|

市场调查报告书

商品编码

1402982

网路安全 -市场占有率分析、产业趋势/统计、2024-2029 年成长预测Cybersecurity - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

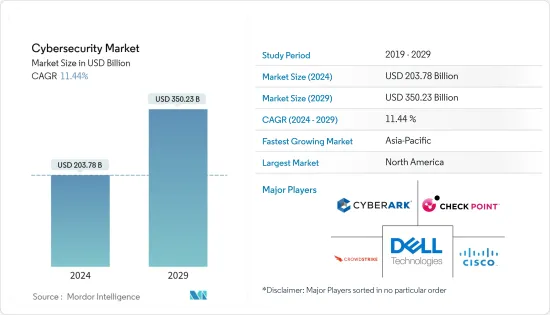

网路安全市场规模预计到 2024 年为 2037.8 亿美元,预计到 2029 年将达到 3502.3 亿美元,在预测期内(2024-2029 年)复合年增长率为 11.44%。

网路安全保护网路、资讯和个人资料免受网路攻击。网路安全领域的 BYOD、人工智慧、物联网和机器学习趋势正在迅速扩张。例如,机器学习在异常检测方面具有优势,有利于网路安全。

主要亮点

- 网路安全产业生态系统由多个网路安全公司区域丛集组成,这些公司为全球市场的动态做出了贡献。在当前的市场情况下,网路安全产业活跃在三个丛集:旧金山湾区(SFBA)、华盛顿特区和以色列。

- 这三个网路安全丛集有两个重要特征。首先,新兴企业和高科技创新文化是这三个生态系统的重要成长动力。 SFBA 和以色列拥有蓬勃发展的新兴企业生态系统以及相关的创投流动。儘管这些公司以产品为中心,但华盛顿州以服务为基础的公司比例更高(华盛顿网路安全公司中只有 11% 只专注于产品)。第二个特点是人力资本与国家安全的连结。

- 勒索软体攻击已经袭击了许多州和地方公共机构。在某些情况下,由于敏感资料大规模外洩和服务中断,整个地方政府被迫宣布进入紧急状态。例如,2021 年 6 月,全球领先的肉类加工公司之一 JBS Foods 遭受网路攻击,导致全球多个地点生产中断,其中包括美国、澳洲和加拿大的生产设施,随后遭到勒索软体攻击。宣布已向威胁行为者REVIL 支付1,100 万美元赎金。

- 网路攻击增加的主要原因之一是各行业缺乏熟练的网路安全人才。与金融机构、政府机构和私人公司/产业应对网路威胁的安全专业人员的需求相比,经验丰富的网路安全专业人员的数量较少,特别是在欧洲、亚太地区、拉丁美洲和中东。

- 随着 COVID-19 疫情的持续爆发,世界各国都在实施预防措施。随着学校关闭和社区被要求留在家里,多个组织已经找到了允许员工在家工作的方法。因此,视讯通讯平台的采用正在增加。

网路安全市场趋势

云端业务将经历显着成长

- 随着企业越来越意识到透过将资料移至云端基础而不是建置和维护新的资料储存来节省成本和资源的重要性,对基于云端的解决方案的需求正在增加。云端平台和生态系统具有多种优势,预计将成为未来几年数位创新爆炸性步伐和规模的跳板。

- 云端基础的解决方案还受益于较低的资本支出需求,使其更具吸引力。透过实施云端基础的服务,企业无需投资硬体组件即可显着降低资本投资需求。云端解决方案还允许企业更准确地预测其应用程式的成本,因此企业无需初期成本来实施该技术。由于硬体和 IT 支援的节省,云端基础的解决方案也变得更加经济实惠。

- 考虑从本地软体迁移到云端基础的解决方案的公司主要检查潜在解决方案的标准合规性以及入侵防御和侦测等关键安全功能。

- 2022 年 10 月,Google Cloud 宣布对其可信任云端生态系进行重大扩展。我们重点介绍与 20 多个合作伙伴的新整合和产品,专注于加强资料主权管理、支援零信任模型、统一身分管理以及提高全球企业的端点安全性。

- 云端技术使组织能够根据业务需求弹性增加或减少频宽。这种方法可以降低成本并为您带来竞争优势。

北美预计将占据主要市场占有率

- 近年来,由于美国组织和个人面临的网路威胁和攻击数量不断增加,网路安全已成为一个日益重要的领域。根据身分盗窃资源中心的数据,2022 年美国发生了 1,802 起资料外洩事件,影响了 4.2214 亿人。

- 网路攻击的日益频繁和复杂性正在推动网路安全解决方案在美国的采用。此外,不断增加的监管要求正在推动许多组织实施和投资网路安全解决方案,因为美国的许多行业都受到 HIPPA、GDPR 和 PCI DSS 等法规的约束。

- 2022 年美国资料外洩和勒索软体方面,教育、公共部门、大学、医疗保健和市政当局是受网路攻击影响的主要部门。美国正在大力投资网路安全研究和开发。美国政府拨出了大量资金。例如,2022年4月,美国能源局(DOE)开发了创新的网路安全技术,以确保能源输送系统的设计、安装、操作和维护能够生存并从网路攻击中快速恢復。宣布在六个专案中投资1200万美元新的研发 (RD&D)计划

- 网路犯罪在加拿大正在迅速蔓延,其影响正在以惊人的速度增长。据魁北克政府数位转型部称,大约 3,992 个省级政府网站,包括与健康、教育和政府相关的网站,可能面临风险。

- 为支持发展强大的国家网路安全生态系统,创新、科学和工业部长于2022年2月宣布,国家网路安全联盟(NCC)将主导网路安全创新网路(CSIN),并宣布已接受高达80美元的资金百万。这笔资金对于培育加拿大强大的国家网路安全生态系统并将加拿大定位为网路安全的全球领导者至关重要。

网路安全产业概述

网路安全市场是一个竞争激烈的市场空间,全球和地区的多个参与企业都在争夺注意力。儘管市场对新参与企业设置了很高的进入壁垒,但一些新参与企业正在引领潮流。主要企业包括 Crowdstrike Holdings Inc.、Check Point Software Technologies Ltd.、Cisco Systems Inc.、Cyberark Software Ltd. 和 Dell Technologies Inc.。

- 2023 年 2 月,Check Point Software Technologies Ltd. 宣布推出协作网路安全解决方案 Check Point Horizon XDR/XPR。透过智慧关联资料并尝试阻止所有媒介的攻击,该产品有效地保护组织免受不断演变的网路威胁,减少威胁影响,并帮助监督和分析师让人们更容易理解和回应事件。

- 2022 年 12 月,CrowdStrike 宣布开发 CrowdStrike Falcon 平台,这是业界最好的主导驱动的外部攻击面管理 (EASM) 解决方案,可实现更好的对手情报和即时网路存取侦测。我们提供CrowdStrike Falcon Surface 是一个独立模组,由最近收购的 Reposify 提供支持,作为平台更新的一部分宣布。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章产业生态系分析

第五章市场动态

- 目前的市场情景和网路安全相关业务的演变

- 市场驱动因素

- 迅速增加的网路安全事件和有关其报告的法规

- M2M/物联网连接的增加要求提高企业网路安全

- 市场挑战

- 网路安全专家短缺

- 高度依赖传统认证方式且准备不足

- 市场机会

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 竞争公司之间的敌对关係

- 替代品的威胁

第六章 全球与区域重大安全漏洞分析

第七章 COVID-19 对网路安全市场的影响

第八章市场区隔

- 依产品类型

- 解决方案

- 应用程式安全

- 云端安全

- 消费者安全软体

- 资料安全

- 身分和存取管理

- 基础设施保护

- 整合风险管理

- 网路安全设备

- 其他解决方案

- 服务

- 专业的

- 管理

- 解决方案

- 按发展

- 本地

- 云

- 按最终用户产业

- BFSI

- 医疗保健

- 航太/国防

- 资讯科技/通讯

- 政府机关

- 零售

- 製造业

- 其他最终用户产业

- 按地区

- 北美洲

- 美国

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 荷兰

- 北欧地区

- 波兰

- 俄罗斯

- 亚太地区

- 中国

- 韩国

- 日本

- 印度

- 新加坡

- 马来西亚

- 澳洲

- 印尼

- 拉丁美洲

- 巴西

- 墨西哥

- 哥伦比亚

- 阿根廷

- 中东/非洲

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 海湾合作委员会国家

- 南非

- 埃及

- 摩洛哥

- 北美洲

第9章供应商市场占有率分析

第10章竞争形势

- 公司简介

- CrowdStrike Holdings Inc.

- Check Point Software Technologies Ltd

- Cisco Systems Inc.

- CyberArk Software Ltd

- Dell Technologies Inc.

- Mandiant Inc.

- Fortinet Inc.

- IBM Corporation

- Imperva Inc.

- Intel Security(Intel Corporation)

- Palo Alto Networks Inc.

- Proofpoint Inc.

- Rapid7 Inc.

- NortonLifelock Inc.

- Trend Micro Inc.

第十一章投资分析

第十二章投资分析市场的未来

The Cybersecurity Market size is estimated at USD 203.78 billion in 2024, and is expected to reach USD 350.23 billion by 2029, growing at a CAGR of 11.44% during the forecast period (2024-2029).

Cybersecurity protects the network, information, and personal data from cyberattacks. The trends of BYOD, AI, IoT, and machine learning in cybersecurity are rapidly growing. For instance, machine learning offers advantages in outlier detection, which benefits cybersecurity.

Key Highlights

- The cybersecurity industry ecosystem comprises several regional clusters of cybersecurity firms contributing to global market dynamics. In the current market scenario, the cybersecurity industry operates in three distinct mega-clusters: the San Francisco Bay Area (SFBA), Metropolitan Washington, DC, and Israel.

- The three cybersecurity mega-clusters share two essential characteristics. The first is that the startup and high-tech innovation culture is a significant growth driver for all three ecosystems. SFBA and Israel have thriving startup ecosystems with a substantial associated flow of risk capital. They are heavily focused on products, while Washington exhibits a higher proportion of service-based firms (in Washington, only 11% of cybersecurity firms are focused solely on products). The second characteristic is the link between human capital and national security.

- Ransomware attacks have ravaged many state and local public sector agencies. In some cases, entire local governments were forced to declare an emergency due to massive leaks of sensitive data and loss of services. For instance, in June 2021, JBS Foods, the world's leading meatpacking enterprise, declared that it had paid a USD 11 million ransom to REvil ransomware threat actors following a cyberattack that forced the company to shut down production at several sites worldwide, including its production facilities in United States, Australia, and Canada.

- One of the major causes of growing cyberattacks is the lack of skilled cybersecurity personnel in each industry. The number of experienced cybersecurity professionals, especially in Europe, Asia-Pacific, Latin America, and the Middle-East, is low compared to the need for security professionals to handle cyber threats for financial institutes, government organizations, and private sector/industrial businesses.

- Due to the ongoing COVID-19 pandemic, countries worldwide have implemented preventive measures. With schools being closed and communities being asked to stay at home, multiple organizations have found a way to enable their employees to work from their homes. This has, thus, resulted in a rise in the adoption of video communication platforms.

Cybersecurity Market Trends

The Cloud Segment to Witness Significant Growth

- The increasing realization among enterprises about the importance of saving money and resources by moving their data to the cloud instead of building and maintaining new data storage drives the demand for cloud-based solutions. Owing to multiple benefits, cloud platforms and ecosystems are anticipated to serve as a launchpad for the explosion in the pace and scale of digital innovation over the next few years.

- Cloud-based solutions also benefit from lower capital expenditure requirements, making them much more compelling. Deploying cloud-based services can significantly reduce the Capex requirements as companies need not invest in hardware components. Cloud solutions also enable better prediction of the cost of an application, and companies don't incur much upfront cost to incorporate the technology. Also, the hardware and IT support savings make cloud-based solutions much more affordable.

- Companies that are considering moving from on-premise software to cloud-based solutions are primarily checking the potential solutions for their key security features, including standards compliance and intrusion prevention and detection.

- In October 2022, Google Cloud declared a significant expansion of its trusted cloud ecosystem. It highlighted new integrations and offerings with more than twenty partners, focusing on enabling greater data sovereignty controls, supporting Zero Trust models, unifying identity management, and improving endpoint security for global businesses.

- Cloud technology provides organizations with the flexibility they need to increase and decrease their bandwidth with the needs of their operations. This approach can cut costs and give businesses an edge over the competition.

North America is Expected to Hold Major Market Share

- Cybersecurity has become an increasingly important area of focus in the United States in recent years due to the growing number of cyber threats and attacks that organizations and individuals face. According to the Identity Theft Resource Center, the number of data compromises and individuals impacted in the United States in 2022 was 1,802 and 422.14 million, respectively.

- The increasing frequency and sophistication of cyber-attacks are driving the adoption of cybersecurity solutions in the United States. Moreover, the growing regulatory requirement leads many organizations to adopt and invest in cybersecurity solutions, as many industries in the United States are subject to regulations such as HIPPA, GDPR, and PCI DSS.

- Education, the public sector, universities, healthcare, and municipalities were among the major sectors affected by cyber-attacks in terms of data breaches and ransomware in the United States in 2022. There has been significant investment in cybersecurity research and development in the United States. The United States government is allocating a large number of funds. For instance, in April 2022, the United States Department of Energy (DOE) announced that it would invest USD 12 million in six new research, development, and demonstration (RD&D) projects to develop innovative cybersecurity technology to ensure that energy delivery systems are designed, installed, operated, and maintained to survive and recover quickly from cyberattacks.

- In Canada, cybercrime is rapidly gaining traction, and the impact is increasing alarmingly. According to the Ministry for Government Digital Transformation, Quebec, around 3,992 provincial government websites, including those related to health, education, and public administration, can be at risk.

- In order to support the development of a strong national cyber security ecosystem, the Minister of Innovation, Science and Industry announced that the National Cybersecurity Consortium (NCC) received up to USD 80 million to lead the Cyber Security Innovation Network (CSIN) in February 2022. This funding was crucial to foster a strong national cyber security ecosystem in Canada and position the country as a global leader in cyber security.

Cybersecurity Industry Overview

The cybersecurity market comprises several global and regional players vying for attention in a fairly contested market space. Although the market poses high barriers to entry for new players, several new entrants have been able to gain traction. Crowdstrike Holdings Inc., Check Point Software Technologies Ltd, Cisco Systems Inc., Cyberark Software Ltd, and Dell Technologies Inc. are major players in the market.

- In February 2023, Check Point Software Technologies Ltd announced the introduction of Check Point Horizon XDR/XPR, a cooperative cybersecurity solution. It effectively protects organizations against developing cyber threats by smartly correlating data and trying to thwart attacks across all vectors, reducing the impact of threats and making it simple for supervisors and analysts to comprehend and respond to incidents.

- In December 2022, CrowdStrike announced the development of the CrowdStrike Falcon platform to give the sector's finest adversary-driven external attack surface management (EASM) solution for better adversary intelligence and real-time internet access detection. CrowdStrike Falcon Surface, a standalone module featuring abilities from the recent acquisition of Reposify, was announced as part of the platform update.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 INDUSTRY ECOSYSTEM ANALYSIS

5 MARKET DYNAMICS

- 5.1 Current Market Scenario and Evolution of Cybersecurity Related Practices

- 5.2 Market Drivers

- 5.2.1 Rapidly Increasing Cybersecurity Incidents and Regulations Regarding their Reporting

- 5.2.2 Growing M2M/IoT Connections Demanding Strengthened Cybersecurity in Enterprises

- 5.3 Market Challenges

- 5.3.1 Lack of Cybersecurity Professionals

- 5.3.2 High Reliance on Traditional Authentication Methods and Low Preparedness

- 5.4 Market Opportunities

- 5.5 Industry Attractiveness - Porter's Five Forces Analysis

- 5.5.1 Bargaining Power of Suppliers

- 5.5.2 Bargaining Power of Consumers

- 5.5.3 Threat of New Entrants

- 5.5.4 Competitive Rivalry within the Industry

- 5.5.5 Threat of Substitutes

6 ANALYSIS OF MAJOR SECURITY BREACHES AT A GLOBAL AND REGIONAL LEVEL

7 IMPACT OF COVID-19 ON THE CYBERSECURITY MARKET

8 MARKET SEGMENTATION

- 8.1 By Product Type

- 8.1.1 Solutions

- 8.1.1.1 Application Security

- 8.1.1.2 Cloud Security

- 8.1.1.3 Consumer Security Software

- 8.1.1.4 Data Security

- 8.1.1.5 Identity and Access Management

- 8.1.1.6 Infrastructure Protection

- 8.1.1.7 Integrated Risk Management

- 8.1.1.8 Network Security Equipment

- 8.1.1.9 Other Solutions

- 8.1.2 Services

- 8.1.2.1 Professional

- 8.1.2.2 Managed

- 8.1.1 Solutions

- 8.2 By Deployment

- 8.2.1 On-premise

- 8.2.2 Cloud

- 8.3 By End-user Industry

- 8.3.1 BFSI

- 8.3.2 Healthcare

- 8.3.3 Aerospace and Defense

- 8.3.4 IT and Telecommunication

- 8.3.5 Government

- 8.3.6 Retail

- 8.3.7 Manufacturing

- 8.3.8 Other End-user Industries

- 8.4 By Geography

- 8.4.1 North America

- 8.4.1.1 United States

- 8.4.1.2 Canada

- 8.4.2 Europe

- 8.4.2.1 United Kingdom

- 8.4.2.2 Germany

- 8.4.2.3 France

- 8.4.2.4 Italy

- 8.4.2.5 Spain

- 8.4.2.6 The Netherlands

- 8.4.2.7 Nordic Region

- 8.4.2.8 Poland

- 8.4.2.9 Russia

- 8.4.3 Asia-Pacific

- 8.4.3.1 China

- 8.4.3.2 South Korea

- 8.4.3.3 Japan

- 8.4.3.4 India

- 8.4.3.5 Singapore

- 8.4.3.6 Malaysia

- 8.4.3.7 Australia

- 8.4.3.8 Indonesia

- 8.4.4 Latin America**

- 8.4.4.1 Brazil

- 8.4.4.2 Mexico

- 8.4.4.3 Colombia

- 8.4.4.4 Argentina

- 8.4.5 Middle East and Africa**

- 8.4.5.1 Saudi Arabia

- 8.4.5.2 United Arab Emirates

- 8.4.5.3 GCC***

- 8.4.5.4 South Africa

- 8.4.5.5 Egypt

- 8.4.5.6 Morocco

- 8.4.1 North America

9 VENDOR MARKET SHARE ANALYSIS

10 COMPETITIVE LANDSCAPE

- 10.1 Company Profiles*

- 10.1.1 CrowdStrike Holdings Inc.

- 10.1.2 Check Point Software Technologies Ltd

- 10.1.3 Cisco Systems Inc.

- 10.1.4 CyberArk Software Ltd

- 10.1.5 Dell Technologies Inc.

- 10.1.6 Mandiant Inc.

- 10.1.7 Fortinet Inc.

- 10.1.8 IBM Corporation

- 10.1.9 Imperva Inc.

- 10.1.10 Intel Security (Intel Corporation)

- 10.1.11 Palo Alto Networks Inc.

- 10.1.12 Proofpoint Inc.

- 10.1.13 Rapid7 Inc.

- 10.1.14 NortonLifelock Inc.

- 10.1.15 Trend Micro Inc.

11 INVESTMENT ANALYSIS

12 FUTURE OF THE MARKET

2024 年电信网路安全解决方案全球市场报告

2024 年电信网路安全解决方案全球市场报告 2024 年资讯科技 (IT) 和通讯安全全球市场报告

2024 年资讯科技 (IT) 和通讯安全全球市场报告 2024 年银行网路安全全球市场报告

2024 年银行网路安全全球市场报告 攻击面管理市场:依产品、部署型态、产业、组织规模划分 - 2024-2030 年全球预测

攻击面管理市场:依产品、部署型态、产业、组织规模划分 - 2024-2030 年全球预测 暴露控制市场:按产品、应用、部署和最终用途分类 - 2024-2030 年全球预测

暴露控制市场:按产品、应用、部署和最终用途分类 - 2024-2030 年全球预测 全球攻击面管理 (ASM) 市场:按产品、部署方法、组织规模、产业、地区划分 - 预测(~2029 年)

全球攻击面管理 (ASM) 市场:按产品、部署方法、组织规模、产业、地区划分 - 预测(~2029 年) 网路安全培训的全球市场规模、份额和趋势分析:按认证、目标受众、培训类型、交付方法、内容、行业和地区分類的展望和预测(2024-2031)

网路安全培训的全球市场规模、份额和趋势分析:按认证、目标受众、培训类型、交付方法、内容、行业和地区分類的展望和预测(2024-2031) 全球暴露管理市场规模、份额和趋势分析报告:按组件、按部署模式、按应用、按最终用途、按地区、展望和预测,2023-2030 年

全球暴露管理市场规模、份额和趋势分析报告:按组件、按部署模式、按应用、按最终用途、按地区、展望和预测,2023-2030 年 全球暴露管理市场:按元件(解决方案/服务)、部署模式(云端、本地)、应用程式(漏洞管理、威胁情报、攻击面管理)、最终用户产业、地区 - 预测(截至 2029 年)

全球暴露管理市场:按元件(解决方案/服务)、部署模式(云端、本地)、应用程式(漏洞管理、威胁情报、攻击面管理)、最终用户产业、地区 - 预测(截至 2029 年) 全球消费者网路安全软体市场规模、份额和趋势分析报告:按部署、按设备类型、按产品、按地区、展望和预测,2023-2030 年

全球消费者网路安全软体市场规模、份额和趋势分析报告:按部署、按设备类型、按产品、按地区、展望和预测,2023-2030 年