|

市场调查报告书

商品编码

1403118

智慧交通:市场占有率分析、产业趋势与统计、2024年至2029年成长预测Smart Transportation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

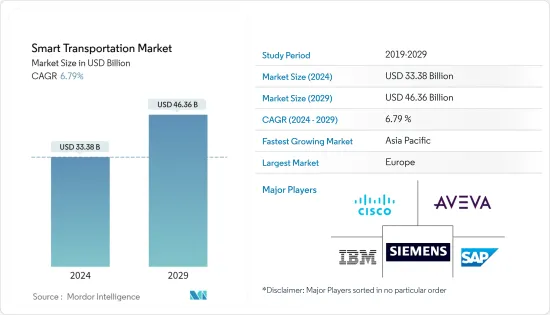

智慧交通市场规模预计到2024年为333.8亿美元,预计到2029年将达到463.6亿美元,在预测期内(2024-2029年)复合年增长率为6.79%。将要。

交通量的增加、旨在减少温室气体影响的政府措施、城市计划数量的增加、特大城市的崛起、都市化和人口成长是推动市场成长的因素。联合国预计,2030年,全球70%以上的人口将实现城市化,印度将有7亿人居住在城市。这些预测为规划、设计和建立一个生态学和经济永续的新印度提供了独特的机会。此外,都市化正在推动世界各地的国家经济发展,因为世界75%的经济生产发生在城市。

主要亮点

- 日益增长的都市化反映了世界城市日益复杂的情况,包括其交通需求。运输市场面临的主要挑战之一是解决这种复杂性。在预测期内,物联网和连接设备的成长趋势可能会与智慧城市计划一起持续下去。特别是,由于智慧家庭、智慧电錶、智慧交通和智慧照明等透过物联网相互通讯的连网产品的使用越来越多,预计该市场将会扩大。此外,预计到2025年将有超过26个智慧城市,其中大部分位于北美和欧洲,人工智慧和物联网技术在智慧城市的采用是主要推动力。

- 创新城市发展的主要目标之一是智慧运输,包括交通。建构高效、灵活、一体化的交通网络对于智慧运输至关重要。智慧运输是现代城市中心的重要发展驱动力,有潜力改善游客和居民的日常生活。到 2040 年,城市预计将容纳世界人口的 65%。城市交通管理优先考虑健康的交通途径,例如步行和骑自行车。移动管理还可以最大限度地减少碳排放,并为当地社区提供最佳的交通流量分析。

- 人口从郊区和农村地区快速迁移到城市,以及人口向大城市中心集中,加剧了交通拥堵。由于道路设计不佳和城市规划不完善,城市变得更加密集,城市拥挤现像日益严重。例如,2022 年,美国驾驶者平均在交通中损失 51 小时,即每週约 1 小时。根据行动分析公司 Inrix 的 2022 年全球交通记分卡,这比以前多了 15 个小时,美国驾驶者在交通上浪费的每一个小时的成本为 869 美元。

- 此外,2022 年 4 月,电子和资讯技术部 (MeitY) 在智慧型运输系统(ITS) 下启动了多项应用程序,作为 InTranSE-II 计划的一部分,以改善印度的交通状况。印度专用的 ADAS(高级驾驶辅助系统)、汇流排讯号优先系统和 CoSMiC(通用智慧物联网连接)软体是 CDAC(高级运算开发中心)和 IIT-M(印度马德拉斯理工学院)的合资企业。设计的。 Mahindra & Mahindra 是该计划的工业合作伙伴。政府宣称 ODAWS 的目的是改善高速公路基础设施。

- 然而,由于需要标准化策略,智慧交通涉及软体、硬体、行动网路组件等许多混合方面,由多家厂商生产,引发了相容性问题。此外,各国的通讯协定差异很大,这使得製造商确保其产品获得全球认可成为一项挑战。

- 在后 COVID-19 的情况下,公共运输、基于感测器的技术和票务技术对生物识别、整合、非接触式和行动付款的采用不断增长的需求可能会对市场产生积极影响。此外,各公司的发展也预计将推动智慧交通的需求。

智慧交通市场趋势

不断发展的都市化、特大城市和人口成长推动市场

- 人口的增加以及都市化和大城市的增加是推动市场的关键因素。此外,随着人口成长和都市化,许多城市将面临交通挑战,增加了对智慧交通的需求。例如,根据人口研究所的数据,2022年全球都市化为57%。北美是都市化最高的地区,五分之四以上的人口居住在都市区。

- 世界上一半以上的城市人口居住在亚洲,而印度和中国等一些国家仅都市区就已有约 10 亿人。其他城市人口相对较多的地区是北美、欧洲和非洲。都市化的不断加快意味着世界城市交通变得更加复杂。解决这些复杂性是这些地区交通市场面临的关键挑战之一。例如,根据联合国的数据,到2050年,68%的人将居住在都市区。

- 城市人口成长对大众交通工具基础设施带来巨大压力。大城市的居民可能期望公共运输快速、有效率、负担得起、安全且环保。提供此类交通基础设施是未来城市面临的关键挑战之一。此外,快速的都市化导致严重的交通拥堵、严重的安全问题和不断扩大的城市差距。为了克服这些挑战,透过弹性网路控制提供即时运动和交通资讯的智慧交通解决方案近年来在许多高度都市化的城市中获得了广泛的欢迎。

- 此外,都市区和特大城市也面临交通拥堵加剧、污染物排放增加和燃料资源枯竭等交通相关问题,这对大都市的整体福祉产生负面影响。为了使交通管理更加有效,世界各地的一些城市正在透过采用智慧交通系统将其现有系统智慧化。

- 此外,城市交通对于提高任何城市公民的生活品质至关重要。如今,世界城市的规模已扩大到令人难以置信的规模。世界大城市的日益成熟以及交通领域技术领域的多重创新进一步推动了市场的成长。

亚太地区预计将录得最快成长

- 中国最近在其「十四五」规划(2021-2025)中提供了综合交通运输系统概述。报告指出,2025年,中国将大力发展智慧型交通、生态交通,运输业整体运能、服务品质和效率显着提升。该计划旨在改善交通运输业的公路、铁路、港口和水路以及所涉及的技术和人力资源。因此,它将支持都市化的成长、消费需求和要素供给的变动。

- 由于物联网(IoT)等智慧交通网路的引入,智慧交通在日本迅速扩张。智慧交通网路需要包含云端、感测器和资料通讯等技术的物联网架构。近年来的快速改进使得增强的设备通讯成为可能。

- 澳洲正在开发与驾驶员和基础设施提供者互动的交通管理技术,以减少交通拥堵并改善安全和交通条件。该国拥有多样化且复杂的交通基础设施网络,对智慧交通技术不断增长的需求为参与企业该国市场提供了机会。

- 亚太地区的其他地区由新加坡、印度和韩国等许多新兴国家组成。这些国家正在兴起智慧城市,交通领域也越来越多地采用智慧型技术,以提高交通效率,为技术供应商创造市场机会。

- 亚太地区国家也透过投资和伙伴关係相互帮助以开拓市场。例如,2022年12月,印度和韩国从韩国经济发展合作基金(EDCF)获得了149.5亿印度卢比(1.8314亿美元)的贷款,用于在那格浦尔-孟买高速公路上建造智慧型交通系统。我们同意接收它。

智慧交通产业概况

由于智慧交通产业的市场渗透率相对较低,企业正在透过提供针对特定细分市场的产品和解决方案,甚至为个人客户量身打造产品来增加差异化和价格实现,我们正在做好准备。智慧交通和商业领域的主要参与企业,如思科、SAP SE 和 IBM,正致力于拓展新领域。这些公司在开发新颖和原创的想法以扩展其在智慧交通领域的产品线方面有着实绩。总体而言,产业竞争对手之间的敌对行动预计在预测期内将会加剧。

- 2022 年 11 月 - 阿尔斯通与哈萨克铁路公司 (KTZ) 签署合作协议。阿尔斯通和 KTZ 加强了在 KTZ火车头更新和维护支援方面的合作伙伴关係,其中包括下一代火车头KZ8A。目前,已有90台货运火车头和39台客运火车头投入商业运营,并计划製造并交付KTZ 160台货运火车头和80台客运火车头。

- 2022 年 10 月——西门子与 16 家合作伙伴启动了计划,旨在增强区域铁路自主运营中的人工智慧,计划运行至 2024年终。该计划的预算为 2,300 万欧元(2,500 万美元),属于德国政府资助的「safe.trAIn」计划。满足这种高度控制和标准化环境下的要求可以显着提高区域铁路运输的效率和永续性。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买方议价能力

- 新进入者的威胁

- 竞争公司之间的敌对关係

- 替代品的威胁

- 产业价值链分析

- 宏观经济走势对市场的影响

- 技术简介

第五章市场动态

- 市场驱动因素

- 都市化的进步、特大城市的增加和人口的成长

- 政府加强交通基础设施的倡议

- 市场抑制因素

- 引进资金要求高

第六章市场区隔

- 按用途

- 交通管理

- 道路安全和安保

- 停车场管理

- 公共运输

- 车用通讯系统

- 货物运输

- 其他应用

- 依产品类型

- 高阶旅客资讯系统 (ATIS)

- 先进运输管理系统(ATMS)

- 智慧型运输定价系统 (ATPS)

- 先进大众交通工具系统 (APTS)

- 协同车辆系统

- 按地区

- 北美洲

- 美国

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 欧洲其他地区

- 亚太地区

- 中国

- 日本

- 澳洲

- 其他亚太地区

- 拉丁美洲

- 墨西哥

- 巴西

- 其他拉丁美洲

- 中东/非洲

- 阿拉伯聯合大公国

- 南非

- 沙乌地阿拉伯

- 中东和非洲其他地区

- 北美洲

第七章竞争形势

- 公司简介

- Cisco Systems Inc.

- SAP SE

- IBM Corporation

- AVEVA Group PLC

- Siemens Corporation

- Oracle Corporation

- Alstom

- Advantech Co. Ltd

- Orange SA

- Huawei Technologies Co. Ltd

- Hitachi Ltd

第八章投资分析

第9章 市场的未来

The Smart Transportation Market size is estimated at USD 33.38 billion in 2024, and is expected to reach USD 46.36 billion by 2029, growing at a CAGR of 6.79% during the forecast period (2024-2029).

Increasing traffic volume, government initiatives aimed at decreasing the effects of greenhouse emissions, rising city projects, and the rise of megacities, urbanization, and population are some factors driving the market growth. The UN forecasts estimate that more than 70% of the world population will be urbanized by 2030, wherein 700 million people will reside in cities in India. These predictions serve as a unique opportunity to plan, design, and build an ecologically and economically sustainable new India. Additionally, urbanization has boosted national economies across the globe, as 75% of global economic production takes place in the cities.

Key Highlights

- Increasing urbanization reflects the growing complexities in cities worldwide, with transportation needs being one of them. One of the primary issues the transportation market faces is resolving this complexity. The trend of a rising number of IoT and linked devices will continue with smart city projects during the projection period. The increased use of linked products like smart homes, smart meters, smart transportation, and smart lighting, among others that use IoT to communicate with one another, is expected to drive market expansion. In addition, it is predicted that by 2025, there will be more than 26 smart cities, with the majority existing in North America and Europe, delivering a significant drive to AI and IoT technology for adoption in smart cities.

- One of the primary objectives of innovative city development is smart mobility, which includes transportation. Creating efficient, flexible, and integrated transportation networks is vital to smart mobility. Smart mobility is a significant development driver in modern urban centers and may improve tourists' and inhabitants' everyday lives. By 2040, cities are expected to accommodate 65% of the world's population. Healthy modes of transportation, such as walking and cycling, are prioritized in urban mobility management. Mobility management also minimizes carbon emissions and provides communities with optimal traffic flow analysis.

- Traffic congestion is increasing due to exponential growth in suburban and rural populations relocating to cities and an equivalent increase in population concentration around metropolitan centers. Vehicle congestion in cities has increased as cities have grown in density, assisted by insufficient roadway designs and bad urban planning. For example, in 2022, the average American motorist wasted 51 hours in traffic congestion, or approximately an hour each week. This is 15 hours longer lost to traffic than previously, and all that time squandered in traffic jams costs the typical American motorist USD 869 in lost time, according to the mobility analytics firm Inrix's 2022 Global Traffic Scorecard.

- Further, in April 2022, the Ministry of Electronics and Information Technology (MeitY) launched several applications under the Intelligent Transportation System (ITS) as part of the InTranSE- II program to improve India's traffic scenario. An indigenous Onboard Driver Assistance and Warning System (ODAWS), Bus Signal Priority System, and Common SMart IoT Connectiv (CoSMiC) software were designed as a joint enterprise by the Centre for Development of Advanced Computing (CDAC) and the Indian Institute of Technology Madras (IIT-M). Mahindra and Mahindra was the industrial collaborator for the project. The government declared that ODAWS aims to improve the highway infrastructure as the number of vehicles and road speed has increased, exacerbating safety concerns.

- However, due to the need for a standardized strategy, smart transportation mixed with numerous aspects, such as software, hardware, and mobile network components, are produced by multiple manufacturers, resulting in compatibility concerns. Furthermore, communication protocols range significantly among nations, posing challenges for manufacturers in terms of worldwide acceptance of their products.

- In the post-COVID-19 scenario, rising demand for biometric, integrated, contactless, mobile payment adoption, sensor-based technology, and ticketing technologies throughout public transit will positively impact the market. Moreover, the development by various companies is also expected to boost the demand for smart transportation.

Smart Transportation Market Trends

Rise of Urbanization, Increasing Mega Cities and Population Drives the Market

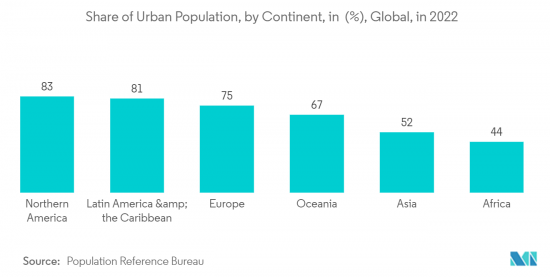

- The population growth, coupled with the increasing urbanization rate and megacities, is the primary factor driving the market. Moreover, as the population grows and urbanizes, many cities will face transportation challenges, thus driving the demand for smart transportation. For instance, according to the Population Reference Bureau, in 2022, the degree of urbanization worldwide was 57%. North America was the region with the highest level of urbanization, with over four-fifths of the population residing in urban areas.

- More than half the world's urban population resides in Asia, where some countries, like India and China, already have about a billion people living in cities alone. The other regions with relatively high urban populations are North America, Europe, and Africa. Increasing urbanization indicates the rising complexities in the transportation of cities worldwide. Resolving these complexities is one of the significant challenges faced by the transport markets across these areas. For instance, according to the United Nations, people living in urban areas are expected to reach 68% by 2050.

- Urban population growth will significantly pressure public transport infrastructure. Residents of big cities will expect public transport that is fast, efficient, affordable, safe, and environmentally friendly. Delivering such transportation infrastructure will be one of the critical challenges confronting future cities. Furthermore, rapid urbanization has brought heavy traffic congestion, serious safety issues, and growing urban inequality. Smart transportation solutions have gained significant traction in the past few years across many highly urbanized cities to overcome such challenges by delivering real-time travel and traffic information with resilient network control.

- Furthermore, besides increasing traffic congestion, the urban areas and megacities face several other transport-related problems, such as growing emissions of pollutants and depleting fuel resources that adversely impact the overall well-being of any major city. To make transport management more effective, several cities worldwide are trying to create intelligence into existing systems by adopting smart transportation systems, which is expected to drive the market's growth at a rapid pace.

- Moreover, urban transportation is becoming crucial for a better quality of life for citizens in any city. Today cities worldwide are expanding to incredible sizes. The rising maturation rate of megacities worldwide and multiple innovations taking place in the technology field for the transportation sector are further driving the market's growth.

Asia Pacific is Expected to Register Fastest Growth

- China outlined a recent comprehensive transportation system in the 14th Five-Year Plan (2021-2025). According to the circular, by 2025, China will have made achievements in pursuing intelligent and green transportation, as well as significant advances in overall competence, service quality, and efficiency of the transportation industry. This plan aims to improve the transportation industry's roads, trains, ports, and waterways and the technology and human resources involved. As a result, this will support growth in urbanization, consumer demand, and factor supply movements.

- Smart transportation is quickly expanding in Japan with the introduction of smart transportation networks, such as the Internet of Things (IoT). Smart transportation networks require IoT architecture, which includes technologies such as the cloud, sensors, and data communication. Rapid improvements in recent years have made it feasible to enhance device communication.

- Australia has been developing traffic management technologies interacting with drivers and infrastructure operators to reduce traffic congestion and enhance safety and traffic conditions. The country has a diverse and complex transportation infrastructure network, creating an opportunity for the market players in the country due to the increasing demand for smart transportation technologies.

- The rest of Asia-Pacific consists of many emerging countries, including Singapore, India, and South Korea. The emergence of smart cities in these countries is increasing the adoption of intelligent technologies in transportation to enhance traffic efficiencies, creating a market opportunity for technology providers.

- Countries in the region are also helping each other by investing and partnering in the market adoption in Asia-Pacific. For instance, in December 2022, India and South Korea agreed to a loan of INR 1,495 crore (USD 183.14 million) from the Economic Development Cooperation Fund (EDCF) of the Republic of Korea to construct an intelligent transport system on the Nagpur-Mumbai Expressway.

Smart Transportation Industry Overview

As the market penetration of the smart transportation industry is relatively low, firms are poised to offer products and solutions that are tailor-made to specific segments and even customize products for individual customers, enhancing differentiation and price realization. The major participants in the smart transportation business, like Cisco, SAP SE, IBM, etc., are focusing on growing their operations in new areas. These companies have a track history of developing novel and inventive ideas to expand their product lines in the smart transportation sector. Overall, the industry's intensity of competitive rivalry is expected to be high during the forecast period.

- November 2022 - Alstom and Kazakhstan Railways (KTZ) signed a cooperation agreement. Alstom and KTZ strengthened their partnership in the renewal of KTZ's locomotive fleet and maintenance support, which includes the next-generation locomotive KZ8A. Currently, 90 freight and 39 passenger locomotives are in commercial service, with 160 freight and 80 passenger locomotives scheduled to be manufactured and delivered for KTZ.

- October 2022 - Siemens and 16 partners started a project likely to last through the end of 2024 to enhance artificial intelligence in the autonomous operation of regional trains. A budget of EUR 23 million (USD 25 million) within the German government-funded "safe.trAIn" project is available for this project. Meeting the requirements in this highly governed and standardized environment can significantly improve the efficiency and sustainability of regional railway transportation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Intensity of Competitive Rivalry

- 4.2.5 Threat of Substitute Products

- 4.3 Industry Value Chain Analysis

- 4.4 Impact of Macroeconomic Trends on the Market

- 4.5 Technology Snapshot

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rise of Urbanization and Increasing Mega Cities and Increasing Population

- 5.1.2 Government Initiatives to Enhance the Transportation Infrastructure

- 5.2 Market Restraints

- 5.2.1 High Capital Required for Deployment

6 MARKET SEGMENTATION

- 6.1 By Application

- 6.1.1 Traffic Management

- 6.1.2 Road Safety and Security

- 6.1.3 Parking Management

- 6.1.4 Public Transport

- 6.1.5 Automotive Telematics

- 6.1.6 Freight

- 6.1.7 Other Applications

- 6.2 By Product Type

- 6.2.1 Advanced Traveler Information Systems (ATIS)

- 6.2.2 Advanced Transportation Management Systems (ATMS)

- 6.2.3 Advanced Transportation Pricing Systems (ATPS)

- 6.2.4 Advanced Public Transportation Systems (APTS)

- 6.2.5 Cooperative Vehicle Systems

- 6.3 By Geography

- 6.3.1 North America

- 6.3.1.1 United States

- 6.3.1.2 Canada

- 6.3.2 Europe

- 6.3.2.1 United Kingdom

- 6.3.2.2 Germany

- 6.3.2.3 France

- 6.3.2.4 Rest of Europe

- 6.3.3 Asia Pacific

- 6.3.3.1 China

- 6.3.3.2 Japan

- 6.3.3.3 Australia

- 6.3.3.4 Rest of the Asia Pacific

- 6.3.4 Latin America

- 6.3.4.1 Mexico

- 6.3.4.2 Brazil

- 6.3.4.3 Rest of Latin America

- 6.3.5 Middle East and Africa

- 6.3.5.1 United Arab Emirates

- 6.3.5.2 South Africa

- 6.3.5.3 Saudi Arabia

- 6.3.5.4 Rest of Middle East and Africa

- 6.3.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Cisco Systems Inc.

- 7.1.2 SAP SE

- 7.1.3 IBM Corporation

- 7.1.4 AVEVA Group PLC

- 7.1.5 Siemens Corporation

- 7.1.6 Oracle Corporation

- 7.1.7 Alstom

- 7.1.8 Advantech Co. Ltd

- 7.1.9 Orange SA

- 7.1.10 Huawei Technologies Co. Ltd

- 7.1.11 Hitachi Ltd

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

智慧交通技术:各种技术与市场

智慧交通技术:各种技术与市场 2025-2033 年日本智慧交通市场报告(按解决方案和服务、交通模式、应用和地区划分)

2025-2033 年日本智慧交通市场报告(按解决方案和服务、交通模式、应用和地区划分) 智慧交通市场:按组成部分、交通类型、技术、应用划分 - 2025-2030 年全球预测

智慧交通市场:按组成部分、交通类型、技术、应用划分 - 2025-2030 年全球预测 全球智慧交通市场(2024-2028)

全球智慧交通市场(2024-2028) 智慧交通市场规模、份额和成长分析:按铁路、按运输方式、按通讯技术、按地区 - 产业预测,2024-2031 年

智慧交通市场规模、份额和成长分析:按铁路、按运输方式、按通讯技术、按地区 - 产业预测,2024-2031 年 2024-2032 年智慧交通市场报告(按解决方案、服务、交通模式、应用和地区)

2024-2032 年智慧交通市场报告(按解决方案、服务、交通模式、应用和地区) 智慧交通市场 - 按应用、产品类型、地区和竞争细分的全球产业规模、份额、趋势、机会和预测,2019-2029 年

智慧交通市场 - 按应用、产品类型、地区和竞争细分的全球产业规模、份额、趋势、机会和预测,2019-2029 年 全球智慧交通市场研究报告 - 2024 年至 2032 年产业分析、规模、份额、成长、趋势和预测

全球智慧交通市场研究报告 - 2024 年至 2032 年产业分析、规模、份额、成长、趋势和预测 2024 年智慧交通全球市场报告

2024 年智慧交通全球市场报告 智慧交通市场、份额、规模、趋势、产业分析报告:按交通方式、按解决方案、按服务、按地区、细分市场预测,2024-2032

智慧交通市场、份额、规模、趋势、产业分析报告:按交通方式、按解决方案、按服务、按地区、细分市场预测,2024-2032