|

市场调查报告书

商品编码

1790686

全球税务管理市场(至 2030 年)依解决方案类型(税务合规与最佳化、文件管理与归檔、报税表准备与彙报、税务分析工具、审核与风险管理工具)及税种(间接税、直接税)划分Tax Management Market by Solution Type (Tax Compliance & Optimization, Document Management & Archiving, Tax Preparation & Reporting, Tax Analytics Tools, Audit & Risk Management Tools), Tax Type (Indirect Tax and Direct Tax) - Global Forecast to 2030 |

||||||

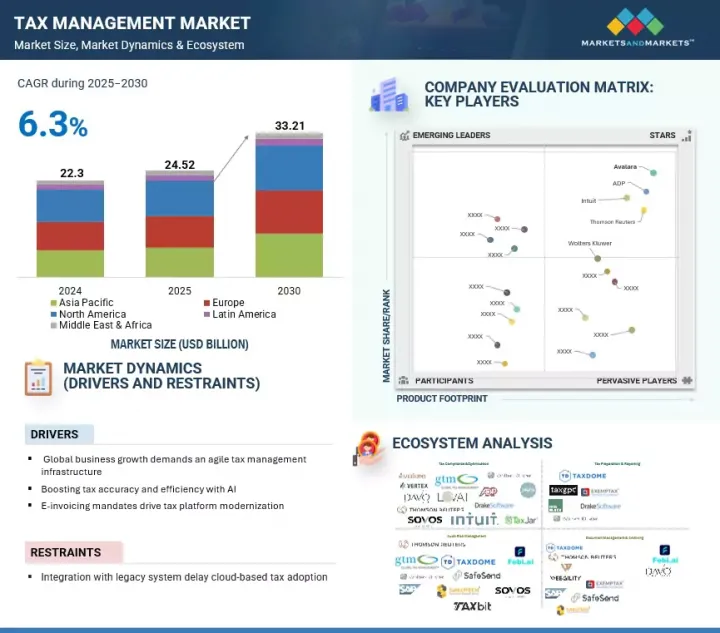

税务管理市场正在迅速扩张,预计将从 2025 年的 245.2 亿美元增长到 2030 年的 332.1 亿美元,预测期内的复合年增长率为 6.3%。

影响税务管理市场的一个关键驱动因素是全球企业发展的加速,这需要一个灵活且扩充性的税务基础设施,以支援跨多个司法管辖区的合规性。

| 调查范围 | |

|---|---|

| 调查年份 | 2020-2030 |

| 基准年 | 2024 |

| 预测期 | 2025-2030 |

| 单元 | 美元 |

| 部门 | 产品类别、部署模式、税种、组织规模、产业 |

| 目标区域 | 北美、欧洲、亚太地区、中东和非洲、拉丁美洲 |

人工智慧的整合进一步提高了税务准确性,实现了即时异常检测、自动规则执行和更快的报告週期。此外,全球范围内电子发货单要求的推广,迫使企业对其传统税务平台进行现代化升级,以适应结构化资料和监管申报要求。然而,市场面临着许多製约因素,包括难以将现代税务解决方案与现有企业系统集成,这减缓了云端基础平台的普及,并限制了在分散式环境中部署先进技术的能力。

“按税种划分,预计间接税部分在预测期内将呈现最高增长。”

随着监管要求明显转向即时合规数位化报告,预计间接税(包括增值税、商品及服务税、销售税、课税和其他交易课税)将出现最大增长。 2024 年 4 月,Sovos 推出了间接税套件,将税务裁决、电子发货单和自动报告整合到一个云端原生平台中,以解决 70 多个司法管辖区日益增长的复杂问题。同年 10 月,Sovos 发布了适用于 SAP 环境的支援 Clean Core 的解决方案,显示需要跨增值税、商品及服务税和销售税系统的深度 ERP 整合和扩充性配置。这些趋势凸显了全球企业在其核心财务流程中实施间接税自动化的迫切性。这为供应商提供了一个重要的机会,可以提供专用平台来执行特定国家的税务规则,确保结构性地遵守发货单义务,并动态适应不断变化的监管变化。为了在这个高成长的间接税领域保持竞争力,供应商必须透过特定司法管辖区的发货单验证、跨境海关自动化以及响应即时政策变化的规则引擎来实现差异化。成功取决于能否提供预先认证的电子发货单模组、智慧对帐工作流程以及持续的配置更新。随着企业优先考虑敏捷性和准确性,能够即时处理异常并提供协同设计的实施支援的供应商将推动与核心税务业务的深度整合,将自己定位为长期转型合作伙伴,并在复杂的合规环境中实现可持续的收益。

本报告调查了全球税务管理市场,并提供了市场概况、影响市场成长的各种因素分析、技术和专利趋势、法律制度、案例研究、市场规模趋势和预测、各个细分市场、地区/主要国家的详细分析、竞争格局和主要企业的概况。

目录

第一章 引言

第二章调查方法

第三章执行摘要

第四章重要考察

第五章市场概况及产业趋势

- 市场动态

- 驱动程式

- 抑制因素

- 机会

- 任务

- 案例研究分析

- 生态系分析

- 供应链分析

- 定价分析

- 专利分析

- 技术分析

- 监管状况

- 波特五力分析

- 主要相关利益者和采购标准

- 2025-2026年重要会议和活动

- 影响我们客户业务的趋势和中断

- 投资金筹措场景

- 产生人工智慧对税务管理的影响

第六章 税务管理市场(依服务细分)

- 解决方案

- 合规性和优化

- 税务规划和彙报

- 审核和风险管理工具

- 税务分析工具

- 文件管理与归檔

- 其他的

- 服务

- 实施与系统集成

- 税务设定和咨询服务

- 支援和监管维护

第七章 税务管理市场(依部署类型)

- 本地

- 云

第 8 章:税务管理市场(依组织规模)

- 大公司

- 小型企业

第九章:税务管理市场(依税种划分)

- 间接税

- 增值税(VAT)

- 商品及服务税(GST)

- 销售税

- 关税

- 其他的

- 直接税

- 公司税

- 资本利得税

- 财产税

- 其他的

第十章:税务管理市场(按行业)

- BFSI

- 资讯科技/通讯

- 製造业

- 零售与电子商务

- 医疗保健与生命科学

- 政府和公共部门

- 能源与公用事业

- 其他的

第 11 章:各地区税务管理市场

- 北美洲

- 市场驱动因素

- 宏观经济展望

- 美国

- 加拿大

- 欧洲

- 市场驱动因素

- 宏观经济展望

- 英国

- 德国

- 法国

- 义大利

- 其他的

- 亚太地区

- 市场驱动因素

- 宏观经济展望

- 中国

- 日本

- 印度

- 其他的

- 中东和非洲

- 市场驱动因素

- 宏观经济展望

- 海湾合作委员会国家

- 南非

- 其他的

- 拉丁美洲

- 市场驱动因素

- 宏观经济展望

- 巴西

- 墨西哥

- 其他的

第十二章竞争格局

- 主要企业/主要企业策略

- 收益分析

- 市场占有率分析

- 品牌/产品比较

- 估值和财务指标

- 公司评估矩阵:主要企业

- 公司估值矩阵:Start-Ups/中小型企业

- 竞争场景

第十三章:公司简介

- 主要企业

- WOLTERS KLUWER

- THOMSON REUTERS

- AVALARA

- ADP

- VERTEX

- SOVOS

- INTUIT

- H&R BLOCK

- SAP

- XERO

- 其他公司

- TAXBIT

- SAILOTECH

- EXEMPTAX

- CLEAR

- DRAKE SOFTWARE

- TAXCLOUD

- LOVAT SOFTWARE

- WEBGILITY

- GLOBAL TAX MANAGEMENT INC.

- TAXDOME

- TAXGPT

- FEBI.AI

- TAXBUDDY

- TAXCALC

- CAPIUM

第 14 章:相邻/相关市场

第十五章 附录

The tax management market is expanding rapidly, with a projected size of USD 24.52 billion in 2025 to reach USD 33.21 billion by 2030, at a CAGR of 6.3% during the forecast period. The key drivers shaping the tax management market include the accelerating pace of global business operations, which requires agile, scalable tax infrastructure capable of supporting multi-jurisdictional compliance.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2020-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | USD Million |

| Segments | Offering, deployment mode, tax type, organization size, and vertical |

| Regions covered | North America, Europe, Asia Pacific, Middle East & Africa, Latin America |

Artificial intelligence integration further enhances tax accuracy, enabling real-time anomaly detection, automated rule application, and faster reporting cycles. Additionally, the global rollout of e-invoicing mandates pushes enterprises to modernize legacy tax platforms to meet structured data and regulatory submission requirements. However, the market also faces notable restraints. Among them is the challenge of integrating modern tax solutions with legacy enterprise systems, which slows the adoption of cloud-based platforms and limits the ability to deploy advanced technologies across distributed environments.

"Indirect tax type is expected to account for the fastest growth during the forecast period."

Indirect tax, comprising value-added tax, goods and services tax, sales tax, customs duties, and other transactional levies, is expected to emerge as the fastest-growing segment in the tax management market as regulatory mandates shift decisively toward real-time compliance and digitalized reporting. In April 2024, Sovos launched its Indirect Tax Suite to address growing complexity in over 70 jurisdictions, integrating determination, e-invoicing, and automated filings into a single cloud-native platform. The October 2024 release of a clean-core, ready solution for SAP environments demonstrated the need for deep ERP integration and scalable configuration across VAT, GST, and sales tax regimes. These developments reflect the urgency among global enterprises to operationalize indirect tax automation across core finance processes. This creates a strong opportunity for vendors to deliver purpose-built platforms that apply country-specific tax rules, ensure structured compliance with invoicing mandates, and adapt dynamically to ongoing regulatory changes. To stay competitive in the high-growth indirect tax segment, vendors must differentiate through jurisdiction-specific invoice clearance, cross-border duty automation, and rule engines that adapt to real-time policy changes. Success will depend on delivering pre-certified e-invoicing modules, intelligent reconciliation workflows, and continuous configuration updates. As enterprises prioritize agility and accuracy, providers that enable real-time exception handling and offer co-engineered deployment support will drive deeper integration into core tax operations, positioning themselves as long-term transformation partners and unlocking sustained revenue in complex compliance environments.

"Large enterprises are expected to hold the largest market share during the forecast period."

Large enterprises require advanced tax solutions to manage complex, multi-jurisdictional compliance and integration with ERP systems. Their scale and regulatory exposure drive demand for automation, real-time calculation, and audit-ready reporting. In October 2024, Sovos partnered with IFS to integrate its indirect tax suite into IFS Cloud, enabling embedded, real-time compliance across more than 20,000 global jurisdictions, tailored explicitly for large multinational entities. Reinforcing this shift, the April 2025 Thomson Reuters Generative AI in Professional Services Report confirmed that 21% of tax and accounting firms now deploy GenAI at scale, while 92% of corporate tax professionals expect it to be part of daily tax operations within five years. These trends signal a decisive enterprise push toward intelligent, high-capacity platforms that combine automation, compliance, and strategic insight. Providers that align with large enterprises' priorities, which are accuracy, agility, and control, will gain a competitive advantage, expand recurring revenue streams, and position themselves as core infrastructure partners in global tax modernization.

"North America is expected to lead the tax management market with established regulatory frameworks, advanced digital infrastructure, and high adoption among large enterprises, while Asia Pacific is the fastest-growing region driven by accelerated e-invoicing mandates, expanding cross-border trade and government-led digitalization of tax administration systems."

North America is expected to lead the tax management market, driven by complex regulatory frameworks, high enterprise demand for automation, and early adoption of AI-powered compliance platforms. In April 2025, Intuit enhanced its TurboTax Business suite with generative AI, improving real-time tax insights and filing accuracy for corporate users. This reflects the region's focus on intelligent, large-scale tax automation. In contrast, Asia Pacific is the fastest-growing region, fueled by rapid tax digitization, cross-border trade, and government-mandated e-invoicing initiatives across India, Indonesia, and Vietnam. Enterprises actively invest in scalable, cloud-based tax platforms, creating strong opportunities for vendors to deliver localized rule engines, real-time reporting tools, and pre-integrated ERP connectors.

Breakdown of Primaries

In-depth interviews were conducted with Chief Executive Officers (CEOs), innovation and technology directors, system integrators, and executives from various key organizations operating in the tax management market.

- By Company: Tier I - 40%, Tier II - 25%, and Tier III - 35%

- By Designation: C-Level Executives - 25%, D-Level Executives -37%, and others - 38%

- By Region: North America - 38%, Europe - 24%, Asia Pacific - 40%, and Rest of the World - 6%

The report includes a study of key players offering tax management services. It profiles major vendors in the tax management market. The major market players include Avalara (US), Intuit (US), ADP (US), Thomson Reuters (Canada), Wolters Kluwer (Netherlands), H&R Block (US), SAP (Germany), Sovos (US), Vertex (US), TaxBit (US), Sailotech (US), TaxCalc (UK), Clear (India), Xero (Australia), Exemptax (US), Taxbuddy (India), Feb.ai (India), Drake Software (US), Tax Cloud (US), Lovat Software (UK), Webgility (US), Global Tax Management Inc. (US), Taxdome (US), and TaxGPT (US).

Research Coverage

This research report categorizes the tax management market based on Offering (Solutions (Tax Compliance & Optimization, Tax Preparation & Reporting, Audit & Risk Management Tools, Tax Analytics Tools, Document Management & Archiving), Services (Implementation & System Integration, Tax Configuration & Advisory Services, Support & Regulatory Maintenance)), Deployment Mode (Cloud, On-premises), Tax Type (Direct Taxes (Corporate Tax, Capital Gains Tax, Property Tax, Other Direct Taxes), Indirect Taxes (Value-Added Tax (VAT), Goods & Services Tax (GST), Sales Tax, Customs Duties, Other Indirect Taxes)), Organization Size (Large Enterprises, SMEs), Vertical (Banking, Financial Services & Insurance (BFSI), IT & Telecom, Retail & E-commerce, Manufacturing, Healthcare & Life Sciences, Government & Public Sector, Energy & Utilities, Other Verticals (Transportation & Logistics, Education, Construction & Real Estate)), and Region (North America, Europe, Asia Pacific, Middle East & Africa, and Latin America). The scope of the report covers detailed information regarding the major factors, such as drivers, restraints, challenges, and opportunities, influencing the growth of the tax management market. A thorough analysis of the key industry players was done to provide insights into their business overview, solutions, and services; key strategies; contracts, partnerships, agreements, new product & service launches, mergers and acquisitions; and recent developments associated with the tax management market. This report also covered the competitive analysis of upcoming startups in the tax management market ecosystem.

Reason to Buy This Report

The report would provide market leaders/new entrants with information on the closest approximations of the revenue numbers for the overall tax management market and its subsegments. It would help stakeholders understand the competitive landscape and gain more insights to better position their businesses and plan suitable go-to-market strategies. It also helps stakeholders understand the market's pulse and provides information on key market drivers, restraints, challenges, and opportunities.

This report provides insights on the following pointers:

- Analysis of key drivers (Global business growth demands an agile tax management infrastructure, Boosting tax accuracy & efficiency with AI, E-invoicing mandates drive tax platform modernization), restraints (Integration with legacy system delay cloud-based tax adoption), opportunities (Automation adoption by SMEs fuels tax management expansion, Advisory services boost innovation in tax management), and challenges (Shortage of skilled workforce slows tax tech adoption, Multi-system complexity hampers tax automation).

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and product & service launches in the tax management market.

- Market Development: Comprehensive information about lucrative markets - the report analyzes the tax management market across varied regions.

- Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the tax management market.

- Competitive Assessment: In-depth assessment of market shares, growth strategies and service offerings of leading players such Avalara (US), Intuit (US), ADP (US), Thomson Reuters (Canada), Wolters Kluwer (Netherlands), H&R Block (US), SAP (Germany), Sovos (US), Vertex (US), TaxBit (US), Sailotech (US), TaxCalc (UK), Clear (India), Xero (Australia), Exemptax (US), Taxbuddy (India), Feb.ai (India), Drake Software (US), Tax Cloud (US), Lovat Software (UK), Webgility (US), Global Tax Management Inc. (US), Taxdome (US), and TaxGPT (US). The report also helps stakeholders understand the pulse of the tax management market and provides them with information on key market drivers, restraints, challenges, and opportunities.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 MARKET SCOPE

- 1.3.1 MARKET SEGMENTATION AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 STAKEHOLDERS

- 1.6 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH APPROACH

- 2.1.1 SECONDARY DATA

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Breakup of primary profiles

- 2.1.2.2 Key industry insights

- 2.2 MARKET BREAKUP AND DATA TRIANGULATION

- 2.3 MARKET SIZE ESTIMATION

- 2.3.1 TOP-DOWN APPROACH

- 2.3.2 BOTTOM-UP APPROACH

- 2.3.3 MARKET ESTIMATION APPROACHES

- 2.4 MARKET FORECAST

- 2.5 RESEARCH ASSUMPTIONS

- 2.6 RESEARCH LIMITATIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN TAX MANAGEMENT MARKET

- 4.2 TAX MANAGEMENT MARKET, BY OFFERING, 2025 VS 2030

- 4.3 TAX MANAGEMENT MARKET, BY DEPLOYMENT MODE, 2025 VS 2030

- 4.4 TAX MANAGEMENT MARKET, BY TAX TYPE, 2025 VS 2030

- 4.5 TAX MANAGEMENT MARKET, BY ORGANIZATION SIZE, 2025 VS 2030

- 4.6 TAX MANAGEMENT MARKET, BY VERTICAL, 2025 VS 2030

- 4.7 TAX MANAGEMENT MARKET, BY REGION, 2025-2030

5 MARKET OVERVIEW AND INDUSTRY TRENDS

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Global business growth demands agile tax management infrastructure

- 5.2.1.2 Adoption of AI tools boosts tax accuracy and efficiency

- 5.2.1.3 E-invoicing mandates drive tax platform modernization

- 5.2.2 RESTRAINTS

- 5.2.2.1 Integration with legacy systems delays cloud-based tax adoption

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Automation adoption by SMEs fuels tax management expansion

- 5.2.3.2 Advisory services boost innovation in tax management

- 5.2.4 CHALLENGES

- 5.2.4.1 Shortage of skilled workforce hinders adoption of tax technologies

- 5.2.4.2 Multi-system complexity hampers tax automation

- 5.2.1 DRIVERS

- 5.3 CASE STUDY ANALYSIS

- 5.3.1 INOVONICS SIMPLIFIES MULTI-STATE TAX COMPLIANCE WITH AVALARA

- 5.3.2 CCH PROSYSTEM FX AND AXCESS BOOST ACCURACY AND EFFICIENCY OF TAX SYSTEMS

- 5.3.3 WESLEYAN UNIVERSITY MANAGES CONFORMITY WITH ADP SMARTCOMPLIANCE

- 5.3.4 VERTEX DELIVERS REAL-TIME TAX ACCURACY FOR LEGO'S ONLINE SALES

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 SUPPLY CHAIN ANALYSIS

- 5.6 PRICING ANALYSIS

- 5.6.1 AVERAGE SELLING PRICE TREND, BY REGION, 2022-2024

- 5.6.2 INDICATIVE PRICING ANALYSIS, BY OFFERING, 2025

- 5.7 PATENT ANALYSIS

- 5.8 TECHNOLOGY ANALYSIS

- 5.8.1 KEY TECHNOLOGIES

- 5.8.1.1 Cloud-native architecture

- 5.8.1.2 Tax determination logic modules

- 5.8.1.3 Compliance filing engine

- 5.8.1.4 GenAI Copilot for tax

- 5.8.2 COMPLEMENTARY TECHNOLOGIES

- 5.8.2.1 Machine learning & AI

- 5.8.2.2 Robotic process automation

- 5.8.2.3 Digital signature & archival solutions

- 5.8.2.4 Low-code/no-code configuration platform

- 5.8.3 ADJACENT TECHNOLOGIES

- 5.8.3.1 Streamlining real estate tax compliance with ONESOURCE solutions

- 5.8.3.2 API management platform

- 5.8.3.3 Geolocation & IP mapping

- 5.8.1 KEY TECHNOLOGIES

- 5.9 REGULATORY LANDSCAPE

- 5.9.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.9.2 REGULATIONS BY REGION

- 5.10 PORTER'S FIVE FORCES ANALYSIS

- 5.10.1 THREAT OF NEW ENTRANTS

- 5.10.2 THREAT OF SUBSTITUTES

- 5.10.3 BARGAINING POWER OF BUYERS

- 5.10.4 BARGAINING POWER OF SUPPLIERS

- 5.10.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.11 KEY STAKEHOLDERS AND BUYING CRITERIA

- 5.11.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 5.11.2 BUYING CRITERIA

- 5.12 KEY CONFERENCES AND EVENTS, 2025-2026

- 5.13 TRENDS AND DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.14 INVESTMENT AND FUNDING SCENARIO

- 5.15 IMPACT OF GEN AI IN TAX MANAGEMENT

- 5.15.1 TOP CLIENTS ADAPTING GEN AI

- 5.15.1.1 H&R Block

- 5.15.1.2 Febi.ai

- 5.15.2 CASE STUDY

- 5.15.2.1 Streamlining Real Estate Tax Compliance with ONESOURCE Solutions

- 5.15.1 TOP CLIENTS ADAPTING GEN AI

6 TAX MANAGEMENT MARKET, BY OFFERING

- 6.1 INTRODUCTION

- 6.1.1 OFFERINGS: TAX MANAGEMENT MARKET DRIVERS

- 6.2 SOLUTIONS

- 6.2.1 COMPLIANCE AND OPTIMIZATION

- 6.2.1.1 Improve operational efficiency in tax compliance and reduce tax liabilities

- 6.2.1.2 Monitor real-time regulatory compliance

- 6.2.1.3 Manage tax exemptions and certificates

- 6.2.1.4 Automate tax calculation for transactions

- 6.2.2 TAX PREPARATION & REPORTING

- 6.2.2.1 Reduce manual efforts & filing errors while ensuring compliance across jurisdictions

- 6.2.2.2 Tax return preparation & filing

- 6.2.2.3 E-audit file generation

- 6.2.2.4 Multi-jurisdiction filing support

- 6.2.3 AUDIT & RISK MANAGEMENT TOOLS

- 6.2.3.1 Enhance audit readiness with real-time data checks

- 6.2.3.2 Data validation and cleansing

- 6.2.3.3 Compliance verification

- 6.2.3.4 Automated data validation

- 6.2.4 TAX ANALYTICS TOOLS

- 6.2.4.1 Improve tax transparency with analytic tools and manage risks through data-driven insights

- 6.2.4.2 Tax data quality assurance

- 6.2.4.3 Data-driven tax decisioning

- 6.2.4.4 Real-time tax risk identification

- 6.2.5 DOCUMENT MANAGEMENT & ARCHIVING

- 6.2.5.1 Automate document organization & categorization

- 6.2.5.2 Tax document repository

- 6.2.5.3 Audit-ready document management

- 6.2.5.4 E-invoicing and certificate archiving

- 6.2.6 OTHERS

- 6.2.1 COMPLIANCE AND OPTIMIZATION

- 6.3 SERVICES

- 6.3.1 IMPLEMENTATION & SYSTEM INTEGRATION

- 6.3.1.1 Configure tax software to match organizational needs and ensure smooth deployment of tax management solutions

- 6.3.2 TAX CONFIGURATION AND ADVISORY SERVICES

- 6.3.2.1 Advise on regulatory changes and compliance strategies

- 6.3.3 SUPPORT & REGULATORY MAINTENANCE

- 6.3.3.1 Adapt tax systems to new regulatory mandates

- 6.3.1 IMPLEMENTATION & SYSTEM INTEGRATION

7 TAX MANAGEMENT MARKET, BY DEPLOYMENT MODE

- 7.1 INTRODUCTION

- 7.1.1 DEPLOYMENT MODE: TAX MANAGEMENT MARKET DRIVERS

- 7.1.2 ON-PREMISES

- 7.1.2.1 Integrates legacy systems with on-premises tax platforms

- 7.1.3 CLOUD

- 7.1.3.1 Automates tax processes with cloud-based platforms

8 TAX MANAGEMENT MARKET, BY ORGANIZATION SIZE

- 8.1 INTRODUCTION

- 8.1.1 ORGANIZATION SIZE: TAX MANAGEMENT MARKET DRIVERS

- 8.1.2 LARGE ENTERPRISES

- 8.1.2.1 Implement enterprise-scale tax automation solutions with complex financial structures

- 8.1.3 SMALL & MEDIUM SIZED ENTERPRISES

- 8.1.3.1 Seek cost-effective, easy-to-deploy tax management solutions that address essential needs

9 TAX MANAGEMENT MARKET, BY TAX TYPE

- 9.1 INTRODUCTION

- 9.1.1 TAX TYPE: TAX MANAGEMENT MARKET DRIVERS

- 9.2 INDIRECT TAXES

- 9.2.1 HELP BUSINESSES GENERATE COMPLIANT INVOICES AND FILE RETURNS

- 9.2.2 VALUE-ADDED TAX (VAT)

- 9.2.3 GOODS & SERVICES TAX (GST)

- 9.2.4 SALES TAX

- 9.2.5 CUSTOM DUTIES

- 9.2.6 OTHER INDIRECT TAXES

- 9.3 DIRECT TAXES

- 9.3.1 INTEGRATE WITH ENTERPRISE FINANCIAL SYSTEMS TO AUTOMATE DATA COLLECTION AND ENSURE ACCURATE FILINGS

- 9.3.2 CORPORATE TAX

- 9.3.3 CAPITAL GAIN TAX

- 9.3.4 PROPERTY TAX

- 9.3.5 OTHER DIRECT TAXES

10 TAX MANAGEMENT MARKET, BY VERTICAL

- 10.1 INTRODUCTION

- 10.1.1 VERTICALS: TAX MANAGEMENT MARKET DRIVERS

- 10.2 BFSI

- 10.2.1 AUTOMATE FINANCIAL TRANSACTION TAX MANAGEMENT IN BANKING AND INSURANCE

- 10.2.2 BFSI: USE CASES

- 10.2.2.1 Automated regulatory tax compliance

- 10.2.2.2 Tax audit & risk management

- 10.3 IT & TELECOM

- 10.3.1 INTEGRATE TAX MANAGEMENT SOLUTIONS WITH TELECOM BILLING SYSTEMS

- 10.3.2 IT & TELECOM: USE CASES

- 10.3.2.1 Digital service tax

- 10.3.2.2 Subscription billing taxation

- 10.3.2.3 Infrastructure asset taxation

- 10.4 MANUFACTURING

- 10.4.1 INTEGRATE TAX MANAGEMENT PLATFORMS WITH MANUFACTURING ERP SYSTEMS

- 10.4.2 MANUFACTURING: USE CASES

- 10.4.2.1 Excise duty and indirect tax compliance

- 10.4.2.2 Transfer pricing compliance

- 10.4.2.3 Tax provisioning & reporting

- 10.5 RETAIL & E-COMMERCE

- 10.5.1 IMPROVE AUDIT READINESS THROUGH REAL-TIME TAX COMPLIANCE IN RETAIL

- 10.5.2 RETAIL & E-COMMERCE: USE CASES

- 10.5.2.1 Automated sales tax calculations

- 10.5.2.2 Multi-channel sales tax integration

- 10.5.2.3 Inventory stock management

- 10.6 HEALTHCARE & LIFE SCIENCES

- 10.6.1 OPTIMIZE TAX COMPLIANCE FOR HEALTHCARE & LIFE SCIENCES

- 10.6.2 HEALTHCARE & LIFE SCIENCES: USE CASES

- 10.6.2.1 VAT exemption management for medical products

- 10.6.2.2 Cross-border tax handling

- 10.6.2.3 Hospital payroll tax processing

- 10.7 GOVERNMENT & PUBLIC SECTOR

- 10.7.1 CENTRALIZE TAX MANAGEMENT OPERATIONS ACROSS PUBLIC SECTOR DEPARTMENTS

- 10.7.2 GOVERNMENT & PUBLIC SECTOR: USE CASES

- 10.7.2.1 Real-time revenue monitoring

- 10.7.2.2 Automated tax compliance

- 10.7.2.3 E-invoicing compliance automation

- 10.8 ENERGY & UTILITIES

- 10.8.1 AUTOMATING EXCISE AND FUEL TAX COMPLIANCE IN ENERGY & UTILITIES OPERATIONS

- 10.8.2 ENERGY & UTILITIES: USE CASES

- 10.8.2.1 Excise & fuel tax automation

- 10.8.2.2 Renewable energy incentive management

- 10.8.2.3 Multi-jurisdictional tax compliance

- 10.9 OTHERS

11 TAX MANAGEMENT MARKET, BY REGION

- 11.1 INTRODUCTION

- 11.2 NORTH AMERICA

- 11.2.1 NORTH AMERICA: MARKET DRIVERS

- 11.2.2 NORTH AMERICA: MACROECONOMIC OUTLOOK

- 11.2.3 US

- 11.2.3.1 Tax software adoption to surge with e-filing growth

- 11.2.4 CANADA

- 11.2.4.1 CRA-driven digital filing to spur demand for tax management solutions

- 11.3 EUROPE

- 11.3.1 EUROPE: MARKET DRIVERS

- 11.3.2 EUROPE: MACROECONOMIC OUTLOOK

- 11.3.3 UK

- 11.3.3.1 HMRC mandates to drive cloud-based tax software adoption

- 11.3.4 GERMANY

- 11.3.4.1 Regulatory changes, digital adoption, and increased automation to drive transformation in tax administration

- 11.3.5 FRANCE

- 11.3.5.1 Fueling expansion of tax management market via e-governance innovation to drive market

- 11.3.6 ITALY

- 11.3.6.1 Rising multinational compliance demand to drive adoption of Cloud-based tax solutions

- 11.3.7 REST OF EUROPE

- 11.4 ASIA PACIFIC

- 11.4.1 ASIA PACIFIC: MARKET DRIVERS

- 11.4.2 ASIA PACIFIC: MACROECONOMIC OUTLOOK

- 11.4.3 CHINA

- 11.4.3.1 Strong government initiatives for online learning to drive market

- 11.4.4 JAPAN

- 11.4.4.1 Enhancing indirect tax management with cloud technology to drive market

- 11.4.5 INDIA

- 11.4.5.1 Accelerating digital tax compliance through TIN 2.0 and e-Filing platforms to drive market

- 11.4.6 REST OF ASIA PACIFIC

- 11.5 MIDDLE EAST & AFRICA

- 11.5.1 MIDDLE EAST & AFRICA: TAX MANAGEMENT MARKET DRIVERS

- 11.5.2 MIDDLE EAST & AFRICA: MACROECONOMIC OUTLOOK

- 11.5.3 GCC

- 11.5.3.1 Transforming tax operations through automation to boost demand for tax management

- 11.5.3.2 KSA

- 11.5.3.3 UAE

- 11.5.3.4 Rest of GCC countries

- 11.5.4 SOUTH AFRICA

- 11.5.4.1 Strengthening tax compliance through automation at SARS to drive market

- 11.5.5 REST OF MIDDLE EAST & AFRICA

- 11.6 LATIN AMERICA

- 11.6.1 LATIN AMERICA: TAX MANAGEMENT MARKET DRIVERS

- 11.6.2 LATIN AMERICA: MACROECONOMIC OUTLOOK

- 11.6.3 BRAZIL

- 11.6.3.1 Increasing regulatory demands and enhancing digital transformation goals to drive market

- 11.6.4 MEXICO

- 11.6.4.1 Need for digital invoices in real-time to push companies to adopt tax software for accurate reporting

- 11.6.5 REST OF LATIN AMERICA

12 COMPETITIVE LANDSCAPE

- 12.1 INTRODUCTION

- 12.2 KEY PLAYERS' STRATEGIES/RIGHT TO WIN

- 12.3 REVENUE ANALYSIS, 2020-2024

- 12.4 MARKET SHARE ANALYSIS, 2024

- 12.5 BRAND/PRODUCT COMPARISON

- 12.6 COMPANY VALUATION AND FINANCIAL METRICS

- 12.6.1 COMPANY VALUATION

- 12.6.2 FINANCIAL METRICS

- 12.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 12.7.1 STARS

- 12.7.2 EMERGING LEADERS

- 12.7.3 PERVASIVE PLAYERS

- 12.7.4 PARTICIPANTS

- 12.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 12.7.5.1 Company footprint

- 12.7.5.2 Region footprint

- 12.7.5.3 Offering footprint

- 12.7.5.4 Deployment mode footprint

- 12.7.5.5 Tax type footprint

- 12.7.5.6 Organization size footprint

- 12.7.5.7 Vertical footprint

- 12.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 12.8.1 PROGRESSIVE COMPANIES

- 12.8.2 RESPONSIVE COMPANIES

- 12.8.3 DYNAMIC COMPANIES

- 12.8.4 STARTING BLOCKS

- 12.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 12.8.5.1 Detailed list of key startups/SMEs

- 12.8.5.2 Competitive benchmarking of key startups/SMEs

- 12.9 COMPETITIVE SCENARIO

- 12.9.1 PRODUCT LAUNCHES

- 12.9.2 DEALS

13 COMPANY PROFILES

- 13.1 INTRODUCTION

- 13.2 KEY PLAYERS

- 13.2.1 WOLTERS KLUWER

- 13.2.1.1 Business overview

- 13.2.1.2 Products/Solutions/Services offered

- 13.2.1.3 Recent developments

- 13.2.1.3.1 Deals

- 13.2.1.4 MnM view

- 13.2.1.4.1 Right to win

- 13.2.1.4.2 Strategic choices

- 13.2.1.4.3 Weaknesses and competitive threats

- 13.2.2 THOMSON REUTERS

- 13.2.2.1 Business overview

- 13.2.2.2 Products/Solutions/Services offered

- 13.2.2.3 Recent developments

- 13.2.2.3.1 Product launches

- 13.2.2.4 MnM view

- 13.2.2.4.1 Right to win

- 13.2.2.4.2 Strategic choices

- 13.2.2.4.3 Weaknesses and competitive threats

- 13.2.3 AVALARA

- 13.2.3.1 Business overview

- 13.2.3.2 Products/Solutions/Services offered

- 13.2.3.3 Recent developments

- 13.2.3.3.1 Product launches

- 13.2.3.3.2 Deals

- 13.2.3.4 MnM view

- 13.2.3.4.1 Right to win

- 13.2.3.4.2 Strategic choices

- 13.2.3.4.3 Weaknesses and competitive threats

- 13.2.4 ADP

- 13.2.4.1 Business overview

- 13.2.4.2 Products/Solutions/Services offered

- 13.2.4.3 Recent developments

- 13.2.4.3.1 Product launches

- 13.2.4.4 MnM view

- 13.2.4.4.1 Right to win

- 13.2.4.4.2 Strategic choices

- 13.2.4.4.3 Weaknesses and competitive threats

- 13.2.5 VERTEX

- 13.2.5.1 Business overview

- 13.2.5.2 Products/Solutions/Services offered

- 13.2.5.3 Recent developments

- 13.2.5.3.1 Product launches

- 13.2.5.3.2 Deals

- 13.2.5.4 MnM view

- 13.2.5.4.1 Right to win

- 13.2.5.4.2 Strategic choices

- 13.2.5.4.3 Weaknesses and competitive threats

- 13.2.6 SOVOS

- 13.2.6.1 Business overview

- 13.2.6.2 Products/Solutions/Services offered

- 13.2.6.3 Recent developments

- 13.2.6.3.1 Product launches

- 13.2.6.3.2 Deals

- 13.2.7 INTUIT

- 13.2.7.1 Business overview

- 13.2.7.2 Products/Solutions/Services offered

- 13.2.7.3 Recent developments

- 13.2.7.3.1 Product launches

- 13.2.7.3.2 Deals

- 13.2.8 H&R BLOCK

- 13.2.8.1 Business overview

- 13.2.8.2 Products/Solutions/Services offered

- 13.2.8.2.1 Product launches

- 13.2.8.2.2 Deals

- 13.2.9 SAP

- 13.2.9.1 Business overview

- 13.2.9.2 Products/Solutions/Services offered

- 13.2.9.3 Recent developments

- 13.2.9.3.1 Deals

- 13.2.10 XERO

- 13.2.10.1 Business overview

- 13.2.10.2 Products/Solutions/Services offered

- 13.2.10.3 Recent developments

- 13.2.10.3.1 Deals

- 13.2.1 WOLTERS KLUWER

- 13.3 OTHER PLAYERS

- 13.3.1 TAXBIT

- 13.3.2 SAILOTECH

- 13.3.3 EXEMPTAX

- 13.3.4 CLEAR

- 13.3.5 DRAKE SOFTWARE

- 13.3.6 TAXCLOUD

- 13.3.7 LOVAT SOFTWARE

- 13.3.8 WEBGILITY

- 13.3.9 GLOBAL TAX MANAGEMENT INC.

- 13.3.10 TAXDOME

- 13.3.11 TAXGPT

- 13.3.12 FEBI.AI

- 13.3.13 TAXBUDDY

- 13.3.14 TAXCALC

- 13.3.15 CAPIUM

14 ADJACENT/RELATED MARKET

- 14.1 INTRODUCTION

- 14.1.1 RELATED MARKETS

- 14.1.2 LIMITATIONS

- 14.2 CLOUD ERP MARKET

- 14.3 TAX TECH MARKET

15 APPENDIX

- 15.1 DISCUSSION GUIDE

- 15.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 15.3 CUSTOMIZATION OPTIONS

- 15.4 RELATED REPORTS

- 15.5 AUTHOR DETAILS

List of Tables

- TABLE 1 USD EXCHANGE RATES, 2019-2024

- TABLE 2 FACTOR ANALYSIS

- TABLE 3 RESEARCH ASSUMPTIONS

- TABLE 4 TAX MANAGEMENT MARKET SIZE AND GROWTH, 2020-2024 (USD MILLION, YOY GROWTH %)

- TABLE 5 TAX MANAGEMENT MARKET SIZE AND GROWTH, 2025-2030 (USD MILLION, YOY GROWTH %)

- TABLE 6 ROLE OF PLAYERS IN TAX MANAGEMENT ECOSYSTEM

- TABLE 7 TAX MANAGEMENT MARKET: AVERAGE SELLING PRICE TREND, BY REGION, 2021-2025 (USD)

- TABLE 8 INDICATIVE PRICING ANALYSIS, BY OFFERING, 2025

- TABLE 9 LIST OF MAJOR PATENTS FOR TAX MANAGEMENT MARKET

- TABLE 10 NORTH AMERICA: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 11 EUROPE: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 12 ASIA PACIFIC: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 13 ROW: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 14 TAX MANAGEMENT MARKET: PORTER'S FIVE FORCES ANALYSIS

- TABLE 15 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP VERTICALS

- TABLE 16 KEY BUYING CRITERIA FOR TOP THREE VERTICALS

- TABLE 17 TAX MANAGEMENT MARKET: LIST OF KEY CONFERENCES AND EVENTS, 2025-2026

- TABLE 18 TAX MANAGEMENT MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 19 TAX MANAGEMENT MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 20 TAX MANAGEMENT MARKET, BY SOLUTION, 2020-2024 (USD MILLION)

- TABLE 21 TAX MANAGEMENT MARKET, BY SOLUTION, 2025-2030 (USD MILLION)

- TABLE 22 SOLUTIONS: TAX MANAGEMENT MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 23 SOLUTIONS: TAX MANAGEMENT MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 24 TAX COMPLIANCE & OPTIMIZATION: TAX MANAGEMENT MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 25 TAX COMPLIANCE & OPTIMIZATION: TAX MANAGEMENT MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 26 TAX PREPARATION & REPORTING: TAX MANAGEMENT MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 27 TAX PREPARATION & REPORTING: TAX MANAGEMENT MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 28 AUDIT & RISK MANAGEMENT TOOLS: TAX MANAGEMENT MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 29 AUDIT & RISK MANAGEMENT TOOLS: TAX MANAGEMENT MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 30 TAX ANALYTICS: TAX MANAGEMENT MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 31 TAX ANALYTICS: TAX MANAGEMENT MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 32 DOCUMENT MANAGEMENT & ARCHIVING: TAX MANAGEMENT MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 33 DOCUMENT MANAGEMENT & ARCHIVING: TAX MANAGEMENT MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 34 OTHERS: TAX MANAGEMENT MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 35 OTHERS: TAX MANAGEMENT MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 36 TAX MANAGEMENT MARKET, BY SERVICE, 2020-2024 (USD MILLION)

- TABLE 37 TAX MANAGEMENT MARKET, BY SERVICE, 2025-2030 (USD MILLION)

- TABLE 38 SERVICES: TAX MANAGEMENT MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 39 SERVICES: TAX MANAGEMENT MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 40 IMPLEMENTATION & SYSTEM INTEGRATION: TAX MANAGEMENT MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 41 IMPLEMENTATION & SYSTEM INTEGRATION: TAX MANAGEMENT MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 42 TAX CONFIGURATION & ADVISORY SERVICES: TAX MANAGEMENT MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 43 TAX CONFIGURATION & ADVISORY SERVICES: TAX MANAGEMENT MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 44 SUPPORT & REGULATORY MAINTENANCE: TAX MANAGEMENT MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 45 SUPPORT & REGULATORY MAINTENANCE: TAX MANAGEMENT MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 46 TAX MANAGEMENT MARKET, BY DEPLOYMENT MODE, 2020-2024 (USD MILLION)

- TABLE 47 TAX MANAGEMENT MARKET, BY DEPLOYMENT MODE, 2025-2030 (USD MILLION)

- TABLE 48 ON-PREMISES: TAX MANAGEMENT MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 49 ON-PREMISES: TAX MANAGEMENT MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 50 CLOUD: TAX MANAGEMENT MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 51 CLOUD: TAX MANAGEMENT MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 52 TAX MANAGEMENT MARKET, BY ORGANIZATION SIZE, 2020-2024 (USD MILLION)

- TABLE 53 TAX MANAGEMENT MARKET, BY ORGANIZATION SIZE, 2025-2030 (USD MILLION)

- TABLE 54 LARGE ENTERPRISES: TAX MANAGEMENT MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 55 LARGE ENTERPRISES: TAX MANAGEMENT MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 56 SMALL & MEDIUM-SIZED ENTERPRISES: TAX MANAGEMENT MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 57 SMALL & MEDIUM-SIZED ENTERPRISES: TAX MANAGEMENT MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 58 TAX MANAGEMENT MARKET, BY TAX TYPE, 2020-2024 (USD MILLION)

- TABLE 59 TAX MANAGEMENT MARKET, BY TAX TYPE, 2025-2030 (USD MILLION)

- TABLE 60 INDIRECT TAXES: TAX MANAGEMENT MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 61 INDIRECT TAXES: TAX MANAGEMENT MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 62 DIRECT TAXES: TAX MANAGEMENT MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 63 DIRECT TAXES: TAX MANAGEMENT MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 64 TAX MANAGEMENT MARKET, BY VERTICAL, 2020-2024 (USD MILLION)

- TABLE 65 TAX MANAGEMENT MARKET, BY VERTICAL, 2025-2030 (USD MILLION)

- TABLE 66 BFSI: TAX MANAGEMENT MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 67 BFSI: TAX MANAGEMENT MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 68 IT & TELECOM: TAX MANAGEMENT MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 69 IT & TELECOM: TAX MANAGEMENT MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 70 MANUFACTURING: TAX MANAGEMENT MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 71 MANUFACTURING: TAX MANAGEMENT MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 72 RETAIL & E-COMMERCE: TAX MANAGEMENT MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 73 RETAIL & E-COMMERCE: TAX MANAGEMENT MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 74 HEALTHCARE & LIFE SCIENCES: TAX MANAGEMENT MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 75 HEALTHCARE & LIFE SCIENCES: TAX MANAGEMENT MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 76 GOVERNMENT & PUBLIC SECTOR: TAX MANAGEMENT MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 77 GOVERNMENT & PUBLIC SECTOR: TAX MANAGEMENT MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 78 ENERGY & UTILITIES: TAX MANAGEMENT MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 79 ENERGY & UTILITIES: TAX MANAGEMENT MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 80 OTHERS: TAX MANAGEMENT MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 81 OTHERS: TAX MANAGEMENT MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 82 TAX MANAGEMENT MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 83 TAX MANAGEMENT MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 84 NORTH AMERICA: TAX MANAGEMENT MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 85 NORTH AMERICA: TAX MANAGEMENT MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 86 NORTH AMERICA: TAX MANAGEMENT MARKET, BY SOLUTION TYPE, 2020-2024 (USD MILLION)

- TABLE 87 NORTH AMERICA: TAX MANAGEMENT MARKET, BY SOLUTION TYPE, 2025-2030 (USD MILLION)

- TABLE 88 NORTH AMERICA: TAX MANAGEMENT MARKET, BY SERVICE, 2020-2024 (USD MILLION)

- TABLE 89 NORTH AMERICA: TAX MANAGEMENT MARKET, BY SERVICE, 2025-2030 (USD MILLION)

- TABLE 90 NORTH AMERICA: TAX MANAGEMENT MARKET, BY DEPLOYMENT MODE, 2020-2024 (USD MILLION)

- TABLE 91 NORTH AMERICA: TAX MANAGEMENT MARKET, BY DEPLOYMENT MODE, 2025-2030 (USD MILLION)

- TABLE 92 NORTH AMERICA: TAX MANAGEMENT MARKET, BY TAX TYPE, 2020-2024 (USD MILLION)

- TABLE 93 NORTH AMERICA: TAX MANAGEMENT MARKET, BY TAX TYPE, 2025-2030 (USD MILLION)

- TABLE 94 NORTH AMERICA: TAX MANAGEMENT MARKET, BY ORGANIZATION SIZE, 2020-2024 (USD MILLION)

- TABLE 95 NORTH AMERICA: TAX MANAGEMENT MARKET, BY ORGANIZATION SIZE, 2025-2030 (USD MILLION)

- TABLE 96 NORTH AMERICA: TAX MANAGEMENT MARKET, BY VERTICAL, 2020-2024 (USD MILLION)

- TABLE 97 NORTH AMERICA: TAX MANAGEMENT MARKET, BY VERTICAL, 2025-2030 (USD MILLION)

- TABLE 98 NORTH AMERICA: TAX MANAGEMENT MARKET, BY COUNTRY, 2020-2024 (USD MILLION)

- TABLE 99 NORTH AMERICA: TAX MANAGEMENT MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 100 US: TAX MANAGEMENT MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 101 US: TAX MANAGEMENT MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 102 CANADA: TAX MANAGEMENT MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 103 CANADA: TAX MANAGEMENT MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 104 EUROPE: TAX MANAGEMENT MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 105 EUROPE: TAX MANAGEMENT MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 106 EUROPE: TAX MANAGEMENT MARKET, BY SOLUTION TYPE, 2020-2024 (USD MILLION)

- TABLE 107 EUROPE: TAX MANAGEMENT MARKET, BY SOLUTION TYPE, 2025-2030 (USD MILLION)

- TABLE 108 EUROPE: TAX MANAGEMENT MARKET, BY SERVICE, 2020-2024 (USD MILLION)

- TABLE 109 EUROPE: TAX MANAGEMENT MARKET, BY SERVICE, 2025-2030 (USD MILLION)

- TABLE 110 EUROPE: TAX MANAGEMENT MARKET, BY DEPLOYMENT MODE, 2020-2024 (USD MILLION)

- TABLE 111 EUROPE: TAX MANAGEMENT MARKET, BY DEPLOYMENT MODE, 2025-2030 (USD MILLION)

- TABLE 112 EUROPE: TAX MANAGEMENT MARKET, BY TAX TYPE, 2020-2024 (USD MILLION)

- TABLE 113 EUROPE: TAX MANAGEMENT MARKET, BY TAX TYPE, 2025-2030 (USD MILLION)

- TABLE 114 EUROPE: TAX MANAGEMENT MARKET, BY ORGANIZATION SIZE, 2020-2024 (USD MILLION)

- TABLE 115 EUROPE: TAX MANAGEMENT MARKET, BY ORGANIZATION SIZE, 2025-2030 (USD MILLION)

- TABLE 116 EUROPE: TAX MANAGEMENT MARKET, BY VERTICAL, 2020-2024 (USD MILLION)

- TABLE 117 EUROPE: TAX MANAGEMENT MARKET, BY VERTICAL, 2025-2030 (USD MILLION)

- TABLE 118 EUROPE: TAX MANAGEMENT MARKET, BY COUNTRY, 2020-2024 (USD MILLION)

- TABLE 119 EUROPE: TAX MANAGEMENT MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 120 UK: TAX MANAGEMENT MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 121 UK: TAX MANAGEMENT MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 122 GERMANY: TAX MANAGEMENT MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 123 GERMANY: TAX MANAGEMENT MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 124 FRANCE: TAX MANAGEMENT MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 125 FRANCE: TAX MANAGEMENT MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 126 ITALY: TAX MANAGEMENT MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 127 ITALY: TAX MANAGEMENT MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 128 REST OF EUROPE: TAX MANAGEMENT MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 129 REST OF EUROPE: TAX MANAGEMENT MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 130 ASIA PACIFIC: TAX MANAGEMENT MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 131 ASIA PACIFIC: TAX MANAGEMENT MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 132 ASIA PACIFIC: TAX MANAGEMENT MARKET, BY SOLUTION TYPE, 2020-2024 (USD MILLION)

- TABLE 133 ASIA PACIFIC: TAX MANAGEMENT MARKET, BY SOLUTION TYPE, 2025-2030 (USD MILLION)

- TABLE 134 ASIA PACIFIC: TAX MANAGEMENT MARKET, BY SERVICE, 2020-2024 (USD MILLION)

- TABLE 135 ASIA PACIFIC: TAX MANAGEMENT MARKET, BY SERVICE, 2025-2030 (USD MILLION)

- TABLE 136 ASIA PACIFIC: TAX MANAGEMENT MARKET, BY DEPLOYMENT MODE, 2020-2024 (USD MILLION)

- TABLE 137 ASIA PACIFIC: TAX MANAGEMENT MARKET, BY DEPLOYMENT MODE, 2025-2030 (USD MILLION)

- TABLE 138 ASIA PACIFIC: TAX MANAGEMENT MARKET, BY TAX TYPE, 2020-2024 (USD MILLION)

- TABLE 139 ASIA PACIFIC: TAX MANAGEMENT MARKET, BY TAX TYPE, 2025-2030 (USD MILLION)

- TABLE 140 ASIA PACIFIC: TAX MANAGEMENT MARKET, BY ORGANIZATION SIZE, 2020-2024 (USD MILLION)

- TABLE 141 ASIA PACIFIC: TAX MANAGEMENT MARKET, BY ORGANIZATION SIZE, 2025-2030 (USD MILLION)

- TABLE 142 ASIA PACIFIC: TAX MANAGEMENT MARKET, BY VERTICAL, 2020-2024 (USD MILLION)

- TABLE 143 ASIA PACIFIC: TAX MANAGEMENT MARKET, BY VERTICAL, 2025-2030 (USD MILLION)

- TABLE 144 ASIA PACIFIC: TAX MANAGEMENT MARKET, BY COUNTRY, 2020-2024 (USD MILLION)

- TABLE 145 ASIA PACIFIC: TAX MANAGEMENT MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 146 CHINA: TAX MANAGEMENT MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 147 CHINA: TAX MANAGEMENT MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 148 JAPAN: TAX MANAGEMENT MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 149 JAPAN: TAX MANAGEMENT MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 150 INDIA: TAX MANAGEMENT MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 151 INDIA: TAX MANAGEMENT MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 152 REST OF ASIA PACIFIC: TAX MANAGEMENT MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 153 REST OF ASIA PACIFIC: TAX MANAGEMENT MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 154 MIDDLE EAST & AFRICA: TAX MANAGEMENT MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 155 MIDDLE EAST & AFRICA: TAX MANAGEMENT MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 156 MIDDLE EAST & AFRICA: TAX MANAGEMENT MARKET, BY SOLUTION TYPE, 2020-2024 (USD MILLION)

- TABLE 157 MIDDLE EAST & AFRICA: TAX MANAGEMENT MARKET, BY SOLUTION TYPE, 2025-2030 (USD MILLION)

- TABLE 158 MIDDLE EAST & AFRICA: TAX MANAGEMENT MARKET, BY SERVICE, 2020-2024 (USD MILLION)

- TABLE 159 MIDDLE EAST & AFRICA: TAX MANAGEMENT MARKET, BY SERVICE, 2025-2030 (USD MILLION)

- TABLE 160 MIDDLE EAST & AFRICA: TAX MANAGEMENT MARKET, BY DEPLOYMENT MODE, 2020-2024 (USD MILLION)

- TABLE 161 MIDDLE EAST & AFRICA: TAX MANAGEMENT MARKET, BY DEPLOYMENT MODE, 2025-2030 (USD MILLION)

- TABLE 162 MIDDLE EAST & AFRICA: TAX MANAGEMENT MARKET, BY TAX TYPE, 2020-2024 (USD MILLION)

- TABLE 163 MIDDLE EAST & AFRICA: TAX MANAGEMENT MARKET, BY TAX TYPE, 2025-2030 (USD MILLION)

- TABLE 164 MIDDLE EAST & AFRICA: TAX MANAGEMENT MARKET, BY ORGANIZATION SIZE, 2020-2024 (USD MILLION)

- TABLE 165 MIDDLE EAST & AFRICA: TAX MANAGEMENT MARKET, BY ORGANIZATION SIZE, 2025-2030 (USD MILLION)

- TABLE 166 MIDDLE EAST & AFRICA: TAX MANAGEMENT MARKET, BY VERTICAL, 2020-2024 (USD MILLION)

- TABLE 167 MIDDLE EAST & AFRICA: TAX MANAGEMENT MARKET, BY VERTICAL, 2025-2030 (USD MILLION)

- TABLE 168 MIDDLE EAST & AFRICA: TAX MANAGEMENT MARKET, BY COUNTRY, 2020-2024 (USD MILLION)

- TABLE 169 MIDDLE EAST & AFRICA: TAX MANAGEMENT MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 170 GCC: TAX MANAGEMENT MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 171 GCC: TAX MANAGEMENT MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 172 GCC COUNTRIES: TAX MANAGEMENT MARKET, BY COUNTRY, 2020-2024 (USD MILLION)

- TABLE 173 GCC COUNTRIES: TAX MANAGEMENT MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 174 KSA: TAX MANAGEMENT MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 175 KSA: TAX MANAGEMENT MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 176 UAE: TAX MANAGEMENT MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 177 UAE: TAX MANAGEMENT MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 178 REST OF GCC: TAX MANAGEMENT MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 179 REST OF GCC: TAX MANAGEMENT MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 180 SOUTH AFRICA: TAX MANAGEMENT MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 181 SOUTH AFRICA: TAX MANAGEMENT MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 182 REST OF MIDDLE EAST & AFRICA: TAX MANAGEMENT MARKET, BY OFFERINGS, 2020-2024 (USD MILLION)

- TABLE 183 REST OF MIDDLE EAST & AFRICA TAX MANAGEMENT MARKET, BY OFFERINGS, 2025-2030 (USD MILLION)

- TABLE 184 LATIN AMERICA: TAX MANAGEMENT MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 185 LATIN AMERICA: TAX MANAGEMENT MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 186 LATIN AMERICA: TAX MANAGEMENT MARKET, BY SOLUTION TYPE, 2020-2024 (USD MILLION)

- TABLE 187 LATIN AMERICA: TAX MANAGEMENT MARKET, BY SOLUTION TYPE, 2025-2030 (USD MILLION)

- TABLE 188 LATIN AMERICA: TAX MANAGEMENT MARKET, BY SERVICE, 2020-2024 (USD MILLION)

- TABLE 189 LATIN AMERICA: TAX MANAGEMENT MARKET, BY SERVICE, 2025-2030 (USD MILLION)

- TABLE 190 LATIN AMERICA: TAX MANAGEMENT MARKET, BY DEPLOYMENT MODE, 2020-2024 (USD MILLION)

- TABLE 191 LATIN AMERICA: TAX MANAGEMENT MARKET, BY DEPLOYMENT MODE, 2025-2030 (USD MILLION)

- TABLE 192 LATIN AMERICA: TAX MANAGEMENT MARKET, BY TAX TYPE, 2020-2024 (USD MILLION)

- TABLE 193 LATIN AMERICA: TAX MANAGEMENT MARKET, BY TAX TYPE, 2025-2030 (USD MILLION)

- TABLE 194 LATIN AMERICA: TAX MANAGEMENT MARKET, BY ORGANIZATION SIZE, 2020-2024 (USD MILLION)

- TABLE 195 LATIN AMERICA: TAX MANAGEMENT MARKET, BY ORGANIZATION SIZE, 2025-2030 (USD MILLION)

- TABLE 196 LATIN AMERICA: TAX MANAGEMENT MARKET, BY VERTICAL, 2020-2024 (USD MILLION)

- TABLE 197 LATIN AMERICA: TAX MANAGEMENT MARKET, BY VERTICAL, 2025-2030 (USD MILLION)

- TABLE 198 LATIN AMERICA: TAX MANAGEMENT MARKET, BY COUNTRY, 2020-2024 (USD MILLION)

- TABLE 199 LATIN AMERICA: TAX MANAGEMENT MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 200 BRAZIL: TAX MANAGEMENT MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 201 BRAZIL: TAX MANAGEMENT MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 202 MEXICO: TAX MANAGEMENT MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 203 MEXICO: TAX MANAGEMENT MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 204 REST OF LATIN AMERICA: TAX MANAGEMENT MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 205 REST OF LATIN AMERICA: TAX MANAGEMENT MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 206 OVERVIEW OF STRATEGIES ADOPTED BY KEY PLAYERS IN TAX MANAGEMENT MARKET, 2023-2025

- TABLE 207 TAX MANAGEMENT MARKET: DEGREE OF COMPETITION, 2024

- TABLE 208 TAX MANAGEMENT MARKET: REGION FOOTPRINT

- TABLE 209 TAX MANAGEMENT MARKET: OFFERING FOOTPRINT

- TABLE 210 TAX MANAGEMENT MARKET: DEPLOYMENT MODE FOOTPRINT

- TABLE 211 TAX MANAGEMENT MARKET: TAX TYPE FOOTPRINT

- TABLE 212 TAX MANAGEMENT MARKET: ORGANIZATION SIZE FOOTPRINT

- TABLE 213 TAX MANAGEMENT MARKET: VERTICAL FOOTPRINT

- TABLE 214 TAX MANAGEMENT MARKET: LIST OF KEY STARTUPS/SMES

- TABLE 215 TAX MANAGEMENT MARKET: COMPETITIVE BENCHMARKING OF STARTUPS/SMES

- TABLE 216 TAX MANAGEMENT MARKET: PRODUCT LAUNCHES, FEBRUARY 2023-JUNE 2025

- TABLE 217 TAX MANAGEMENT MARKET: DEALS, FEBRUARY 2023-JUNE 2025

- TABLE 218 WOLTERS KLUWER: COMPANY OVERVIEW

- TABLE 219 WOLTERS KLUWER: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 220 WOLTERS KLUWER: DEALS

- TABLE 221 THOMSON REUTERS: COMPANY OVERVIEW

- TABLE 222 THOMSON REUTERS: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 223 THOMSON REUTERS: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 224 AVALARA: COMPANY OVERVIEW

- TABLE 225 AVALARA: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 226 AVALARA: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 227 AVALARA: DEALS

- TABLE 228 ADP: COMPANY OVERVIEW

- TABLE 229 ADP: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 230 ADP: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 231 VERTEX: COMPANY OVERVIEW

- TABLE 232 VERTEX: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 233 VERTEX: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 234 VERTEX: DEALS

- TABLE 235 SOVOS: COMPANY OVERVIEW

- TABLE 236 SOVOS: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 237 SOVOS: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 238 SOVOS: DEALS

- TABLE 239 INTUIT: COMPANY OVERVIEW

- TABLE 240 INTUIT: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 241 INTUIT: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 242 INTUIT: DEALS

- TABLE 243 H&R BLOCK: COMPANY OVERVIEW

- TABLE 244 H&R BLOCK: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 245 H&R BLOCK: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 246 H&R BLOCK: DEALS

- TABLE 247 SAP: COMPANY OVERVIEW

- TABLE 248 SAP: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 249 SAP: DEALS

- TABLE 250 XERO: COMPANY OVERVIEW

- TABLE 251 XERO: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 252 XERO: DEALS

- TABLE 253 CLOUD ERP MARKET, BY OFFERINGS, 2019-2023 (USD MILLION)

- TABLE 254 CLOUD ERP MARKET, BY OFFERINGS, 2024-2029 (USD MILLION)

- TABLE 255 CLOUD ERP MARKET, BY DEPLOYMENT TYPE, 2019-2023 (USD MILLION)

- TABLE 256 CLOUD ERP MARKET, BY DEPLOYMENT TYPE, 2024-2029 (USD MILLION)

- TABLE 257 TAX TECH MARKET, BY OFFERINGS, 2019-2023 (USD MILLION)

- TABLE 258 TAX TECH MARKET, BY OFFERINGS, 2024-2030 (USD MILLION)

- TABLE 259 TAX TECH MARKET, BY DEPLOYMENT MODE, 2019-2023 (USD MILLION)

- TABLE 260 TAX TECH MARKET, BY DEPLOYMENT MODE, 2024-2030 (USD MILLION)

List of Figures

- FIGURE 1 TAX MANAGEMENT MARKET: RESEARCH DESIGN

- FIGURE 2 BREAKUP OF PRIMARY INTERVIEWS, BY COMPANY TYPE, DESIGNATION, AND REGION

- FIGURE 3 TAX MANAGEMENT MARKET: TOP-DOWN AND BOTTOM-UP APPROACHES

- FIGURE 4 MARKET SIZE ESTIMATION METHODOLOGY: TOP-DOWN APPROACH

- FIGURE 5 MARKET SIZE ESTIMATION METHODOLOGY: BOTTOM-UP APPROACH

- FIGURE 6 TAX MANAGEMENT MARKET: RESEARCH FLOW

- FIGURE 7 MARKET SIZE ESTIMATION METHODOLOGY: SUPPLY-SIDE ANALYSIS

- FIGURE 8 MARKET SIZE ESTIMATION METHODOLOGY: BOTTOM-UP APPROACH FROM SUPPLY SIDE - COLLECTIVE REVENUE OF VENDORS

- FIGURE 9 TAX MANAGEMENT MARKET: DEMAND-SIDE APPROACH

- FIGURE 10 RESEARCH LIMITATIONS

- FIGURE 11 GLOBAL TAX MANAGEMENT MARKET TO WITNESS SIGNIFICANT GROWTH

- FIGURE 12 FASTEST-GROWING SEGMENTS IN TAX MANAGEMENT MARKET, 2025-2030

- FIGURE 13 TAX MANAGEMENT MARKET: REGIONAL SNAPSHOT

- FIGURE 14 GROWING COMPLEXITY IN TAX LAWS ACROSS JURISDICTIONS TO ADOPT TAX MANAGEMENT SOLUTIONS FOR ACCURATE COMPLIANCE AND REPORTING

- FIGURE 15 SERVICES SEGMENT TO ACCOUNT FOR LARGEST MARKET SHARE DURING FORECAST PERIOD

- FIGURE 16 CLOUD SEGMENT TO ACCOUNT FOR LARGEST MARKET SHARE DURING FORECAST PERIOD

- FIGURE 17 INDIRECT TAX SEGMENT TO ACCOUNT FOR LARGEST MARKET SHARE DURING FORECAST PERIOD

- FIGURE 18 LARGE ENTERPRISES SEGMENT TO ACCOUNT FOR LARGEST MARKET SHARE DURING FORECAST PERIOD

- FIGURE 19 BFSI VERTICAL TO ACCOUNT FOR LARGEST MARKET SHARE DURING FORECAST PERIOD

- FIGURE 20 ASIA PACIFIC TO EMERGE AS BEST MARKET FOR INVESTMENT IN NEXT FIVE YEARS

- FIGURE 21 TAX MANAGEMENT MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

- FIGURE 22 TAX MANAGEMENT MARKET: ECOSYSTEM ANALYSIS

- FIGURE 23 TAX MANAGEMENT MARKET: SUPPLY CHAIN ANALYSIS

- FIGURE 24 TAX MANAGEMENT MARKET: AVERAGE SELLING PRICE TREND, BY REGION, 2021-2025

- FIGURE 25 NUMBER OF PATENTS PUBLISHED, 2014-2024

- FIGURE 26 TAX MANAGEMENT MARKET: PORTER'S FIVE FORCES ANALYSIS

- FIGURE 27 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR VERTICALS

- FIGURE 28 KEY BUYING CRITERIA FOR TOP THREE VERTICALS

- FIGURE 29 TAX MANAGEMENT MARKET: TRENDS AND DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- FIGURE 30 INVESTMENT AND FUNDING SCENARIO OF MAJOR TAX MANAGEMENT COMPANIES

- FIGURE 31 SOLUTIONS SEGMENT TO DOMINATE MARKET DURING FORECAST PERIOD

- FIGURE 32 CLOUD SEGMENT TO LEAD MARKET DURING FORECAST PERIOD

- FIGURE 33 LARGE ENTERPRISES SEGMENT TO HOLD LARGEST MARKET SIZE DURING FORECAST PERIOD

- FIGURE 34 INDIRECT TAX TYPE SEGMENT TO DOMINATE MARKET DURING FORECAST PERIOD

- FIGURE 35 BFSI SEGMENT TO DOMINATE MARKET DURING FORECAST PERIOD

- FIGURE 36 NORTH AMERICA TO HOLD LARGEST MARKET SIZE DURING FORECAST PERIOD

- FIGURE 37 NORTH AMERICA: MARKET SNAPSHOT

- FIGURE 38 ASIA PACIFIC: MARKET SNAPSHOT

- FIGURE 39 TAX MANAGEMENT MARKET: REVENUE ANALYSIS OF KEY PLAYERS, 2020-2024

- FIGURE 40 TAX MANAGEMENT MARKET: MARKET SHARE ANALYSIS, 2024

- FIGURE 41 TAX MANAGEMENT MARKET: BRAND PRODUCT COMPARISON

- FIGURE 42 COMPANY VALUATION OF KEY VENDORS

- FIGURE 43 FINANCIAL METRICS OF KEY VENDORS

- FIGURE 44 YEAR-TO-DATE (YTD) PRICE TOTAL RETURN AND FIVE-YEAR STOCK BETA OF KEY VENDORS

- FIGURE 45 COMPANY EVALUATION MATRIX FOR KEY PLAYERS: CRITERIA WEIGHTAGE

- FIGURE 46 TAX MANAGEMENT MARKET: COMPANY EVALUATION MATRIX (KEY PLAYERS), 2024

- FIGURE 47 TAX MANAGEMENT MARKET: COMPANY FOOTPRINT

- FIGURE 48 EVALUATION MATRIX FOR STARTUPS/SMES: CRITERIA WEIGHTAGE

- FIGURE 49 TAX MANAGEMENT MARKET: COMPANY EVALUATION MATRIX (STARTUPS/SMES), 2024

- FIGURE 50 WOLTERS KLUWER: COMPANY SNAPSHOT

- FIGURE 51 THOMSON REUTERS: COMPANY SNAPSHOT

- FIGURE 52 ADP: COMPANY SNAPSHOT

- FIGURE 53 VERTEX: COMPANY SNAPSHOT

- FIGURE 54 INTUIT: COMPANY SNAPSHOT

- FIGURE 55 H&R BLOCK: COMPANY SNAPSHOT

- FIGURE 56 SAP: COMPANY SNAPSHOT

- FIGURE 57 XERO: COMPANY SNAPSHOT