|

市场调查报告书

商品编码

1329866

建筑粘合剂的市场规模和份额分析 - 增长趋势和预测(2023-2028)Construction Adhesives Market Size & Share Analysis - Growth Trends & Forecasts (2023 - 2028) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

建筑粘合剂市场规模预计将从2023年的89.4亿美元增长到2028年的120.2亿美元,预测期内(2023-2028年)复合年增长率为6.10%。

COVID-19 的爆发对建筑行业产生了一些短期和长期影响,并可能影响对建筑粘合剂和密封剂的需求。 美国总承包商协会(AGC)表示,将会出现工作中断和项目取消的情况,办公、娱乐和体育设施等“非必要”项目的需求可能会减少。 这些项目和其他建筑活动的暂停往往会减少对建筑粘合剂的需求。

主要亮点

- 短期来看,新兴国家住房和建筑项目的增加以及建筑业投资的增加是推动市场的主要因素。

- 但是,严格的排放环境法规可能会抑制市场增长。

- 建筑行业对生物基和混合粘合剂的需求不断增加,以及粘合剂对绿色建筑的贡献,可能会在未来为市场创造机会。

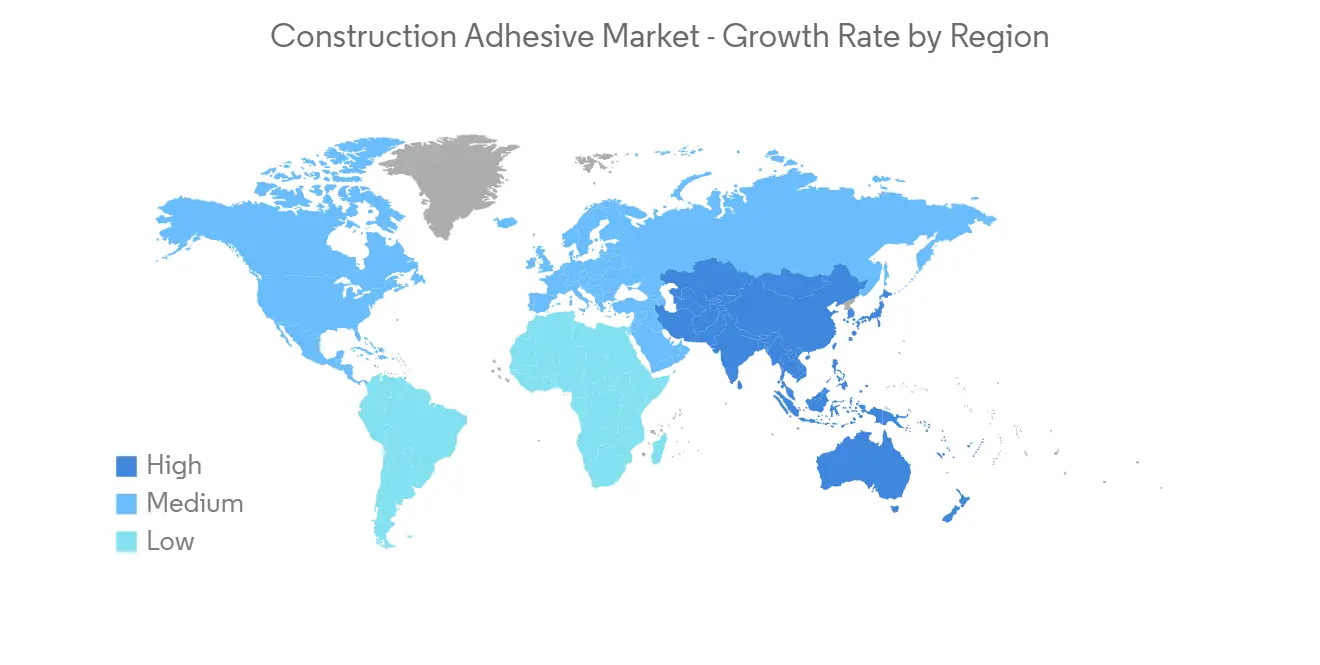

- 亚太地区在市场中占据主导地位,并且由于中国和印度的建筑活动不断增加,预计在预测期内将继续占据主导地位。

建筑胶粘剂市场趋势

主要住宅区

- 在住宅建筑中,粘合剂有多个应用领域,例如铺设地毯、层压檯面、安装地板和粘贴壁纸。 通过使用粘合剂,您可以减少使用的螺钉数量并提高房屋的耐候性。

- 受人口增长、农村地区向服务业集群转移以及核心家庭增多等因素影响,过去几年全球住房建设呈现显着增长。 此外,土地与人口比率的下降以及高层住宅和城镇建设的增长趋势正在促进粘合剂在全球住宅建筑领域的应用。

- 在全球范围内,满足住房需求的供应严重短缺。 这为投资者和开发商提供了巨大的机会,可以采用替代的施工方法和新的合作伙伴关係来推动发展。

- 根据牛津经济研究院的估计,2020 年全球建筑业产值为 10.7 万亿美元,2020 年至 2030 年间将增长 42%,达到 4.5 万亿美元和 15.2 万亿美元。预计将达到 例如

- 在美国,《今日世界建筑》报导称,美国总承包商委员会 (AGC) 评估了联邦数据,并确定对多种类型商业建筑的需求将在一段时间内保持强劲。

- 据国际建设报导,中国政府计划从2023年起同比增加重大建设和基础设施项目支出1.8万亿美元,以支持地区经济从疫情中復苏。

- 在加拿大,各种政府项目正在支持该行业的扩张,包括经济适用房计划 (AHI)、加拿大新建计划 (NBCP) 和加拿大製造。

- 根据欧盟统计局的数据,与 2023 年 1 月相比,2023 年 2 月欧元区 (EA20) 的建筑产量增长了 2.3%,欧盟 27 国的建筑产量增长了 2.1%。

- 由于上述因素,全球建筑业预计将增长,建筑粘合剂的需求预计也会增加。

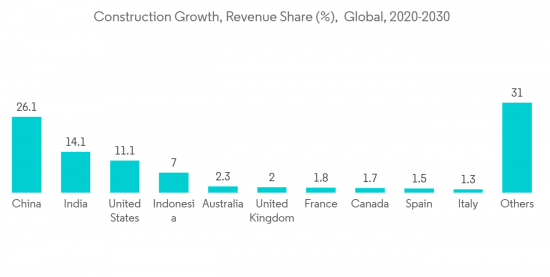

亚太地区主导市场

- 由于印度、中国和东南亚国家建筑市场的巨大需求,亚太地区是建筑粘合剂的最大市场。

- 过去十年,由于主要经济和商业中心的发展,以及建筑商之间对有吸引力的外观和可持续、经济的建筑的竞争,该地区的商业办公楼和建筑数量有所增加。

- 由于中央政府鼓励对该行业的投资作为维持经济增长的手段,中国建筑业迅速发展。

- 根据中国国家统计局的数据,2022 年中国建筑业增加值约为 8.3 万亿元人民币(1.18 万亿美元)。

- 儘管中国政府努力实现经济再平衡,转向更加以服务为导向的模式,但我们仍制定了建设计划。

- 根据印度品牌资产基金会 (IBEF) 的数据,到 2025 年,印度建筑业将发展成为全球第三大市场,规模约为 1 万亿美元。

- 根据日本国土交通省的数据,2022 年日本将建造约 859,500 套住房。 根据经济研究所的数据,截至2023年4月的日本月度建筑材料价格指数为147.8。

- 这些因素预计将推动亚太地区建筑粘合剂市场的发展。

建筑胶粘剂行业概况

全球建筑粘合剂市场本质上是整合的。 主要参与者包括汉高粘合剂技术印度私人有限公司、陶氏化学、H.B. Fuller、阿科玛集团和 3M。

其他好处

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第一章简介

- 调查的先决条件

- 调查范围

第二章研究方法

第 3 章执行摘要

第 4 章市场动态

- 促进因素

- 增加建筑业投资

- 新兴国家的住房和建筑项目增加

- 其他司机

- 抑制因素

- 严格的环境法规

- 其他抑制因素

- 价值链分析

- 波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第 5 章市场细分(基于价值的市场规模)

- 类型

- 水性

- 溶剂型

- 热熔胶

- 反应性

- 其他类型

- 应用

- 住宅用途

- 商业

- 基础设施

- 工业/设施

- 地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 其他亚太地区

- 北美

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 意大利

- 法国

- 欧洲其他地区

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东/非洲

- 沙特阿拉伯

- 南非

- 其他中东和非洲地区

- 亚太地区

第6章竞争态势

- 併购、合资企业、联盟、协议

- 市场份额(%)分析**/市场排名分析

- 各大公司的战略

- 公司简介

- 3M

- Adhesives Technology Corporation(ATC)

- Ashland

- Avery Dennison Corporation

- Bostik

- Don Construction Products Limited

- Dow

- Franklin International

- Gorilla Glue Inc.

- H.B. Fuller Company

- Henkel Adhesives Technologies India Private Limited

- Huntsman International LLC

- MAPEI S.p.A.

- RPM International Inc.

- Sika AG

- Wacker Chemie AG

第7章市场机会和未来趋势

- 建筑行业对生物基和混合粘合剂的需求增加

- 有助于绿色建筑的粘合剂

The Construction Adhesives Market size is expected to grow from USD 8.94 billion in 2023 to USD 12.02 billion by 2028, at a CAGR of 6.10% during the forecast period (2023-2028).

The outbreak of COVID-19 brought several short-term and long-term consequences in the construction industry, which is likely to affect the demand for construction adhesives and sealants. According to the Associated General Contractors of America (AGC), there were disruptions to work or canceled projects, and the demand may be potentially less for "non-essential" projects, like offices, entertainment, and sports facilities. Due to the shutdown of such projects and other construction activities, the demand for construction adhesives tends to constrain.

Key Highlights

- In the short term, major factors driving the market studied are the increase in housing and construction projects in emerging countries and increasing investments in the construction industry.

- However, stringent environmental regulations related to emissions will likely restrain the market's growth.

- Increasing demand for bio-based and hybrid adhesives in the construction sector and adhesive contribution to green construction is likely to create opportunities for the market in the future.

- Asia-Pacific dominated the market and is projected to continue its dominance during the forecast period due to the rise in construction activities in China and India.

Construction Adhesives Market Trends

The Residential Segment to Dominate the Market

- In residential construction, adhesives have several application areas like carpet laying, laminating countertops, installing flooring, wallpapering, etc. The use of adhesives can reduce the usage of screws and help in weatherproofing the house.

- Residential construction across the globe has been witnessing significant growth over the past few years owing to factors like population growth, migration from rural areas to service sector clusters, and the growing trend of nuclear families. Besides, decreasing land-to-population ratio and the growing trend of constructing high-rise residential buildings and townships have been driving the application of adhesives in the residential construction segment across the globe.

- Globally, there has been a significant undersupply to meet the demand for housing. This presented a major opportunity for the investors and developers to embrace alternative construction methods and new partnerships to bring forward development.

- According to Oxford Economics Estimates, in 2020, the global construction output was USD 10.7 trillion and is expected to grow by 42% or USD 4.5 trillion between 2020 and 2030 to reach USD 15.2 trillion. For instance:

- In the United States, according to World Construction Today, the Associated General Contractors of America's- AGC evaluation of the federal data determined that the demand for numerous kinds of commercial construction will remain strong for the immediate future.

- According to International Construction, the Chinese government is set to increase its spending on large construction and infrastructure projects by USD 1.8 trillion year-on-year starting from 2023 to help regional economies recover from the pandemic.

- Various government projects in Canada, including the Affordable Housing Initiative (AHI), New Building Canada Plan (NBCP), and Made in Canada, have supported the sector's expansion.

- According to Eurostat, in February 2023, construction production increased by 2.3% in the euro area (EA20) and 2.1% in EU-27 compared to January 2023.

- Due to all the factors above, the global construction industry is expected to grow, so the demand for construction adhesives is also expected to increase.

Asia-Pacific Region to Dominate the Market

- Asia-Pacific accounted for the largest market for construction adhesives, owing to huge demand from the construction market in India, China, and various countries in Southeast Asia.

- The number of commercial offices and buildings in the region has increased since the last decade, owing to major economic and business centers' growth and competition among the construction players for attractive looks and sustainable and economical construction.

- China's construction industry developed rapidly due to the central government's push for investment in the construction industry as a means to sustain economic growth.

- China's construction industry generated an added value of around 8.3 trillion yuan (USD 1.18 trillion) in 2022, according to the National Bureau of Statistics of China.

- The Chinese government rolled out massive construction plans, including making provision for the movement of 250 million people to its new megacities over the next ten years, despite efforts to rebalance its economy to a more service-oriented form.

- According to the India Brand Equity Foundation (IBEF), India's construction industry is set to emerge as the third-largest market in the world, with a size of almost USD 1 trillion by 2025.

- According to MLIT (Japan), around 859.5 thousand housing units were initiated in Japan in 2022. According to the Economic Research Association, as of April 2023, Japan's construction materials monthly price index stood at 147.8.

- These factors are expected to drive the construction adhesives market in the Asia-Pacific region.

Construction Adhesives Industry Overview

The global construction adhesive market is consolidated in nature. Some of the major players include Henkel Adhesives Technologies India Private Limited, Dow, H.B. Fuller, Arkema Group, and 3M.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Investments in the Construction Industry

- 4.1.2 Increase in Housing and Construction Projects in Emerging Countries

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Stringent Environmental Regulations

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Type

- 5.1.1 Water-based

- 5.1.2 Solvent-based

- 5.1.3 Hot-melt

- 5.1.4 Reactive

- 5.1.5 Other Types

- 5.2 Application

- 5.2.1 Residential

- 5.2.2 Commercial

- 5.2.3 Infrastructure

- 5.2.4 Industrial and Institutional

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%) Analysis**/Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 3M

- 6.4.2 Adhesives Technology Corporation (ATC)

- 6.4.3 Ashland

- 6.4.4 Avery Dennison Corporation

- 6.4.5 Bostik

- 6.4.6 Don Construction Products Limited

- 6.4.7 Dow

- 6.4.8 Franklin International

- 6.4.9 Gorilla Glue Inc.

- 6.4.10 H.B. Fuller Company

- 6.4.11 Henkel Adhesives Technologies India Private Limited

- 6.4.12 Huntsman International LLC

- 6.4.13 MAPEI S.p.A.

- 6.4.14 RPM International Inc.

- 6.4.15 Sika AG

- 6.4.16 Wacker Chemie AG

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increase In Demand for Bio-based and Hybrid Adhesives in the Construction Industry

- 7.2 Adhesives Contribute to Green Construction

全球建筑黏合剂市场 2023-2030

全球建筑黏合剂市场 2023-2030 建筑黏合剂市场(产品:聚氨酯、丙烯酸、环氧树脂、聚醋酸乙烯酯(PVA)、有机硅;应用:结构性、非结构性)- 全球产业分析、规模、份额、成长、趋势和预测,2023-2031 年

建筑黏合剂市场(产品:聚氨酯、丙烯酸、环氧树脂、聚醋酸乙烯酯(PVA)、有机硅;应用:结构性、非结构性)- 全球产业分析、规模、份额、成长、趋势和预测,2023-2031 年 2024 年建筑黏剂全球市场报告

2024 年建筑黏剂全球市场报告 建筑黏剂市场规模、份额、趋势分析报告:按树脂类型、按技术、按应用、按地区、细分市场预测,2024-2030年

建筑黏剂市场规模、份额、趋势分析报告:按树脂类型、按技术、按应用、按地区、细分市场预测,2024-2030年 全球建筑粘合剂市场

全球建筑粘合剂市场 全球建筑密封胶市场

全球建筑密封胶市场 建设用密封胶的全球市场 (~2028年):树脂类型·用途·各地区

建设用密封胶的全球市场 (~2028年):树脂类型·用途·各地区 全球建筑密封胶市场 2023-2030

全球建筑密封胶市场 2023-2030 建筑黏剂市场:按类型、按树脂类型、按技术、按用途、按最终用户 - 俄罗斯-乌克兰衝突、高通货膨胀的累积影响 - 2023-2030 年全球预测

建筑黏剂市场:按类型、按树脂类型、按技术、按用途、按最终用户 - 俄罗斯-乌克兰衝突、高通货膨胀的累积影响 - 2023-2030 年全球预测 到 2028 年的建筑胶粘剂市场预测——按树脂类型(聚醋酸乙烯酯、聚氨酯、环氧树脂、丙烯酸树脂、有机硅)、技术、应用、最终用户和地区进行的全球分析

到 2028 年的建筑胶粘剂市场预测——按树脂类型(聚醋酸乙烯酯、聚氨酯、环氧树脂、丙烯酸树脂、有机硅)、技术、应用、最终用户和地区进行的全球分析