|

市场调查报告书

商品编码

1334415

液体合成橡胶市场规模和份额分析-增长趋势和预测(2023-2028)Liquid Synthetic Rubber Market Size & Share Analysis - Growth Trends & Forecasts (2023 - 2028) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

液体合成橡胶的全球市场规模预计将从2023年的158.7亿美元增长到2028年的199.9亿美元,预测期内(2023-2028年)复合年增长率为4.72%。

COVID-19 对 2020-2021 年的市场产生了负面影响。 鑑于大流行情况,在政府为遏制新的COVID-19病例传播而采取的封锁措施期间,汽车製造活动暂时停止,导致轮胎、传动带、密封件和垫片的生产。软管和油箱衬里等汽车零部件价格下跌。 然而,市场预计将在 2023 年恢復增长轨迹,并且在预测期内可能遵循类似的轨迹。

主要亮点

- 短期内,粘合剂行业需求的增加预计将推动市场增长。

- 另一方面,原材料价格波动预计将阻碍市场增长。

- 生物基合成橡胶原材料的开发在预测期内可能是一个机遇。

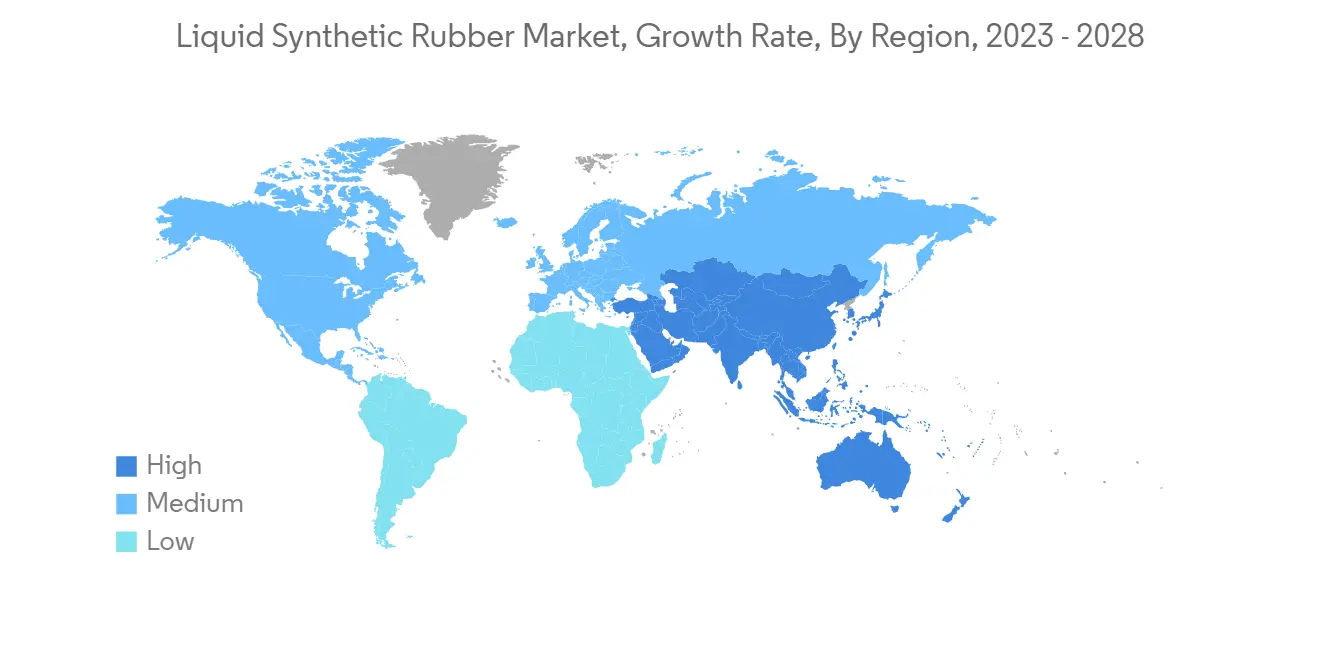

- 亚太地区在液体合成橡胶市场占据主导地位,其中中国、印度和日本等国家的消费量最高。

液体合成橡胶市场趋势

轮胎领域的需求增加

- 液体合成橡胶广泛应用于轮胎製造,因为随着轮胎标籤法规的采用,它们可提供更高的耐用性和卓越的性能。

- 轮胎製造中使用的主要产品是聚丁二烯。 主要用作轮胎胎侧,改善行驶时连续弯曲引起的疲劳。 此外,丁二烯在其他汽车零部件中也有多种用途。

- 根据美国轮胎製造商协会的数据,乘用车和轻型卡车轮胎中合成橡胶的体积比为24%,重型卡车轮胎中合成橡胶的体积比为11%。 此外,约50%的乘用车轮胎由丁苯橡胶与天然橡胶混合製成。

- 根据国际轮胎橡胶协会 (ITRA) 的数据,中国和美国是全球两个最大的轮胎生产国。 中国海关总署数据显示,2022年上半年,中国共出口橡胶轮胎377万吨,同比增长7.2%。

- 此外,根据美国轮胎製造商协会的数据,乘用车和轻型卡车使用的轮胎中有 24% 是合成橡胶(如 SBR),重型卡车使用的轮胎有 11% 是合成橡胶。

- 根据国际汽车製造商组织 (OICA) 的数据,2022 年全球汽车产量将达到约 8,501 万辆,较 2021 年的 8,020.5 万辆增长 5.99%。这表明汽车行业对轮胎的需求将增加行业。 2022年,全球乘用车产量将在6000万辆左右,较2021年增长近7.35%。

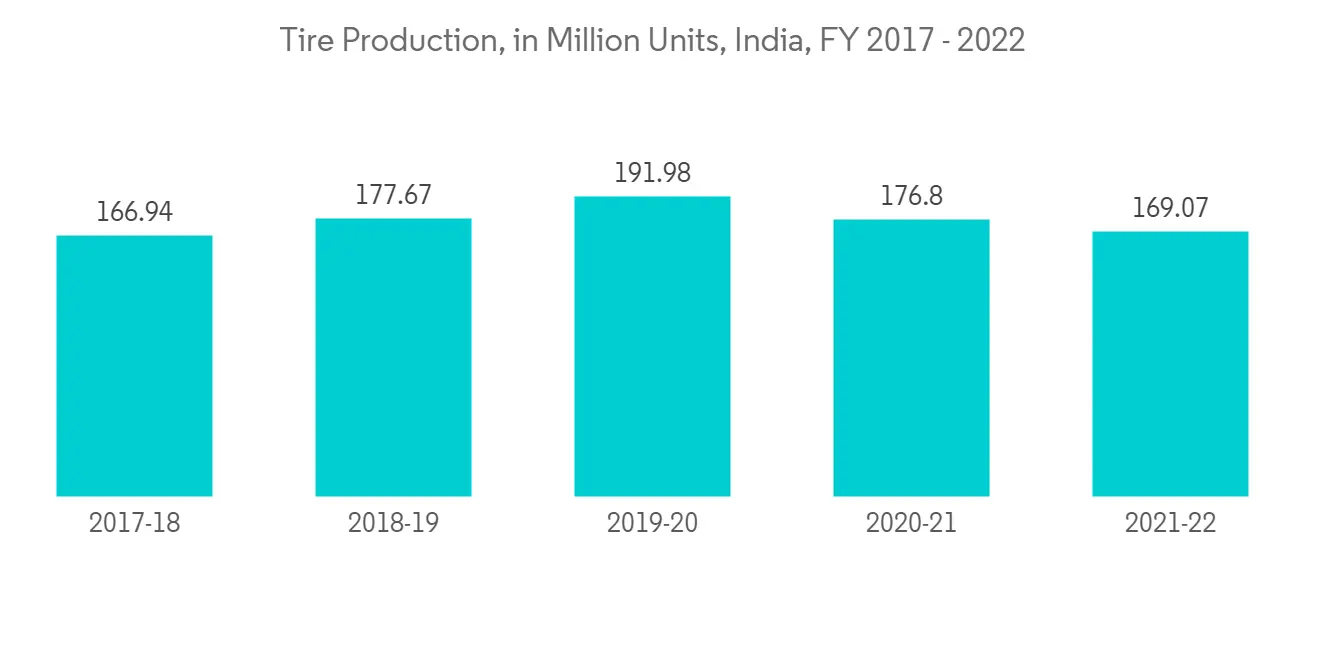

- 但是,在亚洲和欧洲的一些国家,售后市场和 OEM(原始设备製造商)的需求都在下降,导致轮胎产量缓慢但持续下降。 例如,根据ATMA公布的数据,2021-2022年印度轮胎总产量同比下降4%,至1.6907亿条。

- 总体而言,上述所有因素都影响了轮胎生产,预计这将进一步影响液体合成橡胶市场。

亚太地区主导市场

- 预计亚太地区将在预测期内主导液体合成橡胶市场。 这是因为中国、印度和日本等国家的轮胎製造、工业橡胶製造、粘合剂、密封剂、涂料和聚合物改性等应用的需求不断增长。

- 中国是最大的汽车生产国和消费国。 中国汽车工业协会的报告显示,2022年,中国汽车销量同比增长约2.1%。 2022 年销量约为 2,686 万辆,而 2021 年销量为 2,627 万辆。

- 液体合成橡胶也应用于建筑行业。 据国家发展和改革委员会称,中国政府已批准26个基础设施项目,预计投资约1420亿美元,预计将于2023年底完工,目前正在进行中。 摩天大楼和酒店建设的增加正在推动市场研究。

- 截至 2022 年,印度是全球第四大橡胶消费国。 印度人均橡胶消费量目前为 1.2 公斤,而全球人均橡胶消费量为 3.2 公斤。 印度橡胶工业的产值约为 12,000 印度卢比(14.5 亿美元)。 轮胎行业消耗了印度橡胶产量的大部分,占该国总产量的一半以上。

- 印度的橡胶工业是橡胶生产部门与快速增长的橡胶製品製造和消费部门并存的。 推动该国橡胶工业发展的因素包括旨在自给自足和进口替代的机构的积极干预。

- 该地区对轮胎、工业橡胶、粘合剂、密封剂等的需求持续增长,行业内几家主要公司正在扩建生产工厂,预计增长稳定。

液体合成橡胶行业概况

液体合成橡胶市场较为分散,世界各地都有不同的参与者。 在全球市场上保持着较大份额的参与者包括中国石油天然气集团公司、ENEOS公司、赢创工业股份公司、锦湖石化和沙特阿拉伯石油公司阿朗新公司。

其他好处:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章简介

- 调查的先决条件

- 调查范围

第 2 章研究方法

第 3 章执行摘要

第 4 章市场动态

- 促进因素

- 黏合剂行业的需求增加

- 全球轮胎产量增长

- 抑制因素

- 原材料价格变化

- 价值链分析

- 波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第 5 章市场细分(基于价值的市场规模)

- 产品类型

- 液体异戊二烯

- 液体丁二烯

- 液体苯乙烯丁二烯

- 其他产品类型(液体 EPDM、液体 NBR)

- 应用

- 黏合剂

- 工业橡胶

- 轮胎

- 聚合物改性

- 其他用途(防水涂料和鞋类)

- 地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 其他亚太地区

- 北美

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 法国

- 英国

- 意大利

- 欧洲其他地区

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东/非洲

- 沙特阿拉伯

- 南非

- 其他中东和非洲地区

- 亚太地区

第 6 章竞争态势

- 併购、合资企业、联盟、协议

- 市场排名分析

- 各大公司的战略

- 公司简介

- Asahi Kasei Advance Corporation

- China National Petroleum Corporation

- ENEOS Corporation

- Evonik Industries AG

- H.B. Fuller Company

- KUMHO PETROCHEMICAL

- Kuraray Co. Ltd

- Linshi Chem(Puyang)Advanced Material Co. Ltd.

- Lion Elastomers

- NIPPON SODA CO. LTD.

- Saudi Arabian Oil Co.(Arlanxeo)

- SIBUR Holding PJSC

- Synthomer PLC

- TER Group

第 7 章市场机会和未来趋势

- 合成橡胶生物基原材料的开发

The Global Liquid Synthetic Rubber Market size is expected to grow from USD 15.87 billion in 2023 to USD 19.99 billion by 2028, at a CAGR of 4.72% during the forecast period (2023-2028).

COVID-19 negatively impacted the market in 2020-2021. Considering the pandemic scenario, automotive manufacturing activities were temporarily stopped during the government-imposed lockdown to curb the spread of new COVID-19 cases, thereby reducing the demand for liquid synthetic rubber-based automotive parts such as tires, drive belts, seals, gaskets, hoses, tank linings, and others. However, the market is expected to regain its growth trajectory in 2023 and is likely to follow a similar trajectory during the forecast period.

Key Highlights

- Over the short term, the rising demand from the adhesive segment is expected to drive the market's growth.

- On the flip side, fluctuating raw material prices are expected to hinder the market growth.

- Developing bio-based feedstock for synthetic rubber will likely act as an opportunity during the forecast period.

- The Asia-Pacific region dominated the liquid synthetic rubber market, with the largest consumption from countries such as China, India, and Japan.

Liquid Synthetic Rubber Market Trends

Increasing Demand from the Tire Segment

- Liquid synthetic rubber has wide applications in the manufacturing of tires because it provides enhanced durability and superior performance, along with the adoption of tire labeling regulations.

- The primary product used in the manufacturing of tires is polybutadiene. It is primarily used as a sidewall in tires to improve fatigue caused by continuous flexing during the run. Besides, butadiene has various applications in other automobile parts.

- According to the US Tire Manufacturers Association, tires used in passenger and light trucks have 24% synthetic rubber by volume, and tires used in heavy trucks have 11% synthetic rubber by volume. Furthermore, around 50% of car tires are made of styrene-butadiene rubber, which blends with natural rubber.

- According to the International Tyre and Rubber Association (ITRA), China and the United States are the two largest tire-producing countries in the world. According to data from the General Administration of Customs of the PRC, 3.77 million tons of rubber tires were cumulatively exported from China in the first half of 2022, up 7.2% from the same period last year.

- The US Tire Manufacturers Association also stated that tires used in passenger and light trucks use 24% synthetic rubber (such as SBR), and heavy trucks use 11% synthetic rubber by volume.

- According to the Organisation Internationale Des Constructeurs d'Automobiles (OICA), in 2022, around 85.01 million vehicles were produced across the globe, witnessing a growth rate of 5.99% compared to 80.205 million vehicles in 2021, thereby indicating an increased demand for tires from the automotive industry. In 2022, around 60 million passenger cars were manufactured worldwide, up nearly 7.35% compared to 2021.

- However, in several Asian and European countries, production of tires has been witnessing a gradual yet consistent decline due to reduced demand in both the replacement and original equipment manufacturer (OEM) segments. For instance, the total tire production in India declined by 4% to 169.07 million in FY 2021-2022, compared to the previous year, as per the data released from ATMA.

- Overall, all the factors above have impacted tire production, which is further expected to affect the liquid synthetic rubber market.

Asia-Pacific Region to Dominate the Market

- The Asia-Pacific region is expected to dominate the market for liquid synthetic rubber during the forecast period. In countries like China, India, and Japan, owing to the increasing demand from applications such as tire manufacturing, industrial rubber manufacturing, adhesives, sealants, coatings, and polymer modification.

- China is the largest producer and consumer of automotive vehicles. The China Association of Automobile Manufacturers reports that, compared to the prior year, China's automobile sales increased by about 2.1% in 2022. Compared to the 26.27 million automobiles sold in 2021, around 26.86 million were sold in 2022.

- Liquid synthetic rubber also finds application in the construction industry. According to the National Development and Reform Commission, the Chinese government approved 26 infrastructure projects at an estimated investment of about USD 142 billion, estimated to be completed by the end of 2023 and ongoing. The increase in the construction of tall buildings and hotels is driving the market study.

- India is the fourth-largest consumer of rubber in the world as of 2022. Rubber usage per capita in India is currently 1.2 kg, compared to 3.2 kg globally. India's rubber industry generates approximately INR 12,000 crore (USD 1.45 billion). The tire sector consumes most of India's rubber production, accounting for over half of the country's total output.

- The Indian rubber industry exhibits the co-existence of the rubber production sector and the fast-growing rubber product manufacturing and consumption sectors. Factors driving the rubber industry in the country include the positive intervention of institutional agencies that aim at self-sufficiency and import substitution.

- With the ever-increasing demand for tires, industrial rubber, adhesives, and sealants in the region and the expansion of production plants by several major players in the industry, the market for liquid synthetic rubber is also expected to grow steadily during the forecast period.

Liquid Synthetic Rubber Industry Overview

The liquid synthetic rubber market is fragmented in nature, with the presence of a wide range of players worldwide. Some of the players that maintain a significant share in the global market include (not in particular order) China National Petroleum Corporation, ENEOS Corporation, Evonik Industries AG, Kumho Petrochemical, and Saudi Arabian Oil Co. (Arlanxeo).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Rising Demand from the Adhesive Segment

- 4.1.2 Growth in Tire Production Worldwide

- 4.2 Restraints

- 4.2.1 Fluctuating Raw Material Prices

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Product Type

- 5.1.1 Liquid Isoprene

- 5.1.2 Liquid Butadiene

- 5.1.3 Liquid Styrene Butadiene

- 5.1.4 Other Product Types (Liquid EPDM and Liquid NBR)

- 5.2 Application

- 5.2.1 Adhesives

- 5.2.2 Industrial Rubber

- 5.2.3 Tire

- 5.2.4 Polymer Modification

- 5.2.5 Other Applications (Waterproofing Coatings and Footwear)

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 France

- 5.3.3.3 United Kingdom

- 5.3.3.4 Italy

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Asahi Kasei Advance Corporation

- 6.4.2 China National Petroleum Corporation

- 6.4.3 ENEOS Corporation

- 6.4.4 Evonik Industries AG

- 6.4.5 H.B. Fuller Company

- 6.4.6 KUMHO PETROCHEMICAL

- 6.4.7 Kuraray Co. Ltd

- 6.4.8 Linshi Chem (Puyang) Advanced Material Co. Ltd.

- 6.4.9 Lion Elastomers

- 6.4.10 NIPPON SODA CO. LTD.

- 6.4.11 Saudi Arabian Oil Co. (Arlanxeo)

- 6.4.12 SIBUR Holding PJSC

- 6.4.13 Synthomer PLC

- 6.4.14 TER Group

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Development of Bio-based Feedstock for Synthetic Rubber

2025年全球液体合成橡胶市场

2025年全球液体合成橡胶市场 全球液体合成橡胶市场:市场规模、份额、趋势分析(按产品和地区)、细分市场预测(2025-2030 年)

全球液体合成橡胶市场:市场规模、份额、趋势分析(按产品和地区)、细分市场预测(2025-2030 年) 2025年全球液体合成橡胶市场报告

2025年全球液体合成橡胶市场报告 全球液态合成橡胶市场(按类型、应用、最终用户和销售管道)预测(2025-2030 年)

全球液态合成橡胶市场(按类型、应用、最终用户和销售管道)预测(2025-2030 年) 全球液体合成橡胶市场:市场占有率和排名、总销售量和需求预测(2025-2031)

全球液体合成橡胶市场:市场占有率和排名、总销售量和需求预测(2025-2031) 液体合成橡胶市场规模、份额和成长分析(按产品类型、应用、聚合製程、最终用途和地区)- 产业预测 2025-2032液体合成橡胶市场机会、成长动力、产业趋势分析及 2024 - 2032 年预测

液体合成橡胶市场规模、份额和成长分析(按产品类型、应用、聚合製程、最终用途和地区)- 产业预测 2025-2032液体合成橡胶市场机会、成长动力、产业趋势分析及 2024 - 2032 年预测 液状合成橡胶的全球市场 2023-2027

液状合成橡胶的全球市场 2023-2027