOTON)

- TABLE 139 NORTH AMERICA: CNSL MARKET, BY COUNTRY, 2025-2030 (KILOTON)

- TABLE 140 NORTH AMERICA: CNSL MARKET, BY COUNTRY, 2020-2024 (USD MILLION)

- TABLE 141 NORTH AMERICA: CNSL MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 142 US: CNSL MARKET, BY APPLICATION, 2020-2024 (KILOTON)

- TABLE 143 US: CNSL MARKET, BY APPLICATION, 2025-2030 (KILOTON)

- TABLE 144 US: CNSL MARKET, BY APPLICATION, 2020-2024 (USD MILLION)

- TABLE 145 US: CNSL MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 146 MEXICO: CNSL MARKET, BY APPLICATION, 2020-2024 (KILOTON)

- TABLE 147 MEXICO: CNSL MARKET, BY APPLICATION, 2025-2030 (KILOTON)

- TABLE 148 MEXICO: CNSL MARKET, BY APPLICATION, 2020-2024 (USD MILLION)

- TABLE 149 MEXICO: CNSL MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 150 CANADA: CNSL MARKET, BY APPLICATION, 2020-2024 (KILOTON)

- TABLE 151 CANADA: CNSL MARKET, BY APPLICATION, 2025-2030 (KILOTON)

- TABLE 152 CANADA: CNSL MARKET, BY APPLICATION, 2020-2024 (USD MILLION)

- TABLE 153 CANADA: CNSL MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 154 EUROPE: CNSL MARKET, BY APPLICATION, 2020-2024 (KILOTON)

- TABLE 155 EUROPE: CNSL MARKET, BY APPLICATION, 2025-2030 (KILOTON)

- TABLE 156 EUROPE: CNSL MARKET, BY APPLICATION, 2020-2024 (USD MILLION)

- TABLE 157 EUROPE: CNSL MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 158 EUROPE: CNSL MARKET, BY PRODUCT TYPE, 2020-2024 (KILOTON)

- TABLE 159 EUROPE: CNSL MARKET, BY PRODUCT TYPE, 2025-2030 (KILOTON)

- TABLE 160 EUROPE: CNSL MARKET, BY PRODUCT TYPE, 2020-2024 (USD MILLION)

- TABLE 161 EUROPE: CNSL MARKET, BY PRODUCT TYPE, 2025-2030 (USD MILLION)

- TABLE 162 EUROPE: CNSL MARKET, BY COUNTRY, 2020-2024 (KILOTON)

- TABLE 163 EUROPE: CNSL MARKET, BY COUNTRY, 2025-2030 (KILOTON)

- TABLE 164 EUROPE: CNSL MARKET, BY COUNTRY, 2020-2024 (USD MILLION)

- TABLE 165 EUROPE: CNSL MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 166 GERMANY: CNSL MARKET, BY APPLICATION, 2020-2024 (KILOTON)

- TABLE 167 GERMANY: CNSL MARKET, BY APPLICATION, 2025-2030 (KILOTON)

- TABLE 168 GERMANY: CNSL MARKET, BY APPLICATION, 2020-2024 (USD MILLION)

- TABLE 169 GERMANY: CNSL MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 170 FRANCE: CNSL MARKET, BY APPLICATION, 2020-2024 (KILOTON)

- TABLE 171 FRANCE: CNSL MARKET, BY APPLICATION, 2025-2030 (KILOTON)

- TABLE 172 FRANCE: CNSL MARKET, BY APPLICATION, 2020-2024 (USD MILLION)

- TABLE 173 FRANCE: CNSL MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 174 UK: CNSL MARKET, BY APPLICATION, 2020-2024 (KILOTON)

- TABLE 175 UK: CNSL MARKET, BY APPLICATION, 2025-2030 (KILOTON)

- TABLE 176 UK: CNSL MARKET, BY APPLICATION, 2020-2024 (USD MILLION)

- TABLE 177 UK: CNSL MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 178 ITALY: CNSL MARKET, BY APPLICATION, 2020-2024 (KILOTON)

- TABLE 179 ITALY: CNSL MARKET, BY APPLICATION, 2025-2030 (KILOTON)

- TABLE 180 ITALY: CNSL MARKET, BY APPLICATION, 2020-2024 (USD MILLION)

- TABLE 181 ITALY: CNSL MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 182 NETHERLANDS: CNSL MARKET, BY APPLICATION, 2020-2024 (KILOTON)

- TABLE 183 NETHERLANDS: CNSL MARKET, BY APPLICATION, 2025-2030 (KILOTON)

- TABLE 184 NETHERLANDS: CNSL MARKET, BY APPLICATION, 2020-2024 (USD MILLION)

- TABLE 185 NETHERLANDS: CNSL MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 186 SOUTH AMERICA: CNSL MARKET, BY APPLICATION, 2020-2024 (KILOTON)

- TABLE 187 SOUTH AMERICA: CNSL MARKET, BY APPLICATION, 2025-2030 (KILOTON)

- TABLE 188 SOUTH AMERICA: CNSL MARKET, BY APPLICATION, 2020-2024 (USD MILLION)

- TABLE 189 SOUTH AMERICA: CNSL MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 190 SOUTH AMERICA: CNSL MARKET, BY PRODUCT TYPE, 2020-2024 (KILOTON)

- TABLE 191 SOUTH AMERICA: CNSL MARKET, BY PRODUCT TYPE, 2025-2030 (KILOTON)

- TABLE 192 SOUTH AMERICA: CNSL MARKET, BY PRODUCT TYPE, 2020-2024 (USD MILLION)

- TABLE 193 SOUTH AMERICA: CNSL MARKET, BY PRODUCT TYPE, 2025-2030 (USD MILLION)

- TABLE 194 SOUTH AMERICA: CNSL MARKET, BY COUNTRY, 2020-2024 (KILOTON)

- TABLE 195 SOUTH AMERICA: CNSL MARKET, BY COUNTRY, 2025-2030 (KILOTON)

- TABLE 196 SOUTH AMERICA: CNSL MARKET, BY COUNTRY, 2020-2024 (USD MILLION)

- TABLE 197 SOUTH AMERICA: CNSL MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 198 BRAZIL: CNSL MARKET, BY APPLICATION, 2020-2024 (KILOTON)

- TABLE 199 BRAZIL: CNSL MARKET, BY APPLICATION, 2025-2030 (KILOTON)

- TABLE 200 BRAZIL: CNSL MARKET, BY APPLICATION, 2020-2024 (USD MILLION)

- TABLE 201 BRAZIL: CNSL MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 202 MIDDLE EAST & AFRICA: CNSL MARKET, BY APPLICATION, 2020-2024 (KILOTON)

- TABLE 203 MIDDLE EAST & AFRICA: CNSL MARKET, BY APPLICATION, 2025-2030 (KILOTON)

- TABLE 204 MIDDLE EAST & AFRICA: CNSL MARKET, BY APPLICATION, 2020-2024 (USD MILLION)

- TABLE 205 MIDDLE EAST & AFRICA: CNSL MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 206 MIDDLE EAST & AFRICA: CNSL MARKET, BY PRODUCT TYPE, 2020-2024 (KILOTON)

- TABLE 207 MIDDLE EAST & AFRICA: CNSL MARKET, BY PRODUCT TYPE, 2025-2030 (KILOTON)

- TABLE 208 MIDDLE EAST & AFRICA: CNSL MARKET, BY PRODUCT TYPE, 2020-2024 (USD MILLION)

- TABLE 209 MIDDLE EAST & AFRICA: CNSL MARKET, BY PRODUCT TYPE, 2025-2030 (USD MILLION)

- TABLE 210 MIDDLE EAST & AFRICA: CNSL MARKET, BY COUNTRY, 2020-2024 (KILOTON)

- TABLE 211 MIDDLE EAST & AFRICA: CNSL MARKET, BY COUNTRY, 2025-2030 (KILOTON)

- TABLE 212 MIDDLE EAST & AFRICA: CNSL MARKET, BY COUNTRY, 2020-2024 (USD MILLION)

- TABLE 213 MIDDLE EAST & AFRICA: CNSL MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 214 UAE: CNSL MARKET, BY APPLICATION, 2020-2024 (KILOTON)

- TABLE 215 UAE: CNSL MARKET, BY APPLICATION, 2025-2030 (KILOTON)

- TABLE 216 UAE: CNSL MARKET, BY APPLICATION, 2020-2024 (USD MILLION)

- TABLE 217 UAE: CNSL MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 218 SAUDI ARABIA: CNSL MARKET, BY APPLICATION, 2020-2024 (KILOTON)

- TABLE 219 SAUDI ARABIA: CNSL MARKET, BY APPLICATION, 2025-2030 (KILOTON)

- TABLE 220 SAUDI ARABIA: CNSL MARKET, BY APPLICATION, 2020-2024 (USD MILLION)

- TABLE 221 SAUDI ARABIA: CNSL MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 222 SOUTH AFRICA: CNSL MARKET, BY APPLICATION, 2020-2024 (KILOTON)

- TABLE 223 SOUTH AFRICA: CNSL MARKET, BY APPLICATION, 2025-2030 (KILOTON)

- TABLE 224 SOUTH AFRICA: CNSL MARKET, BY APPLICATION, 2020-2024 (USD MILLION)

- TABLE 225 SOUTH AFRICA: CNSL MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 226 STRATEGIES ADOPTED BY KEY CNSL MANUFACTURERS, JANUARY 2022-JUNE 2025

- TABLE 227 CNSL MARKET: DEGREE OF COMPETITION

- TABLE 228 CNSL MARKET: REGION FOOTPRINT

- TABLE 229 CNSL MARKET: PRODUCT TYPE FOOTPRINT

- TABLE 230 CNSL MARKET: APPLICATION FOOTPRINT

- TABLE 231 CNSL MARKET: KEY STARTUPS/SMES

- TABLE 232 CNSL MARKET: COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES

- TABLE 233 CNSL MARKET: DEALS, JANUARY 2022-JUNE 2025

- TABLE 234 CNSL MARKET: EXPANSIONS, JANUARY 2022-JUNE 2025

- TABLE 235 CARDOLITE CORPORATION: COMPANY OVERVIEW

- TABLE 236 CARDOLITE CORPORATION: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 237 GHW (VIETNAM) CO., LTD: COMPANY OVERVIEW

- TABLE 238 GHW (VIETNAM) CO., LTD: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 239 PALMER INTERNATIONAL: COMPANY OVERVIEW

- TABLE 240 PALMER INTERNATIONAL: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 241 PALMER INTERNATIONAL: DEALS, JANUARY 2022-JUNE 2025

- TABLE 242 PALMER INTERNATIONAL: EXPANSIONS, JANUARY 2022-JUNE 2025

- TABLE 243 LC BUFFALO CO. LTD.: COMPANY OVERVIEW

- TABLE 244 LC BUFFALO CO. LTD.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 245 CAT LOI CASHEW OIL PRODUCTION & EXPORT JOINT STOCK COMPANY: COMPANY OVERVIEW

- TABLE 246 CAT LOI CASHEW OIL PRODUCTION & EXPORT JOINT STOCK COMPANY: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 247 ZHEJIANG WANSHENG: COMPANY OVERVIEW

- TABLE 248 ZHEJIANG WANSHENG: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 249 CASHEW CHEM INDIA: COMPANY OVERVIEW

- TABLE 250 CASHEW CHEM INDIA: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 251 SRI DEVI GROUP: COMPANY OVERVIEW

- TABLE 252 SRI DEVI GROUP: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 253 ADMARK POLYCOATS PVT. LTD.: COMPANY OVERVIEW

- TABLE 254 ADMARK POLYCOATS PVT. LTD: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 255 GOLDEN CASHEW PRODUCTS PVT. LTD.: COMPANY OVERVIEW

- TABLE 256 GOLDEN CASHEW PRODUCTS PVT. LTD.: PRODUCTS/SOLUTIONS/ SERVICES OFFERED

- TABLE 257 PALADIN PAINTS & CHEMICALS PVT. LTD.: COMPANY OVERVIEW

- TABLE 258 SATYA CASHEW CHEMICALS PRIVATE LIMITED: COMPANY OVERVIEW

- TABLE 259 K2P CHEMICALS: COMPANY OVERVIEW

- TABLE 260 ZANTYE AGRO INDUSTRIES: COMPANY OVERVIEW

- TABLE 261 SON CHAU CO.,LTD: COMPANY OVERVIEW

- TABLE 262 SHIVAM CASHEW INDUSTRY: COMPANY OVERVIEW

- TABLE 263 HUNG LOC PHAT CASHEW OIL CO. LTD. : COMPANY OVERVIEW

- TABLE 264 KUMARASAMY INDUSTRIES: COMPANY OVERVIEW

- TABLE 265 MIRAE GREEN CHEMICAL CO., LTD.: COMPANY OVERVIEW

- TABLE 266 VIKO BIOFUEL COMPANY LIMITED: COMPANY OVERVIEW

- TABLE 267 THINH DAI CHEMICAL: COMPANY OVERVIEW

- TABLE 268 PT COMEXTRA MAJORA: COMPANY OVERVIEW

- TABLE 269 CUONG THINH CASHEW OIL PRODUCTION COMPANY LIMITED: COMPANY OVERVIEW

- TABLE 270 CNSL INDUSTRIAL CO., LTD.: COMPANY OVERVIEW

- TABLE 271 TAN LOC CASHEW OIL PRODUCTION COMPANY LIMITED: COMPANY OVERVIEW

- TABLE 272 COATING RESINS MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 273 COATING RESINS MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 274 COATING RESINS MARKET, BY REGION, 2020-2023 (KILOTON)

- TABLE 275 COATING RESINS MARKET, BY REGION, 2024-2029 (KILOTON)

- TABLE 276 ASIA PACIFIC: COATING RESINS MARKET, BY COUNTRY, 2020-2023 (USD MILLION)

- TABLE 277 ASIA PACIFIC: COATING RESINS MARKET, BY COUNTRY, 2024-2029 (USD MILLION)

- TABLE 278 ASIA PACIFIC: COATING RESINS MARKET, BY COUNTRY, 2020-2023 (KILOTON)

- TABLE 279 ASIA PACIFIC: COATING RESINS MARKET, BY COUNTRY, 2024-2029 (KILOTON)

- TABLE 280 NORTH AMERICA: COATING RESINS MARKET, BY COUNTRY, 2020-2023 (USD MILLION)

- TABLE 281 NORTH AMERICA: COATING RESINS MARKET, BY COUNTRY, 2024-2029 (USD MILLION)

- TABLE 282 NORTH AMERICA: COATING RESINS MARKET, BY COUNTRY, 2020-2023 (KILOTON)

- TABLE 283 NORTH AMERICA: COATING RESINS MARKET, BY COUNTRY, 2024-2029 (KILOTON)

- TABLE 284 EUROPE: COATING RESINS MARKET, BY COUNTRY, 2020-2023 (USD MILLION)

- TABLE 285 EUROPE: COATING RESINS MARKET, BY COUNTRY, 2024-2029 (USD MILLION)

- TABLE 286 EUROPE: COATING RESINS MARKET, BY COUNTRY, 2020-2023 (KILOTON)

- TABLE 287 EUROPE: COATING RESINS MARKET, BY COUNTRY, 2024-2029 (KILOTON)

- TABLE 288 MIDDLE EAST & AFRICA: COATING RESINS MARKET, BY COUNTRY, 2020-2023 (USD MILLION)

- TABLE 289 MIDDLE EAST & AFRICA: COATING RESINS MARKET, BY COUNTRY, 2024-2029 (USD MILLION)

- TABLE 290 MIDDLE EAST & AFRICA: COATING RESINS MARKET, BY COUNTRY, 2020-2023 (KILOTON)

- TABLE 291 MIDDLE EAST & AFRICA: COATING RESINS MARKET, BY COUNTRY, 2024-2029 (KILOTON)

- TABLE 292 SOUTH AMERICA: COATING RESINS MARKET, BY COUNTRY, 2020-2023 (USD MILLION)

- TABLE 293 SOUTH AMERICA: COATING RESINS MARKET, BY COUNTRY, 2024-2029 (USD MILLION)

- TABLE 294 SOUTH AMERICA: COATING RESINS MARKET, BY COUNTRY, 2020-2023 (KILOTON)

- TABLE 295 SOUTH AMERICA: COATING RESINS MARKET, BY COUNTRY, 2024-2029 (KILOTON)

List of Figures

- FIGURE 1 CNSL MARKET SEGMENTATION AND REGIONAL SCOPE

- FIGURE 2 CNSL MARKET: RESEARCH DESIGN

- FIGURE 3 MARKET SIZE ESTIMATION METHODOLOGY: APPROACH 1 (SUPPLY SIDE): COLLECTIVE MARKET SHARE OF KEY PLAYERS

- FIGURE 4 MARKET SIZE ESTIMATION METHODOLOGY: APPROACH 2 -BOTTOM-UP (SUPPLY SIDE): COLLECTIVE REVENUE OF ALL PRODUCTS

- FIGURE 5 MARKET SIZE ESTIMATION METHODOLOGY: APPROACH 3 -BOTTOM-UP (DEMAND SIDE)

- FIGURE 6 MARKET SIZE ESTIMATION METHODOLOGY: APPROACH 3 -TOP-DOWN

- FIGURE 7 CNSL MARKET: DATA TRIANGULATION

- FIGURE 8 CNSL MARKET CAGR PROJECTIONS FROM SUPPLY SIDE

- FIGURE 9 MARKET GROWTH PROJECTIONS FROM DEMAND-SIDE DRIVERS AND OPPORTUNITIES

- FIGURE 10 EPOXY MODIFIERS & RESINS SEGMENT TO DOMINATE CNSL MARKET DURING FORECAST PERIOD

- FIGURE 11 COATINGS SEGMENT TO DRIVE CNSL MARKET DURING FORECAST PERIOD

- FIGURE 12 EUROPE ACCOUNTED FOR LARGEST MARKET SHARE IN 2024

- FIGURE 13 CNSL MARKET TO WITNESS HIGH GROWTH DURING FORECAST PERIOD

- FIGURE 14 EUROPE TO BE FASTEST-GROWING CNSL MARKET DURING FORECAST PERIOD

- FIGURE 15 CHINA ACCOUNTED FOR LARGEST SHARE OF ASIA PACIFIC MARKET IN 2024

- FIGURE 16 COATINGS APPLICATION LED CNSL MARKET ACROSS REGIONS IN 2024

- FIGURE 17 GERMANY TO REGISTER HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 18 DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES IN CNSL MARKET

- FIGURE 19 CNSL MARKET: PORTER'S FIVE FORCES ANALYSIS

- FIGURE 20 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP THREE APPLICATIONS

- FIGURE 21 KEY BUYING CRITERIA FOR TOP THREE APPLICATIONS

- FIGURE 22 CNSL MARKET: SUPPLY CHAIN ANALYSIS

- FIGURE 23 AVERAGE SELLING PRICE OF CNSL OFFERED BY KEY PLAYERS FOR TOP THREE APPLICATIONS, 2024

- FIGURE 24 AVERAGE SELLING PRICE TREND OF CNSL, BY REGION, 2022-2030

- FIGURE 25 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- FIGURE 26 CNSL MARKET: ECOSYSTEM ANALYSIS

- FIGURE 27 IMPORT DATA FOR HS CODE 1302-COMPLIANT PRODUCTS, BY KEY COUNTRY, 2020-2024 (USD MILLION)

- FIGURE 28 EXPORT DATA FOR HS CODE 1302-COMPLIANT PRODUCTS, BY KEY COUNTRY, 2020-2024 (USD MILLION)

- FIGURE 29 PATENTS REGISTERED FOR CNSL, 2014-2024

- FIGURE 30 MAJOR PATENTS RELATED TO CNSL, 2014-2024

- FIGURE 31 LEGAL STATUS OF PATENTS FILED RELATED TO CNSL, 2014-2024

- FIGURE 32 MAXIMUM PATENTS FILED IN JURISDICTION OF US, 2014-2024

- FIGURE 33 IMPACT OF AI/GEN AI ON CNSL MARKET

- FIGURE 34 COATINGS TO BE LARGEST APPLICATION OF CNSL MARKET DURING FORECAST PERIOD

- FIGURE 35 EPOXY MODIFIERS & RESINS SEGMENT TO LEAD MARKET DURING FORECAST PERIOD

- FIGURE 36 EUROPE TO BE LARGEST CNSL MARKET BETWEEN 2025 AND 2030

- FIGURE 37 ASIA PACIFIC: CNSL MARKET SNAPSHOT

- FIGURE 38 NORTH AMERICA: CNSL MARKET SNAPSHOT

- FIGURE 39 EUROPE: CNSL MARKET SNAPSHOT

- FIGURE 40 MARKET SHARE ANALYSIS OF TOP FIVE PLAYERS, 2024

- FIGURE 41 REVENUE ANALYSIS OF KEY COMPANIES IN CNSL MARKET, 2020-2024

- FIGURE 42 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- FIGURE 43 CNSL MARKET: COMPANY FOOTPRINT

- FIGURE 44 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- FIGURE 45 BRAND/PRODUCT COMPARISON

- FIGURE 46 CNSL MARKET: EV/EBITDA OF KEY MANUFACTURERS

- FIGURE 47 CNSL MARKET: ENTERPRISE VALUATION (EV) OF KEY PLAYERS

- FIGURE 48 GHW (VIETNAM) CO., LTD: COMPANY SNAPSHOT

全球腰果壳液市场规模调查及预测:按产品类型、等级、萃取製程、应用领域、最终用户和地区分類的预测(2026-2035 年)

全球腰果壳液市场规模调查及预测:按产品类型、等级、萃取製程、应用领域、最终用户和地区分類的预测(2026-2035 年) 腰果壳液市场:2026-2032年全球市场预测(按类型、提取方法、最终用户、应用和分销管道划分)

腰果壳液市场:2026-2032年全球市场预测(按类型、提取方法、最终用户、应用和分销管道划分) 腰果壳液的全球市场

腰果壳液的全球市场