|

市场调查报告书

商品编码

1936064

全球铝挤型市场依合金等级、产品、表面处理、最终用途产业及地区划分-预测至2030年Aluminum Extrusion Market by Product, Alloy Grade, Surface Finish, End-use Industry, and Region - Global Forecast to 2030 |

||||||

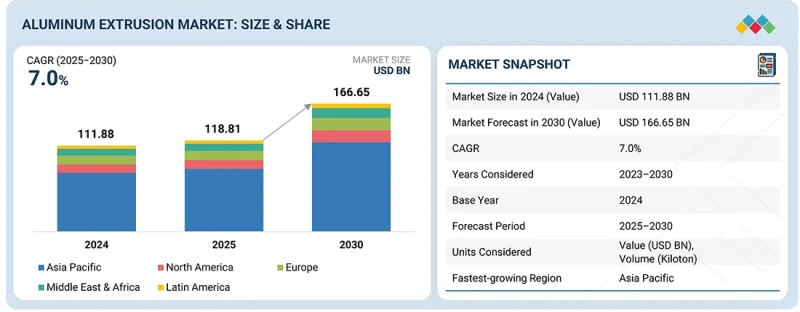

预计到 2024 年,铝挤型市场价值将达到 1,118.8 亿美元,预计到 2030 年将达到 1,666.5 亿美元,2025 年至 2030 年的复合年增长率为 7.0%。

| 调查范围 | |

|---|---|

| 调查期 | 2023-2030 |

| 基准年 | 2024 |

| 预测期 | 2025-2030 |

| 目标单元 | 价值(百万美元/十亿美元),数量(千吨) |

| 部分 | 按合金等级、产品、表面处理、最终用途行业和地区划分 |

| 目标区域 | 欧洲、北美、亚太地区、拉丁美洲、中东和非洲 |

实心型材因其易于製造和结构强度高,在铝挤型市场中占据主导地位。实心型材包括棒材、条材、扁条、角材(L形)、槽材(U形或C形)和樑等形状,其强度源自于高材料密度且内部无孔隙。它们使用简单的实心晶粒挤压而成,因此与半空心和空心型材等更复杂的形状相比,生产速度更快、成本更低。

6xxx系列铝合金凭藉其优异的挤压性能、中高强度、耐腐蚀性和热处理性能,在铝挤型市场中占据主导地位。这些合金主要与镁(Mg)和硅(Si)合金化形成硅化镁,从而能够加工出挤压所需的复杂形状和薄壁型材。

6xxx系列合金在挤压成形性方面表现出色,与4xxx或5xxx系列焊丝焊接性能良好,且表面光洁度优异,适用于阳极氧化和喷漆。在常见的T5和T6等热处理条件下,透过在160-182 ℃(350-382℉)下沉淀硬化,可以提高强度。它们兼具良好的抗拉强度(18-58 ksi)和延展性,但如果控制不当,则容易开裂。

预计在预测期内,毛坯挤出件将占据市场主导地位,并实现最高的复合年增长率。毛坯挤出件因其省去了表面处理工程,降低了生产成本,尤其在原物料价格上涨和通膨压力加剧的情况下,对大规模生产极具吸引力。此细分市场的前置作业时间短,能够快速满足下游製程中需要客製化精加工的工业用户的需求。

预计在预测期内,建筑和基础设施产业的复合年增长率将达到6.9%,成为成长最快的产业。建设产业也是铝挤型产品的主要终端使用者之一。铝材因其轻质高强、永续性、可回收利用和用途广泛等诸多优点,被认为是最实用的建筑材料之一。铝材在建筑业得到广泛应用,因为它有助于建筑计划获得LEED(能源与环境设计先锋奖)绿色建筑认证。

亚太地区在全球铝挤型市场占有主导地位。这一主导地位归功于快速的工业化、都市化以及关键产业需求的激增。中国、印度、日本和韩国等国的强劲经济成长推动了计划和高层建筑的建设,而这些项目和建筑由于挤压铝材的轻质、高强度和耐腐蚀性,需要大量使用挤压铝材。

中国是全球最大的汽车市场,在日益严格的排放气体法规下,该地区的汽车产业正优先考虑使用轻质材料来製造节能汽车。铝的导电性和多功能性也进一步推动了其在电子、机械和可再生能源(例如太阳能板框架)领域的应用。

该报告对公司概况进行了全面分析:

主要企业包括:金达尔铝业有限公司(印度)、印度铝业有限公司(印度)、美国铝业公司(美国)、中国铝业股份有限公司(中国)、俄罗斯铝业公司(俄罗斯)、世纪铝业公司(美国)、挪威海德鲁公司(挪威) 、康斯坦铝业(法国)、凯撒铝业(美国)、哈默勒铝业(奥地利)、班科铝业私人有限公司(印度)、曼铝有限公司(印度)、深圳东方图尔多铁器有限公司(中国)、ETEM(希腊)和阿洛姆集团(印度)。

调查范围

本研究报告按产品、合金等级、表面处理、终端应用产业和地区对铝挤压市场进行细分。报告涵盖影响铝挤压市场成长的关键因素的详细资讯,包括驱动因素、限制因素、挑战和机会。该报告对主要行业参与者进行了深入研究,提供了对其业务概况、解决方案和服务、关键策略、合约、合作关係和协议的洞察。报告还涵盖了新产品和服务的发布、併购以及铝挤型市场的最新发展。此外,报告还对铝挤型市场生态系统中新兴的Start-Ups进行了竞争分析。

购买本报告的益处:

本报告提供铝挤型市场及其细分市场最准确的收入估计值,旨在帮助市场领导和新参与企业。报告可协助相关人员了解竞争格局,并提供有助于他们优化业务定位和製定合适打入市场策略的洞察。此外,报告还概述了市场趋势,并提供有关关键市场驱动因素、限制、挑战和机会的资讯。

本报告深入分析了以下内容:

- 影响铝挤型市场成长的关键驱动因素(汽车产业需求成长、跨产业采用)、限制因素(资本密集、高能耗)、机会(先进製造技术、对优质合金和服务的未满足需求)和挑战(原材料成本波动、能源消耗和永续性)。

- 产品开发/创新:深入分析铝挤型市场即将出现的技术趋势、研发活动以及新产品和服务发布。

- 市场发展:关于盈利市场的全面资讯-该报告分析了各个地区的铝挤型市场。

- 市场多元化:全面介绍铝挤型市场的新产品和服务、前沿地区、最新趋势和投资情况。

- 竞争格局分析:主要企业- 对铝挤型市场主要参与者的市场份额、成长策略和服务产品进行详细评估,包括 Jindal Aluminum Limited(印度)、Hindalco Industries Ltd.(印度)、Alcoa Corporation(美国)、中国铝业股份有限公司(中国)、RUSAL(俄罗斯)、Century Aluminum Company(美国)、NorsS Hydium(中国)、法国) Hydroium(美国)、挪威) Aluminum(美国)、Hammerer Aluminum Industries(奥地利)、Banco Aluminum 主要企业 Limited(印度)、Maan Aluminum Limited(印度)、深圳东方图尔多铁器有限公司(中国)、ETEM(希腊)和 Alom Group(印度)。

目录

第一章 引言

第二章执行摘要

第三章重要考察

第四章 市场概览

- 市场动态

- 未满足的需求和差距

- 相互关联的市场与跨产业机会

- 新的经营模式和生态系统变化

- 一级/二级/三级公司的策略性倡议

第五章 产业趋势

- 波特五力分析

- 总体经济指标

- 价值链分析

- 生态系分析

- 定价分析

- 贸易分析

- 2026年重大会议和活动

- 影响客户业务的趋势/干扰因素

- 案例研究分析

- 2025年美国关税对铝挤型市场的影响

第六章:科技、专利、数位化和人工智慧应用带来的策略颠覆

- 关键新兴技术

- 互补技术

- 技术/产品蓝图

- 分析

- 未来应用

- 人工智慧/生成式人工智慧对铝挤型市场的影响

- 成功案例和实际应用

第七章永续性和监管环境

- 地方法规和合规性

- 对永续性的承诺

- 永续性影响和监管政策倡议

- 认证、标籤和环境标准

第八章:顾客状况与购买行为

- 决策流程

- 主要相关人员和采购标准

- 招募障碍和内部挑战

- 各个终端用户产业中尚未满足的需求

- 市场盈利

9. 铝挤型市场(依合金等级划分)

- 6XXX

- 1XXX

- 5XXX

- 其他的

第十章 铝挤型市场(依产品分类)

- 实心型材

- 半空心型材

- 中空型材

第十一章 铝挤型市场(依表面处理分类)

- 轧製表面

- 阳极处理

- 粉末涂装

第十二章 铝挤型市场(依终端用户产业划分)

- 建筑和基础设施

- 汽车和公共交通

- 电机与电子工程

- 机械和设备

- 其他的

第十三章 铝挤型市场(依地区划分)

- 北美洲

- 欧洲

- 亚太地区

- 中东和非洲

- 拉丁美洲

第十四章 竞争格局

- 概述

- 主要参与企业的策略/优势

- 收入分析

- 市占率分析

- 品牌/产品对比

- 公司估值矩阵:主要参与企业,2024 年

- 公司估值矩阵:Start-Ups/中小企业,2024 年

- 估值和财务指标

- 竞争场景

第十五章 公司简介

- 主要参与企业

- HINDALCO INDUSTRIES LTD.

- ALCOA CORPORATION

- PRODUCT LAUNCHES

- ALUMINIUM CORPORATION OF CHINA LIMITED

- RUSAL

- KAISER ALUMINUM

- CENTURY ALUMINUM COMPANY

- CONSTELLIUM

- NORSK HYDRO ASA

- JINDAL ALUMINUM LIMITED

- HAMMERER ALUMINUM INDUSTRIES

- ALOM GROUP

- BANCO ALUMINUM PRIVATE LIMITED

- MAAN ALUMINIUM LIMITED

- SHENZHEN ORIENTAL TURDO IRONWARES CO., LTD

- ETEM

- 其他公司

- GUANGDONG ZHENHAN SPECIAL LIGHT ALLOY CO., LTD

- ALBRAS

- YK ALUMINIUM

- ELEANOR INDUSTRIES PVT. LTD

- ALUPCO

- ZAHIT ALUMINYUM

- ARCONIC

- HULAMIN

- GULF EXTRUSION

- BENKAM ALU EXTRUSIONS

第十六章调查方法

第十七章附录

The aluminum extrusion market is estimated at USD 111.88 billion in 2024 and is projected to reach USD 166.65 billion by 2030, at a CAGR of 7.0% from 2025 to 2030.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2023-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD Million/Billion), Volume (Kiloton) |

| Segments | By Type, By Alloy Grade, By Surface Finish, By End-use Industry, and By Region |

| Regions covered | Europe, North America, Asia Pacific, Latin America, Middle East & Africa |

Solid profiles dominated the overall aluminum extrusion market owing to the simplicity in manufacturing and structural solidity. Solid profiles include shapes like rods, bars, flat bars, angles (L-profiles), channels (U or C shapes), and beams, offering high material density for strength without internal openings. They are extruded using straightforward solid dies, making production faster and more cost-effective than complex profiles like semi-hollow and hollow profiles.

''By alloy grade, 6xxx alloy grade accounted for the largest share of the overall aluminum extrusion market in 2024.''

6xxx series aluminum alloys dominate the aluminum extrusion market due to their optimal combination of extrudability, medium-to-high strength, corrosion resistance, and heat-treatable properties. These alloys, primarily alloyed with magnesium (Mg) and silicon (Si) to form magnesium silicide, enable complex shapes and thin-walled profiles essential for extrusions.

6xxx alloys offer excellent formability during extrusion, good weldability with 4xxx or 5xxx fillers, and superior surface finish for anodizing or painting. Common tempers like T5 or T6 enhance strength via precipitation hardening at 160-182°C. They balance tensile strength (18-58 ksi) with ductility, though sensitive to cracking if not managed.

''The mill-finished segment is estimated to be the most preferred surface finish of aluminum extrusion during the forecast period.''

The mill-finished segment is expected to dominate the market and register the highest CAGR during the forecast period. Lower production costs from skipping finishing processes make mill-finished extrusions attractive for high-volume manufacturing, especially amid rising raw material prices and inflation pressures. This segment benefits from shorter lead times, enabling quick supply to industrial users who apply custom finishes later.

''The construction & infrastructure end-use industry dominated the aluminum extrusion market in 2024.'

The construction & infrastructure sector is projected to grow at the highest CAGR of 6.9% during the forecast period, in terms of value. The construction industry is also one of the major end users of aluminum extruded products. Aluminum is considered one of the most viable building materials due to the wide range of benefits it offers, such as light strength-to-weight ratio, sustainability, recyclability, and versatility. Aluminum is widely used in construction as it helps building projects qualify for green building status under the Leadership in Energy and Environmental Design (LEED) standards.

"Asia Pacific is estimated to account for the largest share in the overall aluminum extrusion market."

Asia Pacific holds the dominant share in the global aluminum extrusion market. This leadership stems from rapid industrialization, urbanization, and surging demand across key sectors. Robust economic growth in countries like China, India, Japan, and South Korea fuels infrastructure projects and high-rise construction, which heavily rely on extruded aluminum for its lightweight strength and corrosion resistance.

The automotive industry in the region prioritizes lightweight materials for fuel-efficient vehicles amid strict emissions rules, with China as the world's largest auto market. Electronics, machinery, and renewable energy sectors (like solar frames) further boost usage due to aluminum's conductivity and versatility.

This study has been validated through primary interviews with industry experts globally. These primary sources have been divided based on the following three categories:

- By Company Type - Tier 1 - 60%, Tier 2 - 20%, and Tier 3 - 20%

- By Designation - C Level - 33%, Director Level - 33%, and Others - 34%

- By Region - North America - 20%, Europe - 25%, Asia Pacific - 25%, Middle East & Africa -20%, South America - 10%.

The report provides a comprehensive analysis of company profiles:

Prominent companies include Jindal Aluminum Limited (India), Hindalco Industries Ltd. (India), Alcoa Corporation (US), Aluminum Corporation of China Limited (China), RUSAL (Russia), Century Aluminum Company (US), Norsk Hydro ASA (Norway), Constellium (France), Kaiser Aluminum (US), Hammerer Aluminum Industries (Austria), Banco Aluminium Private Limited (India), Maan Aluminium Limited (India), Shenzhen Oriental Turdo Ironwares Co., Ltd. (China), ETEM (Greece), and Alom Group (India).

Research Coverage

This research report categorizes the aluminum extrusion market by product (solid profiles, semi-hollow profiles, and hollow profiles), alloy grade (6xxx, 1xxx, 5xxx, and other grades), surface finish (mill-finished, anodized, and powder coated), end-use industry (construction & infrastructure, automotive & mass transport, electrical & electronics, and machinery & equipment), and region (North America, Europe, Asia Pacific, Middle East & Africa, and Latin America). The scope of the report includes detailed information about the major factors influencing the growth of the aluminum extrusion market, such as drivers, restraints, challenges, and opportunities. A thorough examination of the key industry players has been conducted to provide insights into their business overview, solutions, and services, key strategies, contracts, partnerships, and agreements. New product and service launches, mergers & acquisitions, and recent developments in the aluminum extrusion market are all covered. This report includes a competitive analysis of upcoming startups in the aluminum extrusion market ecosystem.

Reasons to buy this report:

The report will help the leaders/new entrants in this market with information on the closest approximations of the revenue numbers for the overall aluminum extrusion market and the subsegments. This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights on the following pointers:

- Analysis of key drivers (Rising demand from automotive sector, Cross-industry adoption), restraints (Capital Intensity, High Energy Consumption), opportunities (Advanced manufacturing technologies, Unmet needs for premium alloys or services), and challenges (Raw material cost volatility, Energy consumption and sustainability) influencing the growth of the aluminum extrusion market.

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product & service launches in the aluminum extrusion market.

- Market Development: Comprehensive information about lucrative markets - the report analyses the aluminum extrusion market across varied regions.

- Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the aluminum extrusion market

- Competitive Assessment: In-depth assessment of market shares, growth strategies and service offerings of leading players, such as Jindal Aluminum Limited (India), Hindalco Industries Ltd. (India), Alcoa Corporation (US), Aluminum Corporation of China Limited (China), RUSAL (Russia), Century Aluminum Company (US), Norsk Hydro ASA (Norway), Constellium (France), Kaiser Aluminum (US), Hammerer Aluminum Industries (Austria), Banco Aluminium Private Limited (India), Maan Aluminium Limited (India), Shenzhen Oriental Turdo Ironwares Co., Ltd. (China), ETEM (Greece), and Alom Group (India) in the aluminum extrusion market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.3.5 UNIT CONSIDERED

- 1.4 STAKEHOLDERS

- 1.5 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: SHARE INSIGHTS AND STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING MARKET

- 2.4 HIGH-GROWTH SEGMENTS & EMERGING FRONTIERS

- 2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN ALUMINUM EXTRUSION MARKET

- 3.2 ALUMINUM EXTRUSION MARKET, BY PRODUCT AND REGION

- 3.3 ALUMINUM EXTRUSION MARKET, BY ALLOY GRADE

- 3.4 ALUMINUM EXTRUSION MARKET, BY SURFACE FINISH

- 3.5 ALUMINUM EXTRUSION MARKET, BY END-USE INDUSTRY

- 3.6 ALUMINUM EXTRUSION MARKET, BY COUNTRY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Rising demand from automotive sector

- 4.2.1.2 Cross-industry adoption

- 4.2.2 RESTRAINTS

- 4.2.2.1 Capital intensity

- 4.2.2.2 High energy consumption

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Advanced manufacturing technologies

- 4.2.3.2 Unmet needs for premium alloys or services

- 4.2.4 CHALLENGES

- 4.2.4.1 Raw material cost volatility

- 4.2.4.2 Energy consumption and sustainability

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS IN ALUMINUM EXTRUSION MARKET

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 EMERGING BUSINESS MODELS AND ECOSYSTEM SHIFTS

- 4.5.1 EMERGING BUSINESS MODELS

- 4.5.2 ECOSYSTEM SHIFTS

- 4.6 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

- 4.6.1 KEY MOVES AND STRATEGIC FOCUS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF BUYERS

- 5.1.4 BARGAINING POWER OF SUPPLIERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC INDICATORS

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST

- 5.2.3 TRENDS IN GLOBAL AUTOMOTIVE & MASS TRANSPORT INDUSTRY

- 5.2.4 TRENDS IN GLOBAL AEROSPACE & DEFENSE INDUSTRY

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 AVERAGE SELLING PRICE BY KEY PLAYERS

- 5.5.2 AVERAGE SELLING PRICE TREND, BY REGION

- 5.6 TRADE ANALYSIS

- 5.6.1 IMPORT SCENARIO (HS CODE 760421)

- 5.6.2 EXPORT SCENARIO (HS CODE 760421)

- 5.7 KEY CONFERENCES AND EVENTS, 2026

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.9 CASE STUDY ANALYSIS

- 5.9.1 HIGH-STRENGTH ALUMINUM ALLOYS IN ADVANCED AIRCRAFT PROGRAM

- 5.9.2 ALCOA ALLOY ADVANCEMENTS: A210 EXTRUSTRONG & C611 EZCAST

- 5.9.3 PROJECT M-LIGHTEN: CONSTELLIUM & GORDON MURRAY GROUP PARTNERSHIP

- 5.10 IMPACT OF 2025 US TARIFF ON ALUMINUM EXTRUSION MARKET

- 5.10.1 INTRODUCTION

- 5.10.2 KEY TARIFF RATES

- 5.10.3 PRICE IMPACT ANALYSIS

- 5.10.4 IMPACT ON COUNTRIES/REGIONS

- 5.10.4.1 US

- 5.10.4.2 Europe

- 5.10.4.3 Asia Pacific

- 5.10.5 IMPACT ON END-USE INDUSTRIES

6 STRATEGIC DISRUPTION THROUGH TECHNOLOGY, PATENTS, DIGITAL, AND AI ADOPTION

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.1.1 EXTRUSION TECHNOLOGY

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 LASER POWDER BED FUSION

- 6.3 TECHNOLOGY/PRODUCT ROADMAP

- 6.3.1 SHORT-TERM (2025-2027) | FOUNDATION & EARLY COMMERCIALIZATION

- 6.3.2 MID-TERM (2027-2030) | EXPANSION & STANDARDIZATION

- 6.3.3 LONG-TERM (2030-2035+) | MASS COMMERCIALIZATION & DISRUPTION

- 6.4 ANALYSIS

- 6.4.1 INTRODUCTION

- 6.4.2 METHODOLOGY

- 6.4.3 DOCUMENT TYPE

- 6.4.4 INSIGHTS

- 6.4.5 LEGAL STATUS OF PATENTS

- 6.4.6 JURISDICTION ANALYSIS

- 6.4.7 TOP APPLICANTS

- 6.4.8 LIST OF PATENTS BY JIANGSU GIANSUN PRECISION TECH GROUP CO., LTD.

- 6.4.9 LIST OF PATENTS BY SUZHOU WORTEL PRECISION MOLD MACHINERY CO., LTD.

- 6.4.10 LIST OF PATENTS BY HEBEI AOYI NEW MAT CO., LTD.

- 6.5 FUTURE APPLICATIONS

- 6.5.1 AUTOMOTIVE & MASS TRANSPORT: LIGHTWEIGHTING & STRUCTURAL COMPONENTS

- 6.5.2 BUILDING & CONSTRUCTION: WINDOW FRAMES, FACADES, AND PROFILES

- 6.5.3 ELECTRICAL & ELECTRONICS: HEAT SINKS & ENCLOSURES

- 6.6 IMPACT OF AI/GEN AI ON ALUMINUM EXTRUSION MARKET

- 6.6.1 TOP USE CASES AND MARKET POTENTIAL

- 6.6.2 BEST PRACTICES IN ALUMINUM EXTRUSION PROCESSING

- 6.6.3 CASE STUDIES OF AI IMPLEMENTATION IN ALUMINUM EXTRUSION MARKET

- 6.6.4 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.6.5 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN ALUMINUM EXTRUSION MARKET

- 6.7 SUCCESS STORIES AND REAL-WORLD APPLICATIONS

- 6.7.1 ALCOA CORPORATION: INNOVATING EV STRUCTURES WITH MEGACASTING ALUMINUM EXTRUDED COMPONENTS

- 6.7.2 CONSTELLIUM: REVOLUTIONIZING COMPONENTS WITH AHEADD CP1

- 6.7.3 BOEING: AI-DRIVEN AUTOMATION FOR 777X AND 737 ASSEMBLY

7 SUSTAINABILITY AND REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

- 7.2 SUSTAINABILITY INITIATIVES

- 7.2.1 CARBON IMPACT AND ECO-APPLICATIONS OF ALUMINUM EXTRUDED PRODUCTS

- 7.2.1.1 Eco-applications

- 7.2.1 CARBON IMPACT AND ECO-APPLICATIONS OF ALUMINUM EXTRUDED PRODUCTS

- 7.3 SUSTAINABILITY IMPACT AND REGULATORY POLICY INITIATIVES

- 7.4 CERTIFICATIONS, LABELING, AND ECO-STANDARDS

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS AND BUYING CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.4 UNMET NEEDS IN VARIOUS END-USE INDUSTRIES

- 8.5 MARKET PROFITABILITY

- 8.5.1 REVENUE POTENTIAL

- 8.5.2 COST DYNAMICS

- 8.5.3 MARGIN OPPORTUNITIES, BY END-USE INDUSTRY

9 ALUMINUM EXTRUSION MARKET, BY ALLOY GRADE

- 9.1 INTRODUCTION

- 9.2 6XXX

- 9.2.1 OPTIMAL COMBINATION OF EXTRUDABILITY AND HEAT-TREATABLE PROPERTIES TO DRIVE DEMAND

- 9.3 1XXX

- 9.3.1 SUPERIOR CONDUCTIVITY TO DRIVE ADOPTION IN ELECTRICAL & ELECTRONICS INDUSTRY

- 9.4 5XXX

- 9.4.1 MAGNESIUM ADDITION OFFERS ADDITIONAL STRENGTH AND EXCELLENT CORROSION RESISTANCE TO PROPEL GROWTH

- 9.5 OTHER GRADES

10 ALUMINUM EXTRUSION MARKET, BY PRODUCT

- 10.1 INTRODUCTION

- 10.2 SOLID PROFILES

- 10.2.1 SIMPLICITY IN MANUFACTURING AND STRUCTURAL SOLIDITY TO DRIVE DEMAND

- 10.2.2 RODS & BARS

- 10.2.3 ANGLES & CHANNELS

- 10.2.4 BEAMS

- 10.3 SEMI-HOLLOW PROFILES

- 10.3.1 GROWING DEMAND FROM CONSTRUCTION & INFRASTRUCTURE TO DRIVE MARKET

- 10.3.2 WINDOW FRAMES & TRACK SYSTEMS

- 10.3.3 C-SHAPED PROFILES

- 10.4 HOLLOW PROFILES

- 10.4.1 DEMAND FROM HVAC, AUTOMOTIVE, AND AEROSPACE SECTORS TO BOOST MARKET

- 10.4.2 PIPES & TUBES

11 ALUMINUM EXTRUSION MARKET, BY SURFACE FINISH

- 11.1 INTRODUCTION

- 11.2 MILL-FINISHED

- 11.2.1 LOWER PRODUCTION COSTS DRIVING DEMAND

- 11.3 ANODIZED

- 11.3.1 HIGH DURABILITY AND WEATHER RESISTANCE TO DRIVE ADOPTION

- 11.4 POWDER-COATED

- 11.4.1 AUTOMOTIVE AND EV EXPANSION TO BOOST MARKET

12 ALUMINUM EXTRUSION MARKET, BY END-USE INDUSTRY

- 12.1 INTRODUCTION

- 12.2 CONSTRUCTION & INFRASTRUCTURE

- 12.2.1 HIGHER STRENGTH-TO-WEIGHT RATIO COMPARED TO OTHER MATERIALS TO DRIVE DEMAND

- 12.3 AUTOMOTIVE & MASS TRANSPORT

- 12.3.1 GROWING ADOPTION IN EV MANUFACTURING TO PROPEL GROWTH

- 12.4 ELECTRICAL & ELECTRONICS

- 12.4.1 SUPERIOR CONDUCTIVITY-TO-WEIGHT RATIO TO DRIVE ADOPTION

- 12.5 MACHINERY & EQUIPMENT

- 12.5.1 LIGHTWEIGHT STRUCTURE & MODULARITY TO DRIVE MARKET

- 12.6 OTHER END-USE INDUSTRIES

13 ALUMINUM EXTRUSION MARKET, BY REGION

- 13.1 INTRODUCTION

- 13.2 NORTH AMERICA

- 13.2.1 NORTH AMERICA: ALUMINUM EXTRUSION MARKET, BY PRODUCT TYPE

- 13.2.2 NORTH AMERICA: ALUMINUM EXTRUSION MARKET, BY ALLOY GRADE

- 13.2.3 NORTH AMERICA: ALUMINUM EXTRUSION MARKET, BY SURFACE FINISH

- 13.2.4 NORTH AMERICA: ALUMINUM EXTRUSION MARKET, BY END-USE INDUSTRY

- 13.2.5 NORTH AMERICA: ALUMINUM EXTRUSION MARKET, BY COUNTRY

- 13.2.6 US

- 13.2.6.1 Strategic investments and capacity expansion by key players to boost market

- 13.2.7 US: ALUMINUM EXTRUSION MARKET, BY END-USE INDUSTRY

- 13.2.8 CANADA

- 13.2.8.1 Expansion of sustainable construction and industrial initiatives to drive market

- 13.2.9 CANADA: ALUMINUM EXTRUSION MARKET, BY END-USE INDUSTRY

- 13.3 EUROPE

- 13.3.1 EUROPE: ALUMINUM EXTRUSION MARKET, BY PRODUCT TYPE

- 13.3.2 EUROPE: ALUMINUM EXTRUSION MARKET, BY ALLOY GRADE

- 13.3.3 EUROPE: ALUMINUM EXTRUSION MARKET, BY SURFACE FINISH

- 13.3.4 EUROPE: ALUMINUM EXTRUSION MARKET, BY END-USE INDUSTRY

- 13.3.5 EUROPE: ALUMINUM EXTRUSION MARKET, BY COUNTRY

- 13.3.6 GERMANY

- 13.3.6.1 Automotive lightweighting and industrial engineering to boost market

- 13.3.7 GERMANY: ALUMINUM EXTRUSION MARKET, BY END-USE INDUSTRY

- 13.3.8 FRANCE

- 13.3.8.1 Sustainable construction and transportation modernization to drive market growth

- 13.3.9 FRANCE: ALUMINUM EXTRUSION MARKET, BY END-USE INDUSTRY

- 13.3.10 UK

- 13.3.10.1 Strong supplier base to fuel growth of market

- 13.3.11 UK: ALUMINUM EXTRUSION MARKET, BY END-USE INDUSTRY

- 13.3.12 SPAIN

- 13.3.12.1 Infrastructure development and industrial growth to drive market

- 13.3.13 SPAIN: ALUMINUM EXTRUSION MARKET, BY END-USE INDUSTRY

- 13.3.14 ITALY

- 13.3.14.1 Industrial modernization trend to drive market

- 13.3.15 ITALY: ALUMINUM EXTRUSION MARKET, BY END-USE INDUSTRY

- 13.3.16 REST OF EUROPE

- 13.3.16.1 Rest of Europe: Aluminum extrusion market, by end-use industry

- 13.4 ASIA PACIFIC

- 13.4.1 ASIA PACIFIC: ALUMINUM EXTRUSION MARKET, BY PRODUCT TYPE

- 13.4.2 ASIA PACIFIC: ALUMINUM EXTRUSION MARKET, BY ALLOY GRADE

- 13.4.3 ASIA PACIFIC: ALUMINUM EXTRUSION MARKET, BY SURFACE FINISH

- 13.4.4 ASIA PACIFIC: ALUMINUM EXTRUSION MARKET, BY END-USE INDUSTRY

- 13.4.5 ASIA PACIFIC: ALUMINUM EXTRUSION MARKET, BY COUNTRY

- 13.4.6 CHINA

- 13.4.6.1 Expansion in electric vehicle manufacturing to drive demand

- 13.4.7 CHINA: ALUMINUM EXTRUSION MARKET, BY END-USE INDUSTRY

- 13.4.8 JAPAN

- 13.4.8.1 Electronics and electrical equipment boost specialized demand in market

- 13.4.9 JAPAN: ALUMINUM EXTRUSION MARKET, BY END-USE INDUSTRY

- 13.4.10 INDIA

- 13.4.10.1 Presence of major aluminum extrusion manufacturers drives growth

- 13.4.11 INDIA: ALUMINUM EXTRUSION MARKET, BY END-USE INDUSTRY

- 13.4.12 SOUTH KOREA

- 13.4.12.1 Favorable government policies and standards to drive market

- 13.4.13 SOUTH KOREA: ALUMINUM EXTRUSION MARKET, BY END-USE INDUSTRY

- 13.4.14 REST OF ASIA PACIFIC

- 13.4.14.1 Rest of Asia Pacific: Aluminum extrusion market, by end-use industry

- 13.5 MIDDLE EAST & AFRICA

- 13.5.1 MIDDLE EAST & AFRICA: ALUMINUM EXTRUSION MARKET, BY PRODUCT

- 13.5.2 MIDDLE EAST & AFRICA: ALUMINUM EXTRUSION MARKET, BY ALLOY GRADE

- 13.5.3 MIDDLE EAST & AFRICA: ALUMINUM EXTRUSION MARKET, BY SURFACE FINISH

- 13.5.4 MIDDLE EAST & AFRICA: ALUMINUM EXTRUSION MARKET, BY END-USE INDUSTRY

- 13.5.5 MIDDLE EAST & AFRICA: ALUMINUM EXTRUSION MARKET, BY COUNTRY

- 13.5.5.1 GCC countries

- 13.5.5.1.1 UAE

- 13.5.5.1.1.1 Presence of major aluminum producers drives growth

- 13.5.5.1.1.2 UAE: Aluminum extrusion market, by end-use industry

- 13.5.5.1.2 Saudi Arabia

- 13.5.5.1.2.1 Shift toward advanced manufacturing and lightweighting to drive growth

- 13.5.5.1.2.2 Saudi Arabia: Aluminum extrusion market, by end-use industry

- 13.5.5.1.1 UAE

- 13.5.5.2 Other GCC countries

- 13.5.5.2.1 Other GCC Countries: Aluminum extrusion market, by end-use industry

- 13.5.5.3 South Africa

- 13.5.5.3.1 Expansion of domestic manufacturing and extrusion capabilities to drive market

- 13.5.5.3.2 South Africa: Aluminum extrusion market, by end-use industry

- 13.5.5.1 GCC countries

- 13.5.6 REST OF MIDDLE EAST & AFRICA

- 13.5.6.1 Rest of Middle East & Africa: Aluminum extrusion market, By end-use industry

- 13.6 LATIN AMERICA

- 13.6.1 LATIN AMERICA: ALUMINUM EXTRUSION MARKET, BY PRODUCT TYPE

- 13.6.2 LATIN AMERICA: ALUMINUM EXTRUSION MARKET, BY ALLOY GRADE

- 13.6.3 LATIN AMERICA: ALUMINUM EXTRUSION MARKET, BY SURFACE FINISH

- 13.6.4 LATIN AMERICA: ALUMINUM EXTRUSION MARKET, BY END-USE INDUSTRY

- 13.6.5 LATIN AMERICA: ALUMINUM EXTRUSION MARKET, BY COUNTRY

- 13.6.6 BRAZIL

- 13.6.6.1 Infrastructure development and industrial diversification

- 13.6.7 BRAZIL: ALUMINUM EXTRUSION MARKET, BY END-USE INDUSTRY

- 13.6.8 MEXICO

- 13.6.8.1 Automotive manufacturing expansion driving Mexico aluminum extrusion market

- 13.6.9 MEXICO: ALUMINUM EXTRUSION MARKET, BY END-USE INDUSTRY

- 13.6.10 REST OF LATIN AMERICA

- 13.6.10.1 Rest of Latin America: Aluminum extrusion market, by end-use industry

14 COMPETITIVE LANDSCAPE

- 14.1 OVERVIEW

- 14.2 KEY PLAYERS' STRATEGIES/RIGHT TO WIN

- 14.3 REVENUE ANALYSIS

- 14.4 MARKET SHARE ANALYSIS

- 14.5 BRAND/PRODUCT COMPARISON

- 14.6 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 14.6.1 STARS

- 14.6.2 EMERGING LEADERS

- 14.6.3 PERVASIVE PLAYERS

- 14.6.4 PARTICIPANTS

- 14.6.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 14.6.5.1 Company footprint

- 14.6.5.2 Region footprint

- 14.6.5.3 Product footprint

- 14.6.5.4 Alloy grade footprint

- 14.6.5.5 Surface finish footprint

- 14.6.5.6 End-use industry footprint

- 14.7 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 14.7.1 PROGRESSIVE COMPANIES

- 14.7.2 RESPONSIVE COMPANIES

- 14.7.3 DYNAMIC COMPANIES

- 14.7.4 STARTING BLOCKS

- 14.7.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 14.7.5.1 Detailed list of key startups/SMEs

- 14.7.5.2 Competitive benchmarking of key startups/SMEs

- 14.8 COMPANY VALUATION AND FINANCIAL METRICS

- 14.9 COMPETITIVE SCENARIO

- 14.9.1 PRODUCT LAUNCHES

- 14.9.2 DEALS

- 14.9.3 EXPANSIONS

15 COMPANY PROFILES

- 15.1 KEY PLAYERS

- 15.1.1 HINDALCO INDUSTRIES LTD.

- 15.1.1.1 Business overview

- 15.1.1.2 Products/Solutions/Services offered

- 15.1.1.3 Recent Developments

- 15.1.1.3.1 Deals

- 15.1.1.3.2 Expansions

- 15.1.1.4 MnM view

- 15.1.1.4.1 Right to win

- 15.1.1.4.2 Strategic choices

- 15.1.1.4.3 Weaknesses and competitive threats

- 15.1.2 ALCOA CORPORATION

- 15.1.2.1 Business overview

- 15.1.2.2 Products/Solutions/Services offered

- 15.1.2.3 Recent developments

- 15.1.3 PRODUCT LAUNCHES

- 15.1.3.1 MnM view

- 15.1.3.1.1 Right to win

- 15.1.3.1.2 Strategic choices

- 15.1.3.1.3 Weaknesses and competitive threats

- 15.1.3.1 MnM view

- 15.1.4 ALUMINIUM CORPORATION OF CHINA LIMITED

- 15.1.4.1 Business overview

- 15.1.4.2 Products/Solutions/Services offered

- 15.1.4.3 MnM view

- 15.1.4.3.1 Right to win

- 15.1.4.3.2 Strategic choices

- 15.1.4.3.3 Weaknesses and competitive threats

- 15.1.5 RUSAL

- 15.1.5.1 Business overview

- 15.1.5.2 Products/Solutions/Services offered

- 15.1.6 KAISER ALUMINUM

- 15.1.6.1 Business overview

- 15.1.6.2 Products/Solutions/Services offered

- 15.1.6.3 MnM view

- 15.1.6.3.1 Right to win

- 15.1.6.3.2 Strategic choices

- 15.1.6.3.3 Weaknesses and competitive threats

- 15.1.7 CENTURY ALUMINUM COMPANY

- 15.1.7.1 Business overview

- 15.1.7.2 Products/Solutions/Services offered

- 15.1.8 CONSTELLIUM

- 15.1.8.1 Business overview

- 15.1.8.2 Products/Solutions/Services offered

- 15.1.8.3 Recent Developments

- 15.1.8.3.1 Deals

- 15.1.9 NORSK HYDRO ASA

- 15.1.9.1 Business overview

- 15.1.9.2 Products/Solutions/Services offered

- 15.1.10 JINDAL ALUMINUM LIMITED

- 15.1.10.1 Business overview

- 15.1.10.2 Products/Solutions/Services offered

- 15.1.10.3 MnM view

- 15.1.10.3.1 Right to win

- 15.1.10.3.2 Strategic choices

- 15.1.10.3.3 Weaknesses and competitive threats

- 15.1.11 HAMMERER ALUMINUM INDUSTRIES

- 15.1.11.1 Business overview

- 15.1.11.2 Products/Solutions/Services offered

- 15.1.12 ALOM GROUP

- 15.1.12.1 Business overview

- 15.1.12.2 Products/Solutions/Services offered

- 15.1.13 BANCO ALUMINUM PRIVATE LIMITED

- 15.1.13.1 Business overview

- 15.1.13.2 Products/Solutions/Services offered

- 15.1.14 MAAN ALUMINIUM LIMITED

- 15.1.14.1 Business overview

- 15.1.14.2 Products/Solutions/Services offered

- 15.1.15 SHENZHEN ORIENTAL TURDO IRONWARES CO., LTD

- 15.1.15.1 Business overview

- 15.1.15.2 Products/Solutions/Services offered

- 15.1.16 ETEM

- 15.1.16.1 Business overview

- 15.1.16.2 Products/Solutions/Services offered

- 15.1.16.3 Recent Developments

- 15.1.16.3.1 Deals

- 15.1.1 HINDALCO INDUSTRIES LTD.

- 15.2 OTHER PLAYERS

- 15.2.1 GUANGDONG ZHENHAN SPECIAL LIGHT ALLOY CO., LTD

- 15.2.2 ALBRAS

- 15.2.3 YK ALUMINIUM

- 15.2.4 ELEANOR INDUSTRIES PVT. LTD

- 15.2.5 ALUPCO

- 15.2.6 ZAHIT ALUMINYUM

- 15.2.7 ARCONIC

- 15.2.8 HULAMIN

- 15.2.9 GULF EXTRUSION

- 15.2.10 BENKAM ALU EXTRUSIONS

16 RESEARCH METHODOLOGY

- 16.1 RESEARCH DATA

- 16.1.1 SECONDARY DATA

- 16.1.1.1 Key data from secondary sources

- 16.1.2 PRIMARY DATA

- 16.1.2.1 Key data from primary sources

- 16.1.2.2 Key primary interview participants

- 16.1.2.3 Breakdown of primary interviews

- 16.1.2.4 Key industry insights

- 16.1.1 SECONDARY DATA

- 16.2 MARKET SIZE ESTIMATION

- 16.2.1 BOTTOM-UP APPROACH

- 16.2.2 TOP-DOWN APPROACH

- 16.3 BASE NUMBER CALCULATION

- 16.3.1 APPROACH 1: SUPPLY-SIDE ANALYSIS

- 16.3.2 APPROACH 2: DEMAND-SIDE ANALYSIS

- 16.4 MARKET FORECAST APPROACH

- 16.4.1 SUPPLY SIDE

- 16.4.2 DEMAND SIDE

- 16.5 DATA TRIANGULATION

- 16.6 FACTOR ANALYSIS

- 16.7 RESEARCH ASSUMPTIONS

- 16.8 RESEARCH LIMITATIONS AND RISK ASSESSMENT

17 APPENDIX

- 17.1 DISCUSSION GUIDE

- 17.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 17.3 CUSTOMIZATION OPTIONS

- 17.4 RELATED REPORTS

- 17.5 AUTHOR DETAILS

List of Tables

- TABLE 1 ALUMINUM EXTRUSION MARKET: PORTER'S FIVE FORCES ANALYSIS

- TABLE 2 GDP PERCENTAGE CHANGE, BY KEY COUNTRY, 2021-2029

- TABLE 3 ALUMINUM EXTRUSION MARKET: ROLE OF COMPANIES IN ECOSYSTEM

- TABLE 4 AVERAGE SELLING PRICE OF ALUMINUM EXTRUSION IN TOP END-USE INDUSTRIES, BY KEY PLAYERS, 2024 (USD/KG)

- TABLE 5 AVERAGE SELLING PRICE TREND OF ALUMINUM EXTRUSION, BY REGION, 2023-2024 (USD/KG)

- TABLE 6 IMPORT DATA FOR HS CODE 760421-COMPLIANT PRODUCTS, 2020-2024 (USD MILLION)

- TABLE 7 EXPORT DATA FOR HS CODE 760421-COMPLIANT PRODUCTS, 2020-2024 (USD MILLION)

- TABLE 8 ALUMINUM EXTRUSION MARKET: KEY CONFERENCES AND EVENTS, 2026

- TABLE 9 US-ADJUSTED RECIPROCAL TARIFF RATES

- TABLE 10 EXPECTED CHANGE IN PRICES AND IMPACT ON END-USE MARKET DUE TO TARIFFS

- TABLE 11 ALUMINUM EXTRUSION MARKET: TOTAL NUMBER OF PATENTS, 2015-2025

- TABLE 12 TOP USE CASES AND MARKET POTENTIAL

- TABLE 13 BEST PRACTICES: COMPANIES IMPLEMENTING USE CASES

- TABLE 14 ALUMINUM EXTRUSION MARKET: CASE STUDIES RELATED TO AI IMPLEMENTATION

- TABLE 15 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- TABLE 16 NORTH AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 17 EUROPE: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 18 ASIA PACIFIC: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 19 ROW: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 20 GLOBAL STANDARDS IN ALUMINUM EXTRUSION MARKET

- TABLE 21 CERTIFICATIONS, LABELING, AND ECO-STANDARDS IN ALUMINUM EXTRUSION MARKET

- TABLE 22 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS, BY END-USE INDUSTRY (%)

- TABLE 23 KEY BUYING CRITERIA, BY END-USE INDUSTRY

- TABLE 24 ALUMINUM EXTRUSION MARKET: UNMET NEEDS IN KEY END-USE INDUSTRIES

- TABLE 25 ALUMINUM EXTRUSION MARKET, BY ALLOY GRADE, 2023-2030 (USD MILLION)

- TABLE 26 ALUMINUM EXTRUSION MARKET, BY ALLOY GRADE, 2023-2030 (KILOTON)

- TABLE 27 6XXX: ALUMINUM EXTRUSION MARKET, BY REGION, 2023-2030 (USD MILLION)

- TABLE 28 6XXX: ALUMINUM EXTRUSION MARKET, BY REGION, 2023-2030 (KILOTON)

- TABLE 29 1XXX: ALUMINUM EXTRUSION MARKET, BY REGION, 2023-2030 (USD MILLION)

- TABLE 30 1XXX: ALUMINUM EXTRUSION MARKET, BY REGION, 2023-2030 (KILOTON)

- TABLE 31 5XXX: ALUMINUM EXTRUSION MARKET, BY REGION, 2023-2030 (USD MILLION)

- TABLE 32 5XXX: ALUMINUM EXTRUSION MARKET, BY REGION, 2023-2030 (KILOTON)

- TABLE 33 OTHER GRADES: ALUMINUM EXTRUSION MARKET, BY REGION, 2023-2030 (USD MILLION)

- TABLE 34 OTHER GRADES: ALUMINUM EXTRUSION MARKET, BY REGION, 2023-2030 (KILOTON)

- TABLE 35 ALUMINUM EXTRUSION MARKET, BY PRODUCT, 2023-2030 (USD MILLION)

- TABLE 36 ALUMINUM EXTRUSION MARKET, BY PRODUCT, 2023-2030 (KILOTON)

- TABLE 37 SOLID PROFILES: ALUMINUM EXTRUSION MARKET, BY REGION, 2023-2030 (USD MILLION)

- TABLE 38 SOLID PROFILES: ALUMINUM EXTRUSION MARKET, BY REGION, 2023-2030 (KILOTON)

- TABLE 39 SEMI-HOLLOW PROFILES: ALUMINUM EXTRUSION MARKET, BY REGION, 2023-2030 (USD MILLION)

- TABLE 40 SEMI-HOLLOW PROFILES: ALUMINUM EXTRUSION MARKET, BY REGION, 2023-2030 (KILOTON)

- TABLE 41 HOLLOW PROFILES: ALUMINUM EXTRUSION MARKET, BY REGION, 2023-2030 (USD MILLION)

- TABLE 42 HOLLOW PROFILES: ALUMINUM EXTRUSION MARKET, BY REGION, 2023-2030 (KILOTON)

- TABLE 43 ALUMINUM EXTRUSION MARKET, BY SURFACE FINISH, 2023-2030 (USD MILLION)

- TABLE 44 ALUMINUM EXTRUSION MARKET, BY SURFACE FINISH, 2023-2030 (KILOTON)

- TABLE 45 MILL-FINISHED: ALUMINUM EXTRUSION MARKET, BY REGION, 2023-2030 (USD MILLION)

- TABLE 46 MILL-FINISHED: ALUMINUM EXTRUSION MARKET, BY REGION, 2023-2030 (KILOTON)

- TABLE 47 ANODIZED: ALUMINUM EXTRUSION MARKET, BY REGION, 2023-2030 (USD MILLION)

- TABLE 48 ANODIZED: ALUMINUM EXTRUSION MARKET, BY REGION, 2023-2030 (KILOTON)

- TABLE 49 POWDER-COATED: ALUMINUM EXTRUSION MARKET, BY REGION, 2023-2030 (USD MILLION)

- TABLE 50 POWDER-COATED: ALUMINUM EXTRUSION MARKET, BY REGION, 2023-2030 (KILOTON)

- TABLE 51 ALUMINUM EXTRUSION MARKET, BY END-USE INDUSTRY, 2023-2030 (USD MILLION)

- TABLE 52 ALUMINUM EXTRUSION MARKET, BY END-USE INDUSTRY, 2023-2030 (KILOTON)

- TABLE 53 CONSTRUCTION & INFRASTRUCTURE: ALUMINUM EXTRUSION MARKET, BY REGION, 2023-2030 (USD MILLION)

- TABLE 54 CONSTRUCTION & INFRASTRUCTURE: ALUMINUM EXTRUSION MARKET, BY REGION, 2023-2030 (KILOTON)

- TABLE 55 AUTOMOTIVE & MASS TRANSPORT: ALUMINUM EXTRUSION MARKET, BY REGION, 2023-2030 (USD MILLION)

- TABLE 56 AUTOMOTIVE & MASS TRANSPORT: ALUMINUM EXTRUSION MARKET, BY REGION, 2023-2030 (KILOTON)

- TABLE 57 ELECTRICAL & ELECTRONICS: ALUMINUM EXTRUSION MARKET, BY REGION, 2023-2030 (USD MILLION)

- TABLE 58 ELECTRICAL & ELECTRONICS: ALUMINUM EXTRUSION MARKET, BY REGION, 2023-2030 (KILOTON)

- TABLE 59 MACHINERY & EQUIPMENT: ALUMINUM EXTRUSION MARKET, BY REGION, 2023-2030 (USD MILLION)

- TABLE 60 MACHINERY & EQUIPMENT: ALUMINUM EXTRUSION MARKET, BY REGION, 2023-2030 (KILOTON)

- TABLE 61 OTHER END-USE INDUSTRIES: ALUMINUM EXTRUSION MARKET, BY REGION, 2023-2030 (USD MILLION)

- TABLE 62 OTHER END-USE INDUSTRIES: ALUMINUM EXTRUSION MARKET, BY REGION, 2023-2030 (KILOTON)

- TABLE 63 ALUMINUM EXTRUSION MARKET, BY REGION, 2023-2030 (USD MILLION)

- TABLE 64 ALUMINUM EXTRUSION MARKET, BY REGION, 2023-2030 (KILOTON)

- TABLE 65 NORTH AMERICA: ALUMINUM EXTRUSION MARKET, BY PRODUCT TYPE, 2023-2030 (USD MILLION)

- TABLE 66 NORTH AMERICA: ALUMINUM EXTRUSION MARKET, BY PRODUCT TYPE, 2023-2030 (KILOTON)

- TABLE 67 NORTH AMERICA: ALUMINUM EXTRUSION MARKET, BY ALLOY GRADE, 2023-2030 (USD MILLION)

- TABLE 68 NORTH AMERICA: ALUMINUM EXTRUSION MARKET, BY ALLOY GRADE, 2023-2030 (KILOTON)

- TABLE 69 NORTH AMERICA: ALUMINUM EXTRUSION MARKET, BY SURFACE FINISH, 2023-2030 (USD MILLION)

- TABLE 70 NORTH AMERICA: ALUMINUM EXTRUSION MARKET, BY SURFACE FINISH, 2023-2030 (KILOTON)

- TABLE 71 NORTH AMERICA: ALUMINUM EXTRUSION MARKET, BY END-USE INDUSTRY, 2023-2030 (USD MILLION)

- TABLE 72 NORTH AMERICA: ALUMINUM EXTRUSION MARKET, BY END-USE INDUSTRY, 2023-2030 (KILOTON)

- TABLE 73 NORTH AMERICA: ALUMINUM EXTRUSION MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 74 NORTH AMERICA: ALUMINUM EXTRUSION MARKET, BY COUNTRY, 2023-2030 (KILOTON)

- TABLE 75 US: ALUMINUM EXTRUSION MARKET, BY END-USE INDUSTRY, 2023-2030 (USD MILLION)

- TABLE 76 US: ALUMINUM EXTRUSION MARKET, BY END-USE INDUSTRY, 2023-2030 (KILOTON)

- TABLE 77 CANADA: ALUMINUM EXTRUSION MARKET, BY END-USE INDUSTRY, 2023-2030 (USD MILLION)

- TABLE 78 CANADA: ALUMINUM EXTRUSION MARKET, BY END-USE INDUSTRY, 2023-2030 (KILOTON)

- TABLE 79 EUROPE: ALUMINUM EXTRUSION MARKET, BY PRODUCT TYPE, 2023-2030 (USD MILLION)

- TABLE 80 EUROPE: ALUMINUM EXTRUSION MARKET, BY PRODUCT TYPE, 2023-2030 (KILOTON)

- TABLE 81 EUROPE: ALUMINUM EXTRUSION MARKET, BY ALLOY GRADE, 2023-2030 (USD MILLION)

- TABLE 82 EUROPE: ALUMINUM EXTRUSION MARKET, BY ALLOY GRADE, 2023-2030 (KILOTON)

- TABLE 83 EUROPE: ALUMINUM EXTRUSION MARKET, BY SURFACE FINISH, 2023-2030 (USD MILLION)

- TABLE 84 EUROPE: ALUMINUM EXTRUSION MARKET, BY SURFACE FINISH, 2023-2030 (KILOTON)

- TABLE 85 EUROPE: ALUMINUM EXTRUSION MARKET, BY END-USE INDUSTRY, 2023-2030 (USD MILLION)

- TABLE 86 EUROPE: ALUMINUM EXTRUSION MARKET, BY END-USE INDUSTRY, 2023-2030 (KILOTON)

- TABLE 87 EUROPE: ALUMINUM EXTRUSION MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 88 EUROPE: ALUMINUM EXTRUSION MARKET, BY COUNTRY, 2023-2030 (KILOTON)

- TABLE 89 GERMANY: ALUMINUM EXTRUSION MARKET, BY END-USE INDUSTRY, 2023-2030 (USD MILLION)

- TABLE 90 GERMANY: ALUMINUM EXTRUSION MARKET, BY END-USE INDUSTRY, 2023-2030 (KILOTON)

- TABLE 91 FRANCE: ALUMINUM EXTRUSION MARKET, BY END-USE INDUSTRY, 2023-2030 (USD MILLION)

- TABLE 92 FRANCE: ALUMINUM EXTRUSION MARKET, BY END-USE INDUSTRY, 2023-2030 (KILOTON)

- TABLE 93 UK: ALUMINUM EXTRUSION MARKET, BY END-USE INDUSTRY, 2023-2030 (USD MILLION)

- TABLE 94 UK: ALUMINUM EXTRUSION MARKET, BY END-USE INDUSTRY, 2023-2030 (KILOTON)

- TABLE 95 SPAIN: ALUMINUM EXTRUSION MARKET, BY END-USE INDUSTRY, 2023-2030 (USD MILLION)

- TABLE 96 SPAIN: ALUMINUM EXTRUSION MARKET, BY END-USE INDUSTRY, 2023-2030 (KILOTON)

- TABLE 97 ITALY: ALUMINUM EXTRUSION MARKET, BY END-USE INDUSTRY, 2023-2030 (USD MILLION)

- TABLE 98 ITALY: ALUMINUM EXTRUSION MARKET, BY END-USE INDUSTRY, 2023-2030 (KILOTON)

- TABLE 99 REST OF EUROPE: ALUMINUM EXTRUSION MARKET, BY END-USE INDUSTRY, 2023-2030 (USD MILLION)

- TABLE 100 REST OF EUROPE: ALUMINUM EXTRUSION MARKET, BY END-USE INDUSTRY, 2023-2030 (KILOTON)

- TABLE 101 ASIA PACIFIC: ALUMINUM EXTRUSION MARKET, BY PRODUCT TYPE, 2023-2030 (USD MILLION)

- TABLE 102 ASIA PACIFIC: ALUMINUM EXTRUSION MARKET, BY PRODUCT TYPE, 2023-2030 (KILOTON)

- TABLE 103 ASIA PACIFIC: ALUMINUM EXTRUSION MARKET, BY ALLOY GRADE, 2023-2030 (USD MILLION)

- TABLE 104 ASIA PACIFIC: ALUMINUM EXTRUSION MARKET, BY ALLOY GRADE, 2023-2030 (KILOTON)

- TABLE 105 ASIA PACIFIC: ALUMINUM EXTRUSION MARKET, BY SURFACE FINISH, 2023-2030 (USD MILLION)

- TABLE 106 ASIA PACIFIC: ALUMINUM EXTRUSION MARKET, BY SURFACE FINISH, 2023-2030 (KILOTON)

- TABLE 107 ASIA PACIFIC: ALUMINUM EXTRUSION MARKET, BY END-USE INDUSTRY, 2023-2030 (USD MILLION)

- TABLE 108 ASIA PACIFIC: ALUMINUM EXTRUSION MARKET, BY END-USE INDUSTRY, 2023-2030 (KILOTON)

- TABLE 109 ASIA PACIFIC: ALUMINUM EXTRUSION MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 110 ASIA PACIFIC: ALUMINUM EXTRUSION MARKET, BY COUNTRY, 2023-2030 (KILOTON)

- TABLE 111 CHINA: ALUMINUM EXTRUSION MARKET, BY END-USE INDUSTRY, 2023-2030 (USD MILLION)

- TABLE 112 CHINA: ALUMINUM EXTRUSION MARKET, BY END-USE INDUSTRY, 2023-2030 (KILOTON)

- TABLE 113 JAPAN: ALUMINUM EXTRUSION MARKET, BY END-USE INDUSTRY, 2023-2030 (USD MILLION)

- TABLE 114 JAPAN: ALUMINUM EXTRUSION MARKET, BY END-USE INDUSTRY, 2023-2030 (KILOTON)

- TABLE 115 INDIA: ALUMINUM EXTRUSION MARKET, BY END-USE INDUSTRY, 2023-2030 (USD MILLION)

- TABLE 116 INDIA: ALUMINUM EXTRUSION MARKET, BY END-USE INDUSTRY, 2023-2030 (KILOTON)

- TABLE 117 SOUTH KOREA: ALUMINUM EXTRUSION MARKET, BY END-USE INDUSTRY, 2023-2030 (USD MILLION)

- TABLE 118 SOUTH KOREA: ALUMINUM EXTRUSION MARKET, BY END-USE INDUSTRY, 2023-2030 (KILOTON)

- TABLE 119 REST OF ASIA PACIFIC: ALUMINUM EXTRUSION MARKET, BY END-USE INDUSTRY, 2023-2030 (USD MILLION)

- TABLE 120 REST OF ASIA PACIFIC: ALUMINUM EXTRUSION MARKET, BY END-USE INDUSTRY, 2023-2030 (KILOTON)

- TABLE 121 MIDDLE EAST & AFRICA: ALUMINUM EXTRUSION MARKET, BY PRODUCT, 2023-2030 (USD MILLION)

- TABLE 122 MIDDLE EAST & AFRICA: ALUMINUM EXTRUSION MARKET, BY PRODUCT, 2023-2030 (KILOTON)

- TABLE 123 MIDDLE EAST & AFRICA: ALUMINUM EXTRUSION MARKET, BY ALLOY GRADE, 2023-2030 (USD MILLION)

- TABLE 124 MIDDLE EAST & AFRICA: ALUMINUM EXTRUSION MARKET, BY ALLOY GRADE, 2023-2030 (KILOTON)

- TABLE 125 MIDDLE EAST & AFRICA: ALUMINUM EXTRUSION MARKET, BY SURFACE FINISH, 2023-2030 (USD MILLION)

- TABLE 126 MIDDLE EAST & AFRICA: ALUMINUM EXTRUSION MARKET, BY SURFACE FINISH, 2023-2030 (KILOTON)

- TABLE 127 MIDDLE EAST & AFRICA: ALUMINUM EXTRUSION MARKET, BY END-USE INDUSTRY, 2023-2030 (USD MILLION)

- TABLE 128 MIDDLE EAST & AFRICA: ALUMINUM EXTRUSION MARKET, BY END-USE INDUSTRY, 2023-2030 (KILOTON)

- TABLE 129 MIDDLE EAST & AFRICA: ALUMINUM EXTRUSION MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 130 MIDDLE EAST & AFRICA: ALUMINUM EXTRUSION MARKET, BY COUNTRY, 2023-2030 (KILOTON)

- TABLE 131 UAE: ALUMINUM EXTRUSION MARKET, BY END-USE INDUSTRY, 2023-2030 (USD MILLION)

- TABLE 132 UAE: ALUMINUM EXTRUSION MARKET, BY END-USE INDUSTRY, 2023-2030 (KILOTON)

- TABLE 133 SAUDI ARABIA: ALUMINUM EXTRUSION MARKET, BY END-USE INDUSTRY, 2023-2030 (USD MILLION)

- TABLE 134 SAUDI ARABIA: ALUMINUM EXTRUSION MARKET, BY END-USE INDUSTRY, 2023-2030 (KILOTON)

- TABLE 135 OTHER GCC COUNTRIES: ALUMINUM EXTRUSION MARKET, BY END-USE INDUSTRY, 2023-2030 (USD MILLION)

- TABLE 136 OTHER GCC COUNTRIES: ALUMINUM EXTRUSION MARKET, BY END-USE INDUSTRY, 2023-2030 (KILOTON)

- TABLE 137 SOUTH AFRICA: ALUMINUM EXTRUSION MARKET, BY END-USE INDUSTRY, 2023-2030 (USD MILLION)

- TABLE 138 SOUTH AFRICA: ALUMINUM EXTRUSION MARKET, BY END-USE INDUSTRY, 2023-2030 (KILOTON)

- TABLE 139 REST OF MIDDLE EAST & AFRICA: ALUMINUM EXTRUSION MARKET, BY END-USE INDUSTRY, 2023-2030 (USD MILLION)

- TABLE 140 REST OF MIDDLE EAST & AFRICA: ALUMINUM EXTRUSION MARKET, BY END-USE INDUSTRY, 2023-2030 (KILOTON)

- TABLE 141 LATIN AMERICA: ALUMINUM EXTRUSION MARKET, BY PRODUCT TYPE, 2023-2030 (USD MILLION)

- TABLE 142 LATIN AMERICA: ALUMINUM EXTRUSION MARKET, BY PRODUCT TYPE, 2023-2030 (KILOTON)

- TABLE 143 LATIN AMERICA: ALUMINUM EXTRUSION MARKET, BY ALLOY GRADE, 2023-2030 (USD MILLION)

- TABLE 144 LATIN AMERICA: ALUMINUM EXTRUSION MARKET, BY ALLOY GRADE, 2023-2030 (KILOTON)

- TABLE 145 LATIN AMERICA: ALUMINUM EXTRUSION MARKET, BY SURFACE FINISH, 2023-2030 (USD MILLION)

- TABLE 146 LATIN AMERICA: ALUMINUM EXTRUSION MARKET, BY SURFACE FINISH, 2023-2030 (KILOTON)

- TABLE 147 LATIN AMERICA: ALUMINUM EXTRUSION MARKET, BY END-USE INDUSTRY, 2023-2030 (USD MILLION)

- TABLE 148 LATIN AMERICA: ALUMINUM EXTRUSION MARKET, BY END-USE INDUSTRY, 2023-2030 (KILOTON)

- TABLE 149 LATIN AMERICA: ALUMINUM EXTRUSION MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 150 LATIN AMERICA: ALUMINUM EXTRUSION MARKET, BY COUNTRY, 2023-2030 (KILOTON)

- TABLE 151 BRAZIL: ALUMINUM EXTRUSION MARKET, BY END-USE INDUSTRY, 2023-2030 (USD MILLION)

- TABLE 152 BRAZIL: ALUMINUM EXTRUSION MARKET, BY END-USE INDUSTRY, 2023-2030 (KILOTON)

- TABLE 153 MEXICO: ALUMINUM EXTRUSION MARKET, BY END-USE INDUSTRY, 2023-2030 (USD MILLION)

- TABLE 154 MEXICO: ALUMINUM EXTRUSION MARKET, BY END-USE INDUSTRY, 2023-2030 (KILOTON)

- TABLE 155 REST OF LATIN AMERICA: ALUMINUM EXTRUSION MARKET, BY END-USE INDUSTRY, 2023-2030 (USD MILLION)

- TABLE 156 REST OF LATIN AMERICA: ALUMINUM EXTRUSION MARKET, BY END-USE INDUSTRY, 2023-2030 (KILOTON)

- TABLE 157 ALUMINUM EXTRUSION MARKET: KEY STRATEGIES ADOPTED BY MAJOR PLAYERS

- TABLE 158 ALUMINUM EXTRUSION MARKET: DEGREE OF COMPETITION, 2024

- TABLE 159 ALUMINUM EXTRUSION MARKET: REGION FOOTPRINT

- TABLE 160 ALUMINUM EXTRUSION MARKET: PRODUCT FOOTPRINT

- TABLE 161 ALUMINUM EXTRUSION MARKET: ALLOY GRADE FOOTPRINT

- TABLE 162 ALUMINUM EXTRUSION MARKET: SURFACE FINISH FOOTPRINT

- TABLE 163 ALUMINUM EXTRUSION MARKET: END-USE INDUSTRY FOOTPRINT

- TABLE 164 ALUMINUM EXTRUSION MARKET: DETAILED LIST OF KEY STARTUPS/SMES

- TABLE 165 ALUMINUM EXTRUSION MARKET: COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES (1/2)

- TABLE 166 ALUMINUM EXTRUSION MARKET: COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES (2/2)

- TABLE 167 ALUMINUM EXTRUSION MARKET: PRODUCT LAUNCHES, JANUARY 2020-DECEMBER 2025

- TABLE 168 ALUMINUM EXTRUSION MARKET: DEALS, JANUARY 2020-DECEMBER 2025

- TABLE 169 ALUMINUM EXTRUSION MARKET: EXPANSIONS, JANUARY 2020-DECEMBER 2025

- TABLE 170 HINDALCO INDUSTRIES LTD.: COMPANY OVERVIEW

- TABLE 171 HINDALCO INDUSTRIES LTD.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 172 HINDALCO INDUSTRIES LTD.: DEALS

- TABLE 173 HINDALCO INDUSTRIES LTD.: EXPANSIONS

- TABLE 174 ALCOA CORPORATION: COMPANY OVERVIEW

- TABLE 175 ALCOA CORPORATION: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 176 ALCOA CORPORATION: PRODUCT LAUNCHES

- TABLE 177 ALUMINIUM CORPORATION OF CHINA LIMITED: COMPANY OVERVIEW

- TABLE 178 ALUMINUM CORPORATION OF CHINA LIMITED: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 179 RUSAL: COMPANY OVERVIEW

- TABLE 180 RUSAL: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 181 KAISER ALUMINUM: COMPANY OVERVIEW

- TABLE 182 KAISER ALUMINUM: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 183 CENTURY ALUMINUM COMPANY: COMPANY OVERVIEW

- TABLE 184 CENTURY ALUMINUM COMPANY: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 185 CONSTELLIUM: COMPANY OVERVIEW

- TABLE 186 CONSTELLIUM: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 187 CONSTELLIUM: DEALS

- TABLE 188 NORSK HYDRO ASA: COMPANY OVERVIEW

- TABLE 189 NORSK HYDRO ASA: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 190 JINDAL ALUMINUM LIMITED: COMPANY OVERVIEW

- TABLE 191 JINDAL ALUMINUM LIMITED: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 192 HAMMERER ALUMINUM INDUSTRIES: COMPANY OVERVIEW

- TABLE 193 HAMMERER ALUMINUM INDUSTRIES: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 194 ALOM GROUP: COMPANY OVERVIEW

- TABLE 195 ALOM GROUP: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 196 BANCO ALUMINUM PRIVATE LIMITED: COMPANY OVERVIEW

- TABLE 197 BANCO ALUMINUM PRIVATE LIMITED: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 198 MAAN ALUMINIUM LIMITED: COMPANY OVERVIEW

- TABLE 199 MAAN ALUMINIUM LIMITED: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 200 SHENZHEN ORIENTAL TURDO IRONWARES CO., LTD: COMPANY OVERVIEW

- TABLE 201 SHENZHEN ORIENTAL TURDO IRONWARES CO., LTD: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 202 ETEM: COMPANY OVERVIEW

- TABLE 203 ETEM: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 204 ETEM: DEALS

- TABLE 205 GUANGDONG ZHENHAN SPECIAL LIGHT ALLOY CO., LTD: COMPANY OVERVIEW

- TABLE 206 ALBRAS: COMPANY OVERVIEW

- TABLE 207 YK ALUMINIUM.: COMPANY OVERVIEW

- TABLE 208 ELEANOR INDUSTRIES PVT. LTD: COMPANY OVERVIEW

- TABLE 209 ALUPCO: COMPANY OVERVIEW

- TABLE 210 ZAHIT ALUMINYUM: COMPANY OVERVIEW

- TABLE 211 ARCONIC: COMPANY OVERVIEW

- TABLE 212 HULAMIN: COMPANY OVERVIEW

- TABLE 213 GULF EXTRUSION: COMPANY OVERVIEW

- TABLE 214 BENKAM ALU EXTRUSIONS: COMPANY OVERVIEW

List of Figures

- FIGURE 1 ALUMINUM EXTRUSION MARKET SEGMENTATION AND REGIONAL SCOPE

- FIGURE 2 KEY INSIGHTS AND MARKET HIGHLIGHTS

- FIGURE 3 GLOBAL ALUMINUM EXTRUSION MARKET, 2025-2030

- FIGURE 4 MAJOR STRATEGIES ADOPTED BY KEY PLAYERS IN ALUMINUM EXTRUSION MARKET (2020-2025)

- FIGURE 5 DISRUPTIVE TRENDS IMPACTING GROWTH OF ALUMINUM EXTRUSION MARKET

- FIGURE 6 HIGH-GROWTH SEGMENTS AND EMERGING FRONTIERS IN ALUMINUM EXTRUSION MARKET, 2024

- FIGURE 7 ASIA PACIFIC TO REGISTER HIGHEST GROWTH RATE DURING FORECAST PERIOD

- FIGURE 8 HIGH DEMAND IN CONSTRUCTION & INFRASTRUCTURE TO CREATE LUCRATIVE OPPORTUNITIES FOR MARKET PLAYERS

- FIGURE 9 SOLID PROFILES SEGMENT ACCOUNTED FOR LARGEST MARKET SHARE IN 2024

- FIGURE 10 6XXX ALLOY GRADE DOMINATED ALUMINUM EXTRUSION MARKET IN 2024

- FIGURE 11 MILL-FINISHED SEGMENT LED MARKET IN 2025

- FIGURE 12 CONSTRUCTION & INFRASTRUCTURE SEGMENT WAS LARGEST IN 2025

- FIGURE 13 CHINA TO REGISTER HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 14 ALUMINUM EXTRUSION MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

- FIGURE 15 LIGHTWEIGHTING POTENTIAL OF ALUMINUM EXTRUDED PRODUCTS FOR AUTOMOTIVE INDUSTRY

- FIGURE 16 ALUMINUM EXTRUSION MARKET: PORTER'S FIVE FORCES ANALYSIS

- FIGURE 17 ALUMINUM EXTRUSION MARKET: VALUE CHAIN ANALYSIS

- FIGURE 18 ALUMINUM EXTRUSION MARKET: KEY PARTICIPANTS IN ECOSYSTEM

- FIGURE 19 ALUMINUM EXTRUSION MARKET: ECOSYSTEM ANALYSIS

- FIGURE 20 AVERAGE SELLING PRICE TREND BY REGION, 2023-2024

- FIGURE 21 IMPORT SCENARIO FOR HS CODE 760421-COMPLIANT PRODUCTS, KEY COUNTRIES, 2020-2024

- FIGURE 22 EXPORT SCENARIO FOR HS CODE 760421-COMPLIANT PRODUCTS, KEY COUNTRIES, 2020-2024

- FIGURE 23 TRENDS/DISRUPTIONS INFLUENCING CUSTOMER BUSINESS

- FIGURE 24 PATENT ANALYSIS, BY DOCUMENT TYPE, 2015-2025

- FIGURE 25 PATENT PUBLICATION TRENDS, 2015-2025

- FIGURE 26 ALUMINUM EXTRUSION MARKET: LEGAL STATUS OF PATENTS, JANUARY 2015-DECEMBER 2025

- FIGURE 27 CHINA REGISTERED HIGHEST SHARE OF PATENTS, 2015-2025

- FIGURE 28 TOP PATENT APPLICANTS, 2015-2025

- FIGURE 29 FUTURE APPLICATIONS OF ALUMINUM EXTRUSION

- FIGURE 30 ALUMINUM EXTRUSION MARKET: DECISION-MAKING FACTORS

- FIGURE 31 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS, BY END-USE INDUSTRY

- FIGURE 32 KEY BUYING CRITERIA, BY END-USE INDUSTRY

- FIGURE 33 ADOPTION BARRIERS & INTERNAL CHALLENGES

- FIGURE 34 6XXX ALLOY GRADE SEGMENT TO DOMINATE MARKET

- FIGURE 35 HOLLOW PROFILES SEGMENT TO REGISTER HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 36 MILL-FINISHED SEGMENT TO REGISTER HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 37 CONSTRUCTION & INFRASTRUCTURE SEGMENT TO LEAD MARKET DURING FORECAST PERIOD

- FIGURE 38 CHINA TO REGISTER HIGHEST GROWTH DURING FORECAST PERIOD

- FIGURE 39 NORTH AMERICA: ALUMINUM EXTRUSION MARKET SNAPSHOT

- FIGURE 40 EUROPE: ALUMINUM EXTRUSION MARKET SNAPSHOT

- FIGURE 41 ASIA PACIFIC: ALUMINUM EXTRUSION MARKET SNAPSHOT

- FIGURE 42 ALUMINUM EXTRUSION MARKET: REVENUE ANALYSIS OF KEY PLAYERS, 2020-2024

- FIGURE 43 ALUMINUM EXTRUSION MARKET SHARE ANALYSIS, 2024

- FIGURE 44 ALUMINUM EXTRUSION MARKET: BRAND/PRODUCT COMPARISON

- FIGURE 45 ALUMINUM EXTRUSION MARKET: COMPANY EVALUATION MATRIX (KEY PLAYERS), 2024

- FIGURE 46 ALUMINUM EXTRUSION MARKET: COMPANY FOOTPRINT

- FIGURE 47 ALUMINUM EXTRUSION MARKET: COMPANY EVALUATION MATRIX (STARTUPS/SMES), 2024

- FIGURE 48 ALUMINUM EXTRUSION MARKET: EV/EBITDA OF KEY MANUFACTURERS

- FIGURE 49 ALUMINUM EXTRUSION MARKET: YEAR-TO-DATE (YTD) PRICE TOTAL RETURN AND 5-YEAR STOCK BETA OF KEY MANUFACTURERS

- FIGURE 50 HINDALCO INDUSTRIES LTD.: COMPANY SNAPSHOT

- FIGURE 51 ALCOA CORPORATION: COMPANY SNAPSHOT

- FIGURE 52 ALUMINIUM CORPORATION OF CHINA LIMITED: COMPANY SNAPSHOT

- FIGURE 53 RUSAL: COMPANY SNAPSHOT

- FIGURE 54 KAISER ALUMINUM: COMPANY SNAPSHOT

- FIGURE 55 CENTURY ALUMINUM COMPANY: COMPANY SNAPSHOT

- FIGURE 56 CONSTELLIUM: COMPANY SNAPSHOT

- FIGURE 57 NORSK HYDRO ASA: COMPANY SNAPSHOT

- FIGURE 58 MAAN ALUMINIUM: COMPANY SNAPSHOT

- FIGURE 59 ALUMINUM EXTRUSION MARKET: RESEARCH DESIGN

- FIGURE 60 ALUMINUM EXTRUSION MARKET: BOTTOM-UP AND TOP-DOWN APPROACH

- FIGURE 61 ALUMINUM EXTRUSION MARKET: DATA TRIANGULATION

铝挤型市场:2026-2032年全球市场预测(依铝种类、原料类型、製造流程、产品形状、公司规模、截面形状、型材种类及应用划分)

铝挤型市场:2026-2032年全球市场预测(依铝种类、原料类型、製造流程、产品形状、公司规模、截面形状、型材种类及应用划分) 铝挤型市场规模、份额、趋势和预测:按产品类型、合金类型、最终用途产业和地区划分,2026-2034年

铝挤型市场规模、份额、趋势和预测:按产品类型、合金类型、最终用途产业和地区划分,2026-2034年 2026年全球非标铝型材市场报告铝矿石及精矿市场:2026-2032年全球市场预测(依产品类型、等级、通路、应用及最终用途产业划分)

2026年全球非标铝型材市场报告铝矿石及精矿市场:2026-2032年全球市场预测(依产品类型、等级、通路、应用及最终用途产业划分) 2026-2030年全球铝挤型市场

2026-2030年全球铝挤型市场 全球铝挤型市场规模、份额、趋势和成长分析报告(2026-2034)日本铝挤压市场规模、份额、趋势和预测:按产品类型、合金类型、最终用途行业和地区划分,2026-2034年2026年全球铝挤型市场报告铝挤型服务市场按服务类型、合金类型、挤压方法、最终用途产业和通路划分-2026-2032年全球预测

全球铝挤型市场规模、份额、趋势和成长分析报告(2026-2034)日本铝挤压市场规模、份额、趋势和预测:按产品类型、合金类型、最终用途行业和地区划分,2026-2034年2026年全球铝挤型市场报告铝挤型服务市场按服务类型、合金类型、挤压方法、最终用途产业和通路划分-2026-2032年全球预测 铝挤型市场规模、份额和成长分析(按合金类型、产品、应用、类型和地区划分)-2026-2033年产业预测

铝挤型市场规模、份额和成长分析(按合金类型、产品、应用、类型和地区划分)-2026-2033年产业预测