|

市场调查报告书

商品编码

1403072

压力感测器:市场占有率分析、产业趋势/统计、成长预测,2024-2029Pressure Sensors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

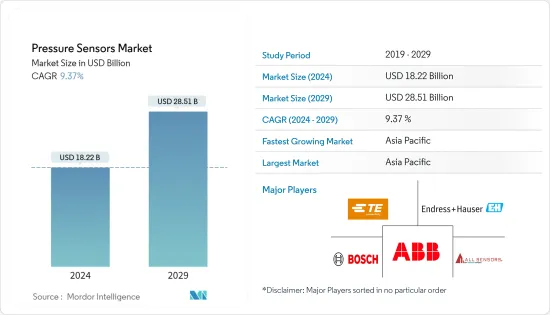

压力感测器市场规模预计到2024年为182.2亿美元,预计到2029年将达到285.1亿美元,在预测期内(2024-2029年)复合年增长率为9.37%。

主要亮点

- 压力感测器是一种配备压感的装置,可测量气体或液体对不銹钢或硅胶製成的隔膜的压力,将测量值转换为电信号并输出。

- 持续收集静态和动态压力变化的资料对于大多数製造设备和工业机构以及许多消费品的正常运作至关重要。压力过高可能会导致输出劣化和负移等问题,并且通常会损害应用程式的正常效能。近年来,压力感测器变得数位化、更小、更便宜、低耗电量,这对收益的快速成长产生了积极影响。这些变化正在提高感测器的效率和性能,掀起新一波的技术创新浪潮。

- 压力感测器有多种应用,需要多种感测器类型和特性。它们有多种类型,包括用于恶劣或腐蚀性环境的类型以及用于高可靠性应用的类型。例如,近几十年来,汽车一直是推动这些设备需求的关键产业之一。为该行业製造感测器的公司通常需要保持 IATF 16949、ISO 21750:2006、ISO 1550-2:2012 和 ISO 26262 等认证。汽车产业的压力感测器还必须满足 ISO 1142-4 的抗电气干扰要求。

- 市场成长归因于对车辆安全功能的需求不断增加、政府法规不断加强以及汽车产业的成长。随着更严格的安全法规的出台,压力感测器的作用预计将得到加强,设计人员主要将其用于三个应用领域:引擎优化、排放控制和安全增强。

- 感测器市场多样化且不断成长,设计工程师将更多感测器装入从汽车到智慧型手机的各种产品中,并将其应用到智慧牙刷和猫砂盒等新应用中。随着感测器变得普及,成本问题继续困扰着工程师。与感测产品相关的高成本预计将阻碍市场成长。

- 在后 COVID-19 的情况下,2022 年初对于全球消费性电子市场来说非常重要,同时由于多种因素的影响也非常困难。例如,受乌克兰战争和通膨失控的影响,消费者信心全面暴跌。此外,2022年春季,我们最大的销售市场中国发生了封锁,这进一步对销售产生了负面影响。

压力感测器市场趋势

汽车预计将占据很大份额

- 汽车领域的压力感知器受轮胎压力、煞车油压力、燃料箱蒸气压、燃油喷射和CDRi、歧管绝对压力等主要因素驱动,创造了应用机会。

- 长期以来,压力感知器广泛应用于各个行业,包括汽车行业,用于测量关键流体的压力,例如发动机油、变速箱和传动油、制动、冷却和燃油系统中的液压油。我做过。汽车产业正在不断取得技术进步,以提高安全性、舒适性和娱乐性,提供各种各样的压力感测器选项。这些感测器的紧凑尺寸极大地影响了它们在汽车设计中的广泛采用。

- 此外,电动车中还使用压力感测器来防止手指被夹在车内。大多数电动车冷却系统都致力于将电池组长时间保持在最佳动作温度。随着汽车製造商希望在电动车中配备更大的电池组,对冷却系统来满足这些需求的需求也随之增加。

- 因此,压力测量是电动车液体冷却系统的关键要素。压力感测器在为冷却系统的调整和优化提供反馈以及检测可能表明洩漏的压力损失方面发挥着至关重要的作用。随着液体冷却系统变得越来越复杂,电动车冷却系统对精确、弹性压力感测器的需求预计将比以往任何时候都成长。

- 微机电系统 (MEMS) 感测器用作压力侦测和空气质量流量感测器。技术的进步正在开发更小的、无电池的轮胎压力感测器模组。基于 MEMS 的能源采集系统目前正在整合到轮胎中,以减小模组尺寸。

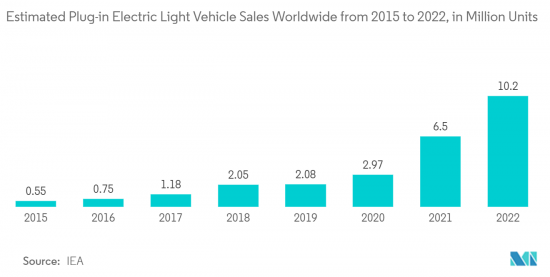

- 随着电动车销量和产量的增加,各种应用都需要压力感测器,包括电池冷却剂和蒸汽检测。 IEA 表示,在净零排放情境下,到 2030 年,电动车销售将占汽车总销量的 65% 左右。电动车销量的成长可能会创造对压力感测器的需求。

亚太地区主导市场

- 对于全球医疗保健产业来说,中国是一个极具前景的市场,其特点是规模庞大、多样性和成长潜力,加上政府的支持和不断变化的人口结构。此外,由于老年人口不断增加以及对优质医疗设备的需求不断增长,各国政府正在优先开拓医疗保健产业,这是市场的关键驱动力。

- 压力感测器在医疗设备中用于监测室内压力并调整治疗期间给药的压力水平。中国是全球着名的医疗设备製造中心。

- 根据国家药品监督管理局的数据,到2022年12月,我国医疗设备企业数量将达到32,632家,从2008年的13,000家稳定成长。这些企业90%以上是中小企业。这些重要的功能可能会增加压力感测器在该地区的应用机会。

- 日本汽车工业汽车产量位居世界第三,在22个都道府县拥有78家工厂。丰田、圭亚那、日产等大企业对日本经济贡献大,汽车製造业占交通设备产业的89%。

- 此外,汽车零件供应商的成长已成为日本经济的重要组成部分。此类关键的汽车功能对各种应用产生了对压力感知器的需求,包括测量关键流体的压力,例如煞车、冷却和燃油系统中的引擎油、变速箱、变速箱油和液压油。此外,电动车(EV)销量增加的地区也有望刺激市场需求。

- HVAC 系统中使用压力感测器来监测空气过滤器的状况。当过滤器被颗粒堵塞时,可以侦测到过滤器两端压差的增加。由于对暖通空调设备的需求不断增加,印度对压力感测器的需求也预计会增加。由于住宅和商业基础设施的快速建设,预计这一需求将加速,而该地区城市人口的成长预计将扩大住宅和商业基础设施的规模。

- 消费性电子製造的增加、汽车产业的投资以及其他产业的发展预计将推动亚太地区压力感测器的发展。

压力感测器产业概况

压力感测器市场呈现分散化、竞争激烈的特点,国内外厂商林立。业界的技术进步为供应商提供了永续的竞争优势。该市场的着名公司包括 ABB Ltd.、TE Connectivity、Endress+Hauser AG、Bosch Sensortec GmbH 和 All Sensors Corporation。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买方议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争公司之间敌对关係的强度

- 产业价值链分析

- 宏观趋势对市场的影响

第五章市场动态

- 市场驱动因素

- 汽车和医疗保健等最终用户行业的成长

- MEMS 和 NEMS 系统在工业中的采用率不断提高

- 市场抑制因素

- 感测产品成本高

第六章市场区隔

- 依感测器类型

- 有线

- 无线的

- 依产品类型

- 绝对

- 微分

- 测量

- 依技术

- 压电电阻

- 电磁

- 容量

- 共振固态

- 光学

- 其他的

- 按申请

- 车

- 医疗保健

- 消费性电子产品

- 产业

- 航太/国防

- 食品与饮品

- HVAC

- 按地区

- 北美洲

- 美国

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 其他欧洲国家

- 亚太地区

- 中国

- 日本

- 印度

- 其他亚太地区

- 拉丁美洲

- 中东/非洲

- 北美洲

第七章竞争形势

- 公司简介

- ABB Ltd

- All Sensors Corporation

- Bosch Sensortec GmbH

- Endress+Hauser AG

- TE Connectivity

- Honeywell International Inc.

- Schneider Electric

- Kistler Group

- Rockwell Automation Inc.

- Emerson Electric Co.

- Sensata Technologies Inc.

- SIEMENS AG

- Yokogawa Corporation

- Infineon Technologies Ag

- STMicroelectronics

- 压力感测器供应商 -市场占有率

第八章投资分析

第九章 市场机会及未来趋势

The Pressure Sensors Market size is estimated at USD 18.22 billion in 2024, and is expected to reach USD 28.51 billion by 2029, growing at a CAGR of 9.37% during the forecast period (2024-2029).

Key Highlights

- A pressure sensor is a device equipped with a pressure-sensitive element that measures the pressure of a gas or a liquid against a diaphragm made of stainless steel, silicon, etc., and converts the measured value into an electrical signal as an output.

- Gathering and collecting continuous data on static and dynamic pressure changes is vital for most manufacturing units and industrial institutions and for the proper operation of many consumer products. Overpressure could cause issues such as deterioration and negative shifts of outputs and generally harm the normal performance of applications. In recent years, pressure sensors have turned digital, miniaturized, lower-cost, and lower-powered, thus positively impacting its revenue surge. These changes have increased sensor efficiency and performance, generating a new wave of innovation.

- There are many different types of applications for pressure sensors, which create a need for a wide variety of sensor types and characteristics. Variants are available for harsh or corrosive environments and are aimed at high-integrity applications. For instance, in the last couple of decades, automotive has been one of the main sectors to drive demand for these devices. Companies that manufacture sensors for this industry must often maintain certification under IATF 16949, ISO 21750:2006, ISO 1550-2:2012, ISO 26262, and others. Pressure sensors in the automotive industry must also meet the requirements of ISO 1142-4 for resistance to electrical interference.

- The market's growth is attributed to the increasing demand for vehicle safety features, rising government regulations, and the growing automotive industry. With strict safety regulations coming into existence, the role of pressure sensors is expected to strengthen as designers use automotive pressure sensors primarily in three application areas: engine optimization, emission control, and safety enhancement.

- The market for sensors is getting diverse and growing, with design engineers packing more sensors into everything from automobiles to smartphones and applying them in new applications like smart toothbrushes and cat litter boxes. As sensors proliferate, concerns over cost continue to preoccupy engineers. The high costs associated with sensing products are expected to hinder the growth of the market.

- In the post-COVID-19 scenario, the start of 2022 was crucial as well as highly difficult for the global consumer electronics market due to numerous factors. For instance, the impact of the war in Ukraine and runaway inflation led consumer sentiment to plummet across the board. Additionally, in spring 2022, there were lockdowns in the largest sales market, China, which further negatively impacted sales. Notably, the football World Cup in the fourth quarter was expected to offer an opportunity to compensate for the weak first half of the year, but experience has shown that major events such as increased demand, particularly for TVs. However, given the poor consumer sentiment, this effect was not big enough to keep sales in the consumer electronics market from decreasing during 2022 overall.

Pressure Sensors Market Trends

Automotive is Expected to Hold Significant Share

- The pressure sensors in the automotive sector are driven by major factors such as tire pressure, brake fluid pressure, vapor pressure in the fuel tank, fuel injection and CDRi, and manifold absolute pressure, among others, which create application opportunities.

- For a long time, pressure sensors have been extensively utilized in various industries, including the automobile sector, to gauge the pressure of crucial fluids such as engine oil, gearbox and transmission oil, and hydraulic oil in braking, cooling, and fuel systems. The automotive industry offers diverse pressure sensor alternatives as it undergoes technological advancements to enhance safety, comfort, and entertainment. The compact size of these sensors has significantly influenced their widespread adoption in automotive design.

- Moreover, pressure sensors are utilized in electric vehicles to prevent finger entrapment indoors. Additionally, most electric vehicle cooling systems strive to maintain battery packs at their optimal operating temperature for extended periods. As automakers endeavor to incorporate battery packs with greater capacity in electric vehicles, the requirements for these cooling systems to manage such demands are also escalating.

- Therefore, pressure measurement has emerged as a crucial factor in the liquid cooling system of an electric vehicle. Pressure sensors play a pivotal role in providing feedback for regulating and optimizing the cooling system and detecting pressure loss that may indicate leakage. With the increasing complexity of liquid cooling systems, the need for precise and resilient pressure sensors for electric vehicle cooling systems is anticipated to be higher than ever.

- Microelectromechanical systems (MEMS) sensors are utilized for pressure sensing and as an air mass flow sensor. Technological advancements have led to the development of more compact and battery-free tire pressure sensor modules. MEMS-based energy harvesting systems are currently integrated into tires to reduce module size.

- The increasing sales and production of electric vehicles necessitate pressure sensors for various applications, including battery cooling fluid and vapor detection. As per the IEA, electric vehicle sales will constitute approximately 65% of total car sales by 2030 in the Net Zero Scenario. Such rising EV sales will create demand for pressure sensors.

Asia Pacific to Dominate the Market

- China presents a highly promising market for the global medical industry, characterized by vast size, diversity, and growth potential, driven by a confluence of government backing and evolving demographics. Furthermore, with an increasingly elderly populace and heightened demand for superior medical equipment, the government has prioritized developing the healthcare sector, serving as a key impetus for the market.

- Pressure sensors are utilized in medical devices to oversee the pressure within the chamber and regulate the pressure level administered during treatment. China is a prominent global hub for medical device manufacturing.

- As per the National Medical Products Administration, the number of medical device companies in China reached 32,632 by December 2022, exhibiting a steady growth from 13,000 in 2008. Most of these companies, over 90%, are small and medium-sized enterprises. Such significant capabilities will enhance the application opportunities for the pressure sensors in the region.

- The automotive industry in Japan is the third-largest producer of automobiles globally, boasting 78 factories across 22 prefectures. Major companies such as Toyota, Kei, and Nissan contribute significantly to the country's economy, with automotive manufacturing accounting for 89% of the transportation machinery industry.

- Additionally, the growth of auto parts suppliers has become a substantial component of Japan's economy. Such significant automotive capabilities will create the demand for pressure sensors for various applications, such as to gauge the pressure of crucial fluids such as engine oil, gearbox and transmission oil, and hydraulic oil in the braking, cooling, and fuel systems. The region's progress in augmenting electric vehicle (EV) sales is also anticipated to stimulate market demand.

- Pressure sensors are utilized in HVAC systems to monitor the state of air filters. The rise in differential pressure across the filter can be detected as it becomes clogged with particulates. The demand for pressure sensors in India is estimated to rise due to the increasing demand for HVAC equipment. This demand is expected to accelerate due to the rapid construction of residential and commercial infrastructure, which is anticipated to expand as a result of the growing urban population in the region.

- The rising consumer electronics manufacturing, investments in the automotive industry, and developments in other sectors are expected to create the damned for pressure sensors in Asia-Pacific.

Pressure Sensors Industry Overview

The pressure sensor market is characterized by fragmentation and intense competition, with a presence of both domestic and international players. Technological advancements in the industry provide vendors with a sustainable competitive edge. Notable companies in this market include ABB Ltd., TE Connectivity, Endress+Hauser AG, Bosch Sensortec GmbH, and All Sensors Corporation.

In June 2023, Thermo Control, in partnership with Schneider Electric, implemented the Ecostruxure Building Management System (BMS) solution in a new factory constructed by IFM Prover in Sibiu, Romania. This system serves to monitor, control, and manage all electrical and mechanical installations within the factory. Additionally, the factory has integrated photovoltaic panels and heat pumps into the BMS solution, enhancing energy efficiency and reducing utility costs. Furthermore, the temperature, humidity, and pressure sensors utilized in the monitoring and control processes are manufactured within the IFM factory.

In January 2023, Bosch Sensortec unveiled a range of new sensors at CES 2023, including an AI-enabled sensor and a next-generation magnetometer. The newly introduced BMP585 barometric pressure sensors offer altitude tracking capabilities even in challenging environments, such as for wearables designed for swimming. These sensors boast ultra-low power consumption, ensuring extended battery life while delivering high accuracy and minimal noise levels.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Impact of Macro Trends on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growth of End-user Verticals, Such as Automotive and Healthcare

- 5.1.2 Increasing Adoption of MEMS and NEMS Systems in the Industry

- 5.2 Market Restraints

- 5.2.1 High Costs Associated with Sensing Products

6 MARKET SEGMENTATION

- 6.1 By Type of Sensor

- 6.1.1 Wired

- 6.1.2 Wireless

- 6.2 By Product Type

- 6.2.1 Absolute

- 6.2.2 Differential

- 6.2.3 Gauge

- 6.3 By Technology

- 6.3.1 Piezoresistive

- 6.3.2 Electromagnetic

- 6.3.3 Capacitive

- 6.3.4 Resonant Solid-State

- 6.3.5 Optical

- 6.3.6 Other Pressure Sensors

- 6.4 By Applications

- 6.4.1 Automotive

- 6.4.2 Medical

- 6.4.3 Consumer Electronics

- 6.4.4 Industrial

- 6.4.5 Aerospace and Defense

- 6.4.6 Food and Beverage

- 6.4.7 HVAC

- 6.5 By Geography

- 6.5.1 North America

- 6.5.1.1 United States

- 6.5.1.2 Canada

- 6.5.2 Europe

- 6.5.2.1 United Kingdom

- 6.5.2.2 Germany

- 6.5.2.3 France

- 6.5.2.4 Rest of Europe

- 6.5.3 Asia-Pacific

- 6.5.3.1 China

- 6.5.3.2 Japan

- 6.5.3.3 India

- 6.5.3.4 Rest of Asia Pacific

- 6.5.4 Latin America

- 6.5.5 Middle East and Africa

- 6.5.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles*

- 7.1.1 ABB Ltd

- 7.1.2 All Sensors Corporation

- 7.1.3 Bosch Sensortec GmbH

- 7.1.4 Endress+Hauser AG

- 7.1.5 TE Connectivity

- 7.1.6 Honeywell International Inc.

- 7.1.7 Schneider Electric

- 7.1.8 Kistler Group

- 7.1.9 Rockwell Automation Inc.

- 7.1.10 Emerson Electric Co.

- 7.1.11 Sensata Technologies Inc.

- 7.1.12 SIEMENS AG

- 7.1.13 Yokogawa Corporation

- 7.1.14 Infineon Technologies Ag

- 7.1.15 STMicroelectronics

- 7.2 Pressure Sensors Vendors - Market Share

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS

2024 年压力感测器全球市场报告

2024 年压力感测器全球市场报告 全球光纤压力感测器市场:趋势、预测、竞争分析(~2030 年)

全球光纤压力感测器市场:趋势、预测、竞争分析(~2030 年) 2024-2028年压力感测器全球市场

2024-2028年压力感测器全球市场 全球压力感测器市场规模、占有率和行业趋势分析报告:2023-2030年按类型、产品、技术、应用和地区分類的展望和预测

全球压力感测器市场规模、占有率和行业趋势分析报告:2023-2030年按类型、产品、技术、应用和地区分類的展望和预测 MEMS压力感测器全球市场2024-2028

MEMS压力感测器全球市场2024-2028 压力感测器:各种技术和全球市场

压力感测器:各种技术和全球市场 压力感测器市场:2023-2028 年全球产业趋势、份额、规模、成长、机会与预测

压力感测器市场:2023-2028 年全球产业趋势、份额、规模、成长、机会与预测 压力感测器市场 - 2018-2028 年全球产业规模、份额、趋势、机会和预测,按感测器类型、产品类型、技术、应用、地区和竞争细分

压力感测器市场 - 2018-2028 年全球产业规模、份额、趋势、机会和预测,按感测器类型、产品类型、技术、应用、地区和竞争细分 压力感测器市场:按类型、技术、用途- 2023-2030 年全球预测

压力感测器市场:按类型、技术、用途- 2023-2030 年全球预测 到 2028 年的压力传感器市场预测 - 按产品、技术、类型、应用和地区分列的全球分析

到 2028 年的压力传感器市场预测 - 按产品、技术、类型、应用和地区分列的全球分析