|

市场调查报告书

商品编码

1403104

物联网中间件:市场占有率分析、产业趋势/统计、2024年至2029年成长预测IoT Middleware - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

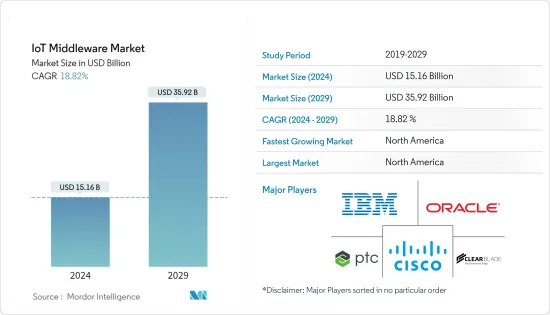

预计2024年物联网中介软体市场规模为151.6亿美元,2029年将达359.2亿美元,在预测期内(2024-2029年)复合年增长率为18.82%。

主要亮点

- 物联网技术在製造、汽车和医疗保健等最终用户行业中的日益采用正在积极推动市场成长。随着传统製造业数位转型,物联网正在推动下一次智慧型互联的工业革命。这正在改变行业处理系统和机械中日益复杂的流程的方式,以提高效率并减少停机时间。随着越来越多的设备连接到互联网,物联网中间件已成为企业的重点关注领域,增加了这些设备之间无缝协作和连接的需求。

- 此外,物联网中介软体市场在各个领域都有庞大的需求。这是由越来越多的连接设备以及管理它们产生的大量资料的需求所推动的。物联网中间件在最终用户领域的整合预计将简化业务、增强服务交付并创造新的商机。

- 采用与产业无关的应用程式中间件在降低未来物联网解决方案变更的复杂性方面发挥关键作用。此外,随着物联网越来越多地整合到行动装置、机器、装置、平板电脑等中,需要一个平台来支援和整合这些需求。

- 智慧城市计划等政府措施预计将创造对物联网中介软体的需求。连网型建筑、智慧工厂和智慧家庭等趋势预计将为市场创造机会。此外,智慧城市概念在能源、废弃物和基础设施领域的物联网方面展现了巨大的前景。

- 后 COVID-19 世界需要对工业IoT云端基础的远端安全控制,而无需训练有素的劳动力。此外,製造、医疗保健和运输等行业中联网设备的普及预计将在未来几年进一步推动对物联网中间件解决方案的需求。

物联网中介软体市场趋势

製造业可望高成长

- 工业 4.0 和物联网是整个物流链开发、生产和管理的新技术方法的核心,即智慧工厂自动化。随着工业4.0 和物联网(IoT) 的普及,製造业发生了巨大转变,正在推动企业变得敏捷、智能,并利用机器人技术补充和增强人类劳动力的技术来推动生产,并减少因流程而导致的工业事故。失败,我们需要采取创新的方法。

- 随着连网型设备和感测器的高采用率以及 M2M通讯的可用性,製造中产生的资料点数量正在迅速增加。这些资料点可以是任何数据,从表示材料经历一个製程週期所需时间的指标到汽车产业中材料应力能力计算等复杂的数据。

- 物联网中间件不仅可以实现基于物联网的工厂自动化,还可以实现基于物联网的虚拟製造应用,允许製造商在其主要製造设施中部署物联网设备。物联网中间件可以实现基于物联网的虚拟製造应用和基于物联网的工厂自动化。物联网中间件使製造业的四个基本要素能够无缝运作:产品、人员、流程和基础设施。

- 此外,製造商前进的一个关键考虑因素是透过支援跨多个装置的客製化和简化软体升级的开放架构来提高弹性。因此,该领域预计将受益于开放原始码联网中间件开发的快速兴起。

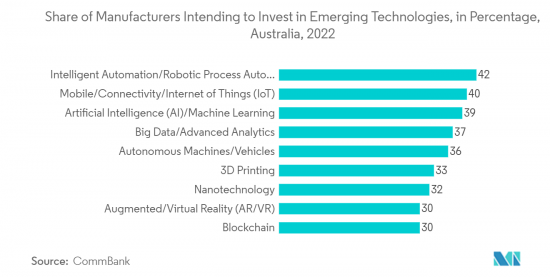

- 此外,世界各地的製造业越来越多地投资于新兴技术,为製造业中物联网中间件的实施创造了巨大的成长机会。例如,CommBank在2022年1月进行的一项研究发现,42%的澳洲製造商将在未来两到三年内投资于与智慧型自动化和机器人流程自动化相关的新兴技术领域,显示有这样做的意图。投资行动、连结和物联网 (IoT) 是第二大可能的投资领域,40% 的製造商表示有投资意愿。

北美地区预计将占据主要市场占有率

- 在互联联网汽车、智慧型能源计划、家庭自动化和智慧製造的推动下,物联网在该地区主要收益终端用户行业中的作用日益增强,预计北美将成为一个重要的市场。 。美国和加拿大是巨量资料、物联网和行动等技术的早期采用者,为物联网中间件市场创造了巨大的成长机会。

- 美国正处于第四次工业革命的边缘。资料在生产中大规模使用,与整个供应链中的各种製造系统整合。因此,资讯科技的出现以及物联网在製造、工业和汽车等广泛应用中的日益广泛使用,为业务运营的实施带来了新的维度。

- 该地区的製造商依靠 IIoT 平台进行常见流程最佳化、仪表板和视觉化以及状态监控。虽然中小型企业提高了将新技术融入现有系统的弹性,但大型製造商却在数位化方面投入了大量预算。

- 此外,当前投入和人事费用不断增加的环境,以及与全球竞争製造商的竞争也是报酬率推动力,有望吸引技术投资。

- 支持这一趋势的是先进製造合作伙伴关係 (AMP) 2.0 的形成,旨在将产业转变为大学。联邦政府正在投资新兴技术和智慧製造倡议,例如智慧製造领导联盟(SMLC),以促进和鼓励製造智慧的广泛采用。预计这些市场趋势也将强调市场对物联网中介软体解决方案的需求。

物联网中介软体产业概况

物联网中介软体市场竞争激烈,可望透过为企业引入创新解决方案来颠覆传统 IT 产业。市场参与者正在采取产品创新、併购和收购等关键策略,以增强产品能力并保持竞争。参与这一市场形势的一些着名公司包括 Cisco Systems Inc.、IBM Corp.、Oracle Corporation、ClearBlade Inc. 和 PTC Inc.。

2023 年 3 月,物联网解决方案专业供应商 Alliot Technologies 宣布推出突破性物联网中介软体平台 Symbius。这个创新平台旨在消除与蜂巢式物联网相关的障碍。 Symbius 提供将记录的资料解码为标准化格式的独特能力,并将成为同类先驱平台之一。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买方议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争公司之间敌对关係的强度

- 产业价值链分析

- 评估 COVID-19 对物联网中介软体生态系的影响

第五章市场动态

- 市场驱动因素

- 开放原始码平台的演变

- M2M通讯的增加

- 市场抑制因素

- 物联网中间件开发涉及的复杂技术

- 物联网中介软体应用分析

- 应用程式管理

- 资料管理

- 其他应用

第六章市场区隔

- 按平台

- 应用程式支援

- 设备管理

- 连线管理

- 按最终用户产业

- 製造业

- 医疗保健

- 能源/公共产业

- 运输/物流

- 农业

- 其他最终用户产业

- 地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东/非洲

第七章竞争形势

- 公司简介

- Cisco Systems Inc.

- IBM Corp.(Red Hat Inc.)

- Oracle Corporation

- ClearBlade Inc.

- PTC Inc.

- Arrayent Inc.

- Axiros GmbH

- Davra Networks

- Amazon Web Services Inc.

- Bosch.IO GmbH

- MuleSoft LLC(Salesforce Company)

第八章投资分析

第九章市场机会与未来性

The IoT Middleware Market size is estimated at USD 15.16 billion in 2024, and is expected to reach USD 35.92 billion by 2029, growing at a CAGR of 18.82% during the forecast period (2024-2029).

Key Highlights

- The growing adoption of IoT technology across end-user industries, such as manufacturing, automotive, and healthcare, is positively driving the market's growth. With the traditional manufacturing sector amid a digital transformation, IoT is fueling the next industrial revolution of intelligent connectivity. This is changing how industries approach increasingly complex processes of systems and machines to improve efficiency and reduce downtime. With the growth in the number of devices connected to the internet, there is a greater need for seamless collaboration and connectivity between those devices, thus making IoT middleware a significant focus area for businesses.

- Additionally, the IoT Middleware market is witnessing substantial demand in various This is driven by the need to manage the growing number of connected devices and the vast amount of data they generate. The integration of IoT middleware in end-user sectors is expected to streamline operations, enhance service delivery, and create new business opportunities.

- Adopting an industry-agnostic application middleware plays a vital role in reducing the complexity of future changes to their IoT solutions. Further, with the growing integration of IoT into mobile devices, machinery, equipment, and tablets, among other devices, the need for a platform to support and integrate such demands has become necessary.

- Government initiatives, such as smart city projects, are expected to create demand for IoT middleware. Trends, such as connected buildings, smart factories, and smart homes, are expected to create opportunities for the market. Moreover, the smart cities' concept has marked a great prospect with the IoT in the energy, waste, and infrastructure sectors.

- In the post-COVID-19 world, cloud-based remote and secure control over industrial IoT without the need for a highly trained workforce has become necessary. Moreover, the proliferation of connected devices in industries such as manufacturing, healthcare, and transportation is further expected to drive the demand for IoT Middleware solutions in the coming years.

IoT Middleware Market Trends

Manufacturing Expected to Have the High Potential Growth

- Industry 4.0 and IoT are at the center of new technological approaches for developing, producing, and managing the entire logistics chain, otherwise known as smart factory automation. Massive shifts in manufacturing due to Industry 4.0 and the acceptance of IoT require enterprises to adopt agile, smarter, and innovative ways to advance production with technologies that complement and augment human labor with robotics and reduce industrial accidents caused by process failure.

- With the high rate of adoption of connected devices and sensors and the enabling of M2M communication, there has been a surge in data points that are generated in the manufacturing industry. These data points can be of various kinds, ranging from a metric describing the time taken for the material to pass through one process cycle to a more advanced one, such as calculating the material stress capability in the automotive industry.

- IoT Middleware can implement IoT-based virtual manufacturing applications as well as IoT-based factory automation, which encourages manufacturers to deploy IoT devices in key manufacturing establishments. Another factor driving the market growth is the advantage of IoT in attaining "informed" manufacturing. IoT middleware enables four essential elements of manufacturing, such as Products, People, Processes, and Infrastructure, to work seamlessly.

- Also, a significant consideration while aiming for the manufacturing industry is the promotion of flexibility through open architectures that support customization and streamlined software upgrades across multiple devices. Therefore, this segment is expected to benefit from the rapid emergence of Open-source IoT middleware developments.

- Additionally, manufacturing organizations in many countries worldwide are increasingly investing in emerging technologies, thus creating significant growth opportunities for adopting IoT middleware in the manufacturing sector. For instance, according to a survey conducted by CommBank in January 2022, 42% of Australian manufacturers intend to invest in the emerging technology area relating to intelligent automation and robotic process automation over the next two to three years. Investment in mobile, connectivity, and the Internet of Things (IoT) was among the second intended investment areas, with 40% of manufacturers intending to invest.

North America Region is Anticipated to Holds Major Market Share

- North America is expected to be a prominent market due to the growing role of IoT among the significant revenue-generating end-user industries of the region, driven by the deployment of connected cars, smart energy projects, home automation, and a focus on smart manufacturing. The US and Canada are the early adopters of technologies, such as Big Data, IoT, and mobility, and it creates significant growth opportunities for the IoT middleware market.

- The United States is on the verge of the fourth industrial revolution. Data is being used on a large scale for production while integrating it with a wide variety of manufacturing systems throughout the supply chain. Therefore, the emergence of information technology and the increased usage of IoT across a wide range of manufacturing, industrial, and automotive applications have added a new dimension to conducting business operations.

- Manufacturers in the region rely on IIoT platforms for general process optimization, dashboards and visualization, and condition monitoring. SMEs are becoming increasingly flexible in incorporating new technologies with their existing systems, whereas large manufacturers have massive budgets for digitization.

- Another significant driver is the prevalence of an environment of increasing input, labor cost, and competition from large global manufacturers, which is expected to attract investment in technologies such as IoT to remain competitive and maintain operating margins.

- Aiding this trend is the formation of the "Advanced Manufacturing Partnership (AMP) 2.0," an initiative undertaken to make the industry universities. The federal government is investing in emerging technologies and smart manufacturing initiatives, such as the Smart Manufacturing Leadership Coalition (SMLC), to drive and facilitate the broad adoption of manufacturing intelligence. Such trends in the market are also expected to emphasize the need for IoT middleware solutions in the market.

IoT Middleware Industry Overview

The IoT middleware market is highly competitive, poised to disrupt the traditional IT industry by introducing innovative solutions for enterprises. Market players are embracing key strategies such as product innovation, mergers, and acquisitions to enhance their product functionality and maintain their competitive edge. Notable companies operating in this market landscape include Cisco Systems Inc., IBM Corp., Oracle Corporation, ClearBlade Inc., and PTC Inc., among others.

In March 2023, Alliot Technologies, a specialized provider of IoT solutions, introduced its groundbreaking IoT Middleware platform called Symbius. This innovative platform is designed to eliminate the barriers associated with cellular IoT. Symbius is set to become one of the pioneering platforms of its kind, offering the unique capability to decode recorded data into a standardized format.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of COVID-19 Impact on the IoT Middleware Ecosystem

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Developments Across Open-source Platforms

- 5.1.2 Increasing M2M Communications

- 5.2 Market Restraints

- 5.2.1 Complex Technologies Pertaining to the Development of IoT Middleware

- 5.3 Analysis of IoT Middleware Applications

- 5.3.1 Application Management

- 5.3.2 Data Management

- 5.3.3 Other Applications

6 MARKET SEGMENTATION

- 6.1 By Platform

- 6.1.1 Application Enablement

- 6.1.2 Device Management

- 6.1.3 Connectivity Management

- 6.2 By End-user Industry

- 6.2.1 Manufacturing

- 6.2.2 Healthcare

- 6.2.3 Energy and Utilities

- 6.2.4 Transportation and Logistics

- 6.2.5 Agriculture

- 6.2.6 Other End-user Industries

- 6.3 Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia-Pacific

- 6.3.4 Latin America

- 6.3.5 Middle East & Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Cisco Systems Inc.

- 7.1.2 IBM Corp. (Red Hat Inc.)

- 7.1.3 Oracle Corporation

- 7.1.4 ClearBlade Inc.

- 7.1.5 PTC Inc.

- 7.1.6 Arrayent Inc.

- 7.1.7 Axiros GmbH

- 7.1.8 Davra Networks

- 7.1.9 Amazon Web Services Inc.

- 7.1.10 Bosch.IO GmbH

- 7.1.11 MuleSoft LLC (Salesforce Company)

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE OF THE MARKET

2024 年物联网中间件全球市场报告

2024 年物联网中间件全球市场报告 物联网中间件市场:按平台类型、组织规模、产业划分 - 2024-2030 年全球预测

物联网中间件市场:按平台类型、组织规模、产业划分 - 2024-2030 年全球预测 IoT中介软体的全球市场

IoT中介软体的全球市场 IoT中介软体的全球市场:现状分析与预测(2022年~2028年)

IoT中介软体的全球市场:现状分析与预测(2022年~2028年)