|

市场调查报告书

商品编码

1403809

汽车活塞引擎系统 - 2024年至2029年市场占有率分析、产业趋势与统计、成长预测Automotive Piston Engine System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

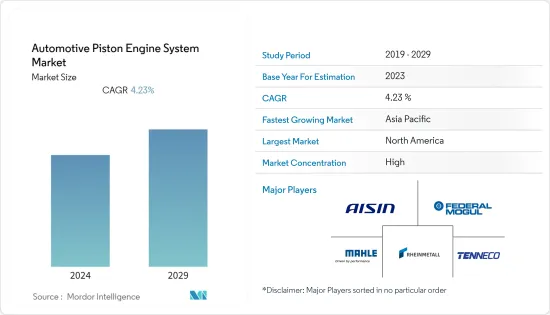

汽车活塞引擎系统市场目前价值42.6亿美元。

预计未来五年将达52.4亿美元,复合年增长率为4.23%。

主要汽车製造商和目标商标产品製造商 (OEM) 的引擎创新和原型设计,加上消费者对高性能和节能车辆的偏好,是推动市场成长的一些关键因素。小型引擎的趋势正在兴起,汽车製造商正在开发具有更好燃油喷射系统的小型引擎。此外,汽车产业将轻量化零件融入车型的快速转型正在推动汽车活塞引擎系统市场的成长。这是由于技术进步和多个零件製造商致力于开发有助于提高车辆效率的先进活塞。

随着越来越多的政府专注于推广普及电动车作为减少二氧化碳排放的措施,燃油动力车的销售趋势正在受到显着影响。电动车中是否包含活塞是可选的,这给汽车活塞引擎系统市场带来了重大挑战。同时,由于汽车持有的增加,活塞系统的生产在售后市场管道中越来越受欢迎。购买二手车的消费者总是需要对汽车的零件进行升级。这些对汽车活塞引擎系统市场的需求产生正面影响。

中国、印度和日本正在成为世界汽车製造商的成长中心,而亚太地区液化石油气 (LPG)、压缩天然气 (CNG) 和柴油引擎等替代燃料汽车的产量正在增加。因此,预计将继续作为汽车活塞系统的主要市场。此外,新兴市场预计将看到各种轻质活塞零件市场的进一步开拓,以提高车辆效率和燃油效率。

汽车活塞引擎系统市场趋势

小客车领域预计将主导市场

越来越多的消费者更喜欢液化石油气压缩天然气汽车等替代燃料汽车,这预示着活塞发动机系统市场的成长。各汽车製造商不断花费大量资金开发新时代汽车,汽车上使用的轻量化活塞零件有需求。同时,一些地区对二手车的需求正在增加,并且由于消费者偏好使用私人交通途径而导致汽车持有的增加对汽车活塞发动机系统市场的需求产生了积极影响。随着车辆老化并持续需要升级,燃油汽车售后市场中活塞系统的改造预计将推动该细分市场的市场发展。

另一方面,电动车销量的增加正在阻碍汽车活塞系统市场的成长。销售量的快速成长是各个组织和政府加强监管标准以控制废气水平和普及零排放汽车的结果。因此,汽车製造商持续致力于增加电动车研发支出。

自2018年以来,全球电动车市场(包括纯电动车、燃料电池电动车和插电式混合)的註册车销量每年都大幅成长。几乎所有细分市场都出现了这一成长,包括小客车和商用车。例如

- 2022年全球纯电动车(BEV)销量达730万辆,而2021年为460万辆,2021年至2022与前一年同期比较增58.7%。

在预测期内,汽车产业的电动车可能会成为市场的主要抑制因素,因为人们对电动车的偏好不断增加,政府提供补贴,以及对自动化和排放的需求不断增长。

亚太地区将在预测期内主导市场

预计在预测期内,亚太地区将成为汽车活塞引擎系统市场的领先地区。这主要是由于严重依赖内燃机,特别是在商用车领域。例如

- 2022年印度商用车与前一年同期比较为93.3万辆,而2021年为67.7万辆,2021年至2022年年增37.8%。

- 同样, 与前一年同期比较22.7万辆。

在亚太地区,电动商用车近年来已成为驱动力,但内燃机商用车市场在2022年仍将保持强劲。然而,由于内燃机商用车在亚太市场的普及不断提高,汽车活塞引擎系统市场的成长在未来几年可能会放缓。

都市化的提高、汽车持有的增加以及消费者人均可支配收入的增加正在推动亚太汽车市场的发展。随着越来越多的消费者迁移到都市区寻找更好的工作和经济机会,对使用私人交通的偏好不断增加,对该地区的小客车市场产生了积极影响。这对该地区的小客车市场产生正面影响,也对该地区的定位引擎系统市场产生正面影响。

儘管电动车的普及不断加速,活塞製造商在售后市场上仍然有巨大的机会来迎合燃油动力二手车的消费者。在亚太地区,儘管人们越来越倾向于电动车,但由于传统电动车市场庞大,预计汽车活塞引擎系统在预测期内的成长潜力将很高。

汽车活塞引擎系统产业概况

汽车活塞引擎系统市场整合且竞争激烈,只有少数公司占据市场主导地位。市场上营运的一些主要企业包括爱信精机、辉门控股有限责任公司、马勒有限公司、天纳克公司、莱茵金属汽车股份公司、日立汽车系统和理研公司。这些参与企业正在积极努力与汽车製造商建立长期合作伙伴关係,透过为汽油和柴油车提供各种活塞零件来加强其品牌组合。

- 2023年1月,莱茵金属正式将大直径活塞的生产转移至瑞典哥德堡的Koncentra Verkstads AB (KVAB)。 2022年10月,莱茵金属宣布了此次出售。这反映了杜塞尔多夫技术集团的策略转变,专注于小缸径活塞的开发。

- 2022年8月,日本活塞环与理研株式会社宣布签署谅解备忘录(MoU)协议,透过相互股权转让方式成立联合控股公司。两家公司将在同等条件下整合。根据协议,新合资企业的商号将为 NPR-Riken Corporation。该公司旨在加速汽车行业先进定位解决方案的开发。

预计市场将在未来几年内推出各种先进的轻型活塞部件,这些参与企业希望透过多样化的产品系列来竞争。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 调查先决条件

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场动态

- 市场驱动因素

- 对轻质活塞的需求不断增加

- 市场抑制因素

- 电动车普及阻碍市场成长

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买家/消费者的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争公司之间敌对关係的强度

第五章市场区隔(市场规模-美元)

- 依原料类型

- 铸铁

- 铝合金

- 其他原料(例如钢材)

- 按车型

- 小客车

- 商用车

- 按燃料

- 汽油

- 柴油引擎

- 按成分

- 活塞

- 活塞环

- 活塞销

- 按地区

- 北美洲

- 美国

- 加拿大

- 北美其他地区

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 欧洲其他地区

- 亚太地区

- 印度

- 中国

- 日本

- 韩国

- 其他亚太地区

- 世界其他地区 中东/非洲

- 南美洲

- 中东/非洲

- 北美洲

第六章竞争形势

- 供应商市场占有率

- 公司简介

- Aisin Seiki

- Capricorn Automotive

- Federal Mogul Holding LLC

- Mahle GmbH

- Rheinmetall

- Hitachi Automotive Systems

- Shriram Pistons & Rings Ltd

- Magna International

- Tenneco Inc

- Riken Corporation

- PT Astra Otoparts Tbk

第七章 市场机会及未来趋势

- 由于二手汽油/柴油车的成长,售后市场的机会不断扩大

The automotive piston engine system market is valued at USD 4.26 billion in the current year. It is anticipated to reach a net valuation of USD 5.24 billion within the next five years, registering a CAGR of 4.23% over the forecast period.

Innovations and prototypes of engines from major automakers and original equipment manufacturers (OEMs), coupled with consumer preferences for high-performance and fuel-efficient automobiles, are some of the major factors propelling the market growth. Engine downsizing trends are on the rise, with automakers developing smaller engines with better fuel injection systems. Further, the rapid transformation of the automotive industry in integrating lightweight components in their vehicle models is propelling the growth of the automotive piston engine system market. It is owing to the enhancement in technology and commitment by several parts and component manufacturers to develop advanced pistons, which assist in improving vehicle efficiency.

With the increasing focus of the government to promote the usage of electric vehicles to combat carbon emissions, the sales trends of fuel-operated vehicles are significantly being affected. It poses a major challenge for the automotive piston engine system market, as the integration of pistons in electric vehicles is optional. On the other hand, the production of piston systems is gaining traction in the aftermarket channels, owing to the growth in vehicle parc. Consumers availing of used cars are constantly in need of upgrading their vehicle's parts and components. These positively impact the demand for the automotive piston engine systems market.

With China, India, and Japan growing as global automotive manufacturer hubs, the Asia-Pacific region is expected to continue as a major market for automotive piston systems due to the increase in manufacturing of alternative fuel vehicles such as liquefied petroleum gas (LPG), compressed natural gas (CNG), and diesel engines. Further, the market is anticipated to witness the development of various lightweight piston components to improve the efficiency of vehicles and better fuel consumption capability.

Automotive Piston Engine System Market Trends

Passenger Car Segment is Anticipated to Dominate the Market

Increasing preference of consumers to avail alternative fuel vehicles, such as LPG CNG operated cars, is anticipated the growth of the piston engine system market. Various auto manufacturers are constantly spending hefty sums in developing new-age vehicles, which require lightweight piston components to be utilized in the vehicles. Coupled with that, the growing demand for used cars in several regions and increasing vehicle parc, owing to consumers' preference towards availing private transportation medium, is positively impacting the demand for automotive piston engine system market. The increasing age of vehicles requires constant upgradation, and therefore, changing piston systems in the aftermarket for fuel-operated vehicles is expected to drive this segment of the market.

On the other hand, the rise in sales of electric vehicles is hindering the growth of the automotive piston system market. The spike in sales is the result of an increase in regulatory norms by various organizations and governments to control emission levels and to propagate zero-emission vehicles. As a result, automakers are continually working and focusing on increasing their expenditure on the R&D of electric vehicles, which may aid OEMs in marketing electric vehicles in the future.

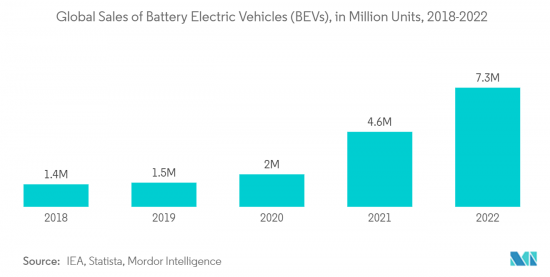

The global electric vehicles (including battery electric vehicles, fuel cell electric vehicles, and plug-in hybrid vehicles) market observed a tremendous increase in the number of sales registered every year since 2018. This increase was registered in almost all segments of vehicles, which include passenger vehicles and commercial vehicles. For instance-

- In 2022, global sales of battery electric vehicles (BEVs) touched 7.3 million units, compared to 4.6 million units in 2021, representing a 58.7% Y-o-Y growth between 2021 and 2022.

With the increased inclination toward electric vehicles, governments of different countries offering subsidies, and the growing need for automation and reduced emissions, the electrification of the automotive industry will serve as a major restraint for the market during the forecast period.

Asia-Pacific to Dominate the Market during the forecast period

Asia-Pacific region is projected to be the leading region for the automotive piston engine system market during the forecast period. It is mainly due to the heavy reliance on internal combustion engines, especially in the commercial vehicles sector. For instance,

- In 2022, India witnessed sales of 933 thousand units of commercial vehicles, compared to 677 thousand units in 2021, recording a Y-o-Y growth of 37.8% between 2021 and 2022.

- Similarly, new sales of commercial vehicles in Indonesia touched 264 thousand units in 2022, compared to 227 thousand units in 2021, representing a 16.3% Y-o-Y between 2021 and 2022.

Although electric commercial vehicles in the Asia-Pacific region gained traction in recent years, the market of ICE commercial vehicles remained strong as of 2022. However, with the increasing penetration of ICE commercial vehicles in the Asia-Pacific market, the automotive piston engine system market might witness falling growth in the coming years.

The increasing urbanization rate, growing vehicle parc, and the rising per capita disposable income of consumers are driving the automotive market in the Asia-Pacific region. As more consumers migrate to urban for better employment and financial opportunities, the preference towards availing private transportation medium shoots up, which positively impacts the passenger car market in the region. It, in turn, positively impacts the position engine system market in this region.

Despite the ramping penetration of electric vehicles at a faster rate, there remains a massive potential in the aftermarket for piston manufacturers to cater to consumers who avail of fuel-operated used cars. With the immense market for conventional IC engines in the regions, despite the growing inclination toward electric vehicles, the growth potential for automotive piston engine systems is expected to be high in Asia-Pacific during the forecast period.

Automotive Piston Engine System Industry Overview

The automobile piston engine system market is consolidated and highly competitive, with only a few companies dominating the market. Some of the major companies operating in the market are Aisin Seiki, Federal-Mogul Holding LLC, Mahle GmbH, Tenneco Inc, Rheinmetall Automotive AG, Hitachi Automotive Systems, and Riken Corporation, among others. These players actively engage in forming long-term partnerships with auto manufacturers to enhance their brand portfolio by offering various piston components for gasoline or diesel vehicles.

- In January 2023, Rheinmetall officially transferred its large-bore pistons production to Koncentra Verkstads AB (KVAB) of Gothenburg, Sweden. In October 2022, Rheinmetall announced the sale, which reflected the Dusseldorf tech group's strategic reorientation towards an improved focus on developing small-bore pistons.

- In August 2022, Nippon Piston Ring and Riken Corporation announced a Memorandum of Understanding (MoU) agreement to establish a joint holding company formed by mutual stock transfer. It is to consolidate the two companies on equal terms. As per the agreement, the trading name of the new joint company will be NPR-Riken Corporation. The company aims to facilitate the development of advanced position solutions for the automotive industry.

The market is anticipated to witness the launch of various advanced lightweight piston components in the coming years as these players try to gain a competitive edge with the diversification of their product portfolio.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Growing Demand for Lightweight Pistons

- 4.2 Market Restraints

- 4.2.1 Increasing Adoption of Electric Vehicles Deters the Growth of the Market

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size in Value - USD)

- 5.1 By Raw Material Type

- 5.1.1 Cast Iron

- 5.1.2 Aluminum Alloy

- 5.1.3 Other Raw Materials (Steel, etc.)

- 5.2 By Vehicle Type

- 5.2.1 Passenger Cars

- 5.2.2 Commerical Vehicles

- 5.3 By Fuel Type

- 5.3.1 Gasoline

- 5.3.2 Diesel

- 5.4 By Component Type

- 5.4.1 Piston

- 5.4.2 Piston Ring

- 5.4.3 Piston Pin

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Spain

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 India

- 5.5.3.2 China

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 Rest of the World

- 5.5.4.1 South America

- 5.5.4.2 Middle-East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles*

- 6.2.1 Aisin Seiki

- 6.2.2 Capricorn Automotive

- 6.2.3 Federal Mogul Holding LLC

- 6.2.4 Mahle GmbH

- 6.2.5 Rheinmetall

- 6.2.6 Hitachi Automotive Systems

- 6.2.7 Shriram Pistons & Rings Ltd

- 6.2.8 Magna International

- 6.2.9 Tenneco Inc

- 6.2.10 Riken Corporation

- 6.2.11 PT Astra Otoparts Tbk

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Rising Opportunity in the Aftermarket owing to the Growth in Used Gasoline/Diesel Cars

按车辆类型、引擎类型、材质、分销管道和活塞设计分類的汽车活塞系统市场 - 全球预测(2025-2032 年)

按车辆类型、引擎类型、材质、分销管道和活塞设计分類的汽车活塞系统市场 - 全球预测(2025-2032 年) 2025年全球钢活塞市场报告

2025年全球钢活塞市场报告 汽车活塞引擎系统市场预测至2032年:按组件、引擎类型、车辆类型、燃料类型、销售管道和地区进行的全球分析

汽车活塞引擎系统市场预测至2032年:按组件、引擎类型、车辆类型、燃料类型、销售管道和地区进行的全球分析 全球汽车活塞市场(至 2035 年)按形状(平顶、碗状、圆顶)、材质(钢、铝)、涂层(隔热层、干膜、脱油)、零件(销、环、头)、燃料类型、车辆类型、售后零件和地区划分2025年活塞全球市场报告2025年全球汽车活塞市场报告

全球汽车活塞市场(至 2035 年)按形状(平顶、碗状、圆顶)、材质(钢、铝)、涂层(隔热层、干膜、脱油)、零件(销、环、头)、燃料类型、车辆类型、售后零件和地区划分2025年活塞全球市场报告2025年全球汽车活塞市场报告 汽车活塞市场规模、份额及成长分析(按零件、车型、材料、涂层、燃料类型、几何形状和地区)-2025-2032 年产业预测

汽车活塞市场规模、份额及成长分析(按零件、车型、材料、涂层、燃料类型、几何形状和地区)-2025-2032 年产业预测 汽车活塞销市场,按燃料类型、按车辆类型、按配销通路、按国家和地区 - 2025 年至 2032 年的行业分析、市场规模、市场份额和预测

汽车活塞销市场,按燃料类型、按车辆类型、按配销通路、按国家和地区 - 2025 年至 2032 年的行业分析、市场规模、市场份额和预测 气动活塞振动器市场规模、份额、成长分析(按产品类型、按安装类型、按工作压力、按尺寸、按功能、按应用、按最终用途行业、按地区)- 行业预测,2025 年至 2032 年

气动活塞振动器市场规模、份额、成长分析(按产品类型、按安装类型、按工作压力、按尺寸、按功能、按应用、按最终用途行业、按地区)- 行业预测,2025 年至 2032 年 2025 年至 2033 年汽车活塞市场报告(按材料类型、车辆类型、活塞涂层类型、活塞类型、配销通路和地区)

2025 年至 2033 年汽车活塞市场报告(按材料类型、车辆类型、活塞涂层类型、活塞类型、配销通路和地区)