|

市场调查报告书

商品编码

1794024

全球门市场按材料、产品类型、应用、机制、用途和地区分類的预测(至 2030 年)Doors Market by Material, Product Type, Mode of Application, Mechanism (Sliding Doors, Swinging Doors, Folding Doors, and Overhead Doors), Application (Residential and Non-residential), and Region - Global Forecast to 2030 |

||||||

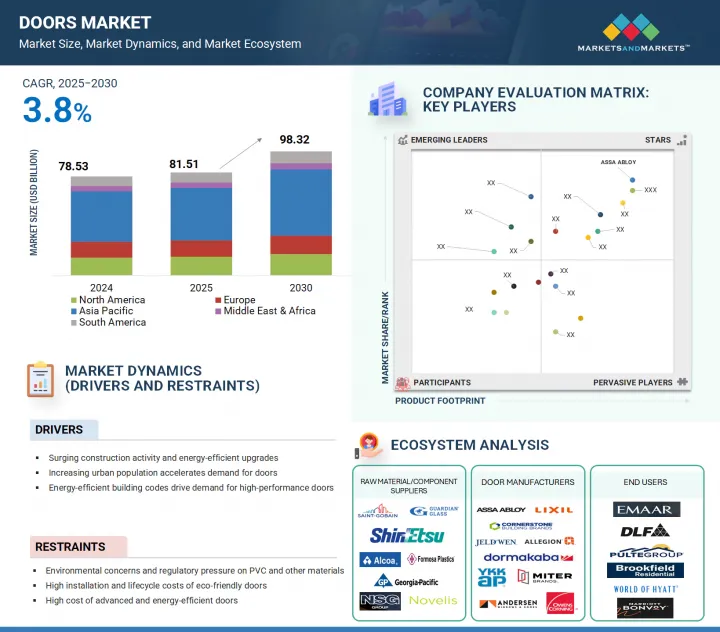

全球门市场预计将从 2025 年的 815.1 亿美元成长到 2030 年的 983.2 亿美元,复合年增长率为 3.8%。

| 调查范围 | |

|---|---|

| 调查年份 | 2021-2030 |

| 基准年 | 2024 |

| 预测期 | 2025-2030 |

| 单元 | 金额(百万美元)、数量(吨) |

| 部分 | 材料、产品类型、机制、施工方法、应用、地区 |

| 目标区域 | 北美、亚太地区、欧洲、中东和非洲、南美 |

在住宅、商业和工业领域对安全、节能和高性能解决方案日益增长的需求的推动下,门市场持续扩张。现代门的设计着重长寿命、隔热、隔音和耐候性,使其适用于室内和室外应用。先进的门系统通常具有防火功能,配有自动锁并采用可回收或永续材料。由于人们越来越重视安全、智慧存取和永续性,需求也在成长。精密製造和客製化生产方法正在提高市场上的产品品质和设计适应性。现代门实现了两个承诺:提高居住者的舒适度和美观度,同时提供安全性和结构性能的机会。门越来越被依赖为建筑组件,因为除了提供有意义的外观和功能外,构造和饰面也越来越依赖基于性能的法令遵循。

“到2024年,新建筑将占据门业市场的最大份额。”

到2024年,新建建筑将占据门业市场的最大份额,这得益于已开发市场和新兴市场的住宅、商业和基础设施建设的不断增长。新计划成长的关键驱动因素包括都市化的加速、强劲的住房市场以及政府对建设经济适用房的奖励。这导致公共和私营部门的建筑活动、建筑风格和建筑设计的增加。传统上,建筑物的设计要符合能源效率、消防安全和无障碍设施等现代标准。永续性目标和标准进一步推动了创新材料和技术在建筑设计中的使用。强劲的全球建设活动维持了门业新建筑领域的主导地位。

“到2024年,室内门将占据门市场的大部分份额。”

受住宅和商业建筑及活性化活动兴起的推动,室内门在2024年占据了门市场的最大份额。室内门对于保护隐私、隔音和分隔空间至关重要,是住宅和职场的基本功能。室内门的流行得益于其种类繁多的材料、款式和饰面,这些都符合现代设计偏好。都市化的加速、可支配收入的增加以及生活方式的改变,推动了人们对美观实用的室内门的需求。复合木材、玻璃和PVC等材料的创新,以及智慧家庭的功能性和永续性趋势,正在巩固室内门在整个门市场中的主导地位。

“2024年亚太地区将主导门市场。”

预计到2024年,亚太地区将成为全球最大的门市场,这得益于中国、印度和东南亚等国家快速的都市化、经济成长和基础建设。印度「总理个人住房计划」(PMAY)等经济适用房计划以及中国的城市更新计划正在刺激该地区住宅和商业的增长,从而增加对门的需求。德里-孟买工业走廊等工业走廊以及智慧城市计划正在进一步加速先进门系统的普及。

该地区还受益于低廉的生产成本、高素质的劳动力以及不断增长的外国建筑和房地产投资。此外,对节能安全门的需求,例如高层建筑的安全门和商业领域的自动门,正在推动市场成长。老旧都市区的重建日益增多,以及新建现代化零售、饭店和医疗设施的兴建,也进一步巩固了该地区作为亚太地区领先门市场的地位。

本报告对全球门市场进行了分析,提供了关键驱动因素和限制因素、竞争格局和未来趋势的资讯。

目录

第一章 引言

第二章调查方法

第三章执行摘要

第四章 主要发现

- 门业市场对企业来说极具吸引力的机会

- 亚太门市场(按产品类型和国家/地区划分)

- 按材质分類的门市场

- 按产品类型分類的门市场

- 门市场:按机制

- 以安装方式分類的门市场

- 门市场按应用

- 各国门市场

第五章市场概述

- 介绍

- 市场动态

- 驱动程式

- 抑制因素

- 机会

- 任务

- 影响客户业务的趋势和中断

- 生态系分析

- 价值链分析

- 关税和监管格局

- 海关分析(HS编码:441820)

- 监管机构、政府机构和其他组织

- 主要法规

- 定价分析

- 贸易分析

- 出口情形(HS 编码 441820)

- 进口情形(HS 编码 441820)

- 技术分析

- 主要技术

- 互补技术

- 邻近技术

- 专利分析

- 介绍

- 调查方法

- 门市场专利分析

- 大型会议及活动

- 案例研究分析

- DEUREN 蜂蜜橡木 TAVOLE 前门,带来清新的乡村魅力

- FedEx 设施透过改用 PERFORMAX MAXSPEED 橡胶门每年可节省 50,000 美元

- EFAFLEX PS 系列高速门增强停车场安全性

- 投资金筹措场景

- 生成式人工智慧/人工智慧对门市场的影响

- 波特五力分析

- 主要相关利益者和采购标准

- 宏观经济分析

- 介绍

- GDP趋势与预测

- 2025年美国关税对门市场的影响

- 介绍

- 主要关税税率

- 价格影响分析

- 对国家的影响

- 对终端产业的影响

第六章门市场按材质

- 介绍

- 木头

- 玻璃

- 金属

- 塑胶

- 复合材料

第七章 门市场(按机制)

- 介绍

- 摇摆门

- 滑动门

- 织户

- 高架大门

- 其他机制门

第八章门市场按产品类型

- 介绍

- 室内门

- 外门

第九章门市场依安装方式

- 介绍

- 新建筑

- 售后市场

第 10 章门市场应用

- 介绍

- 住房

- 独立式住宅

- 多用户住宅

- 非住宅

- 医院

- 办公室

- 饭店

- 政府大楼

- 教育机构

- 零售

- 其他非住宅用途

第十一章 门市场区域分布

- 介绍

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 印尼

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 法国

- 义大利

- 英国

- 俄罗斯

- 其他欧洲国家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东和非洲

- 海湾合作委员会国家

- 南非

- 其他中东和非洲地区

第十二章竞争格局

- 概述

- 主要参与企业的策略

- 市场占有率分析

- 收益分析

- 公司估值及财务指标

- 产品/品牌比较

- 企业评估矩阵:主要企业(2024年)

- 公司评估矩阵:Start-Ups/中小企业(2024 年)

- 竞争场景

第十三章:公司简介

- 主要企业

- ASSA ABLOY

- LIXIL CORPORATION

- CORNERSTONE BUILDING BRANDS, INC.

- JELD-WEN, INC.

- ALLEGION PLC

- DORMAKABA GROUP

- YKK AP

- OWENS CORNING

- ANDERSEN CORPORATION

- MITER BRANDS

- 其他公司

- PELLA CORPORATION

- SIMPSON DOOR COMPANY

- BOON EDAM

- REYNAERS ALUMINIUM

- NOVOFERM GMBH

- FENESTA BUILDING SYSTEMS

- HORMANN

- WERU GMBH

- THERMA-TRU CORP.

- MARVIN

- PDS DOORSETS

- SGM WINDOW MANUFACTURING LIMITED

- VINYLGUARD WINDOW & DOOR SYSTEMS LTD.

- PROVIA LLC

- KOLBE WINDOWS & DOORS

第14章:相邻市场与相关市场

- 介绍

- 限制

- 门窗市场

第十五章 附录

The doors market is projected to grow from USD 81.51 billion in 2025 to USD 98.32 billion in 2030, at a CAGR of 3.8%.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD Million) and Volume (Ton) |

| Segments | Material, Product Type, Mechanism, Mode of Application, Application, and Region |

| Regions covered | North America, Asia Pacific, Europe, Middle East & Africa, and South America |

The doors market is witnessing consistent expansion driven by increasing demand for secure, energy-efficient, and high-performance solutions in residential, commercial, and industrial sectors. Contemporary doors are engineered for longevity, thermal insulation, acoustic attenuation, and weather resistance, rendering them appropriate for both internal and external applications. Sophisticated door systems typically made from fire-resistant materials possess automatic locking and utilize recyclable or sustainable materials. They are increasingly in demand due to the increased focus on safety, intelligent access, and sustainability. Product quality and the adaptability of design have improved in the market due to precision manufacturing and bespoke production methods. Modern doors satisfy two aspects: they improve occupants' comfort and aesthetics and provide opportunities for security and structural performance. Doors are becoming increasingly relied on as building components, as construction and finishes are becoming more reliant on performance-based compliance regulations in combination with providing meaningful appearance and functionality.

"New constructions accounted for the largest share in the doors market in 2024."

In 2024, new construction accounted for the largest share of the doors market, growing due to an increase in residential, commercial, and infrastructure development in both advanced and emerging markets. The main drivers of increases in projects for new constructions are the accelerating rates of urbanization, the strength of the housing market, and government incentives to build affordable housing. In response to these conditions, there is an increase in public and private sector building activity, building styles, and architectural design, in which the building has traditionally been designed to meet modern standards for energy efficiency, fire safety, and accessibility. Sustainability goals and criteria further incentivize the use of innovative materials and technologies in building designs. The new construction segment's dominance in the doors industry is maintained by the strong global construction activity.

"The interior doors segment accounted for a larger share of the doors market in 2024."

In 2024, the interior doors segment held the largest share of the doors market, driven by rising residential and commercial construction, along with increased renovation activity. Interior doors are essential for privacy, sound insulation, and spatial separation, making them a fundamental feature in homes and workplaces. Their popularity is enhanced by a diverse array of materials, styles, and finishes that align with contemporary design preferences. Rising urbanization, rising disposable incomes, and changes in lifestyle have amplified the need for aesthetically pleasing and practical interior doors. Innovations in materials such as composite wood, glass, and PVC, coupled with smart-home functionalities and sustainability tendencies, persist in reinforcing the segment's supremacy in the overall doors market.

"Asia Pacific dominated the regional market for doors in 2024."

Asia Pacific was the largest market for the doors market in 2024, supported by rapid urbanization, economic growth, and developed infrastructure in countries such as China, India, and Southeast Asia. Increased residential and commercial growth in the region, highlighted by affordable housing schemes such as Pradhan Mantri Awas Yojana (PMAY) in India and urban renewal projects in China, has also led to high demand for doors. Industrial corridors such as the Delhi-Mumbai Industrial Corridor and smart city projects have further accelerated the use of advanced door systems.

The area also benefits from low production costs, an educated workforce, and foreign investment growing in construction and real estate. Furthermore, demand for energy-efficient and secure doors, including safety-rated doors for high-rise buildings and automated doors for commercial areas, is fueling the market growth. Urban renovation in aging city areas and the growth of new construction of modern retail, hospitality, and healthcare properties further entrench Asia Pacific's status as the top regional door market.

By Company Type: Tier 1: 25%, Tier 2: 42%, and Tier 3: 33%

By Designation: C-level Executives: 20%, Directors: 30%, and Other Designations: 50%

By Region: North America: 20%, Europe: 10%, Asia Pacific: 40%, South America: 10%, and Middle East & Africa 20%

Notes: Other designations include sales, marketing, and product managers.

Tier 1: >USD 1 Billion; Tier 2: USD 500 million: 1 Billion; and Tier 3: <USD 500 million

Companies Covered: ASSA ABLOY (Sweden), LIXIL Corporation (Japan), Cornerstone Building Brands, Inc. (US), JELD-WEN, Inc. (US), Allegion plc (Ireland), dormakaba Group (Switzerland), YKK AP (Japan), Owens Corning (US), Andersen Corporation (US), and Miter Brands (US) are covered in the report.

The study includes an in-depth competitive analysis of these key players in the doors market, as well as their company profiles, recent developments, and key market strategies.

Research Coverage

This research report categorizes the doors market based on material (Wood, Glass, Metal, Plastic, and Composite), product type (Interior doors and exterior doors), mechanism (Sliding doors, Swinging doors, Folding doors, Overhead doors, and Others), mode of application (New Construction and Aftermarket), application (Residential and Non-residential) and Region (Asia Pacific, North America, Europe, South America, and Middle East & Africa). The report's scope covers detailed information regarding the drivers, restraints, challenges, and opportunities influencing the growth of the doors market. A detailed analysis of the key industry players has been done to provide insights into their business overview, products offered, and key strategies, such as partnerships, collaborations, mergers, acquisitions, product launches, and expansions, associated with the doors market. This report covers a competitive analysis of upcoming startups in the doors market ecosystem.

Reasons to Buy the Report

The report will offer the market leaders/new entrants information on the closest approximations of the revenue numbers for the overall doors market and the subsegments. This report will help stakeholders understand the competitive landscape, gain more insights into positioning their businesses better, and plan suitable go-to-market strategies. The report will help stakeholders understand the pulse of the market and provide them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following points:

- Analysis of key drivers (surging construction activity and energy-efficient upgrades fuel market growth, increasing urban population accelerates demand for doors, and energy-efficient building codes drive demand for high-performance doors ), restraints (environmental concerns and regulatory pressure on PVC and other materials, high installation and lifecycle costs of eco-friendly doors, and High cost of advanced and energy-efficient doors), opportunities (renovation surge and infrastructure investment fuel demand for advanced door solutions and leveraging smart technologies and sustainable innovations to shape the future of doors), and challenges (meeting environmental expectations and regulatory requirements and Vulnerability to global supply chain disruptions)

- Product Development/Innovation: Detailed insights into upcoming technologies, research & development activities, and product & service launches in the doors market

- Market Development: Comprehensive information about profitable markets-the report analyzes the doors market across varied regions

- Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the doors market.

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players such as ASSA ABLOY (Sweden), LIXIL Corporation (Japan), Cornerstone Building Brands, Inc. (US), JELD-WEN, Inc. (US), Allegion plc (Ireland), dormakaba Group (Switzerland), YKK AP (Japan), Owens Corning (US), Andersen Corporation (US), and Miter Brands (US), among others

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.3.5 UNITS CONSIDERED

- 1.4 LIMITATIONS

- 1.5 STAKEHOLDERS

- 1.6 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY DATA

- 2.1.1.1 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Key data from primary sources

- 2.1.2.2 Key industry insights

- 2.1.1 SECONDARY DATA

- 2.2 MARKET SIZE ESTIMATION

- 2.3 BASE NUMBER CALCULATION

- 2.3.1 DEMAND-SIDE APPROACH

- 2.3.2 SUPPLY-SIDE APPROACH

- 2.4 MARKET FORECAST APPROACH

- 2.4.1 SUPPLY SIDE

- 2.4.2 DEMAND SIDE

- 2.5 DATA TRIANGULATION

- 2.6 FACTOR ANALYSIS

- 2.7 RESEARCH ASSUMPTIONS

- 2.8 RESEARCH LIMITATIONS AND RISK ASSESSMENT

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN DOORS MARKET

- 4.2 ASIA PACIFIC: DOORS MARKET, BY PRODUCT TYPE AND COUNTRY

- 4.3 DOORS MARKET, BY MATERIAL

- 4.4 DOORS MARKET, BY PRODUCT TYPE

- 4.5 DOORS MARKET, BY MECHANISM

- 4.6 DOORS MARKET, BY MODE OF APPLICATION

- 4.7 DOORS MARKET, BY APPLICATION

- 4.8 DOORS MARKET, BY COUNTRY

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Surging construction activity and energy-efficient upgrades

- 5.2.1.2 Increase in urban population

- 5.2.1.3 Energy-efficient building codes drive demand for high-performance doors

- 5.2.2 RESTRAINTS

- 5.2.2.1 Environmental concerns and regulatory pressure on PVC and other materials

- 5.2.2.2 High installation and lifecycle costs of eco-friendly doors

- 5.2.2.3 High cost of advanced and energy-efficient doors

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Renovation surge and infrastructure investment fuel demand for advanced door solutions

- 5.2.3.2 Leveraging smart technologies and sustainable innovations to shape future of doors

- 5.2.4 CHALLENGES

- 5.2.4.1 Meeting environmental expectations and regulatory requirements

- 5.2.4.2 Vulnerability to global supply chain disruptions

- 5.2.1 DRIVERS

- 5.3 TRENDS AND DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

- 5.3.1 TRENDS AND DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 VALUE CHAIN ANALYSIS

- 5.6 TARIFF AND REGULATORY LANDSCAPE

- 5.6.1 TARIFF ANALYSIS (HS CODE: 441820)

- 5.6.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.6.3 KEY REGULATIONS

- 5.6.3.1 Fire Safety (England) Regulations 2022

- 5.6.3.2 NFPA 80 - Standard for Fire Doors and Other Opening Protectives

- 5.6.3.3 BHMA Door Assemblies Standards (ANSI A156 Series)

- 5.6.3.4 ASTM E2074 - Standard Test Method for Fire Tests of Door Assemblies

- 5.6.4 PRICING ANALYSIS

- 5.6.4.1 Average selling price trend of key materials, by key player

- 5.6.4.2 Average selling price of key materials, by region

- 5.7 TRADE ANALYSIS

- 5.7.1 EXPORT SCENARIO (HS CODE 441820)

- 5.7.2 IMPORT SCENARIO (HS CODE 441820)

- 5.8 TECHNOLOGY ANALYSIS

- 5.8.1 KEY TECHNOLOGIES

- 5.8.1.1 Energy-efficient glazing

- 5.8.1.2 Smart door technology

- 5.8.2 COMPLEMENTARY TECHNOLOGIES

- 5.8.2.1 Building information modeling (BIM)

- 5.8.2.2 Acoustic and soundproofing technology

- 5.8.3 ADJACENT TECHNOLOGIES

- 5.8.3.1 Invisible frame door technology with ultra-thin, eco-friendly panels

- 5.8.1 KEY TECHNOLOGIES

- 5.9 PATENT ANALYSIS

- 5.9.1 INTRODUCTION

- 5.9.2 METHODOLOGY

- 5.9.3 PATENT ANALYSIS FOR DOORS MARKET

- 5.10 KEY CONFERENCES AND EVENTS

- 5.11 CASE STUDY ANALYSIS

- 5.11.1 TRANSFORMING RURAL CHARM WITH DEUREN'S TAVOLE FRONT DOOR IN HONEY OAK

- 5.11.2 FEDEX FACILITY SAVES USD 50,000 ANNUALLY BY SWITCHING TO PERFORMAX MAXSPEED RUBBER DOORS

- 5.11.3 ENHANCING PARKING FACILITY SECURITY WITH EFAFLEX'S PS SERIES HIGH-SPEED DOORS

- 5.12 INVESTMENT AND FUNDING SCENARIO

- 5.13 IMPACT OF GEN AI/AI ON DOORS MARKET

- 5.13.1 INTRODUCTION

- 5.14 PORTER'S FIVE FORCES ANALYSIS

- 5.14.1 THREAT OF NEW ENTRANTS

- 5.14.2 THREAT OF SUBSTITUTES

- 5.14.3 BARGAINING POWER OF SUPPLIERS

- 5.14.4 BARGAINING POWER OF BUYERS

- 5.14.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.15 KEY STAKEHOLDERS AND BUYING CRITERIA

- 5.15.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 5.15.2 BUYING CRITERIA

- 5.16 MACROECONOMIC ANALYSIS

- 5.16.1 INTRODUCTION

- 5.16.2 GDP TRENDS AND FORECASTS

- 5.17 IMPACT OF 2025 US TARIFF ON DOORS MARKET

- 5.17.1 INTRODUCTION

- 5.17.2 KEY TARIFF RATES

- 5.17.3 PRICE IMPACT ANALYSIS

- 5.17.4 IMPACT ON COUNTRY/REGION

- 5.17.4.1 US

- 5.17.4.2 Canada

- 5.17.4.3 EU

- 5.17.4.4 China

- 5.17.5 END-USE INDUSTRY IMPACT

6 DOORS MARKET, BY MATERIAL

- 6.1 INTRODUCTION

- 6.2 WOOD

- 6.2.1 WOOD HELPS BALANCE AESTHETICS, INSULATION, AND SUSTAINABILITY

- 6.3 GLASS

- 6.3.1 RISE IN DEMAND FOR GLASS DOORS IN OFFICE ENVIRONMENTS

- 6.4 METAL

- 6.4.1 STRENGTH, SECURITY, AND PERFORMANCE OF METAL-SUITABLE FOR MODERN BUILDINGS

- 6.5 PLASTIC

- 6.5.1 LIGHTWEIGHT EFFICIENCY WITH LOW-MAINTENANCE VERSATILITY OFFERED BY PLASTIC

- 6.6 COMPOSITE

- 6.6.1 GROWTH IN ADOPTION OF COMPOSITE DOORS FOR ENHANCED STRENGTH AND NOISE REDUCTION

7 DOORS MARKET, BY MECHANISM

- 7.1 INTRODUCTION

- 7.2 SWINGING DOORS

- 7.2.1 ENDURING APPEAL WITH NEXT-GENERATION ENHANCEMENTS TO DRIVE MARKET

- 7.3 SLIDING DOORS

- 7.3.1 STREAMLINED DESIGN WITH ENERGY-EFFICIENT INNOVATIONS IN SLIDING DOORS

- 7.4 FOLDING DOORS

- 7.4.1 ARCHITECTURAL FLEXIBILITY OFFERED BY FOLDING DOORS FOR INDOOR-OUTDOOR LIVING

- 7.5 OVERHEAD DOORS

- 7.5.1 OVERHEAD DOORS: INDUSTRIAL STRENGTH MEETS SMART SUSTAINABILITY

- 7.6 DOORS OF OTHER MECHANISMS

8 DOORS MARKET, BY PRODUCT TYPE

- 8.1 INTRODUCTION

- 8.2 INTERIOR DOORS

- 8.2.1 GROWING CUSTOMIZATION, MATERIAL INNOVATION, AND LIFESTYLE TRENDS AFFECT DEMAND FOR INTERIOR DOORS

- 8.3 EXTERIOR DOORS

- 8.3.1 TECHNOLOGICAL ADVANCEMENTS AND SAFETY STANDARDS: KEY FOR EXTERIOR DOORS

9 DOORS MARKET, BY MODE OF APPLICATION

- 9.1 INTRODUCTION

- 9.2 NEW CONSTRUCTION

- 9.2.1 FOCUS ON ENERGY EFFICIENCY, COST SAVINGS, AND COMPLIANCE OFFERED BY NEW CONSTRUCTIONS

- 9.3 AFTERMARKET

- 9.3.1 SMART RETROFITS, CUSTOMIZATION, AND ENERGY REBATES TO FUEL DEMAND IN AFTERMARKET

10 DOORS MARKET, BY APPLICATION

- 10.1 INTRODUCTION

- 10.2 RESIDENTIAL

- 10.2.1 SINGLE-FAMILY RESIDENCES

- 10.2.1.1 Rise in investment in premium exterior doors aimed at enhancing security

- 10.2.2 MULTI-FAMILY RESIDENCES

- 10.2.2.1 Growth in adoption of green building practices

- 10.2.1 SINGLE-FAMILY RESIDENCES

- 10.3 NON-RESIDENTIAL

- 10.3.1 HOSPITALS

- 10.3.1.1 Demand for hygienic and functional doors for healthcare environments

- 10.3.2 OFFICES

- 10.3.2.1 Need to enhance security and access control with advanced door solutions

- 10.3.3 HOTELS

- 10.3.3.1 Strengthening security amid rising safety concerns in hospitality

- 10.3.4 GOVERNMENT BUILDINGS

- 10.3.4.1 Importance of rigorous security measures in governmental spaces

- 10.3.5 EDUCATIONAL INSTITUTIONS

- 10.3.5.1 Need to prioritize safety and durability in door selection

- 10.3.6 RETAIL

- 10.3.6.1 Security and efficiency risks offered by foot traffic and open layouts

- 10.3.7 OTHER NON-RESIDENTIAL APPLICATIONS

- 10.3.1 HOSPITALS

11 DOORS MARKET, BY REGION

- 11.1 INTRODUCTION

- 11.2 ASIA PACIFIC

- 11.2.1 CHINA

- 11.2.1.1 Urban renewal and green building policies to fuel demand for high-performance doors

- 11.2.2 INDIA

- 11.2.2.1 Real estate growth and smart urban development to propel demand

- 11.2.3 JAPAN

- 11.2.3.1 Urban redevelopment and demographic trends to drive growth

- 11.2.4 AUSTRALIA

- 11.2.4.1 Infrastructure investment and aging demographics to drive growth

- 11.2.5 INDONESIA

- 11.2.5.1 Urban development and sectoral growth to fuel demand growth

- 11.2.6 REST OF ASIA PACIFIC

- 11.2.1 CHINA

- 11.3 NORTH AMERICA

- 11.3.1 US

- 11.3.1.1 Steady construction activity and code-compliant to demand drive growth

- 11.3.2 CANADA

- 11.3.2.1 Construction and infrastructure investment to propel growth

- 11.3.3 MEXICO

- 11.3.3.1 Construction surge to fuel doors market expansion

- 11.3.1 US

- 11.4 EUROPE

- 11.4.1 GERMANY

- 11.4.1.1 Climate-neutral building targets and rising demand for energy-efficient retrofits to drive growth

- 11.4.2 FRANCE

- 11.4.2.1 Recovery signals amid slowdown and green building push to propel market

- 11.4.3 ITALY

- 11.4.3.1 Shift toward public investment and green renovation to fuel demand

- 11.4.4 UK

- 11.4.4.1 Energy-efficiency grants to fuel demand for high-performance solutions

- 11.4.5 RUSSIA

- 11.4.5.1 Government-led energy reforms and smart city initiatives to drive demand

- 11.4.6 REST OF EUROPE

- 11.4.1 GERMANY

- 11.5 SOUTH AMERICA

- 11.5.1 BRAZIL

- 11.5.1.1 Surging housing development and government support to fuel demand

- 11.5.2 ARGENTINA

- 11.5.2.1 Localized infrastructure and residential recovery to power Argentina's door market

- 11.5.3 REST OF SOUTH AMERICA

- 11.5.1 BRAZIL

- 11.6 MIDDLE EAST & AFRICA

- 11.6.1 GCC COUNTRIES

- 11.6.1.1 Saudi Arabia

- 11.6.1.1.1 Government initiatives and strategic investments to drive demand

- 11.6.1.2 UAE

- 11.6.1.2.1 Mega projects and urban growth to drive market

- 11.6.1.3 Rest of GCC Countries

- 11.6.1.1 Saudi Arabia

- 11.6.2 SOUTH AFRICA

- 11.6.2.1 Urbanization and infrastructure momentum to drive market

- 11.6.3 REST OF MIDDLE EAST & AFRICA

- 11.6.1 GCC COUNTRIES

12 COMPETITIVE LANDSCAPE

- 12.1 OVERVIEW

- 12.2 KEY PLAYER STRATEGIES

- 12.3 MARKET SHARE ANALYSIS

- 12.4 REVENUE ANALYSIS

- 12.5 COMPANY VALUATION AND FINANCIAL METRICS

- 12.6 PRODUCT/BRAND COMPARISON

- 12.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 12.7.1 STARS

- 12.7.2 EMERGING LEADERS

- 12.7.3 PERVASIVE PLAYERS

- 12.7.4 PARTICIPANTS

- 12.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 12.7.5.1 Company footprint

- 12.7.5.2 Regional footprint

- 12.7.5.3 Product type footprint

- 12.7.5.4 Material footprint

- 12.7.5.5 Mechanism footprint

- 12.7.5.6 Mode of application footprint

- 12.7.5.7 Application footprint

- 12.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 12.8.1 PROGRESSIVE COMPANIES

- 12.8.2 RESPONSIVE COMPANIES

- 12.8.3 DYNAMIC COMPANIES

- 12.8.4 STARTING BLOCKS

- 12.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 12.8.5.1 Detailed list of key startups/SMEs

- 12.8.5.2 Competitive benchmarking of key startups/SMEs

- 12.9 COMPETITIVE SCENARIO

- 12.9.1 PRODUCT LAUNCHES

- 12.9.2 DEALS

- 12.9.3 EXPANSIONS

13 COMPANY PROFILES

- 13.1 KEY PLAYERS

- 13.1.1 ASSA ABLOY

- 13.1.1.1 Business overview

- 13.1.1.2 Products offered

- 13.1.1.3 Recent developments

- 13.1.1.3.1 Product launches

- 13.1.1.3.2 Deals

- 13.1.1.4 MnM view

- 13.1.1.4.1 Right to win

- 13.1.1.4.2 Strategic choices

- 13.1.1.4.3 Weaknesses & competitive threats

- 13.1.2 LIXIL CORPORATION

- 13.1.2.1 Business overview

- 13.1.2.2 Products offered

- 13.1.2.3 Recent developments

- 13.1.2.3.1 Product launches

- 13.1.2.3.2 Deals

- 13.1.2.3.3 Expansions

- 13.1.2.4 MnM view

- 13.1.2.4.1 Right to win

- 13.1.2.4.2 Strategic choices

- 13.1.2.4.3 Weaknesses & competitive threats

- 13.1.3 CORNERSTONE BUILDING BRANDS, INC.

- 13.1.3.1 Business overview

- 13.1.3.2 Products offered

- 13.1.3.3 Recent developments

- 13.1.3.3.1 Product launches

- 13.1.3.3.2 Deals

- 13.1.3.4 MnM view

- 13.1.3.4.1 Right to win

- 13.1.3.4.2 Strategic choices

- 13.1.3.4.3 Weaknesses & competitive threats

- 13.1.4 JELD-WEN, INC.

- 13.1.4.1 Business overview

- 13.1.4.2 Products offered

- 13.1.4.3 Recent developments

- 13.1.4.3.1 Product launches

- 13.1.4.3.2 Deals

- 13.1.4.3.3 Expansions

- 13.1.4.4 MnM view

- 13.1.4.4.1 Right to win

- 13.1.4.4.2 Strategic choices

- 13.1.4.4.3 Weaknesses & competitive threats

- 13.1.5 ALLEGION PLC

- 13.1.5.1 Business overview

- 13.1.5.2 Products offered

- 13.1.5.3 Recent developments

- 13.1.5.3.1 Deals

- 13.1.5.4 MnM view

- 13.1.5.4.1 Right to win

- 13.1.5.4.2 Strategic choices

- 13.1.5.4.3 Weaknesses & competitive threats

- 13.1.6 DORMAKABA GROUP

- 13.1.6.1 Business overview

- 13.1.6.2 Products offered

- 13.1.6.3 Recent developments

- 13.1.6.3.1 Product launches

- 13.1.6.3.2 Deals

- 13.1.6.3.3 Expansions

- 13.1.6.4 MnM view

- 13.1.7 YKK AP

- 13.1.7.1 Business overview

- 13.1.7.2 Products offered

- 13.1.7.3 Recent developments

- 13.1.7.3.1 Product launches

- 13.1.7.3.2 Deals

- 13.1.7.3.3 Expansions

- 13.1.7.4 MnM view

- 13.1.8 OWENS CORNING

- 13.1.8.1 Business overview

- 13.1.8.2 Products offered

- 13.1.8.3 Recent developments

- 13.1.8.3.1 Deals

- 13.1.8.4 MnM view

- 13.1.9 ANDERSEN CORPORATION

- 13.1.9.1 Business overview

- 13.1.9.2 Products offered

- 13.1.9.3 Recent developments

- 13.1.9.3.1 Product launches

- 13.1.9.3.2 Deals

- 13.1.9.3.3 Expansions

- 13.1.9.4 MnM view

- 13.1.10 MITER BRANDS

- 13.1.10.1 Business overview

- 13.1.10.2 Products offered

- 13.1.10.3 Recent developments

- 13.1.10.3.1 Product launches

- 13.1.10.3.2 Deals

- 13.1.10.3.3 Expansions

- 13.1.10.4 MnM view

- 13.1.1 ASSA ABLOY

- 13.2 OTHER PLAYERS

- 13.2.1 PELLA CORPORATION

- 13.2.2 SIMPSON DOOR COMPANY

- 13.2.3 BOON EDAM

- 13.2.4 REYNAERS ALUMINIUM

- 13.2.5 NOVOFERM GMBH

- 13.2.6 FENESTA BUILDING SYSTEMS

- 13.2.7 HORMANN

- 13.2.8 WERU GMBH

- 13.2.9 THERMA-TRU CORP.

- 13.2.10 MARVIN

- 13.2.11 PDS DOORSETS

- 13.2.12 SGM WINDOW MANUFACTURING LIMITED

- 13.2.13 VINYLGUARD WINDOW & DOOR SYSTEMS LTD.

- 13.2.14 PROVIA LLC

- 13.2.15 KOLBE WINDOWS & DOORS

14 ADJACENT & RELATED MARKET

- 14.1 INTRODUCTION

- 14.2 LIMITATIONS

- 14.2.1 DOORS & WINDOWS MARKET

- 14.2.1.1 Market definition

- 14.2.1.2 Doors & windows market, by product

- 14.2.1.3 Doors & windows market, by construction type

- 14.2.1.4 Doors & windows market, by material

- 14.2.1.5 Doors & windows market, by end-use industry

- 14.2.1.6 Doors & windows market, by region

- 14.2.1 DOORS & WINDOWS MARKET

15 APPENDIX

- 15.1 DISCUSSION GUIDE

- 15.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 15.3 CUSTOMIZATION OPTIONS

- 15.4 RELATED REPORTS

- 15.5 AUTHOR DETAILS

List of Tables

- TABLE 1 INCLUSIONS AND EXCLUSIONS

- TABLE 2 RESEARCH LIMITATIONS AND RISK ASSESSMENT

- TABLE 3 MONTHLY NEW RESIDENTIAL CONSTRUCTION, MAY 2025

- TABLE 4 ROLES OF COMPANIES IN DOORS ECOSYSTEM

- TABLE 5 TARIFF SCENARIO FOR HS CODE 441820-COMPLIANT PRODUCTS, BY COUNTRY, 2024 (%)

- TABLE 6 NORTH AMERICA: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, INDUSTRY ASSOCIATIONS, AND OTHER ORGANIZATIONS

- TABLE 7 EUROPE: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, INDUSTRY ASSOCIATIONS, AND OTHER ORGANIZATIONS

- TABLE 8 ASIA PACIFIC: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, INDUSTRY ASSOCIATIONS, AND OTHER ORGANIZATIONS

- TABLE 9 MIDDLE EAST & AFRICA: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, INDUSTRY ASSOCIATIONS, AND OTHER ORGANIZATIONS

- TABLE 10 SOUTH AMERICA: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, INDUSTRY ASSOCIATIONS, AND OTHER ORGANIZATIONS

- TABLE 11 AVERAGE SELLING PRICE OF DOOR MATERIALS, BY KEY PLAYER, 2024 (USD/UNITS)

- TABLE 12 AVERAGE SELLING PRICE OF KEY DOOR MATERIALS, BY REGION, 2021-2024 ( USD/UNIT)

- TABLE 13 EXPORT DATA RELATED TO HS CODE 441820-COMPLIANT PRODUCTS, BY COUNTRY, 2020-2024 (USD THOUSAND)

- TABLE 14 IMPORT DATA RELATED TO HS CODE 441820-COMPLIANT PRODUCTS, BY COUNTRY, 2020-2024 (USD THOUSAND)

- TABLE 15 DOORS MARKET: LIST OF KEY PATENTS, 2022-2024

- TABLE 16 DOORS MARKET: DETAILED LIST OF CONFERENCES AND EVENTS, 2025-2026

- TABLE 17 PORTER'S FIVE FORCES ANALYSIS

- TABLE 18 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR KEY APPLICATIONS

- TABLE 19 KEY BUYING CRITERIA FOR KEY APPLICATIONS

- TABLE 21 DOORS MARKET, BY MATERIAL, 2021-2023 (USD MILLION)

- TABLE 22 DOORS MARKET, BY MATERIAL, 2024-2030 (USD MILLION)

- TABLE 23 DOORS MARKET, BY MATERIAL, 2021-2023 (MILLION UNITS)

- TABLE 24 DOORS MARKET, BY MATERIAL, 2024-2030 (MILLION UNITS)

- TABLE 25 DOORS MARKET, BY MECHANISM, 2021-2023 (USD MILLION)

- TABLE 26 DOORS MARKET, BY MECHANISM, 2024-2030 (USD MILLION)

- TABLE 27 DOORS MARKET, BY MECHANISM, 2021-2023 (MILLION UNITS)

- TABLE 28 DOORS MARKET, BY MECHANISM, 2024-2030 (MILLION UNITS)

- TABLE 29 DOORS MARKET, BY PRODUCT TYPE, 2021-2023 (USD MILLION)

- TABLE 30 DOORS MARKET, BY PRODUCT TYPE, 2024-2030 (USD MILLION)

- TABLE 31 DOORS MARKET, BY PRODUCT TYPE, 2021-2023 (MILLION UNITS)

- TABLE 32 DOORS MARKET, BY PRODUCT TYPE, 2024-2030 (MILLION UNITS)

- TABLE 33 DOORS MARKET, BY MODE OF APPLICATION, 2021-2023 (USD MILLION)

- TABLE 34 DOORS MARKET, BY MODE OF APPLICATION, 2024-2030 (USD MILLION)

- TABLE 35 DOORS MARKET, BY MODE OF APPLICATION, 2021-2023 (MILLION UNITS)

- TABLE 36 DOORS MARKET, BY MODE OF APPLICATION, 2024-2030 (MILLION UNITS)

- TABLE 37 DOORS MARKET, BY APPLICATION, 2021-2023 (USD MILLION)

- TABLE 38 DOORS MARKET, BY APPLICATION, 2024-2030 (USD MILLION)

- TABLE 39 DOORS MARKET, BY APPLICATION, 2021-2023 (MILLION UNITS)

- TABLE 40 DOORS MARKET, BY APPLICATION, 2024-2030 (MILLION UNITS)

- TABLE 41 DOORS MARKET, BY REGION, 2021-2023 (USD MILLION)

- TABLE 42 DOORS MARKET, REGION, 2024-2030 (USD MILLION)

- TABLE 43 DOORS MARKET, BY REGION, 2021-2023 (MILLION UNITS)

- TABLE 44 DOORS MARKET, BY REGION, 2024-2030 (MILLION UNITS)

- TABLE 45 ASIA PACIFIC: DOORS MARKET, BY COUNTRY, 2021-2023 (USD MILLION)

- TABLE 46 ASIA PACIFIC: DOORS MARKET, BY COUNTRY, 2024-2030 (USD MILLION)

- TABLE 47 ASIA PACIFIC: DOORS MARKET, BY COUNTRY, 2021-2023 (MILLION UNITS)

- TABLE 48 ASIA PACIFIC: DOORS MARKET, BY COUNTRY, 2024-2030 (MILLION UNITS)

- TABLE 49 ASIA PACIFIC: DOORS MARKET, BY MATERIAL, 2021-2023 (USD MILLION)

- TABLE 50 ASIA PACIFIC: DOORS MARKET, BY MATERIAL, 2024-2030 (USD MILLION)

- TABLE 51 ASIA PACIFIC: DOORS MARKET, BY MATERIAL, 2021-2023 (MILLION UNITS)

- TABLE 52 ASIA PACIFIC: DOORS MARKET, BY MATERIAL, 2024-2030 (MILLION UNITS)

- TABLE 53 ASIA PACIFIC: DOORS MARKET, BY MECHANISM, 2021-2023 (USD MILLION)

- TABLE 54 ASIA PACIFIC: DOORS MARKET, BY MECHANISM, 2024-2030 (USD MILLION)

- TABLE 55 ASIA PACIFIC: DOORS MARKET, BY MECHANISM, 2021-2023 (MILLION UNITS)

- TABLE 56 ASIA PACIFIC: DOORS MARKET, BY MECHANISM, 2024-2030 (MILLION UNITS)

- TABLE 57 ASIA PACIFIC: DOORS MARKET, BY PRODUCT TYPE, 2021-2023 (USD MILLION)

- TABLE 58 ASIA PACIFIC: DOORS MARKET, BY PRODUCT TYPE, 2024-2030 (USD MILLION)

- TABLE 59 ASIA PACIFIC: DOORS MARKET, BY PRODUCT TYPE, 2021-2023 (MILLION UNITS)

- TABLE 60 ASIA PACIFIC: DOORS MARKET, BY PRODUCT TYPE, 2024-2030 (MILLION UNITS)

- TABLE 61 ASIA PACIFIC: DOORS MARKET, BY APPLICATION, 2021-2023 (USD MILLION)

- TABLE 62 ASIA PACIFIC: DOORS MARKET, BY APPLICATION, 2024-2030 (USD MILLION)

- TABLE 63 ASIA PACIFIC: DOORS MARKET, BY APPLICATION, 2021-2023 (MILLION UNITS)

- TABLE 64 ASIA PACIFIC: DOORS MARKET, BY APPLICATION, 2024-2030 (MILLION UNITS)

- TABLE 65 ASIA PACIFIC: DOORS MARKET, BY MODE OF APPLICATION, 2021-2023 (USD MILLION)

- TABLE 66 ASIA PACIFIC: DOORS MARKET, BY MODE OF APPLICATION, 2024-2030 (USD MILLION)

- TABLE 67 ASIA PACIFIC: DOORS MARKET, BY MODE OF APPLICATION, 2021-2023 (MILLION UNITS)

- TABLE 68 ASIA PACIFIC: DOORS MARKET, BY MODE OF APPLICATION, 2024-2030 (MILLION UNITS)

- TABLE 69 CHINA: DOORS MARKET, BY MATERIAL, 2021-2023 (USD MILLION)

- TABLE 70 CHINA: DOORS MARKET, BY MATERIAL, 2024-2030 (USD MILLION)

- TABLE 71 CHINA: DOORS MARKET, BY MATERIAL, 2021-2023 (MILLION UNITS)

- TABLE 72 CHINA: DOORS MARKET, BY MATERIAL, 2024-2030 (MILLION UNITS)

- TABLE 73 CHINA: DOORS MARKET, BY MECHANISM, 2021-2023 (USD MILLION)

- TABLE 74 CHINA: DOORS MARKET, BY MECHANISM, 2024-2030 (USD MILLION)

- TABLE 75 CHINA: DOORS MARKET, BY MECHANISM, 2021-2023 (MILLION UNITS)

- TABLE 76 CHINA: DOORS MARKET, BY MECHANISM, 2024-2030 (MILLION UNITS)

- TABLE 77 INDIA: DOORS MARKET, BY MATERIAL, 2021-2023 (USD MILLION)

- TABLE 78 INDIA: DOORS MARKET, BY MATERIAL, 2024-2030 (USD MILLION)

- TABLE 79 INDIA: DOORS MARKET, BY MATERIAL, 2021-2023 (MILLION UNITS)

- TABLE 80 INDIA: DOORS MARKET, BY MATERIAL, 2024-2030 (MILLION UNITS)

- TABLE 81 INDIA: DOORS MARKET, BY MECHANISM, 2021-2023 (USD MILLION)

- TABLE 82 INDIA: DOORS MARKET, BY MECHANISM, 2024-2030 (USD MILLION)

- TABLE 83 INDIA: DOORS MARKET, BY MECHANISM, 2021-2023 (MILLION UNITS)

- TABLE 84 INDIA: DOORS MARKET, BY MECHANISM, 2024-2030 (MILLION UNITS)

- TABLE 85 JAPAN: DOORS MARKET, BY MATERIAL, 2021-2023 (USD MILLION)

- TABLE 86 JAPAN: DOORS MARKET, BY MATERIAL, 2024-2030 (USD MILLION)

- TABLE 87 JAPAN: DOORS MARKET, BY MATERIAL, 2021-2023 (MILLION UNITS)

- TABLE 88 JAPAN: DOORS MARKET, BY MATERIAL, 2024-2030 (MILLION UNITS)

- TABLE 89 JAPAN: DOORS MARKET, BY MECHANISM, 2021-2023 (USD MILLION)

- TABLE 90 JAPAN: DOORS MARKET, BY MECHANISM, 2024-2030 (USD MILLION)

- TABLE 91 JAPAN: DOORS MARKET, BY MECHANISM, 2021-2023 (MILLION UNITS)

- TABLE 92 JAPAN: DOORS MARKET, BY MECHANISM, 2024-2030 (MILLION UNITS)

- TABLE 93 AUSTRALIA: DOORS MARKET, BY MATERIAL, 2021-2023 (USD MILLION)

- TABLE 94 AUSTRALIA: DOORS MARKET, BY MATERIAL, 2024-2030 (USD MILLION)

- TABLE 95 AUSTRALIA: DOORS MARKET, BY MATERIAL, 2021-2023 (MILLION UNITS)

- TABLE 96 AUSTRALIA: DOORS MARKET, BY MATERIAL, 2024-2030 (MILLION UNITS)

- TABLE 97 AUSTRALIA: DOORS MARKET, BY MECHANISM, 2021-2023 (USD MILLION)

- TABLE 98 AUSTRALIA: DOORS MARKET, BY MECHANISM, 2024-2030 (USD MILLION)

- TABLE 99 AUSTRALIA: DOORS MARKET, BY MECHANISM, 2021-2023 (MILLION UNITS)

- TABLE 100 AUSTRALIA: DOORS MARKET, BY MECHANISM, 2024-2030 (MILLION UNITS)

- TABLE 101 INDONESIA: DOORS MARKET, BY MATERIAL, 2021-2023 (USD MILLION)

- TABLE 102 INDONESIA: DOORS MARKET, BY MATERIAL, 2024-2030 (USD MILLION)

- TABLE 103 INDONESIA: DOORS MARKET, BY MATERIAL, 2021-2023 (MILLION UNITS)

- TABLE 104 INDONESIA: DOORS MARKET, BY MATERIAL, 2024-2030 (MILLION UNITS)

- TABLE 105 INDONESIA: DOORS MARKET, BY MECHANISM, 2021-2023 (USD MILLION)

- TABLE 106 INDONESIA: DOORS MARKET, BY MECHANISM, 2024-2030 (USD MILLION)

- TABLE 107 INDONESIA: DOORS MARKET, BY MECHANISM, 2021-2023 (MILLION UNITS)

- TABLE 108 INDONESIA: DOORS MARKET, BY MECHANISM, 2024-2030 (MILLION UNITS)

- TABLE 109 REST OF ASIA PACIFIC: DOORS MARKET, BY MATERIAL, 2021-2023 (USD MILLION)

- TABLE 110 REST OF ASIA PACIFIC: DOORS MARKET, BY MATERIAL, 2024-2030 (USD MILLION)

- TABLE 111 REST OF ASIA PACIFIC: DOORS MARKET, BY MATERIAL, 2021-2023 (MILLION UNITS)

- TABLE 112 REST OF ASIA PACIFIC: DOORS MARKET, BY MATERIAL, 2024-2030 (MILLION UNITS)

- TABLE 113 REST OF ASIA PACIFIC: DOORS MARKET, BY MECHANISM, 2021-2023 (USD MILLION)

- TABLE 114 REST OF ASIA PACIFIC: DOORS MARKET, BY MECHANISM, 2024-2030 (USD MILLION)

- TABLE 115 REST OF ASIA PACIFIC: DOORS MARKET, BY MECHANISM, 2021-2023 (MILLION UNITS)

- TABLE 116 REST OF ASIA PACIFIC: DOORS MARKET, BY MECHANISM, 2024-2030 (MILLION UNITS)

- TABLE 117 NORTH AMERICA: DOORS MARKET, BY COUNTRY, 2021-2023 (USD MILLION)

- TABLE 118 NORTH AMERICA: DOORS MARKET, BY COUNTRY, 2024-2030 (USD MILLION)

- TABLE 119 NORTH AMERICA: DOORS MARKET, BY COUNTRY, 2021-2023 (MILLION UNITS)

- TABLE 120 NORTH AMERICA: DOORS MARKET, BY COUNTRY, 2024-2030 (MILLION UNITS)

- TABLE 121 NORTH AMERICA: DOORS MARKET, BY MATERIAL, 2021-2023 (USD MILLION)

- TABLE 122 NORTH AMERICA: DOORS MARKET, BY MATERIAL, 2024-2030 (USD MILLION)

- TABLE 123 NORTH AMERICA: DOORS MARKET, BY MATERIAL, 2021-2023 (MILLION UNITS)

- TABLE 124 NORTH AMERICA: DOORS MARKET, BY MATERIAL, 2024-2030 (MILLION UNITS)

- TABLE 125 NORTH AMERICA: DOORS MARKET, BY MECHANISM, 2021-2023 (USD MILLION)

- TABLE 126 NORTH AMERICA: DOORS MARKET, BY MECHANISM, 2024-2030 (USD MILLION)

- TABLE 127 NORTH AMERICA: DOORS MARKET, BY MECHANISM, 2021-2023 (MILLION UNITS)

- TABLE 128 NORTH AMERICA: DOORS MARKET, BY MECHANISM, 2024-2030 (MILLION UNITS)

- TABLE 129 NORTH AMERICA: DOORS MARKET, BY PRODUCT TYPE, 2021-2023 (USD MILLION)

- TABLE 130 NORTH AMERICA: DOORS MARKET, BY PRODUCT TYPE, 2024-2030 (USD MILLION)

- TABLE 131 NORTH AMERICA: DOORS MARKET, BY PRODUCT TYPE, 2021-2023 (MILLION UNITS)

- TABLE 132 NORTH AMERICA: DOORS MARKET, BY PRODUCT TYPE, 2024-2030 (MILLION UNITS)

- TABLE 133 NORTH AMERICA: DOORS MARKET, BY APPLICATION, 2021-2023 (USD MILLION)

- TABLE 134 NORTH AMERICA: DOORS MARKET, BY APPLICATION, 2024-2030 (USD MILLION)

- TABLE 135 NORTH AMERICA: DOORS MARKET, BY APPLICATION, 2021-2023 (MILLION UNITS)

- TABLE 136 NORTH AMERICA: DOORS MARKET, BY APPLICATION, 2024-2030 (MILLION UNITS)

- TABLE 137 NORTH AMERICA: DOORS MARKET, BY MODE OF APPLICATION, 2021-2023 (USD MILLION)

- TABLE 138 NORTH AMERICA: DOORS MARKET, BY MODE OF APPLICATION, 2024-2030 (USD MILLION)

- TABLE 139 NORTH AMERICA: DOORS MARKET, BY MODE OF APPLICATION, 2021-2023 (MILLION UNITS)

- TABLE 140 NORTH AMERICA: DOORS MARKET, BY MODE OF APPLICATION, 2024-2030 (MILLION UNITS)

- TABLE 141 US: DOORS MARKET, BY MATERIAL, 2021-2023 (USD MILLION)

- TABLE 142 US: DOORS MARKET, BY MATERIAL, 2024-2030 (USD MILLION)

- TABLE 143 US: DOORS MARKET, BY MATERIAL, 2021-2023 (MILLION UNITS)

- TABLE 144 US: DOORS MARKET, BY MATERIAL, 2024-2030 (MILLION UNITS)

- TABLE 145 US: DOORS MARKET, BY MECHANISM, 2021-2023 (USD MILLION)

- TABLE 146 US: DOORS MARKET, BY MECHANISM, 2024-2030 (USD MILLION)

- TABLE 147 US: DOORS MARKET, BY MECHANISM, 2021-2023 (MILLION UNITS)

- TABLE 148 US: DOORS MARKET, BY MECHANISM, 2024-2030 (MILLION UNITS)

- TABLE 149 CANADA: DOORS MARKET, BY MATERIAL, 2021-2023 (USD MILLION)

- TABLE 150 CANADA: DOORS MARKET, BY MATERIAL, 2024-2030 (USD MILLION)

- TABLE 151 CANADA: DOORS MARKET, BY MATERIAL, 2021-2023 (MILLION UNITS)

- TABLE 152 CANADA: DOORS MARKET, BY MATERIAL, 2024-2030 (MILLION UNITS)

- TABLE 153 CANADA: DOORS MARKET, BY MECHANISM, 2021-2023 (USD MILLION)

- TABLE 154 CANADA: DOORS MARKET, BY MECHANISM, 2024-2030 (USD MILLION)

- TABLE 155 CANADA: DOORS MARKET, BY MECHANISM, 2021-2023 (MILLION UNITS)

- TABLE 156 CANADA: DOORS MARKET, BY MECHANISM, 2024-2030 (MILLION UNITS)

- TABLE 157 MEXICO: DOORS MARKET, BY MATERIAL, 2021-2023 (USD MILLION)

- TABLE 158 MEXICO: DOORS MARKET, BY MATERIAL, 2024-2030 (USD MILLION)

- TABLE 159 MEXICO: DOORS MARKET, BY MATERIAL, 2021-2023 (MILLION UNITS)

- TABLE 160 MEXICO: DOORS MARKET, BY MATERIAL, 2024-2030 (MILLION UNITS)

- TABLE 161 MEXICO: DOORS MARKET, BY MECHANISM, 2021-2023 (USD MILLION)

- TABLE 162 MEXICO: DOORS MARKET, BY MECHANISM, 2024-2030 (USD MILLION)

- TABLE 163 MEXICO: DOORS MARKET, BY MECHANISM, 2021-2023 (MILLION UNITS)

- TABLE 164 MEXICO: DOORS MARKET, BY MECHANISM, 2024-2030 (MILLION UNITS)

- TABLE 165 EUROPE: DOORS MARKET, BY COUNTRY, 2021-2023 (USD MILLION)

- TABLE 166 EUROPE: DOORS MARKET, BY COUNTRY, 2024-2030 (USD MILLION)

- TABLE 167 EUROPE: DOORS MARKET, BY COUNTRY, 2021-2023 (MILLION UNITS)

- TABLE 168 EUROPE: DOORS MARKET, BY COUNTRY, 2024-2030 (MILLION UNITS)

- TABLE 169 EUROPE: DOORS MARKET, BY MATERIAL, 2021-2023 (USD MILLION)

- TABLE 170 EUROPE: DOORS MARKET, BY MATERIAL, 2024-2030 (USD MILLION)

- TABLE 171 EUROPE: DOORS MARKET, BY MATERIAL, 2021-2023 (MILLION UNITS)

- TABLE 172 EUROPE: DOORS MARKET, BY MATERIAL, 2024-2030 (MILLION UNITS)

- TABLE 173 EUROPE: DOORS MARKET, BY MECHANISM, 2021-2023 (USD MILLION)

- TABLE 174 EUROPE: DOORS MARKET, BY MECHANISM, 2024-2030 (USD MILLION)

- TABLE 175 EUROPE: DOORS MARKET, BY MECHANISM, 2021-2023 (MILLION UNITS)

- TABLE 176 EUROPE: DOORS MARKET, BY MECHANISM, 2024-2030 (MILLION UNITS)

- TABLE 177 EUROPE: DOORS MARKET, BY PRODUCT TYPE, 2021-2023 (USD MILLION)

- TABLE 178 EUROPE: DOORS MARKET, BY PRODUCT TYPE, 2024-2030 (USD MILLION)

- TABLE 179 EUROPE: DOORS MARKET, BY PRODUCT TYPE, 2021-2023 (MILLION UNITS)

- TABLE 180 EUROPE: DOORS MARKET, BY PRODUCT TYPE, 2024-2030 (MILLION UNITS)

- TABLE 181 EUROPE: DOORS MARKET, BY APPLICATION, 2021-2023 (USD MILLION)

- TABLE 182 EUROPE: DOORS MARKET, BY APPLICATION, 2024-2030 (USD MILLION)

- TABLE 183 EUROPE: DOORS MARKET, BY APPLICATION, 2021-2023 (MILLION UNITS)

- TABLE 184 EUROPE: DOORS MARKET, BY APPLICATION, 2024-2030 (MILLION UNITS)

- TABLE 185 EUROPE: DOORS MARKET, BY MODE OF APPLICATION, 2021-2023 (USD MILLION)

- TABLE 186 EUROPE: DOORS MARKET, BY MODE OF APPLICATION, 2024-2030 (USD MILLION)

- TABLE 187 EUROPE: DOORS MARKET, BY MODE OF APPLICATION, 2021-2023 (MILLION UNITS)

- TABLE 188 EUROPE: DOORS MARKET, BY MODE OF APPLICATION, 2024-2030 (MILLION UNITS)

- TABLE 189 GERMANY: DOORS MARKET, BY MATERIAL, 2021-2023 (USD MILLION)

- TABLE 190 GERMANY: DOORS MARKET, BY MATERIAL, 2024-2030 (USD MILLION)

- TABLE 191 GERMANY: DOORS MARKET, BY MATERIAL, 2021-2023 (MILLION UNITS)

- TABLE 192 GERMANY: DOORS MARKET, BY MATERIAL, 2024-2030 (MILLION UNITS)

- TABLE 193 GERMANY: DOORS MARKET, BY MECHANISM, 2021-2023 (USD MILLION)

- TABLE 194 GERMANY: DOORS MARKET, BY MECHANISM, 2024-2030 (USD MILLION)

- TABLE 195 GERMANY: DOORS MARKET, BY MECHANISM, 2021-2023 (MILLION UNITS)

- TABLE 196 GERMANY: DOORS MARKET, BY MECHANISM, 2024-2030 (MILLION UNITS)

- TABLE 197 FRANCE: DOORS MARKET, BY MATERIAL, 2021-2023 (USD MILLION)

- TABLE 198 FRANCE: DOORS MARKET, BY MATERIAL, 2024-2030 (USD MILLION)

- TABLE 199 FRANCE: DOORS MARKET, BY MATERIAL, 2021-2023 (MILLION UNITS)

- TABLE 200 FRANCE: DOORS MARKET, BY MATERIAL, 2024-2030 (MILLION UNITS)

- TABLE 201 FRANCE: DOORS MARKET, BY MECHANISM, 2021-2023 (USD MILLION)

- TABLE 202 FRANCE: DOORS MARKET, BY MECHANISM, 2024-2030 (USD MILLION)

- TABLE 203 FRANCE: DOORS MARKET, BY MECHANISM, 2021-2023 (MILLION UNITS)

- TABLE 204 FRANCE: DOORS MARKET, BY MECHANISM, 2024-2030 (MILLION UNITS)

- TABLE 205 ITALY: DOORS MARKET, BY MATERIAL, 2021-2023 (USD MILLION)

- TABLE 206 ITALY: DOORS MARKET, BY MATERIAL, 2024-2030 (USD MILLION)

- TABLE 207 ITALY: DOORS MARKET, BY MATERIAL, 2021-2023 (MILLION UNITS)

- TABLE 208 ITALY: DOORS MARKET, BY MATERIAL, 2024-2030 (MILLION UNITS)

- TABLE 209 ITALY: DOORS MARKET, BY MECHANISM, 2021-2023 (USD MILLION)

- TABLE 210 ITALY: DOORS MARKET, BY MECHANISM, 2024-2030 (USD MILLION)

- TABLE 211 ITALY: DOORS MARKET, BY MECHANISM, 2021-2023 (MILLION UNITS)

- TABLE 212 ITALY: DOORS MARKET, BY MECHANISM, 2024-2030 (MILLION UNITS)

- TABLE 213 UK: DOORS MARKET, BY MATERIAL, 2021-2023 (USD MILLION)

- TABLE 214 UK: DOORS MARKET, BY MATERIAL, 2024-2030 (USD MILLION)

- TABLE 215 UK: DOORS MARKET, BY MATERIAL, 2021-2023 (MILLION UNITS)

- TABLE 216 UK: DOORS MARKET, BY MATERIAL, 2024-2030 (MILLION UNITS)

- TABLE 217 UK: DOORS MARKET, BY MECHANISM, 2021-2023 (USD MILLION)

- TABLE 218 UK: DOORS MARKET, BY MECHANISM, 2024-2030 (USD MILLION)

- TABLE 219 UK: DOORS MARKET, BY MECHANISM, 2021-2023 (MILLION UNITS)

- TABLE 220 UK: DOORS MARKET, BY MECHANISM, 2024-2030 (MILLION UNITS)

- TABLE 221 RUSSIA: DOORS MARKET, BY MATERIAL, 2021-2023 (USD MILLION)

- TABLE 222 RUSSIA: DOORS MARKET, BY MATERIAL, 2024-2030 (USD MILLION)

- TABLE 223 RUSSIA: DOORS MARKET, BY MATERIAL, 2021-2023 (MILLION UNITS)

- TABLE 224 RUSSIA: DOORS MARKET, BY MATERIAL, 2024-2030 (MILLION UNITS)

- TABLE 225 RUSSIA: DOORS MARKET, BY MECHANISM, 2021-2023 (USD MILLION)

- TABLE 226 RUSSIA: DOORS MARKET, BY MECHANISM, 2024-2030 (USD MILLION)

- TABLE 227 RUSSIA: DOORS MARKET, BY MECHANISM, 2021-2023 (MILLION UNITS)

- TABLE 228 RUSSIA: DOORS MARKET, BY MECHANISM, 2024-2030 (MILLION UNITS)

- TABLE 229 REST OF EUROPE: DOORS MARKET, BY MATERIAL, 2021-2023 (USD MILLION)

- TABLE 230 REST OF EUROPE: DOORS MARKET, BY MATERIAL, 2024-2030 (USD MILLION)

- TABLE 231 REST OF EUROPE: DOORS MARKET, BY MATERIAL, 2021-2023 (MILLION UNITS)

- TABLE 232 REST OF EUROPE: DOORS MARKET, BY MATERIAL, 2024-2030 (MILLION UNITS)

- TABLE 233 REST OF EUROPE: DOORS MARKET, BY MECHANISM, 2021-2023 (USD MILLION)

- TABLE 234 REST OF EUROPE: DOORS MARKET, BY MECHANISM, 2024-2030 (USD MILLION)

- TABLE 235 REST OF EUROPE: DOORS MARKET, BY MECHANISM, 2021-2023 (MILLION UNITS)

- TABLE 236 REST OF EUROPE: DOORS MARKET, BY MECHANISM, 2024-2030 (MILLION UNITS)

- TABLE 237 SOUTH AMERICA: DOORS MARKET, BY COUNTRY, 2021-2023 (USD MILLION)

- TABLE 238 SOUTH AMERICA: DOORS MARKET, BY COUNTRY, 2024-2030 (USD MILLION)

- TABLE 239 SOUTH AMERICA: DOORS MARKET, BY COUNTRY, 2021-2023 (MILLION UNITS)

- TABLE 240 SOUTH AMERICA: DOORS MARKET, BY COUNTRY, 2024-2030 (MILLION UNITS)

- TABLE 241 SOUTH AMERICA: DOORS MARKET, BY MATERIAL, 2021-2023 (USD MILLION)

- TABLE 242 SOUTH AMERICA: DOORS MARKET, BY MATERIAL, 2024-2030 (USD MILLION)

- TABLE 243 SOUTH AMERICA: DOORS MARKET, BY MATERIAL, 2021-2023 (MILLION UNITS)

- TABLE 244 SOUTH AMERICA: DOORS MARKET, BY MATERIAL, 2024-2030 (MILLION UNITS)

- TABLE 245 SOUTH AMERICA: DOORS MARKET, BY MECHANISM, 2021-2023 (USD MILLION)

- TABLE 246 SOUTH AMERICA: DOORS MARKET, BY MECHANISM, 2024-2030 (USD MILLION)

- TABLE 247 SOUTH AMERICA: DOORS MARKET, BY MECHANISM, 2021-2023 (MILLION UNITS)

- TABLE 248 SOUTH AMERICA: DOORS MARKET, BY MECHANISM, 2024-2030 (MILLION UNITS)

- TABLE 249 SOUTH AMERICA: DOORS MARKET, BY PRODUCT TYPE, 2021-2023 (USD MILLION)

- TABLE 250 SOUTH AMERICA: DOORS MARKET, BY PRODUCT TYPE, 2024-2030 (USD MILLION)

- TABLE 251 SOUTH AMERICA: DOORS MARKET, BY PRODUCT TYPE, 2021-2023 (MILLION UNITS)

- TABLE 252 SOUTH AMERICA: DOORS MARKET, BY PRODUCT TYPE, 2024-2030 (MILLION UNITS)

- TABLE 253 SOUTH AMERICA: DOORS MARKET, BY APPLICATION, 2021-2023 (USD MILLION)

- TABLE 254 SOUTH AMERICA: DOORS MARKET, BY APPLICATION, 2024-2030 (USD MILLION)

- TABLE 255 SOUTH AMERICA: DOORS MARKET, BY APPLICATION, 2021-2023 (MILLION UNITS)

- TABLE 256 SOUTH AMERICA: DOORS MARKET, BY APPLICATION, 2024-2030 (MILLION UNITS)

- TABLE 257 SOUTH AMERICA: DOORS MARKET, BY MODE OF APPLICATION, 2021-2023 (USD MILLION)

- TABLE 258 SOUTH AMERICA: DOORS MARKET, BY MODE OF APPLICATION, 2024-2030 (USD MILLION)

- TABLE 259 SOUTH AMERICA: DOORS MARKET, BY MODE OF APPLICATION, 2021-2023 (MILLION UNITS)

- TABLE 260 SOUTH AMERICA: DOORS MARKET, BY MODE OF APPLICATION, 2024-2030 (MILLION UNITS)

- TABLE 261 BRAZIL: DOORS MARKET, BY MATERIAL, 2021-2023 (USD MILLION)

- TABLE 262 BRAZIL: DOORS MARKET, BY MATERIAL, 2024-2030 (USD MILLION)

- TABLE 263 BRAZIL: DOORS MARKET, BY MATERIAL, 2021-2023 (MILLION UNITS)

- TABLE 264 BRAZIL: DOORS MARKET, BY MATERIAL, 2024-2030 (MILLION UNITS)

- TABLE 265 BRAZIL: DOORS MARKET, BY MECHANISM, 2021-2023 (USD MILLION)

- TABLE 266 BRAZIL: DOORS MARKET, BY MECHANISM, 2024-2030 (USD MILLION)

- TABLE 267 BRAZIL: DOORS MARKET, BY MECHANISM, 2021-2023 (MILLION UNITS)

- TABLE 268 BRAZIL: DOORS MARKET, BY MECHANISM, 2024-2030 (MILLION UNITS)

- TABLE 269 ARGENTINA: DOORS MARKET, BY MATERIAL, 2021-2023 (USD MILLION)

- TABLE 270 ARGENTINA: DOORS MARKET, BY MATERIAL, 2024-2030 (USD MILLION)

- TABLE 271 ARGENTINA: DOORS MARKET, BY MATERIAL, 2021-2023 (MILLION UNITS)

- TABLE 272 ARGENTINA: DOORS MARKET, BY MATERIAL, 2024-2030 (MILLION UNITS)

- TABLE 273 ARGENTINA: DOORS MARKET, BY MECHANISM, 2021-2023 (USD MILLION)

- TABLE 274 ARGENTINA: DOORS MARKET, BY MECHANISM, 2024-2030 (USD MILLION)

- TABLE 275 ARGENTINA: DOORS MARKET, BY MECHANISM, 2021-2023 (MILLION UNITS)

- TABLE 276 ARGENTINA: DOORS MARKET, BY MECHANISM, 2024-2030 (MILLION UNITS)

- TABLE 277 REST OF SOUTH AMERICA: DOORS MARKET, BY MATERIAL, 2021-2023 (USD MILLION)

- TABLE 278 REST OF SOUTH AMERICA: DOORS MARKET, BY MATERIAL, 2024-2030 (USD MILLION)

- TABLE 279 REST OF SOUTH AMERICA: DOORS MARKET, BY MATERIAL, 2021-2023 (MILLION UNITS)

- TABLE 280 REST OF SOUTH AMERICA: DOORS MARKET, BY MATERIAL, 2024-2030 (MILLION UNITS)

- TABLE 281 REST OF SOUTH AMERICA: DOORS MARKET, BY MECHANISM, 2021-2023 (USD MILLION)

- TABLE 282 REST OF SOUTH AMERICA: DOORS MARKET, BY MECHANISM, 2024-2030 (USD MILLION)

- TABLE 283 REST OF SOUTH AMERICA: DOORS MARKET, BY MECHANISM, 2021-2023 (MILLION UNITS)

- TABLE 284 REST OF SOUTH AMERICA: DOORS MARKET, BY MECHANISM, 2024-2030 (MILLION UNITS)

- TABLE 285 MIDDLE EAST & AFRICA: DOORS MARKET, BY COUNTRY, 2021-2023 (USD MILLION)

- TABLE 286 MIDDLE EAST & AFRICA: DOORS MARKET, BY COUNTRY, 2024-2030 (USD MILLION)

- TABLE 287 MIDDLE EAST & AFRICA: DOORS MARKET, BY COUNTRY, 2021-2023 (MILLION UNITS)

- TABLE 288 MIDDLE EAST & AFRICA: DOORS MARKET, BY COUNTRY, 2024-2030 (MILLION UNITS)

- TABLE 289 MIDDLE EAST & AFRICA: DOORS MARKET, BY MATERIAL, 2021-2023 (USD MILLION)

- TABLE 290 MIDDLE EAST & AFRICA: DOORS MARKET, BY MATERIAL, 2024-2030 (USD MILLION)

- TABLE 291 MIDDLE EAST & AFRICA: DOORS MARKET, BY MATERIAL, 2021-2023 (MILLION UNITS)

- TABLE 292 MIDDLE EAST & AFRICA: DOORS MARKET, BY MATERIAL, 2024-2030 (MILLION UNITS)

- TABLE 293 MIDDLE EAST & AFRICA: DOORS MARKET, BY MECHANISM, 2021-2023 (USD MILLION)

- TABLE 294 MIDDLE EAST & AFRICA: DOORS MARKET, BY MECHANISM, 2024-2030 (USD MILLION)

- TABLE 295 MIDDLE EAST & AFRICA: DOORS MARKET, BY MECHANISM, 2021-2023 (MILLION UNITS)

- TABLE 296 MIDDLE EAST & AFRICA: DOORS MARKET, BY MECHANISM, 2024-2030 (MILLION UNITS)

- TABLE 297 MIDDLE EAST & AFRICA: DOORS MARKET, BY PRODUCT TYPE, 2021-2023 (USD MILLION)

- TABLE 298 MIDDLE EAST & AFRICA: DOORS MARKET, BY PRODUCT TYPE, 2024-2030 (USD MILLION)

- TABLE 299 MIDDLE EAST & AFRICA: DOORS MARKET, BY PRODUCT TYPE, 2021-2023 (MILLION UNITS)

- TABLE 300 MIDDLE EAST & AFRICA: DOORS MARKET, BY PRODUCT TYPE, 2024-2030 (MILLION UNITS)

- TABLE 301 MIDDLE EAST & AFRICA: DOORS MARKET, BY APPLICATION, 2021-2023 (USD MILLION)

- TABLE 302 MIDDLE EAST & AFRICA: DOORS MARKET, BY APPLICATION, 2024-2030 (USD MILLION)

- TABLE 303 MIDDLE EAST & AFRICA: DOORS MARKET, BY APPLICATION, 2021-2023 (MILLION UNITS)

- TABLE 304 MIDDLE EAST & AFRICA: DOORS MARKET, BY APPLICATION, 2024-2030 (MILLION UNITS)

- TABLE 305 MIDDLE EAST & AFRICA: DOORS MARKET, BY MODE OF APPLICATION, 2021-2023 (USD MILLION)

- TABLE 306 MIDDLE EAST & AFRICA: DOORS MARKET, BY MODE OF APPLICATION, 2024-2030 (USD MILLION)

- TABLE 307 MIDDLE EAST & AFRICA: DOORS MARKET, BY MODE OF APPLICATION, 2021-2023 (MILLION UNITS)

- TABLE 308 MIDDLE EAST & AFRICA: DOORS MARKET, BY MODE OF APPLICATION, 2024-2030 (MILLION UNITS)

- TABLE 309 GCC COUNTRIES: DOORS MARKET, BY MATERIAL, 2021-2023 (USD MILLION)

- TABLE 310 GCC COUNTRIES: DOORS MARKET, BY MATERIAL, 2024-2030 (USD MILLION)

- TABLE 311 GCC COUNTRIES: DOORS MARKET, BY MATERIAL, 2021-2023 (MILLION UNITS)

- TABLE 312 GCC COUNTRIES: DOORS MARKET, BY MATERIAL, 2024-2030 (MILLION UNITS)

- TABLE 313 GCC COUNTRIES: DOORS MARKET, BY MECHANISM, 2021-2023 (USD MILLION)

- TABLE 314 GCC COUNTRIES: DOORS MARKET, BY MECHANISM, 2024-2030 (USD MILLION)

- TABLE 315 GCC COUNTRIES: DOORS MARKET, BY MECHANISM, 2021-2023 (MILLION UNITS)

- TABLE 316 GCC COUNTRIES: DOORS MARKET, BY MECHANISM, 2024-2030 (MILLION UNITS)

- TABLE 317 SAUDI ARABIA: DOORS MARKET, BY MATERIAL, 2021-2023 (USD MILLION)

- TABLE 318 SAUDI ARABIA: DOORS MARKET, BY MATERIAL, 2024-2030 (USD MILLION)

- TABLE 319 SAUDI ARABIA: DOORS MARKET, BY MATERIAL, 2021-2023 (MILLION UNITS)

- TABLE 320 SAUDI ARABIA: DOORS MARKET, BY MATERIAL, 2024-2030 (MILLION UNITS)

- TABLE 321 SAUDI ARABIA: DOORS MARKET, BY MECHANISM, 2021-2023 (USD MILLION)

- TABLE 322 SAUDI ARABIA: DOORS MARKET, BY MECHANISM, 2024-2030 (USD MILLION)

- TABLE 323 SAUDI ARABIA: DOORS MARKET, BY MECHANISM, 2021-2023 (MILLION UNITS)

- TABLE 324 SAUDI ARABIA: DOORS MARKET, BY MECHANISM, 2024-2030 (MILLION UNITS)

- TABLE 325 UAE: DOORS MARKET, BY MATERIAL, 2021-2023 (USD MILLION)

- TABLE 326 UAE: DOORS MARKET, BY MATERIAL, 2024-2030 (USD MILLION)

- TABLE 327 UAE: DOORS MARKET, BY MATERIAL, 2021-2023 (MILLION UNITS)

- TABLE 328 UAE: DOORS MARKET, BY MATERIAL, 2024-2030 (MILLION UNITS)

- TABLE 329 UAE: DOORS MARKET, BY MECHANISM, 2021-2023 (USD MILLION)

- TABLE 330 UAE: DOORS MARKET, BY MECHANISM, 2024-2030 (USD MILLION)

- TABLE 331 UAE: DOORS MARKET, BY MECHANISM, 2021-2023 (MILLION UNITS)

- TABLE 332 UAE: DOORS MARKET, BY MECHANISM, 2024-2030 (MILLION UNITS)

- TABLE 333 REST OF GCC COUNTRIES: DOORS MARKET, BY MATERIAL, 2021-2023 (USD MILLION)

- TABLE 334 REST OF GCC COUNTRIES: DOORS MARKET, BY MATERIAL, 2024-2030 (USD MILLION)

- TABLE 335 REST OF GCC COUNTRIES: DOORS MARKET, BY MATERIAL, 2021-2023 (MILLION UNITS)

- TABLE 336 REST OF GCC COUNTRIES: DOORS MARKET, BY MATERIAL, 2024-2030 (MILLION UNITS)

- TABLE 337 REST OF GCC COUNTRIES: DOORS MARKET, BY MECHANISM, 2021-2023 (USD MILLION)

- TABLE 338 REST OF GCC COUNTRIES: DOORS MARKET, BY MECHANISM, 2024-2030 (USD MILLION)

- TABLE 339 REST OF GCC COUNTRIES: DOORS MARKET, BY MECHANISM, 2021-2023 (MILLION UNITS)

- TABLE 340 REST OF GCC COUNTRIES: DOORS MARKET, BY MECHANISM, 2024-2030 (MILLION UNITS)

- TABLE 341 SOUTH AFRICA: DOORS MARKET, BY MATERIAL, 2021-2023 (USD MILLION)

- TABLE 342 SOUTH AFRICA: DOORS MARKET, BY MATERIAL, 2024-2030 (USD MILLION)

- TABLE 343 SOUTH AFRICA: DOORS MARKET, BY MATERIAL, 2021-2023 (MILLION UNITS)

- TABLE 344 SOUTH AFRICA: DOORS MARKET, BY MATERIAL, 2024-2030 (MILLION UNITS)

- TABLE 345 SOUTH AFRICA: DOORS MARKET, BY MECHANISM, 2021-2023 (USD MILLION)

- TABLE 346 SOUTH AFRICA: DOORS MARKET, BY MECHANISM, 2024-2030 (USD MILLION)

- TABLE 347 SOUTH AFRICA: DOORS MARKET, BY MECHANISM, 2021-2023 (MILLION UNITS)

- TABLE 348 SOUTH AFRICA: DOORS MARKET, BY MECHANISM, 2024-2030 (MILLION UNITS)

- TABLE 349 REST OF MIDDLE EAST & AFRICA: DOORS MARKET, BY MATERIAL, 2021-2023 (USD MILLION)

- TABLE 350 REST OF MIDDLE EAST & AFRICA: DOORS MARKET, BY MATERIAL, 2024-2030 (USD MILLION)

- TABLE 351 REST OF MIDDLE EAST & AFRICA: DOORS MARKET, BY MATERIAL, 2021-2023 (MILLION UNITS)

- TABLE 352 REST OF MIDDLE EAST & AFRICA: DOORS MARKET, BY MATERIAL, 2024-2030 (MILLION UNITS)

- TABLE 353 REST OF MIDDLE EAST & AFRICA: DOORS MARKET, BY MECHANISM, 2021-2023 (USD MILLION)

- TABLE 354 REST OF MIDDLE EAST & AFRICA: DOORS MARKET, BY MECHANISM, 2024-2030 (USD MILLION)

- TABLE 355 REST OF MIDDLE EAST & AFRICA: DOORS MARKET, BY MECHANISM, 2021-2023 (MILLION UNITS)

- TABLE 356 REST OF MIDDLE EAST & AFRICA: DOORS MARKET, BY MECHANISM, 2024-2030 (MILLION UNITS)

- TABLE 357 DOORS MARKET: OVERVIEW OF MAJOR STRATEGIES ADOPTED BY KEY PLAYERS, JANUARY 2020-JULY 2025

- TABLE 358 DOORS MARKET: DEGREE OF COMPETITION, 2024

- TABLE 359 DOORS MARKET: REGIONAL FOOTPRINT, 2024

- TABLE 360 DOORS MARKET: PRODUCT TYPE FOOTPRINT, 2024

- TABLE 361 DOORS MARKET: MATERIAL FOOTPRINT, 2024

- TABLE 362 DOORS MARKET: MECHANISM FOOTPRINT, 2024

- TABLE 363 DOORS MARKET: MODE OF APPLICATION FOOTPRINT, 2024

- TABLE 364 DOORS MARKET: APPLICATION FOOTPRINT, 2024

- TABLE 365 DOORS MARKET: DETAILED LIST OF KEY STARTUPS/SMES, 2024

- TABLE 366 DOORS MARKET: COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES, 2024

- TABLE 367 DOORS MARKET: PRODUCT LAUNCHES, JANUARY 2020-JULY 2025

- TABLE 368 DOORS MARKET: DEALS, JANUARY 2020-JULY 2025

- TABLE 369 DOORS MARKET: EXPANSIONS, JANUARY 2020-JULY 2025

- TABLE 370 ASSA ABLOY: COMPANY OVERVIEW

- TABLE 371 ASSA ABLOY: PRODUCTS OFFERED

- TABLE 372 ASSA ABLOY: PRODUCT LAUNCHES

- TABLE 373 ASSA ABLOY: DEALS

- TABLE 374 LIXIL CORPORATION: COMPANY OVERVIEW

- TABLE 375 LIXIL CORPORATION: PRODUCTS OFFERED

- TABLE 376 LIXIL CORPORATION: PRODUCT LAUNCHES

- TABLE 377 LIXIL CORPORATION: DEALS

- TABLE 378 LIXIL CORPORATION: EXPANSIONS

- TABLE 379 CORNERSTONE BUILDING BRANDS, INC.: COMPANY OVERVIEW

- TABLE 380 CORNERSTONE BUILDING BRANDS, INC.: PRODUCTS OFFERED

- TABLE 381 CORNERSTONE BUILDING BRANDS, INC.: PRODUCT LAUNCHES

- TABLE 382 CORNERSTONE BUILDING BRANDS, INC.: DEALS

- TABLE 383 JELD-WEN, INC.: COMPANY OVERVIEW

- TABLE 384 JELD-WEN, INC.: PRODUCTS OFFERED

- TABLE 385 JELD-WEN, INC.: PRODUCT LAUNCHES

- TABLE 386 JELD-WEN, INC.: DEALS

- TABLE 387 JELD-WEN, INC.: EXPANSIONS

- TABLE 388 ALLEGION PLC: COMPANY OVERVIEW

- TABLE 389 ALLEGION PLC: PRODUCTS OFFERED

- TABLE 390 ALLEGION PLC: DEALS

- TABLE 391 DORMAKABA GROUP: COMPANY OVERVIEW

- TABLE 392 DORMAKABA GROUP: PRODUCTS OFFERED

- TABLE 393 DORMAKABA GROUP: PRODUCT LAUNCHES

- TABLE 394 DORMAKABA GROUP: DEALS

- TABLE 395 DORMAKABA GROUP: EXPANSIONS

- TABLE 396 YKK AP: COMPANY OVERVIEW

- TABLE 397 YKK AP: PRODUCTS OFFERED

- TABLE 398 YKK AP: PRODUCT LAUNCHES

- TABLE 399 YKK AP: DEALS

- TABLE 400 YKK AP: EXPANSIONS

- TABLE 401 OWENS CORNING: COMPANY OVERVIEW

- TABLE 402 OWENS CORNING: PRODUCTS OFFERED

- TABLE 403 OWENS CORNING: DEALS

- TABLE 404 ANDERSEN CORPORATION: COMPANY OVERVIEW

- TABLE 405 ANDERSEN CORPORATION: PRODUCTS OFFERED

- TABLE 406 ANDERSEN CORPORATION: PRODUCT LAUNCHES

- TABLE 407 ANDERSEN CORPORATION: DEALS

- TABLE 408 ANDERSEN CORPORATION: EXPANSIONS

- TABLE 409 MITER BRANDS: COMPANY OVERVIEW

- TABLE 410 MITER BRANDS: PRODUCTS OFFERED

- TABLE 411 MITER BRANDS: PRODUCT LAUNCHES

- TABLE 412 MITER BRANDS: DEALS

- TABLE 413 MITER BRANDS: EXPANSIONS

- TABLE 414 PELLA CORPORATION: COMPANY OVERVIEW

- TABLE 415 SIMPSON DOOR COMPANY: COMPANY OVERVIEW

- TABLE 416 BOON EDAM: COMPANY OVERVIEW

- TABLE 417 REYNAERS ALUMINIUM: COMPANY OVERVIEW

- TABLE 418 NOVOFERM GMBH: COMPANY OVERVIEW

- TABLE 419 FENESTA BUILDING SYSTEMS: COMPANY OVERVIEW

- TABLE 420 HORMANN: COMPANY OVERVIEW

- TABLE 421 WERU GMBH: COMPANY OVERVIEW

- TABLE 422 THERMA-TRU CORP.: COMPANY OVERVIEW

- TABLE 423 MARVIN: COMPANY OVERVIEW

- TABLE 424 PDS DOORSETS: COMPANY OVERVIEW

- TABLE 425 SGM WINDOW MANUFACTURING LIMITED: COMPANY OVERVIEW

- TABLE 426 VINYLGUARD WINDOW & DOOR SYSTEMS LTD.: COMPANY OVERVIEW

- TABLE 427 PROVIA LLC: COMPANY OVERVIEW

- TABLE 428 KOLBE WINDOWS & DOORS: COMPANY OVERVIEW

- TABLE 429 DOORS & WINDOWS MARKET, BY PRODUCT, 2022-2029 (USD MILLION)

- TABLE 430 DOORS & WINDOWS MARKET, BY PRODUCT, 2022-2029 (MILLION SQUARE METERS)

- TABLE 431 DOORS & WINDOWS MARKET, BY CONSTRUCTION TYPE, 2022-2029 (USD MILLION)

- TABLE 432 DOORS & WINDOWS MARKET, BY CONSTRUCTION TYPE, 2022-2029 (MILLION SQUARE METERS)

- TABLE 433 DOORS & WINDOWS MARKET, BY MATERIAL, 2022-2029 (USD MILLION)

- TABLE 434 DOORS & WINDOWS MARKET, BY MATERIAL, 2022-2029 (MILLION SQUARE METER)

- TABLE 435 DOORS & WINDOWS MARKET, BY END-USE INDUSTRY, 2022-2029 (USD MILLION)

- TABLE 436 DOORS & WINDOWS MARKET, BY END-USE INDUSTRY, 2022-2029 (MILLION SQUARE METER)

- TABLE 437 DOORS & WINDOWS MARKET, BY REGION, 2022-2029 (USD MILLION)

- TABLE 438 DOORS & WINDOWS MARKET, BY REGION, 2022-2029 (MILLION SQUARE METER)

List of Figures

- FIGURE 1 DOORS MARKET SEGMENTATION AND REGIONAL SCOPE

- FIGURE 2 STUDY YEARS CONSIDERED

- FIGURE 3 DOORS MARKET: RESEARCH DESIGN

- FIGURE 4 KEY DATA FROM SECONDARY SOURCES

- FIGURE 5 KEY DATA FROM PRIMARY SOURCES

- FIGURE 6 KEY INDUSTRY INSIGHTS

- FIGURE 7 BREAKDOWN OF INTERVIEWS WITH EXPERTS

- FIGURE 8 MARKET SIZE ESTIMATION: BOTTOM-UP APPROACH

- FIGURE 9 MARKET SIZE ESTIMATION: TOP-DOWN APPROACH

- FIGURE 3 DOORS MARKET: DATA TRIANGULATION

- FIGURE 4 FACTOR ANALYSIS

- FIGURE 5 RESEARCH ASSUMPTIONS

- FIGURE 6 METAL TO BE FASTEST-GROWING DOOR MATERIAL DURING FORECAST PERIOD

- FIGURE 7 EXTERIOR DOORS TO GROW FASTER THAN INTERIOR DOORS DURING FORECAST PERIOD

- FIGURE 8 SWINGING DOORS TO BE FASTEST-GROWING SEGMENT AMONG DOOR MECHANISMS DURING FORECAST PERIOD

- FIGURE 9 NEW CONSTRUCTION TO DEMAND MORE DOORS DURING FORECAST PERIOD

- FIGURE 10 NON-RESIDENTIAL DOORS TO BE FASTER-GROWING SEGMENT DURING FORECAST PERIOD

- FIGURE 11 ASIA PACIFIC TO BE FASTEST-GROWING MARKET DURING FORECAST PERIOD

- FIGURE 12 EMERGING ECONOMIES OFFER ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN DOORS MARKET

- FIGURE 13 EXTERIOR DOORS AND CHINA LED RESPECTIVE SEGMENTS IN DOORS MARKET IN 2024

- FIGURE 14 METAL SEGMENT TO GROW AT HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 15 EXTERIOR DOORS SEGMENT TO LEAD MARKET DURING FORECAST PERIOD

- FIGURE 16 SLIDING DOORS ACCOUNT FOR LARGEST DEMAND DURING FORECAST PERIOD

- FIGURE 17 NEW CONSTRUCTION SEGMENT TO BE FASTEST GROWING DURING FORECAST PERIOD

- FIGURE 18 NON-RESIDENTIAL PROJECTED TO BE LARGEST SEGMENT OF DOORS MARKET

- FIGURE 19 MARKET IN INDIA TO GROW AT HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 20 DOORS MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

- FIGURE 21 GLOBAL BUILDING FLOOR AREA IN ADVANCED, EMERGING, AND DEVELOPING ECONOMIES (2010-2022) WITH 2030 PROJECTION (BILLION M2)

- FIGURE 22 URBAN POPULATION TREND, 2000-2030 (BILLION)

- FIGURE 23 TRENDS/DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

- FIGURE 24 DOORS MARKET: ECOSYSTEM ANALYSIS

- FIGURE 25 DOORS MARKET: VALUE CHAIN ANALYSIS

- FIGURE 26 AVERAGE SELLING PRICE TREND OF DOOR MATERIALS, BY KEY PLAYER, 2024 (USD/UNIT)

- FIGURE 27 AVERAGE SELLING PRICE OF KEY MATERIALS, BY REGION, 2021-2024 (USD/UNIT)

- FIGURE 28 EXPORT DATA FOR HS CODE 441820-COMPLIANT PRODUCTS, BY COUNTRY, 2020-2024 (USD THOUSAND)

- FIGURE 29 IMPORT DATA FOR HS CODE 441820-COMPLIANT PRODUCTS, BY COUNTRY, 2020-2024 (USD THOUSAND)

- FIGURE 30 LIST OF MAJOR PATENTS FOR DOORS, 2015-2024

- FIGURE 31 MAJOR PATENTS APPLIED AND GRANTED RELATED TO DOORS, BY COUNTRY/REGION, 2015-2024

- FIGURE 32 INVESTMENT AND FUNDING SCENARIO, 2018-2024 (USD MILLION)

- FIGURE 33 IMPACT OF GEN AI/AI ON DOORS MARKET

- FIGURE 34 DOORS MARKET: PORTER'S FIVE FORCES ANALYSIS

- FIGURE 35 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS

- FIGURE 36 KEY BUYING CRITERIA FOR KEY APPLICATIONS

- FIGURE 37 METAL DOORS TO BE FASTEST GROWING DURING FORECAST PERIOD

- FIGURE 38 SWINGING DOORS SEGMENT TO LEAD DOORS MARKET

- FIGURE 39 EXTERIOR DOORS SEGMENT TO BE FASTEST GROWING DURING FORECAST PERIOD

- FIGURE 40 NEW CONSTRUCTION SEGMENT DOMINATED DOORS MARKET IN 2024

- FIGURE 41 NON-RESIDENTIAL SEGMENT TO BE FASTEST GROWING DURING FORECAST PERIOD

- FIGURE 42 INDIA TO BE FASTEST-GROWING COUNTRY DURING FORECAST PERIOD

- FIGURE 43 SIA PACIFIC TO DOMINATE MARKET DURING FORECAST PERIOD

- FIGURE 44 ASIA PACIFIC: DOORS MARKET SNAPSHOT

- FIGURE 45 NORTH AMERICA: DOORS MARKET SNAPSHOT

- FIGURE 46 DOORS MARKET SHARE ANALYSIS, 2024

- FIGURE 47 DOORS MARKET: REVENUE ANALYSIS OF KEY COMPANIES IN LAST FIVE YEARS, 2020-2024 (USD BILLION)

- FIGURE 48 DOORS MARKET: COMPANY VALUATION, 2024 (USD BILLION)

- FIGURE 49 DOORS MARKET: FINANCIAL MATRIX: EV/EBITDA RATIO, 2024

- FIGURE 50 DOORS MARKET: YEAR-TO-DATE PRICE AND FIVE-YEAR STOCK BETA, 2024

- FIGURE 51 DOORS MARKET: PRODUCT/BRAND COMPARISON

- FIGURE 52 DOORS MARKET: COMPANY EVALUATION MATRIX (KEY PLAYERS), 2024

- FIGURE 53 DOORS MARKET: COMPANY FOOTPRINT, 2024

- FIGURE 54 DOORS MARKET: COMPANY EVALUATION MATRIX (STARTUPS/SMES), 2024

- FIGURE 55 ASSA ABLOY: COMPANY SNAPSHOT (2024)

- FIGURE 56 LIXIL CORPORATION: COMPANY SNAPSHOT (2024)

- FIGURE 57 CORNERSTONE BUILDING BRANDS, INC.: COMPANY SNAPSHOT (2024)

- FIGURE 58 JELD-WEN, INC.: COMPANY SNAPSHOT (2024)

- FIGURE 59 ALLEGION PLC: COMPANY SNAPSHOT (2024)

- FIGURE 60 DORMAKABA GROUP: COMPANY SNAPSHOT (2023)

- FIGURE 61 OWENS CORNING: COMPANY SNAPSHOT (2024)

船用舱壁防水门市场:依产品类型、材质、销售管道、应用与最终用户划分-2026-2032年全球预测

船用舱壁防水门市场:依产品类型、材质、销售管道、应用与最终用户划分-2026-2032年全球预测 景观门市场规模、份额和成长分析:按产品类型、材料、应用、最终用户、分销管道和地区划分-2026-2033年产业预测住宅滑动谷仓门市场按类型、材料、分销渠道、最终用户、表面处理、应用和门尺寸划分,全球预测,2026-2032年

景观门市场规模、份额和成长分析:按产品类型、材料、应用、最终用户、分销管道和地区划分-2026-2033年产业预测住宅滑动谷仓门市场按类型、材料、分销渠道、最终用户、表面处理、应用和门尺寸划分,全球预测,2026-2032年 含铅胶合板市场规模、份额和成长分析:按类型、厚度、核心材料、铅含量、应用和地区划分-2026-2033年产业预测

含铅胶合板市场规模、份额和成长分析:按类型、厚度、核心材料、铅含量、应用和地区划分-2026-2033年产业预测 铝合金门窗市场规模、份额及成长分析(按产品类型、机制、最终用户和地区划分)-2026-2033年产业预测

铝合金门窗市场规模、份额及成长分析(按产品类型、机制、最终用户和地区划分)-2026-2033年产业预测 2026-2034年全球室内折迭门市场规模、份额、趋势和成长分析报告全球木质室内门市场规模、份额、趋势和成长分析报告(2026-2034年)

2026-2034年全球室内折迭门市场规模、份额、趋势和成长分析报告全球木质室内门市场规模、份额、趋势和成长分析报告(2026-2034年) 2026年全球保温钢捲门市场报告2026年全球木质室内门市场报告2026年全球车库门和捲门市场报告

2026年全球保温钢捲门市场报告2026年全球木质室内门市场报告2026年全球车库门和捲门市场报告