|

市场调查报告书

商品编码

1402992

可程式逻辑控制器 (PLC):市场占有率分析、产业趋势/统计、成长预测,2024-2029 年Programmable Logic Controller (PLC) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

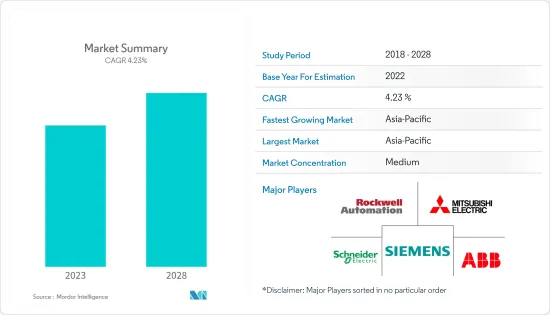

可程式逻辑控制器(PLC)市场规模预计到2024年为128.3亿美元,预计到2029年将达到150.7亿美元,复合年增长率预计为4.23%。

主要亮点

- PLC 是管理自动化机械的主要计算系统。该系统还有助于检测错误和缺陷并向技术人员发出警报。由于尺寸紧凑,PLC 系统比继电器和交换器盒等传统系统更受欢迎。 PLC 的另一个优点是其多功能性(由于其可程式特性,可根据应用进行多种操作)。

- 机器停机时间是影响工业製造效率的关键因素。停机时间占营运期间製造损失的 5-20%。实施 PLC 系统可以识别和纠正错误,并在无需人工干预的情况下产生快速反应,从而提高工业流程的效率。

- 工业自动化是推动PLC市场成长的关键因素之一。自动化是指透过提高效率和优化资源利用来减少流程中人为干预的自动化处理系统。业界现在正在发现利用自动化系统可以实现的可靠性和长期利益。特别是输送系统和包装系统可以使用 PLC 系统实现自动化。工业领域自动化渗透率的不断提高预计也将有利于所研究市场的成长。

- 此外,PLC 还可以帮助控制製造流程,例如组装、机器人设备或任何需要可靠控制、轻鬆编程和操作故障诊断的活动。 PLC 不断发展,仍然是各种工业自动化应用的最佳选择。可扩充性、大内存容量、小型化、高速(Gigabit)乙太网路和内建无线是新兴可程式逻辑控制器(PLC)的特征。

- 现代消费者对个人化产品的需求正在推动产业从大规模生产模式转向大规模客製化。 PLC 在流程不变的行业中被广泛接受。然而,随着最终用户对产品客製化需求的增加,製造过程变得更加精密和复杂,需要频繁调整,因此,最终用户正在使用基于PC或云端基础的控制器而不是PLC。投资更灵活的系统,这对研究市场的成长构成了挑战。

- 区域经济状况、地缘政治问题等宏观经济因素在产业部门产业部门的成长中发挥重要作用,因为它们影响该部门的投资和扩张能力。例如,最近的俄罗斯和乌克兰战争对一些国家的经济和地缘政治产生了影响,从而为工业部门的成长创造了不利条件。随着 PLC 在工业中的广泛应用,这种趋势阻碍了市场的成长。

PLC市场趋势

汽车预计将成为成长最快的最终用户产业

- PLC 在阶段的应用是为了满足汽车产业不断增长的需求。最初,它被用作汽车製造中的继电器替代装置。 PLC 使製造商能够更聪明、更快速地工作,随着自动化流程减少瓶颈的发生,从而降低工业中的营运和生产时间成本。

- 各汽车公司的製造工厂正在进行製造创新,将新技术融入製造流程,以提高生产力和效率。例如,ATS Applied Tech Systems Ltd. 使用 InTrack、InTouch 和 GE-Fanuc PLC 开发了安全气囊追踪和追踪系统,以实现完整的防错和可追溯性。透过此系统设置,如果在生产过程中检测到缺陷,则可以在生产后长达 10 年内追踪安全气囊的来源和製造机械的状况。

- 已经证实,自动化显着提高了汽车组装流程的效率。结果,全球生产的汽车数量不断增加,但成本却同时下降。多年来,汽车行业一直在各种製造工艺的组装上使用机器人。汽车製造商目前正在探索在更多流程中使用机器人。对于这些生产线来说,机器人更加灵活、有效率、准确、可靠。这项技术也使汽车产业仍然是工业机器人最重要的采用者之一,并持有自动化程度最高的供应链之一。

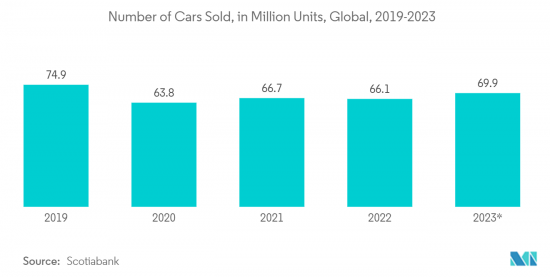

- 世界各地对汽车的需求正在增加。据丰业银行称,到 2023 年,全球汽车销量预计将达到 6,990 万辆,并在未来几年进一步成长。

- 此外,车辆电动、联网汽车和自动驾驶汽车等不断增长的趋势也对所研究市场的成长做出了重大贡献,因为这些车辆通常使用大量电控系统,其中 PLC 发挥重要作用。一种影响。因此,此类上升趋势预计将在预测期内推动研究市场机会。

亚太地区预计成长更快

- 在过去的几十年里,亚太地区的汽车、工业和製造业等各行业都取得了显着的成长,预计在预测期内这种成长轨迹将持续下去,为所研究的市场提供了成长机会。例如,製造业是中国经济的重要组成部分,随着工业4.0围绕全球製造业的扩张,物联网的发展正在经历快速转型。这一重大转变使该国在PLC市场上处于领先地位。

- 印度正受到机器人流程自动化 (RPA) 和人工智慧 (AI) 技术的日益使用的推动。根据全球 RPA 论坛 Automation Anywhere 的数据,印度目前是仅次于美国的第二大收益来源。全球产能中心、服务供应商和印度公司是该公司在印度最重要的客户。

- 印度的工业自动化产业正在透过製造业的数位和实体方面的整合进行转型,以提供最佳性能。对精益生产和缩短时间的关注正在加速市场成长。

- 日本在机器人製造方面拥有最大的市场占有率,并引进了工业机器人组装机器人的方式。根据2022年3月IFR报告,日本是全球第一大工业机器人製造国,供应全球机器人供应量的45%。此类案例预计将推动自动化需求并带动 PLC 在该地区的发展。

- 亚太地区的其他国家包括韩国、新加坡、印尼、澳洲和泰国。泰国和马来西亚凭藉着良好的原料可得性和低廉的土地价格,逐渐取代中国成为主要工业中心。这一趋势预计将有利于亚太地区 PLC 市场的成长。

PLC产业概况

可程式逻辑控制器 (PLC) 市场较为分散,主要企业包括 ABB Ltd、三菱电机、Schneider Electric、罗克韦尔自动化和西门子股份公司。市场上的竞争正在采取联盟、併购和收购等策略来增强其产品阵容并获得永续的竞争优势。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买方议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争公司之间的敌对关係

- 宏观趋势对市场的影响

第五章市场动态

- 市场驱动因素

- 自动化系统的采用率增加

- PLC 程式设计的易用性和熟悉度支援成长

- 市场抑制因素

- 离散製造业产品客製化需求及从批量加工阶段转向连续加工

- 更采用具有增强安全性和先进控制功能的分散式控制系统 (DCS)

第六章市场区隔

- 按类型

- 硬体和软体

- 大型PLC

- 奈米PLC

- 小型PLC

- 中型PLC

- 其他的

- 按服务

- 硬体和软体

- 按最终用户产业

- 食品、烟草、饮料

- 车

- 化学/石化

- 能源/公用事业

- 纸浆/造纸製造

- 油和气

- 水处理/污水处理

- 製药

- 其他的

- 按地区

- 北美洲

- 美国

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 其他欧洲国家

- 亚太地区

- 中国

- 印度

- 日本

- 其他亚太地区

- 拉丁美洲

- 中东/非洲

- 北美洲

第七章竞争形势

- 公司简介

- ABB Ltd

- Mitsubishi Electric Corporation

- Schneider Electric SE

- Rockwell Automation Inc.

- Siemens AG

- Honeywell International Inc.

- Omron Corporation

- Panasonic Corporation

- Robert Bosch GmbH

- Emerson Electric Co.

- Hitachi Ltd

- Toshiba International Corporation

第八章投资分析

第9章市场的未来

The Programmable Logic Controller Market size is estimated at USD 12.83 billion in 2024, and is expected to reach USD 15.07 billion by 2029, growing at a CAGR of 4.23% during the forecast period (2024-2029).

Key Highlights

- PLC is the major computing system that manages automated machines. The system also assists in detecting errors or flaws and cautions the technician. Due to their packed sizes, PLC systems are desired over traditional ones, like relays and switch boxes. Another benefit of PLCs is their multi-functionality (due to their programmable nature that can be utilized for multiple operations relying on the application).

- Machine downtime is a significant factor affecting an industry's manufacturing efficiency. Downtime is responsible for 5-20% of the manufacturing losses during operation. Installing PLC systems allows the identification and rectification of errors and can create quick reactions even without human intervention, thereby bringing efficiency into industrial processes.

- Industry automation is one of the significant factors driving the growth of the PLC market. Automation can be described as automatic processing systems to improve the efficiency and reduce human intervention in the process via the optimal usage of resources. The industries have now discovered the reliability and long-term profits that can be accomplished by utilizing automated systems. Conveyor systems & packaging systems, among others, can be automated using PLC systems. The growing penetration of automation in the industrial sector isn also anticipated to favor the studied market's growth.

- Furtheremore, PLCs also help control manufacturing processes, like assembly lines, robotic devices, or any activity requiring high-reliability control and easy programming & operation fault diagnosis. PLCs are growing and remain the best choice for different industrial automation applications. Scalability, greater memory, smaller sizes, high-speed (gigabit) Ethernet, & built-in wireless are among the emerging programmable logic controller capabilities.

- Due to modern consumers' need for personalized products, industries have driven themselves from a mass production model into mass customization. PLCs are broadly embraced in industries whose processes do not change. However, the growing end-user need for customization of products has made the manufacturing processes more refined and complicated, with the need for frequent adjustments, consequently fueling the end-users to adopt and invest in more flexible systems, like PC-based and cloud-based controllers, rather than PLCs which is challenging the studied market's growth.

- Macroeconomic factors such as the genera economic condition of a region, geopolitical issues, etc. plays a crucial role in the industrial sector's growth as these factors influence the investment and expansion capabilities of the industrial sector. For instance, the recent Russia Ukraine war is impacting several countries on both economic as well as geopolitical stability verticals, which in turn is creating an unfavorable condition for the growth of the industrial sector. As PLCs are widely used in industries, such trends hamper the studied market's growth.

PLC Market Trends

Automotive is Expected to Be the Fastest-growing End-user Industry

- PLCs are used at the manufacturing stage to handle the growing demands of the automotive industry. Initially, these were employed as relay replacement equipment in automotive manufacturing. PLCs let manufacturers work smarter & faster, and as automated processes reduce the occurrence of bottlenecks, this reduces expenses in operation and production time in the industry.

- Manufacturing plants of various automotive companies have been experiencing manufacturing changes to integrate new technology into the manufacturing stream to improve productivity and efficiency. For instance, ATS Applied Tech Systems Ltd developed a tracking and tracing system for airbags using InTrack, InTouch, and GE-Fanuc PLCs to gain full error-proofing and traceability. Using the system set-up, it is feasible to trace the airbag's origin and the production machines' status during manufacturing, in case a fault is detected, even up to 10 years after production.

- It has been identified that automation has significantly increased the efficiency of auto assembly process. As a result, it is showing a growing pattern in the number of cars being produced globally while simultaneously cutting costs, paving the way for the growth of smart factories' implementation in this sector. For many years, the automotive industry has used robots in the assembly lines for various manufacturing processes. Nowadays, automakers are exploring the use of robotics in more procedures. Robots are more flexible, efficient, accurate, and dependable for these product lines. This technology also enables the automotive industry to remain one of the most significant adopters of industrial and possess one of the most automated supply chains.

- There has been an increasing demand for automobiles across the world. According to Scotiabank, worldwide automobile sales will reach 69.9 million units by 2023 and are anticipated to be more in forthcoming years.

- Furthermore, the growing proliferation of trends such as electrification of vehicles, connected and autonomous cars, etc. are also anticipated to influence the studied market's growth significantly as these automobiles generally use a larger number of electronic and control units wherein PLCs play a crucial role. Hence, the growing such trends are anticipated to drive opportunities in the studied market during the forecast period.

Asia-Pacific is Expected to Witness a Faster Growth

- In the last few decades, the Asia Pacific region has witnessed remarkable growth across various sectors, including automotive, industrial, manufacturing, etc., and is anticipated to continue its upward growth trajectory during the forecast period, creating opportunities in the studied market. For instance, the manufacturing sector constitutes a substantial part of China's economy, which is experiencing a fast transformation with the current growth in IoT due to the expansion of Industry 4.0 around the manufacturing industries worldwide. This large-scale conversion has put the country in one of the top positions in the PLC market.

- India is fueled by the increasing usage of robotic process automation (RPA) & artificial intelligence (AI)-based technologies. According to the global RPA forum Automation Anywhere, India is presently its second-biggest revenue generator behind the United States. Global capacity centers, service providers, and Indian enterprises are its most prominent customers in India.

- India's industrial automation sector has been transformed by the integration of digital and physical aspects of manufacturing to provide optimum performance. The emphasis on acquiring zero waste production and a faster time to reach the market has augmented the market's growth.

- Japan has the most significant market share in the robot manufacturing industry and installed methods where industrial robots are used to assemble robots. According to a report by IFR in March 2022, Japan is the world's number on industrial robot manufacturer, delivering 45% of the global supply for robots worldwide. Such instances are anticipated to drive the demand for automation, resulting in the developing of PLCs in the region.

- The other countries from the Asia-Pacific region include countries like South Korea, Singapore, Indonesia, Australia, and Thailand. With the excellent availability of raw materials and cheaper land rates, Thailand and Malaysia are gradually emerging as major industrial hubs, an alternative to China. This trend is anticipated to favor the growth of the PLC market in Asia-Pacific.

PLC Industry Overview

The programmable logic controller (PLC) Market is moderately fragmented, with major players such as ABB Ltd, Mitsubishi Electric Corporation, Schneider Electric SE, Rockwell Automation Inc, and Siemens AG. Players in the market are adopting strategies like partnerships, mergers, and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

- July 2023 - Siemens launched a complete virtual programmable logic controller. The Simatic S7-1500V expands the company's existing Simatic portfolio to special market requirements, including virtual hosting of PLC computing. According to the company, Simatic S7-1500V is part of Industrial Operations X, under which the company is consistently focusing on integrating IT and software capabilities into the automation landscape.

- November 2022 - Arduino announced its "first micro PLC," the Opta, a powerful gadget devised with the Industrial Internet of Things (IIoT) at the fore. In addition, it is designed in partnership with Finder. It uses an STMicro STM32H747XI dual-core microcontroller, which contains a single high-performance Arm Cortex-M7 core operating at up to 480MHz & a lower-power Cortex-M4 core driving at up to 240MHz alongside a disseminated floating-point unit (FPU), Chrom-ART accelerator, a hardware JPEG accelerator, 2MB flash, a total of 1,056kB of RAM plus 1,024-byte and 4kB backup static RAM (SRAM).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Impact of Macro Trends on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increased Adoption of Automation Systems

- 5.1.2 Ease of Use and Familiarity with PLC Programming to Sustain Growth

- 5.2 Market Restraints

- 5.2.1 Demand for Customization of Products and Gradual Shift from Batch to Continuous Processing in the Discrete Industries

- 5.2.2 Increase in Adoption of Distributed Control Systems (DCS), with Enhanced Safety and Advanced Control Capabilities

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Hardware and Software

- 6.1.1.1 Large PLC

- 6.1.1.2 Nano PLC

- 6.1.1.3 Small PLC

- 6.1.1.4 Medium PLC

- 6.1.1.5 Other Types

- 6.1.2 Services

- 6.1.1 Hardware and Software

- 6.2 By End-user Industry

- 6.2.1 Food, Tobacco, and Beverage

- 6.2.2 Automotive

- 6.2.3 Chemical and Petrochemical

- 6.2.4 Energy and Utilities

- 6.2.5 Pulp and Paper

- 6.2.6 Oil and Gas

- 6.2.7 Water and Wastewater Treatment

- 6.2.8 Pharmaceutical

- 6.2.9 Other End-user Industries

- 6.3 By Geography

- 6.3.1 North America

- 6.3.1.1 United States

- 6.3.1.2 Canada

- 6.3.2 Europe

- 6.3.2.1 United Kingdom

- 6.3.2.2 Germany

- 6.3.2.3 France

- 6.3.2.4 Rest of Europe

- 6.3.3 Asia-Pacific

- 6.3.3.1 China

- 6.3.3.2 India

- 6.3.3.3 Japan

- 6.3.3.4 Rest of Asia-Pacific

- 6.3.4 Latin America

- 6.3.5 Middle East and Africa

- 6.3.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 ABB Ltd

- 7.1.2 Mitsubishi Electric Corporation

- 7.1.3 Schneider Electric SE

- 7.1.4 Rockwell Automation Inc.

- 7.1.5 Siemens AG

- 7.1.6 Honeywell International Inc.

- 7.1.7 Omron Corporation

- 7.1.8 Panasonic Corporation

- 7.1.9 Robert Bosch GmbH

- 7.1.10 Emerson Electric Co.

- 7.1.11 Hitachi Ltd

- 7.1.12 Toshiba International Corporation

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

可程式逻辑控制器市场:按类型、尺寸、架构、型态、电源、最终用户产业划分 - 2024-2030 年全球预测

可程式逻辑控制器市场:按类型、尺寸、架构、型态、电源、最终用户产业划分 - 2024-2030 年全球预测 2024-2032 年按类型、最终用途产业和地区分類的可程式逻辑控制器市场报告

2024-2032 年按类型、最终用途产业和地区分類的可程式逻辑控制器市场报告 2024年微纳PLC全球市场报告

2024年微纳PLC全球市场报告 可程式逻辑控制器 (PLC) 市场,按类型、按应用、国家和地区 - 2023-2030 年行业分析、市场规模、市场份额和预测

可程式逻辑控制器 (PLC) 市场,按类型、按应用、国家和地区 - 2023-2030 年行业分析、市场规模、市场份额和预测 可程式逻辑控制器 (PLC) 市场规模-按最终用途(航太与国防、汽车、化学、能源与公用事业、食品与饮料、医疗保健、製造、采矿与金属、石油与天然气、运输)、类型、组件和预测, 2024-2032

可程式逻辑控制器 (PLC) 市场规模-按最终用途(航太与国防、汽车、化学、能源与公用事业、食品与饮料、医疗保健、製造、采矿与金属、石油与天然气、运输)、类型、组件和预测, 2024-2032 可程式逻辑控制器(PLC)全球市场2024-2028

可程式逻辑控制器(PLC)全球市场2024-2028 可编程逻辑控制器(PLC)的全球市场:实际成果与预测(2018年~2029年)

可编程逻辑控制器(PLC)的全球市场:实际成果与预测(2018年~2029年) 可编程逻辑控制器 (PLC) 的全球市场

可编程逻辑控制器 (PLC) 的全球市场 微·奈米PLC的全球市场

微·奈米PLC的全球市场 2023-2027 年 PLC 软件全球市场

2023-2027 年 PLC 软件全球市场