|

市场调查报告书

商品编码

1856920

全球病患安全与风险软体市场按功能、部署模式、最终用户和地区划分-预测至2030年Patient Safety and Risk Software Market by Function (Incident Reporting, Compliance, Clinical Safety, Claims Management), End User, Deployment, and Region - Global Forecasts to 2030 |

||||||

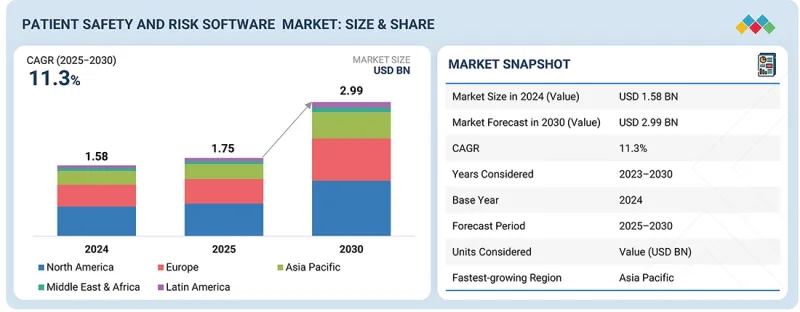

全球病患安全与风险软体市场预计将从 2025 年的 17.5 亿美元成长到 2030 年的 29.9 亿美元,预测期内复合年增长率将达到 11.36%。

病人安全和风险软体市场已成为全球医疗保健系统关注的重点,旨在最大限度地减少医疗差错并提高医疗品质。不利事件发生率的上升、医疗服务日益复杂化以及向价值导向医疗模式的转变,都在推动该市场的成长。

| 调查范围 | |

|---|---|

| 调查年度 | 2024-2030 |

| 基准年 | 2024 |

| 预测期 | 2025-2030 |

| 考虑单位 | 金额(十亿美元) |

| 部分 | 按功能、部署模式、最终用户和区域划分 |

| 目标区域 | 北美、欧洲、亚太地区、拉丁美洲、中东和非洲 |

美国食品药物管理局 (FDA)、欧洲药品管理局 (EMA) 和联合委员会等法规结构要求严格的报告、监测和合规性,迫使医疗保健和生命科学公司采用先进的患者安全风险管理 (PSRM) 解决方案。同时,美国卫生与公众服务部病人安全计画和欧盟药物安全检测法规等政府措施正在加速这些解决方案的普及。然而,高昂的实施成本、缺乏全球标准化、与旧有系统整合难题以及安全事件报告不足等障碍仍然限制这些解决方案的广泛应用。

在预测期内,合规与管治板块预计将成为成长最快的板块,这主要得益于各方日益重视满足监管要求和维护医疗营运透明度。监管机构日益严格的审查,以及对标准化报告和审核追踪的需求,正促使医疗机构采用先进的合规管理解决方案。这些工具透过确保遵守品质标准、资料保护条例和病患安全通讯协定,帮助降低风险并提高整个医疗生态系统的营运效率。

云端基础方案是成长最快的细分市场,这主要得益于数位医疗技术的日益普及以及向灵活可扩展部署模式的转变。云端解决方案可在医疗环境中提供无缝的资料存取、互通性和即时协作,从而加快决策速度并提高病患安全。此外,更低的初始成本、更少的IT基础设施需求以及透过进阶加密和合规措施增强的资料安全性,进一步加速了云端基础平台在该市场的普及。

亚太地区预计将成为患者安全和风险软体市场复合年增长率最高的地区,这主要得益于前所未有的医疗数位化、政府倡议以及大量的技术投资。例如,中国的智慧医院计画旨在2025年为超过1000家公立医院升级整合IT解决方案。医疗事故的增加、医疗基础设施的扩建以及印度、中国和东南亚等新兴经济体电子健康记录/电子病历(EHR/EMR)整合度的提高,进一步推动了相关技术的应用。该地区製药和医疗设备产业的扩张以及病患数量的成长,也催生了对高效风险管理和安全解决方案的强劲需求。

本报告对全球患者安全和风险软体市场进行了分析,按功能、部署模式、最终用户和地理趋势进行了细分,并对参与该市场的公司进行了概况介绍。

目录

第一章 引言

第二章调查方法

第三章执行摘要

第四章重要考察

第五章 市场概览

- 介绍

- 市场动态

- 产业趋势

- 影响客户业务的趋势/颠覆性因素

- 定价分析

- 价值链分析

- 生态系分析

- 投资和资金筹措方案

- 技术分析

- 专利分析

- 2025年至2027年主要会议及活动

- 案例研究分析

- 监管状态

- 波特五力分析

- 主要相关人员和采购标准

- 终端用户分析

- 经营模式

- 人工智慧/生成式人工智慧对病人安全和风险软体市场的影响

- 2025年美国关税的影响

6. 病人安全与风险软体市场(依功能划分)

- 介绍

- 风险与安全管理

- 合规与管治

- 临床安全管理

- 财务和法律风险管理

7. 按部署模式分類的病患安全与风险软体市场

- 介绍

- 本地部署

- 云端基础的部署

- 混合部署

8. 病人安全与风险软体市场(依最终使用者划分)

- 介绍

- 医疗保健提供者

- 製药和生物技术公司

- 医疗保健支付方

- 医疗技术公司

- 其他的

9. 各地区病患安全与风险软体市场

- 介绍

- 北美洲

- 北美宏观经济展望

- 美国

- 加拿大

- 欧洲

- 欧洲宏观经济展望

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 其他的

- 亚太地区

- 亚太宏观经济展望

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 其他的

- 拉丁美洲

- 拉丁美洲宏观经济展望

- 巴西

- 墨西哥

- 其他的

- 中东和非洲

- 中东和非洲宏观经济展望

- 海湾合作委员会国家

- 南非

- 其他的

第十章 竞争格局

- 介绍

- 主要参与企业的策略/优势

- 2020-2024年收入份额分析

- 2024年市占率分析

- 品牌/软体对比

- 估值和财务指标

- 公司估值矩阵:主要参与企业,2024 年

- 公司估值矩阵:Start-Ups/中小企业,2024 年

- 竞争场景

第十一章:公司简介

- 主要参与企业

- RISKONNECT, INC.

- ORIGAMI RISK LLC

- RLDATIX

- HEALTH CATALYST

- SYMPLR

- CLARITY GROUP, INC.

- PERFORMANCE HEALTH PARTNERS

- MORCARE

- RISKQUAL TECHNOLOGIES, INC.

- PRISTA CORPORATION

- SAFEQUAL

- IQVIA

- INOVALON

- NAVEX GLOBAL, INC.

- CENSINET

- AMERICAN DATA NETWORK

- ARVENTA

- COMPLIANCEQUEST

- RADAR HEALTHCARE INC

- PASCAL METRICS INC.

- 其他公司

- OMNIGO

- LOGICMANAGER, INC.

- DEXUR

- HEALTHCARE GRC PTE LTD.

- NOSOTECH INC.

第十二章附录

The global patient safety and risk software market is projected to reach USD 2.99 billion by 2030 from USD 1.75 billion in 2025, at a high CAGR of 11.36% during the forecast period. The patient safety and risk software market is emerging as a critical priority for healthcare systems worldwide, aimed at minimizing medical errors and improving the quality of care. Its growth is being driven by rising incidences of adverse events, increasing complexity of healthcare delivery, and the push toward value-based care models.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2024-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD billion) |

| Segments | Function, Deployment, and End User |

| Regions covered | North America, Europe, Asia Pacific, Latin America, and Middle East & Africa |

Regulatory frameworks from bodies such as the FDA, EMA, and The Joint Commission mandate strict reporting, monitoring, and compliance, compelling providers and life sciences companies to adopt advanced PSRM solutions. At the same time, government initiatives, such as the US Department of Health and Human Services' patient safety programs and the EU's pharmacovigilance regulations, are accelerating adoption. However, barriers such as high implementation costs, lack of global standardization, integration challenges with legacy systems, and underreporting of safety events continue to limit widespread adoption.

Compliance & governance under the function segment is expected to register the fastest growth during the forecast period.

The compliance & governance segment is the fastest-growing segment during the forecast period, driven by the rising emphasis on meeting regulatory requirements and maintaining transparency in healthcare operations. Increasing scrutiny from regulatory bodies, coupled with the need for standardized reporting and audit trails, is encouraging healthcare organizations to adopt advanced compliance management solutions. These tools help ensure adherence to quality standards, data protection regulations, and patient safety protocols, thereby supporting risk mitigation and operational efficiency across the healthcare ecosystem.

The cloud-based deployment segment is projected to register the fastest growth during the forecast period.

The cloud-based segment is the fastest-growing segment, driven by the rising adoption of digital health technologies and the shift toward flexible, scalable deployment models. Cloud solutions offer seamless data access, interoperability, and real-time collaboration across healthcare settings, enabling faster decision-making and improved patient safety outcomes. Additionally, lower upfront costs, reduced IT infrastructure requirements, and enhanced data security through advanced encryption and compliance measures are further accelerating the adoption of cloud-based platforms in this market.

Asia Pacific is expected to witness the highest growth rate during the forecast period.

The Asia Pacific region is positioned to register the highest CAGR in the patient safety and risk software market, driven by unprecedented healthcare digitization, government initiatives, and substantial technology investments. For example, the smart hospital program in China aims to upgrade over 1,000 public hospitals by 2025 with integrated IT solutions. The growing burden of medical errors, expansion of healthcare infrastructure, and the push for EHR/EMR integration across emerging economies such as India, China, and Southeast Asia are further fueling adoption. The expanding pharmaceutical and medical device sectors in the region, coupled with a rising patient population, are creating strong demand for efficient risk management and safety solutions.

In-depth interviews have been conducted with chief executive officers (CEOs), Directors, and other executives from various key organizations operating in the authentication and brand protection marketplace. The breakdown of primary participants is as mentioned below:

- By Company Type - Tier 1: 31%, Tier 2: 28%, and Tier 3: 41%

- By Designation - C Level: 31%, Director Level: 25%, and Others: 44%

- By Region - North America: 32%, Europe: 32%, Asia Pacific: 26%, Middle East & Africa: 5%, Latin America: 5%

Key Players

The key players operating in the patient safety and risk software market include Riskonnect, Inc. (US), Origami Risk LLC (US), RLDatix (US), Health Catalyst (US), symplr (US), Clarity Group, Inc. (US), Performance Health Partners (US), MorCare, LLC (US), RiskQual Technologies, Inc. (US), Prista Corporation (US), IQVIA Inc. (US), Inovalon (US), NAVEX Global, Inc. (US), Censinet (US), American Data Network (US), Arventa Pty Ltd (Australia), ComplianceQuest (US), Radar Healthcare Inc (UK), Pascal Metrics Inc. (US), and SafeQual Health (US)

Research Coverage

The report analyzes the patient safety and risk software market and estimate the market size and future growth potential of various market segments, based on function, deployment mode, end user, and region. The report also provides a competitive analysis of the key players operating in this market, along with their company profiles, product offerings, recent developments, and key market strategies.

Reasons to Buy the Report

This report will enrich established firms as well as new entrants/smaller firms to gauge the pulse of the market, which, in turn, would help them garner a higher share of the market. Firms purchasing the report could use one or a combination of the following strategies to strengthen their positions in the market.

This report provides insights into:

- Analysis of key drivers (rising patient safety incidents, increasing prioritization of patient safety, escalating healthcare costs and shift toward value-based care models, increasing adoption of digital health technologies), restraints (high implementation and maintenance costs, resistance to adoption and perceived complexity of patient safety and risk software, data privacy and interoperability challenges), opportunities (growing adoption of AI, predictive analytics, and automation, increasing adoption of patient safety and risk software into MedTech and pharma safety domains, integration of patient safety and risk software with population health and real-world evidence platforms), challenges (lack of global standardization in safety reporting, complex integration with legacy systems, limited awareness and underreporting of safety incidents)

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and solution launches in the patient safety and risk software market.

- Market Development: Comprehensive information on the lucrative emerging markets, function, deployment mode, end user, and region

- Market Diversification: Exhaustive information about the product portfolios, growing geographies, recent developments, and investments in the patient safety and risk software market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, product offerings, and capabilities of the leading players in the patient safety & risk software market such as Riskonnect, Inc. (US), Origami Risk LLC (US), RLDatix (US), symplr (US), and Radar Healthcare Inc (UK)

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 STAKEHOLDERS

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY DATA

- 2.1.1.1 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Key data from primary sources

- 2.1.2.2 Insights from primary experts

- 2.1.1 SECONDARY DATA

- 2.2 MARKET SIZE ESTIMATION

- 2.3 MARKET BREAKDOWN AND DATA TRIANGULATION

- 2.4 RESEARCH ASSUMPTIONS

- 2.4.1 MARKET SIZING ASSUMPTIONS

- 2.4.2 OVERALL STUDY ASSUMPTIONS

- 2.5 RESEARCH LIMITATIONS

- 2.5.1 METHODOLOGY-RELATED LIMITATIONS

- 2.5.2 SCOPE-RELATED LIMITATIONS

- 2.6 RISK ANALYSIS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 PATIENT SAFETY AND RISK SOFTWARE MARKET OVERVIEW

- 4.2 PATIENT SAFETY AND RISK SOFTWARE MARKET, BY END USER AND REGION

- 4.3 PATIENT SAFETY AND RISK SOFTWARE MARKET: GEOGRAPHIC SNAPSHOT

- 4.4 PATIENT SAFETY AND RISK SOFTWARE MARKET: DEVELOPED MARKETS VS. EMERGING MARKETS

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Rising patient safety incidents

- 5.2.1.2 Increasing prioritization of patient safety

- 5.2.1.3 Escalating healthcare costs and shift toward value-based care models

- 5.2.1.4 Increasing adoption of digital health technologies

- 5.2.2 RESTRAINTS

- 5.2.2.1 High implementation and maintenance costs

- 5.2.2.2 Resistance to adoption and perceived complexity of patient safety and risk software

- 5.2.2.3 Data privacy and interoperability challenges

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Growing adoption of AI, predictive analytics, and automation

- 5.2.3.2 Increasing adoption of patient safety and risk solutions into MedTech and pharma safety domains

- 5.2.3.3 Integration of patient safety and risk software with population health and real-world evidence platforms

- 5.2.4 CHALLENGES

- 5.2.4.1 Lack of global standardization in safety reporting

- 5.2.4.2 Complex integration with legacy systems

- 5.2.4.3 Limited awareness and underreporting of safety events

- 5.2.1 DRIVERS

- 5.3 INDUSTRY TRENDS

- 5.3.1 MOBILE HEALTH PLATFORMS

- 5.3.2 CLOUD-BASED ALARM MANAGEMENT SOLUTION

- 5.3.3 IOT-ENABLED SOLUTIONS

- 5.4 TRENDS/DISRUPTIONS IMPACTING CUSTOMERS' BUSINESS

- 5.5 PRICING ANALYSIS

- 5.5.1 INDICATIVE PRICING ANALYSIS, BY KEY PLAYER

- 5.5.2 INDICATIVE PRICING ANALYSIS, BY REGION

- 5.6 VALUE CHAIN ANALYSIS

- 5.7 ECOSYSTEM ANALYSIS

- 5.8 INVESTMENT AND FUNDING SCENARIO

- 5.9 TECHNOLOGY ANALYSIS

- 5.9.1 KEY TECHNOLOGIES

- 5.9.1.1 AI-powered risk scoring

- 5.9.1.2 Automated root cause analysis

- 5.9.1.3 Real-time safety dashboards

- 5.9.1.4 Mobile incident reporting apps

- 5.9.2 ADJACENT TECHNOLOGIES

- 5.9.2.1 Cloud SaaS platforms

- 5.9.2.2 Blockchain

- 5.9.3 COMPLEMENTARY TECHNOLOGIES

- 5.9.3.1 EHR/EMR integration

- 5.9.3.2 Claims and billing systems

- 5.9.3.3 Credentialing systems

- 5.9.1 KEY TECHNOLOGIES

- 5.10 PATENT ANALYSIS

- 5.10.1 PATENT PUBLICATION TREND

- 5.10.2 LIST OF PATENTS

- 5.11 KEY CONFERENCES AND EVENTS, 2025-2027

- 5.12 CASE STUDY ANALYSIS

- 5.12.1 ADOPTION OF VIRTUAL OBSERVATION SOLUTION TO REDUCE FALL RATES IN PATIENTS

- 5.12.2 UTILIZATION OF ENTERPRISE RISK MANAGEMENT SYSTEM FOR ENHANCED PATIENT SAFETY

- 5.12.3 USE OF COMPREHENSIVE HEALTHCARE RISK MANAGEMENT SOFTWARE FOR IMPROVED REGULATORY COMPLIANCE

- 5.13 REGULATORY LANDSCAPE

- 5.13.1 REGULATORY ANALYSIS

- 5.13.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.14 PORTER'S FIVE FORCES ANALYSIS

- 5.14.1 BARGAINING POWER OF SUPPLIERS

- 5.14.2 BARGAINING POWER OF BUYERS

- 5.14.3 THREAT OF NEW ENTRANTS

- 5.14.4 THREAT OF SUBSTITUTES

- 5.14.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.15 KEY STAKEHOLDERS AND BUYING CRITERIA

- 5.15.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 5.15.2 BUYING CRITERIA

- 5.16 END-USER ANALYSIS

- 5.16.1 UNMET NEEDS

- 5.16.2 END-USER EXPECTATIONS

- 5.17 BUSINESS MODEL

- 5.17.1 SUBSCRIPTION LICENSING

- 5.17.2 MODULAR PLATFORM APPROACH

- 5.17.3 IMPLEMENTATION AND INTEGRATION FEES

- 5.17.4 VALUE-ADDED SERVICES

- 5.17.5 MARKETPLACE INTEGRATION AND REGIONAL PRICING

- 5.18 IMPACT OF AI/GEN AI ON PATIENT SAFETY AND RISK SOFTWARE MARKET

- 5.18.1 INTRODUCTION

- 5.18.2 TOP USE CASES AND MARKET POTENTIAL

- 5.18.3 KEY USE CASES

- 5.18.4 CASE STUDY ON AI/GENERATIVE AI IMPLEMENTATION

- 5.18.4.1 Use of AI-powered data extraction platform with risk management software

- 5.18.5 INTERCONNECTED AND ADJACENT ECOSYSTEMS

- 5.18.5.1 Pharmacovigilance and drug safety monitoring

- 5.18.5.2 Healthcare information exchange

- 5.18.5.3 Quality improvement software

- 5.18.5.4 Healthcare GRC

- 5.18.6 USER READINESS AND IMPACT ASSESSMENT

- 5.18.6.1 Healthcare providers

- 5.18.6.2 Pharmaceutical & biotechnology companies

- 5.19 IMPACT OF 2025 US TARIFF

- 5.19.1 INTRODUCTION

- 5.19.2 KEY TARIFF RATES

- 5.19.3 PRICE IMPACT ANALYSIS

- 5.19.4 IMPACT ON COUNTRY/REGION

- 5.19.4.1 US

- 5.19.4.2 Europe

- 5.19.4.3 Asia Pacific

- 5.19.5 IMPACT ON END-USE INDUSTRIES

6 PATIENT SAFETY AND RISK SOFTWARE MARKET, BY FUNCTION

- 6.1 INTRODUCTION

- 6.2 RISK & SAFETY MANAGEMENT

- 6.2.1 INCIDENT REPORTING SYSTEMS

- 6.2.1.1 Need for real-time reporting and automated workflows to support growth

- 6.2.2 EVENT MANAGEMENT & ROOT CAUSE ANALYSIS SOFTWARE

- 6.2.2.1 Ability to analyze incident patterns and implement risk mitigation to promote growth

- 6.2.3 PATIENT LEARNING SYSTEMS

- 6.2.3.1 Increasing focus on improving patient safety to foster growth

- 6.2.1 INCIDENT REPORTING SYSTEMS

- 6.3 COMPLIANCE & GOVERNANCE

- 6.3.1 RISK/COMPLIANCE MONITORING AND ANALYTICS SOFTWARE

- 6.3.1.1 Evolving need for continuous surveillance of organizational activities to aid growth

- 6.3.2 GOVERNANCE, RISK, AND COMPLIANCE PLATFORMS

- 6.3.2.1 Growing shift from reactive compliance management to proactive risk prevention to boost market

- 6.3.1 RISK/COMPLIANCE MONITORING AND ANALYTICS SOFTWARE

- 6.4 CLINICAL SAFETY CONTROLS

- 6.4.1 MEDICATION SAFETY & PHARMACY-LEVEL CONTROL SOFTWARE

- 6.4.1.1 Need to prevent medication errors to contribute to growth

- 6.4.2 INFECTION CONTROL SYSTEMS

- 6.4.2.1 Rise in proactive surveillance, rapid intervention, and continuous monitoring to expedite growth

- 6.4.1 MEDICATION SAFETY & PHARMACY-LEVEL CONTROL SOFTWARE

- 6.5 FINANCIAL & LEGAL RISK HANDLING

- 6.5.1 CLAIMS MANAGEMENT SOLUTIONS

- 6.5.1.1 Need to leverage data-driven claims management to minimize costs to favor growth

- 6.5.2 REVENUE INTEGRITY & RISK MANAGEMENT SOLUTIONS

- 6.5.2.1 Growing focus on minimizing financial and legal risks to propel market

- 6.5.1 CLAIMS MANAGEMENT SOLUTIONS

7 PATIENT SAFETY AND RISK SOFTWARE MARKET, BY DEPLOYMENT MODE

- 7.1 INTRODUCTION

- 7.2 ON-PREMISE DEPLOYMENT

- 7.2.1 HIGHER CONTROL, SECURITY, AND CUSTOMIZATION TO BOLSTER GROWTH

- 7.3 CLOUD-BASED DEPLOYMENT

- 7.3.1 NEED TO REDUCE IT OVERHEAD AND ENABLE FASTER INNOVATION TO SPUR GROWTH

- 7.4 HYBRID DEPLOYMENT

- 7.4.1 ABILITY TO SUPPORT REAL-TIME INCIDENT REPORTING, ROOT CAUSE ANALYSIS, AND COMPLIANCE MONITORING TO DRIVE MARKET

8 PATIENT SAFETY AND RISK SOFTWARE MARKET, BY END USER

- 8.1 INTRODUCTION

- 8.2 HEALTHCARE PROVIDERS

- 8.2.1 HOSPITALS

- 8.2.1.1 Rising demand for high-quality care and patient safety to accelerate growth

- 8.2.2 CLINICS

- 8.2.2.1 Increasing demand for quality care in outpatient and ambulatory settings to facilitate growth

- 8.2.3 AMBULATORY CARE CENTERS

- 8.2.3.1 Growing shift toward outpatient and value-based care models to drive market

- 8.2.4 LONG-TERM CARE CENTERS

- 8.2.4.1 Increasing focus on elderly care and patients with chronic conditions to aid growth

- 8.2.5 PHARMACIES

- 8.2.5.1 Enhanced medical safety and regulatory compliance to augment growth

- 8.2.6 OTHER HEALTHCARE PROVIDERS

- 8.2.1 HOSPITALS

- 8.3 PHARMACEUTICAL & BIOTECH COMPANIES

- 8.3.1 NEED TO MAINTAIN PRODUCT QUALITY, REGULATORY COMPLIANCE, AND PHARMACOVIGILANCE TO ENCOURAGE GROWTH

- 8.4 HEALTHCARE PAYERS

- 8.4.1 INCREASING ADOPTION OF PATIENT SAFETY AND RISK SOFTWARE FOR ENHANCED QUALITY ACROSS HEALTHCARE ECOSYSTEM TO AID GROWTH

- 8.5 MEDTECH COMPANIES

- 8.5.1 GROWING RISK OF DATA INTEGRITY AND CYBERSECURITY TO FUEL MARKET

- 8.6 OTHER END USERS

9 PATIENT SAFETY AND RISK SOFTWARE MARKET, BY REGION

- 9.1 INTRODUCTION

- 9.2 NORTH AMERICA

- 9.2.1 MACROECONOMIC OUTLOOK FOR NORTH AMERICA

- 9.2.2 US

- 9.2.2.1 Increasing initiatives for improving patient and healthcare workforce safety to aid growth

- 9.2.3 CANADA

- 9.2.3.1 Rise in patient safety improvement programs to contribute to growth

- 9.3 EUROPE

- 9.3.1 MACROECONOMIC OUTLOOK FOR EUROPE

- 9.3.2 GERMANY

- 9.3.2.1 Targeted government policies and push toward modernizing healthcare delivery to propel market

- 9.3.3 UK

- 9.3.3.1 Growing initiatives on improving patient outcomes and reducing medical errors to drive market

- 9.3.4 FRANCE

- 9.3.4.1 Increasing use of integrated digital platforms in hospitals to expedite growth

- 9.3.5 ITALY

- 9.3.5.1 Favorable national legislation and regional healthcare policies to promote growth

- 9.3.6 SPAIN

- 9.3.6.1 Rising commitment toward enhanced healthcare quality and culture of safety to aid growth

- 9.3.7 REST OF EUROPE

- 9.4 ASIA PACIFIC

- 9.4.1 MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

- 9.4.2 CHINA

- 9.4.2.1 Increasing deployment of critical incident reporting systems and EHR-linked safety modules to fuel market

- 9.4.3 JAPAN

- 9.4.3.1 Growing focus on supporting error reporting, root cause analysis, and clinical protocols to boost market

- 9.4.4 INDIA

- 9.4.4.1 Strong public-private sector initiatives to support growth

- 9.4.5 AUSTRALIA

- 9.4.5.1 Increasing emphasis on quality improvement across public and private hospitals to spur growth

- 9.4.6 SOUTH KOREA

- 9.4.6.1 Innovation-driven healthcare ecosystem to facilitate growth

- 9.4.7 REST OF ASIA PACIFIC

- 9.5 LATIN AMERICA

- 9.5.1 MACROECONOMIC OUTLOOK FOR LATIN AMERICA

- 9.5.2 BRAZIL

- 9.5.2.1 Increasing focus on reducing adverse events and hospital-acquired infections to encourage growth

- 9.5.3 MEXICO

- 9.5.3.1 Expanding healthcare digitization and national policies promoting patient safety to drive market

- 9.5.4 REST OF LATIN AMERICA

- 9.6 MIDDLE EAST & AFRICA

- 9.6.1 MACROECONOMIC OUTLOOK FOR MIDDLE EAST & AFRICA

- 9.6.2 GCC COUNTRIES

- 9.6.2.1 Saudi Arabia

- 9.6.2.1.1 Increasing modernization efforts in healthcare to accelerate growth

- 9.6.2.2 UAE

- 9.6.2.2.1 Evolving digital health landscape to favor growth

- 9.6.2.3 Rest of GCC countries

- 9.6.2.1 Saudi Arabia

- 9.6.3 SOUTH AFRICA

- 9.6.3.1 Increasing awareness about patient safety in public and private healthcare sectors to boost market

- 9.6.4 REST OF MIDDLE EAST & AFRICA

10 COMPETITIVE LANDSCAPE

- 10.1 INTRODUCTION

- 10.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 10.2.1 OVERVIEW OF STRATEGIES ADOPTED BY KEY PLAYERS IN PATIENT SAFETY AND RISK SOFTWARE MARKET

- 10.3 REVENUE SHARE ANALYSIS, 2020-2024

- 10.4 MARKET SHARE ANALYSIS, 2024

- 10.5 BRAND/SOFTWARE COMPARISON

- 10.6 COMPANY VALUATION AND FINANCIAL METRICS

- 10.6.1 COMPANY VALUATION

- 10.6.2 FINANCIAL METRICS

- 10.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 10.7.1 STARS

- 10.7.2 EMERGING LEADERS

- 10.7.3 PERVASIVE PLAYERS

- 10.7.4 PARTICIPANTS

- 10.7.5 COMPANY FOOTPRINT, 2024

- 10.7.5.1 Company footprint

- 10.7.5.2 Region footprint

- 10.7.5.3 Deployment mode footprint

- 10.7.5.4 Function footprint

- 10.7.5.5 End-user footprint

- 10.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 10.8.1 PROGRESSIVE COMPANIES

- 10.8.2 RESPONSIVE COMPANIES

- 10.8.3 DYNAMIC COMPANIES

- 10.8.4 STARTING BLOCKS

- 10.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 10.8.5.1 Detailed list of key startups/SMEs

- 10.8.5.2 Competitive benchmarking of key startups/SMEs

- 10.9 COMPETITIVE SCENARIO

- 10.9.1 SOLUTION LAUNCHES AND ENHANCEMENTS

- 10.9.2 DEALS

- 10.9.3 EXPANSIONS

11 COMPANY PROFILES

- 11.1 KEY PLAYERS

- 11.1.1 RISKONNECT, INC.

- 11.1.1.1 Business overview

- 11.1.1.2 Solutions offered

- 11.1.1.3 Recent developments

- 11.1.1.3.1 Solution launches and enhancements

- 11.1.1.3.2 Deals

- 11.1.1.4 MnM view

- 11.1.1.4.1 Right to win

- 11.1.1.4.2 Strategic choices

- 11.1.1.4.3 Weaknesses and competitive threats

- 11.1.2 ORIGAMI RISK LLC

- 11.1.2.1 Business overview

- 11.1.2.2 Solutions offered

- 11.1.2.3 Recent developments

- 11.1.2.3.1 Solution launches and enhancements

- 11.1.2.4 MnM view

- 11.1.2.4.1 Right to win

- 11.1.2.4.2 Strategic choices

- 11.1.2.4.3 Weaknesses and competitive threats

- 11.1.3 RLDATIX

- 11.1.3.1 Business overview

- 11.1.3.2 Solutions offered

- 11.1.3.3 Recent developments

- 11.1.3.3.1 Solution launches and enhancements

- 11.1.3.3.2 Deals

- 11.1.3.3.3 Expansions

- 11.1.3.4 MnM view

- 11.1.3.4.1 Right to win

- 11.1.3.4.2 Strategic choices

- 11.1.3.4.3 Weaknesses and competitive threats

- 11.1.4 HEALTH CATALYST

- 11.1.4.1 Business overview

- 11.1.4.2 Solutions offered

- 11.1.4.3 Recent developments

- 11.1.4.3.1 Solution launches and enhancements

- 11.1.4.3.2 Deals

- 11.1.5 SYMPLR

- 11.1.5.1 Business overview

- 11.1.5.2 Solutions offered

- 11.1.5.3 Recent developments

- 11.1.5.3.1 Solution launches and enhancements

- 11.1.5.3.2 Deals

- 11.1.5.4 MnM view

- 11.1.5.4.1 Right to win

- 11.1.5.4.2 Strategic choices

- 11.1.5.4.3 Weaknesses and competitive threats

- 11.1.6 CLARITY GROUP, INC.

- 11.1.6.1 Business overview

- 11.1.6.2 Solutions offered

- 11.1.7 PERFORMANCE HEALTH PARTNERS

- 11.1.7.1 Business overview

- 11.1.7.2 Solutions offered

- 11.1.7.3 Recent developments

- 11.1.7.3.1 Deals

- 11.1.8 MORCARE

- 11.1.8.1 Business overview

- 11.1.8.2 Solutions offered

- 11.1.9 RISKQUAL TECHNOLOGIES, INC.

- 11.1.9.1 Business overview

- 11.1.9.2 Solutions offered

- 11.1.10 PRISTA CORPORATION

- 11.1.10.1 Business overview

- 11.1.10.2 Solutions offered

- 11.1.11 SAFEQUAL

- 11.1.11.1 Business overview

- 11.1.11.2 Solutions offered

- 11.1.12 IQVIA

- 11.1.12.1 Business overview

- 11.1.12.2 Solutions offered

- 11.1.12.3 Recent developments

- 11.1.12.3.1 Solution launches and enhancements

- 11.1.12.3.2 Deals

- 11.1.13 INOVALON

- 11.1.13.1 Business overview

- 11.1.13.2 Solutions offered

- 11.1.13.3 Recent developments

- 11.1.13.3.1 Solution launches and enhancements

- 11.1.14 NAVEX GLOBAL, INC.

- 11.1.14.1 Business overview

- 11.1.14.2 Solutions offered

- 11.1.14.3 Recent developments

- 11.1.14.3.1 Solution launches and enhancements

- 11.1.14.3.2 Deals

- 11.1.14.3.3 Expansions

- 11.1.15 CENSINET

- 11.1.15.1 Business overview

- 11.1.15.2 Solutions offered

- 11.1.15.3 Recent developments

- 11.1.15.3.1 Solution launches and enhancements

- 11.1.16 AMERICAN DATA NETWORK

- 11.1.16.1 Business overview

- 11.1.16.2 Solutions offered

- 11.1.17 ARVENTA

- 11.1.17.1 Business overview

- 11.1.17.2 Solutions offered

- 11.1.18 COMPLIANCEQUEST

- 11.1.18.1 Business overview

- 11.1.18.2 Solutions offered

- 11.1.18.3 Recent developments

- 11.1.18.3.1 Solution launches and enhancements

- 11.1.18.3.2 Deals

- 11.1.19 RADAR HEALTHCARE INC

- 11.1.19.1 Business overview

- 11.1.19.2 Solutions offered

- 11.1.20 PASCAL METRICS INC.

- 11.1.20.1 Business overview

- 11.1.20.2 Solutions offered

- 11.1.1 RISKONNECT, INC.

- 11.2 OTHER PLAYERS

- 11.2.1 OMNIGO

- 11.2.2 LOGICMANAGER, INC.

- 11.2.3 DEXUR

- 11.2.4 HEALTHCARE GRC PTE LTD.

- 11.2.5 NOSOTECH INC.

12 APPENDIX

- 12.1 DISCUSSION GUIDE

- 12.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 12.3 CUSTOMIZATION OPTIONS

- 12.4 RELATED REPORTS

- 12.5 AUTHOR DETAILS

List of Tables

- TABLE 1 FACTOR ANALYSIS

- TABLE 2 PATIENT SAFETY AND RISK SOFTWARE MARKET: RISK ANALYSIS

- TABLE 3 PATIENT SAFETY AND RISK SOFTWARE MARKET: IMPACT ANALYSIS OF MARKET DYNAMICS

- TABLE 4 NORTH AMERICA: HEALTHCARE DATA BREACHES, 2021-2025

- TABLE 5 INDICATIVE PRICING ANALYSIS OF PATIENT SAFETY AND RISK SOFTWARE, BY KEY PLAYER, 2024 (USD)

- TABLE 6 PATIENT SAFETY AND RISK SOFTWARE MARKET: ROLE OF COMPANIES IN ECOSYSTEM

- TABLE 7 PATIENT SAFETY AND RISK SOFTWARE MARKET: JURISDICTION ANALYSIS OF TOP APPLICANT COUNTRIES, JANUARY 2022-SEPTEMBER 2025

- TABLE 8 PATIENT SAFETY AND RISK SOFTWARE MARKET: LIST OF PATENTS, JANUARY 2022-SEPTEMBER 2025

- TABLE 9 PATIENT SAFETY AND RISK SOFTWARE MARKET: KEY CONFERENCES AND EVENTS, 2025-2027

- TABLE 10 REGULATORY SCENARIO IN NORTH AMERICA

- TABLE 11 REGULATORY SCENARIO IN EUROPE

- TABLE 12 REGULATORY SCENARIO IN ASIA PACIFIC

- TABLE 13 REGULATORY SCENARIO IN MIDDLE EAST & AFRICA

- TABLE 14 REGULATORY SCENARIO IN LATIN AMERICA

- TABLE 15 NORTH AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 16 EUROPE: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 17 ASIA PACIFIC: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 18 LATIN AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 19 MIDDLE EAST & AFRICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 20 PATIENT SAFETY AND RISK SOFTWARE MARKET: PORTER'S FIVE FORCES ANALYSIS

- TABLE 21 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP THREE END USERS

- TABLE 22 KEY BUYING CRITERIA FOR TOP THREE END USERS

- TABLE 23 PATIENT SAFETY AND RISK SOFTWARE MARKET: UNMET NEEDS

- TABLE 24 PATIENT SAFETY AND RISK SOFTWARE MARKET: END-USER EXPECTATIONS

- TABLE 25 US ADJUSTED RECIPROCAL TARIFF RATES

- TABLE 26 PATIENT SAFETY AND RISK SOFTWARE MARKET, BY FUNCTION, 2023-2030 (USD MILLION)

- TABLE 27 PATIENT SAFETY AND RISK SOFTWARE MARKET FOR RISK & SAFETY MANAGEMENT, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 28 PATIENT SAFETY AND RISK SOFTWARE MARKET FOR RISK & SAFETY MANAGEMENT, BY REGION, 2023-2030 (USD MILLION)

- TABLE 29 PATIENT SAFETY AND RISK SOFTWARE MARKET FOR INCIDENT REPORTING SYSTEMS, BY REGION, 2023-2030 (USD MILLION)

- TABLE 30 PATIENT SAFETY AND RISK SOFTWARE MARKET FOR EVENT MANAGEMENT & ROOT CAUSE ANALYSIS SOFTWARE, BY REGION, 2023-2030 (USD MILLION)

- TABLE 31 PATIENT SAFETY AND RISK SOFTWARE MARKET FOR PATIENT LEARNING SYSTEMS, BY REGION, 2023-2030 (USD MILLION)

- TABLE 32 PATIENT SAFETY AND RISK SOFTWARE MARKET FOR COMPLIANCE & GOVERNANCE, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 33 PATIENT SAFETY AND RISK SOFTWARE MARKET FOR COMPLIANCE & GOVERNANCE, BY REGION, 2023-2030 (USD MILLION)

- TABLE 34 PATIENT SAFETY AND RISK SOFTWARE MARKET FOR RISK/COMPLIANCE MONITORING & ANALYTICS SOFTWARE, BY REGION, 2023-2030 (USD MILLION)

- TABLE 35 PATIENT SAFETY AND RISK SOFTWARE MARKET FOR GOVERNANCE, RISK, AND COMPLIANCE PLATFORMS, BY REGION, 2023-2030 (USD MILLION)

- TABLE 36 PATIENT SAFETY AND RISK SOFTWARE MARKET FOR CLINICAL SAFETY CONTROLS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 37 PATIENT SAFETY AND RISK SOFTWARE MARKET FOR CLINICAL SAFETY CONTROLS, BY REGION, 2023-2030 (USD MILLION)

- TABLE 38 PATIENT SAFETY AND RISK SOFTWARE MARKET FOR MEDICATION SAFETY & PHARMACY-LEVEL CONTROL SOFTWARE, BY REGION, 2023-2030 (USD MILLION)

- TABLE 39 PATIENT SAFETY AND RISK SOFTWARE MARKET FOR INFECTION CONTROL SYSTEMS, BY REGION, 2023-2030 (USD MILLION)

- TABLE 40 PATIENT SAFETY AND RISK SOFTWARE MARKET FOR FINANCIAL & LEGAL RISK HANDLING, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 41 PATIENT SAFETY AND RISK SOFTWARE MARKET FOR FINANCIAL & LEGAL RISK HANDLING, BY REGION, 2023-2030 (USD MILLION)

- TABLE 42 PATIENT SAFETY AND RISK SOFTWARE MARKET FOR CLAIMS MANAGEMENT SOLUTIONS, BY REGION, 2023-2030 (USD MILLION)

- TABLE 43 PATIENT SAFETY AND RISK SOFTWARE MARKET FOR REVENUE INTEGRITY & RISK MANAGEMENT SOLUTIONS, BY REGION, 2023-2030 (USD MILLION)

- TABLE 44 PATIENT SAFETY AND RISK SOFTWARE MARKET, BY DEPLOYMENT MODE, 2023-2030 (USD MILLION)

- TABLE 45 PATIENT SAFETY AND RISK SOFTWARE MARKET FOR ON-PREMISE DEPLOYMENT, BY REGION, 2023-2030 (USD MILLION)

- TABLE 46 PATIENT SAFETY & RISK SOFTWARE MARKET FOR CLOUD-BASED DEPLOYMENT, BY REGION, 2023-2030 (USD MILLION)

- TABLE 47 PATIENT SAFETY AND RISK SOFTWARE MARKET FOR HYBRID DEPLOYMENT, BY REGION, 2023-2030 (USD MILLION)

- TABLE 48 PATIENT SAFETY AND RISK SOFTWARE MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 49 PATIENT SAFETY AND RISK SOFTWARE MARKET FOR HEALTHCARE PROVIDERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 50 PATIENT SAFETY AND RISK SOFTWARE MARKET FOR HEALTHCARE PROVIDERS, BY REGION, 2023-2030 (USD MILLION)

- TABLE 51 PATIENT SAFETY AND RISK SOFTWARE MARKET FOR HOSPITALS, BY REGION, 2023-2030 (USD MILLION)

- TABLE 52 PATIENT SAFETY AND RISK SOFTWARE MARKET FOR CLINICS, BY REGION, 2023-2030 (USD MILLION)

- TABLE 53 PATIENT SAFETY AND RISK SOFTWARE MARKET FOR AMBULATORY CARE CENTERS, BY REGION, 2023-2030 (USD MILLION)

- TABLE 54 PATIENT SAFETY AND RISK SOFTWARE MARKET FOR LONG-TERM CARE CENTERS, BY REGION, 2023-2030 (USD MILLION)

- TABLE 55 PATIENT SAFETY AND RISK SOFTWARE MARKET FOR PHARMACIES, BY REGION, 2023-2030 (USD MILLION)

- TABLE 56 PATIENT SAFETY AND RISK SOFTWARE MARKET FOR OTHER HEALTHCARE PROVIDERS, BY REGION, 2023-2030 (USD MILLION)

- TABLE 57 PATIENT SAFETY AND RISK SOFTWARE MARKET FOR PHARMACEUTICAL & BIOTECH COMPANIES, BY REGION, 2023-2030 (USD MILLION)

- TABLE 58 PATIENT SAFETY AND RISK SOFTWARE MARKET FOR HEALTHCARE PAYERS, BY REGION, 2023-2030 (USD MILLION)

- TABLE 59 PATIENT SAFETY AND RISK SOFTWARE MARKET FOR MEDTECH COMPANIES, BY REGION, 2023-2030 (USD MILLION)

- TABLE 60 PATIENT SAFETY AND RISK SOFTWARE MARKET FOR OTHER END USERS, BY REGION, 2023-2030 (USD MILLION)

- TABLE 61 PATIENT SAFETY AND RISK SOFTWARE MARKET, BY REGION, 2023-2030 (USD MILLION)

- TABLE 62 NORTH AMERICA: PATIENT SAFETY AND RISK SOFTWARE MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 63 NORTH AMERICA: PATIENT SAFETY AND RISK SOFTWARE MARKET, BY FUNCTION, 2023-2030 (USD MILLION)

- TABLE 64 NORTH AMERICA: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR RISK & SAFETY MANAGEMENT, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 65 NORTH AMERICA: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR COMPLIANCE & GOVERNANCE, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 66 NORTH AMERICA: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR CLINICAL SAFETY CONTROLS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 67 NORTH AMERICA: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR FINANCIAL & LEGAL RISK HANDLING, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 68 NORTH AMERICA: PATIENT SAFETY AND RISK SOFTWARE MARKET, BY DEPLOYMENT MODE, 2023-2030 (USD MILLION)

- TABLE 69 NORTH AMERICA: PATIENT SAFETY AND RISK SOFTWARE MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 70 NORTH AMERICA: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR HEALTHCARE PROVIDERS, BY TYPE, 2023-2030(USD MILLION)

- TABLE 71 KEY ACTIVITIES IN US PATIENT SAFETY AND RISK MANAGEMENT SOFTWARE MARKET

- TABLE 72 US: PATIENT SAFETY AND RISK SOFTWARE MARKET, BY FUNCTION, 2023-2030 (USD MILLION)

- TABLE 73 US: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR RISK & SAFETY MANAGEMENT, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 74 US: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR COMPLIANCE & GOVERNANCE, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 75 US: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR CLINICAL SAFETY CONTROLS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 76 US: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR FINANCIAL & LEGAL RISK HANDLING, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 77 US: PATIENT SAFETY AND RISK SOFTWARE MARKET, BY DEPLOYMENT MODE, 2023-2030 (USD MILLION)

- TABLE 78 US: PATIENT SAFETY AND RISK MANAGEMENT SOFTWARE MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 79 US: PATIENT SAFETY AND RISK MANAGEMENT SOFTWARE MARKET FOR HEALTHCARE PROVIDERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 80 CANADA: PATIENT SAFETY AND RISK MANAGEMENT SOFTWARE MARKET, BY FUNCTION, 2023-2030(USD MILLION)

- TABLE 81 CANADA: PATIENT SAFETY AND RISK MANAGEMENT SOFTWARE MARKET FOR RISK & SAFETY MANAGEMENT, BY TYPE, 2023-2030(USD MILLION)

- TABLE 82 CANADA: PATIENT SAFETY AND RISK MANAGEMENT SOFTWARE MARKET FOR COMPLIANCE & GOVERNANCE, BY TYPE, 2023-2030(USD MILLION)

- TABLE 83 CANADA: PATIENT SAFETY AND RISK MANAGEMENT SOFTWARE MARKET FOR CLINICAL SAFETY CONTROLS, BY TYPE, 2023-2030(USD MILLION)

- TABLE 84 CANADA: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR FINANCIAL & LEGAL RISK HANDLING, BY TYPE, 2023-2030(USD MILLION)

- TABLE 85 CANADA: PATIENT SAFETY AND RISK SOFTWARE MARKET, BY DEPLOYMENT MODE, 2023-2030 (USD MILLION)

- TABLE 86 CANADA: PATIENT SAFETY AND RISK SOFTWARE MARKET, BY END USER, 2023-2030(USD MILLION)

- TABLE 87 CANADA: PATIENT SAFETY AND RISK MANAGEMENT SOFTWARE MARKET FOR HEALTHCARE PROVIDERS, BY TYPE, 2023-2030(USD MILLION)

- TABLE 88 EUROPE: PATIENT SAFETY AND RISK SOFTWARE MARKET, BY COUNTRY, 2023-2030(USD MILLION)

- TABLE 89 EUROPE: PATIENT SAFETY AND RISK SOFTWARE MARKET, BY FUNCTION, 2023-2030(USD MILLION)

- TABLE 90 EUROPE: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR RISK & SAFETY MANAGEMENT, BY TYPE, 2023-2030(USD MILLION)

- TABLE 91 EUROPE: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR COMPLIANCE & GOVERNANCE, BY TYPE, 2023-2030(USD MILLION)

- TABLE 92 EUROPE: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR CLINICAL SAFETY CONTROLS, BY TYPE, 2023-2030(USD MILLION)

- TABLE 93 EUROPE: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR FINANCIAL & LEGAL RISK HANDLING, BY TYPE, 2023-2030(USD MILLION)

- TABLE 94 EUROPE: PATIENT SAFETY AND RISK SOFTWARE MARKET, BY DEPLOYMENT MODE, 2023-2030 (USD MILLION)

- TABLE 95 EUROPE: PATIENT SAFETY AND RISK SOFTWARE MARKET, BY END USER, 2023-2030(USD MILLION)

- TABLE 96 EUROPE: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR HEALTHCARE PROVIDERS, BY TYPE, 2023-2030(USD MILLION)

- TABLE 97 GERMANY: PATIENT SAFETY AND RISK SOFTWARE MARKET, BY FUNCTION, 2023-2030(USD MILLION)

- TABLE 98 GERMANY: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR RISK & SAFETY MANAGEMENT, BY TYPE, 2023-2030(USD MILLION)

- TABLE 99 GERMANY: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR COMPLIANCE & GOVERNANCE, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 100 GERMANY: PATIENT SAFETY AND RISK MANAGEMENT SOFTWARE MARKET FOR CLINICAL SAFETY CONTROLS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 101 GERMANY: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR FINANCIAL & LEGAL RISK HANDLING, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 102 GERMANY: PATIENT SAFETY AND RISK SOFTWARE MARKET, BY DEPLOYMENT MODE, 2023-2030 (USD MILLION)

- TABLE 103 GERMANY: PATIENT SAFETY AND RISK SOFTWARE MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 104 GERMANY: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR HEALTHCARE PROVIDERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 105 UK: PATIENT SAFETY AND RISK SOFTWARE MARKET, BY FUNCTION, 2023-2030 (USD MILLION)

- TABLE 106 UK: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR RISK & SAFETY MANAGEMENT, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 107 UK: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR COMPLIANCE & GOVERNANCE, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 108 UK: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR CLINICAL SAFETY CONTROLS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 109 UK: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR FINANCIAL & LEGAL RISK HANDLING, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 110 UK: PATIENT SAFETY AND RISK SOFTWARE MARKET, BY DEPLOYMENT MODE, 2023-2030 (USD MILLION)

- TABLE 111 UK: PATIENT SAFETY AND RISK SOFTWARE MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 112 UK: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR HEALTHCARE PROVIDERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 113 FRANCE: PATIENT SAFETY AND RISK SOFTWARE MARKET, BY FUNCTION, 2023-2030 (USD MILLION)

- TABLE 114 FRANCE: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR RISK & SAFETY MANAGEMENT, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 115 FRANCE: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR COMPLIANCE & GOVERNANCE, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 116 FRANCE: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR CLINICAL SAFETY CONTROLS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 117 FRANCE: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR FINANCIAL & LEGAL RISK HANDLING, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 118 FRANCE: PATIENT SAFETY AND RISK SOFTWARE MARKET, BY DEPLOYMENT MODE, 2023-2030 (USD MILLION)

- TABLE 119 FRANCE: PATIENT SAFETY AND RISK SOFTWARE MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 120 FRANCE: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR HEALTHCARE PROVIDERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 121 ITALY: PATIENT SAFETY AND RISK SOFTWARE MARKET, BY FUNCTION, 2023-2030 (USD MILLION)

- TABLE 122 ITALY: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR RISK & SAFETY MANAGEMENT, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 123 ITALY: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR COMPLIANCE & GOVERNANCE, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 124 ITALY: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR CLINICAL SAFETY CONTROLS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 125 ITALY: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR FINANCIAL & LEGAL RISK HANDLING, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 126 ITALY: PATIENT SAFETY AND RISK SOFTWARE MARKET, BY DEPLOYMENT MODE, 2023-2030 (USD MILLION)

- TABLE 127 ITALY: PATIENT SAFETY AND RISK SOFTWARE MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 128 ITALY: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR HEALTHCARE PROVIDERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 129 SPAIN: PATIENT SAFETY AND RISK SOFTWARE MARKET, BY FUNCTION, 2023-2030 (USD MILLION)

- TABLE 130 SPAIN: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR RISK & SAFETY MANAGEMENT, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 131 SPAIN: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR COMPLIANCE & GOVERNANCE, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 132 SPAIN: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR CLINICAL SAFETY CONTROLS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 133 SPAIN: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR FINANCIAL & LEGAL RISK HANDLING, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 134 SPAIN: PATIENT SAFETY AND RISK SOFTWARE MARKET, BY DEPLOYMENT MODE, 2023-2030 (USD MILLION)

- TABLE 135 SPAIN: PATIENT SAFETY AND RISK SOFTWARE MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 136 SPAIN: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR HEALTHCARE PROVIDERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 137 REST OF EUROPE: PATIENT SAFETY AND RISK SOFTWARE MARKET, BY FUNCTION, 2023-2030 (USD MILLION)

- TABLE 138 REST OF EUROPE: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR RISK & SAFETY MANAGEMENT, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 139 REST OF EUROPE: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR COMPLIANCE & GOVERNANCE, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 140 REST OF EUROPE: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR CLINICAL SAFETY CONTROLS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 141 REST OF EUROPE: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR FINANCIAL & LEGAL RISK HANDLING, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 142 REST OF EUROPE: PATIENT SAFETY AND RISK SOFTWARE MARKET, BY DEPLOYMENT MODE, 2023-2030 (USD MILLION)

- TABLE 143 REST OF EUROPE: PATIENT SAFETY AND RISK SOFTWARE MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 144 REST OF EUROPE: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR HEALTHCARE PROVIDERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 145 ASIA PACIFIC: PATIENT SAFETY AND RISK SOFTWARE MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 146 ASIA PACIFIC: PATIENT SAFETY AND RISK SOFTWARE MARKET, BY FUNCTION, 2023-2030 (USD MILLION)

- TABLE 147 ASIA PACIFIC: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR RISK & SAFETY MANAGEMENT, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 148 ASIA PACIFIC: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR COMPLIANCE & GOVERNANCE, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 149 ASIA PACIFIC: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR CLINICAL SAFETY CONTROLS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 150 ASIA PACIFIC: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR FINANCIAL & LEGAL RISK HANDLING, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 151 ASIA PACIFIC: PATIENT SAFETY AND RISK SOFTWARE MARKET, BY DEPLOYMENT MODE, 2023-2030 (USD MILLION)

- TABLE 152 ASIA PACIFIC: PATIENT SAFETY AND RISK SOFTWARE MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 153 ASIA PACIFIC: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR HEALTHCARE PROVIDERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 154 CHINA: PATIENT SAFETY AND RISK SOFTWARE MARKET, BY FUNCTION, 2023-2030 (USD MILLION)

- TABLE 155 CHINA: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR RISK & SAFETY MANAGEMENT, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 156 CHINA: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR COMPLIANCE & GOVERNANCE, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 157 CHINA: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR CLINICAL SAFETY CONTROLS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 158 CHINA: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR FINANCIAL & LEGAL RISK HANDLING, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 159 CHINA: PATIENT SAFETY AND RISK SOFTWARE MARKET, BY DEPLOYMENT MODE, 2023-2030 (USD MILLION)

- TABLE 160 CHINA: PATIENT SAFETY AND RISK SOFTWARE MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 161 CHINA: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR HEALTHCARE PROVIDERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 162 JAPAN: PATIENT SAFETY AND RISK SOFTWARE MARKET, BY FUNCTION, 2023-2030 (USD MILLION)

- TABLE 163 JAPAN: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR RISK & SAFETY MANAGEMENT, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 164 JAPAN: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR COMPLIANCE & GOVERNANCE, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 165 JAPAN: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR CLINICAL SAFETY CONTROLS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 166 JAPAN: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR FINANCIAL & LEGAL RISK HANDLING, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 167 JAPAN: PATIENT SAFETY AND RISK SOFTWARE MARKET, BY DEPLOYMENT MODE, 2023-2030 (USD MILLION)

- TABLE 168 JAPAN: PATIENT SAFETY AND RISK SOFTWARE MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 169 JAPAN: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR HEALTHCARE PROVIDERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 170 INDIA: PATIENT SAFETY AND RISK SOFTWARE MARKET, BY FUNCTION, 2023-2030 (USD MILLION)

- TABLE 171 INDIA: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR RISK & SAFETY MANAGEMENT, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 172 INDIA: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR COMPLIANCE & GOVERNANCE, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 173 INDIA: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR CLINICAL SAFETY CONTROLS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 174 INDIA: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR FINANCIAL & LEGAL RISK HANDLING, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 175 INDIA: PATIENT SAFETY AND RISK SOFTWARE MARKET, BY DEPLOYMENT MODE, 2023-2030 (USD MILLION)

- TABLE 176 INDIA: PATIENT SAFETY AND RISK SOFTWARE MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 177 INDIA: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR HEALTHCARE PROVIDERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 178 AUSTRALIA: PATIENT SAFETY AND RISK SOFTWARE MARKET, BY FUNCTION, 2023-2030 (USD MILLION)

- TABLE 179 AUSTRALIA: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR RISK & SAFETY MANAGEMENT, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 180 AUSTRALIA: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR COMPLIANCE & GOVERNANCE, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 181 AUSTRALIA: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR CLINICAL SAFETY CONTROLS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 182 AUSTRALIA: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR FINANCIAL & LEGAL RISK HANDLING, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 183 AUSTRALIA: PATIENT SAFETY AND RISK SOFTWARE MARKET, BY DEPLOYMENT MODE, 2023-2030 (USD MILLION)

- TABLE 184 AUSTRALIA: PATIENT SAFETY AND RISK SOFTWARE MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 185 AUSTRALIA: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR HEALTHCARE PROVIDERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 186 SOUTH KOREA: PATIENT SAFETY AND RISK SOFTWARE MARKET, BY FUNCTION, 2023-2030 (USD MILLION)

- TABLE 187 SOUTH KOREA: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR RISK & SAFETY MANAGEMENT, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 188 SOUTH KOREA: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR COMPLIANCE & GOVERNANCE, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 189 SOUTH KOREA: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR CLINICAL SAFETY CONTROLS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 190 SOUTH KOREA: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR FINANCIAL & LEGAL RISK HANDLING, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 191 SOUTH KOREA: PATIENT SAFETY AND RISK SOFTWARE MARKET, BY DEPLOYMENT MODE, 2023-2030 (USD MILLION)

- TABLE 192 SOUTH KOREA: PATIENT SAFETY AND RISK SOFTWARE MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 193 SOUTH KOREA: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR HEALTHCARE PROVIDERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 194 REST OF ASIA PACIFIC: PATIENT SAFETY AND RISK SOFTWARE MARKET, BY FUNCTION, 2023-2030 (USD MILLION)

- TABLE 195 REST OF ASIA PACIFIC: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR RISK AND SAFETY MANAGEMENT, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 196 REST OF ASIA PACIFIC: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR COMPLIANCE & GOVERNANCE, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 197 REST OF ASIA PACIFIC: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR CLINICAL SAFETY CONTROLS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 198 REST OF ASIA PACIFIC: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR FINANCIAL & LEGAL RISK HANDLING, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 199 REST OF ASIA PACIFIC: PATIENT SAFETY AND RISK SOFTWARE MARKET, BY DEPLOYMENT MODE, 2023-2030 (USD MILLION)

- TABLE 200 REST OF ASIA PACIFIC: PATIENT SAFETY AND RISK SOFTWARE MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 201 REST OF ASIA PACIFIC: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR HEALTHCARE PROVIDERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 202 LATIN AMERICA: PATIENT SAFETY AND RISK SOFTWARE MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 203 LATIN AMERICA: PATIENT SAFETY AND RISK SOFTWARE MARKET, BY FUNCTION, 2023-2030 (USD MILLION)

- TABLE 204 LATIN AMERICA: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR RISK AND SAFETY MANAGEMENT, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 205 LATIN AMERICA: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR COMPLIANCE & GOVERNANCE, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 206 LATIN AMERICA: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR CLINICAL SAFETY CONTROLS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 207 LATIN AMERICA: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR FINANCIAL & LEGAL RISK HANDLING, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 208 LATIN AMERICA: PATIENT SAFETY AND RISK SOFTWARE MARKET, BY DEPLOYMENT MODE, 2023-2030 (USD MILLION)

- TABLE 209 LATIN AMERICA: PATIENT SAFETY AND RISK SOFTWARE MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 210 LATIN AMERICA: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR HEALTHCARE PROVIDERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 211 BRAZIL: PATIENT SAFETY AND RISK SOFTWARE MARKET, BY FUNCTION, 2023-2030 (USD MILLION)

- TABLE 212 BRAZIL: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR RISK & SAFETY MANAGEMENT, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 213 BRAZIL: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR COMPLIANCE & GOVERNANCE, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 214 BRAZIL: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR CLINICAL SAFETY CONTROLS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 215 BRAZIL: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR FINANCIAL AND LEGAL RISK HANDLING, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 216 BRAZIL: PATIENT SAFETY AND RISK SOFTWARE MARKET, BY DEPLOYMENT MODE, 2023-2030 (USD MILLION)

- TABLE 217 BRAZIL: PATIENT SAFETY AND RISK SOFTWARE MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 218 BRAZIL: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR HEALTHCARE PROVIDERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 219 MEXICO: PATIENT SAFETY AND RISK SOFTWARE MARKET, BY FUNCTION, 2023-2030 (USD MILLION)

- TABLE 220 MEXICO: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR RISK & SAFETY MANAGEMENT, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 221 MEXICO: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR COMPLIANCE & GOVERNANCE, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 222 MEXICO: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR CLINICAL SAFETY CONTROLS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 223 MEXICO: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR FINANCIAL & LEGAL RISK HANDLING, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 224 MEXICO: PATIENT SAFETY AND RISK SOFTWARE MARKET, BY DEPLOYMENT MODE, 2023-2030 (USD MILLION)

- TABLE 225 MEXICO: PATIENT SAFETY AND RISK SOFTWARE MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 226 MEXICO: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR HEALTHCARE PROVIDERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 227 REST OF LATIN AMERICA: PATIENT SAFETY AND RISK SOFTWARE MARKET, BY FUNCTION, 2023-2030 (USD MILLION)

- TABLE 228 REST OF LATIN AMERICA: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR RISK AND SAFETY MANAGEMENT, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 229 REST OF LATIN AMERICA: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR COMPLIANCE & GOVERNANCE, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 230 REST OF LATIN AMERICA: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR CLINICAL SAFETY CONTROLS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 231 REST OF LATIN AMERICA: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR FINANCIAL & LEGAL RISK HANDLING, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 232 REST OF LATIN AMERICA: PATIENT SAFETY AND RISK SOFTWARE MARKET, BY DEPLOYMENT MODE, 2023-2030 (USD MILLION)

- TABLE 233 REST OF LATIN AMERICA: PATIENT SAFETY AND RISK SOFTWARE MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 234 REST OF LATIN AMERICA: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR HEALTHCARE PROVIDERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 235 MIDDLE EAST & AFRICA: PATIENT SAFETY AND RISK SOFTWARE MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 236 MIDDLE EAST & AFRICA: PATIENT SAFETY AND RISK SOFTWARE MARKET, BY FUNCTION, 2023-2030 (USD MILLION)

- TABLE 237 MIDDLE EAST & AFRICA: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR RISK & SAFETY MANAGEMENT, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 238 MIDDLE EAST & AFRICA: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR COMPLIANCE & GOVERNANCE, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 239 MIDDLE EAST & AFRICA: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR CLINICAL SAFETY CONTROLS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 240 MIDDLE EAST & AFRICA: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR FINANCIAL & LEGAL RISK HANDLING, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 241 MIDDLE EAST & AFRICA: PATIENT SAFETY AND RISK SOFTWARE MARKET, BY DEPLOYMENT MODE, 2023-2030 (USD MILLION)

- TABLE 242 MIDDLE EAST & AFRICA: PATIENT SAFETY AND RISK SOFTWARE MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 243 MIDDLE EAST AND AFRICA: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR HEALTHCARE PROVIDERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 244 GCC COUNTRIES: PATIENT SAFETY AND RISK SOFTWARE MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 245 GCC COUNTRIES: PATIENT SAFETY AND RISK SOFTWARE MARKET, BY FUNCTION, 2023-2030 (USD MILLION)

- TABLE 246 GCC COUNTRIES: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR RISK AND SAFETY MANAGEMENT, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 247 GCC COUNTRIES: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR COMPLIANCE & GOVERNANCE, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 248 GCC COUNTRIES: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR CLINICAL SAFETY CONTROLS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 249 GCC COUNTRIES: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR FINANCIAL & LEGAL RISK HANDLING, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 250 GCC COUNTRIES: PATIENT SAFETY AND RISK SOFTWARE MARKET, BY DEPLOYMENT MODE, 2023-2030 (USD MILLION)

- TABLE 251 GCC COUNTRIES: PATIENT SAFETY AND RISK SOFTWARE MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 252 GCC COUNTRIES: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR HEALTHCARE PROVIDERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 253 SAUDI ARABIA: PATIENT SAFETY AND RISK SOFTWARE MARKET, BY FUNCTION, 2023-2030 (USD MILLION)

- TABLE 254 SAUDI ARABIA: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR RISK & SAFETY MANAGEMENT, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 255 SAUDI ARABIA: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR COMPLIANCE & GOVERNANCE, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 256 SAUDI ARABIA: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR CLINICAL SAFETY CONTROLS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 257 SAUDI ARABIA: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR FINANCIAL AND LEGAL RISK HANDLING, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 258 SAUDI ARABIA: PATIENT SAFETY AND RISK SOFTWARE MARKET, BY DEPLOYMENT MODE, 2023-2030 (USD MILLION)

- TABLE 259 SAUDI ARABIA: PATIENT SAFETY AND RISK SOFTWARE MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 260 SAUDI ARABIA: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR HEALTHCARE PROVIDERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 261 UAE: PATIENT SAFETY AND RISK SOFTWARE MARKET, BY FUNCTION, 2023-2030 (USD MILLION)

- TABLE 262 UAE: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR RISK AND SAFETY MANAGEMENT, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 263 UAE: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR COMPLIANCE & GOVERNANCE, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 264 UAE: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR CLINICAL SAFETY CONTROLS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 265 UAE: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR FINANCIAL AND LEGAL RISK HANDLING, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 266 UAE: PATIENT SAFETY AND RISK SOFTWARE MARKET, BY DEPLOYMENT MODE, 2023-2030 (USD MILLION)

- TABLE 267 UAE: PATIENT SAFETY AND RISK SOFTWARE MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 268 UAE: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR HEALTHCARE PROVIDERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 269 REST OF GCC COUNTRIES: PATIENT SAFETY AND RISK SOFTWARE MARKET, BY FUNCTION, 2023-2030 (USD MILLION)

- TABLE 270 REST OF GCC COUNTRIES: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR RISK & SAFETY MANAGEMENT, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 271 REST OF GCC COUNTRIES: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR COMPLIANCE & GOVERNANCE, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 272 REST OF GCC COUNTRIES: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR CLINICAL SAFETY CONTROLS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 273 REST OF GCC COUNTRIES: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR FINANCIAL & LEGAL RISK HANDLING, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 274 REST OF GCC COUNTRIES: PATIENT SAFETY AND RISK SOFTWARE MARKET, BY DEPLOYMENT MODE, 2023-2030 (USD MILLION)

- TABLE 275 REST OF GCC COUNTRIES: PATIENT SAFETY AND RISK SOFTWARE MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 276 REST OF GCC COUNTRIES: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR HEALTHCARE PROVIDERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 277 SOUTH AFRICA: PATIENT SAFETY AND RISK SOFTWARE MARKET, BY FUNCTION, 2023-2030 (USD MILLION)

- TABLE 278 SOUTH AFRICA: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR RISK & SAFETY MANAGEMENT, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 279 SOUTH AFRICA: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR COMPLIANCE & GOVERNANCE, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 280 SOUTH AFRICA: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR CLINICAL SAFETY CONTROLS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 281 SOUTH AFRICA: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR FINANCIAL & LEGAL RISK HANDLING, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 282 SOUTH AFRICA: PATIENT SAFETY AND RISK SOFTWARE MARKET, BY DEPLOYMENT MODE, 2023-2030 (USD MILLION)

- TABLE 283 SOUTH AFRICA: PATIENT SAFETY AND RISK SOFTWARE MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 284 SOUTH AFRICA: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR HEALTHCARE PROVIDERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 285 REST OF MIDDLE EAST & AFRICA: PATIENT SAFETY AND RISK SOFTWARE MARKET, BY FUNCTION, 2023-2030 (USD MILLION)

- TABLE 286 REST OF MIDDLE EAST & AFRICA: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR RISK & SAFETY MANAGEMENT, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 287 REST OF MIDDLE EAST & AFRICA: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR COMPLIANCE & GOVERNANCE, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 288 REST OF MIDDLE EAST & AFRICA: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR CLINICAL SAFETY CONTROLS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 289 REST OF MIDDLE EAST & AFRICA: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR FINANCIAL AND LEGAL RISK HANDLING, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 290 REST OF MIDDLE EAST & AFRICA: PATIENT SAFETY AND RISK SOFTWARE MARKET, BY DEPLOYMENT MODE, 2023-2030 (USD MILLION)

- TABLE 291 REST OF MIDDLE EAST & AFRICA: PATIENT SAFETY AND RISK SOFTWARE MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 292 REST OF MIDDLE EAST & AFRICA: PATIENT SAFETY AND RISK SOFTWARE MARKET FOR HEALTHCARE PROVIDERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 293 OVERVIEW OF STRATEGIES ADOPTED BY KEY PLAYERS IN PATIENT SAFETY AND RISK SOFTWARE MARKET, JANUARY 2022-SEPTEMBER 2025

- TABLE 294 PATIENT SAFETY AND RISK SOFTWARE MARKET: DEGREE OF COMPETITION

- TABLE 295 PATIENT SAFETY AND RISK SOFTWARE MARKET: REGION FOOTPRINT

- TABLE 296 PATIENT SAFETY AND RISK SOFTWARE MARKET: DEPLOYMENT MODE FOOTPRINT

- TABLE 297 PATIENT SAFETY AND RISK SOFTWARE MARKET: FUNCTION FOOTPRINT

- TABLE 298 PATIENT SAFETY AND RISK SOFTWARE MARKET: END-USER FOOTPRINT

- TABLE 299 PATIENT SAFETY AND RISK SOFTWARE MARKET: DETAILED LIST OF KEY STARTUP/SME PLAYERS

- TABLE 300 PATIENT SAFETY AND RISK SOFTWARE MARKET: COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES

- TABLE 301 PATIENT SAFETY AND RISK SOFTWARE MARKET: SOLUTION LAUNCHES AND ENHANCEMENTS, JANUARY 2022-SEPTEMBER 2025

- TABLE 302 PATIENT SAFETY AND RISK SOFTWARE MARKET: DEALS, JANUARY 2022-SEPTEMBER 2025

- TABLE 303 PATIENT SAFETY AND RISK SOFTWARE MARKET: EXPANSIONS, JANUARY 2022-AUGUST 2025

- TABLE 304 RISKONNECT, INC.: COMPANY OVERVIEW

- TABLE 305 RISKONNECT, INC.: SOLUTIONS OFFERED

- TABLE 306 RISKONNECT, INC.: SOLUTION LAUNCHES AND ENHANCEMENTS, JANUARY 2022-SEPTEMBER 2025

- TABLE 307 RISKONNECT, INC.: DEALS, JANUARY 2022-SEPTEMBER 2025

- TABLE 308 ORIGAMI RISK LLC: COMPANY OVERVIEW

- TABLE 309 ORIGAMI RISK LLC: SOLUTIONS OFFERED

- TABLE 310 ORIGAMI RISK LLC: SOLUTION LAUNCHES AND ENHANCEMENTS, JANUARY 2022-SEPTEMBER 2025

- TABLE 311 RLDATIX: COMPANY OVERVIEW

- TABLE 312 RLDATIX: SOLUTIONS OFFERED

- TABLE 313 RLDATIX: SOLUTION LAUNCHES AND ENHANCEMENTS, JANUARY 2022-SEPTEMBER 2025

- TABLE 314 RLDATIX: DEALS, JANUARY 2022-SEPTEMBER 2025

- TABLE 315 RLDATIX: EXPANSIONS, JANUARY 2022-SEPTEMBER 2025

- TABLE 316 HEALTH CATALYST: COMPANY OVERVIEW

- TABLE 317 HEALTH CATALYST: SOLUTIONS OFFERED

- TABLE 318 HEALTH CATALYST: SOLUTION LAUNCHES AND ENHANCEMENTS, JANUARY 2022-SEPTEMBER 2025

- TABLE 319 HEALTH CATALYST: DEALS, JANUARY 2022-SEPTEMBER 2025

- TABLE 320 SYMPLR: COMPANY OVERVIEW

- TABLE 321 SYMPLR: SOLUTIONS OFFERED

- TABLE 322 SYMPLR: SOLUTION LAUNCHES AND ENHANCEMENTS, JANUARY 2022-SEPTEMBER 2025

- TABLE 323 SYMPLR: DEALS, JANUARY 2022-SEPTEMBER 2025

- TABLE 324 CLARITY GROUP, INC.: COMPANY OVERVIEW

- TABLE 325 CLARITY GROUP, INC.: SOLUTIONS OFFERED

- TABLE 326 PERFORMANCE HEALTH PARTNERS: COMPANY OVERVIEW

- TABLE 327 PERFORMANCE HEALTH PARTNERS: SOLUTIONS OFFERED

- TABLE 328 PERFORMANCE HEALTH PARTNERS: DEALS, JANUARY 2022-SEPTEMBER 2025

- TABLE 329 MORCARE: COMPANY OVERVIEW

- TABLE 330 MORCARE: SOLUTIONS OFFERED

- TABLE 331 RISKQUAL TECHNOLOGIES, INC.: COMPANY OVERVIEW

- TABLE 332 RISKQUAL TECHNOLOGIES, INC.: SOLUTIONS OFFERED

- TABLE 333 PRISTA CORPORATION: COMPANY OVERVIEW

- TABLE 334 PRISTA CORPORATION: SOLUTIONS OFFERED

- TABLE 335 SAFEQUAL: COMPANY OVERVIEW

- TABLE 336 SAFEQUAL: SOLUTIONS OFFERED

- TABLE 337 IQVIA: COMPANY OVERVIEW

- TABLE 338 IQVIA: SOLUTIONS OFFERED

- TABLE 339 IQVIA: SOLUTION LAUNCHES AND ENHANCEMENTS, JANUARY 2022-SEPTEMBER 2025

- TABLE 340 IQVIA: DEALS, JANUARY 2022-SEPTEMBER 2025

- TABLE 341 INOVALON: COMPANY OVERVIEW

- TABLE 342 INOVALON: SOLUTIONS OFFERED

- TABLE 343 INOVALON: SOLUTION LAUNCHES AND ENHANCEMENTS, JANUARY 2022-SEPTEMBER 2025

- TABLE 344 NAVEX GLOBAL, INC.: COMPANY OVERVIEW

- TABLE 345 NAVEX GLOBAL, INC.: SOLUTIONS OFFERED

- TABLE 346 NAVEX GLOBAL, INC.: SOLUTION LAUNCHES AND ENHANCEMENTS, JANUARY 2022-SEPTEMBER 2025

- TABLE 347 NAVEX GLOBAL, INC.: DEALS, JANUARY 2022-SEPTEMBER 2024

- TABLE 348 NAVEX GLOBAL, INC.: EXPANSIONS, JANUARY 2022-SEPTEMBER 2025

- TABLE 349 CENSINET: COMPANY OVERVIEW

- TABLE 350 CENSINET: SOLUTIONS OFFERED

- TABLE 351 CENSINET: SOLUTION LAUNCHES AND ENHANCEMENTS, JANUARY 2022-SEPTEMBER 2025

- TABLE 352 AMERICAN DATA NETWORK: COMPANY OVERVIEW

- TABLE 353 AMERICAN DATA NETWORK: SOLUTIONS OFFERED

- TABLE 354 ARVENTA: COMPANY OVERVIEW

- TABLE 355 ARVENTA: SOLUTIONS OFFERED

- TABLE 356 COMPLIANCEQUEST: COMPANY OVERVIEW

- TABLE 357 COMPLIANCEQUEST: SOLUTIONS OFFERED

- TABLE 358 COMPLIANCEQUEST: SOLUTION LAUNCHES AND ENHANCEMENTS, JANUARY 2022-SEPTEMBER 2025

- TABLE 359 COMPLIANCEQUEST: DEALS, JANUARY 2022-SEPTEMBER 2025

- TABLE 360 RADAR HEALTHCARE INC: COMPANY OVERVIEW

- TABLE 361 RADAR HEALTHCARE INC: SOLUTIONS OFFERED

- TABLE 362 PASCAL METRICS INC.: COMPANY OVERVIEW

- TABLE 363 PASCAL METRICS INC.: SOLUTIONS OFFERED

- TABLE 364 OMNIGO: COMPANY OVERVIEW

- TABLE 365 LOGICMANAGER, INC.: COMPANY OVERVIEW

- TABLE 366 DEXUR: COMPANY OVERVIEW

- TABLE 367 HEALTHCARE GRC PTE. LTD.: COMPANY OVERVIEW

- TABLE 368 NOSOTECH INC.: COMPANY OVERVIEW

List of Figures

- FIGURE 1 PATIENT SAFETY AND RISK SOFTWARE MARKET SEGMENTATION AND REGIONAL SCOPE

- FIGURE 2 RESEARCH DESIGN

- FIGURE 3 PRIMARY SOURCES

- FIGURE 4 BREAKDOWN OF PRIMARY INTERVIEWS (DEMAND-SIDE): BY COMPANY TYPE, DESIGNATION, AND REGION

- FIGURE 5 SUPPLY-SIDE MARKET ESTIMATION

- FIGURE 6 PATIENT SAFETY AND RISK SOFTWARE MARKET: REVENUE ESTIMATION APPROACH

- FIGURE 7 BOTTOM-UP APPROACH: END-USER SPENDING ON PATIENT SAFETY AND RISK SOFTWARE

- FIGURE 8 CAGR PROJECTIONS FROM MARKET DYNAMICS, 2025-2030

- FIGURE 9 CAGR PROJECTIONS: SUPPLY-SIDE ANALYSIS

- FIGURE 10 TOP-DOWN APPROACH

- FIGURE 11 DATA TRIANGULATION METHODOLOGY

- FIGURE 12 PATIENT SAFETY AND RISK SOFTWARE MARKET, BY FUNCTION, 2025 VS. 2030 (USD MILLION)

- FIGURE 13 PATIENT SAFETY AND RISK SOFTWARE MARKET, BY DEPLOYMENT MODE, 2025 VS. 2030 (USD MILLION)

- FIGURE 14 PATIENT SAFETY AND RISK SOFTWARE MARKET, BY END USER, 2025 VS. 2030 (USD MILLION)

- FIGURE 15 PATIENT SAFETY AND RISK SOFTWARE MARKET: GEOGRAPHICAL SNAPSHOT

- FIGURE 16 GROWING HEALTHCARE EXPENDITURE AND RISING ADOPTION OF ADVANCED TECHNOLOGIES TO DRIVE MARKET

- FIGURE 17 HEALTHCARE PROVIDERS AND US LED NORTH AMERICAN MARKET IN 2024

- FIGURE 18 INDIA TO REGISTER HIGHEST GROWTH DURING FORECAST PERIOD

- FIGURE 19 EMERGING MARKETS TO HAVE HIGHER GROWTH THAN DEVELOPED MARKETS DURING FORECAST PERIOD

- FIGURE 20 PATIENT SAFETY AND RISK SOFTWARE MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

- FIGURE 21 REPORTS SUBMITTED TO PENNSYLVANIA'S PATIENT SAFETY REPORTING SYSTEM BY HOSPITALS, 2022-2024

- FIGURE 22 REPORTS SUBMITTED TO PENNSYLVANIA'S PATIENT SAFETY REPORTING SYSTEM BY NON-HOSPITALS, 2022-2024

- FIGURE 23 REVENUE SHIFT IN PATIENT SAFETY AND RISK SOFTWARE MARKET

- FIGURE 24 PATIENT SAFETY AND RISK SOFTWARE MARKET: VALUE CHAIN ANALYSIS

- FIGURE 25 PATIENT SAFETY AND RISK SOFTWARE MARKET: ECOSYSTEM ANALYSIS

- FIGURE 26 PATIENT SAFETY AND RISK SOFTWARE MARKET: INVESTMENT AND FUNDING SCENARIO

- FIGURE 27 PATIENT SAFETY AND RISK SOFTWARE MARKET: JURISDICTION AND TOP APPLICANT ANALYSIS, JANUARY 2022-SEPTEMBER 2025

- FIGURE 28 PATIENT SAFETY AND RISK SOFTWARE MARKET: PATENT ANALYSIS, JANUARY 2015-SEPTEMBER 2025

- FIGURE 29 PATIENT SAFETY AND RISK SOFTWARE MARKET: PORTER'S FIVE FORCES ANALYSIS

- FIGURE 30 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS OF TOP THREE END USERS

- FIGURE 31 KEY BUYING CRITERIA FOR TOP THREE END USERS

- FIGURE 32 MARKET POTENTIAL OF AI/GENERATIVE AI IN PATIENT SAFETY AND RISK SOFTWARE

- FIGURE 33 IMPACT OF AI/GEN AI ON INTERCONNECTED AND ADJACENT ECOSYSTEMS

- FIGURE 34 NORTH AMERICA: PATIENT SAFETY AND RISK SOFTWARE MARKET SNAPSHOT

- FIGURE 35 ASIA PACIFIC: PATIENT SAFETY AND RISK SOFTWARE MARKET SNAPSHOT

- FIGURE 36 REVENUE ANALYSIS OF KEY PLAYERS IN PATIENT SAFETY AND RISK SOFTWARE MARKET, 2020-2024 (USD MILLION)

- FIGURE 37 MARKET SHARE ANALYSIS OF KEY PLAYERS IN PATIENT SAFETY AND RISK SOFTWARE MARKET, 2024

- FIGURE 38 PATIENT SAFETY AND RISK SOFTWARE MARKET: BRAND/SOFTWARE COMPARISON

- FIGURE 39 YEAR-TO-DATE (YTD) PRICE TOTAL RETURN AND 5-YEAR STOCK BETA OF KEY VENDORS

- FIGURE 40 EV/EBITDA OF KEY VENDORS

- FIGURE 41 PATIENT SAFETY AND RISK SOFTWARE MARKET: COMPANY EVALUATION MATRIX (KEY PLAYERS), 2024

- FIGURE 42 PATIENT SAFETY AND RISK SOFTWARE MARKET: COMPANY FOOTPRINT

- FIGURE 43 PATIENT SAFETY AND RISK SOFTWARE MARKET: COMPANY EVALUATION MATRIX (STARTUPS/SMES), 2024

- FIGURE 44 HEALTH CATALYST: COMPANY SNAPSHOT (2024)

- FIGURE 45 IQVIA: COMPANY SNAPSHOT (2024)

2026年全球病患安全与风险管理软体市场报告

2026年全球病患安全与风险管理软体市场报告 CSSD感染控制清洁耗材市场按产品类型、灭菌方法、最终用户和分销管道划分,全球预测,2026-2032年共用医院陪伴床市场:依技术、材质、最终用户和分销管道划分-2026-2032年全球预测

CSSD感染控制清洁耗材市场按产品类型、灭菌方法、最终用户和分销管道划分,全球预测,2026-2032年共用医院陪伴床市场:依技术、材质、最终用户和分销管道划分-2026-2032年全球预测 病人安全与风险管理软体市场规模、份额及成长分析(按类型、部署类型、最终用户和地区划分)-2026-2033年产业预测2025年病患风险分层全球市场报告

病人安全与风险管理软体市场规模、份额及成长分析(按类型、部署类型、最终用户和地区划分)-2026-2033年产业预测2025年病患风险分层全球市场报告 病患安全与风险管理软体市场 - 全球产业规模、份额、趋势、机会和预测,按类型、最终用户、地区和竞争细分,2020-2030 年

病患安全与风险管理软体市场 - 全球产业规模、份额、趋势、机会和预测,按类型、最终用户、地区和竞争细分,2020-2030 年 医疗保健安全风险管理解决方案市场:全球产业分析,规模,占有率,成长,趋势,2024-2032年预测

医疗保健安全风险管理解决方案市场:全球产业分析,规模,占有率,成长,趋势,2024-2032年预测 病患安全与风险管理软体市场规模、份额、趋势分析报告:按类型、按部署类型、按最终用途、按地区、细分市场预测,2024-2030 年

病患安全与风险管理软体市场规模、份额、趋势分析报告:按类型、按部署类型、按最终用途、按地区、细分市场预测,2024-2030 年