|

市场调查报告书

商品编码

1248847

邮政服务市场 - COVID-19 的增长、趋势、影响和预测 (2023-2028)Postal Services Market - Growth, Trends, and Forecasts (2023 - 2028) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

在预测期内,邮政服务市场预计将以 1% 左右的复合年增长率增长。

COVID-19 的传播迫使各国关闭公共活动,改变了政府、企业和人们对邮政系统的看法。 随着越来越多的人被要求呆在家里以阻止病毒传播,邮政服务越来越被认为是重要的服务提供商。

主要亮点

- COVID-19 大流行在 2020 年抑制了邮政服务市场,因为政府封锁并限制人员和货物的流动以遏制感染的传播。 大流行已将行业增长从邮政收入推向包裹。 根据国际邮政公司 (IPC) 的数据,2020 年包裹收入增加了 193 亿欧元(217 亿美元),而邮政收入减少了 61 亿欧元(68□□ 亿美元)。

- 近年来,邮政服务行业受到互联网和数字行业的衝击。 随着向在线通信的转变,传统的核心邮政递送业务正在衰退。 同时,行业也面临着快速增长的电商包裹市场的激烈竞争。 因此,邮政和邮政业务正从国有垄断向多元化经营的商业企业转变。

- 目前,世界顶级邮政公司包括美国邮政 (USPS)、德国邮政 DHL(德国)、法国邮政和日本邮政。

- 对邮政和邮寄服务的需求取决于交易量和公司的直接营销支出。 此外,个别公司的盈利能力取决于其营运效率。

- 最大的邮政和邮寄市场包括中国、美国、英国、法国、德国和意大利。 高增长市场包括加拿大、印度、葡萄牙和新加坡。

- 2021 年,全球邮政和快递活动的主要市场是德国、英国、法国、意大利和荷兰。 展望未来,数据分析的引入、技术发展以及自动驾驶和电动汽车的使用可能会对市场产生积极影响。 未来,劳动力短缺等因素将阻碍邮政服务市场的增长。

邮政服务市场趋势

电子商务扩展邮政服务的可能性

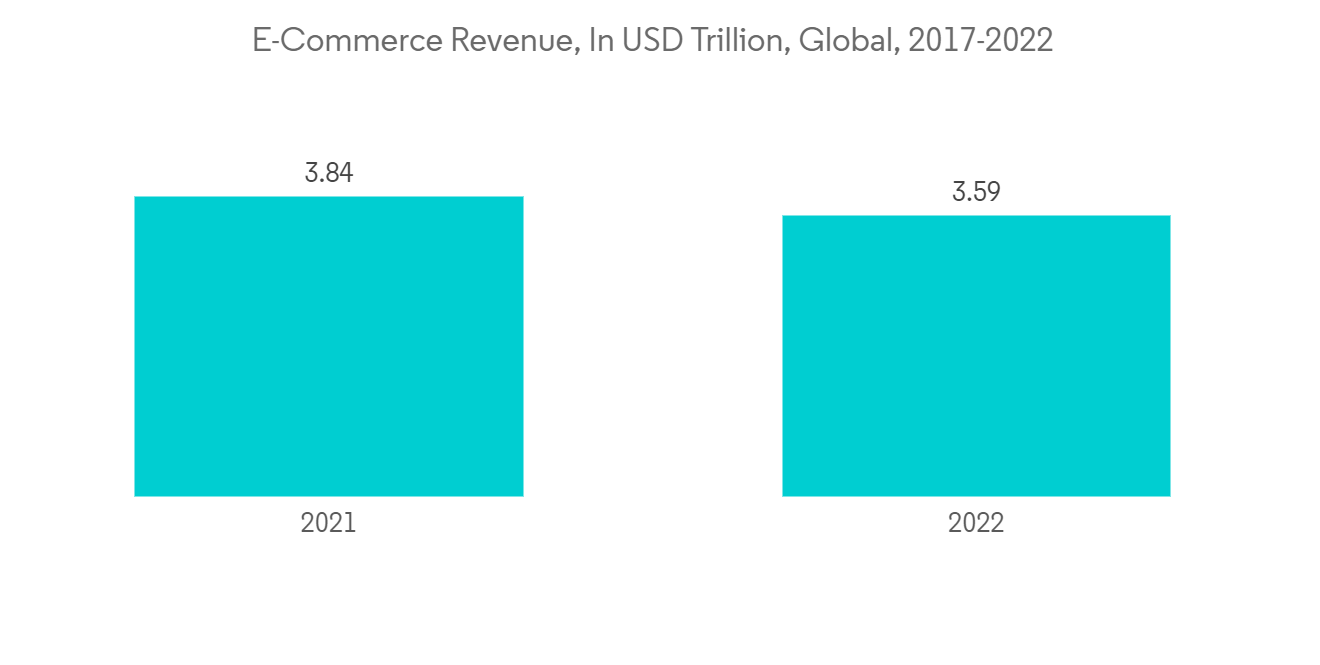

电子商务对邮政业务来说是一个巨大的机遇。 消费者越来越习惯于从新兴的电子商务平台在线订购产品,而传统的实体店也正在转向数字环境。 随着在线销售的兴起,电子商务运营商□□正在寻求具有成本效益的渠道来交付和收集所购买的商品。 在这方面,拥有全国网络和最后一英里交付经验的邮政运营商正在成为有效的合作伙伴。 例如,在肯尼亚,在线市场 Jumia 和肯尼亚邮政服务合作,允许客户在最近的邮局领取他们购买的 Jumia。

但是,世界各地的许多邮政运营商都没有做好充分利用电子商务增长的准备。 B2C 电子商务在全球范围内呈现 17% 的增长率,而邮政公司的包裹量增长不到 5%。 部分问题在于,在表现不佳的邮政运营商中,数字技术作为核心业务和创新驱动力的采用率较低。 凡是采用数字技术的地方,创新都将不可避免地发生。 例如,肯尼亚邮政推出了mPost,将每一部手机都变成了一个官方邮政地址,让信件和包裹在全国任何地方都可以访问。

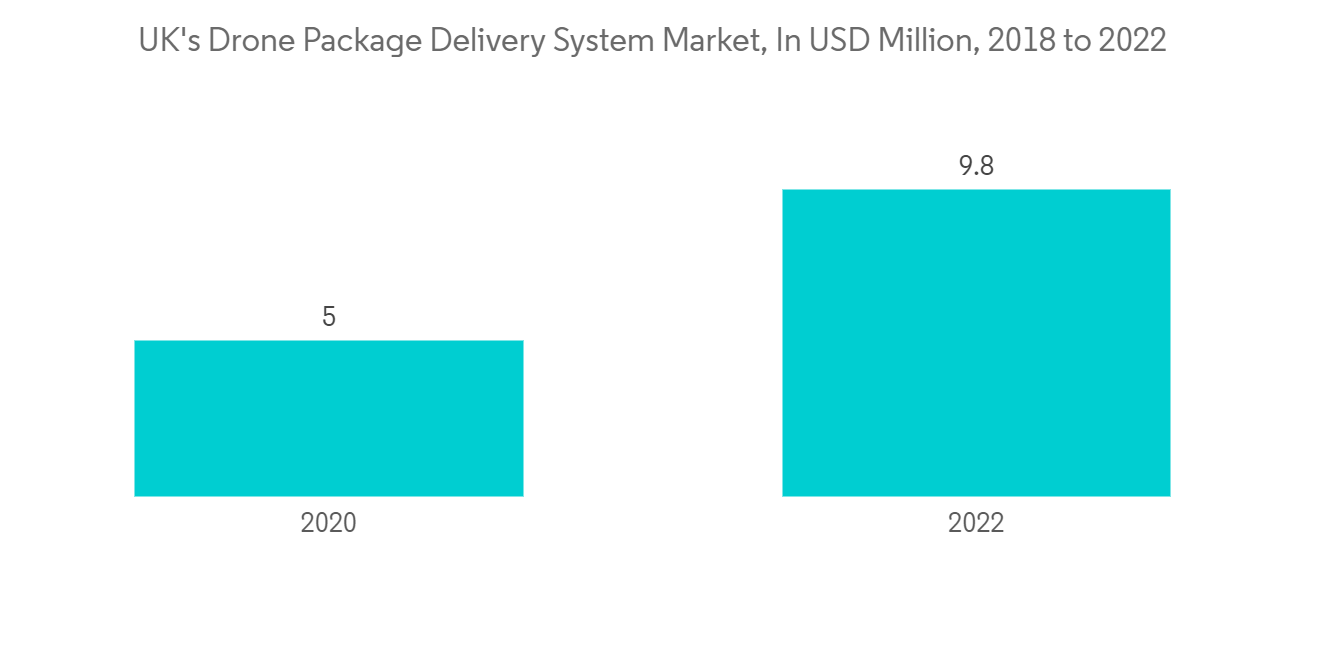

英国使用无人机改善邮件投递

COVID-19 疫情正在重新定义邮政和包裹行业对自主递送系统的需求。

United Kindome Royal Mail 计划在未来三年内推出 50 条新的“邮政无人机路线”,作为其增加使用交付无人机的一部分。 儘管需要航空管理局的许可,但与物流无人机运营商 Windracers 的合作将为农村地区提供更快、更实用的服务。 锡利岛、设得兰群岛、奥克尼群岛和赫布里底群岛将成为这项新服务的首批目的地。 皇家邮政计划在未来三年内使用多达 200 架,最终超过 500 架无人机,为英国的每个地区提供服务。 皇家邮政在过去一年半中进行了四次无人机试验,包括在苏格兰的马尔岛、康沃尔海岸的锡利岛以及奥克尼群岛的柯克沃尔和北罗纳德赛。 新服务的试飞在勒威克的廷沃尔机场和安斯特之间进行,单程距离为 50 英里。 信件和包裹随后由附近的邮递员和妇女使用这次采用的无人机运送。 无人机每天可以在岛屿之间往返两次,最多可携带 100 公斤的邮件。

邮政服务行业概览

该行业相当分散。 大公司具有广泛的基础设施和服务多样性的优势。 较小的公司通过提高专业化来竞争。 在大多数国家,政府拥有的邮政服务占据了大部分市场。 这些政府邮局通常垄断邮件投递,但面临来自私营包裹投递公司的激烈竞争。 相互竞争的运营商结成伙伴关係以利用彼此的优势。 例如,主要的快递公司联邦快递 (FedEx) 和联合包裹服务 (UPS) 将部分住宅递送外包给美国邮政服务 (USPS),后者又将空运外包给 FedEx 和 UPS。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

内容

第一章介绍

- 调查假设和市场定义

- 调查范围

第二章研究方法论

第 3 章执行摘要

第四章市场动态

- 当前市场情况

- 市场驱动因素

- 市场製约因素

- 市场机器

- 波特的五力分析

- 新进入者的威胁

- 买家/消费者的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争强度

- 价值链/供应链分析

- 关于 COVID-19 对市场的影响

第 5 章市场细分

- 按类型

- 快递邮政服务

- 标准邮政服务

- 按项目

- 来信

- 包裹

- 按目的地

- 国内航班

- 国际航班

- 按地区

- 北美

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 意大利

- 西班牙

- 其他欧洲

- 亚太地区

- 印度

- 中国

- 日本

- 其他亚太地区

- 世界其他地区

- 拉丁美洲

- 中东和非洲

- 北美

第六章竞争格局

- 市场集中度概述

- 公司简介

- United States Postal Services

- Deutsche Post DHL

- Le Groupe La Poste

- Royal Mail Group

- Japan Post

- Swiss Post

- Post NL

- Poczta Polska

- The Singapore Post

- The Australian Post AG

- China Post*

第七章期货市场

第8章附录

The postal services market is estimated to register a CAGR of approximately 1% during the forecast period. The spreading of COVID-19 has forced nations to suspend public activities, changing how governments, corporations, and people see the postal system. When more people are required to stay at home to stop the virus from spreading, posts are becoming more and more recognized as crucial service providers.

Key Highlights

- The COVID-19 outbreak restrained the postal services market in 2020 as governments imposed lockdowns and restricted the movement of people and goods to contain the transmission. The pandemic drove industry growth away from mail revenue and toward parcels. According to the International Post Corporation (IPC), the parcel revenue rose by EUR 19.3 billion (USD 21.7 billion), while mail revenue fell by EUR 6.1 billion (USD 6.8 billion) in 2020.

- Over recent years, the postal service industry has suffered disruptions from the internet and digital industries. The traditional core mail delivery business is declining as communications move online. Meanwhile, the industry also faces fierce competition in the rapidly growing e-commerce parcel market. As a result, postal and mailing businesses are shifting from state-owned monopolies to commercial companies with diversified portfolios.

- Currently, some of the top postal service companies across the world include the US Postal Service (USPS), Deutsche Post DHL (Germany), La Poste (France), and Japan Post.

- The demand for postal and mailing services depends on transaction volume and corporate spending on direct marketing. The profitability of individual companies depends on the efficiency of their operations.

- Some of the largest postal and mailing markets are China, the United States, the United Kingdom, France, Germany, and Italy. High-growth markets include Canada, India, Portugal, and Singapore.

- In 2021, the leading markets for postal and courier activities worldwide were Germany, the United Kingdom, France, Italy, and the Netherlands. In the future, the adoption of data analytics, technology development, and the use of automated and electric vehicles may positively impact the market. Factors that could hinder the growth of the postal services market in the future include workforce shortage, etc.

Postal Services Market Trends

E-commerce Opens Opportunities for Postal Services

E-commerce represents a tremendous opportunity for postal services as consumers become increasingly comfortable ordering items online from emerging e-commerce platforms, and traditional brick-and-mortar outlets are also transitioning to digital environments. As the volume of online sales increases, e-commerce providers are seeking cost-effective channels for the delivery and collection of purchased items. Postal services, with their long-established national networks and experience in last-mile delivery, are emerging as effective partners in this regard. In Kenya, for example, a partnership between online marketplace Jumia and the Postal Corporation of Kenya enables online shoppers to collect items they purchase on Jumia from their nearest post office.

However, many global postal services organizations are not equipped to take advantage of this growth in e-commerce. While B2C eCommerce is growing at a global rate of 17%, parcel volumes among postal services organizations have been growing at less than 5%. Part of the issue is the low adoption of digital technologies as core business and innovation drivers among low-performing postal services organizations. Where digital adoption is high, innovations inevitably emerge. The launch of mPost by Kenya's postal services, for example, has turned every mobile phone into a formal postal address, enabling people to access letters and parcels from anywhere in the country.

United Kingdom Boost the Postal Delivery Service by Drones

The COVID-19 epidemic is redefining how much the post and parcel sector needs autonomous delivery systems.

United Kindom: In the coming three years, Royal Mail will establish 50 new "postal drone routes" as part of its increased usage of drones for delivery. The move, which is subject to Civil Aviation Authority permission, would give rural communities speedier and more practical services thanks to cooperation with the logistics drone business Windracers. The Isles of Scilly, Shetland Islands, Orkney Islands, and the Hebrides are among the initial destinations for the new service. For the next three years, Royal Mail said it plans to utilize up to 200 drones, and eventually more than 500, to service every part of the UK. Four drone tests have been carried out by Royal Mail over the past 18 months, including flights over the Scottish Isle of Mull, the Isles of Scilly off the coast of Cornwall, and the Orkney Islands' Kirkwall and North Ronaldsay. Between Tingwall Airport in Lerwick and Unst, a 50-mile journey each way, test flights for the new service have been conducted. Letters and packages are subsequently carried by the neighborhood postman or lady using the drones employed in the study, which can carry up to 100kg of mail for two daily return trips between the islands.

Postal Services Industry Overview

The industry is moderately fragmented. Large companies have advantages in widespread infrastructure and diversity of services. Small companies compete by specializing. Most nations have a government-owned postal service that controls a major portion of the market there. These Government-owned postal agencies typically have a monopoly on mail delivery but face heavy competition from private package delivery companies. The competing entities form partnerships to capitalize on each other's strengths. For instance, major express delivery companies Federal Express (FedEx) and United Parcel Service (UPS) contract certain residential deliveries to the US Postal Service (USPS), while the USPS contracts air transportation out to FedEx and UPS.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Current Market Scenario

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Market Opportunities

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 Value Chain/Supply Chain Analysis

- 4.7 Impact of COVID-19 on the Market

5 MARKET SEGMENTATION

- 5.1 By Type

- 5.1.1 Express Postal Services

- 5.1.2 Standard Postal Services

- 5.2 By Item

- 5.2.1 Letter

- 5.2.2 Parcel

- 5.3 By Destination

- 5.3.1 Domestic

- 5.3.2 International

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 India

- 5.4.3.2 China

- 5.4.3.3 Japan

- 5.4.3.4 Rest of Asia-Pacific

- 5.4.4 Rest of the World

- 5.4.4.1 Latin America

- 5.4.4.2 Middle East & Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration Overview

- 6.2 Company Profiles

- 6.2.1 United States Postal Services

- 6.2.2 Deutsche Post DHL

- 6.2.3 Le Groupe La Poste

- 6.2.4 Royal Mail Group

- 6.2.5 Japan Post

- 6.2.6 Swiss Post

- 6.2.7 Post NL

- 6.2.8 Poczta Polska

- 6.2.9 The Singapore Post

- 6.2.10 The Australian Post AG

- 6.2.11 China Post*