|

市场调查报告书

商品编码

1334485

光波长服务市场规模和份额分析 - 增长趋势和预测(2023-2028)Optical Wavelength Services Market Size & Share Analysis - Growth Trends & Forecasts (2023 - 2028) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

光波长服务市场规模预计将从2023年的43.3亿美元增长到2028年的75.4亿美元,预测期内(2023-2028年)复合年增长率为11.71%。

主要亮点

- 预计到 2025 年,全球数据量将翻一番,因此更加需要关注每比特成本和功耗。长距离扩展大波长可以为最终用户提供更具成本效益和更高效的服务。波长扩展还可以显着增加网络带宽,这对于高清内容、5G 蜂窝网络、物联网、远程工作和其他应用至关重要。

- 对光纤到户(FTTH)系统的需求不断增加,不仅在城市地区,而且在农村和偏远地区加速了网络连接的部署。这些投资正在加剧有线电视公司之间的竞争,以提供更密集、更高性能的无线网络和更高波长的服务。

- 2023 年 2 月,Fujitsu发布了 1FINITY,这是一款超可靠的光传输平台,可实现每波长 1.2 太比特每秒 (Tbps) 的数据速率。该平台有助于降低功耗,并将全网二氧化碳排放量减少60%。

- 儘管跨网络更广泛部署 FTTH 具有诸多好处,但运营商对安装额外光纤或最终用户光调製解调器的成本仍犹豫不决。随着行业转向更大的带宽(例如 50G 和 100G),这一成本问题可能会变得更加严重,这需要调製解调器中的相干技术。

- 即使在 COVID-19 大流行之后,网络运营商仍在继续增加设备和容量,以支持远程工作、基于云的服务、流媒体视频、物联网和 5G 无线技术。数据和高速网络日益增长的需求和供应中断正在推动网络解决方案提供商开发高波长网络,该网络可以快速扩展容量以解决流量瓶颈并降低数据传输速率,并推动招聘。

光波长业务市场趋势

10Gbps以下的带宽推动了市场

- 相干WDM技术是一种先进的光传输技术,具有更高的比特率、更大的灵活性、更简单的DWDM线路系统以及更好的光学性能等众多优点。该技术使得DWDM网络中经济高效且可靠的光传输得以发展,波长速度从前相干时代的10Gb/s到100Gb/s、200Gb/s,以及现在现代相干光设备中的波长速度。已提高到400Gb/s和800Gb/s。

- CWDM 和 DWDM 是适应信息传输所需的增加带宽的两种不同方法。DWDM 使用更窄的波长带或通道,而 CWDM 每个通道使用更宽的波长带。

- 英国广播、通信和邮政行业的官方监管机构和竞争机构——通信办公室 (Ofcom) 表示。平均每个人每月使用大约 2.9GB 的数据,并且随着数字化的进步,这一需求只会不断增加。但我们发现10Gb/s对于普通手机用户来说已经足够了。

- 2023 年 2 月,新加坡电信公司 StarHub 推出了超高速宽带,其速度和带宽比新加坡标准宽带服务快 10 倍。这种高速宽带服务显着改善了家庭连接,为在线游戏和光速内容流提供最佳响应能力。

- 2022年6月,视频传输服务MASV采用了具有10Gbps性能的下一代光纤互联网服务。通过此次升级,MASV 现在可以通过云安全高效地传输 PB 级视频,让任何人都可以更快、更经济高效地传输大量视频数据。

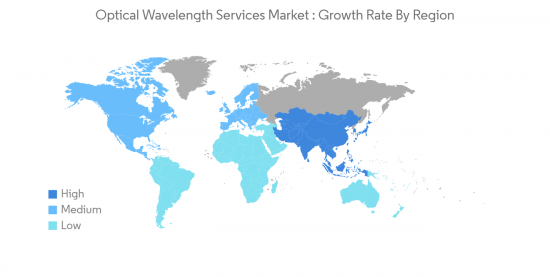

亚太地区占据压倒性的市场份额

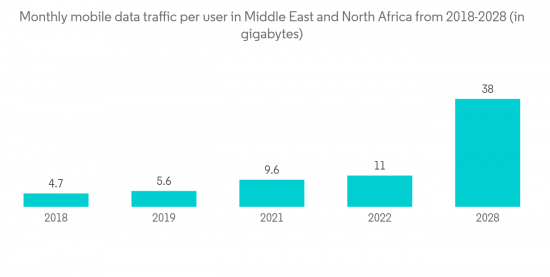

- 印度和中国这两个国家占据了全球移动数据流量的近一半,而北美和欧洲合计仅占全球移动数据服务的四分之一。印度尤其成为移动数据服务市场的主要参与者,其每月移动数据消耗量为全球最高,为每用户 12GB。

- 此外,印度每季度新增 2500 万智能手机用户,使其成为移动数据服务的重要市场。由于智能手机用户的快速增长,预计到 2022 年,每个用户的平均每月数据消耗量将达到 19.5 GB,这表明对数据驱动的应用程序和服务的需求正在增加。这一发展凸显了印度作为全球移动数据市场主要参与者的地位,具有进一步增长和创新的巨大潜力。

- 移动数据服务的强劲增长也刺激了对 5G 设备的需求,而私营部门在 5G 网络上的支出导致这些设备在印度的出货量强劲。据估计,印度5G设备出货量已超过7000万台,到2027年,民用无线网络投资预计将达到约2.5亿美元。这将鼓励运营商提供更强的网络连接速度,进而推动光波长服务的增长。

- 新兴国家政府正在采取举措,促进本国电信基础设施的发展。尤其是亚太地区,由于其廉价劳动力和工业 4.0 的高渗透率,正在成为受欢迎的製造中心。亚洲各国政府正在通过“中国製造2025”等计划积极促进新公司的发展,旨在广泛支持中国製造业和工业4.0的采用。

光波长服务行业概况

光波长服务市场目前竞争适中,但随着供应商计划推出新产品、建立合作伙伴关係和收购,该领域预计将增长。该领域的市场领导者包括 Zayo Group、Nokia、Century Link、Verizon Wireless、Century Link、Windstream Communications。与其他网络设置相比,光波长网络提供了可扩展的解决方案,可以快速增加容量以应对数据传输速率下降或处理流量瓶颈。

2022年3月,电信网络提供商E-Net与EXA基础设施签署协议,在都柏林与其欧洲和北大西洋数据中心之间建立新的高速数据中心间光纤网络连接。该 International Wave 项目旨在在数据中心之间提供具有价格竞争力、安全、快速和透明的连接。

同月,光纤通信解决方案提供商 Zayo Group Holdings 与网络解决方案提供商 Infinera 合作,开发了全球最长的地面 800G 光波长,商用网络覆盖 1,044.51 公里。Infinera硬件解决方案的集成使该项目能够满足更高线速下更多带宽的需求。Zayo 拥有的光纤线路从犹他州斯普林维尔延伸至内华达州里诺,并将由 Infinera 的 ICE6 800G 相干技术提供照明和供电。这一发展展示了光波长服务满足高速数据传输和网络连接不断增长的需求的潜力。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究假设和市场定义

- 调查范围

第二章研究方法论

第三章执行摘要

第四章市场洞察

- 市场概况

- 行业价值链分析

- 行业吸引力——波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争公司之间敌对关係的强度

- 评估 COVID-19 对行业的影响

第五章市场动态

- 市场驱动力

- 互联网需求增加

- 加速带宽密集型应用程序

- 市场製约因素

- 增加带宽可用性限制

- 对虚拟连接的需求增加

第六章市场细分

- 按带宽

- 小于 10Gbps

- 40Gbps

- 100Gbps

- 100Gbps 或更多

- 按地区

- 北美

- 欧洲

- 亚太地区

- 世界其他地区

第七章 竞争格局

- 公司简介

- Nokia Corporation

- Zayo Group Holdings, Inc.

- Verizon Communications Inc.

- GTT Communications, Inc.

- AT&T Inc.

- Lumen Technologies Inc.

- T-Mobile US Inc.

- Crown Castle Inc.

- Comcast Corporation

- Charter Communications

- Windstream Holdings, Inc.

- Colt Technology Services Group Limited

- Cox Communications

- Jaguar Network SAS

- CarrierBid Communications

- EUnetworks Group

- Telia Carrier

- Exascale Limited

第八章投资分析

第 9 章 市场期货

The Optical Wavelength Services Market size is expected to grow from USD 4.33 billion in 2023 to USD 7.54 billion by 2028, at a CAGR of 11.71% during the forecast period (2023-2028).

Key Highlights

- With global data volumes projected to double by 2025, there is a growing need to focus on cost and power consumption per bit. Extending large wavelengths across longer distances can make services more cost-effective and efficient for end-users. Larger wavelengths also provide significant network bandwidth expansion, essential to power high-definition content, 5G cell networks, IoT, remote work, and other applications.

- The demand for fiber-to-home (FTTH) systems is increasing, accelerating the deployment of network connections not just in urban areas but also in rural and remote locations. These investments lead to more robust competition among cable companies to create a denser, higher-performance wireless network and high wavelength services.

- In February 2023, Fujitsu launched the Ultra Optical System called 1FINITY, a hyper-reliable optical transport platform delivering extreme performance and scalability with data rates of 1.2 terabits per second (Tbps) on a single wavelength. This platform helps to reduce power consumption and achieve a 60% reduction of CO2 emissions throughout networks.

- Despite the benefits of implementing FTTH more extensively across networks, carriers are still discouraged by the cost of installing additional fiber and the end-users' optical modems. As the industry transitions to larger bandwidths, such as 50G and 100G, which require coherent technology in the modems, this cost issue will worsen.

- Even after the Covid-19 pandemic, network operators continue to add more gear and capacity to support remote work, cloud-based services, streaming video, IoT, and 5G wireless technology. This increasing demand for data and high-speed networks with uninterrupted supply drives Network Solution providers to adopt high wavelengths that can quickly scale up capacity to address traffic bottlenecks or combat slower data transfer speeds.

Optical Wavelength Services Market Trends

Less than 10 Gbps Bandwidth has Been Driving the Market

- Coherent WDM technology is a highly advanced optical transmission technology that offers numerous benefits, including higher bit rates, greater flexibility, simpler DWDM line systems, and better optical performance. This technology has enabled the development of cost-effective and highly reliable optical transport in DWDM networks, with wavelength speeds increasing from 10 Gb/s in the pre-coherent era to 100 Gb/s, 200 Gb/s, and now even 400 or 800 Gb/s with the latest coherent optical equipment.

- CWDM and DWDM are two different methods for addressing the increasing bandwidth requirements for information transmission. DWDM employs a larger number of narrower wavelength bands or channels, while CWDM uses broader wavelength bands per channel.

- According to the of Communications (Ofcom), the government-approved regulatory and competition authority for the broadcasting, telecommunications, and postal industries of the United Kingdom. The average person uses around 2.9GB of data per month, and this demand is continuously increasing with the evolution of digitalization. However, this confirms that 10Gb/s is more than enough for the average phone user.

- In February 2023, StarHub, the Singaporean telco, introduced ultra-speed broadband with up to 10 times the speed and bandwidth of standard broadband services in Singapore. This high-speed broadband service will significantly enhance household connectivity, providing optimal responsiveness for online gaming and lightning-fast content streaming.

- In June 2022, MASV, the video transfer service, adopted next-generation fiber-optic internet services with 10Gbps performance. This upgrade enables MASV to move Petabytes of video securely and efficiently through the cloud, making it faster, better, and more cost-effective for anyone to transfer large amounts of video data.

Asia Pacific to Hold Dominant Share of the Market

- India and China are the two countries that account for nearly half of the world's mobile traffic, while North America and Europe together only account for a quarter of the global mobile data services. India, in particular, has emerged as a major player in the mobile data services market, with the highest mobile data consumption rate of 12 GB/user a month globally.

- Moreover, India witnesses a remarkable increase of 25 million new smartphone users every quarter, making it a crucial market for mobile data services. This surge in smartphone usage has led to an average data consumption rate of 19.5 GB per user per month in 2022, indicating a growing demand for data-driven applications and services. This trend highlights India's position as a key player in the global mobile data market, with enormous potential for further growth and innovation in the future.

- The strong growth of mobile data services has also fueled demand for 5G devices, with private enterprise spending on 5G networks leading to robust shipments of these devices in India. It is estimated that over 70 million 5G devices have been shipped to India, and the country's investment in private wireless networks is expected to reach approximately USD 250 million by 2027. This will encourage telecom providers to offer more powerful network connection speeds, which, in turn, will promote the growth of Optical Wavelength Services.

- Governments in developing nations are taking initiatives to encourage the development of communication infrastructure in their countries. The Asia-Pacific region, in particular, is becoming increasingly popular as a hub for manufacturing due to its cheap labor and high adoption rate of the Industry 4.0 movement. Governments in Asian countries are aggressively promoting the growth of new firms, with programs like "Made in China 2025" designed to broadly support Chinese manufacturing and the implementation of Industry 4.0.

Optical Wavelength Services Industry Overview

The Optical Wavelength Services Market currently experiences moderate competition, but this sector is expected to grow as vendors plan new product launches, partnerships, and acquisitions. Some of the market leaders in this segment include Zayo Group, Nokia, Century Link, Verizon Wireless, Century Link, and Windstream Communications. Compared to other network setups, optical wavelength networks offer a scalable solution that can quickly increase capacity to combat slower data transfer speeds or address traffic bottlenecks.

In March 2022, Enet, a telecom network provider, signed a contract with EXA Infrastructure to establish new high-speed datacentre-to-datacentre optical network connections between Dublin and data centers in Europe and the North Atlantic. This International Wave project aims to provide price-competitive, secure, high-speed, and transparent inter-datacentre connectivity.

In the same month, Zayo Group Holdings, a provider of fiber-based communications solutions, collaborated with Infinera, a networking solutions provider, to jointly develop the world's longest-known terrestrial 800G optical wavelength in a commercial network that covers 1,044.51 km. With the integration of Infinera's hardware solutions, the project was able to fulfill the demand for more bandwidth at higher line rates. The Zayo-owned fiber route spans from Springville, Utah, to Reno, Nevada, and is lit and powered by Infinera's ICE6 800G coherent technology. This development showcases the potential of optical wavelength services to meet the growing demand for high-speed data transfer and network connectivity.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHT

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Assesment of Covid-19 Impact on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Demand for the Internet

- 5.1.2 Accelerated Bandwidth-intensive Applications

- 5.2 Market Restraints

- 5.2.1 Limited Availability of Incremental Bandwidth

- 5.2.2 Increasing Demand for Virtual Connectivity

6 MARKET SEGMENTATION

- 6.1 By Bandwidth

- 6.1.1 Less than 10 Gbps

- 6.1.2 40 Gbps

- 6.1.3 100 Gbps

- 6.1.4 More Than 100 Gbps

- 6.2 Geography

- 6.2.1 North America

- 6.2.2 Europe

- 6.2.3 Asia Pacific

- 6.2.4 Rest of the World

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles*

- 7.1.1 Nokia Corporation

- 7.1.2 Zayo Group Holdings, Inc.

- 7.1.3 Verizon Communications Inc.

- 7.1.4 GTT Communications, Inc.

- 7.1.5 AT&T Inc.

- 7.1.6 Lumen Technologies Inc.

- 7.1.7 T-Mobile US Inc.

- 7.1.8 Crown Castle Inc.

- 7.1.9 Comcast Corporation

- 7.1.10 Charter Communications

- 7.1.11 Windstream Holdings, Inc.

- 7.1.12 Colt Technology Services Group Limited

- 7.1.13 Cox Communications

- 7.1.14 Jaguar Network SAS

- 7.1.15 CarrierBid Communications

- 7.1.16 EUnetworks Group

- 7.1.17 Telia Carrier

- 7.1.18 Exascale Limited

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

2024-2032 年按频宽、介面、组织规模、应用和地区分類的光波长服务市场报告

2024-2032 年按频宽、介面、组织规模、应用和地区分類的光波长服务市场报告 2024 年光波长服务全球市场报告

2024 年光波长服务全球市场报告 光波长服务的全球市场

光波长服务的全球市场 到 2028 年的光波长服务市场预测——按带宽、光纤通道接口、组织规模和地区进行的全球分析

到 2028 年的光波长服务市场预测——按带宽、光纤通道接口、组织规模和地区进行的全球分析