|

市场调查报告书

商品编码

1402995

农用轮胎:市场占有率分析、产业趋势/统计、成长预测,2024-2029Agricultural Tires - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

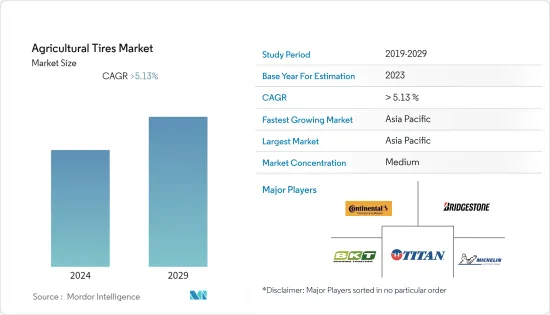

目前农用轮胎市场规模为65.7亿美元。

预计未来五年将达88.8亿美元,预测期内复合年增长率将超过5.13%。

虽然整体市场情况乐观,但需求高度依赖经济中断,这肯定会影响农民的收入和农业机械的购买。然而,由于COVID-19大流行严重影响了包括农用轮胎市场在内的汽车产业,2020年农业设备销售出现下滑。

对高效、多产农业机械最终产品的需求不断增长正在推动市场,特别是在已开发国家。德国是继中国之后的第二大农用轮胎出口国和製造商。人口成长和农业机械技术进步对农产品的需求是推动市场成长的主要因素。

农用轮胎售后市场高度分散,为该行业的OEM带来了很高的风险。随着农业机械设计的变化并渗透到更新、更未知的领域,可能需要采用更新、更强橡胶化合物的轮胎。浮动轮胎、林业轮胎、拖车轮胎和钢製柔性壁复合橡胶轮胎是农用轮胎市场的趋势。

农用轮胎市场趋势

拖拉机需求的增加推动了市场

大多数新兴国家的农村人口向都市区迁移、人事费用上升以及技术纯熟劳工短缺正在推动拖拉机销售。农业劳动力稀缺及其成本上升是农业机械化程度不断提高的主要原因之一。

对工作效率的日益增长的需求和不断上升的劳动力成本预计将推动对农用拖拉机的需求。在预测期内,农用拖拉机市场可能会受到劳动力有限的推动。

考虑到简单的供需经济学和劳动力从都市区的流动,农业劳动力的成本与一个国家从事农业的总人口的比例直接相关。因此,为了减少对人力的依赖,农民正在投资农业机械,以减少耕作所需的时间和精力。

各国政府推出了新的地产地销策略,以弥合供应链差距并解决农业部门的劳动力短缺问题。为了支持小农,政府实施了许多全面的税收改革。例如

- 印度政府实施了“农业宏观管理计画”,对35 PTO马力以下的拖拉机提供25%的补贴。同时,加拿大政府推出了《加拿大农业贷款法案》,为农民提供高达50万美元的贷款,用于购买土地和拖拉机。它也可用于建筑物维修。

农民正在增加对农业设备的投资,以更少的劳动力实现最佳性能。虽然此类设备需要较高的初始投资,但有助于提高作物的整体品质和数量。许多农民现在正在缩小农场规模并出租部分农场,以抵消不断上涨的人事费用。

随着越来越多的农民减少对劳动力的依赖,拖拉机销售预计在未来几年将健康成长,从而推动预测期内对拖拉机轮胎的需求。

儘管农业收入下降,美国的需求仍在增加

美国经济的整体实力,包括收入水准、购买力、基础建设发展等因素,对农用轮胎的需求起到了推动作用。强劲的经济支持农业部门的投资,导致对设备和轮胎的需求增加。 2001年,农业总收入为2,499亿美元,大幅成长,到年终超过6,041亿美元。

该国农业部门广泛且高度发达,拥有大量农场和大规模农业经营。如此大规模的耕作需要大量的农用轮胎来支撑各种设备和机械。此外,到 2022 年,美国将有 200 万个农场,低于 2007 年的 220 万个。同样,农业用地面积也将持续减少,从2002年的9.15亿英亩减少到2022年的8.93亿英亩。平均农地面积将从 1970 年代的 440 英亩小幅增加到 2022 年的 446 英亩。

儘管农民数量有所下降,但由于美国仍然位居榜首。大型且技术先进的农场受益于规模经济和专业化,使它们能够提高生产力和效率。再加上农业实践、设备和基础设施的进步,帮助美国维持了主要农业生产国的地位。

此外,美国是重要的农产品出口国,向国内和国际市场供应食品和家庭用品。这种出口导向农业依赖高效的耕作方法和农业机械,进一步推动了对农用轮胎的需求。

过去25年,美国农产品出口稳定成长,从1997年的628亿美元成长到2022年的1,960亿美元。由于全球人口成长、收入增加和饮食多样化,包括乳製品、肉类、水果和蔬菜等高价值产品在内的消费品出口大幅增加。

这些因素将在未来几年继续推动美国农用轮胎的需求。

农用轮胎行业概况

农用轮胎市场集中度中等。农用轮胎市场的主要企业包括普利司通公司(凡士通)、泰坦国际公司(固特异轮胎)、BKT、Continental Reifen Deutschland GmbH、米其林等。

其他产业公司包括 Carlisle Companies Incorp.、Trelleborg Wheel Systems 和 McCreary Tire &Rubber Co.。为了保持市场主导地位,主要企业正在专注于产品升级和定制,扩大整体产品线,并在农用轮胎市场提供强大的产品。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 调查先决条件

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场动态

- 市场驱动因素

- 世界人口成长

- 其他的

- 市场抑制因素

- 产品价格波动

- 其他的

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买家/消费者的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争公司之间敌对关係的强度

第五章市场区隔

- 销售管道类型

- OEM

- 更换/售后

- 应用程式类型

- 联结机

- 联合收割机

- 散布

- 预告片

- 装载机

- 其他的

- 轮胎类型

- 斜交轮胎

- 子午线轮胎

- 地区

- 北美洲

- 美国

- 加拿大

- 北美其他地区

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 其他欧洲国家

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 其他亚太地区

- 其他地区

- 南美洲

- 中东/非洲

- 北美洲

第六章竞争形势

- 供应商市场占有率

- 公司简介

- Bridgestone Corp.

- Continental AG

- Balakrishna Industries Limited

- Titan International Inc.

- Trelleborg AB

- Michelin

- Nokian Tyres PLC

- Pirelli & C SpA(Prometeon Tyre Group)

- Alliance Tire Group

- Apollo Tyres

- Magna Tyres

第七章 市场机会及未来趋势

- 胎压监测系统集成

- 向环保、节能农用轮胎的动态转变

The agricultural tires market is valued at USD 6.57 billion in the current year. It is expected to reach a value of USD 8.88 billion over the next five years, registering a CAGR above 5.13% during the forecast period.

While the overall scenario of the market is positive, the demand is hugely dependent on the economic turmoil that invariably affects the farmers' income and purchase of farm machinery. However, a downturn in farming equipment sales was witnessed in 2020, as the COVID-19 pandemic severely impacted the automotive industries, including the agriculture tires market.

The rise in demand for efficient and productive agricultural machinery end-products, especially among developed nations, drives the agriculture tires market. After China, Germany is the second-largest exporter and manufacturer of agricultural tires. The demand for farm products from expanding populations and technological advancements in agricultural equipment are the primary factors propelling the market growth.

The agriculture tires aftermarket is highly fragmented and poses a high risk to OEMs in this field. Changing agriculture machinery design and increasing penetration into newer unknown terrain may require tires with newer and stronger rubber compounds. Floatation tires, forestry tires, trailer tires, and compound rubber tires with steel flex walls are the trending tires in the agricultural tires market.

Agricultural Tires Market Trends

The Increasing Demand for Tractors is Driving the Market

The migration of people from rural to urban regions, rising labor costs, and skilled labor lack in most developing countries are fueling tractor sales. Shortage of farm labor and its rising cost are among the main reasons for the increasing mechanization of the farming industry.

The increasing need for operational efficiency and the rise in labor costs are expected to boost the demand for agricultural tractors. Over the forecast period, the market for agricultural tractors will be driven by limited labor availability.

Considering simple demand-supply economics and the transfer of labor from urban to rural areas, the cost of farm labor includes a direct link to the percentage of a country's entire population employed in agriculture. Hence, to reduce dependency on human labor, farm owners are investing in farm equipment, thereby reducing the time and effort taken for farming.

Various governments introduced new strategies to produce and consume locally to bridge the supply chain gaps and address the labor shortage in the agriculture sector. To assist smaller players, the governments implemented a few comprehensive tax reforms. For example:

- The Indian government implemented the 'Macro-Management Scheme of Agriculture,' which provides a 25% subsidy on tractors up to 35 PTO HP. At the same time, the Canadian government introduced the 'Canadian Agricultural Loans Act,' which offers farmers a loan of up to USD 500,000 when purchasing land or a tractor. It may also be used to repair buildings.

Farmers are increasingly investing in farm equipment to work at optimum capacity with a smaller workforce. Although these equipment types come with a high initial investment, they help improve overall crop quality and quantity. Many farmers are now scaling down their agricultural operations and leasing out a portion of their farms to offset rising labor costs.

As more farmers are reducing their dependency on labor, it is expected that tractor sales will witness healthy growth in the coming years, thereby driving the demand for tractor tires over the forecast period.

Increasing Demand in the United States Despite Falling Farm Income

The overall strength of the US economy, including factors such as income levels, purchasing power, and infrastructure development, plays a role in driving demand for agricultural tires. A robust economy supports investments in the agricultural sector, leading to increased demand for equipment and tires. In 2001, the gross farm income totaled USD 249.9 billion, which increased significantly by the end of 2022 to over USD 604.1 billion.

The country holds a vast and highly developed agricultural sector, with a significant number of farms and extensive agricultural operations. This large-scale farming requires a substantial number of agricultural tires to support various equipment and machinery. Moreover, in 2022, 2 million farms were in the United States, down from 2.20 million in 2007. In a similar vein, farmland acres continue to decline, falling from 915 million acres in 2002 to 893 million acres in 2022. The average farm size increased a bit from 440 acres in the 1970s to 446 acres in 2022.

Despite the decrease in the number of farms, the United States remains at the top due to the consolidation and modernization of the agricultural sector. Larger, more technologically advanced farms benefit from economies of scale and specialization, allowing for increased productivity and efficiency. It, combined with advancements in agricultural practices, equipment, and infrastructure, helps the United States maintain its position as a leading agricultural producer.

Additionally, the United States is a significant exporter of agricultural products, supplying food and commodities to both domestic and international markets. This export-oriented agriculture relies on efficient farming practices and equipment, further driving the demand for agricultural tires.

US agricultural exports grew steadily in the past 25 years, from USD 62.8 billion in 1997 to USD 196 billion in 2022. Consumer-oriented products, including high-value items like dairy, meats, fruits, and vegetables, experienced significant export growth due to global population growth, rising incomes, and dietary diversification.

Such factors are likely to drive the demand for agriculture tires in the United States over the coming years.

Agricultural Tires Industry Overview

The agricultural tire market is moderately concentrated. The major players in the agricultural tires market are Bridgestone Corporation (Firestone), Titan International Inc. (Goodyear Tires), BKT, Continental Reifen Deutschland GmbH, and Michelin, among others.

Other companies in the industry include Carlisle Companies Incorp., Trelleborg Wheel Systems, and McCreary Tire & Rubber Co. In order to maintain market dominance, the major companies are focusing on product up-gradation and customization to expand the overall product line, with robust offerings in the agricultural tires market.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Growing Global Population

- 4.1.2 Others

- 4.2 Market Restraints

- 4.2.1 Fluctuating Commodity Prices

- 4.2.2 Others

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Sales Channel Type

- 5.1.1 OEM

- 5.1.2 Replacement/Aftermarket

- 5.2 Application Type

- 5.2.1 Tractors

- 5.2.2 Combine Harvesters

- 5.2.3 Sprayers

- 5.2.4 Trailers

- 5.2.5 Loaders

- 5.2.6 Other Application Types

- 5.3 Tire Type

- 5.3.1 Bias Tires

- 5.3.2 Radial Tires

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Spain

- 5.4.2.5 Italy

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 South Korea

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 Rest of the World

- 5.4.4.1 South America

- 5.4.4.2 Middle-East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles*

- 6.2.1 Bridgestone Corp.

- 6.2.2 Continental AG

- 6.2.3 Balakrishna Industries Limited

- 6.2.4 Titan International Inc.

- 6.2.5 Trelleborg AB

- 6.2.6 Michelin

- 6.2.7 Nokian Tyres PLC

- 6.2.8 Pirelli & C SpA (Prometeon Tyre Group)

- 6.2.9 Alliance Tire Group

- 6.2.10 Apollo Tyres

- 6.2.11 Magna Tyres

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Intergration of Tire Pressure Monitoring System

- 7.2 A Dynamic Shift Towards Eco-Friendly and Energy-Efficient Agriculture Tires

全球农业轮胎市场全球农用轮胎市场

全球农业轮胎市场全球农用轮胎市场 全球农业轮胎市场研究报告 - 产业分析、规模、份额、成长、趋势及预测(2025 年至 2033 年)农业轮胎市场规模、份额、趋势分析报告:按产品、应用、分布、地区、细分市场预测,2025-2030 年

全球农业轮胎市场研究报告 - 产业分析、规模、份额、成长、趋势及预测(2025 年至 2033 年)农业轮胎市场规模、份额、趋势分析报告:按产品、应用、分布、地区、细分市场预测,2025-2030 年 农业轮胎市场按轮胎类型、销售管道、应用和地区划分

农业轮胎市场按轮胎类型、销售管道、应用和地区划分 农业轮胎市场规模、份额和成长分析(设计、应用、尺寸、压力、应用和地区)- 产业预测 2025-2032

农业轮胎市场规模、份额和成长分析(设计、应用、尺寸、压力、应用和地区)- 产业预测 2025-2032 农用轮胎市场:按轮胎类型、销售管道、应用分类 - 2025-2030 年全球预测农用轮胎市场:按结构、应用和最终用户划分 - 2025-2030 年全球预测农业机械轮胎市场:按产品类型、应用、最终用户、销售管道、轮胎尺寸、帘布层等级划分 - 2025-2030 年全球预测曳引机用轮胎市场:轮胎类型,用途,流通管道,各地区,2024年~2031年

农用轮胎市场:按轮胎类型、销售管道、应用分类 - 2025-2030 年全球预测农用轮胎市场:按结构、应用和最终用户划分 - 2025-2030 年全球预测农业机械轮胎市场:按产品类型、应用、最终用户、销售管道、轮胎尺寸、帘布层等级划分 - 2025-2030 年全球预测曳引机用轮胎市场:轮胎类型,用途,流通管道,各地区,2024年~2031年