|

市场调查报告书

商品编码

1331339

动态交联热塑性弹性体 (TPV) 市场规模和份额分析 - 增长趋势和预测 (2023-2028)Thermoplastic Vulcanizate (TPV) Market Size & Share Analysis - Growth Trends & Forecasts (2023 - 2028) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

动态交联热塑性弹性体 (TPV) 市场规模预计将从 2023 年的 417.05 千吨扩大到 2028 年的 558.11 千吨,预测期内(2023-2028 年)复合年增长率为 6%。

COVID-19 大流行扰乱了动态交联热塑性弹性体市场,导致由于运输限制和各行业需求减少而导致供应减少。 然而,由于汽车、建筑行业需求增加,市场于 2022 年復苏。

主要亮点

- 推动市场的主要因素包括汽车行业需求的激增、消费品行业利用率的提高以及与可回收材料使用相关的政府优惠政策。

- 然而,耐化学性差、耐磨性低以及原材料价格波动可能会限制交联热塑性弹性体市场的动态。

- 医疗保健行业的扩大使用和电器需求的激增预计将成为该市场的主要增长机会。

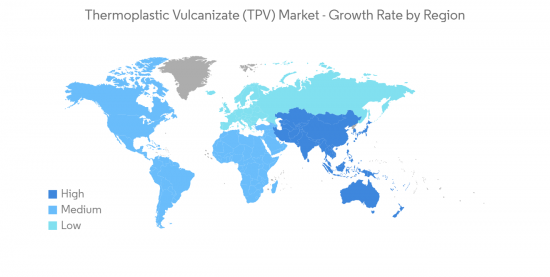

- 预计亚太地区将成为预测期内增长最快的地区。

动态交联热塑性弹性体 (TPV) 市场趋势

汽车领域主导市场

- 近年来,由于对豪华、低排放、安全和高性能车辆的需求不断增长,轻质汽车材料大幅增长。

- 因此,供应商和製造商推出了各种解决方案,帮助 OEM 满足不断收紧的法规并满足广泛的消费者偏好。

- TVP在汽车行业的主要应用包括软管盖、进气管盖、垫圈、密封件、波纹护套、减振器、支柱盖、点火组件、衬套、车窗密封件等。

- TPV 的柔性发动机罩下汽车部件包括进气管和波纹管、轮舱喇叭口、转向系统波纹管和隔音部件。

- 成本是最大的优势,TPV 比 EPDM 低 10-30%;加上重量更轻、设计灵活性更强以及可回收性,TPV 比 EPDM 低 10-30%。 此外,TPV 更轻,使得车辆更省油。

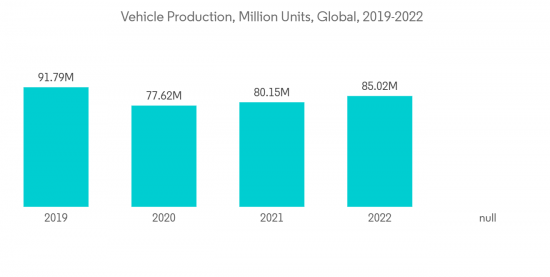

- 根据国际汽车製造商协会 (OICA) 的预测,由于全球私家车需求增加,2022 年全球汽车产量将同比增长 6%。

- 2022年中国汽车产量将达到270,206,615辆,同比增长3%。 2022年加拿大汽车产量也将达到12,28,735辆,比上年增长10%。

- 因此,由于上述因素,汽车行业预计将主导市场。

亚太地区增长迅速

- 中国、日本和印度的广泛需求是推动亚太市场需求的关键原因之一。

- 中国是世界上最大的汽车生产国。 然而,最近中国的汽车产量一直在下降。 经济波动和中美贸易战影响了汽车行业的表现。

- 中国正致力于扩大电动汽车的生产和销售。 为此,中国计划增加电动汽车(EV)的产量。 国际能源署(IEA)设定了到2025年中国新车产量中电动汽车占比达到20%的目标。

- 此外,根据国际汽车製造商协会 (OICA) 的数据,2022 年中国汽车总产量为 27,020,615 辆,较 2021 年增长 3%。

- 中国蓬勃发展的经济为消费品製造商提供了全球最大的增长机会。 被中国消费品市场的巨大潜力所吸引,不少外资企业纷纷在中国设立生产基地。 随着消费品产量的增长,动态交联热塑性弹性体的消费需求也可能会增加。

- 根据世界资源研究所 (WRI) 的数据,中国正处于建设热潮之中。 该国是全球最大的建筑市场,占全球建筑投资的20%。 到 2030 年,预计仅中国的建设投资就将达到约 13 万亿美元。

- 在日本,东京在投资和市场发展前景方面已成为该地区其他主要城市中的顶级市场,在住宅领域占有很大份额。

- 因此,在预测期内,汽车、建筑和消费品行业的预计增长可能会推动亚太地区对动态交联热塑性弹性体的国内需求。

动态交联热塑性弹性体(TPV)行业概述

动态交联热塑性弹性体 (TPV) 市场得到整合,主要参与者占据约 70% 的市场份额。 主要公司(排名不分先后)包括埃克森美孚公司、三井化学、Teknor Apex、Dawn Group 和 KUMHO POLYCHEM。

其他好处:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第一章简介

- 调查的先决条件

- 调查范围

第二章研究方法

第 3 章执行摘要

第 4 章市场动态

- 协调员

- 汽车行业的广泛需求

- 消费品行业越来越多地使用动态交联热塑性弹性体

- 有关使用可回收材料的政府优惠政策

- 抑制因素

- 耐化学性和耐磨性较低

- 原材料价格变化

- 行业价值链分析

- 波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

- 原材料分析

第 5 章市场细分(市场规模:基于数量)

- 最终用户行业

- 汽车

- 建筑/施工

- 消费品

- 医疗保健

- 其他最终用户行业

- 地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 其他亚太地区

- 北美

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 意大利

- 法国

- 西班牙

- 欧洲其他地区

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东/非洲

- 沙特阿拉伯

- 南非

- 其他中东和非洲地区

- 亚太地区

第6章竞争态势

- 併购、合资企业、联盟、协议

- 市场份额 (%)**/排名分析

- 各大公司的战略

- 公司简介

- Avient Corporation

- Celanese Corporation

- Elastron TPE

- Exxon Mobil Corporation

- FM Plastics

- Kumho Polychem

- LCY GROUP

- LyondellBasell Industries holdings B.V.

- Mitsubishi Chemical Corporation

- Mitsui Chemicals Inc.

- Ravago

- RTP Company

- Teknor Apex

- Trinseo

第7章市场机会和未来趋势

- 扩大医疗保健行业的应用

- 对电气应用的需求不断增长

The Thermoplastic Vulcanizate (TPV) Market size is expected to grow from 417.05 kilotons in 2023 to 558.11 kilotons by 2028, at a CAGR of 6% during the forecast period (2023-2028).

The COVID-19 pandemic disrupted the thermoplastic vulcanizate market, resulting in a reduction in supply due to transportation restrictions and a decline in demand from various sectors. Nonetheless, the market rebounded in 2022 due to increased demand from the automotive, building, and construction industries.

Key Highlights

- The major factors driving the market studied are the surge in demand from the automobile industry, the increase in utilization in the consumer goods industry, and favorable government policies related to using recyclable materials.

- However, poor resistance to chemicals and low wear resistance, and fluctuation in raw material prices could restrain the thermoplastic vulcanizate market.

- Growing use in the healthcare industry and surging demand for electrical appliances are expected to be major growth opportunities for the market.

- The Asia-Pacific region is expected to be the largest and fastest-growing region in the forecast period.

Thermoplastic Vulcanizate (TPV) Market Trends

The Automotive Segment to Dominate the Market

- Automotive lightweight materials grew robustly over the past couple of years due to the increasing demand for luxurious, low-on-emission, safe, and high-performance vehicles.

- As a result, suppliers and manufacturers introduced various solutions that help OEMs meet continually tightening regulations and satisfy the widening range of consumers' tastes.

- The major applications of TVP in the automotive industry include hose coverings, air inlet duct covers, gaskets, seals, convoluted boots, vibration dampeners, strut covers, ignition components, bushings, and window seals.

- TPV flexible automotive under-the-hood components include air intake tubes and bellows, wheel well flares, steering system bellows, and sound abatement parts.

- Cost is the biggest advantage, with TPVs being 10-30% lower than EPDM, coupled with lower weight, improved design flexibility, and recyclability. Furthermore, the lightweight of TPV enables more fuel-efficient vehicles.

- In 2022, According to the International Organization of Motor Vehicle Manufacturers (OICA), global automobile production increased by 6% compared to the previous year due to increasing global demand for private mobility.

- In China, the total vehicle production was 270,20,615, with an increase of 3% in 2022 compared to the previous year. Also, in Canada, the total vehicle production was 12,28,735 in 2022, with an increase of 10% in the production of vehicles in the country compared to the previous year.

- Thus, based on the factors above, the automotive segment is expected to dominate the market.

Asia-Pacific to Witness the Fastest Growth

- Extensive demand from China, Japan, and India is one of the key reasons driving the demand in the market in Asia-Pacific.

- China is the world's largest automotive producer. However, the country witnessed a decline in the production of vehicles in the recent past. The economic shifts and China's trade war with the United States affected the automotive industry's performance.

- China is focusing on increasing the production and sales of electric vehicles. For this purpose, the country planned to increase the production of electric vehicles (EVs). It targeted to reach the share of electric vehicles to 20% of China's total new car production by 2025, stated the International Energy Agency (IEA).

- Moreover, according to the International Organization of Motor Vehicle Manufacturers (OICA), in 2022, the total vehicle production in China stood at 27,020,615 units, which increased by 3% compared to 2021.

- China's booming economy offered consumer product companies some of the world's greatest growth opportunities. Attracted by the huge potential of China's consumer goods market, many foreign companies entered China and set up production units. With the growth of consumer goods production, thermoplastic vulcanizate consumption may also see an increased demand.

- According to World Resources Institute (WRI), China is in the middle of a construction mega-boom. The country includes the largest building market in the world, making up 20% of all construction investment globally. The country alone is expected to spend nearly USD 13 trillion on buildings by 2030.

- In Japan, Tokyo emerged as a top market among the rest of the major cities in the region for investments and development prospects, of which the residential sector accounted for the major share.

- Thus, the anticipated growth in the automotive, construction, and consumer goods industries will likely drive the domestic demand for thermoplastic vulcanizate during the forecast period in Asia-Pacific.

Thermoplastic Vulcanizate (TPV) Industry Overview

The thermoplastic vulcanizate (TPV) market is consolidated, with the top players accounting for around 70% of the market share. The major companies (in no particular order) include Exxon Mobil Corporation, Mitsui Chemicals Inc., Teknor Apex, Dawn Group, and KUMHO POLYCHEM.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Extensive Demand from the Automobile Industry

- 4.1.2 Increase in Use of Thermoplastic Vulcanizate in the Consumer Goods Industry

- 4.1.3 Favourable Government Policies Related to the Use of Recyclable Materials

- 4.2 Restraints

- 4.2.1 Poor Chemical and Wear Resistance

- 4.2.2 Fluctuation in Raw Material Prices

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

- 4.5 Raw Material Analysis

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 End-user Industry

- 5.1.1 Automotive

- 5.1.2 Building and Construction

- 5.1.3 Consumer Goods

- 5.1.4 Healthcare

- 5.1.5 Other End-user Industries

- 5.2 Geography

- 5.2.1 Asia-Pacific

- 5.2.1.1 China

- 5.2.1.2 India

- 5.2.1.3 Japan

- 5.2.1.4 South Korea

- 5.2.1.5 Rest of Asia-Pacific

- 5.2.2 North America

- 5.2.2.1 United States

- 5.2.2.2 Canada

- 5.2.2.3 Mexico

- 5.2.3 Europe

- 5.2.3.1 Germany

- 5.2.3.2 United Kingdom

- 5.2.3.3 Italy

- 5.2.3.4 France

- 5.2.3.5 Spain

- 5.2.3.6 Rest of Europe

- 5.2.4 South America

- 5.2.4.1 Brazil

- 5.2.4.2 Argentina

- 5.2.4.3 Rest of South America

- 5.2.5 Middle-East and Africa

- 5.2.5.1 Saudi Arabia

- 5.2.5.2 South Africa

- 5.2.5.3 Rest of Middle-East and Africa

- 5.2.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share(%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Avient Corporation

- 6.4.2 Celanese Corporation

- 6.4.3 Elastron TPE

- 6.4.4 Exxon Mobil Corporation

- 6.4.5 FM Plastics

- 6.4.6 Kumho Polychem

- 6.4.7 LCY GROUP

- 6.4.8 LyondellBasell Industries holdings B.V.

- 6.4.9 Mitsubishi Chemical Corporation

- 6.4.10 Mitsui Chemicals Inc.

- 6.4.11 Ravago

- 6.4.12 RTP Company

- 6.4.13 Teknor Apex

- 6.4.14 Trinseo

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Rising Usage in the Healthcare Industry

- 7.2 Growing Demand in Electrical Applicances

动态交联热可塑性橡胶(TPV) 市场,依类型、应用进行的需求分析,预测至 2034 年

动态交联热可塑性橡胶(TPV) 市场,依类型、应用进行的需求分析,预测至 2034 年 热塑性硫化剂市场:现状分析与未来预测 (2024年~2032年)

热塑性硫化剂市场:现状分析与未来预测 (2024年~2032年) 热塑性硫化橡胶市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测动态交联热塑性弹性体(TPV)市场(2018-2034)

热塑性硫化橡胶市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测动态交联热塑性弹性体(TPV)市场(2018-2034) 热塑性硫化合成橡胶(TPV) 的全球市场规模、份额和成长分析:按等级、加工方法、应用和地区 - 产业预测 (2024-2031)

热塑性硫化合成橡胶(TPV) 的全球市场规模、份额和成长分析:按等级、加工方法、应用和地区 - 产业预测 (2024-2031) 热塑性硫化剂市场:按原料、製程和应用分类 - 全球预测 2025-2030全球热塑性硫化橡胶(TPV)市场规模:依应用、竞争格局、区域格局、预测热塑性硫化橡胶市场规模、份额、趋势分析报告:按应用、牌号、加工方法、地区、细分市场预测,2024-2030

热塑性硫化剂市场:按原料、製程和应用分类 - 全球预测 2025-2030全球热塑性硫化橡胶(TPV)市场规模:依应用、竞争格局、区域格局、预测热塑性硫化橡胶市场规模、份额、趋势分析报告:按应用、牌号、加工方法、地区、细分市场预测,2024-2030 到 2030 年热塑性硫化橡胶的市场预测:按原材料、加工方法、应用、最终用户和地区进行的全球分析

到 2030 年热塑性硫化橡胶的市场预测:按原材料、加工方法、应用、最终用户和地区进行的全球分析 热塑性硫化橡胶市场,按加工方法、按应用、国家和地区划分 - 2023-2030 年行业分析、市场规模、市场份额和预测

热塑性硫化橡胶市场,按加工方法、按应用、国家和地区划分 - 2023-2030 年行业分析、市场规模、市场份额和预测