|

市场调查报告书

商品编码

1273435

聚对苯二甲酸乙二醇酯 (PET) 收缩膜市场 - 增长、趋势、COVID-19 影响和预测 (2023-2028)Polyethylene Terephthalate (PET) Shrink Films Market - Growth, Trends, and Forecasts (2023 - 2028) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

在预测期内,聚对苯二甲酸乙二醇酯收缩膜市场预计将实现健康增长,预计复合年增长率超过 4%。

COVID-19 对 2020 年的市场产生了负面影响。 大流行情况已使世界上多个国家处于封锁状态,以遏制病毒的传播。 然而,这种情况将在 2021 年恢復,有利于预测期内研究的市场增长。

主要亮点

- 市场增长的主要驱动力是食品和饮料行业不断增长的需求。

- PET 收缩膜替代品的出现可能会阻碍市场增长。

- 对环保包装材料不断增长的需求预计将在未来几年带来市场机遇。

- 亚太地区主导市场,预计在预测期内将继续保持最高的复合年增长率。

聚对苯二甲酸乙二醇酯 (PET) 收缩膜市场趋势

食品和饮料行业的需求增加

- PET 是最常用的收缩包装材料之一,因为它可以製成各种密度,并且可以通过添加剂赋予各种功能。

- PET 收缩膜用于食品包装,例如鬆饼、饼干、糖果和其他糖果。 捆绑多个产品时,它用作直接与食品接触的初级包装。

- 它还用于捆绑小型设备和木材。 超市拖车包装也是用 PET 收缩膜製成的。

- 根据美国能源部国家可再生能源实验室的数据,全球每年生产超过 8200 万吨聚对苯二甲酸乙二醇酯 (PET),用于製造一次性饮料瓶、包装、服装和地毯。 到2050年,这一数量预计将达到6亿吨。

- PET 收缩膜在食品和饮料行业的产品周围形成气密密封。 它可以保护产品免受水分、灰尘和其他污染物的影响。 根据产品包装公司 Huhtamaki 2022 年的一份报告,美国包装和餐饮服务塑料的回收率约为 14%。 在欧洲,报告的塑料包装回收率为 40%。

- 根据包装与加工协会 (PMMI) 的数据,到 2028 年,北美饮料包装行业预计将增长 4.5%,其中美国在饮料包装行业处于领先地位。

- PET 塑料是一种可持续的包装选择,也是饮料瓶中使用的主要塑料类型。 这是由于其对有机物和水俱有出色的耐化学性以及高强度重量比。

- 根据关注人们习惯的组织 Habits of Waste 的数据,通过敦促每个人反思他们的浪费行为,全世界每年大约使用 4816.1 亿个塑料瓶。我在这里。 PET 树脂协会 (PETRA) 报告称,美国每年回收超过 15 亿磅的 PET 瓶和容器。

- 聚对苯二甲酸乙二醇酯是最常见的聚酯基热塑性塑料,主要用于包装行业。 许多食品和饮料必需品参与者都在其包装中加入 PET 材料以确保可持续性。 例如,2022 年 5 月,TekniPlex 推出了一系列由 100% 聚对苯二甲酸乙二醇酯 (PET) 材料製成的处理器托盘。 PET 包装提供了优质的产品展示,也解决了常见的包装挑战。

- 由于这些因素,聚对苯二甲酸乙二醇酯收缩膜市场预计在预测期内将在全球范围内增长。

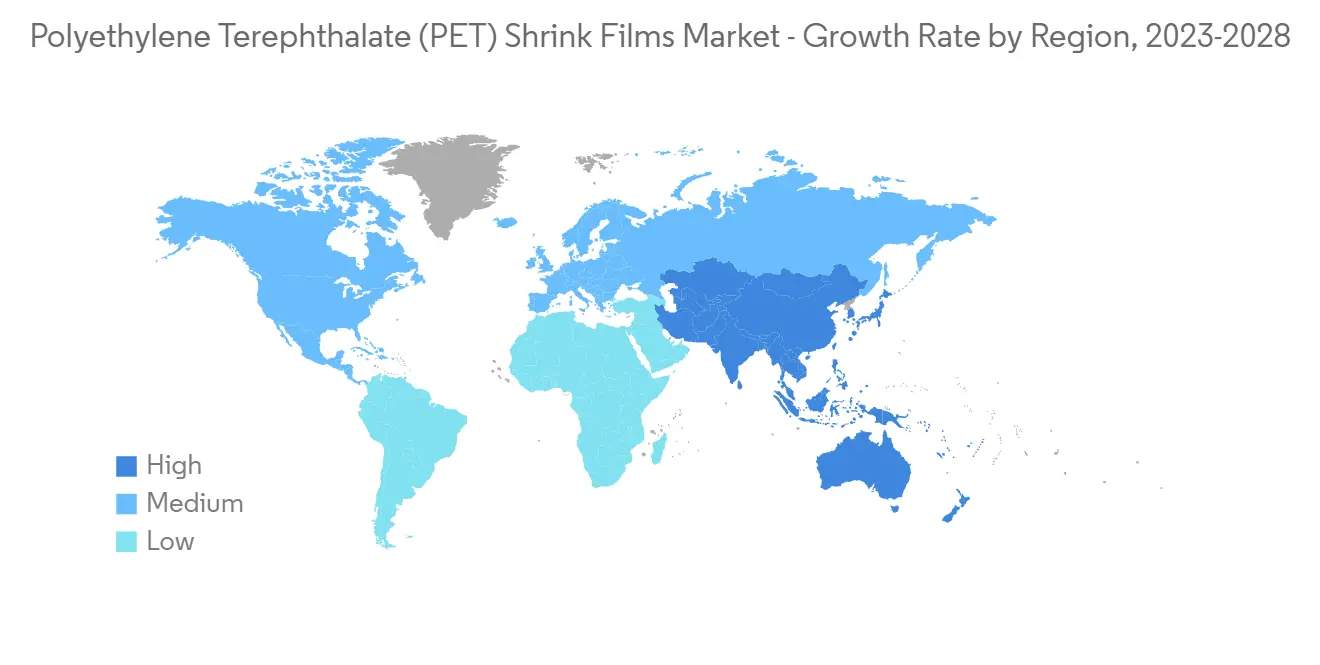

亚太地区主导市场

- 亚太地区以超过 40% 的份额主导着全球市场。 中国、印度、日本和韩国等国家不断发展的包装和医疗保健行业增加了该地区 PET 收缩膜的消费量。

- 中国拥有世界第二大包装产业。 由于定制包装的增加和对包装商品的需求增加,预计该国在预测期内将持续增长。

- 根据国家统计局的数据,2021 年中国将生产 8004 万吨塑料,占世界塑料材料产量的 32%。 这使中国成为仅次于北美的全球最大塑料生产国。

- 此外,中国最近见证了快速消费品 (FMCG) 行业的快速增长。 快速消费品市场的增长归因于该国的中产阶级消费者增加了对优质和注重健康的产品的支出。

- 此外,印度拥有世界第五大包装产业,而且发展势头强劲。 该国的包装行业受到行业创新的驱动,使产品更加小巧便携。

- PET 是世界上在包装、汽车和电子等各个行业中使用最多的聚合物。 据中国国家统计局预测,2021年中国塑料製品总产量将达到8004万吨。 2022年上半年,塑料製品总产量达到3821万吨。

- 收缩包装通常用于产品运输和存储。 船隻、汽车和直升机等交通工具通常使用收缩包装进行包裹,以保护它们在储存和运输过程中免受损□□坏。

- 根据 OICA 的数据,2021 年全球汽车产量将达到 8010 万辆,比上一年的 7760 万辆增长 4%。 根据印度品牌资产基金会的数据,到 2027 年,印度汽车市场预计将达到 548.4 亿美元,复合年增长率超过 9%。 印度的汽车工业製定了到 2026 年将汽车出口翻五倍的目标。 到 2022 年,印度的汽车出口总量将达到 5,617,246 辆。

- 考虑到所有这些因素,预计该地区的聚对苯二甲酸乙二醇酯收缩膜市场在预测期内将稳步增长。

聚对苯二甲酸乙二醇酯(PET)收缩膜行业概况

聚对苯二甲酸乙二醇酯收缩膜市场因其性质而部分整合。 市场上的主要参与者包括 Allen Plastic Industries、Bonset America Corporation、Polyplex、Flint Group、Klockner Pentaplast。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

内容

第一章介绍

- 调查先决条件

- 本次调查的范围

第二章研究方法论

第 3 章执行摘要

第四章市场动态

- 主持人

- 食品和饮料行业的需求增加

- 其他司机

- 约束因素

- PET 收缩膜替代品的可用性

- COVID-19 大流行的影响

- 行业价值链分析

- 波特的五力分析

- 供应商的议价能力

- 消费者的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第 5 章市场细分

- 类型

- 低收缩膜

- 中等收缩膜

- 高收缩膜

- 最终用户行业

- 食品和饮料行业

- 工业包装

- 个人护理和化妆品

- 印刷/文具

- 其他最终用户行业

- 地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 其他亚太地区

- 北美

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 意大利

- 法国

- 其他欧洲

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中东和非洲

- 沙特阿拉伯

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章竞争格局

- 併购、合资、合作、合同等。

- 市场份额 (%) 分析**/排名分析

- 主要公司采用的策略

- 公司简介

- Allen Plastic Industries Co., Ltd.

- Bonset America Corporation

- Flint Group

- Hubei HYF Packaging Co., Ltd.

- Klockner Pentaplast

- KWC Korea

- Plastic Suppliers, Inc.

- Polyplex

- Triton International Enterprises

- Vintech Polymers Pvt.

第7章市场机会与未来趋势

- 对环保包装材料的需求不断增长

During the forecast period, the polyethylene terephthalate shrink films market is estimated to register healthy growth at an estimated CAGR of over 4%.

COVID-19 negatively impacted the market in 2020. Several countries worldwide went into lockdown to curb the virus spreading due to the pandemic scenarios. However, the condition recovered in 2021, benefiting the market growth studied over the forecast period.

Key Highlights

- The primary factor driving the studied market's growth is increasing demand from the food & beverage industry.

- Substitutes' availability for PET shrink films will likely hinder the market's growth.

- Growing demand for eco-friendly packaging material will likely create opportunities for the market in the coming years.

- Asia-Pacific region is expected to dominate the market and is also likely to witness the highest CAGR during the forecast period.

Polyethylene Terephthalate (PET) Shrink Films Market Trends

Increasing Demand from the Food and Beverage Industry

- PET is one of the most commonly used materials for shrink wrapping because it can be produced in various densities and modified with additives to perform many functions.

- PET shrink films are used for packaging food products such as muffins, cookies, candies, and other confectionery products. For bundling multiple products, these films can be used as primary packaging coming into direct contact with the food product.

- Additionally, these films are also used to bundle smaller units and lumber. Supermarket tray wraps are also manufactured using PET shrink films.

- According to the National Renewable Energy Laboratory, US Department of Energy, more than 82 million metric tons of polyethylene terephthalate (PET) is produced each year globally to make single-use beverage bottles, packaging, clothing, and carpets. The volume is expected to reach 600 million tons by 2050.

- PET shrink films form a tight seal around the product in the food and beverage industry. It protects the product from moisture, dust, and other contaminants. According to a 2022 report by Huhtamaki, a product packaging company, the recovery rate for packaging and food service plastics in the United States was about 14%. In Europe, the plastic packaging recycling rate reported was 40%.

- According to the Association for Packaging and Processing, PMMI, the North American beverage packaging industry is expected to increase by 4.5% by 2028, with the United States leading the beverage packaging sector.

- PET plastic is a sustainable packaging option and the leading type of plastic used for beverage bottles. It is due to its excellent chemical resistance to organic materials and water and high strength-to-weight ratio.

- According to Habits of Waste, an organization focused on people's habits by encouraging everyone to rethink wasteful behavior, about 481.61 billion PET bottles are used every year around the world. PET Resin Association (PETRA) reports that more than 1.5 billion pounds of PET plastic bottles and containers are recycled annually in the United States.

- Polyethylene terephthalate is the most common thermoplastic resin of the polyester family and is used majorly in the packaging industry. Many essential food and beverage players are incorporating PET material in their packaging to ensure sustainability. For instance, in May 2022, TekniPlex launched a new line of processor trays made of 100% polyethylene terephthalate (PET) material. PET packaging offers premium product display and also addresses common packaging challenges.

- Owing to all these factors, the market for polyethylene terephthalate shrink films will likely grow worldwide during the forecast period.

Asia-Pacific Region to Dominate the Market

- Asia-Pacific dominated the global market with a share of more than 40%. With growing packaging and healthcare industries in countries like China, India, Japan, and South Korea, PET shrink film consumption is increasing in the region.

- China includes the second-largest packaging industry in the world. The country is expected to witness consistent growth during the forecast period, owing to the rise of customized packaging and increased demand for packaged goods.

- According to the National Bureau of Statistics, China produced 80.04 million metric tons of plastics, accounting for 32% of global plastic materials production in 2021. It makes China the world's largest plastic producer, followed by North America.

- Moreover, China recently witnessed rapid growth in the fast-moving consumer goods (FMCG) sector. The FMCG market growth was driven by the country's increased spending on premium and healthier products by middle-class consumers.

- Additionally, India includes the fifth-largest packaging industry worldwide, which is growing significantly. The country's packaging industry is driven by growing innovation in industries to make their products compact and portable.

- PET is the most used polymer worldwide in various industries, including packaging, automotive, electronics, and others. According to the National Bureau of Statistics of China, the total production volume of plastic products in China amounted to 80.04 million metric tons in 2021. In the first half of 2022, the total plastic products manufactured reached 38.21 million metric tons.

- Shrink wrap is often used to ship and store products. Vehicles such as boats, cars, and helicopters are often wrapped using shrink wrap to protect them from storage and shipping damages.

- According to OICA, in 2021, global vehicle production reached 80.1 million units, an increase of 4% from the previous year's 77.6 million units. According to India Brand Equity Foundation, the Indian car market is expected to reach USD 54.84 billion by 2027, registering a CAGR of over 9%. Indian automotive industry is targeting to increase the export of vehicles by five times by the year 2026. In 2022, total automobile exports from India stood at 5,617,246.

- Due to all such factors, the region's market for polyethylene terephthalate shrink films is expected to grow steadily during the forecast period.

Polyethylene Terephthalate (PET) Shrink Films Industry Overview

The polyethylene terephthalate shrink films market is partially consolidated in nature. Some of the major players in the market include Allen Plastic Industries Co., Ltd., Bonset America Corporation, Polyplex, Flint Group, and Klockner Pentaplast, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand from the Food & Beverage Industry

- 4.1.2 Other Drivers

- 4.2 Restraints

- 4.2.1 Availability of Substitutes for PET Shrink Films

- 4.2.2 Impact of COVID-19 Pandemic

- 4.3 Industry Value-Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Type

- 5.1.1 Low Shrink Film

- 5.1.2 Medium Shrink Film

- 5.1.3 High Shrink Film

- 5.2 End-user Industry

- 5.2.1 Food and Beverage

- 5.2.2 Industrial Packaging

- 5.2.3 Personal Care and Cosmetics

- 5.2.4 Printing and Stationery

- 5.2.5 Other End-user Industries

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%) Analysis**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Allen Plastic Industries Co., Ltd.

- 6.4.2 Bonset America Corporation

- 6.4.3 Flint Group

- 6.4.4 Hubei HYF Packaging Co., Ltd.

- 6.4.5 Klockner Pentaplast

- 6.4.6 KWC Korea

- 6.4.7 Plastic Suppliers, Inc.

- 6.4.8 Polyplex

- 6.4.9 Triton International Enterprises

- 6.4.10 Vintech Polymers Pvt.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing Demand for Eco-Friendly Material for Packaging

全球阻隔收缩薄膜市场规模、份额、成长分析、按产品、按材料、按最终用途 - 产业预测 2024-2031

全球阻隔收缩薄膜市场规模、份额、成长分析、按产品、按材料、按最终用途 - 产业预测 2024-2031 2024 年饮料用合装收缩膜全球市场报告

2024 年饮料用合装收缩膜全球市场报告 收缩塑胶薄膜市场:按类型、薄膜形状、应用分类 - 2024-2030 年全球预测

收缩塑胶薄膜市场:按类型、薄膜形状、应用分类 - 2024-2030 年全球预测 全球聚烯烃收缩薄膜市场评估:依原料、类型、最终用途产业、地区、机会、预测(2016-2030)

全球聚烯烃收缩薄膜市场评估:依原料、类型、最终用途产业、地区、机会、预测(2016-2030) 聚烯烃收缩膜市场:2023-2028 年全球产业趋势、份额、规模、成长、机会与预测

聚烯烃收缩膜市场:2023-2028 年全球产业趋势、份额、规模、成长、机会与预测 全球聚烯烃收缩薄膜市场研究报告 - 2023 年至 2030 年产业分析、规模、份额、成长、趋势与预测

全球聚烯烃收缩薄膜市场研究报告 - 2023 年至 2030 年产业分析、规模、份额、成长、趋势与预测 聚烯烃收缩膜市场 - 按材料类型(聚乙烯 (PE) 收缩膜、聚丙烯 (PP) 收缩膜)、按类型(通用收缩膜、交联收缩膜)、按最终用途和预测,2023 - 2032 年

聚烯烃收缩膜市场 - 按材料类型(聚乙烯 (PE) 收缩膜、聚丙烯 (PP) 收缩膜)、按类型(通用收缩膜、交联收缩膜)、按最终用途和预测,2023 - 2032 年 全球饮料多包装收缩膜市场

全球饮料多包装收缩膜市场 饮料多件装市场(包装类型:标准、多种包装和季节性/促销;饮料类型:酒精和非酒精)- 2023-2031 年全球行业分析、规模、份额、成长、趋势和预测

饮料多件装市场(包装类型:标准、多种包装和季节性/促销;饮料类型:酒精和非酒精)- 2023-2031 年全球行业分析、规模、份额、成长、趋势和预测 阻隔收缩膜市场:依产品(Chub、流动包装、收缩泡棉)、依材料(乙基乙烯醇、聚酰胺、聚乙烯)、最终用户 - 2023-2030 年全球预测

阻隔收缩膜市场:依产品(Chub、流动包装、收缩泡棉)、依材料(乙基乙烯醇、聚酰胺、聚乙烯)、最终用户 - 2023-2030 年全球预测