|

市场调查报告书

商品编码

1331237

聚偏氟乙烯 (PVDF) 市场规模和份额分析 - 增长趋势和预测(2023-2029)Polyvinylidene Fluoride (PVDF) Market Size & Share Analysis - Growth Trends & Forecasts (2023 - 2029) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

聚偏二氟乙烯(PVDF)的全球市场规模预计将从2023年的67.21千吨增长到2028年的152千吨,在预测期内(2023-2029年)复合年增长率为17.73% 。

主要亮点

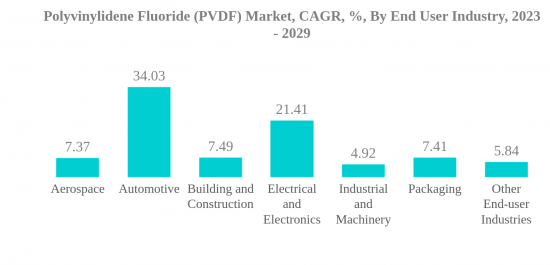

- 工业和机械行业是最大的最终用户行业。 由于涂层和衬里应用对 PVDF 树脂的高需求,工业和机械行业占据了最大的市场份额。

- 汽车是一个快速发展的最终用户行业。 在汽车行业,PVDF材料在电池和电动汽车中的使用越来越多,预计将为市场增长创造机会。

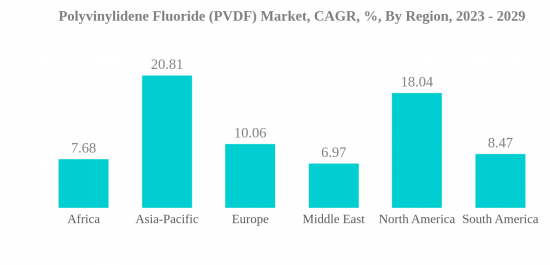

- 亚太地区是最大的地区。 亚太地区以印度、中国、日本和韩国等主要新兴经济体为主导。 这些国家也是PVDF在汽车、食品和饮料等领域的最大消费国。

- 亚太地区是一个快速发展的地区。 亚太地区汽车、建筑、包装等各行业投资大幅增长。 亚太地区预计将成为增长最快的市场。

聚偏二氟乙烯 (PVDF) 市场趋势

汽车行业需求的扩大推动市场增长

- PVDF 是一种高度非反应性含氟聚合物,具有紫外线稳定性、耐化学性、耐磨性和阻燃性。 通常用于需要最高纯度零件的应用。 PVDF是最常用的含氟聚合物之一,到2022年将占全氟聚合物子树脂类型总消费量的16.21%。

- PVDF 具有柔韧性、重量轻、导热性低、耐化学腐蚀和耐高温等理想特性,使电气和电子行业成为按价值计算最大的消费者。 PVDF 通常用作电缆的绝缘材料。 它作为电池(包括锂离子电池)绝缘材料的用途也在扩大。 由于锂离子电池和电缆绝缘材料需求的快速增长,预计在预测期内(2023-2029年)该行业的PVDF需求价值复合年增长率为21.42%。

- 按价值计算,工业机械领域是 PVDF 的第二大消费者。 PVDF因其高拉伸强度、耐辐射、耐磨性和化学特性而成为该领域的首选。 例如,在化学加工工业中,PVDF用于轴承、容器、管道、管件、隔离阀、衬里、泵叶轮壳等。 也用作设备的耐腐蚀、防水涂层。

- 汽车行业是增长最快的消费领域,预测期内价值复合年增长率预计为 34.03%。 制动管、车底紧固件、门槛板和尾灯罩对 PVDF 涂层的需求不断增长,这主要是由于其卓越的耐腐蚀性和耐化学性。

非洲未来可能成为主要市场

- 2022年,全球PVDF市场占全球含氟聚合物市场的12.21%。 全球PVDF的主要消费地区是亚太地区和北美。

- 亚太地区是 PVDF 最大的消费国,预计在预测期内价值复合年增长率为 20.81%。 中国和日本等国家是PVDF的主要用户,到2022年分别占PVDF市场总收入份额的60%和17%。 我国工业机械行业是PVDF的主要消费大国。 近年来,我国大力投资发展先进机床,包括高速、精密机床,以及智能、数字化製造技术。 政府的目标是到2025年使中国成为先进製造业的世界领先者。 政府制定了智能製造五年发展规划,目标是实现70%大型企业数字化。

- 北美是第二大消费国,预计在预测期内的复合年增长率为 18.04%。 这一增长预计将受到该地区电气和电子设备製造投资增加的推动。 施耐德将在2022年投资1亿美元,增加该地区的电气产品产量。 美国是该地区PVDF的主要消费国之一,市场收入份额为92%。 这是由该地区电子行业推动的,预计在预测期内,电子行业的价值复合年增长率为 17.19%。

聚偏二氟乙烯 (PVDF) 行业概览

聚偏氟乙烯(PVDF)市场整合度较高,前五名企业占比77.03%。 该市场的主要参与者是(按字母顺序排列)阿科玛、东岳集团、吴羽株式会社、中化集团和索尔维。

其他好处:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章执行摘要和主要发现

第 2 章报告要约

第 3 章简介

- 研究假设和市场定义

- 调查范围

- 调查方法

第 4 章主要行业趋势

- 最终用户趋势

- 监管框架

- 价值炼和分销渠道分析

第 5 章市场细分

- 最终用户行业

- 航空航天

- 汽车

- 建筑/施工

- 电气/电子

- 工业/机械

- 包装

- 其他最终用户行业

- 地区

- 非洲

- 按国家/地区

- 尼日利亚

- 南非

- 其他非洲

- 亚太地区

- 按国家/地区

- 澳大利亚

- 中国

- 印度

- 日本

- 马来西亚

- 韩国

- 其他亚太地区

- 欧洲

- 按国家/地区

- 法国

- 德国

- 意大利

- 俄罗斯

- 英国

- 欧洲其他地区

- 中东

- 按国家/地区

- 沙特阿拉伯

- 阿拉伯联合酋长国

- 其他中东地区

- 北美

- 按国家/地区

- 加拿大

- 墨西哥

- 美国

- 南美洲

- 按国家/地区

- 阿根廷

- 巴西

- 南美洲其他地区

- 非洲

第 6 章竞争态势

- 主要战略趋势

- 市场份额分析

- 公司情况

- 公司简介

- 3M

- Arkema

- Dongyue Group

- Hubei Everflon Polymer CO., Ltd.

- KUREHA CORPORATION

- RTP Company

- Sinochem

- Solvay

- Zhejiang Juhua Co., Ltd.

- ZheJiang Yonghe Refrigerant Co.,Ltd

第 7 章首席执行官面临的关键战略问题

第 8 章附录

- 世界概览

- 摘要

- 五力分析框架

- 世界价值链分析

- 市场动态 (DRO)

- 来源和参考文献

- 图表列表

- 主要见解

- 数据包

- 词彙表

简介目录

Product Code: 62721

The Global Polyvinylidene Fluoride (PVDF) Market size is expected to grow from 67.21 Kilo metric tons in 2023 to 152 Kilo metric tons by 2028, at a CAGR of 17.73% during the forecast period (2023-2029).

Key Highlights

- Industrial and Machinery is the Largest End User Industry. The industrial and machinery industry registered the largest market share due to the high demand for PVDF resin for coating and lining applications.

- Automotive is the Fastest-growing End User Industry. The increasing usage of PVDF materials in batteries and electric vehicles in the automobile industry is likely to create opportunities for market growth.

- Asia-Pacific is the Largest Region. Asia-Pacific was driven by major developing economies like India, China, Japan, and South Korea. These countries also happen to be the largest consumers of PVDF in automotive, food and beverages, etc.

- Asia-Pacific is the Fastest-growing Region. Asia-Pacific witnessed a significant increase in investments in various industries, including automotive, construction, packaging, etc. It is projected to have the fastest growth in the market.

Polyvinylidene Fluoride (PVDF) Market Trends

GROWING DEMAND FROM THE AUTOMOTIVE INDUSTRY TO LEAD THE MARKET'S GROWTH

- PVDF is known as a highly non-reactive fluoropolymer with UV stability and resistance to chemicals, abrasion, and flame. It is often used in applications that require components of the highest purity levels. PVDF is one of the most frequently used fluoropolymers, accounting for 16.21% of the total consumption of all fluoropolymer sub-resin types in 2022.

- The electrical and electronics segment is the largest consumer of PVDF in terms of value due to its desired properties like flexibility, lightweight nature, low thermal conductivity, chemical corrosion resistance, and heat resistance. PVDF is commonly used as insulation on electrical cables. Its application as an insulating material in batteries, including lithium-ion batteries, has also grown. Owing to the rapidly growing demand for lithium-ion batteries and cable insulations, the demand for PVDF from the segment is expected to record a CAGR of 21.42% in terms of value during the forecast period (2023-2029).

- The industrial machinery segment is the second-largest consumer of PVDF in terms of value. Its high tensile strength, resistance to radiation, abrasion, and chemical properties make it a preferred material in this segment. For instance, in the chemical processing industry, PVDF is used in bearings, vessels, pipes, pipe fittings, isolation valves, linings, and pump impeller casing. It is also used as a corrosion and water-resistance coating for equipment.

- The automotive segment is the fastest-growing consumer, with an expected CAGR of 34.03% in terms of value during the forecast period. The demand for PVDF coating in brake tubes, underbody fasteners, rocker panels, and tail lamp housings is growing, primarily due to its excellent corrosion and chemical resistance.

AFRICA MAY BECOME A MAJOR MARKET IN THE FUTURE

- The global PVDF market accounted for 12.21% of the global fluoropolymers market in 2022. Asia-Pacific and North America are among the major consumers of PVDF globally.

- Asia-Pacific is the largest consumer of PVDF and is expected to record a CAGR of 20.81% in terms of value during the forecast period. Countries like China and Japan majorly utilize PVDF, occupying 60% and 17%, respectively, of the total PVDF market share in terms of revenue in 2022. China's industrial machinery industry is the major consumer of PVDF. In recent years, China has invested heavily in the development of advanced machine tools, such as high-speed and precision machine tools, as well as smart and digitalized manufacturing technologies. The government aims to make China a world leader in advanced manufacturing by 2025. The government has set a five-year plan for smart manufacturing development, with the goal of digitizing 70% of its large enterprises.

- North America is the second-largest consumer and is projected to record a CAGR of 18.04% in terms of value during the forecast period. This growth is expected due to the rising investments in the region's electrical and electronics manufacturing. Schneider invested USD 100 million in 2022 to increase the production of electrical goods in the region. The United States is among the major consumers of PVDF in the region, with a market revenue share of 92%, owing to its electronics industry, which is predicted to record a CAGR of 17.19% in terms of value during the forecast period.

Polyvinylidene Fluoride (PVDF) Industry Overview

The Polyvinylidene Fluoride (PVDF) Market is fairly consolidated, with the top five companies occupying 77.03%. The major players in this market are Arkema, Dongyue Group, KUREHA CORPORATION, Sinochem and Solvay (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End User Trends

- 4.2 Regulatory Framework

- 4.3 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION

- 5.1 End User Industry

- 5.1.1 Aerospace

- 5.1.2 Automotive

- 5.1.3 Building and Construction

- 5.1.4 Electrical and Electronics

- 5.1.5 Industrial and Machinery

- 5.1.6 Packaging

- 5.1.7 Other End-user Industries

- 5.2 Region

- 5.2.1 Africa

- 5.2.1.1 By Country

- 5.2.1.1.1 Nigeria

- 5.2.1.1.2 South Africa

- 5.2.1.1.3 Rest of Africa

- 5.2.2 Asia-Pacific

- 5.2.2.1 By Country

- 5.2.2.1.1 Australia

- 5.2.2.1.2 China

- 5.2.2.1.3 India

- 5.2.2.1.4 Japan

- 5.2.2.1.5 Malaysia

- 5.2.2.1.6 South Korea

- 5.2.2.1.7 Rest of Asia-Pacific

- 5.2.3 Europe

- 5.2.3.1 By Country

- 5.2.3.1.1 France

- 5.2.3.1.2 Germany

- 5.2.3.1.3 Italy

- 5.2.3.1.4 Russia

- 5.2.3.1.5 United Kingdom

- 5.2.3.1.6 Rest of Europe

- 5.2.4 Middle East

- 5.2.4.1 By Country

- 5.2.4.1.1 Saudi Arabia

- 5.2.4.1.2 United Arab Emirates

- 5.2.4.1.3 Rest of Middle East

- 5.2.5 North America

- 5.2.5.1 By Country

- 5.2.5.1.1 Canada

- 5.2.5.1.2 Mexico

- 5.2.5.1.3 United States

- 5.2.6 South America

- 5.2.6.1 By Country

- 5.2.6.1.1 Argentina

- 5.2.6.1.2 Brazil

- 5.2.6.1.3 Rest of South America

- 5.2.1 Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 3M

- 6.4.2 Arkema

- 6.4.3 Dongyue Group

- 6.4.4 Hubei Everflon Polymer CO., Ltd.

- 6.4.5 KUREHA CORPORATION

- 6.4.6 RTP Company

- 6.4.7 Sinochem

- 6.4.8 Solvay

- 6.4.9 Zhejiang Juhua Co., Ltd.

- 6.4.10 ZheJiang Yonghe Refrigerant Co.,Ltd

7 KEY STRATEGIC QUESTIONS FOR ENGINEERING PLASTICS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

02-2729-4219

+886-2-2729-4219

2024-2032 年 PVDF 树脂市场报告(按类型、晶相类型、应用、最终用途行业和地区)

2024-2032 年 PVDF 树脂市场报告(按类型、晶相类型、应用、最终用途行业和地区) 聚二氟亚乙烯市场:依最终用途产业、按涂料、按地区

聚二氟亚乙烯市场:依最终用途产业、按涂料、按地区 PVDF 树脂的全球市场:市场规模、份额、趋势分析 - 按结晶相类型、最终用户、应用、区域分類的展望和预测(2023-2030 年)

PVDF 树脂的全球市场:市场规模、份额、趋势分析 - 按结晶相类型、最终用户、应用、区域分類的展望和预测(2023-2030 年) 聚二氟亚乙烯膜市场报告:2030 年趋势、预测与竞争分析

聚二氟亚乙烯膜市场报告:2030 年趋势、预测与竞争分析 聚偏氟乙烯市场:依最终用户产业、应用分类 - 2024-2030 年全球预测

聚偏氟乙烯市场:依最终用户产业、应用分类 - 2024-2030 年全球预测 全球聚偏氟乙烯 (PVDF) 市场 - 2023-2030

全球聚偏氟乙烯 (PVDF) 市场 - 2023-2030 聚偏氟乙烯管道和附件市场报告:2030 年趋势、预测和竞争分析

聚偏氟乙烯管道和附件市场报告:2030 年趋势、预测和竞争分析 PVDF树脂的全球市场:2023年

PVDF树脂的全球市场:2023年 聚偏氟乙烯 (PVDF) 的全球市场

聚偏氟乙烯 (PVDF) 的全球市场 全球聚偏氟乙烯市场研究报告 - 2023 年至 2030 年行业分析、规模、份额、增长、趋势和预测

全球聚偏氟乙烯市场研究报告 - 2023 年至 2030 年行业分析、规模、份额、增长、趋势和预测

▼