|

市场调查报告书

商品编码

1811753

全球停车管理市场(至 2030 年)按解决方案(停车预订管理、停车通道和收益管理)、停车场地(路外、路内)和最终用户(商业、政府、运输和交通、工业、住宅)划分Parking Management Market by Solutions (Parking Reservation Management, Parking Access & Revenue Control), Parking Site (Off-street, On-street), and End Use (Commercial, Government, Transport & Transit, Industrial, Residential) - Global Forecast to 2030 |

||||||

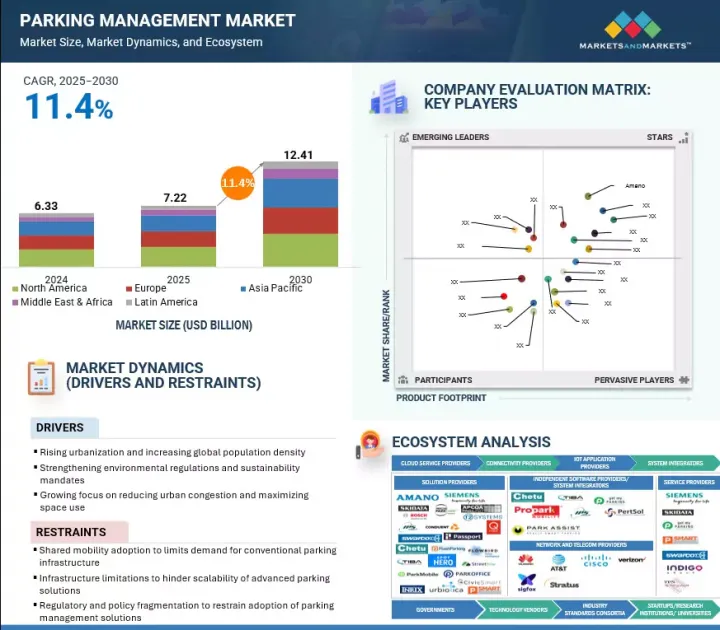

停车管理市场预计将从 2025 年的 72.2 亿美元成长到 2030 年的 124.1 亿美元,复合年增长率为 11.4%。

| 调查范围 | |

|---|---|

| 调查年份 | 2020-2030 |

| 基准年 | 2024 |

| 预测期 | 2025-2030 |

| 单元 | 金额(美元) |

| 部分 | 供应类别,停车场。最终用户,地区 |

| 目标区域 | 北美、欧洲、亚太地区、中东和非洲、拉丁美洲 |

永续性目标推动了这一趋势,各城市纷纷推广绿色停车解决方案,例如为电动车提供专用停车位,并努力减少停放车辆的排放。经济因素也在推动停车技术的普及,营运商透过动态定价模式优化收益并改善与本地企业的联繫。

叫车、共享汽车、共享单车和微旅行服务(例如电动Scooter和电动自行车)等替代出行方式的兴起,正在减少对私家车的依赖以及对传统停车位的需求。因此,停车场营运商面临着利用率下降的问题,这使得投资智慧停车系统变得难以合理化。虽然这些服务促进了城市的永续性,但它们也限制了停车管理市场的发展,迫使营运商适应新的出行趋势。

根据最终用户,预计住宅部分在预测期内将实现最高的复合年增长率。

这一增长是由都市化进程加快和高层住宅建筑兴起所推动的,这推动了封闭式社区和多用户住宅对安全、高效和技术主导的停车解决方案的需求。在印度,DLF 和 Prestige Group 等领先的住宅开发人员正在推出自动停车系统和基于应用程式的居民停车平台,以解决空间限制问题并提供无缝的存取控制。

在新加坡,建屋发展局 (HDB) 的小区已采用与 Parking.sg 应用程式整合的数位停车系统,为居民提供数位支付、远端延期和纸质停车券淘汰等便利。同样,阿联酋迪拜码头和迪拜市中心的豪华住宅区也采用了支援 RFID 的门禁系统,并配备车牌识别功能,实现居民自动出入和访客管理。这些解决方案提高了便利性、增强了安全性,并最佳利用。

这些发展正在为住宅停车管理带来明显的转变,预计将推动对自动化、即时监控和整合数位平台的需求激增。随着城市住房计划的扩大和居民对智慧运输便利性的需求,住宅领域预计将在预测期内成为成长最快的采用领域。

本报告调查了全球停车管理市场,并提供了市场概况、影响市场成长的各种因素分析、技术和专利趋势、法律制度、案例研究、市场规模趋势和预测、各个细分市场、地区/主要国家的详细分析、竞争格局和主要企业的概况。

目录

第一章 引言

第二章调查方法

第三章执行摘要

第四章重要考察

第五章市场概况及产业趋势

- 市场动态

- 驱动程式

- 抑制因素

- 机会

- 任务

- 停车场管理的演变

- 生态系分析

- 案例研究分析

- 供应链分析

- 定价分析

- 技术分析

- 专利分析

- 影响客户业务的趋势/中断

- 波特五力分析

- 关税和监管状况

- 主要相关人员和采购标准

- 2025-2026年重要会议和活动

- 停车管理市场技术蓝图

- 人工智慧和产生人工智慧对停车场管理的影响

- 2024年投资金筹措情景

- 当前和新兴的经营模式经营模式

- 停车管理解决方案最佳实践

- 贸易分析

- 停车管理解决方案中使用的工具、框架和技术

- 2025年美国关税的影响 - 停车管理市场

第六章 停车场管理市场:依产品类别

- 解决方案

- 停车通道和收益管理

- 停车违规执法管理

- 停车预约管理

- 停车资讯

- 停车场安全和监控

- 停车许可证管理

- 其他解决方案

- 服务

- 专业服务

- 託管服务

第七章 停车管理市场(依停车场地划分)

- 路外停车

- 车库停车位

- 停车场

- 街边停车

第八章停车管理市场(依最终用户)

- 住房

- 商业的

- 产业

- 政府/公共

- 交通运输

第九章停车管理市场(按区域)

- 北美洲

- 宏观经济展望

- 美国

- 加拿大

- 欧洲

- 宏观经济展望

- 英国

- 德国

- 法国

- 义大利

- 其他的

- 亚太地区

- 宏观经济展望

- 中国

- 日本

- 印度

- 其他的

- 中东和非洲

- 宏观经济展望

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 南非

- 其他的

- 拉丁美洲

- 宏观经济展望

- 巴西

- 墨西哥

- 其他的

第十章 竞争格局

- 概述

- 主要参与企业的策略/优势

- 收益分析

- 市占率分析

- 估值和财务指标

- 品牌/产品比较

- 公司评估矩阵:主要企业

- 公司估值矩阵:Start-Ups/中小型企业

- 竞争场景

第十一章 公司简介

- 主要企业

- AMANO

- SKIDATA

- GROUP INDIGO

- ARRIVE

- TIBA PARKING SYSTEMS

- SWARCO

- CHETU

- INRIX

- IPS GROUP

- PRECISE PARKLINK

- VERRA MOBILITY

- INFOCOMM GROUP

- EGIS GROUP

- 其他公司

- PASSPORT LABS

- GET MY PARKING

- STREETLINE

- CLEVERCITI

- SPOTHERO

- WAYLEADR

- URBIOTICA

- CIVICSMART

- PARKLIO

- TCS INTERNATIONAL

- PARKABLE

- PARKALOT

- PARKING TELECOM

- OMNITEC

第 12 章:相邻/相关市场

第十三章 附录

The parking management market is estimated to be USD 7.22 billion in 2025 and is projected to reach USD 12.41 billion by 2030 at a CAGR of 11.4%.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2020-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD) Million/Billion |

| Segments | Offering, Parking Site, End Use, and Region |

| Regions covered | North America, Europe, Asia Pacific, Middle East & Africa, and Latin America |

It is driven by sustainability goals, with cities promoting green parking solutions such as dedicated bays for electric vehicles and initiatives to reduce exhaust emissions from parked cars. Economic priorities fuel adoption as operators seek to optimize revenue through dynamic pricing models and improve accessibility for local businesses.

The rise of alternative mobility options, such as ride-hailing, car-sharing, bike-sharing, and micro-mobility services (e-scooters and e-bikes), is decreasing reliance on private vehicle ownership and lowering demand for traditional parking spaces. As a result, parking operators face declining utilization rates, making it harder to justify investments in smart parking systems. While these services promote urban sustainability, they restrain the parking management market and force operators to adapt to new mobility trends.

"Residential end-use segment is projected to register the highest CAGR during the forecast period"

The residential segment is expected to achieve the highest CAGR in the parking management market as rising urbanization and vertical housing trends push demand for secure, efficient, and technology-driven parking solutions within gated communities and apartment complexes. In India, large residential developers, such as DLF and Prestige Group, have begun deploying automated parking systems and app-based resident parking platforms to address space constraints and ensure seamless access control.

In Singapore, Housing and Development Board (HDB) estates adopted digital parking systems integrated with the Parking.sg app, enabling residents to pay digitally, extend sessions remotely, and avoid manual coupon systems. Similarly, in the United Arab Emirates, premium residential complexes in Dubai Marina and Downtown Dubai are increasingly using RFID-enabled gated entry systems combined with license plate recognition for automated resident access and visitor management. These solutions improve convenience, enhance security, and optimize the limited parking spaces available in dense residential areas.

Such developments are driving a clear shift in residential parking management, with a demand for automation, real-time monitoring, and integrated digital platforms expected to surge. As urban housing projects expand and residents seek smart mobility conveniences, the residential end-use segment is poised to emerge as the fastest-growing area of adoption during the forecast period.

"Off-street parking segment to hold the largest market share during forecast period"

The off-street parking segment is expected to contribute the largest market share in adopting parking management systems, as cities and private operators increasingly modernize garages, malls, and institutional facilities with advanced solutions. In the US, operators such as LAZ Parking and SP+ have integrated license plate recognition, digital payment systems, and real-time occupancy management in multi-level parking structures across New York, Chicago, and Los Angeles to enhance efficiency and user convenience. In Europe, major shopping centers and business districts in Paris and Berlin are deploying Skidata's automated revenue control and access systems, allowing seamless entry and exit through ticketless, contactless solutions.

Similarly, in Japan, Amano Corporation equipped large-scale commercial garages in Tokyo with automated parking guidance and integrated EV charging stations, improving space utilization and sustainability compliance. These developments highlight why off-street facilities dominate adoption. They provide controlled environments where integrated hardware and software platforms can deliver measurable efficiency gains, reduce congestion, and optimize revenue generation. With the growing demand for automation, digital payments, and sustainable infrastructure, off-street parking is set to drive the parking management market during the forecast period.

"Asia Pacific will register the highest growth rate, while North America is expected to contribute the largest market share during the forecast period"

Asia Pacific is projected to register the highest CAGR in the parking management market, mainly due to strong government initiatives and regulatory mandates across the region. Singapore is setting a benchmark through its Urban Redevelopment Authority's Parking Guidance System (PGS), which integrates real-time occupancy data, digital signage, and mobile app capabilities for public and commercial parking facilities, creating a model of operational transparency and user convenience. In China, Beijing and Shenzhen are deploying large-scale smart parking systems that incorporate IoT sensors, license plate recognition, and contactless payments as part of national smart city roadmaps, effectively addressing growing urban vehicle volumes.

Japan is fueling adoption by enforcing cashless payment requirements in parking facilities while simultaneously expanding EV-ready infrastructure, aligning its parking sector with broader sustainability goals. South Korea has made strides, particularly in Seoul, where government-led programs mandate e-payments and automated monitoring in public and private parking lots.

North America is expected to capture the largest share of the parking management market, driven by a wave of high-impact, tech-forward implementations across transit hubs and urban centers. Detroit Metropolitan Wayne County Airport is deploying Park Assist's camera-based smart sensor system across more than 18,000 parking spaces to slash search time by up to 63%, boosting convenience and throughput. EnSight Technologies is introducing an AI-powered parking guidance system at Norfolk International Airport, utilizing over 100 cameras to provide real-time occupancy data and digital signage for faster navigation of parking spaces.

At Los Angeles International Airport, ABM's ABMvantage platform has modernized the sprawling LAX Economy Parking facility with touchless entry, pre-booking, license-plate recognition, EV charging, and unified data dashboards. Additionally, the Miami Parking Authority partnered with ParkMobile to expand mobile parking payments across more than 20,000 spaces in the city, thereby enhancing customer convenience and reducing congestion with meter-based systems. These large-scale modernization efforts spanning software-enabled operations, automation, and EV integration demonstrate how strategic deployments in high-traffic venues are fueling North America's leadership in parking management innovation.

Breakdown of Primaries

The study contains insights from various industry experts, from solution vendors to Tier 1 companies. The break-up of the primaries is as follows:

- By Company Type: Tier 1 - 18%, Tier 2 - 44%, and Tier 3 - 38%

- By Designation: C-level -32%, D-level - 36%, and Managers - 32%

- By Region: North America - 38%, Europe - 26%, Asia Pacific - 18%, Middle East & Africa - 10%, and Latin America - 8%

The major players in the parking management market are Amano (Japan), SKIDATA (Austria), Group Indigo (France), Arrive (Sweden), TIBA Parking Systems (Israel), SWARCO (Austria), Chetu (US), INRIX (US), IPS Group (US), Precise ParkLink (Canada), Infocomm Group (Oman), Verra Mobility (US), Egis Group (France), Passport Labs (US), SpotHero (US), Get My Parking (India), Streetline (US), Cleverciti (Germany), Wayleadr (US), Urbiotica (Spain), CivicSmart (US), Parklio (Croatia), TCS International (US), Parkable (New Zealand), Parkalot (Poland), Parking Telecom (France), and Omnitec (Dubai). These players have adopted various growth strategies, such as partnerships, agreements & collaborations, new product launches, enhancements, and acquisitions, to expand their parking management footprint.

Research Coverage

The market study covers the parking management market size across different segments. It aims to estimate the market size and the growth potential across various segments, including offerings (solutions and services), parking sites, end use, and regions. The study includes an in-depth competitive analysis of the leading market players, their company profiles, key observations related to product and business offerings, recent developments, and market strategies.

Key Benefits of Buying the Report

The report will help market leaders and new entrants with information on the closest approximations of the global parking management market's revenue numbers and subsegments. It will also help stakeholders understand the competitive landscape and gain more insights to position their businesses and plan suitable go-to-market strategies. Moreover, the report will provide insights for stakeholders to understand the market's pulse and provide them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the pointers listed below.

1. Product Development/Innovation: Detailed insights on upcoming technologies, research and development activities, and new product and service launches in the parking management market

2. Market Development: Comprehensive information about lucrative markets - the report analyzes various regions' parking management market

3. Market Diversification: Exhaustive information about new products and services, untapped geographies, recent developments, and investments in the parking management market

4. Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players, such as Amano (Japan), SKIDATA (Austria), Group Indigo (France), Arrive (Sweden), TIBA Parking Systems (Israel), SWARCO (Austria), Chetu (US), INRIX (US), IPS Group (US), Precise ParkLink (Canada), Infocomm Group (Oman), Verra Mobility (US), Egis Group (France), Passport Labs (US), SpotHero (US), Get My Parking (India), Streetline (US), Cleverciti (Germany), Wayleadr (US), Urbiotica (Spain), CivicSmart (US), Parklio (Croatia), TCS International (US), Parkable (New Zealand), Parkalot (Poland), Parking Telecom (France), and Omnitec (Dubai)

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 MARKET SCOPE

- 1.3.1 MARKET SEGMENTATION

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 STAKEHOLDERS

- 1.6 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY DATA

- 2.1.1.1 Secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Primary interviews with experts

- 2.1.2.2 Breakup of primary profiles

- 2.1.2.3 Key industry insights

- 2.1.1 SECONDARY DATA

- 2.2 MARKET SIZE ESTIMATION

- 2.2.1 BOTTOM-UP APPROACH

- 2.2.2 TOP-DOWN APPROACH

- 2.2.3 PARKING MANAGEMENT MARKET ESTIMATION: DEMAND-SIDE ANALYSIS

- 2.3 DATA TRIANGULATION

- 2.4 RISK ASSESSMENT

- 2.5 RESEARCH ASSUMPTIONS

- 2.6 RESEARCH LIMITATIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN PARKING MANAGEMENT MARKET

- 4.2 NORTH AMERICA: PARKING MANAGEMENT MARKET, BY END USE AND COUNTRY

- 4.3 ASIA PACIFIC: PARKING MANAGEMENT MARKET, BY END USE AND COUNTRY

- 4.4 PARKING MANAGEMENT MARKET, BY SEGMENT

5 MARKET OVERVIEW AND INDUSTRY TRENDS

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Rising urbanization and increasing global population density

- 5.2.1.2 Strengthening environmental regulations and sustainability mandates

- 5.2.1.3 Growing demand for seamless traffic flow and reduction in fuel consumption

- 5.2.2 RESTRAINTS

- 5.2.2.1 Shared mobility adoption limits demand for conventional parking infrastructure

- 5.2.2.2 Infrastructure limitations hinder scalability of advanced parking solutions

- 5.2.2.3 Regulatory and policy fragmentation restrain adoption of parking management solutions

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Rising smart city initiatives globally

- 5.2.3.2 Emergence of autonomous cars

- 5.2.3.3 Demand for innovative parking management solutions

- 5.2.4 CHALLENGES

- 5.2.4.1 Inefficient utilization of urban parking spaces

- 5.2.4.2 Revenue management and dynamic pricing complexity

- 5.2.4.3 Scalability limitations and growth management

- 5.2.1 DRIVERS

- 5.3 EVOLUTION OF PARKING MANAGEMENT

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 CASE STUDY ANALYSIS

- 5.5.1 CASE STUDY 1: PRECISE PARKLINK ENHANCED PARKING MANAGEMENT AT VICTORIA INTERNATIONAL AIRPORT

- 5.5.2 CASE STUDY 2: FLASH'S SCAN-TO-PAY TRANSFORMED PARKWELL PORTFOLIO

- 5.5.3 CASE STUDY 3: PASSPORT LABS COVERED MORE GROUND WITH LPR IN CLAYTON, MISSOURI

- 5.6 SUPPLY CHAIN ANALYSIS

- 5.7 PRICING ANALYSIS

- 5.7.1 AVERAGE SELLING PRICE OF KEY PLAYERS, BY SOLUTION AND SERVICE

- 5.7.2 INDICATIVE PRICING ANALYSIS FOR PARKING MANAGEMENT SOLUTIONS (PER MONTH)

- 5.8 TECHNOLOGY ANALYSIS

- 5.8.1 KEY TECHNOLOGIES

- 5.8.1.1 Mobile payment & ticketing systems

- 5.8.1.2 License plate recognition (LPR) systems

- 5.8.1.3 Sensor-based parking guidance (ultrasonic, infrared, magnetic field & micro radar, camera)

- 5.8.1.4 Parking access control hardware

- 5.8.2 COMPLEMENTARY TECHNOLOGIES

- 5.8.2.1 Edge computing

- 5.8.2.2 Digital twin

- 5.8.3 ADJACENT TECHNOLOGIES

- 5.8.3.1 Autonomous vehicles and self-parking technology

- 5.8.3.2 Urban mobility and smart city solutions

- 5.8.3.3 Electric vehicle charging infrastructure management

- 5.8.3.4 AES (Advanced Encryption Standard)

- 5.8.3.5 Data masking

- 5.8.3.6 Encrypted databases

- 5.8.1 KEY TECHNOLOGIES

- 5.9 PATENT ANALYSIS

- 5.9.1 METHODOLOGY

- 5.10 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.11 PORTER'S FIVE FORCES ANALYSIS

- 5.11.1 THREAT OF NEW ENTRANTS

- 5.11.2 THREAT OF SUBSTITUTES

- 5.11.3 BARGAINING POWER OF BUYERS

- 5.11.4 BARGAINING POWER OF SUPPLIERS

- 5.11.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.12 TARIFF AND REGULATORY LANDSCAPE

- 5.12.1 TARIFF RELATED TO PARKING MANAGEMENT (853090)

- 5.12.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.13 KEY STAKEHOLDERS AND BUYING CRITERIA

- 5.13.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 5.13.2 BUYING CRITERIA

- 5.14 KEY CONFERENCES AND EVENTS, 2025-2026

- 5.15 TECHNOLOGY ROADMAP FOR PARKING MANAGEMENT MARKET

- 5.15.1 PARKING MANAGEMENT TECHNOLOGY ROADMAP TILL 2030

- 5.15.1.1 Short-term roadmap (2025-2026)

- 5.15.1.2 Mid-term roadmap (2027-2028)

- 5.15.1.3 Long-term roadmap (2029-2030)

- 5.15.1 PARKING MANAGEMENT TECHNOLOGY ROADMAP TILL 2030

- 5.16 IMPACT OF ARTIFICIAL INTELLIGENCE AND GENERATIVE AI ON PARKING MANAGEMENT

- 5.16.1 USE CASES OF GENERATIVE AI IN PARKING MANAGEMENT

- 5.16.2 FUTURE OF GENERATIVE AI IN PARKING MANAGEMENT

- 5.16.3 BEST PRACTICES TO LEVERAGE AI FOR PARKING MANAGEMENT

- 5.17 INVESTMENT AND FUNDING SCENARIO, 2024

- 5.17.1 PARKING MANAGEMENT MARKET: INVESTMENT AND FUNDING SCENARIO OF MAJOR COMPANIES

- 5.18 CURRENT AND EMERGING BUSINESS MODELS

- 5.18.1 SHARED PARKING

- 5.18.2 SMART PARKING

- 5.18.3 PARKING-AS-A-SERVICE (PAAS)

- 5.18.4 ELECTRIC VEHICLE (EV) CHARGING AND PARKING INTEGRATION

- 5.18.5 MARKETPLACE/AGGREGATION PLATFORMS

- 5.18.6 SUBSCRIPTION-BASED BUSINESS MODELS

- 5.19 PARKING MANAGEMENT SOLUTION BEST PRACTICES

- 5.20 TRADE ANALYSIS

- 5.20.1 EXPORT SCENARIO FOR HS CODE: 8530

- 5.20.2 IMPORT SCENARIO FOR HS CODE: 8530

- 5.21 TOOLS, FRAMEWORKS, AND TECHNIQUES USED IN PARKING MANAGEMENT SOLUTIONS

- 5.22 IMPACT OF 2025 US TARIFF - PARKING MANAGEMENT MARKET

- 5.22.1 INTRODUCTION

- 5.22.2 KEY TARIFF RATES

- 5.22.3 PRICE IMPACT ANALYSIS

- 5.22.4 IMPACT ON COUNTRY/REGION

- 5.22.4.1 US

- 5.22.4.2 Europe

- 5.22.4.3 Asia Pacific

- 5.22.5 IMPACT ON END USERS

- 5.22.5.1 Municipal Governments and Public Authorities

- 5.22.5.2 Commercial Property Owners and Managers

- 5.22.5.3 Transportation Hubs

- 5.22.5.4 Residential Complexes

6 PARKING MANAGEMENT MARKET, BY OFFERING

- 6.1 INTRODUCTION

- 6.1.1 OFFERING: PARKING MANAGEMENT MARKET DRIVERS

- 6.2 SOLUTIONS

- 6.2.1 PARKING ACCESS AND REVENUE CONTROL

- 6.2.1.1 Need for proper organization of vehicles in parking facilities to drive market

- 6.2.2 PARKING ENFORCEMENT MANAGEMENT

- 6.2.2.1 Need for strict adherence to parking rules to drive demand for parking management solutions

- 6.2.3 PARKING RESERVATION MANAGEMENT

- 6.2.3.1 Growing demand for convenience parking spaces to drive market

- 6.2.4 PARKING GUIDANCE

- 6.2.4.1 Rising need for reduced traffic congestion and short travel time to drive market

- 6.2.5 PARKING SECURITY AND SURVEILLANCE

- 6.2.5.1 Growing need to prevent theft and ensure personal safety to drive market

- 6.2.6 PARKING PERMIT MANAGEMENT

- 6.2.6.1 Growing need to manage parking permits to drive market

- 6.2.7 OTHER SOLUTIONS

- 6.2.1 PARKING ACCESS AND REVENUE CONTROL

- 6.3 SERVICES

- 6.3.1 PROFESSIONAL SERVICES

- 6.3.1.1 System integration & deployment

- 6.3.1.1.1 Need to improve decision-making, enhance efficiency, and reduce costs to propel market

- 6.3.1.2 Support & maintenance

- 6.3.1.2.1 Need for enhanced performance of parking management solutions to boost market

- 6.3.1.3 Consulting & training

- 6.3.1.3.1 Need to develop and arrange better practices to address specific management requirements to drive market

- 6.3.1.1 System integration & deployment

- 6.3.2 MANAGED SERVICES

- 6.3.2.1 Requirement for technical skills to maintain and update parking management software to drive demand for managed services

- 6.3.1 PROFESSIONAL SERVICES

7 PARKING MANAGEMENT MARKET, BY PARKING SITE

- 7.1 INTRODUCTION

- 7.1.1 PARKING SITE: PARKING MANAGEMENT MARKET DRIVERS

- 7.2 OFF-STREET PARKING

- 7.2.1 FOCUS ON VEHICLE SECURITY, PRE-BOOKING OF PARKING SPOTS, AND PARKING FEE MANAGEMENT TO BOOST MARKET

- 7.2.2 GARAGE PARKING

- 7.2.2.1 Single-level Garage Parking

- 7.2.2.2 Multi-level/Structured Garage Parking

- 7.2.2.3 Automated Garage Parking

- 7.2.3 LOT PARKING

- 7.3 ON-STREET PARKING

- 7.3.1 AVAILABILITY OF ON-STREET PARKING NEAR COMMERCIAL AREAS TO ENCOURAGE MARKET GROWTH

8 PARKING MANAGEMENT MARKET, BY END USE

- 8.1 INTRODUCTION

- 8.1.1 END USE: PARKING MANAGEMENT MARKET DRIVERS

- 8.2 RESIDENTIAL

- 8.2.1 GROWING NUMBER OF APARTMENT COMPLEXES AND GATED COMMUNITIES TO DRIVE MARKET

- 8.2.2 RESIDENTIAL PARKING MANAGEMENT: USE CASES

- 8.3 COMMERCIAL

- 8.3.1 RISING FOCUS OF COMMERCIAL BUSINESSES ON AUTOMATING PARKING OPERATIONS, TRACKING PARKING REVENUE, AND MANAGING PARKING SPACES TO DRIVE MARKET

- 8.3.2 COMMERCIAL PARKING MANAGEMENT: USE CASES

- 8.4 INDUSTRIAL

- 8.4.1 NEED TO STREAMLINE VEHICLE FLOW AND REDUCE CONGESTION IN INDUSTRIAL ZONES TO DRIVE MARKET

- 8.4.2 INDUSTRIAL PARKING MANAGEMENT: USE CASES

- 8.5 GOVERNMENT/PUBLIC

- 8.5.1 GROWING DEMAND FOR PARKING SPACES IN METROPOLITAN AREAS TO DRIVE MARKET

- 8.5.2 GOVERNMENT/PUBLIC PARKING MANAGEMENT: USE CASES

- 8.6 TRANSPORT & TRANSIT

- 8.6.1 RISING URBAN TRANSIT INTEGRATION BOOSTS DEMAND FOR SMART, EFFICIENT PARKING MANAGEMENT SOLUTIONS

- 8.6.2 TRANSPORT & TRANSIT PARKING MANAGEMENT: USE CASES

9 PARKING MANAGEMENT MARKET, BY REGION

- 9.1 INTRODUCTION

- 9.2 NORTH AMERICA

- 9.2.1 NORTH AMERICA: MACROECONOMIC OUTLOOK

- 9.2.2 US

- 9.2.2.1 Need to decrease traffic and reduce accidents to drive market

- 9.2.3 CANADA

- 9.2.3.1 Rising number of vehicles to drive adoption of parking management solutions

- 9.3 EUROPE

- 9.3.1 EUROPE: MACROECONOMIC OUTLOOK

- 9.3.2 UK

- 9.3.2.1 Adoption of new technologies to transform parking facilities to boost market

- 9.3.3 GERMANY

- 9.3.3.1 Focus of companies on technological advancements to drive market

- 9.3.4 FRANCE

- 9.3.4.1 Rising need to upgrade parking facilities with latest technologies to drive market

- 9.3.5 ITALY

- 9.3.5.1 Use of sensors and mobile apps to monitor real-time parking availability to drive market

- 9.3.6 REST OF EUROPE

- 9.4 ASIA PACIFIC

- 9.4.1 ASIA PACIFIC: MACROECONOMIC OUTLOOK

- 9.4.2 CHINA

- 9.4.2.1 Substantial investments in digital technologies to drive market

- 9.4.3 JAPAN

- 9.4.3.1 Increasing number of vehicles and scarcity of land to boost demand for parking management solutions

- 9.4.4 INDIA

- 9.4.4.1 Increasing adoption of technology-based transportation systems to drive market

- 9.4.5 REST OF ASIA PACIFIC

- 9.5 MIDDLE EAST & AFRICA

- 9.5.1 MIDDLE EAST & AFRICA: MACROECONOMIC OUTLOOK

- 9.5.2 UAE

- 9.5.2.1 Significant investment in parking management to boost market

- 9.5.3 KSA

- 9.5.3.1 Government focus on sustainable urban development to drive market

- 9.5.4 SOUTH AFRICA

- 9.5.4.1 Popularity of mobile application-based parking management solutions to drive market

- 9.5.5 REST OF MIDDLE EAST & AFRICA

- 9.6 LATIN AMERICA

- 9.6.1 LATIN AMERICA: MACROECONOMIC OUTLOOK

- 9.6.2 BRAZIL

- 9.6.2.1 Thriving startup ecosystem to drive popularity of parking management solutions

- 9.6.3 MEXICO

- 9.6.3.1 Growing traffic congestion to fuel demand for smart parking solutions

- 9.6.4 REST OF LATIN AMERICA

10 COMPETITIVE LANDSCAPE

- 10.1 OVERVIEW

- 10.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 10.3 REVENUE ANALYSIS

- 10.4 MARKET SHARE ANALYSIS, 2024

- 10.5 COMPANY VALUATION AND FINANCIAL METRICS

- 10.6 BRAND/PRODUCT COMPARISON

- 10.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2023

- 10.7.1 STARS

- 10.7.2 EMERGING LEADERS

- 10.7.3 PERVASIVE PLAYERS

- 10.7.4 PARTICIPANTS

- 10.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 10.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 10.8.1 PROGRESSIVE COMPANIES

- 10.8.2 RESPONSIVE COMPANIES

- 10.8.3 DYNAMIC COMPANIES

- 10.8.4 STARTING BLOCKS

- 10.8.5 COMPETITIVE BENCHMARKING, 2023

- 10.8.5.1 Detailed list of key startups/SMEs

- 10.9 COMPETITIVE SCENARIO

- 10.9.1 PRODUCT LAUNCHES

- 10.9.2 DEALS

11 COMPANY PROFILES

- 11.1 KEY PLAYERS

- 11.1.1 AMANO

- 11.1.1.1 Business overview

- 11.1.1.2 Products/Solutions/Services offered

- 11.1.1.3 Recent developments

- 11.1.1.3.1 Product launches and enhancements

- 11.1.1.3.2 Deals

- 11.1.1.4 MnM view

- 11.1.1.4.1 Key strengths

- 11.1.1.4.2 Strategic choices

- 11.1.1.4.3 Weaknesses and competitive threats

- 11.1.2 SKIDATA

- 11.1.2.1 Business overview

- 11.1.2.2 Products/Solutions/Services offered

- 11.1.2.3 Recent developments

- 11.1.2.3.1 Product launches

- 11.1.2.3.2 Deals

- 11.1.2.4 MnM view

- 11.1.2.4.1 Key strengths

- 11.1.2.4.2 Strategic choices

- 11.1.2.4.3 Weaknesses and competitive threats

- 11.1.3 GROUP INDIGO

- 11.1.3.1 Business overview

- 11.1.3.2 Products/Solutions/Services offered

- 11.1.3.3 Recent developments

- 11.1.3.3.1 Deals

- 11.1.3.4 MnM view

- 11.1.3.4.1 Key strengths

- 11.1.3.4.2 Strategic choices

- 11.1.3.4.3 Weaknesses and competitive threats

- 11.1.4 ARRIVE

- 11.1.4.1 Business overview

- 11.1.4.2 Products/Solutions/Services offered

- 11.1.4.3 Recent developments

- 11.1.4.3.1 Product launches and enhancements

- 11.1.4.3.2 Deals

- 11.1.4.4 MnM view

- 11.1.4.4.1 Key strengths

- 11.1.4.4.2 Strategic choices

- 11.1.4.4.3 Weaknesses and competitive threats

- 11.1.5 TIBA PARKING SYSTEMS

- 11.1.5.1 Business overview

- 11.1.5.2 Products/Solutions/Services offered

- 11.1.5.3 Recent developments

- 11.1.5.3.1 Product launches and enhancements

- 11.1.5.3.2 Deals

- 11.1.5.4 MnM view

- 11.1.5.4.1 Key strengths

- 11.1.5.4.2 Strategic choices

- 11.1.5.4.3 Weaknesses and competitive threats

- 11.1.6 SWARCO

- 11.1.6.1 Business overview

- 11.1.6.2 Products/Solutions/Services offered

- 11.1.6.3 Recent developments

- 11.1.6.3.1 Product launches and enhancements

- 11.1.6.3.2 Deals

- 11.1.7 CHETU

- 11.1.7.1 Business overview

- 11.1.7.2 Products/Solutions/Services Offered

- 11.1.8 INRIX

- 11.1.8.1 Business overview

- 11.1.8.2 Products/Solutions/Services offered

- 11.1.8.3 Recent developments

- 11.1.8.3.1 Product launches and enhancements

- 11.1.8.3.2 Deals

- 11.1.9 IPS GROUP

- 11.1.9.1 Business overview

- 11.1.9.2 Products/Solutions/Services offered

- 11.1.9.3 Recent developments

- 11.1.9.3.1 Deals

- 11.1.10 PRECISE PARKLINK

- 11.1.10.1 Business overview

- 11.1.10.2 Products/Solutions/Services offered

- 11.1.10.3 Recent developments

- 11.1.10.3.1 Deals

- 11.1.11 VERRA MOBILITY

- 11.1.12 INFOCOMM GROUP

- 11.1.13 EGIS GROUP

- 11.1.1 AMANO

- 11.2 OTHER PLAYERS

- 11.2.1 PASSPORT LABS

- 11.2.2 GET MY PARKING

- 11.2.3 STREETLINE

- 11.2.4 CLEVERCITI

- 11.2.5 SPOTHERO

- 11.2.6 WAYLEADR

- 11.2.7 URBIOTICA

- 11.2.8 CIVICSMART

- 11.2.9 PARKLIO

- 11.2.10 TCS INTERNATIONAL

- 11.2.11 PARKABLE

- 11.2.12 PARKALOT

- 11.2.13 PARKING TELECOM

- 11.2.14 OMNITEC

12 ADJACENT/RELATED MARKETS

- 12.1 INTRODUCTION

- 12.2 TRAFFIC MANAGEMENT MARKET - GLOBAL FORECAST TO 2029

- 12.2.1 MARKET DEFINITION

- 12.2.2 MARKET OVERVIEW

- 12.2.2.1 Traffic management market, by offering

- 12.2.2.2 Traffic management market, by area of application

- 12.2.2.3 Traffic management market, by end user

- 12.2.2.4 Traffic management market, by region

- 12.3 FLEET MANAGEMENT MARKET - GLOBAL FORECAST TO 2028

- 12.3.1 MARKET DEFINITION

- 12.3.2 MARKET OVERVIEW

- 12.3.2.1 Fleet management market, by component

- 12.3.2.2 Fleet management market, by fleet type

- 12.3.2.3 Fleet management market, by vertical

13 APPENDIX

- 13.1 DISCUSSION GUIDE

- 13.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 13.3 CUSTOMIZATION OPTIONS

- 13.4 RELATED REPORTS

- 13.5 AUTHOR DETAILS

List of Tables

- TABLE 1 USD EXCHANGE RATES, 2020-2024

- TABLE 2 RISK ASSESSMENT

- TABLE 3 RESEARCH ASSUMPTIONS

- TABLE 4 SMART CITY INITIATIVES AND INVESTMENTS

- TABLE 5 PARKING MANAGEMENT MARKET: ECOSYSTEM

- TABLE 6 AVERAGE SELLING PRICE OF PARKING MANAGEMENT SOLUTIONS AND SERVICES, BY KEY PLAYER, 2024

- TABLE 7 INDICATIVE PRICING ANALYSIS FOR PARKING MANAGEMENT SOLUTIONS

- TABLE 8 LIST OF PATENTS IN PARKING MANAGEMENT MARKET, 2016-2025

- TABLE 9 IMPACT OF EACH FORCE ON PARKING MANAGEMENT MARKET

- TABLE 10 TARIFF RELATED TO ELECTRICAL SIGNALING, SAFETY, OR TRAFFIC CONTROL EQUIPMENT, BY COUNTRY

- TABLE 11 NORTH AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 12 EUROPE: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 13 ASIA PACIFIC: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 14 REST OF THE WORLD: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 15 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP THREE END USES

- TABLE 16 KEY BUYING CRITERIA FOR TOP THREE END USES

- TABLE 17 PARKING MANAGEMENT MARKET: DETAILED LIST OF CONFERENCES AND EVENTS, 2025-2026

- TABLE 18 US ADJUSTED RECIPROCAL TARIFF RATES

- TABLE 19 PARKING MANAGEMENT MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 20 PARKING MANAGEMENT MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 21 SOLUTIONS: PARKING MANAGEMENT MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 22 SOLUTIONS: PARKING MANAGEMENT MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 23 PARKING MANAGEMENT MARKET, BY SOLUTION, 2020-2024 (USD MILLION)

- TABLE 24 PARKING MANAGEMENT MARKET, BY SOLUTION, 2025-2030 (USD MILLION)

- TABLE 25 PARKING ACCESS AND REVENUE CONTROL: PARKING MANAGEMENT MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 26 PARKING ACCESS AND REVENUE CONTROL: PARKING MANAGEMENT MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 27 PARKING ENFORCEMENT MANAGEMENT: PARKING MANAGEMENT MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 28 PARKING ENFORCEMENT MANAGEMENT: PARKING MANAGEMENT MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 29 PARKING RESERVATION MANAGEMENT: PARKING MANAGEMENT MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 30 PARKING RESERVATION MANAGEMENT: PARKING MANAGEMENT MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 31 PARKING GUIDANCE: PARKING MANAGEMENT MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 32 PARKING GUIDANCE: PARKING MANAGEMENT MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 33 PARKING SECURITY AND SURVEILLANCE: PARKING MANAGEMENT MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 34 PARKING SECURITY AND SURVEILLANCE: PARKING MANAGEMENT MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 35 PARKING PERMIT MANAGEMENT: PARKING MANAGEMENT MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 36 PARKING PERMIT MANAGEMENT: PARKING MANAGEMENT MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 37 OTHER SOLUTIONS: PARKING MANAGEMENT MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 38 OTHER SOLUTIONS: PARKING MANAGEMENT MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 39 SERVICES: PARKING MANAGEMENT MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 40 SERVICES: PARKING MANAGEMENT MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 41 PARKING MANAGEMENT MARKET, BY SERVICE, 2020-2024 (USD MILLION)

- TABLE 42 PARKING MANAGEMENT MARKET, BY SERVICE, 2025-2030 (USD MILLION)

- TABLE 43 PARKING MANAGEMENT MARKET, BY PROFESSIONAL SERVICE, 2020-2024 (USD MILLION)

- TABLE 44 PARKING MANAGEMENT MARKET, BY PROFESSIONAL SERVICE, 2025-2030 (USD MILLION)

- TABLE 45 PROFESSIONAL SERVICES: PARKING MANAGEMENT MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 46 PROFESSIONAL SERVICES: PARKING MANAGEMENT MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 47 SYSTEM INTEGRATION & DEPLOYMENT: PARKING MANAGEMENT MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 48 SYSTEM INTEGRATION & DEPLOYMENT: PARKING MANAGEMENT MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 49 SUPPORT & MAINTENANCE: PARKING MANAGEMENT MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 50 SUPPORT & MAINTENANCE: PARKING MANAGEMENT MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 51 CONSULTING & TRAINING: PARKING MANAGEMENT MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 52 CONSULTING & TRAINING: PARKING MANAGEMENT MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 53 MANAGED SERVICES: PARKING MANAGEMENT MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 54 MANAGED SERVICES: PARKING MANAGEMENT MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 55 PARKING MANAGEMENT MARKET, BY PARKING SITE, 2020-2024 (USD MILLION)

- TABLE 56 PARKING MANAGEMENT MARKET, BY PARKING SITE, 2025-2030 (USD MILLION)

- TABLE 57 OFF-STREET PARKING MANAGEMENT MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 58 OFF-STREET PARKING MANAGEMENT MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 59 OFF-STREET PARKING MANAGEMENT MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 60 OFF-STREET PARKING MANAGEMENT MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 61 GARAGE PARKING: PARKING MANAGEMENT MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 62 GARAGE PARKING: PARKING MANAGEMENT MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 63 GARAGE PARKING: PARKING MANAGEMENT MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 64 GARAGE PARKING: PARKING MANAGEMENT MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 65 SINGLE-LEVEL GARAGE PARKING: PARKING MANAGEMENT MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 66 SINGLE-LEVEL GARAGE PARKING: PARKING MANAGEMENT MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 67 MULTI-LEVEL/STRUCTURED GARAGE PARKING: PARKING MANAGEMENT MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 68 MULTI-LEVEL/STRUCTURED GARAGE PARKING: PARKING MANAGEMENT MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 69 AUTOMATED GARAGE PARKING: PARKING MANAGEMENT MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 70 AUTOMATED GARAGE PARKING: PARKING MANAGEMENT MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 71 LOT PARKING: PARKING MANAGEMENT MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 72 LOT PARKING: PARKING MANAGEMENT MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 73 ON-STREET PARKING MANAGEMENT MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 74 ON-STREET PARKING MANAGEMENT MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 75 PARKING MANAGEMENT MARKET, BY END USE, 2020-2024 (USD MILLION)

- TABLE 76 PARKING MANAGEMENT MARKET, BY END USE, 2025-2030 (USD MILLION)

- TABLE 77 RESIDENTIAL: PARKING MANAGEMENT MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 78 RESIDENTIAL: PARKING MANAGEMENT MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 79 COMMERCIAL: PARKING MANAGEMENT MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 80 COMMERCIAL: PARKING MANAGEMENT MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 81 INDUSTRIAL: PARKING MANAGEMENT MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 82 INDUSTRIAL: PARKING MANAGEMENT MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 83 GOVERNMENT/PUBLIC: PARKING MANAGEMENT MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 84 GOVERNMENT/PUBLIC: PARKING MANAGEMENT MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 85 TRANSPORT & TRANSIT: PARKING MANAGEMENT MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 86 TRANSPORT & TRANSIT: PARKING MANAGEMENT MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 87 PARKING MANAGEMENT MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 88 PARKING MANAGEMENT MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 89 NORTH AMERICA: PARKING MANAGEMENT MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 90 NORTH AMERICA: PARKING MANAGEMENT MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 91 NORTH AMERICA: PARKING MANAGEMENT MARKET, BY SOLUTION, 2020-2024 (USD MILLION)

- TABLE 92 NORTH AMERICA: PARKING MANAGEMENT MARKET, BY SOLUTION, 2025-2030 (USD MILLION)

- TABLE 93 NORTH AMERICA: PARKING MANAGEMENT MARKET, BY SERVICE, 2020-2024 (USD MILLION)

- TABLE 94 NORTH AMERICA: PARKING MANAGEMENT MARKET, BY SERVICE, 2025-2030 (USD MILLION)

- TABLE 95 NORTH AMERICA: PARKING MANAGEMENT MARKET, BY PROFESSIONAL SERVICE, 2020-2024 (USD MILLION)

- TABLE 96 NORTH AMERICA: PARKING MANAGEMENT MARKET, BY PROFESSIONAL SERVICE, 2025-2030 (USD MILLION)

- TABLE 97 NORTH AMERICA: PARKING MANAGEMENT MARKET, BY PARKING SITE, 2020-2024 (USD MILLION)

- TABLE 98 NORTH AMERICA: PARKING MANAGEMENT MARKET, BY PARKING SITE, 2025-2030 (USD MILLION)

- TABLE 99 NORTH AMERICA: PARKING MANAGEMENT MARKET, BY OFF-STREET PARKING, 2020-2024 (USD MILLION)

- TABLE 100 NORTH AMERICA: PARKING MANAGEMENT MARKET, BY OFF-STREET PARKING, 2025-2030 (USD MILLION)

- TABLE 101 NORTH AMERICA: PARKING MANAGEMENT MARKET, BY GARAGE PARKING TYPE, 2020-2024 (USD MILLION)

- TABLE 102 NORTH AMERICA: PARKING MANAGEMENT MARKET, BY GARAGE PARKING TYPE, 2025-2030 (USD MILLION)

- TABLE 103 NORTH AMERICA: PARKING MANAGEMENT MARKET, BY END USE, 2020-2024 (USD MILLION)

- TABLE 104 NORTH AMERICA: PARKING MANAGEMENT MARKET, BY END USE, 2025-2030 (USD MILLION)

- TABLE 105 NORTH AMERICA: PARKING MANAGEMENT MARKET, BY COUNTRY, 2020-2024 (USD MILLION)

- TABLE 106 NORTH AMERICA: PARKING MANAGEMENT MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 107 US: PARKING MANAGEMENT MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 108 US: PARKING MANAGEMENT MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 109 US: PARKING MANAGEMENT MARKET, BY SOLUTION, 2020-2024 (USD MILLION)

- TABLE 110 US: PARKING MANAGEMENT MARKET, BY SOLUTION, 2025-2030 (USD MILLION)

- TABLE 111 US: PARKING MANAGEMENT MARKET, BY SERVICE, 2020-2024 (USD MILLION)

- TABLE 112 US: PARKING MANAGEMENT MARKET, BY SERVICE, 2025-2030 (USD MILLION)

- TABLE 113 US: PARKING MANAGEMENT MARKET, BY PROFESSIONAL SERVICE, 2020-2024 (USD MILLION)

- TABLE 114 US: PARKING MANAGEMENT MARKET, BY PROFESSIONAL SERVICE, 2025-2030 (USD MILLION)

- TABLE 115 US: PARKING MANAGEMENT MARKET, BY PARKING SITE, 2020-2024 (USD MILLION)

- TABLE 116 US: PARKING MANAGEMENT MARKET, BY PARKING SITE, 2025-2030 (USD MILLION)

- TABLE 117 US: PARKING MANAGEMENT MARKET, BY OFF-STREET PARKING, 2020-2024 (USD MILLION)

- TABLE 118 US: PARKING MANAGEMENT MARKET, BY OFF-STREET PARKING, 2025-2030 (USD MILLION)

- TABLE 119 US: PARKING MANAGEMENT MARKET, BY GARAGE PARKING TYPE, 2020-2024 (USD MILLION)

- TABLE 120 US: PARKING MANAGEMENT MARKET, BY GARAGE PARKING TYPE, 2025-2030 (USD MILLION)

- TABLE 121 US: PARKING MANAGEMENT MARKET, BY END USE, 2020-2024 (USD MILLION)

- TABLE 122 US: PARKING MANAGEMENT MARKET, BY END USE, 2025-2030 (USD MILLION)

- TABLE 123 CANADA: PARKING MANAGEMENT MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 124 CANADA: PARKING MANAGEMENT MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 125 CANADA: PARKING MANAGEMENT MARKET, BY SOLUTION, 2020-2024 (USD MILLION)

- TABLE 126 CANADA: PARKING MANAGEMENT MARKET, BY SOLUTION, 2025-2030 (USD MILLION)

- TABLE 127 CANADA: PARKING MANAGEMENT MARKET, BY SERVICE, 2020-2024 (USD MILLION)

- TABLE 128 CANADA: PARKING MANAGEMENT MARKET, BY SERVICE, 2025-2030 (USD MILLION)

- TABLE 129 CANADA: PARKING MANAGEMENT MARKET, BY PROFESSIONAL SERVICE, 2020-2024 (USD MILLION)

- TABLE 130 CANADA: PARKING MANAGEMENT MARKET, BY PROFESSIONAL SERVICE, 2025-2030 (USD MILLION)

- TABLE 131 CANADA: PARKING MANAGEMENT MARKET, BY PARKING SITE, 2020-2024 (USD MILLION)

- TABLE 132 CANADA: PARKING MANAGEMENT MARKET, BY PARKING SITE, 2025-2030 (USD MILLION)

- TABLE 133 CANADA: PARKING MANAGEMENT MARKET, BY OFF-STREET PARKING, 2020-2024 (USD MILLION)

- TABLE 134 CANADA: PARKING MANAGEMENT MARKET, BY OFF-STREET PARKING, 2025-2030 (USD MILLION)

- TABLE 135 CANADA: PARKING MANAGEMENT MARKET, BY GARAGE PARKING TYPE, 2020-2024 (USD MILLION)

- TABLE 136 CANADA: PARKING MANAGEMENT MARKET, BY GARAGE PARKING TYPE, 2025-2030 (USD MILLION)

- TABLE 137 CANADA: PARKING MANAGEMENT MARKET, BY END USE, 2020-2024 (USD MILLION)

- TABLE 138 CANADA: PARKING MANAGEMENT MARKET, BY END USE, 2025-2030 (USD MILLION)

- TABLE 139 EUROPE: PARKING MANAGEMENT MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 140 EUROPE: PARKING MANAGEMENT MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 141 EUROPE: PARKING MANAGEMENT MARKET, BY SOLUTION, 2020-2024 (USD MILLION)

- TABLE 142 EUROPE: PARKING MANAGEMENT MARKET, BY SOLUTION, 2025-2030 (USD MILLION)

- TABLE 143 EUROPE: PARKING MANAGEMENT MARKET, BY SERVICE, 2020-2024 (USD MILLION)

- TABLE 144 EUROPE: PARKING MANAGEMENT MARKET, BY SERVICE, 2025-2030 (USD MILLION)

- TABLE 145 EUROPE: PARKING MANAGEMENT MARKET, BY PROFESSIONAL SERVICE, 2020-2024 (USD MILLION)

- TABLE 146 EUROPE: PARKING MANAGEMENT MARKET, BY PROFESSIONAL SERVICE, 2025-2030 (USD MILLION)

- TABLE 147 EUROPE: PARKING MANAGEMENT MARKET, BY PARKING SITE, 2020-2024 (USD MILLION)

- TABLE 148 EUROPE: PARKING MANAGEMENT MARKET, BY PARKING SITE, 2025-2030 (USD MILLION)

- TABLE 149 EUROPE: PARKING MANAGEMENT MARKET, BY OFF-STREET PARKING, 2020-2024 (USD MILLION)

- TABLE 150 EUROPE: PARKING MANAGEMENT MARKET, BY OFF-STREET PARKING, 2025-2030 (USD MILLION)

- TABLE 151 EUROPE: PARKING MANAGEMENT MARKET, BY GARAGE PARKING TYPE, 2020-2024 (USD MILLION)

- TABLE 152 EUROPE: PARKING MANAGEMENT MARKET, BY GARAGE PARKING TYPE, 2025-2030 (USD MILLION)

- TABLE 153 EUROPE: PARKING MANAGEMENT MARKET, BY END USE, 2020-2024 (USD MILLION)

- TABLE 154 EUROPE: PARKING MANAGEMENT MARKET, BY END USE, 2025-2030 (USD MILLION)

- TABLE 155 EUROPE: PARKING MANAGEMENT MARKET, BY COUNTRY, 2020-2024 (USD MILLION)

- TABLE 156 EUROPE: PARKING MANAGEMENT MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 157 UK: PARKING MANAGEMENT MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 158 UK: PARKING MANAGEMENT MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 159 UK: PARKING MANAGEMENT MARKET, BY SOLUTION, 2020-2024 (USD MILLION)

- TABLE 160 UK: PARKING MANAGEMENT MARKET, BY SOLUTION, 2025-2030 (USD MILLION)

- TABLE 161 UK: PARKING MANAGEMENT MARKET, BY SERVICE, 2020-2024 (USD MILLION)

- TABLE 162 UK: PARKING MANAGEMENT MARKET, BY SERVICE, 2025-2030 (USD MILLION)

- TABLE 163 UK: PARKING MANAGEMENT MARKET, BY PROFESSIONAL SERVICE, 2020-2024 (USD MILLION)

- TABLE 164 UK: PARKING MANAGEMENT MARKET, BY PROFESSIONAL SERVICE, 2025-2030 (USD MILLION)

- TABLE 165 UK: PARKING MANAGEMENT MARKET, BY PARKING SITE, 2020-2024 (USD MILLION)

- TABLE 166 UK: PARKING MANAGEMENT MARKET, BY PARKING SITE, 2025-2030 (USD MILLION)

- TABLE 167 UK: PARKING MANAGEMENT MARKET, BY OFF-STREET PARKING, 2020-2024 (USD MILLION)

- TABLE 168 UK: PARKING MANAGEMENT MARKET, BY OFF-STREET PARKING, 2025-2030 (USD MILLION)

- TABLE 169 UK: PARKING MANAGEMENT MARKET, BY GARAGE PARKING TYPE, 2020-2024 (USD MILLION)

- TABLE 170 UK: PARKING MANAGEMENT MARKET, BY GARAGE PARKING TYPE, 2025-2030 (USD MILLION)

- TABLE 171 UK: PARKING MANAGEMENT MARKET, BY END USE, 2020-2024 (USD MILLION)

- TABLE 172 UK: PARKING MANAGEMENT MARKET, BY END USE, 2025-2030 (USD MILLION)

- TABLE 173 GERMANY: PARKING MANAGEMENT MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 174 GERMANY: PARKING MANAGEMENT MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 175 GERMANY: PARKING MANAGEMENT MARKET, BY SOLUTION, 2020-2024 (USD MILLION)

- TABLE 176 GERMANY: PARKING MANAGEMENT MARKET, BY SOLUTION, 2025-2030 (USD MILLION)

- TABLE 177 GERMANY: PARKING MANAGEMENT MARKET, BY SERVICE, 2020-2024 (USD MILLION)

- TABLE 178 GERMANY: PARKING MANAGEMENT MARKET, BY SERVICE, 2025-2030 (USD MILLION)

- TABLE 179 GERMANY: PARKING MANAGEMENT MARKET, BY PROFESSIONAL SERVICE, 2020-2024 (USD MILLION)

- TABLE 180 GERMANY: PARKING MANAGEMENT MARKET, BY PROFESSIONAL SERVICE, 2025-2030 (USD MILLION)

- TABLE 181 GERMANY: PARKING MANAGEMENT MARKET, BY PARKING SITE, 2020-2024 (USD MILLION)

- TABLE 182 GERMANY: PARKING MANAGEMENT MARKET, BY PARKING SITE, 2025-2030 (USD MILLION)

- TABLE 183 GERMANY: PARKING MANAGEMENT MARKET, BY OFF-STREET PARKING, 2020-2024 (USD MILLION)

- TABLE 184 GERMANY: PARKING MANAGEMENT MARKET, BY OFF-STREET PARKING, 2025-2030 (USD MILLION)

- TABLE 185 GERMANY: PARKING MANAGEMENT MARKET, BY GARAGE PARKING TYPE, 2020-2024 (USD MILLION)

- TABLE 186 GERMANY: PARKING MANAGEMENT MARKET, BY GARAGE PARKING TYPE, 2025-2030 (USD MILLION)

- TABLE 187 GERMANY: PARKING MANAGEMENT MARKET, BY END USE, 2020-2024 (USD MILLION)

- TABLE 188 GERMANY: PARKING MANAGEMENT MARKET, BY END USE, 2025-2030 (USD MILLION)

- TABLE 189 FRANCE: PARKING MANAGEMENT MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 190 FRANCE: PARKING MANAGEMENT MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 191 FRANCE: PARKING MANAGEMENT MARKET, BY SOLUTION, 2020-2024 (USD MILLION)

- TABLE 192 FRANCE: PARKING MANAGEMENT MARKET, BY SOLUTION, 2025-2030 (USD MILLION)

- TABLE 193 FRANCE: PARKING MANAGEMENT MARKET, BY SERVICE, 2020-2024 (USD MILLION)

- TABLE 194 FRANCE: PARKING MANAGEMENT MARKET, BY SERVICE, 2025-2030 (USD MILLION)

- TABLE 195 FRANCE: PARKING MANAGEMENT MARKET, BY PROFESSIONAL SERVICE, 2020-2024 (USD MILLION)

- TABLE 196 FRANCE: PARKING MANAGEMENT MARKET, BY PROFESSIONAL SERVICE, 2025-2030 (USD MILLION)

- TABLE 197 FRANCE: PARKING MANAGEMENT MARKET, BY PARKING SITE, 2020-2024 (USD MILLION)

- TABLE 198 FRANCE: PARKING MANAGEMENT MARKET, BY PARKING SITE, 2025-2030 (USD MILLION)

- TABLE 199 FRANCE: PARKING MANAGEMENT MARKET, BY OFF-STREET PARKING, 2020-2024 (USD MILLION)

- TABLE 200 FRANCE: PARKING MANAGEMENT MARKET, BY OFF-STREET PARKING, 2025-2030 (USD MILLION)

- TABLE 201 FRANCE: PARKING MANAGEMENT MARKET, BY GARAGE PARKING TYPE, 2020-2024 (USD MILLION)

- TABLE 202 FRANCE: PARKING MANAGEMENT MARKET, BY GARAGE PARKING TYPE, 2025-2030 (USD MILLION)

- TABLE 203 FRANCE: PARKING MANAGEMENT MARKET, BY END USE, 2020-2024 (USD MILLION)

- TABLE 204 FRANCE: PARKING MANAGEMENT MARKET, BY END USE, 2025-2030 (USD MILLION)

- TABLE 205 ITALY: PARKING MANAGEMENT MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 206 ITALY: PARKING MANAGEMENT MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 207 ITALY: PARKING MANAGEMENT MARKET, BY SOLUTION, 2020-2024 (USD MILLION)

- TABLE 208 ITALY: PARKING MANAGEMENT MARKET, BY SOLUTION, 2025-2030 (USD MILLION)

- TABLE 209 ITALY: PARKING MANAGEMENT MARKET, BY SERVICE, 2020-2024 (USD MILLION)

- TABLE 210 ITALY: PARKING MANAGEMENT MARKET, BY SERVICE, 2025-2030 (USD MILLION)

- TABLE 211 ITALY: PARKING MANAGEMENT MARKET, BY PROFESSIONAL SERVICE, 2020-2024 (USD MILLION)

- TABLE 212 ITALY: PARKING MANAGEMENT MARKET, BY PROFESSIONAL SERVICE, 2025-2030 (USD MILLION)

- TABLE 213 ITALY: PARKING MANAGEMENT MARKET, BY PARKING SITE, 2020-2024 (USD MILLION)

- TABLE 214 ITALY: PARKING MANAGEMENT MARKET, BY PARKING SITE, 2025-2030 (USD MILLION)

- TABLE 215 ITALY: PARKING MANAGEMENT MARKET, BY OFF-STREET PARKING, 2020-2024 (USD MILLION)

- TABLE 216 ITALY: PARKING MANAGEMENT MARKET, BY OFF-STREET PARKING, 2025-2030 (USD MILLION)

- TABLE 217 ITALY: PARKING MANAGEMENT MARKET, BY GARAGE PARKING TYPE, 2020-2024 (USD MILLION)

- TABLE 218 ITALY: PARKING MANAGEMENT MARKET, BY GARAGE PARKING TYPE, 2025-2030 (USD MILLION)

- TABLE 219 ITALY: PARKING MANAGEMENT MARKET, BY END USE, 2020-2024 (USD MILLION)

- TABLE 220 ITALY: PARKING MANAGEMENT MARKET, BY END USE, 2025-2030 (USD MILLION)

- TABLE 221 ASIA PACIFIC: PARKING MANAGEMENT MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 222 ASIA PACIFIC: PARKING MANAGEMENT MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 223 ASIA PACIFIC: PARKING MANAGEMENT MARKET, BY SOLUTION, 2020-2024 (USD MILLION)

- TABLE 224 ASIA PACIFIC: PARKING MANAGEMENT MARKET, BY SOLUTION, 2025-2030 (USD MILLION)

- TABLE 225 ASIA PACIFIC: PARKING MANAGEMENT MARKET, BY SERVICE, 2020-2024 (USD MILLION)

- TABLE 226 ASIA PACIFIC: PARKING MANAGEMENT MARKET, BY SERVICE, 2025-2030 (USD MILLION)

- TABLE 227 ASIA PACIFIC: PARKING MANAGEMENT MARKET, BY PROFESSIONAL SERVICE, 2020-2024 (USD MILLION)

- TABLE 228 ASIA PACIFIC: PARKING MANAGEMENT MARKET, BY PROFESSIONAL SERVICE, 2025-2030 (USD MILLION)

- TABLE 229 ASIA PACIFIC: PARKING MANAGEMENT MARKET, BY PARKING SITE, 2020-2024 (USD MILLION)

- TABLE 230 ASIA PACIFIC: PARKING MANAGEMENT MARKET, BY PARKING SITE, 2025-2030 (USD MILLION)

- TABLE 231 ASIA PACIFIC: PARKING MANAGEMENT MARKET, BY OFF-STREET PARKING, 2020-2024 (USD MILLION)

- TABLE 232 ASIA PACIFIC: PARKING MANAGEMENT MARKET, BY OFF-STREET PARKING, 2025-2030 (USD MILLION)

- TABLE 233 ASIA PACIFIC: PARKING MANAGEMENT MARKET, BY GARAGE PARKING TYPE, 2020-2024 (USD MILLION)

- TABLE 234 ASIA PACIFIC: PARKING MANAGEMENT MARKET, BY GARAGE PARKING TYPE, 2025-2030 (USD MILLION)

- TABLE 235 ASIA PACIFIC: PARKING MANAGEMENT MARKET, BY END USE, 2020-2024 (USD MILLION)

- TABLE 236 ASIA PACIFIC: PARKING MANAGEMENT MARKET, BY END USE, 2025-2030 (USD MILLION)

- TABLE 237 ASIA PACIFIC: PARKING MANAGEMENT MARKET, BY COUNTRY, 2020-2024 (USD MILLION)

- TABLE 238 ASIA PACIFIC: PARKING MANAGEMENT MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 239 CHINA: PARKING MANAGEMENT MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 240 CHINA: PARKING MANAGEMENT MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 241 CHINA: PARKING MANAGEMENT MARKET, BY SOLUTION, 2020-2024 (USD MILLION)

- TABLE 242 CHINA: PARKING MANAGEMENT MARKET, BY SOLUTION, 2025-2030 (USD MILLION)

- TABLE 243 CHINA: PARKING MANAGEMENT MARKET, BY SERVICE, 2020-2024 (USD MILLION)

- TABLE 244 CHINA: PARKING MANAGEMENT MARKET, BY SERVICE, 2025-2030 (USD MILLION)

- TABLE 245 CHINA: PARKING MANAGEMENT MARKET, BY PROFESSIONAL SERVICE, 2020-2024 (USD MILLION)

- TABLE 246 CHINA: PARKING MANAGEMENT MARKET, BY PROFESSIONAL SERVICE, 2025-2030 (USD MILLION)

- TABLE 247 CHINA: PARKING MANAGEMENT MARKET, BY PARKING SITE, 2020-2024 (USD MILLION)

- TABLE 248 CHINA: PARKING MANAGEMENT MARKET, BY PARKING SITE, 2025-2030 (USD MILLION)

- TABLE 249 CHINA: PARKING MANAGEMENT MARKET, BY OFF-STREET PARKING, 2020-2024 (USD MILLION)

- TABLE 250 CHINA: PARKING MANAGEMENT MARKET, BY OFF-STREET PARKING, 2025-2030 (USD MILLION)

- TABLE 251 CHINA: PARKING MANAGEMENT MARKET, BY GARAGE PARKING TYPE, 2020-2024 (USD MILLION)

- TABLE 252 CHINA: PARKING MANAGEMENT MARKET, BY GARAGE PARKING TYPE, 2025-2030 (USD MILLION)

- TABLE 253 CHINA: PARKING MANAGEMENT MARKET, BY END USE, 2020-2024 (USD MILLION)

- TABLE 254 CHINA: PARKING MANAGEMENT MARKET, BY END USE, 2025-2030 (USD MILLION)

- TABLE 255 JAPAN: PARKING MANAGEMENT MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 256 JAPAN: PARKING MANAGEMENT MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 257 JAPAN: PARKING MANAGEMENT MARKET, BY SOLUTION, 2020-2024 (USD MILLION)

- TABLE 258 JAPAN: PARKING MANAGEMENT MARKET, BY SOLUTION, 2025-2030 (USD MILLION)

- TABLE 259 JAPAN: PARKING MANAGEMENT MARKET, BY SERVICE, 2020-2024 (USD MILLION)

- TABLE 260 JAPAN: PARKING MANAGEMENT MARKET, BY SERVICE, 2025-2030 (USD MILLION)

- TABLE 261 JAPAN: PARKING MANAGEMENT MARKET, BY PROFESSIONAL SERVICE, 2020-2024 (USD MILLION)

- TABLE 262 JAPAN: PARKING MANAGEMENT MARKET, BY PROFESSIONAL SERVICE, 2025-2030 (USD MILLION)

- TABLE 263 JAPAN: PARKING MANAGEMENT MARKET, BY PARKING SITE, 2020-2024 (USD MILLION)

- TABLE 264 JAPAN: PARKING MANAGEMENT MARKET, BY PARKING SITE, 2025-2030 (USD MILLION)

- TABLE 265 JAPAN: PARKING MANAGEMENT MARKET, BY OFF-STREET PARKING, 2020-2024 (USD MILLION)

- TABLE 266 JAPAN: PARKING MANAGEMENT MARKET, BY OFF-STREET PARKING, 2025-2030 (USD MILLION)

- TABLE 267 JAPAN: PARKING MANAGEMENT MARKET, BY GARAGE PARKING TYPE, 2020-2024 (USD MILLION)

- TABLE 268 JAPAN: PARKING MANAGEMENT MARKET, BY GARAGE PARKING TYPE, 2025-2030 (USD MILLION)

- TABLE 269 JAPAN: PARKING MANAGEMENT MARKET, BY END USE, 2020-2024 (USD MILLION)

- TABLE 270 JAPAN: PARKING MANAGEMENT MARKET, BY END USE, 2025-2030 (USD MILLION)

- TABLE 271 INDIA: PARKING MANAGEMENT MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 272 INDIA: PARKING MANAGEMENT MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 273 INDIA: PARKING MANAGEMENT MARKET, BY SOLUTION, 2020-2024 (USD MILLION)

- TABLE 274 INDIA: PARKING MANAGEMENT MARKET, BY SOLUTION, 2025-2030 (USD MILLION)

- TABLE 275 INDIA: PARKING MANAGEMENT MARKET, BY SERVICE, 2020-2024 (USD MILLION)

- TABLE 276 INDIA: PARKING MANAGEMENT MARKET, BY SERVICE, 2025-2030 (USD MILLION)

- TABLE 277 INDIA: PARKING MANAGEMENT MARKET, BY PROFESSIONAL SERVICE, 2020-2024 (USD MILLION)

- TABLE 278 INDIA: PARKING MANAGEMENT MARKET, BY PROFESSIONAL SERVICE, 2025-2030 (USD MILLION)

- TABLE 279 INDIA: PARKING MANAGEMENT MARKET, BY PARKING SITE, 2020-2024 (USD MILLION)

- TABLE 280 INDIA: PARKING MANAGEMENT MARKET, BY PARKING SITE, 2025-2030 (USD MILLION)

- TABLE 281 INDIA: PARKING MANAGEMENT MARKET, BY OFF-STREET PARKING, 2020-2024 (USD MILLION)

- TABLE 282 INDIA: PARKING MANAGEMENT MARKET, BY OFF-STREET PARKING, 2025-2030 (USD MILLION)

- TABLE 283 INDIA: PARKING MANAGEMENT MARKET, BY GARAGE PARKING TYPE, 2020-2024 (USD MILLION)

- TABLE 284 INDIA: PARKING MANAGEMENT MARKET, BY GARAGE PARKING TYPE, 2025-2030 (USD MILLION)

- TABLE 285 INDIA: PARKING MANAGEMENT MARKET, BY END USE, 2020-2024 (USD MILLION)

- TABLE 286 INDIA: PARKING MANAGEMENT MARKET, BY END USE, 2025-2030 (USD MILLION)

- TABLE 287 MIDDLE EAST & AFRICA: PARKING MANAGEMENT MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 288 MIDDLE EAST & AFRICA: PARKING MANAGEMENT MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 289 MIDDLE EAST & AFRICA: PARKING MANAGEMENT MARKET, BY SOLUTION, 2020-2024 (USD MILLION)

- TABLE 290 MIDDLE EAST & AFRICA: PARKING MANAGEMENT MARKET, BY SOLUTION, 2025-2030 (USD MILLION)

- TABLE 291 MIDDLE EAST & AFRICA: PARKING MANAGEMENT MARKET, BY SERVICE, 2020-2024 (USD MILLION)

- TABLE 292 MIDDLE EAST & AFRICA: PARKING MANAGEMENT MARKET, BY SERVICE, 2025-2030 (USD MILLION)

- TABLE 293 MIDDLE EAST & AFRICA: PARKING MANAGEMENT MARKET, BY PROFESSIONAL SERVICE, 2020-2024 (USD MILLION)

- TABLE 294 MIDDLE EAST & AFRICA: PARKING MANAGEMENT MARKET, BY PROFESSIONAL SERVICE, 2025-2030 (USD MILLION)

- TABLE 295 MIDDLE EAST & AFRICA: PARKING MANAGEMENT MARKET, BY PARKING SITE, 2020-2024 (USD MILLION)

- TABLE 296 MIDDLE EAST & AFRICA: PARKING MANAGEMENT MARKET, BY PARKING SITE, 2025-2030 (USD MILLION)

- TABLE 297 MIDDLE EAST & AFRICA: PARKING MANAGEMENT MARKET, BY OFF-STREET PARKING, 2020-2024 (USD MILLION)

- TABLE 298 MIDDLE EAST & AFRICA: PARKING MANAGEMENT MARKET, BY OFF-STREET PARKING, 2025-2030 (USD MILLION)

- TABLE 299 MIDDLE EAST & AFRICA: PARKING MANAGEMENT MARKET, BY GARAGE PARKING TYPE, 2020-2024 (USD MILLION)

- TABLE 300 MIDDLE EAST & AFRICA: PARKING MANAGEMENT MARKET, BY GARAGE PARKING TYPE, 2025-2030 (USD MILLION)

- TABLE 301 MIDDLE EAST & AFRICA: PARKING MANAGEMENT MARKET, BY END USE, 2020-2024 (USD MILLION)

- TABLE 302 MIDDLE EAST & AFRICA: PARKING MANAGEMENT MARKET, BY END USE, 2025-2030 (USD MILLION)

- TABLE 303 MIDDLE EAST & AFRICA: PARKING MANAGEMENT MARKET, BY COUNTRY, 2020-2024 (USD MILLION)

- TABLE 304 MIDDLE EAST & AFRICA: PARKING MANAGEMENT MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 305 UAE: PARKING MANAGEMENT MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 306 UAE: PARKING MANAGEMENT MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 307 UAE: PARKING MANAGEMENT MARKET, BY SOLUTION, 2020-2024 (USD MILLION)

- TABLE 308 UAE: PARKING MANAGEMENT MARKET, BY SOLUTION, 2025-2030 (USD MILLION)

- TABLE 309 UAE: PARKING MANAGEMENT MARKET, BY SERVICE, 2020-2024 (USD MILLION)

- TABLE 310 UAE: PARKING MANAGEMENT MARKET, BY SERVICE, 2025-2030 (USD MILLION)

- TABLE 311 UAE: PARKING MANAGEMENT MARKET, BY PROFESSIONAL SERVICE, 2020-2024 (USD MILLION)

- TABLE 312 UAE: PARKING MANAGEMENT MARKET, BY PROFESSIONAL SERVICE, 2025-2030 (USD MILLION)

- TABLE 313 UAE: PARKING MANAGEMENT MARKET, BY PARKING SITE, 2020-2024 (USD MILLION)

- TABLE 314 UAE: PARKING MANAGEMENT MARKET, BY PARKING SITE, 2025-2030 (USD MILLION)

- TABLE 315 UAE: PARKING MANAGEMENT MARKET, BY OFF-STREET PARKING, 2020-2024 (USD MILLION)

- TABLE 316 UAE: PARKING MANAGEMENT MARKET, BY OFF-STREET PARKING, 2025-2030 (USD MILLION)

- TABLE 317 UAE: PARKING MANAGEMENT MARKET, BY GARAGE PARKING TYPE, 2020-2024 (USD MILLION)

- TABLE 318 UAE: PARKING MANAGEMENT MARKET, BY GARAGE PARKING TYPE, 2025-2030 (USD MILLION)

- TABLE 319 UAE: PARKING MANAGEMENT MARKET, BY END USE, 2020-2024 (USD MILLION)

- TABLE 320 UAE: PARKING MANAGEMENT MARKET, BY END USE, 2025-2030 (USD MILLION)

- TABLE 321 KSA: PARKING MANAGEMENT MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 322 KSA: PARKING MANAGEMENT MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 323 KSA: PARKING MANAGEMENT MARKET, BY SOLUTION, 2020-2024 (USD MILLION)

- TABLE 324 KSA: PARKING MANAGEMENT MARKET, BY SOLUTION, 2025-2030 (USD MILLION)

- TABLE 325 KSA: PARKING MANAGEMENT MARKET, BY SERVICE, 2020-2024 (USD MILLION)

- TABLE 326 KSA: PARKING MANAGEMENT MARKET, BY SERVICE, 2025-2030 (USD MILLION)

- TABLE 327 KSA: PARKING MANAGEMENT MARKET, BY PROFESSIONAL SERVICE, 2020-2024 (USD MILLION)

- TABLE 328 KSA: PARKING MANAGEMENT MARKET, BY PROFESSIONAL SERVICE, 2025-2030 (USD MILLION)

- TABLE 329 KSA: PARKING MANAGEMENT MARKET, BY PARKING SITE, 2020-2024 (USD MILLION)

- TABLE 330 KSA: PARKING MANAGEMENT MARKET, BY PARKING SITE, 2025-2030 (USD MILLION)

- TABLE 331 KSA: PARKING MANAGEMENT MARKET, BY OFF-STREET PARKING, 2020-2024 (USD MILLION)

- TABLE 332 KSA: PARKING MANAGEMENT MARKET, BY OFF-STREET PARKING, 2025-2030 (USD MILLION)

- TABLE 333 KSA: PARKING MANAGEMENT MARKET, BY GARAGE PARKING TYPE, 2020-2024 (USD MILLION)

- TABLE 334 KSA: PARKING MANAGEMENT MARKET, BY GARAGE PARKING TYPE, 2025-2030 (USD MILLION)

- TABLE 335 KSA: PARKING MANAGEMENT MARKET, BY END USE, 2020-2024 (USD MILLION)

- TABLE 336 KSA: PARKING MANAGEMENT MARKET, BY END USE, 2025-2030 (USD MILLION)

- TABLE 337 SOUTH AFRICA: PARKING MANAGEMENT MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 338 SOUTH AFRICA: PARKING MANAGEMENT MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 339 SOUTH AFRICA: PARKING MANAGEMENT MARKET, BY SOLUTION, 2020-2024 (USD MILLION)

- TABLE 340 SOUTH AFRICA: PARKING MANAGEMENT MARKET, BY SOLUTION, 2025-2030 (USD MILLION)

- TABLE 341 SOUTH AFRICA: PARKING MANAGEMENT MARKET, BY SERVICE, 2020-2024 (USD MILLION)

- TABLE 342 SOUTH AFRICA: PARKING MANAGEMENT MARKET, BY SERVICE, 2025-2030 (USD MILLION)

- TABLE 343 SOUTH AFRICA: PARKING MANAGEMENT MARKET, BY PROFESSIONAL SERVICE, 2020-2024 (USD MILLION)

- TABLE 344 SOUTH AFRICA: PARKING MANAGEMENT MARKET, BY PROFESSIONAL SERVICE, 2025-2030 (USD MILLION)

- TABLE 345 SOUTH AFRICA: PARKING MANAGEMENT MARKET, BY PARKING SITE, 2020-2024 (USD MILLION)

- TABLE 346 SOUTH AFRICA: PARKING MANAGEMENT MARKET, BY PARKING SITE, 2025-2030 (USD MILLION)

- TABLE 347 SOUTH AFRICA: PARKING MANAGEMENT MARKET, BY OFF-STREET PARKING, 2020-2024 (USD MILLION)

- TABLE 348 SOUTH AFRICA: PARKING MANAGEMENT MARKET, BY OFF-STREET PARKING, 2025-2030 (USD MILLION)

- TABLE 349 SOUTH AFRICA: PARKING MANAGEMENT MARKET, BY GARAGE PARKING TYPE, 2020-2024 (USD MILLION)

- TABLE 350 SOUTH AFRICA: PARKING MANAGEMENT MARKET, BY GARAGE PARKING TYPE, 2025-2030 (USD MILLION)

- TABLE 351 SOUTH AFRICA: PARKING MANAGEMENT MARKET, BY END USE, 2020-2024 (USD MILLION)

- TABLE 352 SOUTH AFRICA: PARKING MANAGEMENT MARKET, BY END USE, 2025-2030 (USD MILLION)

- TABLE 353 LATIN AMERICA: PARKING MANAGEMENT MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 354 LATIN AMERICA: PARKING MANAGEMENT MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 355 LATIN AMERICA: PARKING MANAGEMENT MARKET, BY SOLUTION, 2020-2024 (USD MILLION)

- TABLE 356 LATIN AMERICA: PARKING MANAGEMENT MARKET, BY SOLUTION, 2025-2030 (USD MILLION)

- TABLE 357 LATIN AMERICA: PARKING MANAGEMENT MARKET, BY SERVICE, 2020-2024 (USD MILLION)

- TABLE 358 LATIN AMERICA: PARKING MANAGEMENT MARKET, BY SERVICE, 2025-2030 (USD MILLION)

- TABLE 359 LATIN AMERICA: PARKING MANAGEMENT MARKET, BY PROFESSIONAL SERVICE, 2020-2024 (USD MILLION)

- TABLE 360 LATIN AMERICA: PARKING MANAGEMENT MARKET, BY PROFESSIONAL SERVICE, 2025-2030 (USD MILLION)

- TABLE 361 LATIN AMERICA: PARKING MANAGEMENT MARKET, BY PARKING SITE, 2020-2024 (USD MILLION)

- TABLE 362 LATIN AMERICA: PARKING MANAGEMENT MARKET, BY PARKING SITE, 2025-2030 (USD MILLION)

- TABLE 363 LATIN AMERICA: PARKING MANAGEMENT MARKET, BY OFF-STREET PARKING, 2020-2024 (USD MILLION)

- TABLE 364 LATIN AMERICA: PARKING MANAGEMENT MARKET, BY OFF-STREET PARKING, 2025-2030 (USD MILLION)

- TABLE 365 LATIN AMERICA: PARKING MANAGEMENT MARKET, BY GARAGE PARKING TYPE, 2020-2024 (USD MILLION)

- TABLE 366 LATIN AMERICA: PARKING MANAGEMENT MARKET, BY GARAGE PARKING TYPE, 2025-2030 (USD MILLION)

- TABLE 367 LATIN AMERICA: PARKING MANAGEMENT MARKET, BY END USE, 2020-2024 (USD MILLION)

- TABLE 368 LATIN AMERICA: PARKING MANAGEMENT MARKET, BY END USE, 2025-2030 (USD MILLION)

- TABLE 369 LATIN AMERICA: PARKING MANAGEMENT MARKET, BY COUNTRY, 2020-2024 (USD MILLION)

- TABLE 370 LATIN AMERICA: PARKING MANAGEMENT MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 371 BRAZIL: PARKING MANAGEMENT MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 372 BRAZIL: PARKING MANAGEMENT MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 373 BRAZIL: PARKING MANAGEMENT MARKET, BY SOLUTION, 2020-2024 (USD MILLION)

- TABLE 374 BRAZIL: PARKING MANAGEMENT MARKET, BY SOLUTION, 2025-2030 (USD MILLION)

- TABLE 375 BRAZIL: PARKING MANAGEMENT MARKET, BY SERVICE, 2020-2024 (USD MILLION)

- TABLE 376 BRAZIL: PARKING MANAGEMENT MARKET, BY SERVICE, 2025-2030 (USD MILLION)

- TABLE 377 BRAZIL: PARKING MANAGEMENT MARKET, BY PROFESSIONAL SERVICE, 2020-2024 (USD MILLION)

- TABLE 378 BRAZIL: PARKING MANAGEMENT MARKET, BY PROFESSIONAL SERVICE, 2025-2030 (USD MILLION)

- TABLE 379 BRAZIL: PARKING MANAGEMENT MARKET, BY PARKING SITE, 2020-2024 (USD MILLION)

- TABLE 380 BRAZIL: PARKING MANAGEMENT MARKET, BY PARKING SITE, 2025-2030 (USD MILLION)

- TABLE 381 BRAZIL: PARKING MANAGEMENT MARKET, BY OFF-STREET PARKING, 2020-2024 (USD MILLION)

- TABLE 382 BRAZIL: PARKING MANAGEMENT MARKET, BY OFF-STREET PARKING, 2025-2030 (USD MILLION)

- TABLE 383 BRAZIL: PARKING MANAGEMENT MARKET, BY GARAGE PARKING TYPE, 2020-2024 (USD MILLION)

- TABLE 384 BRAZIL: PARKING MANAGEMENT MARKET, BY GARAGE PARKING TYPE, 2025-2030 (USD MILLION)

- TABLE 385 BRAZIL: PARKING MANAGEMENT MARKET, BY END USE, 2020-2024 (USD MILLION)

- TABLE 386 BRAZIL: PARKING MANAGEMENT MARKET, BY END USE, 2025-2030 (USD MILLION)

- TABLE 387 MEXICO: PARKING MANAGEMENT MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 388 MEXICO: PARKING MANAGEMENT MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 389 MEXICO: PARKING MANAGEMENT MARKET, BY SOLUTION, 2020-2024 (USD MILLION)

- TABLE 390 MEXICO: PARKING MANAGEMENT MARKET, BY SOLUTION, 2025-2030 (USD MILLION)

- TABLE 391 MEXICO: PARKING MANAGEMENT MARKET, BY SERVICE, 2020-2024 (USD MILLION)

- TABLE 392 MEXICO: PARKING MANAGEMENT MARKET, BY SERVICE, 2025-2030 (USD MILLION)

- TABLE 393 MEXICO: PARKING MANAGEMENT MARKET, BY PROFESSIONAL SERVICE, 2020-2024 (USD MILLION)

- TABLE 394 MEXICO: PARKING MANAGEMENT MARKET, BY PROFESSIONAL SERVICE, 2025-2030 (USD MILLION)

- TABLE 395 MEXICO: PARKING MANAGEMENT MARKET, BY PARKING SITE, 2020-2024 (USD MILLION)

- TABLE 396 MEXICO: PARKING MANAGEMENT MARKET, BY PARKING SITE, 2025-2030 (USD MILLION)

- TABLE 397 MEXICO: PARKING MANAGEMENT MARKET, BY OFF-STREET PARKING, 2020-2024 (USD MILLION)

- TABLE 398 MEXICO: PARKING MANAGEMENT MARKET, BY OFF-STREET PARKING, 2025-2030 (USD MILLION)

- TABLE 399 MEXICO: PARKING MANAGEMENT MARKET, BY GARAGE PARKING TYPE, 2020-2024 (USD MILLION)

- TABLE 400 MEXICO: PARKING MANAGEMENT MARKET, BY GARAGE PARKING TYPE, 2025-2030 (USD MILLION)

- TABLE 401 MEXICO: PARKING MANAGEMENT MARKET, BY END USE, 2020-2024 (USD MILLION)

- TABLE 402 MEXICO: PARKING MANAGEMENT MARKET, BY END USE, 2025-2030 (USD MILLION)

- TABLE 403 OVERVIEW OF STRATEGIES ADOPTED BY KEY PLAYERS IN PARKING MANAGEMENT MARKET

- TABLE 404 PARKING MANAGEMENT MARKET: DEGREE OF COMPETITION

- TABLE 405 PARKING MANAGEMENT MARKET: REGION FOOTPRINT

- TABLE 406 PARKING MANAGEMENT MARKET: OFFERING FOOTPRINT

- TABLE 407 PARKING MANAGEMENT MARKET: PARKING SITE FOOTPRINT

- TABLE 408 PARKING MANAGEMENT MARKET: END USE FOOTPRINT

- TABLE 409 PARKING MANAGEMENT MARKET: DETAILED LIST OF KEY STARTUPS/SMES

- TABLE 410 PARKING MANAGEMENT MARKET: COMPETITIVE BENCHMARKING OF STARTUP/SMES

- TABLE 411 PARKING MANAGEMENT MARKET: PRODUCT LAUNCHES, JANUARY 2022-MAY 2025

- TABLE 412 PARKING MANAGEMENT MARKET: DEALS, JANUARY 2022-JULY 2025

- TABLE 413 AMANO: COMPANY OVERVIEW

- TABLE 414 AMANO: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 415 AMANO: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 416 AMANO: DEALS

- TABLE 417 SKIDATA: COMPANY OVERVIEW

- TABLE 418 SKIDATA: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 419 SKIDATA: PRODUCT LAUNCHES

- TABLE 420 SKIDATA: DEALS

- TABLE 421 GROUP INDIGO: COMPANY OVERVIEW

- TABLE 422 GROUP INDIGO: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 423 GROUP INDIGO: DEALS

- TABLE 424 ARRIVE: COMPANY OVERVIEW

- TABLE 425 ARRIVE: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 426 ARRIVE: PRODUCT LAUNCHES AND ENHANCEMENT

- TABLE 427 ARRIVE: DEALS

- TABLE 428 TIBA PARKING SYSTEMS: COMPANY OVERVIEW

- TABLE 429 TIBA PARKING SYSTEMS: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 430 TIBA PARKING SYSTEMS: PRODUCT LAUNCHES AND ENHANCEMENT

- TABLE 431 TIBA PARKING SYSTEMS: DEALS

- TABLE 432 SWARCO: COMPANY OVERVIEW

- TABLE 433 SWARCO: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 434 SWARCO: PRODUCT LAUNCHES AND ENHANCEMENT

- TABLE 435 SWARCO: DEALS

- TABLE 436 CHETU: COMPANY OVERVIEW

- TABLE 437 CHETU: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 438 INRIX: COMPANY OVERVIEW

- TABLE 439 INRIX: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 440 INRIX: PRODUCT LAUNCHES AND ENHANCEMENT

- TABLE 441 INRIX: DEALS

- TABLE 442 IPS GROUP: COMPANY OVERVIEW

- TABLE 443 IPS GROUP: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 444 IPS GROUP: DEALS

- TABLE 445 PRECISE PARKLINK: COMPANY OVERVIEW

- TABLE 446 PRECISE PARKLINK: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 447 PRECISE PARKLINK: DEALS

- TABLE 448 TRAFFIC MANAGEMENT MARKET, BY OFFERING, 2019-2023 (USD MILLION)

- TABLE 449 TRAFFIC MANAGEMENT MARKET, BY OFFERING, 2024-2029 (USD MILLION)

- TABLE 450 TRAFFIC MANAGEMENT MARKET, BY AREA OF APPLICATION, 2019-2023 (USD MILLION)

- TABLE 451 TRAFFIC MANAGEMENT MARKET, BY AREA OF APPLICATION, 2024-2029 (USD MILLION)

- TABLE 452 TRAFFIC MANAGEMENT MARKET, BY END USER, 2019-2023 (USD MILLION)

- TABLE 453 TRAFFIC MANAGEMENT MARKET, BY END USER, 2024-2029 (USD MILLION)

- TABLE 454 TRAFFIC MANAGEMENT MARKET, BY REGION, 2019-2023 (USD MILLION)

- TABLE 455 TRAFFIC MANAGEMENT MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 456 FLEET MANAGEMENT MARKET, BY COMPONENT, 2018-2022 (USD MILLION)

- TABLE 457 FLEET MANAGEMENT MARKET, BY COMPONENT, 2023-2028 (USD MILLION)

- TABLE 458 FLEET MANAGEMENT MARKET, BY FLEET TYPE, 2018-2022 (USD MILLION)

- TABLE 459 FLEET MANAGEMENT MARKET, BY FLEET TYPE, 2023-2028 (USD MILLION)

- TABLE 460 FLEET MANAGEMENT MARKET, BY VERTICAL, 2018-2022 (USD MILLION)

- TABLE 461 FLEET MANAGEMENT MARKET, BY VERTICAL, 2023-2028 (USD MILLION)

List of Figures

- FIGURE 1 PARKING MANAGEMENT MARKET SEGMENTATION

- FIGURE 2 PARKING MANAGEMENT MARKET: RESEARCH DESIGN

- FIGURE 3 BREAKUP OF PROFILES OF PRIMARY PARTICIPANTS, BY COMPANY TYPE, DESIGNATION, AND REGION

- FIGURE 4 BOTTOM-UP APPROACH

- FIGURE 5 MARKET SIZE ESTIMATION METHODOLOGY, BOTTOM-UP (SUPPLY-SIDE): COLLECTIVE REVENUE FROM SOLUTIONS/SERVICES OF PARKING MANAGEMENT MARKET

- FIGURE 6 TOP-DOWN APPROACH

- FIGURE 7 DATA TRIANGULATION

- FIGURE 8 PARKING MANAGEMENT MARKET, 2023-2030

- FIGURE 9 PARKING MANAGEMENT MARKET: REGIONAL SNAPSHOT

- FIGURE 10 GROWING DEMAND FOR EFFICIENT URBAN TRAFFIC FLOW AND REDUCED CONGESTION TO DRIVE MARKET

- FIGURE 11 COMMERCIAL SEGMENT AND US TO ACCOUNT FOR LARGEST SHARES OF NORTH AMERICAN PARKING MANAGEMENT MARKET IN 2025

- FIGURE 12 COMMERCIAL SEGMENT AND CHINA TO ACCOUNT FOR LARGEST SHARES OF ASIA PACIFIC PARKING MANAGEMENT MARKET IN 2025

- FIGURE 13 LEADING SEGMENTS IN PARKING MANAGEMENT MARKET, 2025

- FIGURE 14 PARKING MANAGEMENT MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

- FIGURE 15 EVOLUTION OF PARKING MANAGEMENT

- FIGURE 16 PARKING MANAGEMENT MARKET ECOSYSTEM

- FIGURE 17 PARKING MANAGEMENT MARKET: SUPPLY CHAIN ANALYSIS

- FIGURE 18 AVERAGE SELLING PRICE OF KEY PLAYERS, BY SOLUTION AND SERVICE (PER MONTH), 2024

- FIGURE 19 LIST OF MAJOR PATENTS FOR PARKING MANAGEMENT

- FIGURE 20 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- FIGURE 21 PARKING MANAGEMENT MARKET: PORTER'S FIVE FORCES MODEL

- FIGURE 22 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP THREE END USES

- FIGURE 23 KEY BUYING CRITERIA FOR TOP THREE END USES

- FIGURE 24 TOTAL FUNDING VALUE AND NUMBER OF ROUNDS, BY KEY PLAYER

- FIGURE 25 EXPORT VALUE OF ELECTRICAL SIGNALING, SAFETY, OR TRAFFIC CONTROL EQUIPMENT, BY COUNTRY, 2015-2024 (USD MILLION)

- FIGURE 26 IMPORT VALUE OF ELECTRICAL SIGNALING, SAFETY, OR TRAFFIC CONTROL EQUIPMENT, BY COUNTRY, 2015-2024 (USD MILLION)

- FIGURE 27 SERVICES SEGMENT TO REGISTER HIGHER CAGR DURING FORECAST PERIOD

- FIGURE 28 PARKING RESERVATION MANAGEMENT TO REGISTER HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 29 MANAGED SERVICES SEGMENT TO REGISTER HIGHER CAGR DURING FORECAST PERIOD

- FIGURE 30 ON-STREET PARKING SEGMENT TO REGISTER HIGHER CAGR DURING FORECAST PERIOD

- FIGURE 31 RESIDENTIAL SEGMENT TO REGISTER HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 32 NORTH AMERICA: PARKING MANAGEMENT MARKET SNAPSHOT

- FIGURE 33 ASIA PACIFIC: PARKING MANAGEMENT MARKET SNAPSHOT

- FIGURE 34 PARKING MANAGEMENT MARKET: REVENUE ANALYSIS OF KEY PLAYERS, 2020-2024

- FIGURE 35 PARKING MANAGEMENT MARKET: MARKET SHARE ANALYSIS

- FIGURE 36 FINANCIAL METRICS OF PARKING MANAGEMENT VENDORS

- FIGURE 37 COMPANY VALUATION OF PARKING MANAGEMENT VENDORS

- FIGURE 38 BRAND/PRODUCT COMPARISON

- FIGURE 39 PARKING MANAGEMENT MARKET: COMPANY EVALUATION MATRIX (KEY PLAYERS), 2024

- FIGURE 40 PARKING MANAGEMENT MARKET: COMPANY FOOTPRINT

- FIGURE 41 PARKING MANAGEMENT MARKET: COMPANY EVALUATION MATRIX (STARTUPS/SMES), 2024

- FIGURE 42 AMANO: COMPANY SNAPSHOT

- FIGURE 43 GROUP INDIGO: COMPANY SNAPSHOT

停车设施管理软体市场按设备、部署模式、应用程式和最终用户划分,全球预测(2026-2032年)

停车设施管理软体市场按设备、部署模式、应用程式和最终用户划分,全球预测(2026-2032年) 停车管理解决方案市场分析及预测(至2035年):按类型、产品、服务、技术、组件、应用、部署类型、最终用户和解决方案划分

停车管理解决方案市场分析及预测(至2035年):按类型、产品、服务、技术、组件、应用、部署类型、最终用户和解决方案划分 停车管理市场(至 2035 年):按组件、解决方案、停车地点、部署类型、用途、公司规模、商业模式、最终用户和地区划分:行业趋势和全球市场趋势按组件、技术、部署类型、最终用户和组织规模分類的停车管理系统软体市场 - 全球预测 2026-2032按组织规模、销售管道、应用、部署类型和最终用户分類的停车管理软体市场 - 全球预测 2026-2032

停车管理市场(至 2035 年):按组件、解决方案、停车地点、部署类型、用途、公司规模、商业模式、最终用户和地区划分:行业趋势和全球市场趋势按组件、技术、部署类型、最终用户和组织规模分類的停车管理系统软体市场 - 全球预测 2026-2032按组织规模、销售管道、应用、部署类型和最终用户分類的停车管理软体市场 - 全球预测 2026-2032 停车管理:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

停车管理:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 停车管理市场规模、份额和成长分析(按产品、部署类型、停车地点、最终用途和地区划分)—产业预测,2026-2033年

停车管理市场规模、份额和成长分析(按产品、部署类型、停车地点、最终用途和地区划分)—产业预测,2026-2033年 停车管理系统市场规模、份额和成长分析(按组件、部署方式、停车位置、解决方案、最终用户产业和地区划分)- 产业预测(2026-2033 年)

停车管理系统市场规模、份额和成长分析(按组件、部署方式、停车位置、解决方案、最终用户产业和地区划分)- 产业预测(2026-2033 年) 停车管理市场规模、份额和趋势分析报告:按组件、部署类型、停车地点、应用、地区和细分市场预测(2026-2033 年)

停车管理市场规模、份额和趋势分析报告:按组件、部署类型、停车地点、应用、地区和细分市场预测(2026-2033 年) 欧洲和美国路边管理成长机会(2025-2030 年)

欧洲和美国路边管理成长机会(2025-2030 年)