|

市场调查报告书

商品编码

1273524

失禁设备和造口术市场 - 增长、趋势、COVID-19 影响和预测 (2023-2028)Incontinence Devices and Ostomy Market - Growth, Trends, and Forecasts (2023 - 2028) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

在预测期内,失禁和造口护理产品市场预计将以近 10.1% 的复合年增长率增长。

COVID-19 大流行的爆发对失禁设备和造口术业务产生了重大影响,仅进行了自爆发以来最严重的造口手术。 造口护理是一个经常被忽视的方面,在大流行期间没有发布具体的造口护理建议。 根据国家医学图书馆 2022 年 3 月发表的一项研究,造口数量在 2020 年 3 月至 2021 年 2 月期间减少了 19.5%。 因此,造口相关手术的减少阻碍了大流行期间的市场增长。 然而,由于大多数患者选择了家庭护理,同期家庭护理对造口护理产品的需求显着增加。 因此,COVID-19 对市场增长产生了重大影响。 然而,随着 COVID-19 病例的消退,市场已经恢復得很好,预计在预测期内将保持同样的趋势。

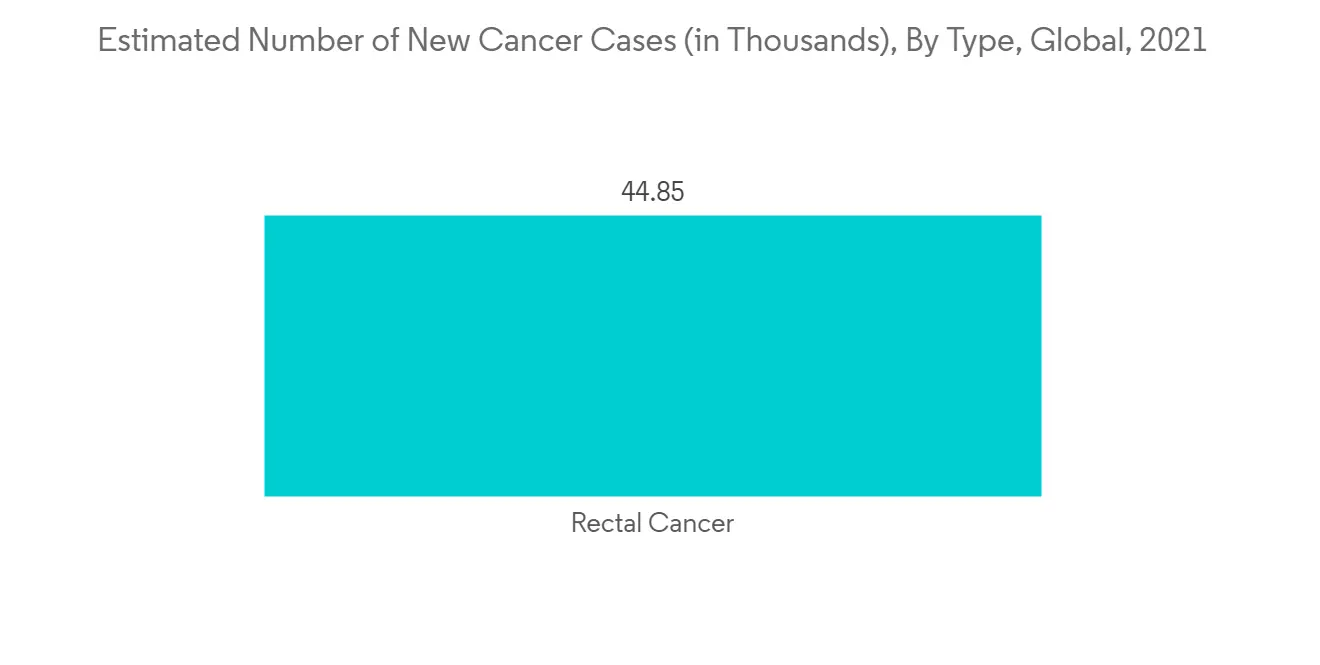

促成研究市场增长的主要因素是炎症性肠病 (IBD) 的高患病率、溃疡性结肠炎和克罗恩病等尿失禁 (UI) 患病率的上升,以及造口手术病例的增加由于结直肠癌。 根据世界卫生组织 2021 年 7 月的更新,到 2030 年,全球结直肠癌病例预计将增加约 70%。 此外,根据 GLOBOCAN 公布的统计数据,结直肠癌 (CRC) 是德国人口中第四大最常见的癌症,2021 年德国报告了大约 57,528 例新的 CRC 病例。我是。 此外,根据 GLOBOCAN 提供的统计数据,2020 年英国报告了约 33,815 例结肠癌新病例和 11,951 例新死亡病例,增加了对造口手术和设备的需求,推动了预测期内的市场增长。我们支持增长。 此外,根据 Female Pelvic Medicine & Reconstructive Surgery 于 2022 年 4 月发表的一项研究,61.8% 的女性患有尿失禁 (UI),相当于美国有 78,297,094 名成年女性,到 2021 年,至少有 32.4% 的所有报告症状每月。 在 UI 患者中,37.5% 被发现有压力性尿失禁,22.0% 有急迫性尿失禁,31.3% 有混合症状,9.2% 有不明原因尿失禁。 因此,预计女性 UI 的高负担将增加对失禁产品的需求,这有望在预测期内推动市场增长。

有助于改善造口术患者生活质量的高效、合适的造口袋系统及相关配件的开发有望在预测期内为所研究的市场开闢增长前景。 例如,Trio Healthcare 推出了一种硅基造口术密封件 Triosiltac。 该产品有助于防止渗漏并保护造口周围的皮肤。 预计此类技术进步将在预测期内推动市场增长。

此外,越来越多的努力提高个人对造口术的认识,进一步推动了市场的增长。 例如,美国联合造口术协会 (UOAA) 致力于提高造口术医疗保健的质量,并在所有医疗保健机构中提高护理标准。 该组织在每年 10 月的第一个星期六举办“世界造口日”,以提高人们对造口护理的认识。 这些努力有望提高公众对造口护理的认识并促进市场增长。

但是,缺乏足够的报销以及与使用造口术和失禁产品相关的并发症可能会限制市场增长。

失禁器械和造口术市场趋势

结肠造口袋有望在应用领域增长良好

结肠造口袋,也称为造口袋或造口袋,是一种用于收集身体排洩物的小型防水袋。 一种称为结肠造口术的外科手术会在大肠和腹壁之间创建一个称为造口或造口术的开口。 这使得废物可以通过腹壁的开口而不是通过大肠、直肠和肛门排出体外。 粪便和其他废物被排入一个囊状的结肠造口袋中,可以定期清空。

由于炎症性肠病 (IBD) 的兴起,对这种袋子的需求逐年增加。 例如,根据 2021 年 8 月发表在 BMC Journal 上的一项研究,在英国,2021 年炎症性肠病(IBD)、克罗恩病(CD)和溃疡性结肠炎(UC)的发病率将是每 100,000 人分别有 28.6、10.2 和 15.7 人。 这些疾病的高发病率预计将推动市场增长。

此外,越来越多的产品发布预计也将在未来几年进一步推动该细分市场的增长。 引入高效和合适的造口袋有助于改善造口术患者的生活质量,预计将为该细分市场的增长提供充足的增长机会。 例如,2021 年 6 月,卡迪夫的 Pelican Healthcare Ltd 推出了 ModaViostomy 袋系列,巩固了其作为英国和爱尔兰医疗保健领域一次性造口设备领先製造商之一的地位。

北美主导市场,预计在预测期内也会如此

北美在失禁和造口护理产品市场占据主导地位,收入份额最大,原因是克罗恩病和溃疡性结肠炎患者数量不断增加,造口护理和造口手术意识不断增强等因素。 .

根据 2023 年约翰霍普金斯大学的一篇论文,超过 2500 万成年美国人患有暂时性或慢性尿失禁。 此外,仅在美国,治疗 UI 的费用就达 163 亿美元,其中 75% 用于治疗女性。 因此,美国尿失禁的患病率正在增加,预计这将推动市场增长。

此外,一些市场参与者正在实施各种战略举措来支持市场的增长。 例如,2021 年 4 月,Welland Medical 通过其经销商 Premier Ostomy Center 扩大了在加拿大的业务。 居住在加拿大的人可以直接使用。 预计此类新兴市场的发展将在预测期内推动该国的市场增长。 此外,2022 年 1 月,Owens & Minor Inc .和 Apria Inc .签订了 Owens & Minor 收购 Apria 的最终协议。 此次收购预计将扩大公司的造口术产品组合。

失禁器械和造口术行业概览

失禁和造口护理市场竞争激烈,由许多主要参与者组成。 Abena AS、B. Braun Melsungen AG、Coloplast Corporation、ConvaTec、Hollister Inc. 和 Kimberly-Clark Corporation 等公司占据了相当大的市场份额。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

内容

第一章介绍

- 调查假设和市场定义

- 本次调查的范围

第二章研究方法论

第 3 章执行摘要

第四章市场动态

- 市场概览

- 市场驱动因素

- 世界失禁人数增加

- 肾臟疾病和肾臟损伤的患病率增加

- 对造口护理产品的认识和接受度不断提高

- 市场製约因素

- 缺乏足够的保险报销

- 与使用造口术和失禁产品相关的并发症

- 波特的五力分析

- 新进入者的威胁

- 买方/消费者议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争公司之间的敌对关係

第 5 章市场细分

- 按产品类型

- 失禁护理产品

- 吸收器

- 失禁包

- 其他产品类型(夹具、除臭剂、清洁剂、小便池等)

- 造口护理产品

- 造口袋

- 结肠造口袋

- 迴肠造口袋

- 泌尿造口袋

- 皮肤屏障

- 灌溉产品

- 其他结肠造口产品

- 失禁护理产品

- 通过使用

- 膀胱癌

- 结肠癌

- 克罗恩病

- 肾结石

- 慢性肾功能衰竭

- 其他用途

- 地区

- 北美

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 意大利

- 西班牙

- 其他欧洲

- 亚太地区

- 中国

- 日本

- 印度

- 澳大利亚

- 韩国

- 其他亚太地区

- 中东和非洲

- 海湾合作委员会

- 南非

- 其他中东和非洲地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 北美

第六章竞争格局

- 公司简介

- Abena AS

- B. Braun Melsungen AG

- Coloplast Corporation

- ConvaTec

- Hollister Inc.

- Kimberly-Clark Corporation

- Salts Healthcare

- Unicharm Corporation

- Welland Medical

- Pelican Healthcare Ltd.

- Flexicare(Group)Limited

- Torbot Group, Inc.

第七章市场机会与未来趋势

The incontinence and ostomy care product market is expected to register a CAGR of nearly 10.1% during the forecast period.

The outbreak of the COVID-19 pandemic significantly impacted the incontinence devices and ostomy business, as only the most acute ostomy surgeries were performed following the outbreak. Stoma care is a potentially overlooked aspect of the outbreak, and no specific stoma care recommendations were published during the pandemic. According to the study published by the National Library of Medicine in March 2022, ostomies decreased by 19.5% during the time between March 2020 and February 2021. Thus, the decline in surgeries related to ostomies hampered the growth of the market during the pandemic. However, the demand for ostomy care products for home care considerably increased during the same period as most patients opted for home treatments. Hence, COVID-19 had a significant impact on market growth. However, as COVID-19 cases have subsided, the market has been recovering very well and is likely to maintain the same trend over the forecast period.

The major factor contributing to the growth of the market studied is the high prevalence of inflammatory bowel diseases (IBD), rising prevalence of urinary incontinence (UI), including ulcerative colitis or Crohn's disease, and colorectal cancer, resulting in increased ostomy surgery cases. According to the WHO updates from July 2021, an increase of around 70% is expected in colorectal cancer cases across the world by 2030. Furthermore, according to statistics published by GLOBOCAN, colorectal cancer (CRC) is the fourth most common type of cancer among the German population, and approximately 57,528 new cases of CRC were reported in Germany in 2021. Additionally, according to statistics provided by GLOBOCAN in 2020, approximately 33,815 new cases of colon cancer and 11,951 new deaths were reported in the United Kingdom in 2020 increasing the demand for ostomy surgeries and devices, thereby boosting the market growth over the forecast period. Moreover, as per a study published in April 2022 by Female Pelvic Medicine & Reconstructive Surgery, 61.8% of women had urinary incontinence (UI), corresponding to 78,297,094 adult United States women, with 32.4% of all women reporting symptoms at least monthly in 2021. Of those with UI, 37.5% had stress urinary incontinence, 22.0% had urgency urinary incontinence, 31.3% had mixed symptoms, and 9.2% had unspecified incontinence. Thus, a high burden of UI in women is expected to increase the demand for incontinence products which is expected to boost the growth of the market over the forecast period.

The development of efficient and suitable pouching systems and associated accessories which help to improve the quality of life of ostomy patients, is expected to open up the growth horizons for the studied market over the forecast period. For instance, the company Trio Healthcare launched a silicone-based ostomy seal, Trio Siltac. This product aids in preventing leakage and protecting the skin around the stoma. Such technological advancements are anticipated to propel the market growth over the forecast period.

Furthermore, an increase in initiatives to raise awareness about ostomy in individuals further propels the growth of the market. For instance, the United Ostomy Association of America Inc. (UOAA) works to improve the quality of ostomy healthcare and promote higher standards of care in all healthcare settings. The organization commemorates World Ostomy Day on the first Saturday of October every year to raise awareness about ostomy care. Such initiatives is likely to create awareness among the general population about stoma care, thereby aiding market growth.

However, lack of proper reimbursement and complications associated with ostomy and usage of incontinence products are likely to restrain the market growth.

Incontinence Devices and Ostomy Market Trends

Colostomy Bags are Expected to Observe Lucrative Growth in the Application Segment

A colostomy bag also called a stoma bag, or ostomy bag, is a small, waterproof pouch used to collect waste from the body. During a surgical procedure known as a colostomy, an opening, called a stoma or ostomy, is formed between the large intestine (colon) and the abdominal wall. This allows waste products to be excreted through the opening in the abdominal wall rather than via the colon through the rectum and anus. Stools and other waste products are drainable into the pouch-like colostomy bag, which can then be emptied at regular intervals.

The demand for these bags has increased over the years due to the increasing incidence of inflammatory bowel diseases (IBD). For instance, according to the research study published in BMC Journal in August 2021, in the United Kingdom, the incidence of inflammatory bowel disease (IBD), Crohn's disease (CD), and ulcerative colitis (UC) were found to be 28.6, 10.2, and 15.7 per 100,000 population, respectively in 2021. Such a high incidence of these diseases is expected to drive market growth.

Furthermore, the rising number of product launches is also expected to further drive segmental growth in the coming years. The introduction of efficient and suitable ostomy bags which help to improve the quality of life of ostomy patients is expected to provide ample growth opportunities for the segment's growth. For instance, in June 2021, Pelican Healthcare Ltd., located in Cardiff, strengthened its position as one of the leading manufacturers of disposable stoma devices in the United Kingdom and Ireland healthcare sectors with the introduction of the ModaViostomy bag range.

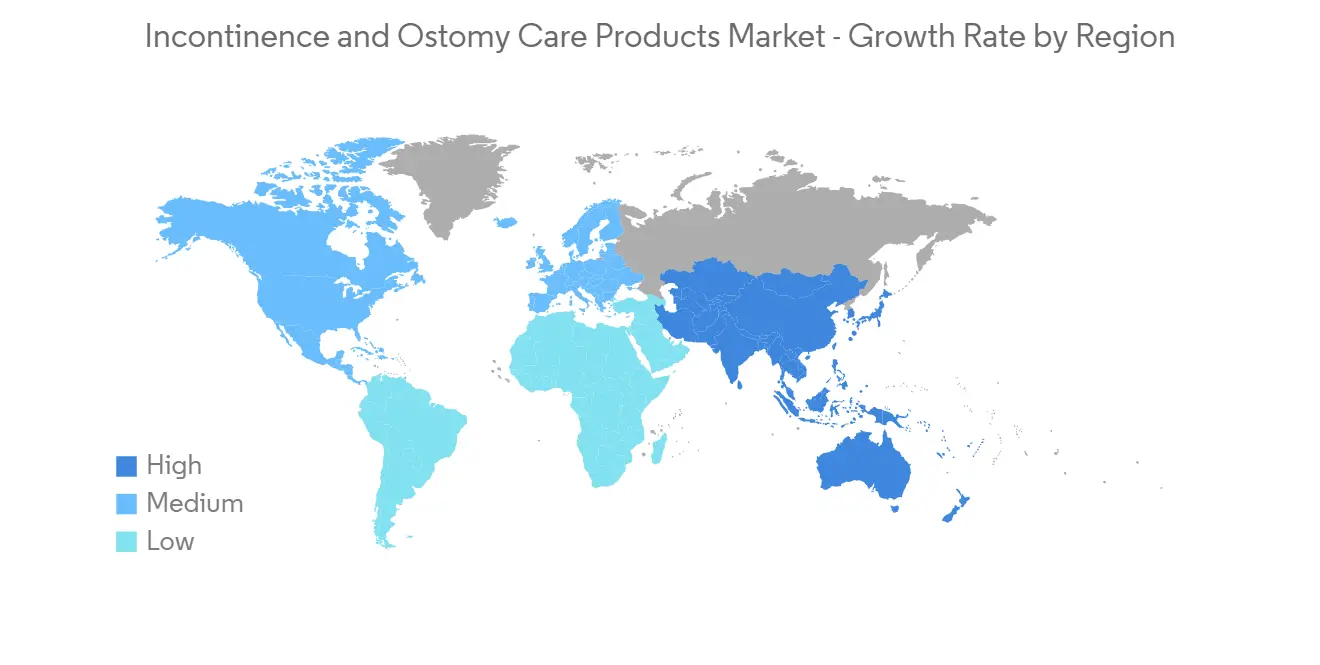

North America Dominates the Market and is Expected to do the Same in the Forecast Period

North America dominated the incontinence and ostomy care products market and accounted for the largest revenue share owing to factors such as an increase in the number of patients due to Crohn's disease, ulcerative colitis, and rising awareness initiatives related to ostomy care or stoma surgical procedures.

As per a Johns Hopkins University article of 2023, more than 25 million adult Americans experience temporary or chronic urinary incontinence. Additionally, the cost of treatment of UI in the United States alone is USD 16.3 billion, 75% of which is spent on the treatment of women. This increasing prevalence of UI in the United States is expected to propel the market's growth.

Moreover, several market players are implementing various strategic initiatives that support the market's growth. For instance, in April 2021, Welland Medical expanded its business in Canada through its distributor, Premier Ostomy Centre. It is directly available to people living in Canada. Such developments are likely to boost the market growth in the nation over the forecast period. Additionally, in January 2022, Owens & Minor Inc. and Apria Inc. entered into a definitive agreement under which Owens & Minor will acquire Apria. The acquisition is anticipated to broaden the company's ostomy portfolio.

Incontinence Devices and Ostomy Industry Overview

The incontinence devices and ostomy care products market is highly competitive and consists of a number of major players. Companies like Abena AS, B. Braun Melsungen AG, Coloplast Corporation, ConvaTec, Hollister Inc., and Kimberly-Clark Corporation, among others, hold substantial shares in the market.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Incontinence Around the World

- 4.2.2 Increasing Prevalence of Renal Diseases and Nephrological Injuries

- 4.2.3 Growing Awareness and Acceptance regarding Ostomy Care Products

- 4.3 Market Restraints

- 4.3.1 Lack of Proper Reimbursement

- 4.3.2 Complications Associated with Ostomy and Usage of Incontinence Products

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD million)

- 5.1 By Product Type

- 5.1.1 Incontinence Care Products

- 5.1.1.1 Absorbents

- 5.1.1.2 Incontinence Bags

- 5.1.1.3 Other Product Types (Clamps, Deodorizers, Cleaners, Urinals, etc.)

- 5.1.2 Ostomy Care Products

- 5.1.2.1 Ostomy Bags

- 5.1.2.1.1 Colostomy Bags

- 5.1.2.1.2 Ileostomy Bags

- 5.1.2.1.3 Urostomy Bags

- 5.1.2.2 Skin Barriers

- 5.1.2.3 Irrigation Products

- 5.1.2.4 Other Ostomy Products

- 5.1.1 Incontinence Care Products

- 5.2 By Application

- 5.2.1 Bladder Cancer

- 5.2.2 Colorectal Cancer

- 5.2.3 Crohn's Disease

- 5.2.4 Kidney Stone

- 5.2.5 Chronic Kidney Failure

- 5.2.6 Other Applications

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Abena AS

- 6.1.2 B. Braun Melsungen AG

- 6.1.3 Coloplast Corporation

- 6.1.4 ConvaTec

- 6.1.5 Hollister Inc.

- 6.1.6 Kimberly-Clark Corporation

- 6.1.7 Salts Healthcare

- 6.1.8 Unicharm Corporation

- 6.1.9 Welland Medical

- 6.1.10 Pelican Healthcare Ltd.

- 6.1.11 Flexicare (Group) Limited

- 6.1.12 Torbot Group, Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

失禁护理市场规模和预测、全球和地区份额、趋势和成长机会分析报告范围:按产品、类型、最终用户和地理位置

失禁护理市场规模和预测、全球和地区份额、趋势和成长机会分析报告范围:按产品、类型、最终用户和地理位置 一次性失禁产品的全球市场规模、份额和趋势分析报告:2023-2030 年失禁类型、产品和地区的展望和预测

一次性失禁产品的全球市场规模、份额和趋势分析报告:2023-2030 年失禁类型、产品和地区的展望和预测 2024 年一次性失禁产品全球市场报告

2024 年一次性失禁产品全球市场报告 失禁产品市场报告:2030 年趋势、预测与竞争分析

失禁产品市场报告:2030 年趋势、预测与竞争分析 一次性失禁产品市场 - 2018-2028 年全球产业规模、份额、趋势、机会和预测,按产品类型、地区按应用和竞争细分

一次性失禁产品市场 - 2018-2028 年全球产业规模、份额、趋势、机会和预测,按产品类型、地区按应用和竞争细分 失禁垫市场 - 2018-2028 年全球产业规模、份额、趋势、机会与预测,按产品类型、病患、最终用途产业、配销通路、地区、竞争细分

失禁垫市场 - 2018-2028 年全球产业规模、份额、趋势、机会与预测,按产品类型、病患、最终用途产业、配销通路、地区、竞争细分 失禁护理产品的全球市场 (ICP) (~2028):产品(吸收性(床保护器、护垫和防护装置)、非吸收性(导管、引流袋))、用途(可重复使用/一次性) 、配销通路(电子-商业)和最终用户(医院)

失禁护理产品的全球市场 (ICP) (~2028):产品(吸收性(床保护器、护垫和防护装置)、非吸收性(导管、引流袋))、用途(可重复使用/一次性) 、配销通路(电子-商业)和最终用户(医院) 失禁护理市场规模、份额和趋势分析报告:按产品、袋子使用、最终用途、地区和细分市场进行预测,2023-2030 年

失禁护理市场规模、份额和趋势分析报告:按产品、袋子使用、最终用途、地区和细分市场进行预测,2023-2030 年 失禁产品的全球市场

失禁产品的全球市场 失禁垫市场规模、份额和趋势分析报告:按产品类型、患者、最终用途、分销管道、地区和细分市场预测,2023-2030 年

失禁垫市场规模、份额和趋势分析报告:按产品类型、患者、最终用途、分销管道、地区和细分市场预测,2023-2030 年