|

市场调查报告书

商品编码

1641832

云端基础的工作负载调度软体 -市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)Cloud-based Workload Scheduling Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

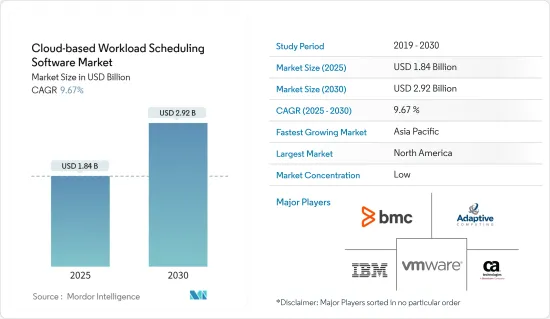

云端基础的工作负载调度软体市场规模预计在 2025 年为 18.4 亿美元,预计到 2030 年将达到 29.2 亿美元,预测期内(2025-2030 年)的复合年增长率为 9.67%。

在采用新技术时,企业必须考虑并规划与分散式和云端环境中的工作负载处理和关键应用程式的可用性相关的影响。因此,预计未来对更好的工作负载调度软体的需求将会成长。

关键亮点

- 云端基础的工作负载调度软体可以协调、监控、操作、分析和预测工作负载。这使该组织能够解决未来可能出现的问题并管理其资产。

- 云端基础的工作负载调度软体有助于在无需人工干预的情况下改善工作负载调度。复杂的调度和分析能力使组织能够提高劳动力效率。这是云端基础的工作量调度软体的主要驱动因素。

- 同样,各跨国企业对云端基础的服务的快速采用和日益增长的偏好预计将在预测期内推动云端基础的工作负载调度软体市场的扩张,从而提供充足的新机会。

- 然而,开放原始码软体的可用性和快速采用是云端基础的工作负载调度软体成长的主要限制因素。满足严格的合规性和法规的日益增长的需求可能会对云端基础的工作负载调度软体的发展构成挑战。

- 疫情期间,出于公共卫生考虑,全球许多国家都强制要求在家在家工作,这增加了对远距工作基础设施的需求。因此,包括政府机构在内的各级组织都必须适应日益增长的虚拟服务需求、公民对这些服务交付日益增长的期望、政府员工队伍重组的长期潜力,并适应不断变化的业务需求。一系列潜在影响,包括需要提供动态监管模式。这就产生了对云端基础的工作量调度软体的需求。疫情过后,随着企业转向云端基础的服务,市场蓬勃发展。

云端基础的工作负载调度软体市场趋势

公共云端服务将占据最大市场占有率

- 企业正在转向云端基础的服务以有效控製成本。管理大量资料也是这项转变解决的问题之一。这一趋势受到免费、开放原始码和高度可自订的云端基础的服务的推动。

- 对于寻求以经济高效的方式管理工作负载的中小型企业来说,转向云端基础的工作量调度软体是一个快速成长的趋势。

- 例如,2022 年 12 月,自主数位企业软体解决方案领域的领导参与企业之一 BMC 宣布,其云端基础的BMC Helix 解决方案将帮助 Buchanan Technologies 和 Mphasis 等公司在其数位转型之旅。 ServiceOps 功能来打破资料孤岛的现代企业提供了选择。

- Start-Ups文化增加了对云端基础的服务的需求,而云端基础的服务的广泛采用仍然是Start-Ups趋势出现的重要因素。

- 根据 Flexera Software 调查,80% 的受访企业使用 Microsoft Azure 满足其公共云端需求。亚马逊、微软 Azure 和谷歌云端被称为超大规模资料中心业者,是全球最大的云端运算平台供应商之一。截至 2022 年 3 月,80% 的企业受访表示他们的公司已经采用了混合云端。转向混合云端通常是以牺牲单一私有云端云和公共云端运作为代价的。

预计北美将占据最大市场占有率

- 在北美,由于IT基础设施的兴起和新组织的出现,对云端基础的工作负载调度软体的需求正在增长。

- 在北美,完全自动化和云端基础的组织日益增长的趋势正在推动市场的发展。北美率先推行自带装置 (BYOD) 文化,推动了 BYOD 的广泛采用。这促使组织转向混合云端模型,透过私有云端确保敏感业务资讯的安全,同时透过公共云端解决方案为员工提供更多应用程式。这一趋势有利于提高生产力,预计在预测期内将持续并成长。

- 北美正在见证来自主要参与者以及 Workfront 等新参与企业的云端基础的工作量调度软体产品的增加。 Asana、Acuity Scheduling 等

- 此外,该地区正在经历混合云端和多重云端环境中采用的新型云工具的爆炸性增长。同时,现有的云端平台正在转型以适应新的混合现实。各大公共云端供应商正在增强其管理、工作负载调度软体、运算、网路、安全性和其他工具,以支援混合云端营运。此外,由于资料完整性和隐私性,对云端平台的需求不断增加,这将在研究期间进一步增加工作负载调度软体市场的采用,从而为主要供应商在市场上的成长提供更多机会。如此。

云端基础的工作负载调度软体产业概况

云端基础的工作负载调度软体市场由 BMC Software(Boxer Parent Company, Inc)、CA, Inc(Broadcom Inc)、VMware, Inc、IBM Corporation 和 Adaptive Computing Enterprises, Inc(ALA Services LLC)等主要企业主导。 )是存在的,而且非常分散。该市场的参与企业正在采用合作和收购等策略来加强其软体产品并获得可持续的竞争优势。

- 2023 年 10 月,全球软体解决方案供应商 TeamPoint Software 与真正的云端反应式即时资源调度和优化 SAAS 应用程式 More-IQ 宣布建立策略合作伙伴关係,预计将改变现场服务管理领域。此次合作将 More-IQ 先进的工作排程技术与 TeamPoint 的现场服务软体解决方案经验结合,为寻求优化业务的公司提供新的机会。 TeamPoint 目前正在透过与智慧工作调度专业公司 More-IQ 合作来推广其产品。 More-IQ 的工作排程软体旨在降低营运费用、改善服务交付并尽可能有效率地分配资源。

- 2023年9月,知名科技公司微软和全球电脑软体公司甲骨文宣布扩大合作伙伴关係,以使客户能够将其关键任务资料库工作负载迁移到Azure。微软与 Oracle 的紧密伙伴关係致力于减少客户将工作负载迁移到公共云端时所遇到的常见障碍。在 Azure 中提供 Oracle 资料库服务的最新解决方案是 Oracle Database@Azure。透过让客户将 Oracle资料库迁移到 OCI 并将其与 Microsoft Cloud 中的当前工作负载一起部署在 Azure 上,组织可以开发创新解决方案并进一步与竞争对手区分开来。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概况

- 产业价值链分析

- 产业吸引力-波特五力分析

- 新进入者的威胁

- 购买者/消费者的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争强度

- COVID-19 对市场的影响

第五章 市场动态

- 市场驱动因素

- 企业转向云端基础的服务

- 云端基础的工作负载调度软体中分析工具的可用性

- 市场限制

- 开放原始码免费软体阻碍市场成长

第六章 市场细分

- 透过云端

- 民众

- 私人的

- 杂交种

- 按最终用户

- 企业

- 政府

- 其他的

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

第七章 竞争格局

- 公司简介

- BMC Software(Boxer Parent Company, Inc.)

- CA, Inc.(Broadcom Inc.)

- VMware, Inc.

- IBM Corporation

- Adaptive Computing Enterprises, Inc.(ALA Services LLC)

- ASG Technologies Group, Inc.

- Cisco Systems Inc.

- Hitachi, Ltd.

- ManageIQ, Inc.(Red Hat, Inc.)

第八章 市场机会与未来趋势

第九章投资分析

The Cloud-based Workload Scheduling Software Market size is estimated at USD 1.84 billion in 2025, and is expected to reach USD 2.92 billion by 2030, at a CAGR of 9.67% during the forecast period (2025-2030).

As enterprises roll out new technologies, they need to consider and plan for impacts related to workload processing and the availability of critical applications across distributed and cloud environments; hence the need for better workload scheduling software is projected to increase in the future.

Key Highlights

- The cloud-based workload scheduling software available can integrate, monitor, and operate workloads, perform analysis, and give predictions for the future. This empowers organizations with abilities to tackle problems that can arise in the future and also manage assets.

- Cloud-based workload scheduling software helps to improve workload scheduling without the need for human intervention. Sophisticated scheduling and analytical abilities help organizations increase employee efficiency. This is a significant drive for the cloud-based workload scheduling software.

- Similarly, the rapid adoption and increasing preference for cloud-based services by various multinational businesses would provide enough new opportunities, driving the expansion of the cloud-based workload scheduling software market during the forecasted period.

- However, the ease of availability, and the rapid growth of open-source software, are acting as major constraints for the growth of cloud-based workload scheduling software. The growing need to meet strict compliance and regulations has the potential to challenge the growth of cloud-based workload scheduling software.

- During the pandemic, many countries across the globe mandated work from home based on public health safety concerns that drove the need for remote working infrastructure. Therefore, organizations operating at all levels, including government bodies, expected a wide range of potential impacts, such as increased demand for virtual services coupled with rising citizen expectations around the delivery of these services, the longer-term potential for reshaping the government workforce, and the need to provide adaptive and dynamic regulatory models. Thus, such impacts necessitated the cloud-based workload scheduling software for enhanced service experience. Post-pandemic, the market grew rapidly, with enterprises shifting towards cloud-based services.

Cloud Based Workload Scheduling Software Market Trends

Public Cloud-Based Services is set to hold the largest market share

- Enterprises are shifting towards cloud-based services effectively manage costs. Large data management is another problem eliminated due to this shift. Adding to this trend is the growing availability of free, open-source, and highly customizable cloud-based services.

- The change to cloud-based workload scheduling software is a trend fast catching up the Small and Medium Enterprises that would like to take up cost-effective alternatives to manage their workloads.

- For instance, in December 2022, BMC, one of the prominent players in software solutions for the Autonomous Digital Enterprise, confirmed that its cloud-based BMC Helix solution is offering a choice for modern enterprises exploring ServiceOps capabilities to break down staff, tool, and data siloes on their digital transformation journeys, such as Buchanan Technologies and Mphasis.

- The startup culture has increased the demand for cloud-based services, and the proliferation of cloud-based services remains an essential factor for the emergence of the startup trend.

- According to Flexera Software, 80 percent of enterprise respondents used Microsoft Azure for public cloud purposes. Amazon, Microsoft Azure, and Google Cloud, known as hyper scalers, are among the largest global cloud computing platform providers. As of March 2022, 80 percent of enterprise respondents stated they had implemented a hybrid cloud in their firm. The transition to hybrid cloud solutions is typically done at the expense of operating single private and public clouds.

North America is Expected to Register the Largest Market Share

- Increasing IT infrastructure and the emergence of new organizations in the North American region have led to increasing demand for cloud-based workload scheduling software.

- The growing trend of an entirely automated and cloud-based organization in the American region drives the market. North America pioneered the bring-your-own-device (BYOD) culture, resulting in widespread incorporation. This has led organizations to shift toward hybrid cloud models to ensure the safety of sensitive business information via private cloud while providing a greater reach of applications to employees through public cloud solutions, which is necessary for some applications requiring on-field access. This trend benefits productivity and is expected to continue and grow during the forecast period.

- North America has witnessed an increase in cloud-based workload scheduling software products from the major players and growing new players like Workfront. Asana, Inc., Acuity Scheduling, and Inc., among others.

- Further, the region is witnessing an explosion of new cloud tools adopted for hybrid and multi-cloud environments. At the same time, established cloud platforms are pivoting to fit into the new hybrid reality. The large public cloud providers are ramping up tools, including offerings in management, workload scheduling software, computing, networking, and security, to support hybrid cloud operations. In addition, the ongoing increase in demand for cloud platforms based on data integrity and privacy is further expected to increase the workload schedule software market adoption in the study period and enable leading vendors with more opportunities to grow in the market.

Cloud Based Workload Scheduling Software Industry Overview

The Cloud-based Workload Scheduling Software Market is highly fragmented, with the presence of key players like BMC Software (Boxer Parent Company, Inc.), CA, Inc. (Broadcom Inc.), VMware, Inc., IBM Corporation, and Adaptive Computing Enterprises, Inc.(ALA Services LLC). Players in the market are adopting strategies such as partnerships and acquisitions to enhance their software offerings and gain sustainable competitive advantage.

- In October 2023, TeamPoint Software, a global software solution provider, and More-IQ, a true cloud reactive and real-time resource scheduling and optimization SAAS application, announced a strategic partnership that is anticipated to transform the field service management sector. Organizations looking to optimize their operations through this partnership will access new opportunities as More-IQ's advanced job scheduling technology and TeamPoint's experience in field service software solutions are combined. TeamPoint is now promoting its products through a partnership with the intelligent job scheduling professionals More-IQ. More-IQ's work scheduling software aims to reduce operating expenses, improve service delivery, and allocate resources as efficiently as possible.

- In September 2023, Microsoft, a prominent technology corporation and Oracle, a global computer software firm, announced extending their partnership to ensure customers can migrate their mission-critical database workloads to Azure. Microsoft's strong partnership with Oracle keeps them focused on lowering clients' typical obstacles when moving workloads to the public cloud. The newest solution to deliver Oracle Database services inside Azure is Oracle Database@Azure. Organizations can develop innovative solutions and further differentiate themselves from competitors by enabling clients to transfer Oracle databases to OCI and deploy them in Azure alongside their present workloads in the Microsoft Cloud.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Enterprises Shifting Towards Cloud-Based Services

- 5.1.2 Availability of Analytical tools in Cloud based Workload Scheduling Software

- 5.2 Market Restraints

- 5.2.1 Opensource-Free Software Hampering the Growth of Market

6 MARKET SEGMENTATION

- 6.1 By Cloud

- 6.1.1 Public

- 6.1.2 Private

- 6.1.3 Hybrid

- 6.2 By End User

- 6.2.1 Corporate

- 6.2.2 Government

- 6.2.3 Other End Users

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia Pacific

- 6.3.4 Latin America

- 6.3.5 Middle East & Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 BMC Software (Boxer Parent Company, Inc.)

- 7.1.2 CA, Inc. (Broadcom Inc.)

- 7.1.3 VMware, Inc.

- 7.1.4 IBM Corporation

- 7.1.5 Adaptive Computing Enterprises, Inc. (ALA Services LLC)

- 7.1.6 ASG Technologies Group, Inc.

- 7.1.7 Cisco Systems Inc.

- 7.1.8 Hitachi, Ltd.

- 7.1.9 ManageIQ, Inc. (Red Hat, Inc.)

8 MARKET OPPORTUNITIES AND FUTURE TRENDS

9 INVESTMENT ANALYSIS

2026年全球云端工作负载调度软体市场报告2026年全球工作负载调度与自动化市场报告

2026年全球云端工作负载调度软体市场报告2026年全球工作负载调度与自动化市场报告 全球工作负载调度和自动化市场规模、份额、趋势和成长分析报告(2026-2034)

全球工作负载调度和自动化市场规模、份额、趋势和成长分析报告(2026-2034) 全球云端基础工作量调度软体市场全球工作负载调度与自动化市场

全球云端基础工作量调度软体市场全球工作负载调度与自动化市场 云端基础的工作负载调度软体的全球市场,2024-2028

云端基础的工作负载调度软体的全球市场,2024-2028