|

市场调查报告书

商品编码

1906295

全球超纯石墨市场(按来源、应用和地区划分)-预测至2030年Ultra-high-purity Graphite Market by Source, Type, Application, End-Use Industry, and Region - Global Forecast to 2030 |

||||||

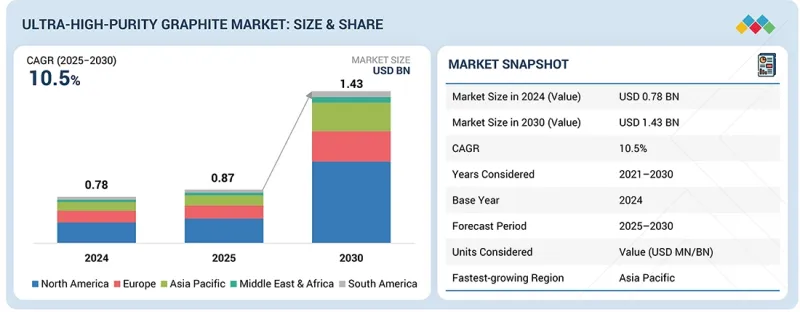

预计超高纯度石墨市场将从 2025 年的 8.7 亿美元成长到 2030 年的 14.3 亿美元,预测期内复合年增长率为 10.5%。

可再生能源整体生产成本下降、电解技术进步以及电力产业和燃料电池电动车需求增加等几个关键因素正在推动超高纯度石墨市场的成长。

| 调查范围 | |

|---|---|

| 调查期 | 2021-2030 |

| 基准年 | 2024 |

| 预测期 | 2025-2030 |

| 目标单元 | 价值(百万美元/十亿美元) |

| 部分 | 按原料、应用、地区划分 |

| 目标区域 | 亚太地区、欧洲、北美、中东和非洲、南美 |

超纯石墨在化学、交通、电网注入和电力等多个行业都有应用。其零排放的生产流程使其作为传统灰氢、褐氢和蓝氢的替代品,越来越受欢迎。技术进步也使超纯石墨的成本更具竞争力。这种永续燃料正成为众多终端使用者产业中石化燃料的可行替代方案。

凭藉其无与伦比的纯度、结构均匀性和超越天然石墨的可扩展性,合成石墨已成为超高纯度(UHP)石墨市场中增长最快、市场份额最高的原材料细分市场。随着包括锂离子电池、半导体、航太和先进核子反应炉在内的高科技产业对杂质含量极低且性能特性精准的材料的需求不断增长,合成石墨的需求也在加速增长。电动车(EV)和大规模能源储存系统生产的快速成长是推动合成石墨发展的关键因素,因为它为高性能电池负极提供了卓越的电化学稳定性、长寿命和快速充电能力。

加强国内供应链、减少对特定地区天然石墨开采的依赖以及消除污染风险等全球趋势,正促使製造商转向工程合成石墨。对先进精炼技术、高效石墨化製程以及可再生能源驱动型生产的投资,都提升了工程石墨的市场吸引力,使其成为支撑现代能源和半导体生态系统快速发展的关键材料。

按应用领域划分,锂离子电池负极材料是超高纯石墨市场中成长最快的细分市场,这主要得益于电动车、大型能源储存系统和便携式电子设备的快速普及。超高纯石墨因其优异的导电性、热稳定性和结构完整性,在这些应用中得到越来越广泛的应用,从而提高了电池效率并延长了电池寿命。主要电池製造商正在投资研发先进的合成石墨和包覆石墨,以提高能量密度和充电性能。政府支持电动车生产和促进再生能源来源併网的措施也推动了对石墨的需求。此外,对下一代电池化学技术研发的持续投入,也拓展了石墨在传统固态电池的应用。这些因素共同作用,使得锂离子电池负极材料细分市场成为全球超高纯石墨市场成长的主要驱动力。

预计亚太地区在整个预测期内仍将是超纯石墨的最大市场,这主要得益于该地区半导体、电子和电动车製造业的快速成长。中国、日本、韩国和台湾等国家和地区被认为是全球晶片和电池生产以及先进材料加工最重要的地区,它们也是超纯石墨的主要用户,这些石墨用于晶圆处理、高温炉部件、锂离子电池负极材料和精密温度控管系统。

政府对扩大半导体产能的大量投资、积极的电动车推广目标以及电池供应链的本地化,进一步推动了该地区的需求。此外,亚太地区位置全球一些最大的超纯石墨生产商和精炼厂,使其在生产规模、成本效益和技术能力方面具有优势。可再生能源系统、先进核能技术和高性能工业流程的日益普及也推动了该地区的市场成长。所有这些因素加在一起,有望使亚太地区在未来几年成为超纯石墨市场规模和成长率的主导地区。

超高纯度石墨市场的主要企业包括:法国的Mersen公司、美国的Superior Graphite公司、日本的Toyo Tanso公司、德国的SGL Carbon公司以及美国的GrafTech International公司。这些主要企业是超高纯度石墨市场的关键贡献者。他们正采取各种策略,例如合作协议、合资企业和业务扩张,以提高市场份额和收入。

研究范围:

本报告根据类型、应用、原材料、终端用户行业和地区对超高纯度石墨市场进行细分,并预测其市场规模。报告对主要企业进行策略性分析,全面剖析其市场占有率和核心竞争优势。此外,报告还追踪和分析市场中的竞争动态,例如扩张、合作和收购。

购买这份报告的理由:

本报告旨在透过提供超高纯度石墨市场及其细分市场最准确的收入预测,帮助市场领导和新参与企业。此外,本报告还将帮助相关人员深入了解市场竞争格局,获取宝贵资讯以巩固其业务地位,并制定有效的打入市场策略。报告还提供了市场趋势以及关键市场驱动因素、限制因素、挑战和机会方面的资讯。

本报告深入分析了以下内容:

- 透过分析关键驱动因素(电动车和储能领域锂离子电池的日益普及、半导体和硅加工行业需求的成长以及太阳能光伏製造的扩张)、限制因素(供应链集中和高度进口依赖、环境法规和合法规挑战)、机会(先进高温核核子反应炉专案的发展、航空航太和高超音速平台中碳碳热防护系统的日益普及)以及挑战(由于先进的提炼和製作流程导致的高生产成本),来确定影响超高纯度石墨市场成长的因素。

- 产品开发与创新:对超高纯度石墨市场即将出现的技术趋势和研发活动进行详细分析。

- 市场发展:关于盈利的市场的全面资讯—该报告按地区分析了超纯石墨市场。

- 市场多元化:全面介绍超纯石墨市场的新产品、各种产品类型、未开发的地区、近期趋势和投资情况。

- 超高纯石墨主要企业包括:Superior Graphite(美国)、Focus Graphite(加拿大)、Toyo Tanso(日本)、Mersen(法国)、HPMS Graphite(美国)、Ceylon Graphite Corp.(美国)、Sarytogan Graphite Limited(美国)、Amsted Graphite Materialerials(美国)、Enter) Minerals(巴西)、XRD Graphite Manufacturing(中国)、SEC Carbon Limited(日本)、SGL Carbon(日本)、American Elements(美国)和Canada Carbon(加拿大)。本报告对主要企业的市场份额、成长策略和产品供应进行了详细评估。

目录

第一章 引言

第二章执行摘要

第三章重要考察

第四章 市场概览

- 市场动态

- 未满足的需求和差距

- 相互关联的市场与跨产业机会

- 新的经营模式和生态系统变化

- 一级/二级/三级公司的策略性倡议

第五章 产业趋势

- 波特五力分析

- 总体经济指标

- 价值链分析

- 生态系分析

- 定价分析

- 贸易分析

- 2025-2026 年主要会议和活动

- 影响客户业务的趋势/干扰因素

- 投资和资金筹措方案

- 案例研究分析

- 2025年美国关税对超纯石墨市场的影响

- 关键新兴技术

- 互补技术

- 邻近技术

- 专利分析

- 未来应用

- 人工智慧/生成式人工智慧对超高纯度石墨市场的影响

- 成功案例和实际应用

第六章永续性和监管环境

- 地方法规和合规性

- 对永续性的承诺

- 永续性影响和监管政策倡议

- 认证、标籤和环境标准

第七章:顾客状况与购买行为

- 决策流程

- 主要相关人员和采购标准

- 招募障碍和内部挑战

- 各个终端用户产业中尚未满足的需求

- 市场盈利

第八章 超纯石墨的类型

- 热解石墨

- 等向性石墨

- 精製天然脉状石墨

- 高纯度合成石墨粉

- 其他的

第九章 超纯石墨终端应用产业

- 核能

- 航太与国防

- 电子学

- 储能

- 冶金

- 太阳能发电

- 其他的

- 医疗保健

- 研究

第十章 超纯石墨市场(按原始材料划分)

- 合成石墨

- 天然石墨

第十一章 超纯石墨市场(依应用领域划分)

- 核子反应炉

- 锂离子电池负极

- 半导体

- 其他的

- 电弧炉电极

- 温度控管系统

- 润滑剂

- 导电涂层

第十二章 超纯石墨市场(按地区划分)

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 其他的

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 法国

- 西班牙

- 英国

- 义大利

- 其他的

- 中东和非洲

- 海湾合作委员会国家

- 南非

- 其他的

- 南美洲

- 巴西

- 阿根廷

- 其他的

第十三章 竞争格局

- 主要参与企业的策略/优势

- 收入分析

- 市占率分析

- 品牌/产品对比

- 公司估值矩阵:主要参与企业,2024 年

- 公司估值矩阵:Start-Ups/中小企业,2024 年

- 竞争场景

- 估值和财务指标

第十四章:公司简介

- 主要参与企业

- MERSEN

- TOYO TANSO CO., LTD.

- SGL CARBON

- ENTEGRIS

- GRAFTECH INTERNATIONAL

- CEYLON GRAPHITE CORP.

- SUPERIOR GRAPHITE

- FOCUS GRAPHITE

- SEC CARBON, LIMITED

- ASBURY CARBONS

- HPMS GRAPHITE

- XRD GRAPHITE MANUFACTURING CO., LTD.

- SARYTOGAN GRAPHITE LIMITED

- AMSTED GRAPHITE MATERIALS

- EAST CARBON

- AMERICAN ELEMENTS

- CANADA CARBON

- ATLAS CRITICAL MINERALS

- JINSUN NEW MATERIAL TECHNOLOGY, LTD.

- 其他公司

- NINGBO RUIYI SEALING MATERIAL CO., LTD.

- XURAN NEW MATERIALS LIMITED

- CANGZHOU CARBON TECHNOLOGY CO., LTD.

- CARBONIUM CORE

第十五章调查方法

第十六章附录

The ultra-high-purity graphite market is projected to grow from USD 0.87 billion in 2025 to USD 1.43 billion by 2030, at a CAGR of 10.5% during the forecast period. Several key factors, such as the decreasing cost of renewable energy production from all sources, advancements in electrolysis technologies, and a rising demand from the power industry and fuel cell electric vehicles, are driving the market for ultra-high-purity graphite.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD Million/Billion) |

| Segments | Type, Application, Source, End-Use Industry, And Region |

| Regions covered | Asia Pacific, Europe, North America, the Middle East & Africa, and South America |

Ultra-high-purity graphite has applications across various industries, including chemicals, mobility, grid injection, and power. It is increasingly being seen as a replacement for conventional gray, brown, and blue hydrogen due to its zero-emission production process. Technological advancements have also made ultra-high-purity graphite more cost-competitive. This sustainable fuel source is emerging as a viable alternative to fossil fuels across various end-use industries.

"By source, the synthetic graphite segment of the ultra-high-purity market is estimated to register the fastest growth, in terms of value, during the forecast period."

Synthetic graphite exhibits the fastest, as well as the highest growth rate, among the source segments in the ultra-high-purity (UHP) graphite market, driven by its unmatched purity, structural uniformity, and scalability, which surpass those of natural graphite. The demand is accelerating as high-tech industries, such as those for lithium-ion batteries, semiconductors, aerospace, and advanced nuclear reactors, require more materials with extremely low levels of impurities and precisely engineered performance characteristics. The rapid rise in the production of electric vehicles (EVs) along with large energy storage systems has been a major factor in favor of synthetic graphite, as it provides the anodes of high-performance batteries with the characteristics of excellent electrochemical stability, long cycle life, and rapid charging capabilities.

The global movement aimed at reinforcing domestic supply chains, reducing reliance on mining natural graphite in specific regions, and eliminating contamination risks are some of the factors that are prompting manufacturers to turn towards engineered synthetic alternatives. Upgraded purification technologies, more efficient graphitization processes, and investment in renewable-powered production are all contributing to the market appeal of artificial graphite, positioning it as an essential material that supports the rapid growth of modern energy and semiconductor ecosystems.

"By application, the lithium-ion battery anodes segment is estimated to be the fastest-growing segment of the ultra-high-purity graphite market during the forecast period."

Based on application, the lithium-ion battery anodes are the fastest-growing source segment in the ultra-high-purity graphite market, driven by the rapid adoption of electric vehicles, grid-scale energy storage, and portable electronics. Ultra-high-purity graphite is increasingly used in such applications due to its superior electrical conductivity, thermal stability, and structural integrity, resulting in enhanced battery efficiency and a longer life cycle. The primary battery makers are investing in advanced synthetic and coated graphite to enhance energy density and charging performance. The incentives provided by the government to support the production of electric vehicles and the integration of renewable energy sources are also increasing the demand for graphite. Additionally, the continued investment in R&D of next-generation battery chemicals is broadening the use of graphite in both conventional and solid-state batteries. All these factors combined make the lithium-ion battery anode segment a key driver of global market growth for ultra-high-purity graphite.

"The ultra-high-purity graphite market in Asia is projected to register the fastest growth, in terms of value and volume, during the forecast period."

Asia Pacific is expected to be the largest market for ultra-high-purity graphite throughout the forecast period, primarily due to the rapid growth of the semiconductor, electronics, and electric vehicle manufacturing sectors in the region. The countries, including China, Japan, South Korea, and Taiwan, are considered to be the most important places worldwide for the production of chips, batteries, and the processing of advanced materials, which are the main users of ultra-high-purity graphite for wafer handling, high-temperature furnace components, lithium-ion battery anodes, and precision thermal management systems.

High investments in semiconductor capacity expansion by governments, aggressive EV adoption targets, and the localization of battery supply chains are further accelerating demand in the region. Moreover, the Asia Pacific is home to some of the largest producers and purification facilities of ultra-high-purity graphite globally. Hence, the region has an advantage in terms of manufacturing scale, cost efficiency, and technological capability. The increasing adoption of renewable energy systems, advanced nuclear technologies, and high-performance industrial processes is also a factor driving the market's growth in the region. Therefore, all these reasons together make the Asia Pacific a leading region in the ultra-high-purity graphite market, both in terms of size and growth rate in the years to come.

Profile break-up of primary participants for the report:

- By Company Type: Tier 1 - 45%, Tier 2 - 22%, and Tier 3 - 33%

- By Designation: C-Level Executives- 50%, Directors- 10%, and Others - 40%

- By Region: North America - 17%, Asia Pacific - 17%, Europe - 33%, Middle East & Africa - 25%, and South America - 8%

Leading players operating in the ultra-high-purity graphite market include Mersen (France), Superior Graphite (US), Toyo Tanso Co., Ltd. (Japan), SGL Carbon (Germany), and GrafTech International (US). These key players are significant contributors to the ultra-high-purity graphite market. These players have adopted various strategies, including agreements, joint ventures, and expansions, to increase their market share and business revenue.

Research Coverage:

The report defines segments and projects the size of the ultra-high-purity graphite market based on type, application, source, end-use industry, and region. It strategically profiles the key players and comprehensively analyzes their market shares and core competencies. It also tracks and analyzes competitive developments, such as expansions, agreements, and acquisitions undertaken by them in the market.

Reasons to Buy the Report:

The report is expected to help market leaders/new entrants by providing them with the closest approximations of revenue numbers for the ultra-high-purity graphite market and its segments. This report is also expected to help stakeholders gain a deeper understanding of the market's competitive landscape, acquire valuable insights to enhance their business positions, and develop effective go-to-market strategies. It also enables stakeholders to understand the market's pulse and provides information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

- Analysis of critical drivers (Growing adoption of lithium-ion batteries in EV and energy storage, rising demand from semiconductor and silicon processing industries, expansion of solar PV manufacturing), restraints (Supply chain concentration and high import dependency, environmental and regulatory compliance challenges), opportunities (Development of advanced high-temperature nuclear reactor programs, increasing use of carbon-carbon thermal protection systems in aerospace and hypersonic platforms), and challenges (High production costs driven by the intensity of purification and processing) that are influencing the growth of the ultra-high-purity graphite market.

- Product Development/Innovation: Detailed insights into upcoming technologies, research & development activities in the ultra-high-purity graphite market.

- Market Development: Comprehensive information about lucrative markets - the report analyzes the ultra-high-purity graphite market across regions.

- Market Diversification: Exhaustive information about new products, various types, untapped geographies, recent developments, and investments in the ultra-high-purity graphite market.

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and product offerings of leading players, such as Superior Graphite (US), Focus Graphite (Canada), Toyo Tanso Co., Ltd. (Japan), Mersen (France), HPMS Graphite (US), Ceylon Graphite Corp. (Canada), Sarytogan Graphite Limited (Australia), Amsted Graphite Materials (US), GrafTech International (US), Entegris (US), East Carbon (China), Atlas Critical Minerals (Brazil), XRD Graphite Manufacturing Co., Ltd. (China), SEC Carbon Limited (Japan), SGL Carbon (Germany), American Elements (US), and Canada Carbon (Canada), are the key players in ultra-high-purity graphite market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS & EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.4 LIMITATIONS

- 1.5 STAKEHOLDERS

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: SHARE INSIGHTS AND STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN THE MARKET

- 2.4 HIGH-GROWTH SEGMENTS & EMERGING FRONTIERS

- 2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN ULTRA-HIGH PURITY GRAPHITE MARKET

- 3.2 ULTRA-HIGH PURITY GRAPHITE MARKET, BY SOURCE AND REGION

- 3.3 ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION

- 3.4 ULTRA-HIGH PURITY GRAPHITE MARKET, BY COUNTRY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Growing adoption of lithium-ion batteries in EV and energy storage

- 4.2.1.2 Rising demand from semiconductor and silicon processing industries

- 4.2.1.3 Expansion of solar PV manufacturing

- 4.2.2 RESTRAINTS

- 4.2.2.1 Supply chain concentration and high import dependency

- 4.2.2.2 Environmental and regulatory compliance challenges

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Development of advanced high-temperature nuclear reactor programs

- 4.2.3.2 Increasing use of carbon-carbon thermal protection systems in aerospace and hypersonic platforms

- 4.2.4 CHALLENGES

- 4.2.4.1 High production costs driven by purification and processing intensity

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS IN ULTRA-HIGH PURITY GRAPHITE MARKET

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 EMERGING BUSINESS MODELS AND ECOSYSTEM SHIFTS

- 4.5.1 EMERGING BUSINESS MODELS

- 4.5.2 ECOSYSTEM SHIFTS

- 4.6 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

- 4.6.1 KEY MOVES AND STRATEGIC FOCUS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMICS INDICATORS

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST

- 5.2.3 TRENDS IN GLOBAL ELECTRONICS INDUSTRY

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 AVERAGE SELLING PRICE, BY KEY PLAYERS

- 5.5.2 AVERAGE SELLING PRICE TREND, BY REGION

- 5.6 TRADE ANALYSIS

- 5.6.1 IMPORT SCENARIO (HS CODE 380110)

- 5.6.2 EXPORT SCENARIO (HS CODE 380110)

- 5.7 KEY CONFERENCES AND EVENTS, 2025-2026

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.9 INVESTMENT AND FUNDING SCENARIO

- 5.10 CASE STUDY ANALYSIS

- 5.10.1 FABRICATING HIGH-PURITY GRAPHITE DISK ELECTRODES AS A COST-EFFECTIVE ALTERNATIVE IN FUNDAMENTAL ELECTROCHEMISTRY RESEARCH

- 5.10.2 PURIFICATION OF SPHERICAL GRAPHITE AS ANODE FOR LI-ION BATTERY: A COMPARATIVE STUDY ON PURIFYING APPROACHES

- 5.10.3 ULTRA-HIGH TEMPERATURE PURIFICATION OF GRAPHITE FOR DEVELOPMENT OF A CONTINUOUS PROCESS

- 5.11 IMPACT OF 2025 US TARIFF ON ULTRA-HIGH PURITY GRAPHITE MARKET

- 5.11.1 INTRODUCTION

- 5.11.2 KEY TARIFF RATES

- 5.11.3 PRICE IMPACT ANALYSIS

- 5.11.4 IMPACT ON COUNTRIES/REGIONS

- 5.11.4.1 US

- 5.11.4.2 Europe

- 5.11.4.3 Asia Pacific

- 5.11.5 IMPACT ON END-USE INDUSTRIES

- 5.12 KEY EMERGING TECHNOLOGIES

- 5.12.1 HIGH-TEMPERATURE THERMAL PURIFICATION

- 5.12.2 CHEMICAL PURIFICATION OF GRAPHITE

- 5.12.3 CHEMICAL VAPOR DEPOSITION OF GRAPHITE

- 5.13 COMPLEMENTARY TECHNOLOGIES

- 5.13.1 PLASMA PURIFICATION OF GRAPHITE

- 5.14 ADJACENT TECHNOLOGIES

- 5.14.1 FLEXIBLE GRAPHITE PRODUCTION PROCESS

- 5.14.2 GRAPHITE INTERCALATION COMPOUND (GIC) SYNTHESIS

- 5.15 PATENT ANALYSIS

- 5.15.1 INTRODUCTION

- 5.15.2 METHODOLOGY

- 5.15.3 DOCUMENT TYPE

- 5.15.4 INSIGHTS

- 5.15.5 LEGAL STATUS OF PATENTS

- 5.15.6 JURISDICTION ANALYSIS

- 5.15.7 TOP APPLICANTS

- 5.15.8 LIST OF MAJOR PATENTS

- 5.16 FUTURE APPLICATIONS

- 5.16.1 SEMICONDUCTOR FURNACE COMPONENTS: NEXT-GENERATION CHIP MANUFACTURING

- 5.16.2 SOLAR-GRADE SILICON PRODUCTION: HIGH-EFFICIENCY PHOTOVOLTAICS

- 5.16.3 ADVANCED BATTERY TECHNOLOGIES: NEXT-GENERATION ENERGY STORAGE SYSTEMS

- 5.16.4 AEROSPACE & DEFENSE SYSTEMS: EXTREME-ENVIRONMENT STRUCTURAL COMPONENTS

- 5.16.5 NUCLEAR TECHNOLOGIES: NEXT-GENERATION REACTORS & FUSION SYSTEMS

- 5.17 IMPACT OF AI/GEN AI ON ULTRA-HIGH PURITY GRAPHITE MARKET

- 5.17.1 TOP USE CASES AND MARKET POTENTIAL

- 5.17.2 BEST PRACTICES: COMPANIES/INSTITUTIONS' USE CASES

- 5.17.3 CASE STUDIES OF ULTRA-HIGH PURITY GRAPHITE

- 5.17.4 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 5.17.5 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN ULTRA-HIGH PURITY GRAPHITE MARKET

- 5.18 SUCCESS STORIES AND REAL-WORLD APPLICATIONS

- 5.18.1 TOYO TANSO: ULTRA-HIGH PURITY ISOTROPIC GRAPHITE

- 5.18.2 MERSEN: ADVANCED PURIFIED GRAPHITE & SIC-COATED SOLUTIONS

- 5.18.3 TSMC (TAIWAN): SEMICONDUCTOR DEMAND DRIVING ULTRA-HIGH PURITY GRAPHITE ADOPTION

6 SUSTAINABILITY AND REGULATORY LANDSCAPE

- 6.1 REGIONAL REGULATIONS AND COMPLIANCE

- 6.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 6.1.2 INDUSTRY STANDARDS

- 6.2 SUSTAINABILITY INITIATIVES

- 6.2.1 CARBON IMPACT AND ECO-APPLICATIONS OF ULTRA-HIGH PURITY GRAPHITE

- 6.2.1.1 Carbon impact reduction

- 6.2.1.2 Eco-applications

- 6.2.1 CARBON IMPACT AND ECO-APPLICATIONS OF ULTRA-HIGH PURITY GRAPHITE

- 6.3 SUSTAINABILITY IMPACT AND REGULATORY POLICY INITIATIVES

- 6.4 CERTIFICATIONS, LABELING, AND ECO-STANDARDS

7 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 7.1 DECISION-MAKING PROCESS

- 7.2 KEY STAKEHOLDERS AND BUYING CRITERIA

- 7.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 7.2.2 BUYING CRITERIA

- 7.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 7.4 UNMET NEEDS IN VARIOUS END-USE INDUSTRIES

- 7.5 MARKET PROFITIBILITY

- 7.5.1 REVENUE POTENTIAL

- 7.5.2 COST DYNAMICS

- 7.5.3 MARGIN OPPORTUNITIES IN KEY APPLICATIONS

8 TYPES OF ULTRA-HIGH PURITY GRAPHITE

- 8.1 INTRODUCTION

- 8.2 PYROLYTIC GRAPHITE

- 8.2.1 RISING USE OF PYROLYTIC GRAPHITE IN HIGH-TEMPERATURE AND ADVANCED INDUSTRIAL APPLICATIONS TO DRIVE DEMAND

- 8.3 SYNTHETIC ISOTROPIC GRAPHITE

- 8.3.1 INCREASING USE IN ENERGY STORAGE & ELECTRONICS TO DRIVE MARKET GROWTH

- 8.4 PURIFIED NATURAL VEIN GRAPHITE

- 8.4.1 INCREASING ADOPTION IN BATTERY AND ENERGY STORAGE APPLICATIONS TO FUEL DEMAND

- 8.5 HIGH-PURITY SYNTHETIC GRAPHITE POWDER

- 8.5.1 RISING APPLICATIONS IN ENERGY STORAGE, ELECTRONICS, AND HIGH-TEMPERATURE SYSTEMS DRIVING DEMAND

- 8.6 OTHERS

9 END-USE INDUSTRIES OF ULTRA-HIGH PURITY GRAPHITE

- 9.1 INTRODUCTION

- 9.2 NUCLEAR POWER

- 9.2.1 EXPANSION OF ADVANCED NUCLEAR TECHNOLOGIES ACCELERATING DEMAND FOR ULTRA-HIGH PURITY GRAPHITE

- 9.3 AEROSPACE & DEFENSE

- 9.3.1 NEED FOR SUPERIOR THERMAL AND STRUCTURAL PERFORMANCE DRIVING ADOPTION

- 9.4 ELECTRONICS

- 9.4.1 EXCEPTIONAL ELECTRICAL AND THERMAL CONDUCTIVITY FUELING DEMAND IN ADVANCED ELECTRONICS APPLICATIONS

- 9.5 ENERGY STORAGE

- 9.5.1 SUPERIOR STRENGTH AND ENERGY EFFICIENCY DRIVING GROWTH IN ENERGY STORAGE TECHNOLOGIES

- 9.6 METALLURGY

- 9.6.1 NEED FOR EXCEPTIONAL THERMAL STABILITY AND CHEMICAL PURITY TO SUPPORT MARKET GROWTH

- 9.7 SOLAR POWER

- 9.7.1 EXCEPTIONAL THERMAL STABILITY AND CHEMICAL PURITY FUELING ADOPTION IN SOLAR INDUSTRY

- 9.8 OTHERS END-USE INDUSTRIES

- 9.8.1 MEDICAL

- 9.8.2 RESEARCH

10 ULTRA-HIGH PURITY GRAPHITE MARKET, BY SOURCE

- 10.1 INTRODUCTION

- 10.2 SYNTHETIC GRAPHITE

- 10.2.1 DEMAND IN ENERGY STORAGE, SEMICONDUCTOR FABRICATION, AND OTHER HIGH-PRECISION APPLICATIONS TO DRIVE MARKET

- 10.3 NATURAL GRAPHITE

- 10.3.1 SUPERIOR CONDUCTIVITY AND HIGH-TEMPERATURE STABILITY DRIVING GROWTH

11 ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION

- 11.1 INTRODUCTION

- 11.2 NUCLEAR REACTORS

- 11.2.1 HIGH HEAT CONDUCTIVITY AND STRONG RADIATION RESISTANCE TO BOOST ADOPTION IN NUCLEAR REACTORS

- 11.3 LITHIUM-ION BATTERY ANODES

- 11.3.1 HIGH ENERGY STORAGE EFFICIENCY AND STRUCTURAL STABILITY INCREASING ADOPTION IN LITHIUM-ION BATTERIES

- 11.4 SEMICONDUCTORS

- 11.4.1 SUPERIOR PURITY AND PRECISION OF ULTRA-HIGH PURITY GRAPHITE TO DRIVE DEMAND IN SEMICONDUCTOR MANUFACTURING

- 11.5 OTHER APPLICATIONS

- 11.5.1 ELECTRIC ARC FURNACE ELECTRODES

- 11.5.2 THERMAL MANAGEMENT SYSTEMS

- 11.5.3 LUBRICANTS

- 11.5.4 CONDUCTIVE COATINGS

12 ULTRA-HIGH PURITY GRAPHITE MARKET, BY REGION

- 12.1 INTRODUCTION

- 12.2 ASIA PACIFIC

- 12.2.1 CHINA

- 12.2.1.1 Advancements in nuclear, semiconductor, and lithium-ion technologies fueling growth

- 12.2.2 INDIA

- 12.2.2.1 Favorable government initiatives driving market growth

- 12.2.3 JAPAN

- 12.2.3.1 Expansion of semiconductor sector and revival of nuclear power supporting market growth

- 12.2.4 AUSTRALIA

- 12.2.4.1 Nuclear policy advancement to drive market growth

- 12.2.5 REST OF ASIA PACIFIC

- 12.2.1 CHINA

- 12.3 NORTH AMERICA

- 12.3.1 US

- 12.3.1.1 Semiconductor growth and nuclear energy expansion driving demand

- 12.3.2 CANADA

- 12.3.2.1 Expansion of nuclear and lithium projects accelerating demand

- 12.3.3 MEXICO

- 12.3.3.1 Semiconductor sector expansion and supportive government policies fueling market growth

- 12.3.1 US

- 12.4 EUROPE

- 12.4.1 GERMANY

- 12.4.1.1 Semiconductor and battery manufacturing expansion driving market growth

- 12.4.2 FRANCE

- 12.4.2.1 Nuclear energy expansion and favorable government policies strengthening market growth

- 12.4.3 SPAIN

- 12.4.3.1 Expansion of semiconductor sector supporting market growth

- 12.4.4 UK

- 12.4.4.1 Nuclear innovation and domestic supply development driving market growth

- 12.4.5 ITALY

- 12.4.5.1 Revival of nuclear energy and semiconductor expansion supporting market growth

- 12.4.6 REST OF EUROPE

- 12.4.1 GERMANY

- 12.5 MIDDLE EAST & AFRICA

- 12.5.1 GCC COUNTRIES

- 12.5.1.1 UAE

- 12.5.1.1.1 Nuclear sector expansion and semiconductor initiatives to drive demand

- 12.5.1.2 Saudi Arabia

- 12.5.1.2.1 Expansion of semiconductor and lithium-ion battery sectors driving growth

- 12.5.1.3 Rest of GCC Countries

- 12.5.1.1 UAE

- 12.5.2 SOUTH AFRICA

- 12.5.2.1 Expansion of nuclear power sector to drive demand

- 12.5.3 REST OF MIDDLE EAST & AFRICA

- 12.5.1 GCC COUNTRIES

- 12.6 SOUTH AMERICA

- 12.6.1 BRAZIL

- 12.6.1.1 Nuclear expansion and semiconductor initiatives accelerating demand

- 12.6.2 ARGENTINA

- 12.6.2.1 Advancing nuclear innovation to drive demand during forecast period

- 12.6.3 REST OF SOUTH AMERICA

- 12.6.1 BRAZIL

13 COMPETITIVE LANDSCAPE

- 13.1 INTRODUCTION

- 13.2 KEY PLAYERS' STRATEGIES/RIGHT TO WIN

- 13.3 REVENUE ANALYSIS

- 13.4 MARKET SHARE ANALYSIS

- 13.4.1 RANKING OF KEY MARKET PLAYERS, 2024

- 13.4.2 MARKET SHARE OF KEY PLAYERS

- 13.5 BRAND/PRODUCT COMPARISON

- 13.5.1 MERSEN

- 13.5.2 TOYO TANSO CO., LTD.

- 13.5.3 SGL CARBON

- 13.5.4 GRAFTECH INTERNATIONAL

- 13.5.5 SUPERIOR GRAPHITE

- 13.6 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 13.6.1 STARS

- 13.6.2 EMERGING LEADERS

- 13.6.3 PERVASIVE PLAYERS

- 13.6.4 PARTICIPANTS

- 13.6.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 13.6.5.1 Company footprint

- 13.6.5.2 Region footprint

- 13.6.5.3 Type footprint

- 13.6.5.4 Application footprint

- 13.6.5.5 Source footprint

- 13.6.5.6 End-use industry

- 13.7 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 13.7.1 PROGRESSIVE COMPANIES

- 13.7.2 RESPONSIVE COMPANIES

- 13.7.3 DYNAMIC COMPANIES

- 13.7.4 STARTING BLOCKS

- 13.7.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 13.7.5.1 Detailed list of key startups/SMEs

- 13.7.5.2 Competitive benchmarking of key startups/SMEs

- 13.8 COMPETITIVE SCENARIO

- 13.8.1 DEALS

- 13.8.2 EXPANSIONS

- 13.9 COMPANY VALUATION AND FINANCIAL METRICS

14 COMPANY PROFILES

- 14.1 MAJOR PLAYERS

- 14.1.1 MERSEN

- 14.1.1.1 Business overview

- 14.1.1.2 Products/Solutions/Services offered

- 14.1.1.3 Recent developments

- 14.1.1.3.1 Deals

- 14.1.1.3.2 Expansions

- 14.1.1.4 MnM view

- 14.1.1.4.1 Right to win

- 14.1.1.4.2 Strategic choices

- 14.1.1.4.3 Weaknesses and competitive threats

- 14.1.2 TOYO TANSO CO., LTD.

- 14.1.2.1 Business overview

- 14.1.2.2 Products/Solutions/Services offered

- 14.1.2.3 MnM view

- 14.1.2.3.1 Right to win

- 14.1.2.3.2 Strategic choices

- 14.1.2.3.3 Weaknesses and competitive threats

- 14.1.3 SGL CARBON

- 14.1.3.1 Business overview

- 14.1.3.2 Products/Solutions/Services offered

- 14.1.3.3 MnM view

- 14.1.3.3.1 Right to win

- 14.1.3.3.2 Strategic choices

- 14.1.3.3.3 Weaknesses and competitive threats

- 14.1.4 ENTEGRIS

- 14.1.4.1 Business overview

- 14.1.4.2 Products/Solutions/Services offered

- 14.1.4.3 MnM view

- 14.1.4.3.1 Right to win

- 14.1.4.3.2 Strategic choices

- 14.1.4.3.3 Weaknesses and competitive threats

- 14.1.5 GRAFTECH INTERNATIONAL

- 14.1.5.1 Business overview

- 14.1.5.2 Products/Solutions/Services offered

- 14.1.5.3 MnM view

- 14.1.5.3.1 Right to win

- 14.1.5.3.2 Strategic choices

- 14.1.5.3.3 Weaknesses and competitive threats

- 14.1.6 CEYLON GRAPHITE CORP.

- 14.1.6.1 Business overview

- 14.1.6.2 Products/Solutions/Services offered

- 14.1.7 SUPERIOR GRAPHITE

- 14.1.7.1 Business overview

- 14.1.7.2 Products offered

- 14.1.7.3 Recent developments

- 14.1.7.3.1 Deals

- 14.1.7.3.2 Expansions

- 14.1.8 FOCUS GRAPHITE

- 14.1.8.1 Business overview

- 14.1.8.2 Products/Solutions/Services offered

- 14.1.9 SEC CARBON, LIMITED

- 14.1.9.1 Business overview

- 14.1.9.2 Products offered

- 14.1.10 ASBURY CARBONS

- 14.1.10.1 Business overview

- 14.1.10.2 Products/Solutions/Services offered

- 14.1.11 HPMS GRAPHITE

- 14.1.11.1 Business overview

- 14.1.11.2 Products/Solutions/Services offered

- 14.1.12 XRD GRAPHITE MANUFACTURING CO., LTD.

- 14.1.12.1 Business overview

- 14.1.12.2 Products/Solutions/Services offered

- 14.1.13 SARYTOGAN GRAPHITE LIMITED

- 14.1.13.1 Business overview

- 14.1.13.2 Products/Solutions/Services offered

- 14.1.14 AMSTED GRAPHITE MATERIALS

- 14.1.14.1 Business overview

- 14.1.14.2 Products/Solutions/Services offered

- 14.1.14.3 Recent developments

- 14.1.14.3.1 Deals

- 14.1.15 EAST CARBON

- 14.1.15.1 Business overview

- 14.1.15.2 Products/Solutions/Services offered

- 14.1.16 AMERICAN ELEMENTS

- 14.1.16.1 Business overview

- 14.1.16.2 Products/Solutions/Services offered

- 14.1.17 CANADA CARBON

- 14.1.17.1 Business overview

- 14.1.17.2 Products/Solutions/Services offered

- 14.1.18 ATLAS CRITICAL MINERALS

- 14.1.18.1 Business overview

- 14.1.18.2 Products/Solutions/Services offered

- 14.1.19 JINSUN NEW MATERIAL TECHNOLOGY, LTD.

- 14.1.19.1 Business overview

- 14.1.19.2 Products/Solutions/Services offered

- 14.1.1 MERSEN

- 14.2 OTHER PLAYERS

- 14.2.1 NINGBO RUIYI SEALING MATERIAL CO., LTD.

- 14.2.2 XURAN NEW MATERIALS LIMITED

- 14.2.3 CANGZHOU CARBON TECHNOLOGY CO., LTD.

- 14.2.4 CARBONIUM CORE

15 RESEARCH METHODOLOGY

- 15.1 RESEARCH DATA

- 15.1.1 SECONDARY DATA

- 15.1.1.1 Key data from secondary sources

- 15.1.2 PRIMARY DATA

- 15.1.2.1 Key data from primary sources

- 15.1.2.2 Breakdown of interviews with experts

- 15.1.1 SECONDARY DATA

- 15.2 DEMAND-SIDE ANALYSIS

- 15.3 MARKET SIZE ESTIMATION

- 15.3.1 BOTTOM-UP APPROACH

- 15.3.2 TOP-DOWN APPROACH

- 15.4 CALCULATION FOR SUPPLY-SIDE ANALYSIS

- 15.5 GROWTH FORECAST

- 15.6 DATA TRIANGULATION

- 15.7 RESEARCH ASSUMPTIONS

- 15.8 RESEARCH LIMITATIONS

- 15.9 RISK ASSESSMENT

16 APPENDIX

- 16.1 DISCUSSION GUIDE

- 16.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 16.3 CUSTOMIZATION OPTIONS

- 16.4 RELATED REPORTS

- 16.5 AUTHOR DETAILS

List of Tables

- TABLE 1 ULTRA-HIGH PURITY GRAPHITE MARKET: PORTER'S FIVE FORCES ANALYSIS

- TABLE 2 GDP PERCENTAGE CHANGE, BY KEY COUNTRIES, 2021-2029

- TABLE 3 ULTRA-HIGH PURITY GRAPHITE MARKET: ROLE OF COMPANIES IN ECOSYSTEM

- TABLE 4 AVERAGE SELLING PRICE OF ULTRA-HIGH PURITY GRAPHITE IN TOP APPLICATIONS, BY KEY PLAYERS, 2024 (USD/TON)

- TABLE 5 AVERAGE SELLING PRICE TREND OF ULTRA-HIGH PURITY GRAPHITE, BY REGION, 2022-2024 (USD/TON)

- TABLE 6 IMPORT DATA FOR HS CODE 380110-COMPLIANT PRODUCTS, 2020-2024 (USD THOUSAND)

- TABLE 7 EXPORT DATA FOR HS CODE 380110-COMPLIANT PRODUCTS, 2020-2024 (USD THOUSAND)

- TABLE 8 ULTRA-HIGH PURITY GRAPHITE MARKET: LIST OF KEY CONFERENCES AND EVENTS, 2025-2026

- TABLE 9 US-ADJUSTED RECIPROCAL TARIFF RATES

- TABLE 10 ULTRA-HIGH PURITY GRAPHITE MARKET: TOTAL NUMBER OF PATENTS, 2014-2024

- TABLE 11 TOP USE CASES AND MARKET POTENTIAL

- TABLE 12 BEST PRACTICES: COMPANIES IMPLEMENTING USE CASES

- TABLE 13 ULTRA-HIGH PURITY GRAPHITE MARKET: CASE STUDIES RELATED TO GEN AI IMPLEMENTATION

- TABLE 14 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- TABLE 15 NORTH AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 16 EUROPE: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 17 ASIA PACIFIC: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 18 ROW: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 19 GLOBAL STANDARDS IN ULTRA-HIGH PURITY GRAPHITE MARKET

- TABLE 20 CERTIFICATIONS, LABELING, AND ECO-STANDARDS IN ULTRA-HIGH PURITY GRAPHITE MARKET

- TABLE 21 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS, BY END-USE INDUSTRY (%)

- TABLE 22 KEY BUYING CRITERIA, BY END-USE INDUSTRY

- TABLE 23 ULTRA-HIGH PURITY GRAPHITE MARKET: UNMET NEEDS IN KEY END-USE INDUSTRIES

- TABLE 24 ULTRA-HIGH PURITY GRAPHITE MARKET, BY SOURCE, 2022-2024 (KILOTON)

- TABLE 25 ULTRA-HIGH PURITY GRAPHITE MARKET, BY SOURCE, 2025-2030 (KILOTON)

- TABLE 26 ULTRA-HIGH PURITY SYNTHETIC GRAPHITE MARKET, BY REGION, 2022-2024 (KILOTON)

- TABLE 27 ULTRA-HIGH PURITY SYNTHETIC GRAPHITE MARKET, BY REGION, 2025-2030 (KILOTON)

- TABLE 28 ULTRA-HIGH PURITY NATURAL GRAPHITE MARKET, BY REGION, 2022-2024 (KILOTON)

- TABLE 29 ULTRA-HIGH PURITY NATURAL GRAPHITE MARKET, BY REGION, 2025-2030 (KILOTON)

- TABLE 30 ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 31 ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 32 ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2022-2024 (KILOTON)

- TABLE 33 ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2025-2030 (KILOTON)

- TABLE 34 ULTRA-HIGH PURITY GRAPHITE MARKET IN NUCLEAR REACTORS, BY REGION, 2022-2024 (USD MILLION)

- TABLE 35 ULTRA-HIGH PURITY GRAPHITE MARKET IN NUCLEAR REACTORS, BY REGION, 2025-2030 (USD MILLION)

- TABLE 36 ULTRA-HIGH PURITY GRAPHITE MARKET IN NUCLEAR REACTORS, BY REGION, 2022-2024 (KILOTON)

- TABLE 37 ULTRA-HIGH PURITY GRAPHITE MARKET IN NUCLEAR REACTORS, BY REGION, 2025-2030 (KILOTON)

- TABLE 38 ULTRA-HIGH PURITY GRAPHITE MARKET IN LITHIUM-ION BATTERY ANODES, BY REGION, 2022-2024 (USD MILLION)

- TABLE 39 ULTRA-HIGH PURITY GRAPHITE MARKET IN LITHIUM-ION BATTERY ANODES, BY REGION, 2025-2030 (USD MILLION)

- TABLE 40 ULTRA-HIGH PURITY GRAPHITE MARKET IN LITHIUM-ION BATTERY ANODES, BY REGION, 2022-2024 (KILOTON)

- TABLE 41 ULTRA-HIGH PURITY GRAPHITE MARKET IN LITHIUM-ION BATTERY ANODES, BY REGION, 2025-2030 (KILOTON)

- TABLE 42 ULTRA-HIGH PURITY GRAPHITE MARKET IN SEMICONDUCTORS, BY REGION, 2022-2024 (USD MILLION)

- TABLE 43 ULTRA-HIGH PURITY GRAPHITE MARKET IN SEMICONDUCTORS, BY REGION, 2025-2030 (USD MILLION)

- TABLE 44 ULTRA-HIGH PURITY GRAPHITE MARKET IN SEMICONDUCTORS, BY REGION, 2022-2024 (KILOTON)

- TABLE 45 ULTRA-HIGH PURITY GRAPHITE MARKET IN SEMICONDUCTORS, BY REGION, 2025-2030 (KILOTON)

- TABLE 46 ULTRA-HIGH PURITY GRAPHITE MARKET IN OTHER APPLICATIONS, BY REGION, 2022-2024 (USD MILLION)

- TABLE 47 ULTRA-HIGH PURITY GRAPHITE MARKET IN OTHER APPLICATIONS, BY REGION, 2025-2030 (USD MILLION)

- TABLE 48 ULTRA-HIGH PURITY GRAPHITE MARKET IN OTHER APPLICATIONS, BY REGION, 2022-2024 (KILOTON)

- TABLE 49 ULTRA-HIGH PURITY GRAPHITE MARKET IN OTHER APPLICATIONS, BY REGION, 2025-2030 (KILOTON)

- TABLE 50 ULTRA-HIGH PURITY GRAPHITE MARKET, BY REGION, 2022-2024 (USD MILLION)

- TABLE 51 ULTRA-HIGH PURITY GRAPHITE MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 52 ULTRA-HIGH PURITY GRAPHITE MARKET, BY REGION, 2022-2024 (KILOTON)

- TABLE 53 ULTRA-HIGH PURITY GRAPHITE MARKET, BY REGION, 2025-2030 (KILOTON)

- TABLE 54 ASIA PACIFIC: ULTRA-HIGH PURITY GRAPHITE MARKET, BY COUNTRY, 2022-2024 (USD MILLION)

- TABLE 55 ASIA PACIFIC: ULTRA-HIGH PURITY GRAPHITE MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 56 ASIA PACIFIC: ULTRA-HIGH PURITY GRAPHITE MARKET, BY COUNTRY, 2022-2024 (KILOTON)

- TABLE 57 ASIA PACIFIC: ULTRA-HIGH PURITY GRAPHITE MARKET, BY COUNTRY, 2025-2030 (KILOTON)

- TABLE 58 ASIA PACIFIC: ULTRA-HIGH PURITY GRAPHITE MARKET, BY SOURCE, 2022-2024 (KILOTON)

- TABLE 59 ASIA PACIFIC: ULTRA-HIGH PURITY GRAPHITE MARKET, BY SOURCE, 2025-2030 (KILOTON)

- TABLE 60 ASIA PACIFIC: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 61 ASIA PACIFIC: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 62 ASIA PACIFIC: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2022-2024 (KILOTON)

- TABLE 63 ASIA PACIFIC: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2025-2030 (KILOTON)

- TABLE 64 CHINA: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 65 CHINA: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 66 CHINA: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2022-2024 (KILOTON)

- TABLE 67 CHINA: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2025-2030 (KILOTON)

- TABLE 68 INDIA: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 69 INDIA: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 70 INDIA: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2022-2024 (KILOTON)

- TABLE 71 INDIA: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2025-2030 (KILOTON)

- TABLE 72 JAPAN: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 73 JAPAN: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 74 JAPAN: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2022-2024 (KILOTON)

- TABLE 75 JAPAN: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2025-2030 (KILOTON)

- TABLE 76 AUSTRALIA: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 77 AUSTRALIA: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 78 AUSTRALIA: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2022-2024 (KILOTON)

- TABLE 79 AUSTRALIA: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2025-2030 (KILOTON)

- TABLE 80 REST OF ASIA PACIFIC: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 81 REST OF ASIA PACIFIC: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 82 REST OF ASIA PACIFIC: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2022-2024 (KILOTON)

- TABLE 83 REST OF ASIA PACIFIC: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2025-2030 (KILOTON)

- TABLE 84 NORTH AMERICA: ULTRA-HIGH PURITY GRAPHITE MARKET, BY COUNTRY, 2022-2024 (USD MILLION)

- TABLE 85 NORTH AMERICA: ULTRA-HIGH PURITY GRAPHITE MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 86 NORTH AMERICA: ULTRA-HIGH PURITY GRAPHITE MARKET, BY COUNTRY, 2022-2024 (KILOTON)

- TABLE 87 NORTH AMERICA: ULTRA-HIGH PURITY GRAPHITE MARKET, BY COUNTRY, 2025-2030 (KILOTON)

- TABLE 88 NORTH AMERICA: ULTRA-HIGH PURITY GRAPHITE MARKET, BY SOURCE, 2022-2024 (KILOTON)

- TABLE 89 NORTH AMERICA: ULTRA-HIGH PURITY GRAPHITE MARKET, BY SOURCE, 2025-2030 (KILOTON)

- TABLE 90 NORTH AMERICA: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 91 NORTH AMERICA: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 92 NORTH AMERICA: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2022-2024 (KILOTON)

- TABLE 93 NORTH AMERICA: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2025-2030 (KILOTON)

- TABLE 94 US: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 95 US: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 96 US: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2022-2024 (KILOTON)

- TABLE 97 US: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2025-2030 (KILOTON)

- TABLE 98 CANADA: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 99 CANADA: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 100 CANADA: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2022-2024 (KILOTON)

- TABLE 101 CANADA: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2025-2030 (KILOTON)

- TABLE 102 MEXICO: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 103 MEXICO: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 104 MEXICO: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2022-2024 (KILOTON)

- TABLE 105 MEXICO: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2025-2030 (KILOTON)

- TABLE 106 EUROPE: ULTRA-HIGH PURITY GRAPHITE MARKET, BY COUNTRY, 2022-2024 (USD MILLION)

- TABLE 107 EUROPE: ULTRA-HIGH PURITY GRAPHITE MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 108 EUROPE: ULTRA-HIGH PURITY GRAPHITE MARKET, BY COUNTRY, 2022-2024 (KILOTON)

- TABLE 109 EUROPE: ULTRA-HIGH PURITY GRAPHITE MARKET, BY COUNTRY, 2025-2030 (KILOTON)

- TABLE 110 EUROPE: ULTRA-HIGH PURITY GRAPHITE MARKET, BY SOURCE, 2022-2024 (KILOTON)

- TABLE 111 EUROPE: ULTRA-HIGH PURITY GRAPHITE MARKET, BY SOURCE, 2025-2030 (KILOTON)

- TABLE 112 EUROPE: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 113 EUROPE: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 114 EUROPE: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2022-2024 (KILOTON)

- TABLE 115 EUROPE: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2025-2030 (KILOTON)

- TABLE 116 GERMANY: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 117 GERMANY: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 118 GERMANY: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2022-2024 (KILOTON)

- TABLE 119 GERMANY: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2025-2030 (KILOTON)

- TABLE 120 FRANCE: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 121 FRANCE: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 122 FRANCE: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2022-2024 (KILOTON)

- TABLE 123 FRANCE: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2025-2030 (KILOTON)

- TABLE 124 SPAIN: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 125 SPAIN: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 126 SPAIN: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2022-2024 (KILOTON)

- TABLE 127 SPAIN: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2025-2030 (KILOTON)

- TABLE 128 UK: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 129 UK: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 130 UK: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2022-2024 (KILOTON)

- TABLE 131 UK: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2025-2030 (KILOTON)

- TABLE 132 ITALY: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 133 ITALY: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 134 ITALY: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2022-2024 (KILOTON)

- TABLE 135 ITALY: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2025-2030 (KILOTON)

- TABLE 136 REST OF EUROPE: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 137 REST OF EUROPE: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 138 REST OF EUROPE: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2022-2024 (KILOTON)

- TABLE 139 REST OF EUROPE: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2025-2030 (KILOTON)

- TABLE 140 MIDDLE EAST & AFRICA: ULTRA-HIGH PURITY GRAPHITE MARKET, BY COUNTRY, 2022-2024 (USD MILLION)

- TABLE 141 MIDDLE EAST & AFRICA: ULTRA-HIGH PURITY GRAPHITE MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 142 MIDDLE EAST & AFRICA: ULTRA-HIGH PURITY GRAPHITE MARKET, BY COUNTRY, 2022-2024 (KILOTON)

- TABLE 143 MIDDLE EAST & AFRICA: ULTRA-HIGH PURITY GRAPHITE MARKET, BY COUNTRY, 2025-2030 (KILOTON)

- TABLE 144 MIDDLE EAST & AFRICA: ULTRA-HIGH PURITY GRAPHITE MARKET, BY SOURCE, 2022-2024 (KILOTON)

- TABLE 145 MIDDLE EAST & AFRICA: ULTRA-HIGH PURITY GRAPHITE MARKET, BY SOURCE, 2025-2030 (KILOTON)

- TABLE 146 MIDDLE EAST & AFRICA: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 147 MIDDLE EAST & AFRICA: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 148 MIDDLE EAST & AFRICA: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2022-2024 (KILOTON)

- TABLE 149 MIDDLE EAST & AFRICA: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2025-2030 (KILOTON)

- TABLE 150 UAE: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 151 UAE: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 152 UAE: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2022-2024 (KILOTON)

- TABLE 153 UAE: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2025-2030 (KILOTON)

- TABLE 154 SAUDI ARABIA: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 155 SAUDI ARABIA: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 156 SAUDI ARABIA: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2022-2024 (KILOTON)

- TABLE 157 SAUDI ARABIA: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2025-2030 (KILOTON)

- TABLE 158 REST OF GCC: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 159 REST OF GCC: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 160 REST OF GCC: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2022-2024 (KILOTON)

- TABLE 161 REST OF GCC: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2025-2030 (KILOTON)

- TABLE 162 SOUTH AFRICA: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 163 SOUTH AFRICA: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 164 SOUTH AFRICA: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2022-2024 (KILOTON)

- TABLE 165 SOUTH AFRICA: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2025-2030 (KILOTON)

- TABLE 166 REST OF MIDDLE EAST & AFRICA: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 167 REST OF MIDDLE EAST & AFRICA: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 168 REST OF MIDDLE EAST & AFRICA: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2022-2024 (KILOTON)

- TABLE 169 REST OF MIDDLE EAST & AFRICA: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2025-2030 (KILOTON)

- TABLE 170 SOUTH AMERICA: ULTRA-HIGH PURITY GRAPHITE MARKET, BY COUNTRY, 2022-2024 (USD MILLION)

- TABLE 171 SOUTH AMERICA: ULTRA-HIGH PURITY GRAPHITE MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 172 SOUTH AMERICA: ULTRA-HIGH PURITY GRAPHITE MARKET, BY COUNTRY, 2022-2024 (KILOTON)

- TABLE 173 SOUTH AMERICA: ULTRA-HIGH PURITY GRAPHITE MARKET, BY COUNTRY, 2025-2030 (KILOTON)

- TABLE 174 SOUTH AMERICA: ULTRA-HIGH PURITY GRAPHITE MARKET, BY SOURCE, 2022-2024 (KILOTON)

- TABLE 175 SOUTH AMERICA: ULTRA-HIGH PURITY GRAPHITE MARKET, BY SOURCE, 2025-2030 (KILOTON)

- TABLE 176 SOUTH AMERICA: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 177 SOUTH AMERICA: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 178 SOUTH AMERICA: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2022-2024 (KILOTON)

- TABLE 179 SOUTH AMERICA: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2025-2030 (KILOTON)

- TABLE 180 BRAZIL: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 181 BRAZIL: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 182 BRAZIL: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2022-2024 (KILOTON)

- TABLE 183 BRAZIL: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2025-2030 (KILOTON)

- TABLE 184 ARGENTINA: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 185 ARGENTINA: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 186 ARGENTINA: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2022-2024 (KILOTON)

- TABLE 187 ARGENTINA: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2025-2030 (KILOTON)

- TABLE 188 REST OF SOUTH AMERICA: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2022-2024 (USD MILLION)

- TABLE 189 REST OF SOUTH AMERICA: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 190 REST OF SOUTH AMERICA: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2022-2024 (KILOTON)

- TABLE 191 REST OF SOUTH AMERICA: ULTRA-HIGH PURITY GRAPHITE MARKET, BY APPLICATION, 2025-2030 (KILOTON)

- TABLE 192 ULTRA-HIGH PURITY GRAPHITE MARKET: OVERVIEW OF STRATEGIES ADOPTED BY KEY PLAYERS, 2020-2025

- TABLE 193 ULTRA-HIGH PURITY GRAPHITE MARKET: DEGREE OF COMPETITION, 2024

- TABLE 194 ULTRA-HIGH PURITY GRAPHITE MARKET: REGION FOOTPRINT

- TABLE 195 ULTRA-HIGH PURITY GRAPHITE MARKET: TYPE FOOTPRINT

- TABLE 196 ULTRA-HIGH PURITY GRAPHITE MARKET: APPLICATION FOOTPRINT

- TABLE 197 ULTRA-HIGH PURITY GRAPHITE MARKET: SOURCE FOOTPRINT

- TABLE 198 ULTRA-HIGH PURITY GRAPHITE MARKET: END-USE INDUSTRY FOOTPRINT

- TABLE 199 ULTRA-HIGH PURITY GRAPHITE MARKET: DETAILED LIST OF KEY STARTUPS/SMES

- TABLE 200 ULTRA-HIGH PURITY GRAPHITE MARKET: COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES

- TABLE 201 ULTRA-HIGH PURITY GRAPHITE MARKET: DEALS, JANUARY 2020-NOVEMBER 2025

- TABLE 202 ULTRA-HIGH PURITY GRAPHITE MARKET: EXPANSIONS, JANUARY 2020-NOVEMBER 2025

- TABLE 203 MERSEN: COMPANY OVERVIEW

- TABLE 204 MERSEN: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 205 MERSEN: DEALS

- TABLE 206 MERSEN: EXPANSIONS

- TABLE 207 TOYO TANSO CO., LTD.: COMPANY OVERVIEW

- TABLE 208 TOYO TANSO CO., LTD.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 209 SGL CARBON: COMPANY OVERVIEW

- TABLE 210 SGL CARBON: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 211 ENTEGRIS: COMPANY OVERVIEW

- TABLE 212 ENTEGRIS: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 213 GRAFTECH INTERNATIONAL: COMPANY OVERVIEW

- TABLE 214 GRAFTECH INTERNATIONAL: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 215 CEYLON GRAPHITE CORP.: COMPANY OVERVIEW

- TABLE 216 CEYLON GRAPHITE CORP.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 217 SUPERIOR GRAPHITE: COMPANY OVERVIEW

- TABLE 218 SUPERIOR GRAPHITE: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 219 SUPERIOR GRAPHITE: DEALS

- TABLE 220 SUPERIOR GRAPHITE: EXPANSIONS

- TABLE 221 FOCUS GRAPHITE: COMPANY OVERVIEW

- TABLE 222 FOCUS GRAPHITE: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 223 SEC CARBON, LIMITED: COMPANY OVERVIEW

- TABLE 224 SEC CARBON, LIMITED.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 225 ASBURY CARBONS: COMPANY OVERVIEW

- TABLE 226 ASBURY CARBONS: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 227 HPMS GRAPHITE: COMPANY OVERVIEW

- TABLE 228 HPMS GRAPHITE: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 229 XRD GRAPHITE MANUFACTURING CO., LTD.: COMPANY OVERVIEW

- TABLE 230 XRD GRAPHITE MANUFACTURING CO., LTD.: PRODUCTS/SOLUTIONS/ SERVICES OFFERED

- TABLE 231 SARYTOGAN GRAPHITE LIMITED.: COMPANY OVERVIEW

- TABLE 232 SARYTOGAN GRAPHITE LIMITED: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 233 AMSTED GRAPHITE MATERIALS: COMPANY OVERVIEW

- TABLE 234 AMSTED GRAPHITE MATERIALS: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 235 AMSTED GRAPHITE MATERIALS: DEALS

- TABLE 236 EAST CARBON: COMPANY OVERVIEW

- TABLE 237 EAST CARBON: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 238 AMERICAN ELEMENTS: COMPANY OVERVIEW

- TABLE 239 AMERICAN ELEMENTS: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 240 CANADA CARBON: COMPANY OVERVIEW

- TABLE 241 CANADA CARBON: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 242 ATLAS CRITICAL MINERALS: COMPANY OVERVIEW

- TABLE 243 ATLAS CRITICAL MINERALS: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 244 JINSUN NEW MATERIAL TECHNOLOGY, LTD.: COMPANY OVERVIEW

- TABLE 245 JINSUN NEW MATERIAL TECHNOLOGY, LTD.: PRODUCTS/SOLUTIONS/ SERVICES OFFERED

- TABLE 246 NINGBO RUIYI SEALING MATERIAL CO., LTD.: COMPANY OVERVIEW

- TABLE 247 XURAN NEW MATERIALS LIMITED: COMPANY OVERVIEW

- TABLE 248 CANGZHOU CARBON TECHNOLOGY CO., LTD.: COMPANY OVERVIEW

- TABLE 249 CARBONIUM CORE: COMPANY OVERVIEW

List of Figures

- FIGURE 1 ULTRA-HIGH PURITY GRAPHITE MARKET SEGMENTATION AND REGIONAL SCOPE

- FIGURE 2 KEY INSIGHTS AND MARKET HIGHLIGHTS

- FIGURE 3 GLOBAL ULTRA-HIGH PURITY GRAPHITE MARKET, 2025-2030

- FIGURE 4 MAJOR STRATEGIES ADOPTED BY KEY PLAYERS IN ULTRA-HIGH PURITY GRAPHITE MARKET (2020-2025)

- FIGURE 5 DISRUPTIVE TRENDS IMPACTING GROWTH OF ULTRA-HIGH PURITY GRAPHITE MARKET

- FIGURE 6 HIGH-GROWTH SEGMENTS AND EMERGING FRONTIERS IN ULTRA-HIGH PURITY GRAPHITE MARKET, 2024

- FIGURE 7 NORTH AMERICA TO REGISTER FASTEST GROWTH DURING FORECAST PERIOD

- FIGURE 8 HIGH DEMAND IN LITHIUM-ION BATTERY ANODES TO CREATE LUCRATIVE OPPORTUNITIES FOR MARKET PLAYERS

- FIGURE 9 SYNTHETIC SEGMENT ACCOUNTED FOR DOMINANT MARKET SHARE IN 2024

- FIGURE 10 LITHIUM-ION BATTERY ANODES SEGMENT ACCOUNTED FOR LARGEST MARKET SHARE IN 2024

- FIGURE 11 CHINA TO REGISTER HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 12 ULTRA-HIGH PURITY GRAPHITE MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

- FIGURE 13 EV BATTERY DEMAND FROM 2021 TO 2023 (GWH)

- FIGURE 14 PROJECTED EV BATTERY DEMAND FROM 2024 TO 2030 (TWH)

- FIGURE 15 GLOBAL SEMICONDUCTOR MARKET SIZE, 2023 TO 2O26

- FIGURE 16 GLOBAL PV CUMULATIVE SUPPLY, 2022-2024 (TW)

- FIGURE 17 GLOBAL NUCLEAR POWER CAPACITY TREND, 2005 TO 2024

- FIGURE 18 ULTRA-HIGH PURITY GRAPHITE MARKET: PORTER'S FIVE FORCES ANALYSIS

- FIGURE 19 ULTRA-HIGH PURITY GRAPHITE MARKET: VALUE CHAIN ANALYSIS

- FIGURE 20 ULTRA-HIGH PURITY GRAPHITE MARKET: KEY PARTICIPANTS IN ECOSYSTEM

- FIGURE 21 ULTRA-HIGH PURITY GRAPHITE MARKET: ECOSYSTEM ANALYSIS

- FIGURE 22 AVERAGE SELLING PRICE, BY APPLICATION

- FIGURE 23 AVERAGE SELLING PRICE TREND, BY REGION, 2022-2024

- FIGURE 24 IMPORT SCENARIO FOR HS CODE 380110-COMPLIANT PRODUCTS, BY KEY COUNTRIES, 2020-2024

- FIGURE 25 EXPORT SCENARIO FOR HS CODE 380110-COMPLIANT PRODUCTS, BY KEY COUNTRIES, 2020-2024

- FIGURE 26 TRENDS/DISRUPTIONS INFLUENCING CUSTOMER BUSINESS

- FIGURE 27 ULTRA-HIGH PURITY GRAPHITE MARKET: INVESTMENT AND FUNDING SCENARIO, 2024

- FIGURE 28 PATENT ANALYSIS, BY DOCUMENT TYPE, 2014-2024

- FIGURE 29 PATENT PUBLICATION TRENDS, 2014 - 2024

- FIGURE 30 LEGAL STATUS OF PATENT, 2014-2024

- FIGURE 31 JURISDICTION OF CHINA REGISTERED HIGHEST SHARE OF PATENTS, 2014-2024

- FIGURE 32 TOP PATENT APPLICANTS, 2014-2024

- FIGURE 33 FUTURE APPLICATIONS OF ULTRA-HIGH PURITY GRAPHITE

- FIGURE 34 ULTRA-HIGH PURITY GRAPHITE MARKET: DECISION-MAKING FACTORS

- FIGURE 35 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS, BY END-USE INDUSTRY

- FIGURE 36 KEY BUYING CRITERIA, BY END-USE INDUSTRY

- FIGURE 37 ADOPTION BARRIERS & INTERNAL CHALLENGES

- FIGURE 38 SYNTHETIC SEGMENT TO DOMINATE ULTRA-HIGH PURITY GRAPHITE MARKET

- FIGURE 39 LITHIUM-ION BATTERY ANODES TO BE LARGEST APPLICATION OF ULTRA-HIGH PURITY GRAPHITE DURING FORECAST PERIOD

- FIGURE 40 ASIA PACIFIC TO ACCOUNT FOR LARGEST MARKET SHARE IN 2030

- FIGURE 41 ASIA PACIFIC: ULTRA-HIGH PURITY GRAPHITE MARKET SNAPSHOT

- FIGURE 42 NORTH AMERICA: ULTRA-HIGH PURITY GRAPHITE MARKET SNAPSHOT

- FIGURE 43 EUROPE: ULTRA-HIGH PURITY GRAPHITE MARKET SNAPSHOT

- FIGURE 44 ULTRA-HIGH PURITY GRAPHITE MARKET: REVENUE ANALYSIS OF KEY COMPANIES, 2020-2024

- FIGURE 45 RANKING OF KEY PLAYERS IN ULTRA-HIGH PURITY GRAPHITE MARKET

- FIGURE 46 ULTRA-HIGH PURITY GRAPHITE MARKET SHARE ANALYSIS, 2024

- FIGURE 47 ULTRA-HIGH PURITY GRAPHITE MARKET: BRAND/PRODUCT COMPARISON

- FIGURE 48 ULTRA-HIGH PURITY GRAPHITE MARKET: COMPANY EVALUATION MATRIX (KEY PLAYERS), 2024

- FIGURE 49 ULTRA-HIGH PURITY GRAPHITE MARKET: COMPANY FOOTPRINT

- FIGURE 50 ULTRA-HIGH PURITY GRAPHITE MARKET: COMPANY EVALUATION MATRIX (STARTUPS/SMES), 2024

- FIGURE 51 ULTRA-HIGH PURITY GRAPHITE MARKET: EV/EBITDA

- FIGURE 52 ULTRA-HIGH PURITY GRAPHITE MARKET: ENTERPRISE VALUE

- FIGURE 53 ULTRA-HIGH PURITY GRAPHITE MARKET: YEAR-TO-DATE (YTD) PRICE TOTAL RETURN AND FIVE-YEAR STOCK BETA OF KEY MANUFACTURERS

- FIGURE 54 MERSEN: COMPANY SNAPSHOT

- FIGURE 55 TOYO TANSO CO., LTD.: COMPANY SNAPSHOT

- FIGURE 56 SGL CARBON: COMPANY SNAPSHOT

- FIGURE 57 ENTEGRIS: COMPANY SNAPSHOT

- FIGURE 58 GRAFTECH INTERNATIONAL: COMPANY SNAPSHOT

- FIGURE 59 ULTRA-HIGH PURITY GRAPHITE MARKET: RESEARCH DESIGN

- FIGURE 60 DEMAND-SIDE ANALYSIS FOR ULTRA-HIGH PURITY GRAPHITE MARKET

- FIGURE 61 MARKET SIZE ESTIMATION METHODOLOGY: BOTTOM-UP APPROACH

- FIGURE 62 MARKET SIZE ESTIMATION METHODOLOGY: TOP-DOWN APPROACH

- FIGURE 63 METHODOLOGY FOR SUPPLY-SIDE SIZING OF ULTRA-HIGH PURITY GRAPHITE MARKET (1/2)

- FIGURE 64 METHODOLOGY FOR SUPPLY-SIDE SIZING OF ULTRA-HIGH PURITY GRAPHITE MARKET (2/2)

- FIGURE 65 ULTRA-HIGH PURITY GRAPHITE MARKET: DATA TRIANGULATION

石墨市场-全球产业规模、份额、趋势、机会和预测,按类型、应用、地区和竞争格局划分,2020-2030年预测

石墨市场-全球产业规模、份额、趋势、机会和预测,按类型、应用、地区和竞争格局划分,2020-2030年预测 人造石墨粉:全球市占率及排名、总收入及需求预测(2025-2031年)特种石墨:全球市占率及排名、总收入及需求预测(2025-2031年)等向性石墨:全球市场份额和排名、总销售额和需求预测(2025-2031 年)

人造石墨粉:全球市占率及排名、总收入及需求预测(2025-2031年)特种石墨:全球市占率及排名、总收入及需求预测(2025-2031年)等向性石墨:全球市场份额和排名、总销售额和需求预测(2025-2031 年) 按石墨类型、纯度等级、形态、应用和终端用户产业分類的绿色石墨市场—2025-2032年全球预测石墨市场:类型、纯度等级与形态-2025-2032 年全球预测

按石墨类型、纯度等级、形态、应用和终端用户产业分類的绿色石墨市场—2025-2032年全球预测石墨市场:类型、纯度等级与形态-2025-2032 年全球预测 2025年全球铺路砖市场报告

2025年全球铺路砖市场报告 2032 年银石墨市场预测:按类型、石墨结构、应用、最终用户和地区分類的全球分析

2032 年银石墨市场预测:按类型、石墨结构、应用、最终用户和地区分類的全球分析 石墨矿业市场规模、份额及成长分析(按采矿类型、品位及地区)-产业预测,2025-2032铺路砖市场-全球产业规模、份额、趋势、机会和预测,按产品类型、形状、应用、地区和竞争细分,2020-2030 年

石墨矿业市场规模、份额及成长分析(按采矿类型、品位及地区)-产业预测,2025-2032铺路砖市场-全球产业规模、份额、趋势、机会和预测,按产品类型、形状、应用、地区和竞争细分,2020-2030 年