|

市场调查报告书

商品编码

1273386

锂化合物市场 - 增长、趋势、COVID-19 影响和预测 (2023-2028)Lithium Compounds Market - Growth, Trends, and Forecasts (2023 - 2028) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

在预测期内,锂化合物市场预计将以超过 8% 的复合年增长率增长。

主要亮点

- COVID-19 大流行对锂化合物市场产生了重大影响。 全球约束影响了汽车、建筑、陶瓷和玻璃行业。 儘管如此,製药业务的需求有所增加,并且在大流行期间市场继续增长。 但是,从 2021 年开始,每个行业都增加了产量,预计市场将在整个预测期内跟进。

- 电池使用量的增加,尤其是在电动汽车中的使用,以及陶瓷和玻璃行业不断增长的需求正在推动锂化合物市场向前发展。 相反,这些化合物的高成本及其被其他替代品的替代预计会阻碍市场增长。

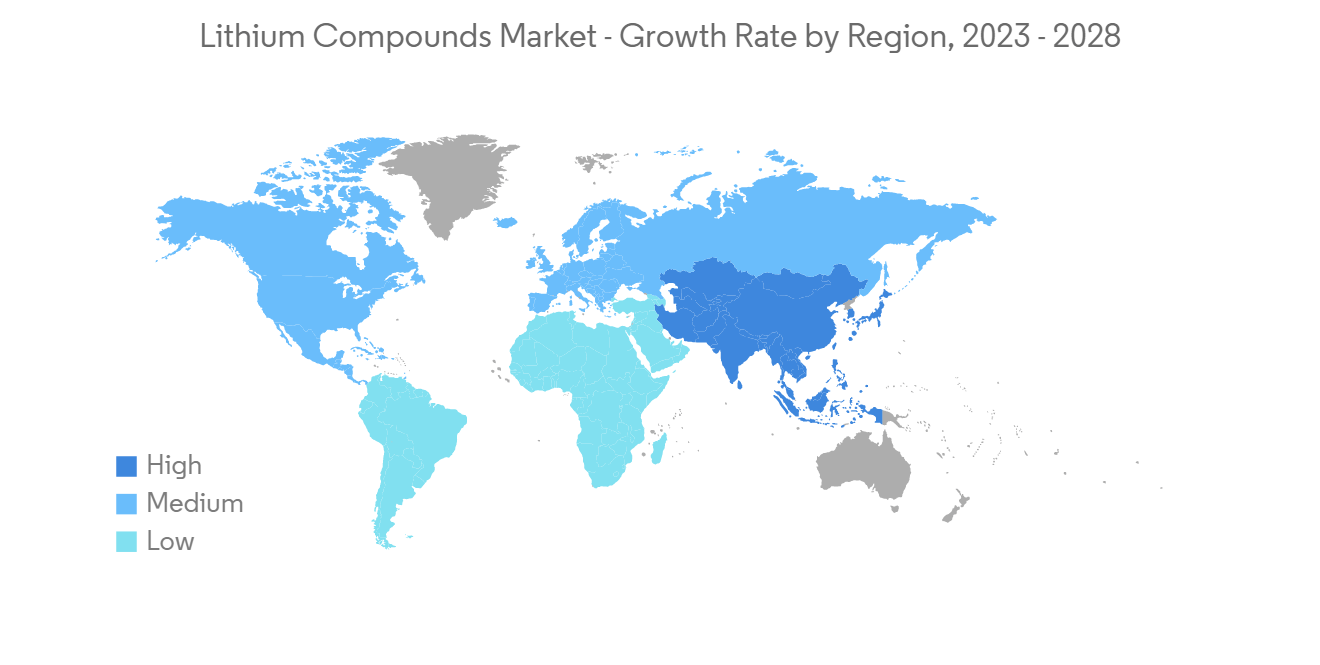

- 不过,对电动汽车不断增长的需求似乎为市场研究提供了契机。 由于建筑和汽车行业的大量支出,亚太地区是最大的锂化合物市场,并且在预测期内仍将占据主导地位。

锂化合物市场趋势

电池需求扩大

- 锂化合物广泛用于锂离子二次电池技术,用于储能和保存。 锂离子二次电池用于手机、照相机、笔记本电脑、动力设备和汽车等设备。

- 锂离子电池在内燃机汽车和电动汽车中都发挥着重要作用。 锂离子电池具有能量密度高、自放电率低、循环寿命长、维护成本低、充电快、重量轻等优点,成为汽车领域的首选。 对镍镉电池的需求也很高,目前用于一些混合动力电动汽车。 与往年相比,印度、东南亚和韩国的混合动力汽车销量和需求均呈现合理增长。

- 根据经济分析局 (BEA) 的数据,2022 年第三季度美国电气设备、设备和组件製造业的增加值约为 738 亿美元,比去年同期增长约 8%去年同期。 前三季度增加值总额接近2200亿美元。

- 此外,美国计算机和电子製造业的总产值在 2022 年前三个季度达到约 1.3 万亿美元。 与 2021 年同期(1.2 万亿美元)相比,2022 年增长 7%。

- 另一方面,国际能源署 (IEA) 在其 2022 年 9 月的电动汽车展望中宣布,儘管供应链受限且 COVID-19 疫情仍在持续,但报告销量的电动汽车数量创历史新高。 电动汽车销量较2020年翻了一番,达到660万辆,道路上行驶的电动汽车总数为1650万辆。

- 新兴市场中电动汽车数量的增加和电子设备使用的增加正在推动对二次电池的需求,这可能会在未来几年推动锂电池市场的发展。

亚太地区主导市场

- 在中国、印度、日本和韩国,电子、汽车、陶瓷和玻璃领域都高度发达,多年来持续投资发展电池技术领域。,亚太有望主导整个锂化合物市场。

- 在过去几年中,由于政府禁止使用内燃机并对内燃机车辆征收重税,中国和印度增加了电动和混合动力汽车的产量。

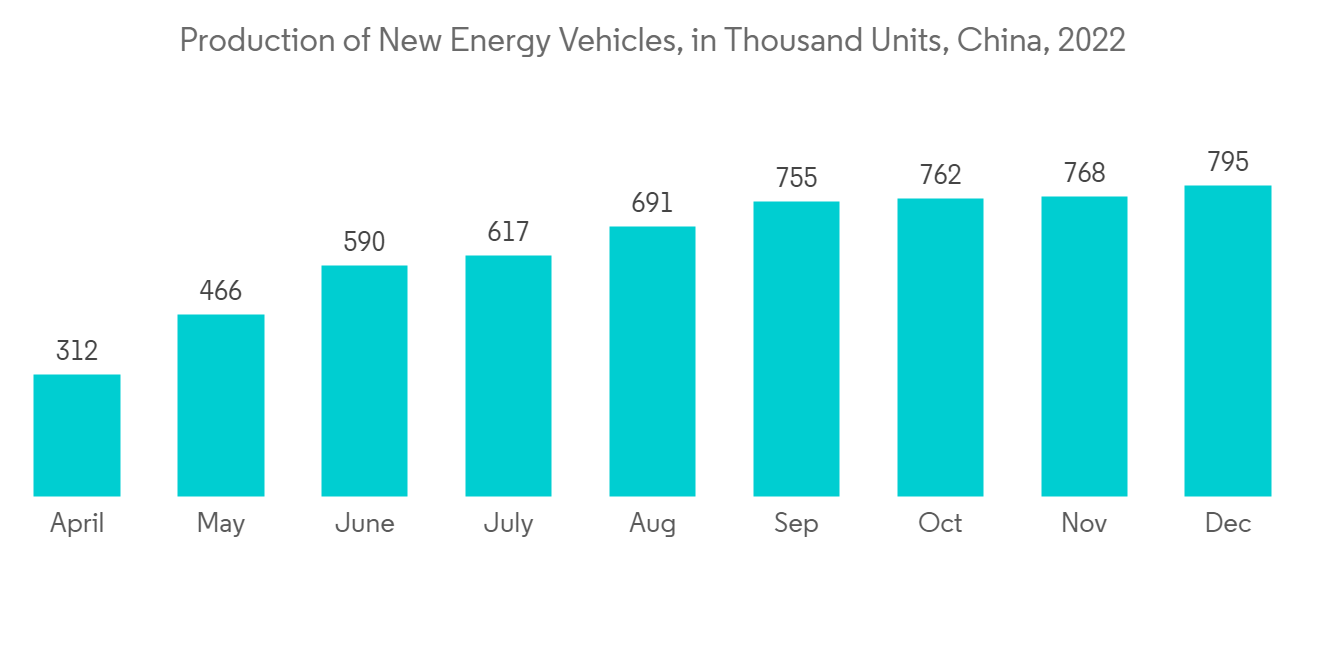

- 中国是最大的电动汽车生产国和消费国,约占全球市场的一半。 根据中国汽车工业协会(CAAM)的数据,2022 年中国新能源汽车(NEV)的总产量约为 700 万辆。 与2021年的产量(354万台)相比,更是实现了近97%的惊人增长。

- 过去几年,即使在印度,人们的注意力也一直集中在该国的电动汽车市场上。 CEEW 能源金融中心的一项研究发现,到 2030 年,印度的电动汽车机会将达到 2060 亿美元,需要 1800 亿美元投资于该国的汽车製造和充电基础设施。

- 根据 IQVIA 的预测,中国是世界第二大药品消费国,从 2021 年开始的五年内,该市场的销量将增长 8%,而支出将增长 19%,增速低于往常。重点可能是致力于扩大获得尖端药物的机会。

- 根据印度品牌资产基金会 (IBEF) 的建议,到 2030 年,印度的製药业预计也将达到 1300 亿美元。 该国是世界上最大的疫苗生产国,到 2021 年将占所有疫苗的 60%,成为世界第三大製药国。

- 根据印度化学和化肥部发布的统计数据,2022-23 年(至 2022 年 7 月)关键化学品的产量将比去年同期的 41.15 乳酸(4115 万吨)增长 5.73%。达43.51内酯(4351万吨)。

- 对高效电池的需求不断增长,这要求锂化合物的先进技术得到改进。 该地区节能设备的持续增长以及製药和化学工业的崛起预计将在未来几年推动锂化合物市场。

锂化合物产业概况

锂化合物市场具有部分整合的性质,少数大公司控制着市场的很大一部分。 主要公司包括 FMC Corporation、SQM SA、Lithium Americas Corp.、Albemarle Corporation 和 Neometals Ltd。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

内容

第一章介绍

- 调查先决条件

- 本次调查的范围

第二章研究方法论

第 3 章执行摘要

第四章市场动态

- 主持人

- 陶瓷和玻璃行业的需求增加

- 电池应用的扩展

- 约束因素

- 新替代品的进入

- 其他抑製剂

- 工业价值链分析

- 波特的五力分析

- 新进入者的威胁

- 买家的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争程度

第 5 章市场细分

- 化合物

- 氮化锂

- 金属锂

- 碳酸锂

- 氢氧化锂

- 氯化锂

- 丁基锂

- 其他化合物

- 申请

- 陶瓷/玻璃

- 润滑剂

- 医药

- 电池

- 化学品

- 冶金

- 其他用途

- 地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 其他亚太地区

- 北美

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 意大利

- 其他欧洲

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中东和非洲

- 沙特阿拉伯

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章竞争格局

- 併购、合资、合作、合同等。

- 市场份额 (%)/排名分析

- 主要公司采用的策略

- 公司简介

- Albemarle Corporation

- Allkem Limited

- China Lithium Products Technology Co., Ltd.

- FMC Corporation

- Lithium Americas Corp.

- Neometals Ltd

- Shanghai China Lithium Industrial Co. Ltd

- Sichuan Tianqi Lithium Chemicals Inc.

- SQM SA

第七章市场机会与未来趋势

- 对电动汽车的需求不断扩大

- 其他机会

简介目录

Product Code: 69425

The lithium compounds market is expected to register a CAGR of over 8% during the forecast period.

Key Highlights

- The COVID-19 pandemic substantially impacted the lithium compounds market. Global constraints affected the automobile, building, and ceramic and glass industries. Despite this, the pharmaceutical business saw an increase in demand, keeping the market growing during the pandemic. However, the industries have increased production since 2021, and the market is expected to follow suit throughout the projection period.

- The increased use of batteries, particularly in electric cars, as well as rising demand from the ceramics and glass industries, are propelling the lithium compounds market forward. On the contrary, the high costs of compounds and their replacement by other substitutes are expected to hinder the market growth.

- Nonetheless, the increasing demand for electric vehicles in the market is likely to act as an opportunity for market study. Asia-Pacific represents the largest market for lithium compounds due to massive spending in the construction and automobile industry and will continue to dominate during the forecast period.

Lithium Compounds Market Trends

Growing Demand for Batteries

- Lithium compounds have been widely used in lithium-ion rechargeable battery technology to preserve and save energy. Lithium-ion batteries are used in devices such as mobile phones, cameras, laptop computers, power equipment, and vehicles.

- Lithium-ion batteries play an important part in vehicles, both combustion and electric. Because of their qualities like high energy density, low self-discharge rate, long life cycle, cheap maintenance, fast charging, and low weight, lithium-ion batteries are preferred in the automotive sector. The demand for Ni-Cd batteries is also high, as they are currently used in some hybrid electric vehicles. The sales of and demand for hybrid vehicles in India, Southeast Asia, and South Korea have witnessed decent growth compared to the previous years.

- According to the Bureau of Economic Analysis (BEA), the value added by manufacturing electrical appliances, equipment, and components in the United States in the third quarter of 2022 was around USD 73.8 billion, an increase of approximately 8% over the same time the previous year. The total value added in the first three quarters was close to USD 220 billion.

- Furthermore, the gross output of computer and electronic products manufacturing in the United States was approximately USD 1,300 billion in the first three quarters of 2022. 2022 saw a 7% gain when compared to the same period in 2021 (USD 1,200 billion).

- Meanwhile, the International Energy Agency (IEA) reported in its 'September 2022 Electric Vehicles Outlook' that despite supply chain constraints and the ongoing Covid-19 pandemic, electric car sales reached a record high in 2021. Sales nearly doubled to 6.6 million in comparison to 2020, bringing the total number of electric vehicles on the road to 16.5 million.

- The rising number of electric vehicles and the increasing usage of electronic equipment in developing countries is driving the demand for rechargeable batteries, which may drive the market for lithium batteries through the coming years.

Asia-Pacific to Dominate the Market

- Asia-Pacific is expected to dominate the overall lithium compounds market, owing to the highly developed electronics, automotive, ceramics, and glass sectors in China, India, Japan, and Korea, coupled with the continuous investments in the region to advance the battery technology sector through the years.

- Due to government prohibitions on internal combustion engines and hefty levies on internal combustion vehicles in China, the manufacture of electric and hybrid vehicles increased in China and India over the past several years.

- China has been the highest producer as well as consumer of electric vehicles, covering approximately half the market all around the globe. According to the China Association of Automobile Manufacturers (CAAM), the total production of new energy vehicles (NEVs) in China in 2022 was about 7 million units. This was a whooping increase of close to 97% when compared with the production of vehicles in the year 2021 (3.54 million units).

- India has also been focusing on the electric vehicles market for the country for the past few years. A study by CEEW Centre for Energy Finance recognized a USD 206 billion opportunity for electric vehicles in India by2030, which will necessitate a USD 180 billion investment in vehicle manufacturing and charging infrastructure in the country.

- According to IQVIA's projections, China, the second-largest pharmaceutical spending nation in the world, will increase segment volume by 8% over five years since 2021, while spending will rise by 19%, a slower rate than in prior years but still with an emphasis on extending access to cutting-edge medications.

- Indian pharmaceutical industry is also expected to reach USD 130 billion by 2030, as India Brand Equity Foundation (IBEF) suggested. The country is the largest producer of vaccines worldwide, accounting for ~60% of the total vaccines as of 2021, and ranks third globally for pharmaceutical production by volume.

- According to the statistics presented by the Ministry of Chemicals and Fertilizers, India, major chemicals production climbed by 5.73% to 43.51 lakh tons (4.351 million tons) in 2022-23 (up to July 2022) compared to 41.15 lakh tons (4.115 million tons) in the previous year's similar period.

- The growing need for high-efficiency batteries necessitates advanced technological improvements in lithium compounds. Continuous growth in energy-saving devices, along with the increasing pharmaceuticals and chemicals industry in the region is expected to drive the market for lithium compounds through the coming years.

Lithium Compounds Industry Overview

The lithium compounds market is partially consolidated in nature, with a few major players dominating a significant portion of the market. Some of the major companies are FMC Corporation, SQM SA, Lithium Americas Corp., Albemarle Corporation, and Neometals Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand for Ceramics and Glass Industry

- 4.1.2 Growing Applications for Batteries

- 4.2 Restraints

- 4.2.1 Entry of New Substitutes

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Compounds

- 5.1.1 Lithium Nitride

- 5.1.2 Lithium Metal

- 5.1.3 Lithium Carbonate

- 5.1.4 Lithium Hydroxide

- 5.1.5 Lithium Chloride

- 5.1.6 Butyllithium

- 5.1.7 Other Compounds

- 5.2 Application

- 5.2.1 Ceramics and Glass

- 5.2.2 Lubricants

- 5.2.3 Pharmaceuticals

- 5.2.4 Batteries

- 5.2.5 Chemicals

- 5.2.6 Metallurgy

- 5.2.7 Other Applications

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Albemarle Corporation

- 6.4.2 Allkem Limited

- 6.4.3 China Lithium Products Technology Co., Ltd.

- 6.4.4 FMC Corporation

- 6.4.5 Lithium Americas Corp.

- 6.4.6 Neometals Ltd

- 6.4.7 Shanghai China Lithium Industrial Co. Ltd

- 6.4.8 Sichuan Tianqi Lithium Chemicals Inc.

- 6.4.9 SQM SA

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Demand for Electric Vehicles

- 7.2 Other Opportunities

02-2729-4219

+886-2-2729-4219

硅酸锂市场:按类型、应用分类 - 2025-2030 年全球预测

硅酸锂市场:按类型、应用分类 - 2025-2030 年全球预测 锂化合物市场:按衍生物、最终用户划分 - 2025-2030 年全球预测

锂化合物市场:按衍生物、最终用户划分 - 2025-2030 年全球预测 锂化合物市场,按化合物、按应用、按最终用户、按国家和地区划分 - 2024-2032 年行业分析、市场规模、市场份额和预测

锂化合物市场,按化合物、按应用、按最终用户、按国家和地区划分 - 2024-2032 年行业分析、市场规模、市场份额和预测 锂化合物市场,按衍生物、按应用、按最终用途、按国家和地区划分 - 2024-2032 年行业分析、市场规模、市场份额和预测

锂化合物市场,按衍生物、按应用、按最终用途、按国家和地区划分 - 2024-2032 年行业分析、市场规模、市场份额和预测 2024-2032 年按类型、最终用途和地区分類的锂化合物市场报告

2024-2032 年按类型、最终用途和地区分類的锂化合物市场报告 全球电池级锂化合物市场 - 2024-2031

全球电池级锂化合物市场 - 2024-2031 锂化合物市场:按类型、按用途:2023-2032 年全球机会分析与产业预测

锂化合物市场:按类型、按用途:2023-2032 年全球机会分析与产业预测 全球硅酸锂市场研究报告-行业分析、规模、份额、增长、趋势及2023年至2030年预测

全球硅酸锂市场研究报告-行业分析、规模、份额、增长、趋势及2023年至2030年预测 全球硅酸锂市场——行业分析、规模、份额、增长、趋势和预测,2022-2031 年

全球硅酸锂市场——行业分析、规模、份额、增长、趋势和预测,2022-2031 年