|

市场调查报告书

商品编码

1950788

全球线控驾驶市场(至2032年):依类型(线控转向、线传煞车、线传换檔、线控泊车、线控油门)、自动驾驶汽车及地区划分Drive By Wire Market by Type (Steer by Wire, Brake by Wire, Shift by Wire, Park by Wire, Throttle by Wire), Autonomous Vehicle, and Region - Global Forecast To 2032 |

||||||

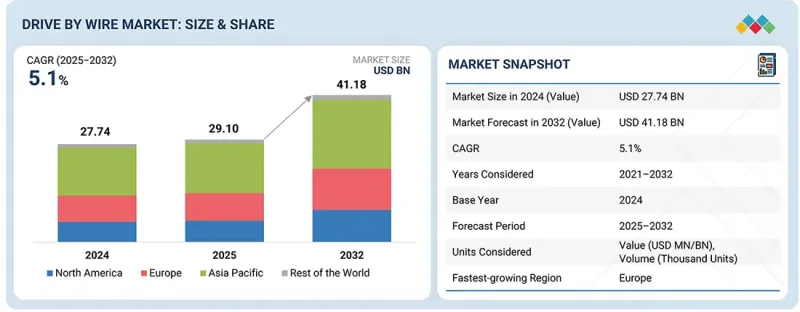

预计线控驾驶市场将从 2025 年的 291 亿美元成长到 2032 年的 411.8 亿美元,复合年增长率为 5.1%。

由于线传换檔和线控油门对监管合规性的要求较低,并且在功能、成本和架构方面具有直接优势,预计它们仍将是应用最广泛的线控驱动应用。

| 调查范围 | |

|---|---|

| 调查期 | 2021-2032 |

| 基准年 | 2024 |

| 预测期 | 2025-2032 |

| 单元 | 金额(美元),数量 |

| 部分 | 线控转向、线传煞车、线传换檔、线控驻车、线控油门、应用 |

| 目标区域 | 北美、亚太地区、欧洲及其他地区 |

线控油门(Throttle-by-wire)技术应用于所有内燃机、混合动力汽车和电动车,以满足排放气体要求、扭矩管理、ADAS(高级驾驶动力传动系统的兼容性。线控换檔(线传换檔)技术则主要由自动变速箱和电动车主导。电子换檔技术能够实现紧凑的车身结构、简化的内装设计、提升安全性,并与自动泊车和遥控功能无缝整合。这些系统为汽车製造商(OEM)提供了一条快速实现软体定义车辆开发和平台标准化的途径,同时避免了诸如製造成本增加、复杂的安全备份以及各国认证等挑战。

“纯电动车(BEV)将对线控驱动系统产生最大的需求。”

由于纯电动车 (BEV) 不需要引擎、机械齿轮传动装置或真空煞车系统,电子控制将成为标准配置,从而对线控驱动系统的需求达到顶峰。与内燃机汽车相比,线控油门、线传煞车和线传换檔更容易整合到平底车身结构和集中式电气系统中。纯电动车的技术进步进一步推动了对线控驱动系统的需求。纯电动车架构支援全电子製动,从而实现精准的煞车控制和高效的能量回收煞车。这些车辆的集中式运算和分区式电子电气架构要求转向、煞车、油门和换檔操作由软体功能而非机械连接来控制。此外,纯电动车正被开发为软体定义平台,其驾驶模式、能量管理、ADAS 功能等均可透过空中下载 (OTA) 进行更新——而这只有线控系统才能实现。这种平台层面的变革使得机械控制与纯电动车的设计目标不符,加速了线控驱动系统的普及。

“预计欧洲将成为线控驾驶系统成长最快的市场。”

预计在预测期内,欧洲将迎来最快的市场成长,这主要得益于法规主导的电气化进程以及高阶OEM厂商的领先地位。此区域线控驱动技术的快速普及,源自于在高度限制的封装环境下对平台架构优化的需求,以及对软体定义功能安全和电子煞车系统的强大製度支援。这种环境有利于线传煞车架构的早期大规模应用。同时,线控转向技术的普及将采取选择性策略,只有在封装、碰撞整合和系统级优势足以抵消额外的检验和冗余复杂性时,才会推进。从市场角度来看,欧洲在模组化车辆架构和以软体为中心的安全性检验的主导地位,预计将在中期内推动线控驱动系统实现高于平均水平的增长率。 OEM厂商的投资可能会优先考虑线传煞车平台作为底层技术,从而在量产领域实现大规模应用,同时满足法规要求并实现平台復用目标。

本报告调查了全球线控驱动市场,并提供了市场概况、影响市场成长的各种因素分析、技术和专利趋势、法律制度、案例研究、市场规模趋势和预测、按各个细分市场、地区/主要国家进行的详细分析、竞争格局以及主要企业的概况。

目录

第一章 引言

第二章执行摘要

第三章重要考察

第四章 市场概览

- 市场动态

- 司机

- 抑制因素

- 机会

- 任务

- 未满足的需求和閒置频段

- 与相关市场和不同产业相关的跨领域机会

- 一级/二级/三级公司的策略性倡议

第五章 产业趋势

- 生态系分析

- 影响客户业务的趋势/干扰因素

- 案例研究分析

- 定价分析

- 供应链分析

- 成本效益分析

- 重大会议和活动

第六章 线控技术的集成

- 智慧型致动器

- 概述

- 主要供应商

- 电动机

- 概述

- 主要供应商

- 整合底盘系统

- 概述

- 主要供应商

- 与ADAS/自动驾驶的协同作用

- 传统系统和线控系统

- 线控技术的特性分析

第七章:技术进步、人工智慧影响、专利、创新与未来应用

- 主要技术

- 先进感测器技术

- 电气/电子架构

- 线控网路中的网路安全

- 人工智慧/生成式人工智慧的影响

- 专利分析

- 未来应用

- 与ADAS和自动驾驶平台集成

第八章:监理环境

- 地方法规和合规性

第九章:按推进系统类别和零件分類的线传煞车

- 类型

- 踏板线传煞车

- 电液线传煞车

- 线传煞车

- 传统煞车系统和线传煞车系统

- 主要特点

- OEM厂商的市场渗透率

- 市场规模及预测

- 按ICE类型

- 按电动汽车类型

- 依感测器类型

- 按组件

- 关键见解

第十章 线控泊车:依促销类别和组件划分

- 类型

- 线控泊车

- 冗余的线下停车系统

- 电动驻煞车系统

- 传统停车系统与线控停车系统

- 主要特点

- OEM厂商的市场渗透率

- 市场规模及预测

- 按ICE类型

- 按电动汽车类型

- 依感测器类型

- 按组件

- 关键见解

第十一章 依推进系统类别和部件分類的线传换檔

- 类型

- 电子换檔器

- 线传换檔按钮

- 线传换檔

- 传统换檔系统与线传换檔系统

- 主要特点

- OEM厂商的市场渗透率

- 市场规模及预测

- 按ICE类型

- 按电动汽车类型

- 依感测器类型

- 按组件

- 关键见解

第十二章 线控转向:依推进系统类别与零件划分

- 类型

- 小齿轮

- 柱子

- 架子

- 传统转向系统与线控转向系统

- 主要特点

- OEM厂商的市场渗透率

- 市场规模及预测

- 按ICE类型

- 按电动汽车类型

- 依感测器类型

- 按组件

- 关键见解

第十三章 依推进系统分类及零件分類的线控油门

- 类型

- 线控踏板油门

- 马达扭矩线控油门

- 驾驶模式自我调整电子油门

- 传统油门系统和线控油门系统

- 主要特点

- OEM厂商的市场渗透率

- 市场规模及预测

- 按ICE类型

- 按电动汽车类型

- 依感测器类型

- 按组件

- 关键见解

第十四章 按应用程式分類的自动驾驶汽车线控市场

- L2级自动驾驶车辆

- L3级自动驾驶车辆

- L4/L5级自动驾驶车辆

- 关键见解

第十五章 线控驾驶市场区域概览

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 泰国

- 其他的

- 欧洲

- 德国

- 法国

- 俄罗斯

- 西班牙

- 英国

- 土耳其

- 义大利

- 其他的

- 北美洲

- 加拿大

- 墨西哥

- 我们

- 世界其他地区

- 巴西

- 伊朗

- 阿根廷

- 南非

- 其他的

第十六章 竞争格局

- 主要参与企业的策略/优势

- 市占率分析

- 收入分析

- 估值和财务指标

- 公司评估矩阵:主要企业

- 公司估值矩阵:新兴企业/中小企业

- 竞争场景

第十七章:公司简介

- 主要企业

- ROBERT BOSCH GMBH

- CONTINENTAL AG

- ZF FRIEDRICHSHAFEN AG

- NEXTEER AUTOMOTIVE

- HITACHI, LTD.

- HL MANDO CORP.

- JTEKT CORPORATION

- THYSSENKRUPP AG

- FICOSA INTERNATIONAL SA

- KONGSBERG AUTOMOTIVE

- CURTISS-WRIGHT CORPORATION

- 其他公司

- SCHAEFFLER TECHNOLOGIES AG & CO. KG

- KSR INTERNATIONAL INC.

- CTS CORPORATION

- HYUNDAI MOBIS

- FORVIA

- NIDEC CORPORATION

- NISSAN CORPORATION

- INFINEON TECHNOLOGIES AG

- BREMBO SPA

- DENSO CORPORATION

- NXP SEMICONDUCTORS NV

- SNT MOTIV CO., LTD.

- LEM EUROPE GMBH

- ALLIED MOTION TECHNOLOGIES INC.

- DURA AUTOMOTIVE SYSTEMS

第十八章调查方法

第十九章附录

The drive by wire market is projected to reach USD 41.18 billion by 2032, from USD 29.10 billion in 2025, with a CAGR of 5.1%. Shift by wire and throttle by wire are expected to remain the most widely adopted drive by wire applications because they deliver immediate functional, cost, and architectural benefits with low regulatory compliance requirements.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Units Considered | Value (USD MN/BN), Volume (Thousand Units) |

| Segments | Steer by Wire, Brake by Wire, Shift by Wire, Park by Wire, Throttle by Wire, Application |

| Regions covered | North America, Asia Pacific, Europe, Rest of the World |

Throttle by wire is used across ICE, hybrid, and electric vehicles due to emission control requirements, torque management, ADAS integration, and to ensure compatibility with the electronic powertrain. Shift by wire adoption is led by automatic and electric vehicles, where electronic gear selection enables compact packaging, simplified interiors, improved safety, and seamless integration with autonomous parking and remote-control features. Together, these systems offer OEMs the fastest path to developing software-defined vehicles and platform standardization, while avoiding higher manufacturing costs, complex safety backups, and country-specific certifications.

"BEVs are expected to generate the highest demand for drive by wire systems."

BEVs are expected to generate the highest demand for drive by wire systems, as they lack engines, mechanical gear linkages, or vacuum-based brake systems, making electronic control the default choice for these vehicles. Throttle by wire, brake by wire, and shift by wire can be integrated easily into flat-floor architectures and centralized electrical systems than in ICE-derived vehicles. Technological changes in BEVs are further creating demand for drive by wire systems. BEV architectures support fully electronic braking, enabling accurate brake control and efficient regenerative braking blending. Centralized computing and zonal E/E architectures in these vehicles require steering, braking, throttle, and shifting to be controlled as software functions rather than mechanical linkages. Additionally, BEVs are developed as software-defined platforms, with drive modes, energy management, and ADAS features updated over the air, which is only feasible with by-wire systems. These platform-level changes make mechanical controls incompatible with BEVs' design goals, accelerating drive by wire adoption.

"Europe is expected to be the fastest-growing market for drive by wire systems."

Europe is expected to see the fastest growth in the drive by wire market during the forecast period, driven by regulation-driven electrification and premium OEM leadership. The region's rapid adoption of drive by wire is primarily driven by the need to optimize platform architectures within tightly constrained packaging environments and by strong institutional readiness for software-defined functional safety and electronically controlled braking systems. This environment supports earlier large-scale deployment of brake by wire architectures, with steer by wire adoption advancing selectively where packaging, crash integration, and system-level benefits justify the added validation and redundancy complexity. From a market-outlook perspective, Europe's leadership in modular vehicle architectures and software-centric safety validation is expected to translate into above-average growth rates for drive by wire systems over the medium term. OEM investments are likely to prioritize brake by wire platforms as a foundation technology, enabling large-scale deployment across high-volume segments while supporting regulatory compliance and platform reuse objectives.

In-depth interviews were conducted with CEOs, marketing directors, other innovation and strategy directors, and executives from various key organizations operating in the drive by wire market.

- By Company Type: Supply-side - 70%, Demand-side - 30%

- By Designation: C level - 25%, Director Level - 30%, Others - 45%

- By Region: Asia Pacific - 55%, Europe - 15%, North America - 20%, Rest of the World - 10%

Research Coverage

The report details the drivers, restraints, opportunities, and challenges in the drive by wire market and forecasts the market through 2032. It also provides a qualitative and quantitative description of different market segments. The report provides a detailed market overview across four regions: North America, Europe, Asia Pacific, and the Rest of the World.

Key Benefits of Buying this Report:

- The report will help market leaders/new entrants with information on the closest approximations of revenue numbers for the overall drive by wire market and its subsegments.

- This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies.

- The report will also help stakeholders understand the market pulse and provide information on key market drivers, restraints, challenges, and opportunities.

The report provides insight into the following pointers:

- Analysis of key drivers (shift toward software-defined vehicle architectures, high operational accuracy and reduced mechanical losses, electrification of commercial and public transport fleets) restraints (legal liability in absence of mature fail-operational precedents, threat of cyberattacks and compliance costs), opportunities (Integration with AI, V2X, and OTA-enabled safety functions, advancements in autonomous vehicles), and challenges (integration challenges in off-highway equipment, electronic failures and rapid developments in automotive electronics)

- Product Development/Innovation: Detailed insights into upcoming technologies and R&D activities in the drive by wire market

- Market Development: Comprehensive information about lucrative markets across varied regions

- Market Diversification: Exhaustive information about untapped geographies, recent developments, and investments in the drive by wire market

- Competitive Assessment: In-depth assessment of market share, growth strategies, and product offerings of leading players, such as Robert Bosch GmbH (Germany), ZF Friedrichshafen AG (Germany), Continental AG (Germany), Nexteer Automotive (US), and Curtiss-Wright Corporation (US)

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 UNIT CONSIDERED

- 1.6 STAKEHOLDERS

- 1.7 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN DRIVE BY WIRE MARKET

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN DRIVE BY WIRE MARKET

- 3.2 L2 AUTONOMOUS VEHICLE DRIVE BY WIRE MARKET, BY APPLICATION

- 3.3 THROTTLE BY WIRE MARKET, BY ICE VEHICLE TYPE

- 3.4 THROTTLE BY WIRE MARKET, BY EV TYPE

- 3.5 BRAKE BY WIRE MARKET, BY ICE VEHICLE TYPE

- 3.6 BRAKE BY WIRE MARKET, BY EV TYPE

- 3.7 STEER BY WIRE MARKET, BY ICE VEHICLE TYPE

- 3.8 STEER BY WIRE MARKET, BY EV TYPE

- 3.9 SHIFT BY WIRE MARKET, BY ICE VEHICLE TYPE

- 3.10 SHIFT BY WIRE MARKET, BY EV TYPE

- 3.11 PARK BY WIRE MARKET, BY ICE VEHICLE TYPE

- 3.12 PARK BY WIRE MARKET, BY EV TYPE

- 3.13 DRIVE BY WIRE MARKET, BY REGION

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Transition to software-defined vehicle architectures

- 4.2.1.1.1 Shift toward zonal architectures

- 4.2.1.2 High operational accuracy and reduced mechanical losses

- 4.2.1.3 Electrification of public transport and commercial fleets

- 4.2.1.1 Transition to software-defined vehicle architectures

- 4.2.2 RESTRAINTS

- 4.2.2.1 Legal liability due to absence of mature fail-operational precedents

- 4.2.2.2 Threat of cyberattacks and compliance costs

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Integration with AI, V2X, and OTA-enabled safety functions

- 4.2.3.2 Advancements in autonomous vehicles

- 4.2.4 CHALLENGES

- 4.2.4.1 Integration challenges in off-highway equipment

- 4.2.4.2 Electronic failures and rapid developments in automotive electronics

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 ECOSYSTEM ANALYSIS

- 5.1.1 RAW MATERIAL SUPPLIERS

- 5.1.2 ACTUATOR AND SENSOR MANUFACTURERS

- 5.1.3 TIER-1 SUPPLIERS/COMPONENT MANUFACTURERS

- 5.1.4 DISTRIBUTORS

- 5.1.5 OEMS

- 5.2 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.3 CASE STUDY ANALYSIS

- 5.3.1 FKA'S STEER BY WIRE SYSTEMS

- 5.3.2 CONTINENTAL'S MK C1 INTELLIGENT BRAKING SYSTEM

- 5.3.3 NEXTEER AUTOMOTIVE'S STEER BY WIRE SYSTEM

- 5.4 PRICING ANALYSIS

- 5.5 SUPPLY CHAIN ANALYSIS

- 5.6 COST-BENEFIT ANALYSIS

- 5.6.1 THROTTLE BY WIRE

- 5.6.2 SHIFT BY WIRE

- 5.6.3 PARK BY WIRE

- 5.6.4 BRAKE BY WIRE

- 5.6.5 STEER BY WIRE

- 5.7 KEY CONFERENCES AND EVENTS

6 INTEGRATION OF BY-WIRE TECHNOLOGIES

- 6.1 SMART ACTUATORS

- 6.1.1 OVERVIEW

- 6.1.2 KEY SUPPLIERS

- 6.2 ELECTRIC MOTORS

- 6.2.1 OVERVIEW

- 6.2.2 KEY SUPPLIERS

- 6.3 INTEGRATED CHASSIS SYSTEMS

- 6.3.1 OVERVIEW

- 6.3.2 KEY SUPPLIERS

- 6.4 SYNERGIES WITH ADAS/AUTONOMY

- 6.5 TRADITIONAL SYSTEMS VS. BY-WIRE SYSTEMS

- 6.6 FEATURE ANALYSIS OF BY-WIRE TECHNOLOGIES

7 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 7.1 KEY TECHNOLOGIES

- 7.1.1 ADVANCED SENSOR TECHNOLOGIES

- 7.1.2 ELECTRICAL/ELECTRONIC ARCHITECTURES

- 7.1.3 CYBERSECURITY IN DRIVE BY WIRE NETWORKS

- 7.2 IMPACT OF AI/GEN AI

- 7.3 PATENT ANALYSIS

- 7.4 FUTURE APPLICATIONS

- 7.4.1 INTEGRATION WITH ADAS AND AUTONOMOUS DRIVING PLATFORMS

8 REGULATORY LANDSCAPE

- 8.1 REGIONAL REGULATIONS AND COMPLIANCE

- 8.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 8.1.2 DRIVE BY WIRE STANDARDS, BY COUNTRY

9 BRAKE BY WIRE, BY PROPULSION AND COMPONENT

- 9.1 INTRODUCTION

- 9.2 TYPES

- 9.2.1 PEDAL-BASED BRAKE BY WIRE

- 9.2.2 ELECTRO-HYDRAULIC BRAKE BY WIRE

- 9.2.3 ELECTRO-MECHANICAL BRAKE BY WIRE

- 9.3 CONVENTIONAL BRAKING SYSTEMS VS. BRAKE BY WIRE SYSTEMS

- 9.4 KEY FEATURES

- 9.5 MARKET UPTAKE - BY OEM

- 9.6 MARKET SIZING AND FORECAST

- 9.6.1 BY ICE VEHICLE TYPE

- 9.6.1.1 Passenger car

- 9.6.1.2 Light commercial vehicle

- 9.6.1.3 Truck

- 9.6.1.4 Bus

- 9.6.2 BY EV TYPE

- 9.6.2.1 BEV

- 9.6.2.2 PHEV

- 9.6.2.3 FCEV

- 9.6.3 BY SENSOR TYPE

- 9.6.3.1 Brake pedal sensor

- 9.6.4 BY COMPONENT

- 9.6.4.1 Actuator

- 9.6.4.2 ECU

- 9.6.1 BY ICE VEHICLE TYPE

- 9.7 PRIMARY INSIGHTS

10 PARK BY WIRE, BY PROPULSION AND COMPONENT

- 10.1 INTRODUCTION

- 10.2 TYPES

- 10.2.1 TRANSMISSION PARK BY WIRE

- 10.2.2 REDUNDANT PARK BY WIRE

- 10.2.3 ELECTRIC PARKING BRAKE

- 10.3 CONVENTIONAL PARKING SYSTEMS VS. PARK BY WIRE SYSTEMS

- 10.4 KEY FEATURES

- 10.5 MARKET UPTAKE - BY OEM

- 10.6 MARKET SIZING AND FORECAST

- 10.6.1 BY ICE VEHICLE TYPE

- 10.6.1.1 Passenger car

- 10.6.1.2 Light commercial vehicle

- 10.6.1.3 Truck

- 10.6.1.4 Bus

- 10.6.2 BY EV TYPE

- 10.6.2.1 BEV

- 10.6.2.2 PHEV

- 10.6.2.3 FCEV

- 10.6.3 BY SENSOR TYPE

- 10.6.3.1 Park sensor

- 10.6.4 BY COMPONENT

- 10.6.4.1 Actuator

- 10.6.4.2 ECU

- 10.6.4.3 Parking pawl

- 10.6.1 BY ICE VEHICLE TYPE

- 10.7 PRIMARY INSIGHTS

11 SHIFT BY WIRE, BY PROPULSION AND COMPONENT

- 11.1 INTRODUCTION

- 11.2 TYPES

- 11.2.1 ELECTRONIC GEAR SELECTOR

- 11.2.2 PUSH-BUTTON SHIFT BY WIRE

- 11.2.3 LEVER-BASED SHIFT BY WIRE

- 11.3 CONVENTIONAL SHIFTING SYSTEMS VS. SHIFT BY WIRE SYSTEMS

- 11.4 KEY FEATURES

- 11.5 MARKET UPTAKE - BY OEM

- 11.6 MARKET SIZING AND FORECAST

- 11.6.1 BY ICE VEHICLE TYPE

- 11.6.1.1 Passenger car

- 11.6.1.2 Light commercial vehicle

- 11.6.1.3 Truck

- 11.6.1.4 Bus

- 11.6.2 BY EV TYPE

- 11.6.2.1 BEV

- 11.6.2.2 PHEV

- 11.6.2.3 FCEV

- 11.6.3 BY SENSOR TYPE

- 11.6.3.1 Gear shift position sensor

- 11.6.4 BY COMPONENT

- 11.6.4.1 Actuator

- 11.6.4.2 ECU

- 11.6.4.3 ETCU

- 11.6.1 BY ICE VEHICLE TYPE

- 11.7 PRIMARY INSIGHTS

12 STEER BY WIRE, BY PROPULSION AND COMPONENT

- 12.1 INTRODUCTION

- 12.2 TYPES

- 12.2.1 PINION

- 12.2.2 COLUMN

- 12.2.3 RACK

- 12.3 CONVENTIONAL STEERING SYSTEMS VS. STEER BY WIRE SYSTEMS

- 12.4 KEY FEATURES

- 12.5 MARKET UPTAKE - BY OEM

- 12.6 MARKET SIZING AND FORECAST

- 12.6.1 BY ICE VEHICLE TYPE

- 12.6.1.1 Passenger car

- 12.6.1.2 Light commercial vehicle

- 12.6.1.3 Truck

- 12.6.1.4 Bus

- 12.6.2 BY EV TYPE

- 12.6.2.1 BEV

- 12.6.2.2 PHEV

- 12.6.2.3 FCEV

- 12.6.3 BY SENSOR TYPE

- 12.6.3.1 Hand wheel angle sensor

- 12.6.3.2 Pinion angle sensor

- 12.6.4 BY COMPONENT

- 12.6.4.1 Actuator

- 12.6.4.2 ECU

- 12.6.4.3 Feedback motor

- 12.6.1 BY ICE VEHICLE TYPE

- 12.7 PRIMARY INSIGHTS

13 THROTTLE BY WIRE, BY PROPULSION AND COMPONENT

- 13.1 INTRODUCTION

- 13.2 TYPES

- 13.2.1 PEDAL-BASED THROTTLE BY WIRE

- 13.2.2 MOTOR-TORQUE THROTTLE BY WIRE

- 13.2.3 DRIVE-MODE ADAPTIVE THROTTLE BY WIRE

- 13.3 CONVENTIONAL THROTTLE SYSTEMS VS. THROTTLE BY WIRE SYSTEMS

- 13.4 KEY FEATURES

- 13.5 MARKET UPTAKE - BY OEM

- 13.6 MARKET SIZING AND FORECAST

- 13.6.1 BY ICE VEHICLE TYPE

- 13.6.1.1 Passenger car

- 13.6.1.2 Light commercial vehicle

- 13.6.1.3 Truck

- 13.6.1.4 Bus

- 13.6.2 BY EV TYPE

- 13.6.2.1 BEV

- 13.6.2.2 PHEV

- 13.6.2.3 FCEV

- 13.6.3 BY SENSOR TYPE

- 13.6.3.1 Throttle pedal sensor

- 13.6.3.2 Throttle position sensor

- 13.6.4 BY COMPONENT

- 13.6.4.1 Actuator

- 13.6.4.2 ECU

- 13.6.4.3 ECM

- 13.6.4.4 ETCM

- 13.6.1 BY ICE VEHICLE TYPE

- 13.7 PRIMARY INSIGHTS

14 AUTONOMOUS VEHICLE DRIVE BY WIRE MARKET, BY APPLICATION

- 14.1 INTRODUCTION

- 14.2 L2 AUTONOMOUS VEHICLE

- 14.3 L3 AUTONOMOUS VEHICLE

- 14.4 L4/L5 AUTONOMOUS VEHICLE

- 14.5 PRIMARY INSIGHTS

15 DRIVE BY WIRE MARKET, BY REGION

- 15.1 INTRODUCTION

- 15.2 ASIA PACIFIC

- 15.2.1 CHINA

- 15.2.1.1 Growing popularity of electronic vehicle control to drive market

- 15.2.2 INDIA

- 15.2.2.1 Rising penetration of automatic transmissions to drive market

- 15.2.3 JAPAN

- 15.2.3.1 Product innovations by domestic manufacturers to drive market

- 15.2.4 SOUTH KOREA

- 15.2.4.1 Regulatory and technology alignment to drive market

- 15.2.5 THAILAND

- 15.2.5.1 Surge in EV sales and localization of electronics to drive market

- 15.2.6 REST OF ASIA PACIFIC

- 15.2.1 CHINA

- 15.3 EUROPE

- 15.3.1 GERMANY

- 15.3.1.1 Strong premium vehicle base and presence of major by-wire suppliers to drive market

- 15.3.2 FRANCE

- 15.3.2.1 High demand for premium vehicles and stringent emission rules to drive market

- 15.3.3 RUSSIA

- 15.3.3.1 Rise of premium vehicle sales to drive market

- 15.3.4 SPAIN

- 15.3.4.1 Increasing consumer demand for luxury brands to drive market

- 15.3.5 UK

- 15.3.5.1 Mature automotive R&D ecosystem to drive market

- 15.3.6 TURKEY

- 15.3.6.1 Expanding presence of foreign luxury automakers to drive market

- 15.3.7 ITALY

- 15.3.7.1 Ongoing technology partnerships to drive market

- 15.3.8 REST OF EUROPE

- 15.3.1 GERMANY

- 15.4 NORTH AMERICA

- 15.4.1 CANADA

- 15.4.1.1 Elevated demand for premium and advanced vehicles to drive market

- 15.4.2 MEXICO

- 15.4.2.1 Robust cross-border supply chains to drive market

- 15.4.3 US

- 15.4.3.1 Strong technology adoption to drive market

- 15.4.1 CANADA

- 15.5 REST OF THE WORLD

- 15.5.1 BRAZIL

- 15.5.1.1 Localization of advanced components and export-oriented production to drive market

- 15.5.2 IRAN

- 15.5.2.1 Preference for manual transmissions to impede market

- 15.5.3 ARGENTINA

- 15.5.3.1 Reduced import duties to drive market

- 15.5.4 SOUTH AFRICA

- 15.5.4.1 New premium vehicle launches to drive market

- 15.5.5 OTHERS

- 15.5.1 BRAZIL

16 COMPETITIVE LANDSCAPE

- 16.1 INTRODUCTION

- 16.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2021-2025

- 16.3 MARKET SHARE ANALYSIS, 2024

- 16.4 REVENUE ANALYSIS, 2020-2024

- 16.5 COMPANY VALUATION AND FINANCIAL METRICS

- 16.6 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 16.6.1 STARS

- 16.6.2 EMERGING LEADERS

- 16.6.3 PERVASIVE PLAYERS

- 16.6.4 PARTICIPANTS

- 16.6.5 COMPANY FOOTPRINT

- 16.6.5.1 Company footprint

- 16.6.5.2 Region footprint

- 16.6.5.3 Component footprint

- 16.6.5.4 Application footprint

- 16.7 COMPANY EVALUATION MATRIX: START-UPS/SMES, 2024

- 16.7.1 PROGRESSIVE COMPANIES

- 16.7.2 RESPONSIVE COMPANIES

- 16.7.3 DYNAMIC COMPANIES

- 16.7.4 STARTING BLOCKS

- 16.7.5 COMPETITIVE BENCHMARKING

- 16.7.5.1 List of start-ups/SMEs

- 16.7.5.2 Competitive benchmarking of start-ups/SMEs

- 16.8 COMPETITIVE SCENARIO

- 16.8.1 PRODUCT LAUNCHES/DEVELOPMENTS

- 16.8.2 DEALS

- 16.8.3 EXPANSIONS

- 16.8.4 OTHER DEVELOPMENTS

17 COMPANY PROFILES

- 17.1 KEY PLAYERS

- 17.1.1 ROBERT BOSCH GMBH

- 17.1.1.1 Business overview

- 17.1.1.2 Products offered

- 17.1.1.3 Recent developments

- 17.1.1.3.1 Product launches/developments

- 17.1.1.3.2 Deals

- 17.1.1.3.3 Other deveopments

- 17.1.1.4 MnM view

- 17.1.1.4.1 Key strengths/Right to win

- 17.1.1.4.2 Strategic choices

- 17.1.1.4.3 Weaknesses and competitive threats

- 17.1.2 CONTINENTAL AG

- 17.1.2.1 Business overview

- 17.1.2.2 Products offered

- 17.1.2.3 Recent developments

- 17.1.2.3.1 Product launches/developments

- 17.1.2.3.2 Deals

- 17.1.2.3.3 Expansions

- 17.1.2.3.4 Other deveopments

- 17.1.2.4 MnM view

- 17.1.2.4.1 Key strengths/Right to win

- 17.1.2.4.2 Strategic choices

- 17.1.2.4.3 Weaknesses and competitive threats

- 17.1.3 ZF FRIEDRICHSHAFEN AG

- 17.1.3.1 Business overview

- 17.1.3.2 Products offered

- 17.1.3.3 Recent developments

- 17.1.3.3.1 Product launches/developments

- 17.1.3.3.2 Deals

- 17.1.3.3.3 Other deveopments

- 17.1.3.4 MnM view

- 17.1.3.4.1 Key strengths/Right to win

- 17.1.3.4.2 Strategic choices

- 17.1.3.4.3 Weaknesses and competitive threats

- 17.1.4 NEXTEER AUTOMOTIVE

- 17.1.4.1 Business overview

- 17.1.4.2 Products offered

- 17.1.4.3 Recent developments

- 17.1.4.3.1 Product launches/developments

- 17.1.4.3.2 Deals

- 17.1.4.3.3 Expansions

- 17.1.4.4 MnM view

- 17.1.4.4.1 Key strengths/Right to win

- 17.1.4.4.2 Strategic choices

- 17.1.4.4.3 Weaknesses and competitive threats

- 17.1.5 HITACHI, LTD.

- 17.1.5.1 Business overview

- 17.1.5.2 Products offered

- 17.1.5.3 Recent developments

- 17.1.5.3.1 Product launches/developments

- 17.1.5.3.2 Deals

- 17.1.5.4 MnM view

- 17.1.5.4.1 Key strengths/Right to win

- 17.1.5.4.2 Strategic choices

- 17.1.5.4.3 Weaknesses and competitive threats

- 17.1.6 HL MANDO CORP.

- 17.1.6.1 Business overview

- 17.1.6.2 Products offered

- 17.1.6.3 Recent developments

- 17.1.6.3.1 Deals

- 17.1.6.3.2 Other developments

- 17.1.7 JTEKT CORPORATION

- 17.1.7.1 Business overview

- 17.1.7.2 Products offered

- 17.1.7.3 Recent developments

- 17.1.7.3.1 Product launches/developments

- 17.1.7.3.2 Deals

- 17.1.7.3.3 Expansions

- 17.1.7.3.4 Other developments

- 17.1.8 THYSSENKRUPP AG

- 17.1.8.1 Business overview

- 17.1.8.2 Products offered

- 17.1.8.3 Recent developments

- 17.1.8.3.1 Deals

- 17.1.9 FICOSA INTERNATIONAL SA

- 17.1.9.1 Business overview

- 17.1.9.2 Products offered

- 17.1.10 KONGSBERG AUTOMOTIVE

- 17.1.10.1 Business overview

- 17.1.10.2 Products offered

- 17.1.10.3 Recent developments

- 17.1.10.3.1 Other developments

- 17.1.11 CURTISS-WRIGHT CORPORATION

- 17.1.11.1 Business overview

- 17.1.11.2 Products offered

- 17.1.11.3 Recent developments

- 17.1.11.3.1 Product launches/developments

- 17.1.11.3.2 Deals

- 17.1.11.3.3 Expansions

- 17.1.11.3.4 Other deveopments

- 17.1.1 ROBERT BOSCH GMBH

- 17.2 OTHER PLAYERS

- 17.2.1 SCHAEFFLER TECHNOLOGIES AG & CO. KG

- 17.2.2 KSR INTERNATIONAL INC.

- 17.2.3 CTS CORPORATION

- 17.2.4 HYUNDAI MOBIS

- 17.2.5 FORVIA

- 17.2.6 NIDEC CORPORATION

- 17.2.7 NISSAN CORPORATION

- 17.2.8 INFINEON TECHNOLOGIES AG

- 17.2.9 BREMBO S.P.A.

- 17.2.10 DENSO CORPORATION

- 17.2.11 NXP SEMICONDUCTORS NV

- 17.2.12 SNT MOTIV CO., LTD.

- 17.2.13 LEM EUROPE GMBH

- 17.2.14 ALLIED MOTION TECHNOLOGIES INC.

- 17.2.15 DURA AUTOMOTIVE SYSTEMS

18 RESEARCH METHODOLOGY

- 18.1 RESEARCH DATA

- 18.1.1 SECONDARY DATA

- 18.1.1.1 List of secondary sources

- 18.1.1.2 Key data from secondary sources

- 18.1.2 PRIMARY DATA

- 18.1.2.1 Primary interviewees from demand and supply sides

- 18.1.2.2 Key primary insights

- 18.1.2.3 Breakdown of primary interviews

- 18.1.2.4 Primary participants

- 18.1.1 SECONDARY DATA

- 18.2 MARKET SIZE ESTIMATION

- 18.2.1 BOTTOM-UP APPROACH

- 18.2.2 TOP-DOWN APPROACH

- 18.3 DATA TRIANGULATION

- 18.4 FACTOR ANALYSIS

- 18.5 RESEARCH ASSUMPTIONS AND RISK ASSESSMENT

- 18.6 RESEARCH LIMITATIONS

19 APPENDIX

- 19.1 INSIGHTS FROM INDUSTRY EXPERTS

- 19.2 DISCUSSION GUIDE

- 19.3 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 19.4 CUSTOMIZATION OPTIONS

- 19.5 RELATED REPORTS

- 19.6 AUTHOR DETAILS

List of Tables

- TABLE 1 MARKET DEFINITION

- TABLE 2 CURRENCY EXCHANGE RATES, 2019-2024

- TABLE 3 POPULAR SOFTWARE-DEFINED VEHICLE MODELS USING DRIVE BY WIRE SYSTEMS

- TABLE 4 ELECTRIFICATION OF PUBLIC TRANSPORT FLEETS

- TABLE 5 COMPARISON BETWEEN DRIVE BY WIRE SYSTEMS OFFERED BY TIER-1/2/3 SUPPLIERS

- TABLE 6 ROLE OF COMPANIES IN ECOSYSTEM

- TABLE 7 AVERAGE SELLING PRICE OF DRIVE BY WIRE SOLUTIONS, BY APPLICATION AND REGION, 2025 (USD)

- TABLE 8 THROTTLE BY WIRE COST-BENEFIT ANALYSIS

- TABLE 9 SHIFT BY WIRE COST-BENEFIT ANALYSIS

- TABLE 10 PARK BY WIRE COST-BENEFIT ANALYSIS

- TABLE 11 BRAKE BY WIRE COST-BENEFIT ANALYSIS

- TABLE 12 STEER BY WIRE COST-BENEFIT ANALYSIS

- TABLE 13 KEY CONFERENCES AND EVENTS, 2026-2027

- TABLE 14 MODEL-WISE BY-WIRE TECHNOLOGIES

- TABLE 15 IMPACT OF AI/GEN AI ON DRIVE BY WIRE SYSTEMS

- TABLE 16 PATENT ANALYSIS

- TABLE 17 NORTH AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 18 EUROPE: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 19 ASIA PACIFIC: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 20 DRIVE BY WIRE STANDARDS, MAJOR COUNTRIES, AND REGIONS

- TABLE 21 CONVENTIONAL BRAKING SYSTEMS VS. BRAKE BY WIRE SYSTEMS

- TABLE 22 BRAKE BY WIRE MARKET, BY ICE VEHICLE TYPE, 2021-2024 (THOUSAND UNITS)

- TABLE 23 BRAKE BY WIRE MARKET, BY ICE VEHICLE TYPE, 2025-2032 (THOUSAND UNITS)

- TABLE 24 BRAKE BY WIRE MARKET, BY ICE VEHICLE TYPE, 2021-2024 (USD MILLION)

- TABLE 25 BRAKE BY WIRE MARKET, BY ICE VEHICLE TYPE, 2025-2032 (USD MILLION)

- TABLE 26 PASSENGER CAR: BRAKE BY WIRE MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 27 PASSENGER CAR: BRAKE BY WIRE MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 28 PASSENGER CAR: BRAKE BY WIRE MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 29 PASSENGER CAR: BRAKE BY WIRE MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 30 LIGHT COMMERCIAL VEHICLE: BRAKE BY WIRE MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 31 LIGHT COMMERCIAL VEHICLE: BRAKE BY WIRE MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 32 LIGHT COMMERCIAL VEHICLE: BRAKE BY WIRE MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 33 LIGHT COMMERCIAL VEHICLE: BRAKE BY WIRE MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 34 TRUCK: BRAKE BY WIRE MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 35 TRUCK: BRAKE BY WIRE MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 36 TRUCK: BRAKE BY WIRE MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 37 TRUCK: BRAKE BY WIRE MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 38 BUS: BRAKE BY WIRE MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 39 BUS: BRAKE BY WIRE MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 40 BUS: BRAKE BY WIRE MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 41 BUS: BRAKE BY WIRE MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 42 BRAKE BY WIRE MARKET, BY EV TYPE, 2021-2024 (THOUSAND UNITS)

- TABLE 43 BRAKE BY WIRE MARKET, BY EV TYPE, 2025-2032 (THOUSAND UNITS)

- TABLE 44 BRAKE BY WIRE MARKET, BY EV TYPE, 2021-2024 (USD MILLION)

- TABLE 45 BRAKE BY WIRE MARKET, BY EV TYPE, 2025-2032 (USD MILLION)

- TABLE 46 BEV: BRAKE BY WIRE MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 47 BEV: BRAKE BY WIRE MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 48 BEV: BRAKE BY WIRE MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 49 BEV: BRAKE BY WIRE MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 50 PHEV: BRAKE BY WIRE MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 51 PHEV: BRAKE BY WIRE MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 52 PHEV: BRAKE BY WIRE MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 53 PHEV: BRAKE BY WIRE MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 54 FCEV: BRAKE BY WIRE MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 55 FCEV: BRAKE BY WIRE MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 56 FCEV: BRAKE BY WIRE MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 57 FCEV: BRAKE BY WIRE MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 58 BRAKE BY WIRE MARKET, BY SENSOR TYPE, 2021-2024 (THOUSAND UNITS)

- TABLE 59 BRAKE BY WIRE MARKET, BY SENSOR TYPE, 2025-2032 (THOUSAND UNITS)

- TABLE 60 BRAKE BY WIRE MARKET, BY SENSOR TYPE, 2021-2024 (USD MILLION)

- TABLE 61 BRAKE BY WIRE MARKET, BY SENSOR TYPE, 2025-2032 (USD MILLION)

- TABLE 62 BRAKE PEDAL SENSOR: BRAKE BY WIRE MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 63 BRAKE PEDAL SENSOR: BRAKE BY WIRE MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 64 BRAKE PEDAL SENSOR: BRAKE BY WIRE MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 65 BRAKE PEDAL SENSOR: BRAKE BY WIRE MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 66 BRAKE BY WIRE MARKET, BY COMPONENT, 2021-2024 (THOUSAND UNITS)

- TABLE 67 BRAKE BY WIRE MARKET, BY COMPONENT, 2025-2032 (THOUSAND UNITS)

- TABLE 68 BRAKE BY WIRE MARKET, BY COMPONENT, 2021-2024 (USD MILLION)

- TABLE 69 BRAKE BY WIRE MARKET, BY COMPONENT, 2025-2032 (USD MILLION)

- TABLE 70 ACTUATOR: BRAKE BY WIRE MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 71 ACTUATOR: BRAKE BY WIRE MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 72 ACTUATOR: BRAKE BY WIRE MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 73 ACTUATOR: BRAKE BY WIRE MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 74 ECU: BRAKE BY WIRE MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 75 ECU: BRAKE BY WIRE MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 76 ECU: BRAKE BY WIRE MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 77 ECU: BRAKE BY WIRE MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 78 CONVENTIONAL PARKING SYSTEMS VS. PARK BY WIRE SYSTEM

- TABLE 79 PARK BY WIRE MARKET, BY ICE VEHICLE TYPE, 2021-2024 (THOUSAND UNITS)

- TABLE 80 PARK BY WIRE MARKET, BY ICE VEHICLE TYPE, 2025-2032 (THOUSAND UNITS)

- TABLE 81 PARK BY WIRE MARKET, BY ICE VEHICLE TYPE, 2021-2024 (USD MILLION)

- TABLE 82 PARK BY WIRE MARKET, BY ICE VEHICLE TYPE, 2025-2032 (USD MILLION)

- TABLE 83 PASSENGER CAR: PARK BY WIRE MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 84 PASSENGER CAR: PARK BY WIRE MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 85 PASSENGER CAR: PARK BY WIRE MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 86 PASSENGER CAR: PARK BY WIRE MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 87 LIGHT COMMERCIAL VEHICLE: PARK BY WIRE MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 88 LIGHT COMMERCIAL VEHICLE: PARK BY WIRE MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 89 LIGHT COMMERCIAL VEHICLE: PARK BY WIRE MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 90 LIGHT COMMERCIAL VEHICLE: PARK BY WIRE MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 91 TRUCK: PARK BY WIRE MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 92 TRUCK: PARK BY WIRE MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 93 TRUCK: PARK BY WIRE MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 94 TRUCK: PARK BY WIRE MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 95 BUS: PARK BY WIRE MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 96 BUS: PARK BY WIRE MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 97 BUS: PARK BY WIRE MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 98 BUS: PARK BY WIRE MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 99 PARK BY WIRE MARKET, BY EV TYPE, 2021-2024 (THOUSAND UNITS)

- TABLE 100 PARK BY WIRE MARKET, BY EV TYPE, 2025-2032 (THOUSAND UNITS)

- TABLE 101 PARK BY WIRE MARKET, BY EV TYPE, 2021-2024 (USD MILLION)

- TABLE 102 PARK BY WIRE MARKET, BY EV TYPE, 2025-2032 (USD MILLION)

- TABLE 103 BEV: PARK BY WIRE MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 104 BEV: PARK BY WIRE MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 105 BEV: PARK BY WIRE MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 106 BEV: PARK BY WIRE MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 107 PHEV: PARK BY WIRE MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 108 PHEV: PARK BY WIRE MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 109 PHEV: PARK BY WIRE MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 110 PHEV: PARK BY WIRE MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 111 FCEV: PARK BY WIRE MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 112 FCEV: PARK BY WIRE MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 113 FCEV: PARK BY WIRE MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 114 FCEV: PARK BY WIRE MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 115 PARK BY WIRE MARKET, BY SENSOR TYPE, 2021-2024 (THOUSAND UNITS)

- TABLE 116 PARK BY WIRE MARKET, BY SENSOR TYPE, 2025-2032 (THOUSAND UNITS)

- TABLE 117 PARK BY WIRE MARKET, BY SENSOR TYPE, 2021-2024 (USD MILLION)

- TABLE 118 PARK BY WIRE MARKET, BY SENSOR TYPE, 2025-2032 (USD MILLION)

- TABLE 119 PARK SENSOR: PARK BY WIRE MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 120 PARK SENSOR: PARK BY WIRE MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 121 PARK SENSOR: PARK BY WIRE MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 122 PARK SENSOR: PARK BY WIRE MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 123 PARK BY WIRE MARKET, BY COMPONENT, 2021-2024 (THOUSAND UNITS)

- TABLE 124 PARK BY WIRE MARKET, BY COMPONENT, 2025-2032 (THOUSAND UNITS)

- TABLE 125 PARK BY WIRE MARKET, BY COMPONENT, 2021-2024 (USD MILLION)

- TABLE 126 PARK BY WIRE MARKET, BY COMPONENT, 2025-2032 (USD MILLION)

- TABLE 127 ACTUATOR: PARK BY WIRE MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 128 ACTUATOR: PARK BY WIRE MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 129 ACTUATOR: PARK BY WIRE MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 130 ACTUATOR: PARK BY WIRE MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 131 ECU: PARK BY WIRE MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 132 ECU: PARK BY WIRE MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 133 ECU: PARK BY WIRE MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 134 ECU: PARK BY WIRE MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 135 PARKING PAWL: PARK BY WIRE MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 136 PARKING PAWL: PARK BY WIRE MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 137 PARKING PAWL: PARK BY WIRE MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 138 PARKING PAWL: PARK BY WIRE MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 139 CONVENTIONAL SHIFTING SYSTEMS VS. SHIFT BY WIRE SYSTEMS

- TABLE 140 SHIFT BY WIRE MARKET, BY ICE VEHICLE TYPE, 2021-2024 (THOUSAND UNITS)

- TABLE 141 SHIFT BY WIRE MARKET, BY ICE VEHICLE TYPE, 2025-2032 (THOUSAND UNITS)

- TABLE 142 SHIFT BY WIRE MARKET, BY ICE VEHICLE TYPE, 2021-2024 (USD MILLION)

- TABLE 143 SHIFT BY WIRE MARKET, BY ICE VEHICLE TYPE, 2025-2032 (USD MILLION)

- TABLE 144 PASSENGER CAR: SHIFT BY WIRE MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 145 PASSENGER CAR: SHIFT BY WIRE MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 146 PASSENGER CAR: SHIFT BY WIRE MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 147 PASSENGER CAR: SHIFT BY WIRE MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 148 LIGHT COMMERCIAL VEHICLE: SHIFT BY WIRE MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 149 LIGHT COMMERCIAL VEHICLE: SHIFT BY WIRE MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 150 LIGHT COMMERCIAL VEHICLE: SHIFT BY WIRE MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 151 LIGHT COMMERCIAL VEHICLE: SHIFT BY WIRE MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 152 TRUCK: SHIFT BY WIRE MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 153 TRUCK: SHIFT BY WIRE MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 154 TRUCK: SHIFT BY WIRE MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 155 TRUCK: SHIFT BY WIRE MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 156 BUS: SHIFT BY WIRE MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 157 BUS: SHIFT BY WIRE MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 158 BUS: SHIFT BY WIRE MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 159 BUS: SHIFT BY WIRE MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 160 SHIFT BY WIRE MARKET, BY EV TYPE, 2021-2024 (THOUSAND UNITS)

- TABLE 161 SHIFT BY WIRE MARKET, BY EV TYPE, 2025-2032 (THOUSAND UNITS)

- TABLE 162 SHIFT BY WIRE MARKET, BY EV TYPE, 2021-2024 (USD MILLION)

- TABLE 163 SHIFT BY WIRE MARKET, BY EV TYPE, 2025-2032 (USD MILLION)

- TABLE 164 BEV: SHIFT BY WIRE MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 165 BEV: SHIFT BY WIRE MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 166 BEV: SHIFT BY WIRE MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 167 BEV: SHIFT BY WIRE MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 168 PHEV: SHIFT BY WIRE MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 169 PHEV: SHIFT BY WIRE MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 170 PHEV: SHIFT BY WIRE MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 171 PHEV: SHIFT BY WIRE MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 172 FCEV: SHIFT BY WIRE MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 173 FCEV: SHIFT BY WIRE MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 174 FCEV: SHIFT BY WIRE MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 175 FCEV: SHIFT BY WIRE MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 176 SHIFT BY WIRE MARKET, BY SENSOR TYPE, 2021-2024 (THOUSAND UNITS)

- TABLE 177 SHIFT BY WIRE MARKET, BY SENSOR TYPE, 2025-2032 (THOUSAND UNITS)

- TABLE 178 SHIFT BY WIRE MARKET, BY SENSOR TYPE, 2021-2024 (USD MILLION)

- TABLE 179 SHIFT BY WIRE MARKET, BY SENSOR TYPE, 2025-2032 (USD MILLION)

- TABLE 180 GEAR SHIFT POSITION SENSOR: SHIFT BY WIRE MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 181 GEAR SHIFT POSITION SENSOR: SHIFT BY WIRE MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 182 GEAR SHIFT POSITION SENSOR: SHIFT BY WIRE MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 183 GEAR SHIFT POSITION SENSOR: SHIFT BY WIRE MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 184 SHIFT BY WIRE MARKET, BY COMPONENT, 2021-2024 (THOUSAND UNITS)

- TABLE 185 SHIFT BY WIRE MARKET, BY COMPONENT, 2025-2032 (THOUSAND UNITS)

- TABLE 186 SHIFT BY WIRE MARKET, BY COMPONENT, 2021-2024 (USD MILLION)

- TABLE 187 SHIFT BY WIRE MARKET, BY COMPONENT, 2025-2032 (USD MILLION)

- TABLE 188 ACTUATOR: SHIFT BY WIRE MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 189 ACTUATOR: SHIFT BY WIRE MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 190 ACTUATOR: SHIFT BY WIRE MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 191 ACTUATOR: SHIFT BY WIRE MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 192 ECU: SHIFT BY WIRE MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 193 ECU: SHIFT BY WIRE MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 194 ECU: SHIFT BY WIRE MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 195 ECU: SHIFT BY WIRE MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 196 ETCU: SHIFT BY WIRE MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 197 ETCU: SHIFT BY WIRE MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 198 ETCU: SHIFT BY WIRE MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 199 ETCU: SHIFT BY WIRE MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 200 CONVENTIONAL STEERING SYSTEMS VS. STEER BY WIRE SYSTEMS

- TABLE 201 STEER BY WIRE MARKET, BY ICE VEHICLE TYPE, 2021-2024 (THOUSAND UNITS)

- TABLE 202 STEER BY WIRE MARKET, BY ICE VEHICLE TYPE, 2025-2032 (THOUSAND UNITS)

- TABLE 203 STEER BY WIRE MARKET, BY ICE VEHICLE TYPE, 2021-2024 (USD MILLION)

- TABLE 204 STEER BY WIRE MARKET, BY ICE VEHICLE TYPE, 2025-2032 (USD MILLION)

- TABLE 205 PASSENGER CAR: STEER BY WIRE MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 206 PASSENGER CAR: STEER BY WIRE MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 207 PASSENGER CAR: STEER BY WIRE MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 208 PASSENGER CAR: STEER BY WIRE MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 209 LIGHT COMMERCIAL VEHICLE: STEER BY WIRE MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 210 LIGHT COMMERCIAL VEHICLE: STEER BY WIRE MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 211 LIGHT COMMERCIAL VEHICLE: STEER BY WIRE MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 212 LIGHT COMMERCIAL VEHICLE: STEER BY WIRE MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 213 TRUCK: STEER BY WIRE MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 214 TRUCK: STEER BY WIRE MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 215 TRUCK: STEER BY WIRE MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 216 TRUCK: STEER BY WIRE MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 217 BUS: STEER BY WIRE MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 218 BUS: STEER BY WIRE MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 219 BUS: STEER BY WIRE MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 220 BUS: STEER BY WIRE MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 221 STEER BY WIRE MARKET, BY EV TYPE, 2021-2024 (THOUSAND UNITS)

- TABLE 222 STEER BY WIRE MARKET, BY EV TYPE, 2025-2032 (THOUSAND UNITS)

- TABLE 223 STEER BY WIRE MARKET, BY EV TYPE, 2021-2024 (USD MILLION)

- TABLE 224 STEER BY WIRE MARKET, BY EV TYPE, 2025-2032 (USD MILLION)

- TABLE 225 BEV: STEER BY WIRE MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 226 BEV: STEER BY WIRE MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 227 BEV: STEER BY WIRE MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 228 BEV: STEER BY WIRE MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 229 PHEV: STEER BY WIRE MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 230 PHEV: STEER BY WIRE MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 231 PHEV: STEER BY WIRE MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 232 PHEV: STEER BY WIRE MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 233 FCEV: STEER BY WIRE MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 234 FCEV: STEER BY WIRE MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 235 FCEV: STEER BY WIRE MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 236 FCEV: STEER BY WIRE MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 237 STEER BY WIRE MARKET, BY SENSOR TYPE, 2021-2024 (THOUSAND UNITS)

- TABLE 238 STEER BY WIRE MARKET, BY SENSOR TYPE, 2025-2032 (THOUSAND UNITS)

- TABLE 239 STEER BY WIRE MARKET, BY SENSOR TYPE, 2021-2024 (USD MILLION)

- TABLE 240 STEER BY WIRE MARKET, BY SENSOR TYPE, 2025-2032 (USD MILLION)

- TABLE 241 HAND WHEEL ANGLE SENSOR: STEER BY WIRE MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 242 HAND WHEEL ANGLE SENSOR: STEER BY WIRE MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 243 HAND WHEEL ANGLE SENSOR: STEER BY WIRE MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 244 HAND WHEEL ANGLE SENSOR: STEER BY WIRE MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 245 PINION ANGLE SENSOR: STEER BY WIRE MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 246 PINION ANGLE SENSOR: STEER BY WIRE MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 247 PINION ANGLE SENSOR: STEER BY WIRE MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 248 PINION ANGLE SENSOR: STEER BY WIRE MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 249 STEER BY WIRE MARKET, BY COMPONENT, 2021-2024 (THOUSAND UNITS)

- TABLE 250 STEER BY WIRE MARKET, BY COMPONENT, 2025-2032 (THOUSAND UNITS)

- TABLE 251 STEER BY WIRE MARKET, BY COMPONENT, 2021-2024 (USD MILLION)

- TABLE 252 STEER BY WIRE MARKET, BY COMPONENT, 2025-2032 (USD MILLION)

- TABLE 253 ACTUATOR: STEER BY WIRE MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 254 ACTUATOR: STEER BY WIRE MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 255 ACTUATOR: STEER BY WIRE MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 256 ACTUATOR: STEER BY WIRE MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 257 ECU: STEER BY WIRE MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 258 ECU: STEER BY WIRE MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 259 ECU: STEER BY WIRE MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 260 ECU: STEER BY WIRE MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 261 FEEDBACK MOTOR: STEER BY WIRE MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 262 FEEDBACK MOTOR: STEER BY WIRE MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 263 FEEDBACK MOTOR: STEER BY WIRE MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 264 FEEDBACK MOTOR: STEER BY WIRE MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 265 CONVENTIONAL THROTTLE SYSTEMS VS. THROTTLE BY WIRE SYSTEMS

- TABLE 266 THROTTLE BY WIRE MARKET, BY ICE VEHICLE TYPE, 2021-2024 (THOUSAND UNITS)

- TABLE 267 THROTTLE BY WIRE MARKET, BY ICE VEHICLE TYPE, 2025-2032 (THOUSAND UNITS)

- TABLE 268 THROTTLE BY WIRE MARKET, BY ICE VEHICLE TYPE, 2021-2024 (USD MILLION)

- TABLE 269 THROTTLE BY WIRE MARKET, BY ICE VEHICLE TYPE, 2025-2032 (USD MILLION)

- TABLE 270 PASSENGER CAR: THROTTLE BY WIRE MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 271 PASSENGER CAR: THROTTLE BY WIRE MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 272 PASSENGER CAR: THROTTLE BY WIRE MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 273 PASSENGER CAR: THROTTLE BY WIRE MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 274 LIGHT COMMERCIAL VEHICLE: THROTTLE BY WIRE MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 275 LIGHT COMMERCIAL VEHICLE: THROTTLE BY WIRE MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 276 LIGHT COMMERCIAL VEHICLE: THROTTLE BY WIRE MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 277 LIGHT COMMERCIAL VEHICLE: THROTTLE BY WIRE MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 278 TRUCK: THROTTLE BY WIRE MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 279 TRUCK: THROTTLE BY WIRE MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 280 TRUCK: THROTTLE BY WIRE MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 281 TRUCK: THROTTLE BY WIRE MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 282 BUS: THROTTLE BY WIRE MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 283 BUS: THROTTLE BY WIRE MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 284 BUS: THROTTLE BY WIRE MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 285 BUS: THROTTLE BY WIRE MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 286 THROTTLE BY WIRE MARKET, BY EV TYPE, 2021-2024 (THOUSAND UNITS)

- TABLE 287 THROTTLE BY WIRE MARKET, BY EV TYPE, 2025-2032 (THOUSAND UNITS)

- TABLE 288 THROTTLE BY WIRE MARKET, BY EV TYPE, 2021-2024 (USD MILLION)

- TABLE 289 THROTTLE BY WIRE MARKET, BY EV TYPE, 2025-2032 (USD MILLION)

- TABLE 290 BEV: THROTTLE BY WIRE MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 291 BEV: THROTTLE BY WIRE MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 292 BEV: THROTTLE BY WIRE MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 293 BEV: THROTTLE BY WIRE MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 294 PHEV: THROTTLE BY WIRE MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 295 PHEV: THROTTLE BY WIRE MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 296 PHEV: THROTTLE BY WIRE MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 297 PHEV: THROTTLE BY WIRE MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 298 FCEV: THROTTLE BY WIRE MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 299 FCEV: THROTTLE BY WIRE MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 300 FCEV: THROTTLE BY WIRE MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 301 FCEV: THROTTLE BY WIRE MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 302 THROTTLE BY WIRE MARKET, BY SENSOR TYPE, 2021-2024 (THOUSAND UNITS)

- TABLE 303 THROTTLE BY WIRE MARKET, BY SENSOR TYPE , 2025-2032 (THOUSAND UNITS)

- TABLE 304 THROTTLE BY WIRE MARKET, BY SENSOR TYPE, 2021-2024 (USD MILLION)

- TABLE 305 THROTTLE BY WIRE MARKET, BY SENSOR TYPE, 2025-2032 (USD MILLION)

- TABLE 306 THROTTLE PEDAL SENSOR: THROTTLE BY WIRE MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 307 THROTTLE PEDAL SENSOR: THROTTLE BY WIRE MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 308 THROTTLE PEDAL SENSOR: THROTTLE BY WIRE MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 309 THROTTLE PEDAL SENSOR: THROTTLE BY WIRE MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 310 THROTTLE POSITION SENSOR: THROTTLE BY WIRE MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 311 THROTTLE POSITION SENSOR: THROTTLE BY WIRE MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 312 THROTTLE POSITION SENSOR: THROTTLE BY WIRE MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 313 THROTTLE POSITION SENSOR: THROTTLE BY WIRE MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 314 THROTTLE BY WIRE MARKET, BY COMPONENT, 2021-2024 (THOUSAND UNITS)

- TABLE 315 THROTTLE BY WIRE MARKET, BY COMPONENT, 2025-2032 (THOUSAND UNITS)

- TABLE 316 THROTTLE BY WIRE MARKET, BY COMPONENT, 2021-2024 (USD MILLION)

- TABLE 317 THROTTLE BY WIRE MARKET, BY COMPONENT, 2025-2032 (USD MILLION)

- TABLE 318 ACTUATOR: THROTTLE BY WIRE MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 319 ACTUATOR: THROTTLE BY WIRE MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 320 ACTUATOR: THROTTLE BY WIRE MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 321 ACTUATOR: THROTTLE BY WIRE MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 322 ECU: THROTTLE BY WIRE MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 323 ECU: THROTTLE BY WIRE MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 324 ECU: THROTTLE BY WIRE MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 325 ECU: THROTTLE BY WIRE MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 326 ECM: THROTTLE BY WIRE MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 327 ECM: THROTTLE BY WIRE MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 328 ECM: THROTTLE BY WIRE MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 329 ECM: THROTTLE BY WIRE MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 330 ETCM: THROTTLE BY WIRE MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 331 ETCM: THROTTLE BY WIRE MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 332 ETCM: THROTTLE BY WIRE MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 333 ETCM: THROTTLE BY WIRE MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 334 L2 AUTONOMOUS VEHICLE DRIVE BY WIRE MARKET, BY APPLICATION, 2021-2024 (THOUSAND UNITS)

- TABLE 335 L2 AUTONOMOUS VEHICLE DRIVE BY WIRE MARKET, BY APPLICATION, 2025-2032 (THOUSAND UNITS)

- TABLE 336 L3 AUTONOMOUS VEHICLE DRIVE BY WIRE MARKET, BY APPLICATION, 2021-2024 (THOUSAND UNITS)

- TABLE 337 L3 AUTONOMOUS VEHICLE DRIVE BY WIRE MARKET, BY APPLICATION, 2025-2032 (THOUSAND UNITS)

- TABLE 338 L4/L5 AUTONOMOUS VEHICLE DRIVE BY WIRE MARKET, BY APPLICATION, 2021-2024 (THOUSAND UNITS)

- TABLE 339 L4/L5 AUTONOMOUS VEHICLE DRIVE BY WIRE MARKET, BY APPLICATION, 2025-2032 (THOUSAND UNITS)

- TABLE 340 DRIVE BY WIRE MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 341 DRIVE BY WIRE MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 342 DRIVE BY WIRE MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 343 DRIVE BY WIRE MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 344 ASIA PACIFIC: DRIVE BY WIRE MARKET, BY COUNTRY, 2021-2024 (THOUSAND UNITS)

- TABLE 345 ASIA PACIFIC: DRIVE BY WIRE MARKET, BY COUNTRY, 2025-2032 (THOUSAND UNITS)

- TABLE 346 ASIA PACIFIC: DRIVE BY WIRE MARKET, BY COUNTRY, 2021-2024 (USD MILLION)

- TABLE 347 ASIA PACIFIC: DRIVE BY WIRE MARKET, BY COUNTRY, 2025-2032 (USD MILLION)

- TABLE 348 CHINA: DRIVE BY WIRE MARKET, BY APPLICATION, 2021-2024 (THOUSAND UNITS)

- TABLE 349 CHINA: DRIVE BY WIRE MARKET, BY APPLICATION, 2025-2032 (THOUSAND UNITS)

- TABLE 350 CHINA: DRIVE BY WIRE MARKET, BY APPLICATION, 2021-2024 (USD MILLION)

- TABLE 351 CHINA: DRIVE BY WIRE MARKET, BY APPLICATION, 2025-2032 (USD MILLION)

- TABLE 352 INDIA: DRIVE BY WIRE MARKET, BY APPLICATION, 2021-2024 (THOUSAND UNITS)

- TABLE 353 INDIA: DRIVE BY WIRE MARKET, BY APPLICATION, 2025-2032 (THOUSAND UNITS)

- TABLE 354 INDIA: DRIVE BY WIRE MARKET, BY APPLICATION, 2021-2024 (USD MILLION)

- TABLE 355 INDIA: DRIVE BY WIRE MARKET, BY APPLICATION, 2025-2032 (USD MILLION)

- TABLE 356 JAPAN: DRIVE BY WIRE MARKET, BY APPLICATION, 2021-2024 (THOUSAND UNITS)

- TABLE 357 JAPAN: DRIVE BY WIRE MARKET, BY APPLICATION, 2025-2032 (THOUSAND UNITS)

- TABLE 358 JAPAN: DRIVE BY WIRE MARKET, BY APPLICATION, 2021-2024 (USD MILLION)

- TABLE 359 JAPAN: DRIVE BY WIRE MARKET, BY APPLICATION, 2025-2032 (USD MILLION)

- TABLE 360 SOUTH KOREA: DRIVE BY WIRE MARKET, BY APPLICATION, 2021-2024 (THOUSAND UNITS)

- TABLE 361 SOUTH KOREA: DRIVE BY WIRE MARKET, BY APPLICATION, 2025-2032 (THOUSAND UNITS)

- TABLE 362 SOUTH KOREA: DRIVE BY WIRE MARKET, BY APPLICATION, 2021-2024 (USD MILLION)

- TABLE 363 SOUTH KOREA: DRIVE BY WIRE MARKET, BY APPLICATION, 2025-2032 (USD MILLION)

- TABLE 364 THAILAND: DRIVE BY WIRE MARKET, BY APPLICATION, 2021-2024 (THOUSAND UNITS)

- TABLE 365 THAILAND: DRIVE BY WIRE MARKET, BY APPLICATION, 2025-2032 (THOUSAND UNITS)

- TABLE 366 THAILAND: DRIVE BY WIRE MARKET, BY APPLICATION, 2021-2024 (USD MILLION)

- TABLE 367 THAILAND: DRIVE BY WIRE MARKET, BY APPLICATION, 2025-2032 (USD MILLION)

- TABLE 368 REST OF ASIA PACIFIC: DRIVE BY WIRE MARKET, BY APPLICATION, 2021-2024 (THOUSAND UNITS)

- TABLE 369 REST OF ASIA PACIFIC: DRIVE BY WIRE MARKET, BY APPLICATION, 2025-2032 (THOUSAND UNITS)

- TABLE 370 REST OF ASIA PACIFIC: DRIVE BY WIRE MARKET, BY APPLICATION, 2021-2024 (USD MILLION)

- TABLE 371 REST OF ASIA PACIFIC: DRIVE BY WIRE MARKET, BY APPLICATION, 2025-2032 (USD MILLION)

- TABLE 372 EUROPE: DRIVE BY WIRE MARKET, BY COUNTRY, 2021-2024 (THOUSAND UNITS)

- TABLE 373 EUROPE: DRIVE BY WIRE MARKET, BY COUNTRY, 2025-2032 (THOUSAND UNITS)

- TABLE 374 EUROPE: DRIVE BY WIRE MARKET, BY COUNTRY, 2021-2024 (USD MILLION)

- TABLE 375 EUROPE: DRIVE BY WIRE MARKET, BY COUNTRY, 2025-2032 (USD MILLION)

- TABLE 376 GERMANY: DRIVE BY WIRE MARKET, BY APPLICATION, 2021-2024 (THOUSAND UNITS)

- TABLE 377 GERMANY: DRIVE BY WIRE MARKET, BY APPLICATION, 2025-2032 (THOUSAND UNITS)

- TABLE 378 GERMANY: DRIVE BY WIRE MARKET, BY APPLICATION, 2021-2024 (USD MILLION)

- TABLE 379 GERMANY: DRIVE BY WIRE MARKET, BY APPLICATION, 2025-2032 (USD MILLION)

- TABLE 380 FRANCE: DRIVE BY WIRE MARKET, BY APPLICATION, 2021-2024 (THOUSAND UNITS)

- TABLE 381 FRANCE: DRIVE BY WIRE MARKET, BY APPLICATION, 2025-2032 (THOUSAND UNITS)

- TABLE 382 FRANCE: DRIVE BY WIRE MARKET, BY APPLICATION, 2021-2024 (USD MILLION)

- TABLE 383 FRANCE: DRIVE BY WIRE MARKET, BY APPLICATION, 2025-2032 (USD MILLION)

- TABLE 384 RUSSIA: DRIVE BY WIRE MARKET, BY APPLICATION, 2021-2024 (THOUSAND UNITS)

- TABLE 385 RUSSIA: DRIVE BY WIRE MARKET, BY APPLICATION, 2025-2032 (THOUSAND UNITS)

- TABLE 386 RUSSIA: DRIVE BY WIRE MARKET, BY APPLICATION, 2021-2024 (USD MILLION)

- TABLE 387 RUSSIA: DRIVE BY WIRE MARKET, BY APPLICATION, 2025-2032 (USD MILLION)

- TABLE 388 SPAIN: DRIVE BY WIRE MARKET, BY APPLICATION, 2021-2024 (THOUSAND UNITS)

- TABLE 389 SPAIN: DRIVE BY WIRE MARKET, BY APPLICATION, 2025-2032 (THOUSAND UNITS)

- TABLE 390 SPAIN: DRIVE BY WIRE MARKET, BY APPLICATION, 2021-2024 (USD MILLION)

- TABLE 391 SPAIN: DRIVE BY WIRE MARKET, BY APPLICATION, 2025-2032 (USD MILLION)

- TABLE 392 UK: DRIVE BY WIRE MARKET, BY APPLICATION, 2021-2024 (THOUSAND UNITS)

- TABLE 393 UK: DRIVE BY WIRE MARKET, BY APPLICATION, 2025-2032 (THOUSAND UNITS)

- TABLE 394 UK: DRIVE BY WIRE MARKET, BY APPLICATION, 2021-2024 (USD MILLION)

- TABLE 395 UK: DRIVE BY WIRE MARKET, BY APPLICATION, 2025-2032 (USD MILLION)

- TABLE 396 TURKEY: DRIVE BY WIRE MARKET, BY APPLICATION, 2021-2024 (THOUSAND UNITS)

- TABLE 397 TURKEY: DRIVE BY WIRE MARKET, BY APPLICATION, 2025-2032 (THOUSAND UNITS)

- TABLE 398 TURKEY: DRIVE BY WIRE MARKET, BY APPLICATION, 2021-2024 (USD MILLION)

- TABLE 399 TURKEY: DRIVE BY WIRE MARKET, BY APPLICATION, 2025-2032 (USD MILLION)

- TABLE 400 ITALY: DRIVE BY WIRE MARKET, BY APPLICATION, 2021-2024 (THOUSAND UNITS)

- TABLE 401 ITALY: DRIVE BY WIRE MARKET, BY APPLICATION, 2025-2032 (THOUSAND UNITS)

- TABLE 402 ITALY: DRIVE BY WIRE MARKET, BY APPLICATION, 2021-2024 (USD MILLION)

- TABLE 403 ITALY: DRIVE BY WIRE MARKET, BY APPLICATION, 2025-2032 (USD MILLION)

- TABLE 404 REST OF EUROPE: DRIVE BY WIRE MARKET, BY APPLICATION, 2021-2024 (THOUSAND UNITS)

- TABLE 405 REST OF EUROPE: DRIVE BY WIRE MARKET, BY APPLICATION, 2025-2032 (THOUSAND UNITS)

- TABLE 406 REST OF EUROPE: DRIVE BY WIRE MARKET, BY APPLICATION, 2021-2024 (USD MILLION)

- TABLE 407 REST OF EUROPE: DRIVE BY WIRE MARKET, BY APPLICATION, 2025-2032 (USD MILLION)

- TABLE 408 NORTH AMERICA: DRIVE BY WIRE MARKET, BY COUNTRY, 2021-2024 (THOUSAND UNITS)

- TABLE 409 NORTH AMERICA: DRIVE BY WIRE MARKET, BY COUNTRY, 2025-2032 (THOUSAND UNITS)

- TABLE 410 NORTH AMERICA: DRIVE BY WIRE MARKET, BY COUNTRY, 2021-2024 (USD MILLION)

- TABLE 411 NORTH AMERICA: DRIVE BY WIRE MARKET, BY COUNTRY, 2025-2032 (USD MILLION)

- TABLE 412 CANADA: DRIVE BY WIRE MARKET, BY APPLICATION, 2021-2024 (THOUSAND UNITS)

- TABLE 413 CANADA: DRIVE BY WIRE MARKET, BY APPLICATION, 2025-2032 (THOUSAND UNITS)

- TABLE 414 CANADA: DRIVE BY WIRE MARKET, BY APPLICATION, 2021-2024 (USD MILLION)

- TABLE 415 CANADA: DRIVE BY WIRE MARKET, BY APPLICATION, 2025-2032 (USD MILLION)

- TABLE 416 MEXICO: DRIVE BY WIRE MARKET, BY APPLICATION, 2021-2024 (THOUSAND UNITS)

- TABLE 417 MEXICO: DRIVE BY WIRE MARKET, BY APPLICATION, 2025-2032 (THOUSAND UNITS)

- TABLE 418 MEXICO: DRIVE BY WIRE MARKET, BY APPLICATION, 2021-2024 (USD MILLION)

- TABLE 419 MEXICO: DRIVE BY WIRE MARKET, BY APPLICATION, 2025-2032 (USD MILLION)

- TABLE 420 US: DRIVE BY WIRE MARKET, BY APPLICATION, 2021-2024 (THOUSAND UNITS)

- TABLE 421 US: DRIVE BY WIRE MARKET, BY APPLICATION, 2025-2032 (THOUSAND UNITS)

- TABLE 422 US: DRIVE BY WIRE MARKET, BY APPLICATION, 2021-2024 (USD MILLION)

- TABLE 423 US: DRIVE BY WIRE MARKET, BY APPLICATION, 2025-2032 (USD MILLION)

- TABLE 424 REST OF THE WORLD: DRIVE BY WIRE MARKET, BY COUNTRY, 2021-2024 (THOUSAND UNITS)

- TABLE 425 REST OF THE WORLD: DRIVE BY WIRE MARKET, BY COUNTRY, 2025-2032 (THOUSAND UNITS)

- TABLE 426 REST OF THE WORLD: DRIVE BY WIRE MARKET, BY COUNTRY, 2021-2024 (USD MILLION)

- TABLE 427 REST OF THE WORLD: DRIVE BY WIRE MARKET, BY COUNTRY, 2025-2032 (USD MILLION)

- TABLE 428 BRAZIL: DRIVE BY WIRE MARKET, BY APPLICATION, 2021-2024 (THOUSAND UNITS)

- TABLE 429 BRAZIL: DRIVE BY WIRE MARKET, BY APPLICATION, 2025-2032 (THOUSAND UNITS)

- TABLE 430 BRAZIL: DRIVE BY WIRE MARKET, BY APPLICATION, 2021-2024 (USD MILLION)

- TABLE 431 BRAZIL: DRIVE BY WIRE MARKET, BY APPLICATION, 2025-2032 (USD MILLION)

- TABLE 432 IRAN: DRIVE BY WIRE MARKET, BY APPLICATION, 2021-2024 (THOUSAND UNITS)

- TABLE 433 IRAN: DRIVE BY WIRE MARKET, BY APPLICATION, 2025-2032 (THOUSAND UNITS)

- TABLE 434 IRAN: DRIVE BY WIRE MARKET, BY APPLICATION, 2021-2024 (USD MILLION)

- TABLE 435 IRAN: DRIVE BY WIRE MARKET, BY APPLICATION, 2025-2032 (USD MILLION)

- TABLE 436 ARGENTINA: DRIVE BY WIRE MARKET, BY APPLICATION, 2021-2024 (THOUSAND UNITS)

- TABLE 437 ARGENTINA: DRIVE BY WIRE MARKET, BY APPLICATION, 2025-2032 (THOUSAND UNITS)

- TABLE 438 ARGENTINA: DRIVE BY WIRE MARKET, BY APPLICATION, 2021-2024 (USD MILLION)

- TABLE 439 ARGENTINA: DRIVE BY WIRE MARKET, BY APPLICATION, 2025-2032 (USD MILLION)

- TABLE 440 SOUTH AFRICA: DRIVE BY WIRE MARKET, BY APPLICATION, 2021-2024 (THOUSAND UNITS)

- TABLE 441 SOUTH AFRICA: DRIVE BY WIRE MARKET, BY APPLICATION, 2025-2032 (THOUSAND UNITS)

- TABLE 442 SOUTH AFRICA: DRIVE BY WIRE MARKET, BY APPLICATION, 2021-2024 (USD MILLION)

- TABLE 443 SOUTH AFRICA: DRIVE BY WIRE MARKET, BY APPLICATION, 2025-2032 (USD MILLION)

- TABLE 444 OTHERS: DRIVE BY WIRE MARKET, BY APPLICATION, 2021-2024 (THOUSAND UNITS)

- TABLE 445 OTHERS: DRIVE BY WIRE MARKET, BY APPLICATION, 2025-2032 (THOUSAND UNITS)

- TABLE 446 OTHERS: DRIVE BY WIRE MARKET, BY APPLICATION, 2021-2024 (USD MILLION)

- TABLE 447 OTHERS: DRIVE BY WIRE MARKET, BY APPLICATION, 2025-2032 (USD MILLION)

- TABLE 448 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2021-2025

- TABLE 449 MARKET SHARE ANALYSIS OF KEY PLAYERS, 2024

- TABLE 450 REGION FOOTPRINT

- TABLE 451 COMPONENT FOOTPRINT

- TABLE 452 APPLICATION FOOTPRINT

- TABLE 453 LIST OF START-UPS/SMES

- TABLE 454 COMPETITIVE BENCHMARKING OF START-UPS/SMES

- TABLE 455 DRIVE BY WIRE MARKET: PRODUCT LAUNCHES/DEVELOPMENTS, 2021-2025

- TABLE 456 DRIVE BY WIRE MARKET: DEALS, 2021-2025

- TABLE 457 DRIVE BY WIRE MARKET: EXPANSIONS, 2021-2025

- TABLE 458 DRIVE BY WIRE MARKET: OTHER DEVELOPMENTS, 2021-2025

- TABLE 459 ROBERT BOSCH GMBH: COMPANY OVERVIEW

- TABLE 460 ROBERT BOSCH GMBH: PRODUCTS OFFERED

- TABLE 461 ROBERT BOSCH GMBH: PRODUCT LAUNCHES/DEVELOPMENTS

- TABLE 462 ROBERT BOSCH GMBH: DEALS

- TABLE 463 ROBERT BOSCH GMBH: OTHER DEVELOPMENTS

- TABLE 464 CONTINENTAL AG: COMPANY OVERVIEW

- TABLE 465 CONTINENTAL AG: PRODUCTS OFFERED

- TABLE 466 CONTINENTAL AG: PRODUCT LAUNCHES/DEVELOPMENTS

- TABLE 467 CONTINENTAL AG: DEALS

- TABLE 468 CONTINENTAL AG: EXPANSIONS

- TABLE 469 CONTINENTAL AG: OTHER DEVELOPMENTS

- TABLE 470 ZF FRIEDRICHSHAFEN AG: COMPANY OVERVIEW

- TABLE 471 ZF FRIEDRICHSHAFEN AG: PRODUCTS OFFERED

- TABLE 472 ZF FRIEDRICHSHAFEN AG: PRODUCT LAUNCHES/DEVELOPMENTS

- TABLE 473 ZF FRIEDRICHSHAFEN AG: DEALS

- TABLE 474 ZF FRIEDRICHSHAFEN: OTHER DEVELOPMENTS

- TABLE 475 NEXTEER AUTOMOTIVE: COMPANY OVERVIEW

- TABLE 476 NEXTEER AUTOMOTIVE: PRODUCTS OFFERED

- TABLE 477 NEXTEER AUTOMOTIVE: PRODUCT LAUNCHES/DEVELOPMENTS

- TABLE 478 NEXTEER AUTOMOTIVE: DEALS

- TABLE 479 NEXTEER AUTOMOTIVE: EXPANSIONS

- TABLE 480 HITACHI, LTD.: COMPANY OVERVIEW

- TABLE 481 HITACHI, LTD.: PRODUCTS OFFERED

- TABLE 482 HITACHI, LTD.: PRODUCT LAUNCHES/DEVELOPMENTS

- TABLE 483 HITACHI, LTD.: DEALS

- TABLE 484 HL MANDO CORP.: COMPANY OVERVIEW

- TABLE 485 HL MANDO CORP.: PRODUCTS OFFERED

- TABLE 486 HL MANDO CORP.: DEALS

- TABLE 487 HL MANDO CORP.: OTHER DEVELOPMENTS

- TABLE 488 JTEKT CORPORATION: COMPANY OVERVIEW

- TABLE 489 JTEKT CORPORATION: PRODUCTS OFFERED

- TABLE 490 JTEKT CORPORATION: PRODUCT LAUNCHES/DEVELOPMENTS

- TABLE 491 JTEKT CORPORATION: DEALS

- TABLE 492 JTEKT CORPORATION: EXPANSIONS

- TABLE 493 JTEKT CORPORATION: OTHER DEVELOPMENTS

- TABLE 494 THYSSENKRUPP AG: COMPANY OVERVIEW

- TABLE 495 THYSSENKRUPP AG: PRODUCTS OFFERED

- TABLE 496 THYSSENKRUPP AG: DEALS

- TABLE 497 FICOSA INTERNATIONAL SA: COMPANY OVERVIEW

- TABLE 498 FICOSA INTERNATIONAL SA: PRODUCTS OFFERED

- TABLE 499 KONGSBERG AUTOMOTIVE: COMPANY OVERVIEW

- TABLE 500 KONGSBERG AUTOMOTIVE: PRODUCTS/S OFFERED

- TABLE 501 KONGSBERG AUTOMOTIVE: OTHER DEVELOPMENTS

- TABLE 502 CURTISS-WRIGHT CORPORATION: COMPANY OVERVIEW

- TABLE 503 CURTISS-WRIGHT CORPORATION: PRODUCTS OFFERED

- TABLE 504 CURTIS-WRIGHT CORPORATION: PRODUCT LAUNCHES/DEVELOPMENTS

- TABLE 505 CURTIS-WRIGHT CORPORATION: DEALS

- TABLE 506 CURTIS-WRIGHT CORPORATION: EXPANSIONS

- TABLE 507 CURTIS-WRIGHT CORPORATION: OTHER DEVELOPMENTS

- TABLE 508 SCHAEFFLER TECHNOLOGIES AG & CO. KG: COMPANY OVERVIEW

- TABLE 509 KSR INTERNATIONAL INC.: COMPANY OVERVIEW

- TABLE 510 CTS CORPORATION: COMPANY OVERVIEW

- TABLE 511 HYUNDAI MOBIS: COMPANY OVERVIEW

- TABLE 512 FORVIA: COMPANY OVERVIEW

- TABLE 513 NIDEC CORPORATION: COMPANY OVERVIEW

- TABLE 514 NISSAN CORPORATION: COMPANY OVERVIEW

- TABLE 515 INFINEON TECHNOLOGIES AG: COMPANY OVERVIEW

- TABLE 516 BREMBO S.P.A.: COMPANY OVERVIEW

- TABLE 517 DENSO CORPORATION: COMPANY OVERVIEW

- TABLE 518 NXP SEMICONDUCTORS NV: COMPANY OVERVIEW

- TABLE 519 SNT MOTIV CO., LTD.: COMPANY OVERVIEW

- TABLE 520 LEM EUROPE GMBH: COMPANY OVERVIEW

- TABLE 521 ALLIED MOTION TECHNOLOGIES INC.: COMPANY OVERVIEW

- TABLE 522 DURA AUTOMOTIVE SYSTEMS: COMPANY OVERVIEW

List of Figures

- FIGURE 1 DRIVE BY WIRE MARKET SEGMENTATION

- FIGURE 2 MARKET SCENARIO

- FIGURE 3 THROTTLE BY WIRE MARKET FOR ICE AND ELECTRIC VEHICLES, 2021-2032 (USD MILLION)

- FIGURE 4 MAJOR STRATEGIES ADOPTED BY KEY PLAYERS IN DRIVE BY WIRE MARKET

- FIGURE 5 DISRUPTIONS INFLUENCING GROWTH OF DRIVE BY WIRE MARKET

- FIGURE 6 HIGH-GROWTH SEGMENTS IN DRIVE BY WIRE MARKET

- FIGURE 7 EUROPE TO RECORD HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 8 FAST-GROWING DRIVE BY WIRE APPLICATIONS TO CREATE HIGH-VALUE OPPORTUNITY POCKETS

- FIGURE 9 THROTTLE BY WIRE SEGMENT TO BE DOMINANT DURING FORECAST PERIOD

- FIGURE 10 PASSENGER CAR TO SURPASS OTHER SEGMENTS IN THROTTLE BY WIRE MARKET DURING FORECAST PERIOD

- FIGURE 11 BEV TO BE LARGEST SEGMENT IN THROTTLE BY WIRE MARKET DURING FORECAST PERIOD

- FIGURE 12 PASSENGER CAR TO BE LEADING SEGMENT IN BRAKE BY WIRE MARKET DURING FORECAST PERIOD

- FIGURE 13 BEV TO HOLD HIGHEST SHARE IN BRAKE BY WIRE MARKET DURING FORECAST PERIOD

- FIGURE 14 PASSENGER CAR SEGMENT TO BE PREVALENT IN STEER BY WIRE MARKET DURING FORECAST PERIOD

- FIGURE 15 BEV TO OUTPACE OTHER SEGMENTS IN STEER BY WIRE MARKET DURING FORECAST PERIOD

- FIGURE 16 TRUCK TO EXHIBIT FASTEST GROWTH IN SHIFT BY WIRE MARKET DURING FORECAST PERIOD

- FIGURE 17 FCEV TO BE FASTEST-GROWING SEGMENT IN SHIFT BY WIRE MARKET DURING FORECAST PERIOD

- FIGURE 18 PASSENGER CAR SEGMENT TO LEAD PARK BY WIRE MARKET DURING FORECAST PERIOD

- FIGURE 19 FCEV TO REGISTER HIGHER CAGR THAN OTHER SEGMENTS IN PARK BY WIRE MARKET DURING FORECAST PERIOD

- FIGURE 20 ASIA PACIFIC CAPTURED LARGEST MARKET SHARE IN 2025

- FIGURE 21 DRIVE BY WIRE MARKET DYNAMICS

- FIGURE 22 EVOLUTION OF NEXT-GENERATION E/E ARCHITECTURE

- FIGURE 23 CURRENT AND PROJECTED NUMBERS OF OPERATIONAL AUTONOMOUS VEHICLES, 2022-2030 (UNITS)

- FIGURE 24 ECOSYSTEM ANALYSIS

- FIGURE 25 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- FIGURE 26 SUPPLY CHAIN ANALYSIS

- FIGURE 27 PATENT ANALYSIS

- FIGURE 28 BRAKE BY WIRE MARKET, BY COMPONENT, 2025 VS. 2032 (USD MILLION)

- FIGURE 29 PARK BY WIRE MARKET, BY EV TYPE, 2025 VS. 2032 (USD MILLION)

- FIGURE 30 PARK BY WIRE MARKET, BY COMPONENT, 2025 VS. 2032 (USD MILLION)

- FIGURE 31 STEER BY WIRE MARKET, BY ICE VEHICLE TYPE, 2025 VS. 2032 (USD MILLION)

- FIGURE 32 STEER BY WIRE MARKET, BY EV TYPE, 2025 VS. 2032 (USD MILLION)

- FIGURE 33 STEER BY WIRE MARKET, BY SENSOR TYPE, 2025 VS. 2032 (USD MILLION)

- FIGURE 34 STEER BY WIRE MARKET, BY COMPONENT, 2025 VS. 2032 (USD MILLION)

- FIGURE 35 THROTTLE BY WIRE MARKET, BY ICE VEHICLE TYPE, 2025 VS. 2032 (USD MILLION)

- FIGURE 36 THROTTLE BY WIRE MARKET, BY EV TYPE, 2025 VS. 2032 (USD MILLION)

- FIGURE 37 THROTTLE BY WIRE MARKET, BY SENSOR TYPE, 2025 VS. 2032 (USD MILLION)

- FIGURE 38 THROTTLE BY WIRE MARKET, BY COMPONENT, 2025 VS. 2032 (USD MILLION)

- FIGURE 39 L2 AUTONOMOUS VEHICLE DRIVE BY WIRE MARKET, BY APPLICATION, 2025 VS. 2032 (THOUSAND UNITS)

- FIGURE 40 L3 AUTONOMOUS VEHICLE DRIVE BY WIRE MARKET, BY APPLICATION, 2025 VS. 2032 (THOUSAND UNITS)

- FIGURE 41 L4/L5 AUTONOMOUS VEHICLE DRIVE BY WIRE MARKET, BY APPLICATION, 2025 VS. 2032 (THOUSAND UNITS)

- FIGURE 42 DRIVE BY WIRE MARKET, BY REGION, 2025 VS. 2032 (USD MILLION)

- FIGURE 43 ASIA PACIFIC: DRIVE BY WIRE MARKET, BY COUNTRY, 2025 VS. 2032 (USD MILLION)

- FIGURE 44 EUROPE: DRIVE BY WIRE MARKET, BY COUNTRY, 2025 VS. 2032 (USD MILLION)

- FIGURE 45 NORTH AMERICA: DRIVE BY WIRE MARKET, BY COUNTRY, 2025 VS. 2032 (USD MILLION)

- FIGURE 46 REST OF THE WORLD: DRIVE BY WIRE MARKET, BY COUNTRY, 2025 VS. 2032 (USD MILLION)

- FIGURE 47 MARKET SHARE ANALYSIS OF KEY PLAYERS, 2024

- FIGURE 48 REVENUE ANALYSIS OF TOP LISTED PUBLIC PLAYERS, 2020-2024

- FIGURE 49 COMPANY VALUATION (USD BILLION)

- FIGURE 50 FINANCIAL METRICS (EV/EBITDA)

- FIGURE 51 COMPANY EVALUATION MATRIX (KEY PLAYERS), 2024

- FIGURE 52 COMPANY FOOTPRINT

- FIGURE 53 COMPANY EVALUATION MATRIX (START-UPS/SMES), 2024

- FIGURE 54 ROBERT BOSCH GMBH: COMPANY SNAPSHOT

- FIGURE 55 CONTINENTAL AG: COMPANY SNAPSHOT

- FIGURE 56 ZF FRIEDRICHSHAFEN AG: COMPANY SNAPSHOT

- FIGURE 57 NEXTEER AUTOMOTIVE: COMPANY SNAPSHOT

- FIGURE 58 HITACHI, LTD.: COMPANY SNAPSHOT

- FIGURE 59 HL MANDO CORP.: COMPANY SNAPSHOT

- FIGURE 60 JTEKT CORPORATION: COMPANY SNAPSHOT

- FIGURE 61 THYSSENKRUPP AG: COMPANY SNAPSHOT

- FIGURE 62 FICOSA INTERNATIONAL SA: COMPANY SNAPSHOT

- FIGURE 63 KONGSBERG AUTOMOTIVE: COMPANY SNAPSHOT

- FIGURE 64 CURTISS-WRIGHT CORPORATION: COMPANY SNAPSHOT

- FIGURE 65 RESEARCH DESIGN

- FIGURE 66 RESEARCH DESIGN MODEL

- FIGURE 67 RESEARCH METHODOLOGY: HYPOTHESIS BUILDING

- FIGURE 68 BOTTOM-UP APPROACH

- FIGURE 69 TOP-DOWN APPROACH

- FIGURE 70 DATA TRIANGULATION

- FIGURE 71 FACTOR ANALYSIS FOR MARKET SIZING: DEMAND AND SUPPLY SIDES

线传市场:按执行器类型、转向技术、变速箱类型、车辆驱动系统和车辆类型划分-2026年至2032年全球市场预测

线传市场:按执行器类型、转向技术、变速箱类型、车辆驱动系统和车辆类型划分-2026年至2032年全球市场预测 2026年全球线传市场报告

2026年全球线传市场报告 2026-2034年全球线传市场规模、份额、趋势及成长分析报告

2026-2034年全球线传市场规模、份额、趋势及成长分析报告 线传市场规模、份额和成长分析(按应用、组件、感测器类型、公路车辆、非公路用车辆和地区划分)-2026-2033年产业预测

线传市场规模、份额和成长分析(按应用、组件、感测器类型、公路车辆、非公路用车辆和地区划分)-2026-2033年产业预测 线控驱动市场:按应用、车辆类型、零件和地区划分2026-2032 年线传市场:依车型、技术、零件和地区划分

线控驱动市场:按应用、车辆类型、零件和地区划分2026-2032 年线传市场:依车型、技术、零件和地区划分 全球线控驱动市场规模研究(按应用、车辆类型、组件和 2022-2032 年区域预测)

全球线控驱动市场规模研究(按应用、车辆类型、组件和 2022-2032 年区域预测) 到 2030 年的线控驾驶市场预测:按车型、零件、自主程度、技术、应用、最终用户和地区进行全球分析

到 2030 年的线控驾驶市场预测:按车型、零件、自主程度、技术、应用、最终用户和地区进行全球分析