|

市场调查报告书

商品编码

1872363

全球实体门禁控制市场(2025-2030)-硬体、软体和身分验证The Physical Access Control Business 2025 to 2030 - Hardware, Software & Credentials Market Analysis |

||||||

实体门禁控制系统 (PACS) 正从独立的门禁安全系统向软体定义平台演进,这些平台由云端架构、行动身分验证和人工智慧 (AI) 驱动,是智慧建筑营运的核心。这正在改变企业保护设施、管理身分和优化工作场所体验的方式,为从製造商到系统整合商的所有利害关係人创造策略机会和竞争风险。

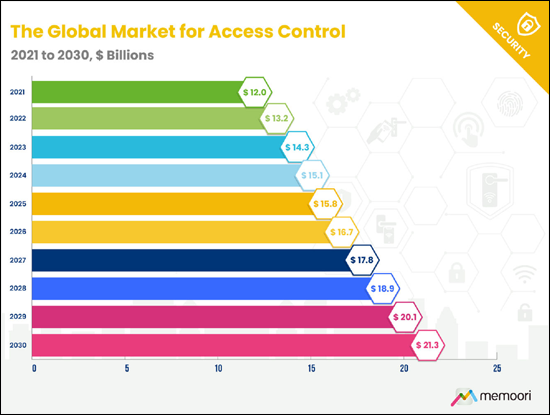

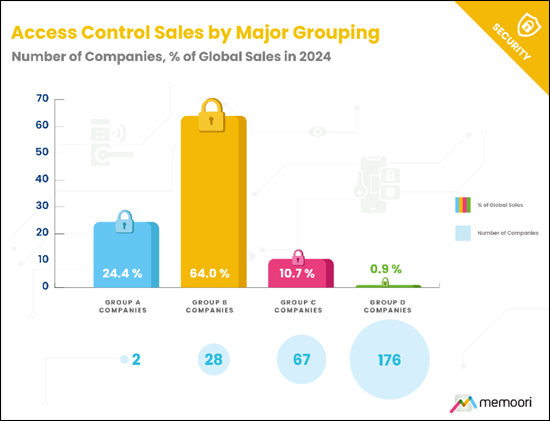

- 全球门禁控制市场规模预计将在 2024 年达到 151 亿美元,到 2030 年达到 213 亿美元,复合年增长率 (CAGR) 为 5.94%。 A 类公司(营收超过 10 亿美元)约占全球营收的 24.4%。 B 类公司(营收在 1 亿美元至 10 亿美元之间)包括28 家公司,平均营收为 3.27 亿美元,占全球销售额的 64%。

- 预计到 2030 年,亚太地区将超越欧洲,成为全球第二大市场。与成熟市场以翻新改造为推动力不同,亚太地区的成长将主要由办公大楼、物流设施、製造设施和政府设施的新建项目所推动。

- 从 2023 年 9 月到 2025 年 9 月,共完成 16 笔交易,总价值达 79 亿美元,其中以霍尼韦尔以 49.5 亿美元收购开利门禁业务最为引人注目。

- 随着经常性软体收入、託管服务和云端订阅取代传统的硬体利润率,价值获取方式正在发生巨大转变。

- 行动身分验证正在彻底改变组织授予、管理和撤销存取权限的方式。 市场正从专有应用程式验证转向直接内建于 Apple Wallet 和 Google Wallet 的钱包原生身分验证。这使得用户无需解锁装置即可实现轻触进入体验,并预设支援生物辨识身份验证。

创投对门禁控制平台的投资已从 2021 年的高峰大幅下降。 2023 年 9 月至 2025 年 9 月期间,该领域已揭露的融资额超过 3.26 亿美元,共达成 12 笔投资交易,资金主要集中在整合云端平台。 Verkada 以 45 亿美元的估值完成了 2 亿美元的 E 轮融资,而 Rhombus Systems 则完成了 4,500 万美元的 C 轮融资。这表明投资者对那些将门禁控制、视讯监控和环境感测器整合到单一管理平台的公司持续充满信心。

策略联盟作为创新结构性推动因素,其重要性日益凸显。身分验证供应商、智慧型手机製造商和云端平台供应商之间的合作正在加速行动身分验证的普及,并使多供应商生态系统走向标准化。

本报告考察了全球实体门禁控制市场,并分析了273家公司的绩效、产品组合和策略定位。

目录

前言

摘要整理

第一章:门禁控制业务结构与形成

- 门禁控制市场结构

- 公司分类与市占率

- 门禁控制市场价值链

- 销售与通路

- 定价、总拥有成本与生命週期经济学

第二章 门禁管制市场

- 门禁管制市场发展历程

- 市场动态、投资与采用趋势

- 市场管理

- 采用讯号与预算展望

- 投资重点

- 买方行为、采购与风险

- 市场规模与成长预测

- 市场规模与趋势:依地区划分

- 北美

- 拉丁美洲和加勒比海地区

- 亚太地区

- 欧洲

- 中东和非洲

- 市场规模与趋势:依产业划分

- 办公

- 政府

- 教育

- 製造和物流

- 医疗保健

- 零售

- 交通运输

- 饭店与餐饮服务

- 资料中心

- 娱乐和休閒

- 硬体

- 电子锁、无线锁、智慧锁

- 读卡机、扫描器、键盘

- 控制面板、伺服器

- 身份验证

- 依认证类型划分的市场规模

- 身份验证比较分析类型

- 磁条卡

- 近距离卡

- 智慧卡

- 行动钱包认证

- 生物辨识认证

- 条码/二维码

- 软体

- 以部署方式划分的软体市场

- 专用门禁软体

- 整合安全解决方案

- PIAM(实体身分和存取管理)

- 相关软体领域

第三章 IP、物联网与互通性

- IP 与物联网的融合

- 开放标准倡议

- 物联网成长与应用趋势

- IP 和物联网的优势

- IP 与物联网应用面临的挑战

- 用于门禁控制的边缘处理

- API、SDK 的兴起以及平台生态系统

第四章:云端与存取控制即服务 (ACaaS)

- 云端存取控制架构

- 云和 ACaaS 的采用趋势和预测

- 基于云端的存取控制的优势和挑战

- ACaaS 竞争格局与商业模式

第五章:存取控制中的人工智慧与机器学习

- 存取控制中的人工智慧创新与应用

- 人工智慧采用趋势

- 主要采用挑战和障碍

- 资料隐私与伦理考量

第六章:行动存取控制

- 行动存取控制技术与身分验证

- 行动采用趋势与市场动态

- 行动存取控制的竞争格局

第七章:生物辨识身份验证

- 生物辨识身分验证技术及模式

- 生物辨识身分验证应用趋势

- 生物辨识身分验证相关挑战

- 监管、法律及隐私权考量

- 生物辨识身分验证竞争格局

第八章:多因素身份验证与多技术领先者

- 多因素身份验证

- 多技术领先者

- 挑战与不足

第九章:系统整合与融合趋势

- 实体安全与逻辑安全的融合

- 视讯门禁整合

- 楼宇管理系统整合

第十章:供应链与製造趋势

- 供应链营运状况

- 地缘政治对供应的影响

- 区域化与本土化趋势

第11章:商业建筑与房地产市场

- 商业不动产与建筑市场对门禁管制需求的影响

- 值得关注的房地产趋势

- 商业建筑展望

第12章:技能、人才与劳动力

- 主要趋势与挑战

- 新兴机遇

第13章:网路安全与资料隐私

- 整合系统对网路安全的影响

- 威胁情势与主要漏洞

- 监理因素

- 网路安全最佳实践风险缓解

第十四章 永续性

- 永续性作为投资推动因素

- 使门禁系统更具永续性

- 面向永续性的门禁控制

- 标准、认证与买家期望

第十五章:併购

- 过往併购市场动态

- 最新併购交易

- 併购趋势及影响

第十六章:策略联盟

- 过往策略联盟及市场动态

- 最新策略联盟(2023年9月至2025年9月)

- 策略联盟趋势及影响

第十七章:投资趋势

- 过往投资交易及市场动态

- 最新投资交易

- 投资趋势及影响力

This report is an in-depth study providing a detailed market analysis of access control, with a specific focus on revenues generated by hardware, software & credentials.

Physical access control (PACS) is evolving from standalone door security into a software-defined platform at the center of smart building operations, with cloud architectures, mobile credentials, and artificial intelligence reshaping how organizations secure facilities, manage identities, and optimize workplace experiences, creating both strategic opportunities and competitive risks for everyone from manufacturers to systems integrators.

It is the second instalment of a two-part series covering Physical Security Technology. Part 1, covering Video Surveillance, was published in Q3 2025. Both these reports are included in Memoori's 2025 Premium Subscription Service.

Key Questions Addressed:

- What is the size and structure of the global access control market in 2025? The market reached $15.1 billion in 2024 and will grow to $21.3 billion by 2030 at a 5.94 percent CAGR. Group A companies (those with over $1 billion in revenues), together represent approximately 24.4 percent of global revenues. Group B (those with between $100 million and $1 billion) encompasses 28 companies with average revenues of $327 million, collectively accounting for 64 percent of global revenues.

- Which region offers the strongest growth opportunity through 2030? Asia Pacific will overtake Europe as the second-largest market by 2030. Unlike mature markets driven by retrofits, Asia Pacific growth comes from new construction across offices, logistics, manufacturing, and government facilities.

- How is M&A reshaping and consolidating the industry? 16 transactions totaling $7.9 billion were completed between September 2023 and September 2025, led by Honeywell's $4.95 billion acquisition of Carrier's access control business.

Within its 238 Pages and 13 Charts, This report presents all the key facts and draws conclusions, so you can understand what is shaping the future of the access control industry:

- Our comprehensive analysis of the global access control market is structured around 3 core revenue categories: hardware (electronic locks, readers, control panels, and supporting infrastructure), credentials (cards, mobile, biometrics, and alternative formats), and software (on-premises and cloud-based platforms). Our methodology evaluates 273 active companies worldwide, classifying vendors into four groups based on 2024 revenues and analyzing their financial performance, product portfolios, and strategic positioning.

- Value capture is shifting dramatically as recurring software revenue, managed services, and cloud subscriptions displace traditional hardware margins. This report maps these dynamics across vendor groups and identifies where profits are concentrating as the industry transitions from product sales to platform economics.

- Mobile credentials represent a significant transformation in how organizations provision, manage, and revoke access rights. The market is shifting from proprietary app-based credentials toward wallet-native credentials embedded directly in Apple Wallet and Google Wallet, enabling tap-to-enter experiences without unlocking devices and supporting biometric authentication by default. This report analyzes adoption patterns across vertical markets, quantifies infrastructure investment requirements, and evaluates competing standards.

This report provides valuable information into how physical security companies can develop their business strategy through mergers, acquisitions, and alliances.

Venture capital investment in access control platforms declined sharply from peak inflows in 2021. Between September 2023 and September 2025, 12 investment deals directed well over $326 million in disclosed funding into the sector, with capital concentrating around unified cloud platforms. Verkada secured $200 million in Series E funding at a $4.5 billion valuation, while Rhombus Systems raised a $45 million Series C round, demonstrating continued investor confidence in companies integrating access control, video surveillance, and environmental sensors into single management platforms.

Strategic partnerships have become important as structural enablers of innovation, with alliances between credential providers, smartphone manufacturers, and cloud platform vendors accelerating mobile credential adoption and normalizing multi-vendor ecosystems.

The report documents funding rounds, analyzes which technologies and business models are attracting capital, maps strategic alliances shaping interoperability standards, and identifies which vendor partnerships deliver genuine integration versus marketing announcements, critical intelligence for buyers evaluating platform longevity and ecosystem risk.

Who Should Buy This Report?

The information in this report will be of value to all those engaged in managing, operating, and investing in electronic security technology companies (and their advisors) around the world. In particular, those wishing to acquire, merge or sell companies will find its contents particularly useful.

Table of Contents

Preface

Executive Summary

1. The Structure & Shape of the Access Control Business

- 1.1. Access Control Market Structure

- 1.2. Company Classifications & Market Share

- 1.3. Access Control Market Value Chain

- 1.4. Sales & Distribution Channels

- 1.5. Pricing, TCO and Lifecycle Economics

2. The Access Control Market

- 2.1. The Evolution of the Access Control Market

- 2.2. Market Dynamics, Investment & Adoption Trends

- 2.2.1. Market Operating Conditions

- 2.2.2. Adoption Signals and Budget Outlook

- 2.2.3. Investment Priorities

- 2.2.4. Buyer Behavior, Procurement and Risk

- 2.3. Market Size & Growth Forecasts

- 2.4. Market Size & Trends by Region

- 2.4.1. North America

- 2.4.2. Latin America & The Caribbean

- 2.4.3. Asia Pacific

- 2.4.4. Europe

- 2.4.5. Middle East & Africa

- 2.5. Market Size & Trends by Vertical

- 2.5.1. Offices

- 2.5.2. Government

- 2.5.3. Education

- 2.5.4. Manufacturing & Logistics

- 2.5.5. Healthcare

- 2.5.6. Retail

- 2.5.7. Transport

- 2.5.8. Hospitality & Food Services

- 2.5.9. Datacenters

- 2.5.10. Entertainment / Leisure

- 2.6. Hardware

- 2.6.1. Electronic, Wireless & Smart Locks

- 2.6.2. Readers, Scanners & Keypads

- 2.6.3. Control Panels and Servers

- 2.7. Credentials

- 2.7.1. Market Size by Credential

- 2.7.2. Comparative Analysis of Credential Types

- 2.7.3. Magnetic Stripe Cards

- 2.7.4. Proximity Cards

- 2.7.5. Smart Cards

- 2.7.6. Mobile-Wallet Credentials

- 2.7.7. Biometrics

- 2.7.8. Barcodes/QR Codes

- 2.8. Software

- 2.8.1. Software Market by Deployment Method

- 2.8.2. Dedicated Access Control Software

- 2.8.3. Unified Security Solutions

- 2.8.4. PIAM (Physical Identity and Access Management)

- 2.8.5. Related Software Domains

3. IP, IoT, and Interoperability

- 3.1. The Convergence of IP and IoT

- 3.2. Open Standards Initiatives

- 3.3. IoT Growth & Adoption Trends

- 3.4. The Benefits of IP & IoT

- 3.5. IP and IoT Adoption Challenges

- 3.6. Edge Processing for Access Control

- 3.7. APIs, SDKs the Rise of Platform Ecosystems

4. The Cloud & ACaaS

- 4.1. Cloud Architectures in Access Control

- 4.2. Cloud & ACaaS Adoption Trends & Forecasts

- 4.3. Benefits & Challenges of Cloud-Based Access Control

- 4.4. ACaaS Competitive Landscape & Business Models

5. AI & Machine Learning in Access Control

- 5.1. AI Innovations & Applications for Access Control

- 5.2. AI Adoption Trends

- 5.3. Key Adoption Challenges & Barriers

- 5.4. Data Privacy & Ethical Considerations

6. Mobile Access Control

- 6.1. Mobile Access Control Technologies & Credentials

- 6.2. Mobile Adoption Trends & Market Dynamics

- 6.3. Mobile Access Control Competitive Landscape

7. Biometrics

- 7.1. Biometrics Technologies & Modalities

- 7.2. Biometric Adoption Trends

- 7.3. Biometrics Related Challenges

- 7.4. Regulatory, Legal & Privacy Considerations

- 7.5. Biometrics Competitive Landscape

8. Multifactor Authentication & Multi Technology Readers

- 8.1. Multifactor Authentication

- 8.2. Multi Technology Readers

- 8.3. Challenges and Drawbacks

9. Systems Integration & Convergence Trends

- 9.1. Physical-Logical Security Convergence

- 9.2. Video-Access Integration

- 9.3. Building Management Systems Integration

10. Supply Chain & Manufacturing Trends

- 10.1. Supply Chain Operating Conditions

- 10.2. Geopolitical Impacts on Supply

- 10.3. Regionalization and onshore trends

11. Commercial Construction & Real Estate Markets

- 11.1. Influence of CRE and Construction Markets on Access Control Demand

- 11.2. Notable Real Estate Trends

- 11.3. Commercial Construction Outlook

12. Skills, Talent & Labor

- 12.1. Key Trends & Challenges

- 12.2. Emerging Opportunities

13. Cybersecurity & Data Privacy

- 13.1. Cybersecurity Implications of Converged Systems

- 13.2. Threat Landscape & Notable Vulnerabilities

- 13.3. Regulatory Drivers

- 13.4. Best Practices for Cyber Risk Mitigation

14. Sustainability

- 14.1. Sustainability as an Investment Driver

- 14.2. Making Access Control Systems More Sustainable

- 14.3. Access Control as a Sustainability Enabler

- 14.4. Standards, Certifications, and Buyer Expectations

15. Mergers & Acquisitions

- 15.1. Historic M&A Market Dynamics

- 15.2. New M&A Deals

- 15.3. M&A Trends and Implications

16. Strategic Alliances

- 16.1. Historic Strategic Alliances and Market Dynamics

- 16.2. New Strategic Alliances (September 2023 to September 2025)

- 16.3. Strategic Alliance Trends and Implications

17. Investment Trends

- 17.1. Historic Investment Deals & Investment Market Dynamics

- 17.2. New Investment Deals

- 17.3. Investment Trends and Implications

List of Charts and Figures

- Fig 1.1: Access Control Market Structure

- Fig 1.2: Access Control Sales by Major Grouping, Number of Companies, % of Global Sales in 2024

- Fig 1.3: Market Share of Global Access Control Sales by Major Vendor 2024

- Fig 2.1: The Security Market Index (SMI)

- Fig 2.2: The Global Market for Access Control 2021 to 2030, $ Billions

- Fig 2.3: The Global Market for Access Control by Category 2021 to 2030, $ Billions

- Fig 2.4: Access Control Sales by Region 2024 & 2030, $ Billions

- Fig 2.5: Distribution of Access Control Sales by Building Type 2024, $ Billions

- Fig 2.6: The Global Market for Access Hardware by Sub-Category 2021 to 2030, $ Billions

- Fig 2.7: The Global Market for Access Control Credentials by Sub-Category 2021 to 2030, $ Billions

- Fig 2.8: The Global Market for Access Control Software, On-Premises vs Cloud Based 2021 to 2030, $ Billions

- Fig 11.1: Annual Change in Global Non-Residential Construction Sector Output

- Fig 11.2: Annual Change in Global Construction by Region

电子门锁平板电脑市场报告:趋势、预测与竞争分析(至2035年)

电子门锁平板电脑市场报告:趋势、预测与竞争分析(至2035年) 门禁控制市场:按产品类型、组织规模和最终用户产业分類的全球市场预测,2026-2032年

门禁控制市场:按产品类型、组织规模和最终用户产业分類的全球市场预测,2026-2032年 2026年全球活动安保服务市场报告

2026年全球活动安保服务市场报告 门禁控制市场分析及预测(至2035年):类型、产品类型、服务、技术、组件、应用、部署、最终用户、功能、安装配置2026年全球数位徽章门禁资料中心市场报告多门门禁系统市场:按组件、门禁技术、门类型、安装类型和最终用户产业划分-2026-2032年全球预测门禁系统市场:依产品类型、认证技术、通讯技术、开/关方式、安装类型和最终用户划分-2026-2032年全球预测2026年全球门禁管制市场报告2026年全球门禁系统市场报告安全系统门禁控制市场:依组件、技术、最终用户、部署模式和组织规模划分,全球预测,2026-2032年

门禁控制市场分析及预测(至2035年):类型、产品类型、服务、技术、组件、应用、部署、最终用户、功能、安装配置2026年全球数位徽章门禁资料中心市场报告多门门禁系统市场:按组件、门禁技术、门类型、安装类型和最终用户产业划分-2026-2032年全球预测门禁系统市场:依产品类型、认证技术、通讯技术、开/关方式、安装类型和最终用户划分-2026-2032年全球预测2026年全球门禁管制市场报告2026年全球门禁系统市场报告安全系统门禁控制市场:依组件、技术、最终用户、部署模式和组织规模划分,全球预测,2026-2032年