|

市场调查报告书

商品编码

1326430

液晶聚合物 (LCP) 市场规模和份额分析 - 增长趋势和预测 (2023-2029)Liquid Crystal Polymers (LCP) Market Size & Share Analysis - Growth Trends & Forecasts (2023 - 2029) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

全球液晶聚合物(LCP)市场规模预计将从2023年的65.52千吨扩大到2028年的83.74千吨,预测期内復合年增长率为5.03%。

主要亮点

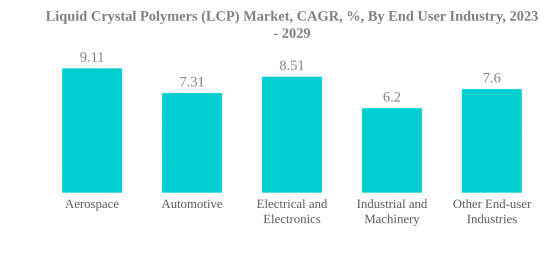

- 电气/电子是最大的终端用户行业,LCP 复合材料因其快速的技术创新、介电性能和耐化学性而主要用于电子行业。 因此,该行业的市场占有率最高。

- 航空航天是一个快速发展的最终用户行业。 LCP用于航空航天工业的微电子领域。 因此,该细分市场预计将成为市场上增长最快的细分市场。

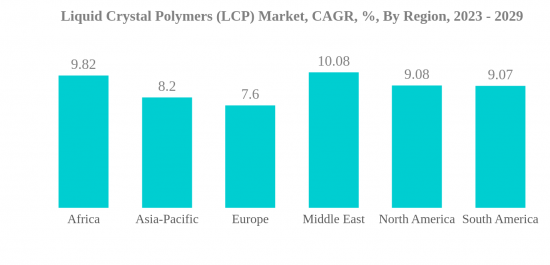

- 亚太地区是最大的地区。 亚太地区主要由中国、印度、日本和韩国等新兴经济体推动。 亚太地区电子行业的复合年增长率预计为6.63%,使亚太地区成为市场上最大的地区。

- 中东是一个快速发展的地区。 预测期内,电子产品产量预计将保持约8.7%的复合年增长率,其中中东预计将成为增长最快的地区。

液晶聚合物(LCP)市场趋势

电子行业技术创新步伐加快,市场需求拉动

- 液晶聚合物 (LCP) 具有多种特性,包括抗蠕变性、耐化学性、抗衝击性和耐磨性。 LCP还具有高介电性能和机械强度,这就是它广泛应用于电子、航空航天和工业机械行业的原因。 2022年LCP市场占全球工程塑料收入的0.65%。

- 2022 年 LCP 树脂的最大消费者是电气和电子行业。 消费电子产品中使用高强度、轻质材料的趋势不断增加,预计将推动对 LCP 树脂的需求。 预计到2023年底,全球消费电子行业收入将达到1.1万亿美元,到2027年每年增长2.17%。

- 到 2022 年,工业机械行业将成为全球第二大 LCP 树脂消费国。 疫情后快速城市化趋势的增强以及机床和结构设备的海外出口復苏推动了2022年工业机械产量的增长,导致LCP树脂消费量大幅增加。 2022年全球LCP市场工业机械领域价值同比增长19.20%。

- 就收入而言,航空航天业是增长最快的最终用户行业。 按价值计算,预测期内的复合年增长率预计为 9.11%,这是由于飞机零部件产量增加,以满足对轻量化和省油飞机不断增长的需求,导致未来 LCP 的消耗增加。被认为是为了 航空航天业生产收入预计到 2029 年将达到 7230 亿美元,而 2022 年将达到 4660 亿美元。

亚太地区将在未来几年主导全球 LCP 市场

- 液晶聚合物 (LCP) 在亚太地区、北美和南美等地区广泛用于各种应用,包括暴露在高温下的薄壁精密零件。 LCP 的一些主要应用是最终用户行业,例如汽车、电气/电子和工业机械。 2022年液晶聚合物(LCP)占全球工程塑料市场销售份额的0.65%。

- 2022 年亚太地区的价值同比增长 3.70%。 这是由电气/电子行业和汽车行业推动的,这两个行业分别占这些最终用户行业对 LCP 的全球需求的 75.96% 和 69.59%。 由于采用在家工作模式的公司和设立家庭办公室的人们对技术、游戏机和电子设备的需求增加,LCP 的全球市场可能会扩大。

- 2022 年,北美是 LCP 消费者的第二大地区,销售份额为 14.27%。 该地区在汽车和电子等工业领域的最终用户应用数量最多,因此占据了全球LCP消费量的压倒性份额。 例如,到2022年,该地区占全球汽车产量的份额将为10.09%,电子元件产量的份额将为9.92%。

- 在电气和电子行业的推动下,非洲是增长第二快的地区,预计 2023 年的价值将比 2022 年增长 9.82%。 韩国领先的电气和电子品牌在非洲站稳了脚跟,其中三星占据了智能手机市场35%的份额。 三星是埃塞俄比亚和苏丹机电产品製造和组装的主要投资者。

液晶聚合物 (LCP) 行业概览

液晶聚合物(LCP)市场高度整合,前五名企业占比80.34%。 该市场的主要参与者包括(按字母顺序排列)塞拉尼斯公司、大赛璐公司、深圳沃特高新材料、索尔维和住友化学。

其他好处:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章执行摘要和主要发现

第 2 章报告要约

第 3 章简介

- 研究假设和市场定义

- 调查范围

- 调查方法

第 4 章主要行业趋势

- 最终用户趋势

- 监管框架

- 价值炼和分销渠道分析

第 5 章市场细分

- 最终用户行业

- 航空航天

- 汽车

- 电气/电子

- 工业/机械

- 其他最终用户行业

- 地区

- 非洲

- 按国家/地区

- 尼日利亚

- 南非

- 其他非洲

- 亚太地区

- 按国家/地区

- 澳大利亚

- 中国

- 印度

- 日本

- 马来西亚

- 韩国

- 其他亚太地区

- 欧洲

- 按国家/地区

- 法国

- 德国

- 意大利

- 俄罗斯

- 英国

- 欧洲其他地区

- 中东

- 按国家/地区

- 沙特阿拉伯

- 阿拉伯联合酋长国

- 其他中东地区

- 北美

- 按国家/地区

- 加拿大

- 墨西哥

- 美国

- 南美洲

- 按国家/地区

- 阿根廷

- 巴西

- 南美洲其他地区

- 非洲

第 6 章竞争态势

- 主要战略趋势

- 市场份额分析

- 公司情况

- 公司简介

- Celanese Corporation

- Daicel Corporation

- Kingfa SCI. & TECH. CO., LTD.

- Ningbo Jujia New Material Technology Co., Ltd

- Shanghai PRET Composite Material Co., Ltd.

- Shenzhen WOTE Advanced Materials Co.,Ltd.

- Solvay

- Sumitomo Chemical Co., Ltd.

- TORAY INDUSTRIES, INC.

- UENO FINE CHEMICALS INDUSTRY, LTD.

第 7 章首席执行官面临的关键战略问题

第 8 章附录

简介目录

Product Code: 47397

The Global Liquid Crystal Polymer (Lcp) Market size is expected to grow from 65.52 kilo metric tons in 2023 to 83.74 kilo metric tons by 2028, at a CAGR of 5.03% during the forecast period.

Key Highlights

- Electrical and Electronics is the Largest End User Industry. Composites of LCP are majorly used in the electronics industry due to rapid innovation, their dielectric properties, and their chemical resistance. Thus, the industry occupied the highest share.

- Aerospace is the Fastest-growing End User Industry. LCP is adopted in microelectronics in the aerospace industry. Thus, the segment is anticipated to witness the fastest growth in the market.

- Asia-Pacific is the Largest Region. Asia-Pacific is majorly driven by emerging economies such as China, India, Japan, and South Korea. Its electronics industry is expected to witness a CAGR of 6.63%, making Asia-Pacific the largest region in the market.

- Middle East is the Fastest-growing Region. With electronics production expected to register a faster CAGR of around 8.7% during the forecast period, the Middle East is projected to be the fastest-growing region.

Liquid Crystal Polymers (LCP) Market Trends

RAPID PACE OF TECHNOLOGICAL INNOVATIONS IN THE ELECTRONICS INDUSTRY TO BOOST MARKET DEMAND

- Liquid crystal polymers (LCP) exhibit versatile properties like resistance to creep, chemicals, impact, and abrasion. LCPs also have high dielectric and mechanical strength, due to which they are used widely in the electronics, aerospace, and industrial machinery industries. The LCP market accounted for 0.65% of the revenue of global engineering plastics in 2022.

- The electrical and electronics industry was the largest consumer of LCP resins in 2022. The rising trend of using high-strength and lightweight materials in consumer electronics is expected to drive the demand for LCP resin. Revenue of the global consumer electronics industry is projected to reach USD 1.10 trillion by the end of 2023 and grow annually by 2.17% till 2027.

- The industrial machinery industry was the second-largest consumer of LCP resin globally in 2022. The growing trends of rapid urbanization and restoration of offshore exports for machine tools and structural equipment post-pandemic boosted the production of industrial machinery in 2022, resulting in a surge in the consumption of LCP resins. The industrial machinery segment of the global LCP market witnessed a growth of 19.20% by value in 2022 compared to the previous year.

- The aerospace industry is the fastest-growing end-user segment in terms of revenue. It is expected to witness a CAGR of 9.11% by value during the forecast period, which can be attributed to the increased production of aircraft components to cater to the growing demand for lighter and more fuel-efficient aircraft that will increase the consumption of LCP in the future. Aerospace production revenue is expected to reach USD 723 billion by 2029 compared to USD 466 billion in 2022.

ASIA-PACIFIC REGION TO DOMINATE THE GLOBAL LCP MARKET OVER THE COMING YEARS

- Liquid crystal polymers are extensively used for various applications, such as in thin-walled high-precision parts exposed to high heat, in regions such as Asia-Pacific, North America, and South America. Some of LCP's key applications are in the automotive, electrical and electronic, and industrial machinery end-user industries. Liquid crystal polymers accounted for a 0.65% share of the global engineering plastics market in 2022 by revenue.

- Asia-Pacific witnessed a 3.70% growth in value in 2022 over the previous year. This could be attributed to the electrical and electronics and automotive industries, which accounted for value shares of 75.96% and 69.59%, respectively, of the global demand for LCP from these end-user industries. With an increase in the demand for technology, gaming consoles, and electronic devices due to companies adopting work-from-home models and people setting up home offices, the global LCP market is likely to increase.

- In 2022, North America was the second-largest regional consumer of LCP, with a share of 14.27% by revenue. The region holds a predominant share in the global consumption of LCP as it accounts for the highest number of end-user applications in industry segments such as automotive and electronics. For example, the region accounted for a 10.09% share of global vehicle production and a 9.92% share of global electronic component production in 2022.

- Africa is the second fastest-growing region, and it is expected to grow by 9.82% by value in 2023 compared to 2022, led by the electrical and electronics industry. The major South Korean electrical and electronics brands have a strong foothold in Africa, with Samsung accounting for 35% of the smartphone market. Samsung is the leading investor in the manufacturing and assembly of electronic machinery goods in Ethiopia and Sudan.

Liquid Crystal Polymers (LCP) Industry Overview

The Liquid Crystal Polymers (LCP) Market is fairly consolidated, with the top five companies occupying 80.34%. The major players in this market are Celanese Corporation, Daicel Corporation, Shenzhen WOTE Advanced Materials Co.,Ltd., Solvay and Sumitomo Chemical Co., Ltd. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End User Trends

- 4.2 Regulatory Framework

- 4.3 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION

- 5.1 End User Industry

- 5.1.1 Aerospace

- 5.1.2 Automotive

- 5.1.3 Electrical and Electronics

- 5.1.4 Industrial and Machinery

- 5.1.5 Other End-user Industries

- 5.2 Region

- 5.2.1 Africa

- 5.2.1.1 By Country

- 5.2.1.1.1 Nigeria

- 5.2.1.1.2 South Africa

- 5.2.1.1.3 Rest of Africa

- 5.2.2 Asia-Pacific

- 5.2.2.1 By Country

- 5.2.2.1.1 Australia

- 5.2.2.1.2 China

- 5.2.2.1.3 India

- 5.2.2.1.4 Japan

- 5.2.2.1.5 Malaysia

- 5.2.2.1.6 South Korea

- 5.2.2.1.7 Rest of Asia-Pacific

- 5.2.3 Europe

- 5.2.3.1 By Country

- 5.2.3.1.1 France

- 5.2.3.1.2 Germany

- 5.2.3.1.3 Italy

- 5.2.3.1.4 Russia

- 5.2.3.1.5 United Kingdom

- 5.2.3.1.6 Rest of Europe

- 5.2.4 Middle East

- 5.2.4.1 By Country

- 5.2.4.1.1 Saudi Arabia

- 5.2.4.1.2 United Arab Emirates

- 5.2.4.1.3 Rest of Middle East

- 5.2.5 North America

- 5.2.5.1 By Country

- 5.2.5.1.1 Canada

- 5.2.5.1.2 Mexico

- 5.2.5.1.3 United States

- 5.2.6 South America

- 5.2.6.1 By Country

- 5.2.6.1.1 Argentina

- 5.2.6.1.2 Brazil

- 5.2.6.1.3 Rest of South America

- 5.2.1 Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Celanese Corporation

- 6.4.2 Daicel Corporation

- 6.4.3 Kingfa SCI. & TECH. CO., LTD.

- 6.4.4 Ningbo Jujia New Material Technology Co., Ltd

- 6.4.5 Shanghai PRET Composite Material Co., Ltd.

- 6.4.6 Shenzhen WOTE Advanced Materials Co.,Ltd.

- 6.4.7 Solvay

- 6.4.8 Sumitomo Chemical Co., Ltd.

- 6.4.9 TORAY INDUSTRIES, INC.

- 6.4.10 UENO FINE CHEMICALS INDUSTRY, LTD.

7 KEY STRATEGIC QUESTIONS FOR ENGINEERING PLASTICS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

02-2729-4219

+886-2-2729-4219

液晶聚合物全球市场报告 2024

液晶聚合物全球市场报告 2024 5G用液晶聚合物(LCP)的全球市场:2023年

5G用液晶聚合物(LCP)的全球市场:2023年 聚合物分散液晶市场报告:2030 年趋势、预测与竞争分析

聚合物分散液晶市场报告:2030 年趋势、预测与竞争分析 液晶聚合物 (LCP) 薄膜和层压材料的全球市场

液晶聚合物 (LCP) 薄膜和层压材料的全球市场 液晶聚合物市场:按类型和用途- 2023-2030 年全球预测

液晶聚合物市场:按类型和用途- 2023-2030 年全球预测 液晶聚合物纤维 (LCP纤维) 的全球市场:考察与预测 (到2029年)

液晶聚合物纤维 (LCP纤维) 的全球市场:考察与预测 (到2029年) 液晶聚合物的全球市场:趋势,机会,竞争分析(2023年~2028年)

液晶聚合物的全球市场:趋势,机会,竞争分析(2023年~2028年) 全球特殊聚合物市场上的液晶聚合物 (2023-2028年):趋势、成长机会、竞争分析

全球特殊聚合物市场上的液晶聚合物 (2023-2028年):趋势、成长机会、竞争分析 液晶聚合物的全球市场

液晶聚合物的全球市场![液晶聚合物 [LCP] 的全球市场(类型:溶致 LCP、热致 LCP、盘状柱状 LCP、金属致 LCP)——行业分析、规模、份额、增长、趋势、预测,2022-2031 年](/sample/img/cover/42/1229504.png) 液晶聚合物 [LCP] 的全球市场(类型:溶致 LCP、热致 LCP、盘状柱状 LCP、金属致 LCP)——行业分析、规模、份额、增长、趋势、预测,2022-2031 年

液晶聚合物 [LCP] 的全球市场(类型:溶致 LCP、热致 LCP、盘状柱状 LCP、金属致 LCP)——行业分析、规模、份额、增长、趋势、预测,2022-2031 年

▼