|

市场调查报告书

商品编码

1384238

日本资料中心市场规模和份额分析 - 成长趋势和预测(2023-2028)Japan Data Center Market Size & Share Analysis - Growth Trends & Forecasts (2023 - 2028) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

日本资料中心市场规模预计将从2023年的190.9亿美元成长到2028年的255.6亿美元,预测期间(2023-2028年)年复合成长率为6.01%。

主要亮点

- IT负担能力:日本资料中心市场的IT负担能力将稳定成长,到2029年可能达到4446.5MW。

- 高架占地面积:到 2029 年,日本的总占地面积预计将达到 1,020 万平方英尺。

- 已安装的机架:预计到2029年,全国已安装的机架总数将达到512,270个。到 2029 年,东京将安装最多数量的机架。

- 直流设备:在日本,绿色直流研发投资备受关注,如北海道石漾市的零排放直流计画。该计划利用了寒冷的气候和接近性可再生能源的优势,为资料成长和政府奖励提供了巨大的潜力。

- 主要市场参与者 在资料中心市场,与竞争相比,AirTrunk Operating Pty Ltd 拥有 15.4% 的高份额。该公司目前营运的IT负担容量为185MW,预计在预测期内将进一步增加。

日本资料中心市场趋势

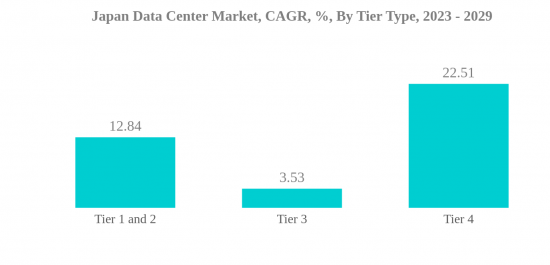

第 3 层是最大的层类型

- 第三层资料中心最受中小型企业的青睐,因为它们具有更好的冗余保护。自第 2 层以来,执行时间已显着改善,第 3 层年度提供 99.982% 的执行时间。该细分市场预计将从2022年的1,309.25兆瓦成长到2029年的1,905.47兆瓦,复合年复合成长率为5.51%。这些资料中心主要是大型企业选择的。

- 第 4 层设施因其效能、低停机时间和 99.99%的执行时间而成为大型企业的下一个首选资料中心。然而,由于其长期的财务和营运永续性,大多数设施仍然更喜欢第 3 级资料中心。 Tier 3 是整个产业采用最广泛的标准。然而,第四级设施预计将出现最大的成长率。

- 由于停机时间长且冗余度低,一级和二级资料中心是最不受欢迎的,但新兴企业通常更喜欢这些资料中心。然而,在日本,新兴企业也更喜欢三级资料中心。目前,日本没有经过 Tier 1 或 Tier 2 认证的设施,预计这一趋势在预测期内将持续下去。

日本资料中心产业概况

日本资料中心市场适度整合,前五名企业占55.68%。该市场的主要企业包括 Colt Technology Services、Digital Realty Trust, Inc.、Equinix, Inc.、IDC Frontier Corporation(软银集团)和 NEC Corporation(按字母顺序排列)。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第1章执行摘要和主要发现

第2章检举要约

第3章简介

- 研究假设和市场定义

- 调查范围

- 调查方法

第4章市场展望

- IT负担能力

- 占地面积

- 主机代管收益

- 安装机架数量

- 机架空间利用率

- 海底电缆

第5章产业主要趋势

- 智慧型手机用户数量

- 每部智慧型手机的资料流量

- 行动资料通讯

- 宽频资料速度

- 光纤连接网路

- 法律规范

- 价值炼和配销通路分析

第6章市场区隔

- 热点

- 大阪

- 东京

- 其他地区

- 资料中心规模

- 大的

- 巨大的

- 中等大小

- 百万

- 小尺寸

- 层级类型

- 1 级和 2 级

- 3 级

- 4 级

- 吞併

- 不曾用过

- 使用

- 按搭配类型

- 超大规模

- 零售

- 批发的

- 按最终用户

- BFSI

- 云

- 电子商务

- 政府机关

- 製造业

- 媒体与娱乐

- 电信

- 其他最终用户

第7章竞争形势

- 市场占有率分析

- 公司形势

- 公司简介

- AirTrunk Operating Pty Ltd.

- Arteria Networks Corporation

- Colt Technology Services

- Digital Edge(Singapore)Holdings Pte Ltd.

- Digital Realty Trust, Inc.

- Equinix, Inc.

- IDC Frontier Inc.(SoftBank Group)

- NEC Corporation

- netXDC(SCSK Corporation)

- NTT Ltd.

- Telehouse(KDDI Corporation)

- Zenlayer Inc

- 调查公司名单

第8章CEO 面临的关键策略问题

第9章附录

- 世界概况

- 概述

- 五力分析框架

- 世界价值链分析

- 全球市场规模和 DRO

- 资讯来源和参考文献

- 图表清单

- 重要见解

- 资料包

- 词彙表

简介目录

Product Code: 71359

The Japan Data Center Market size is expected to grow from USD 19.09 billion in 2023 to USD 25.56 billion by 2028, at a CAGR of 6.01% during the forecast period (2023-2028).

Key Highlights

- IT Load Capacity: The IT load capacity of the Japanese data center market may grow steadily and reach 4446.5 MW by 2029.

- Raised Floor Space: The country's total raised floor area is expected to reach 10.2 million sq. ft by 2029.

- Installed Racks: The country's total number of installed racks is expected to reach 512,270 units by 2029. Tokyo is expected to house the maximum number of racks by 2029.

- DC Facilities: Japan is expected to notice investments in green DC R&D, such as the zero-emission DC plan of Ishikari City, Hokkaido, which leverages the cold climate and proximity to renewable energy, thus offering a huge potential for data growth and government incentives.

- Leading Market Player: AirTrunk Operating Pty Ltd holds the highest share of 15.4% in the data center market compared to its competitors. The company currently operates at an IT load capacity of 185 MW, which is expected to increase during the forecast period.

Japan Data Center Market Trends

Tier 3 is the largest Tier Type

- Tier 3 data centers are mostly preferred by SMBs (small and medium businesses) for their far superior redundancy protection offerings. There is a significant jump in uptime from tier 2, with tier 3 offering annual uptime of 99.982%. The segment is expected to grow from 1,309.25 MW in 2022 to 1,905.47 MW by 2029, registering a CAGR of 5.51%. These data centers are mainly opted for by large companies.

- Tier 4 facilities are the next most preferred data centers by large businesses due to their performance, lower downtime, and 99.99% uptime. However, the majority of facilities still prefer tier 3 data centers due to their long-term financial and operational sustainability. Tier 3 is the most widely adopted standard across the industry. However, the growth rate for tier 4 facilities is expected to be the largest.

- Tier 1 & 2 data centers are the least preferred due to their higher downtime durations and low redundancies, but start-up companies usually prefer these data centers. However, in Japan, start-up companies also prefer tier 3 data center facilities. Currently, in Japan, there are no facilities certified with Tier 1 and Tier 2, and this trend is expected to continue during the forecast period.

Japan Data Center Industry Overview

The Japan Data Center Market is moderately consolidated, with the top five companies occupying 55.68%. The major players in this market are Colt Technology Services, Digital Realty Trust, Inc., Equinix, Inc., IDC Frontier Inc. (SoftBank Group) and NEC Corporation (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 MARKET OUTLOOK

- 4.1 IT Load Capacity

- 4.2 Raised Floor Space

- 4.3 Colocation Revenue

- 4.4 Installed Racks

- 4.5 Rack Space Utilization

- 4.6 Submarine Cable

5 KEY INDUSTRY TRENDS

- 5.1 Smartphone Users

- 5.2 Data Traffic Per Smartphone

- 5.3 Mobile Data Speed

- 5.4 Broadband Data Speed

- 5.5 Fiber Connectivity Network

- 5.6 Regulatory Framework

- 5.7 Value Chain & Distribution Channel Analysis

6 MARKET SEGMENTATION

- 6.1 Hotspot

- 6.1.1 Osaka

- 6.1.2 Tokyo

- 6.1.3 Rest of Japan

- 6.2 Data Center Size

- 6.2.1 Large

- 6.2.2 Massive

- 6.2.3 Medium

- 6.2.4 Mega

- 6.2.5 Small

- 6.3 Tier Type

- 6.3.1 Tier 1 and 2

- 6.3.2 Tier 3

- 6.3.3 Tier 4

- 6.4 Absorption

- 6.4.1 Non-Utilized

- 6.4.2 Utilized

- 6.4.2.1 By Colocation Type

- 6.4.2.1.1 Hyperscale

- 6.4.2.1.2 Retail

- 6.4.2.1.3 Wholesale

- 6.4.2.2 By End User

- 6.4.2.2.1 BFSI

- 6.4.2.2.2 Cloud

- 6.4.2.2.3 E-Commerce

- 6.4.2.2.4 Government

- 6.4.2.2.5 Manufacturing

- 6.4.2.2.6 Media & Entertainment

- 6.4.2.2.7 Telecom

- 6.4.2.2.8 Other End User

7 COMPETITIVE LANDSCAPE

- 7.1 Market Share Analysis

- 7.2 Company Landscape

- 7.3 Company Profiles

- 7.3.1 AirTrunk Operating Pty Ltd.

- 7.3.2 Arteria Networks Corporation

- 7.3.3 Colt Technology Services

- 7.3.4 Digital Edge (Singapore) Holdings Pte Ltd.

- 7.3.5 Digital Realty Trust, Inc.

- 7.3.6 Equinix, Inc.

- 7.3.7 IDC Frontier Inc. (SoftBank Group)

- 7.3.8 NEC Corporation

- 7.3.9 netXDC (SCSK Corporation)

- 7.3.10 NTT Ltd.

- 7.3.11 Telehouse (KDDI Corporation)

- 7.3.12 Zenlayer Inc

- 7.4 LIST OF COMPANIES STUDIED

8 KEY STRATEGIC QUESTIONS FOR DATA CENTER CEOS

9 APPENDIX

- 9.1 Global Overview

- 9.1.1 Overview

- 9.1.2 Porter's Five Forces Framework

- 9.1.3 Global Value Chain Analysis

- 9.1.4 Global Market Size and DROs

- 9.2 Sources & References

- 9.3 List of Tables & Figures

- 9.4 Primary Insights

- 9.5 Data Pack

- 9.6 Glossary of Terms

02-2729-4219

+886-2-2729-4219

资料中心市场:按组件、类型、资料中心评级、最终用户 - 2024-2030 年全球预测

资料中心市场:按组件、类型、资料中心评级、最终用户 - 2024-2030 年全球预测 资料中心耦合市场:按组件、按冷却类型、按资料中心类型、按行业 - 2024-2030 年全球预测

资料中心耦合市场:按组件、按冷却类型、按资料中心类型、按行业 - 2024-2030 年全球预测 资讯中心外包市场:按服务类型、公司规模、产业划分 - 2024-2030 年全球预测

资讯中心外包市场:按服务类型、公司规模、产业划分 - 2024-2030 年全球预测 全球资料中心基础设施管理市场规模、份额、成长分析,按组件、资料中心类型、层级类型、产业 - 产业预测,2024-2031 年

全球资料中心基础设施管理市场规模、份额、成长分析,按组件、资料中心类型、层级类型、产业 - 产业预测,2024-2031 年 2024 年资料中心维修全球市场报告

2024 年资料中心维修全球市场报告 资料中心託管服务全球市场 2024-2028

资料中心託管服务全球市场 2024-2028 永续资料中心市场:全球展望与预测(2023-2028)

永续资料中心市场:全球展望与预测(2023-2028) 2024 年託管资料中心服务全球市场报告

2024 年託管资料中心服务全球市场报告 浮动资料中心市场 - 全球与区域分析(2023-2033)

浮动资料中心市场 - 全球与区域分析(2023-2033) 2024-2028年资料中心维护与支援服务的全球市场

2024-2028年资料中心维护与支援服务的全球市场

▼