|

市场调查报告书

商品编码

1237838

线性低密度聚乙烯 (LLDPE) 市场 - 增长、趋势、COVID-19 的影响和预测 (2023-2028)Linear Low-Density Polyethylene (Lldpe) Market - Growth, Trends, And Forecasts (2023 - 2028) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

在预测期内,全球线性低密度聚乙烯 (LLDPE) 市场预计将以超过 5% 的复合年增长率增长。

由于 COVID-19 的影响,线性低密度聚乙烯生产和乙烯原料供应链受到严重影响,但最终将在 2021 年恢復。 由于卫生和安全问题,包装行业出现了巨大的激增,这将增加对 LLDPE 市场的需求,预计 2022 年将进一步復苏。 汽车、医疗保健、电子商务和包装行业是线性低密度聚乙烯的主要终端用户行业。

主要亮点

- 推动所研究市场增长的主要因素是对包装的需求不断增加以及对薄膜和片材的需求激增。

- 另一方面,在预测期内,用其他聚乙烯产品替代和禁止使用塑料将降低市场增长。

- 茂金属线性低密度聚乙烯 (mLLDPE) 由于其比 LLDPE 更好的抗渗透性,因此在未来可能会带来机会。

线性低密度聚乙烯 (LLDPE) 的市场趋势

LLDPE薄膜需求增加

- 线性低密度聚乙烯 (LLDPE) 具有较高的衝击强度、抗拉强度、抗穿刺性和伸长率等特性,因此被用于包装行业。

- 食品和饮料製造商在包装中使用 LLDPE 薄膜来保护产品免受有害化学物质的侵害并降低水分含量。 近年来,由于全球预蒸和预蒸製品的增加,LLDPE的市场份额猛增。

- 可支配收入的增加以及对快餐和送餐服务的日益偏好导致对 LLDPE 薄膜的需求不断增长。

- 在经历了 2020 年的低迷之后,由于 COVID-19 影响了许多最终用途行业,全球包装行业在 2021 年恢復了稳定增长。

- 包装是LLDPE薄膜最广泛的应用。 中国、美国、日本、印度和德国是世界上包装工业增长速度最快的国家之一。

- 电子商务行业的快速增长与电子商务包装中对 LLDPE 的需求直接相关。

- 预计在预测期内,上述所有因素都会对包装行业对 LLDPE 薄膜的需求产生重大影响。

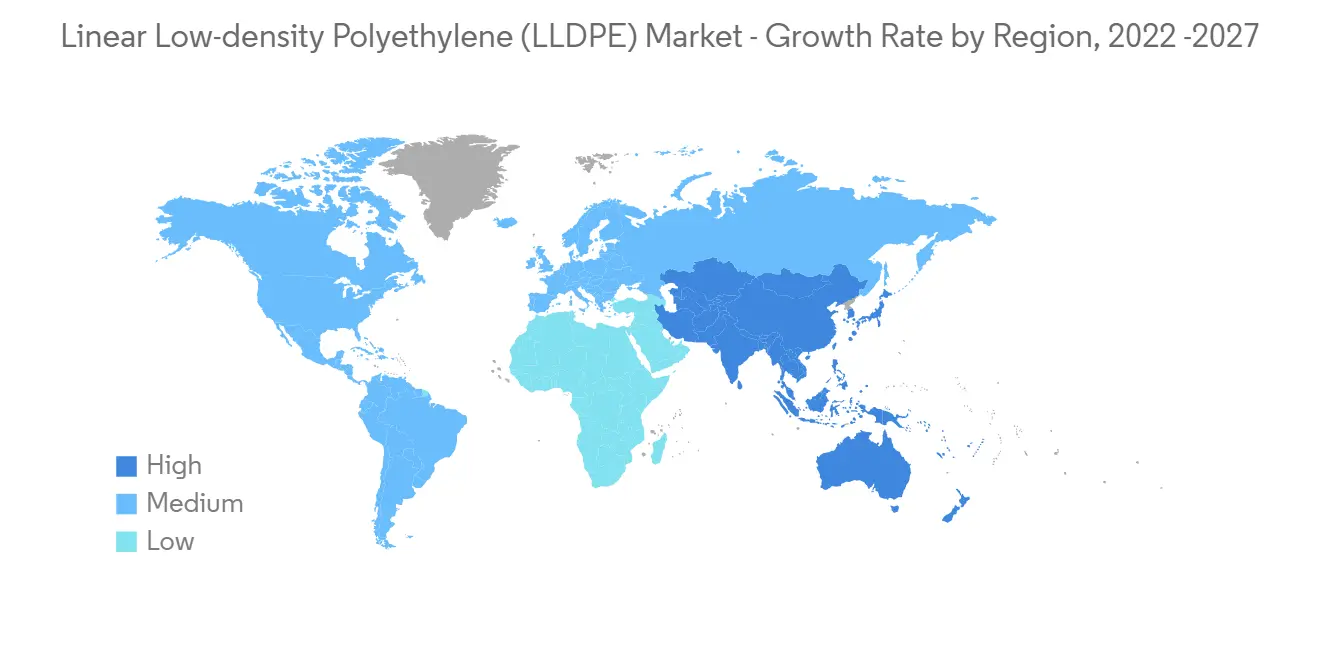

亚太地区主导市场

- 由于快速工业化和对基于 LLDPE 的包装材料的需求不断增长,亚太地区在线性低密度聚乙烯 (LLDPE) 市场中占有最大份额。 在亚洲市场,随着製药、食品加工和汽车行业製造活动的加强,包装业务正在快速扩张。

- 预计到 2025 年,中国包装行业的复合年增长率将达到惊人的近 6.8%,达到 2000 亿美元。 包装行业的这种势头有望提振该国对 LLDPE 的市场需求。

- 在包装行业,主要使用 LLDPE 薄膜。 LLDPE还用于注塑製造,如汽车塑料部件、玩具和水瓶。 注塑成型的增加也将增加LLDPE市场。

- 据 OICA 称,亚太地区的汽车塑料零部件市场有望增长。 2021年中国汽车产量将达到2608万美元。 据估计,汽车产量的增加将推动所研究市场的需求。

- 印度的食品加工是最大的包装消费者,占 45%,其次是药品和个人护理产品。 这些最终用户群不断增长的需求创造了巨大的扩张潜力。

- 由于这些因素,预计线性低密度聚乙烯市场在预测期内将在亚太地区享有高需求。

其他好处

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

内容

第一章介绍

- 调查先决条件

- 调查范围

第二章研究方法论

第 3 章执行摘要

第四章市场动态

- 司机

- 包装行业的需求增加

- 对薄膜和片材的需求激增

- 约束因素

- 用其他聚乙烯产品替代

- 工业价值链分析

- 搬运工五力分析

- 供应商的议价能力

- 消费者的议价能力

- 新进入者的威胁

- 替代产品和替代服务的威胁

- 竞争程度

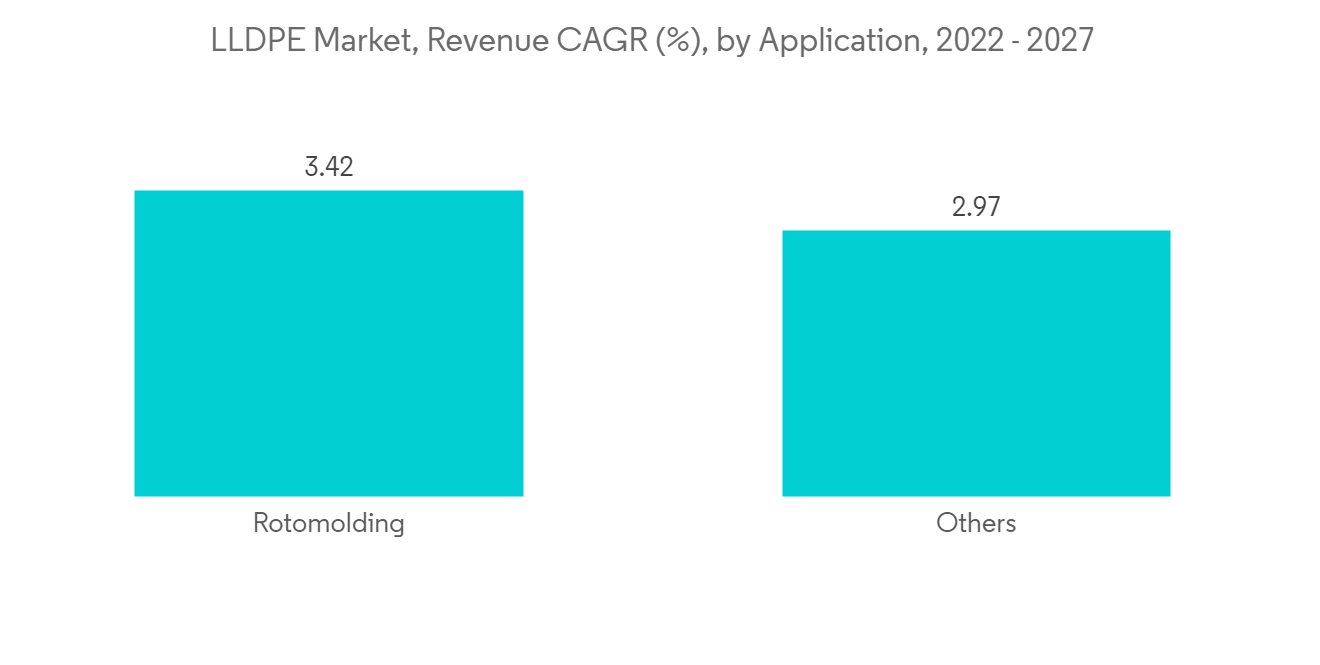

第 5 章市场细分

- 申请

- 电影

- 成型

- 注塑成型

- 其他应用程序类型

- 最终用户行业

- 农业

- 电气/电子

- 包装

- 建筑

- 其他最终用户行业

- 地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 其他亚太地区

- 北美

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 意大利

- 法国

- 其他欧洲

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中东和非洲

- 沙特阿拉伯

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章竞争格局

- 併购、合资、合作、合同等。

- 市场份额 (%)**/排名分析

- 主要参与者采用的策略

- 公司简介

- Chevron Phillips Chemical Company

- CNPC

- Exxon Mobil Corporation

- Formosa Plastic Corporation

- INEOS

- LG Chem

- Lyonde Bassells Industries Holdings BV

- Mitsubishi Chemicals

- Nova Chemicals Corporate

- Reliance Industries Limited

- SABIC

- SINOPEC

- The Dow Chemical Company

第七章市场机会与未来趋势

- 製药行业对 LLDPE 的需求不断扩大

The Global Linear Low-density Polyethylene (LLDPE) market is estimated to register a CAGR of over 5% during the forecast period. Due to the impact of COVID-19, linear low-density polyethylene production and the ethylene raw material supply chain were highly affected but eventually recovered in 2021. Due to hygiene and safety concerns, the packaging industry has seen an enormous surge, thereby increasing the demand for the LLDPE market, which is expected to recover further in 2022. The automotive, healthcare, e-commerce, and packaging industries are among the major end-user industries of linear low-density polyethylene.

Key Highlights

- The major factors driving the growth of the market studied are the rise in demand for packaging and surging demand for film and sheets.

- On the flip side, substituting other polyethylene products and banning plastics reduce market growth during the forecast period.

- The development of Metallocene linear low-density polyethylene (mLLDPE) is likely to act as an opportunity in the future, mLLDPE has relatively more puncture resistance than LLDPE.

Linear Low-density Polyethylene Market Trends

Rise in Demand for LLDPE Films

- Linear low-density polyethylene is used in the packaging industry because of its properties, such as higher impact strength, tensile strength, puncture resistance, elongation, etc.

- Food and beverage manufacturing companies use LLDPE films for packaging to secure their product from harmful chemicals and less moisture content. The recent increase in ready-to-eat and pre-cooked products globally has surged LLDPE's market share.

- The growth in disposable income and the increasing preference for fast food and food delivery services contributed to increasing demand for LLDPE films.

- Following a dip in 2020, the global packaging industry resumed steady growth in 2021, as COVID-19 affected numerous end-use sectors.

- Packaging is the most extensive application of LLDPE films. China, the United States, Japan, India, and Germany are amongst the top countries with the fastest growth rate in the packaging industry across the world.

- Rapid growth in the e-commerce industry directly correlates to the LLDPE demand for e-commerce packaging.

- All the above factors are expected to significantly impact the demand for LLDPE films from the packaging industry during the forecast period.

Asia-Pacific Region to Dominate the Market

- The Asia-Pacific region accounts for the largest share of the Linear low-density polyethylene (LLDPE) market, owing to rapid industrialization and rising LLDPE-based packaging material demand in the region. The packaging business in the Asian market is expanding at a rapid pace with the increased manufacturing activities in the pharmaceutical, food processing, and automotive industries.

- The packaging industry in China is expected to register tremendous growth with a CAGR of nearly 6.8%, reaching USD 0.2 trillion by 2025. This positive momentum in the packaging industry is expected to boost the market demand for LLDPE in the country.

- The packaging industry primarily uses LLDPE films. LLDPE is also used in the injection molding manufacturing sectors in automotive plastic parts, toys, and water bottles. An increase in injection molding also increases the LLDPE market.

- According to the OICA, the Asia-Pacific automotive plastic parts market is expected to grow. In 2021, automotive production in China reached USD 26.08 million. The increase in automotive production is estimated to drive the demand for the market studied.

- Indian food processing is the largest consumer of packaging at 45%, followed by pharmaceuticals and personal care products. Increasing demand from these end-user segments is creating a huge potential for expansion.

- Due to all these factors, the market for linear low-density polyethylene is expected to have a high demand in the Asia-Pacific region during the forecast period.

Linear Low-density Polyethylene Market Competitor Analysis

The Linear low-density polyethylene LLDPE market is partially consolidated in nature. Some of the major players in the market include INEOS, Formosa Plastic Corporation, Dow, Mitsubishi Chemicals, LG Chem, Exxon Mobil Corporation, SINOPEC, SABIC, Lyondellbasell Industries Holdings BV, Reliance Industries Limited, and Chevron Phillips Chemical Company.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increase Demand from the Packaging Industry

- 4.1.2 Surging Demand for Film and Sheets

- 4.2 Restraints

- 4.2.1 Substitution of Other Polyethylene Products

- 4.3 Industry Value Chain Analysis

- 4.4 Poter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Thret of Substitute products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION

- 5.1 Application

- 5.1.1 Films

- 5.1.2 Molding

- 5.1.3 Injection Molding

- 5.1.4 Other Application Types

- 5.2 End-user Industry

- 5.2.1 Agricultute

- 5.2.2 Electrical and Electronics

- 5.2.3 Packaging

- 5.2.4 Constrution

- 5.2.5 Other End-user Industries

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Chevron Phillips Chemical Company

- 6.4.2 CNPC

- 6.4.3 Exxon Mobil Corporation

- 6.4.4 Formosa Plastic Corporation

- 6.4.5 INEOS

- 6.4.6 LG Chem

- 6.4.7 Lyonde Bassells Industries Holdings BV

- 6.4.8 Mitsubishi Chemicals

- 6.4.9 Nova Chemicals Corporate

- 6.4.10 Reliance Industries Limited

- 6.4.11 SABIC

- 6.4.12 SINOPEC

- 6.4.13 The Dow Chemical Company

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Demand for LLDPE in the Pharmaceutical Industry

茂金属线性低密度聚乙烯 (mLLDPE) 的全球市场分析:工厂产能、产量、运营效率、需求/供应、最终用户行业、对外贸易、销售渠道、区域需求、公司份额 (2015-2035)

茂金属线性低密度聚乙烯 (mLLDPE) 的全球市场分析:工厂产能、产量、运营效率、需求/供应、最终用户行业、对外贸易、销售渠道、区域需求、公司份额 (2015-2035) 全球LDPE和LLDPE密封卷材薄膜市场 - 2023-2030年

全球LDPE和LLDPE密封卷材薄膜市场 - 2023-2030年 线型低密度聚乙烯市场:依製程(气相、浆料环路、溶液相)、用途(薄膜、射出成型、滚塑成型)- 2023-2030 年全球预测

线型低密度聚乙烯市场:依製程(气相、浆料环路、溶液相)、用途(薄膜、射出成型、滚塑成型)- 2023-2030 年全球预测 线型低密度聚乙烯(LLDPE)的全球市场

线型低密度聚乙烯(LLDPE)的全球市场 线型低密度聚乙烯的全球市场:产业规模,占有率,趋势,机会,预测(2018年~2028年) - 不同生产过程,各用途,终端用户各业界,各地区,及竞争

线型低密度聚乙烯的全球市场:产业规模,占有率,趋势,机会,预测(2018年~2028年) - 不同生产过程,各用途,终端用户各业界,各地区,及竞争 LDPE/LLDPE 密封胶捲筒薄膜全球市场、规模、研究和预测:按材料类型(低密度聚乙烯、线性低密度聚乙烯)、厚度、应用、最终用户、地区,2022-2029 年

LDPE/LLDPE 密封胶捲筒薄膜全球市场、规模、研究和预测:按材料类型(低密度聚乙烯、线性低密度聚乙烯)、厚度、应用、最终用户、地区,2022-2029 年