|

市场调查报告书

商品编码

1403949

工业马达:市场占有率分析、产业趋势与统计、2024-2029 年成长预测Industrial Motors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

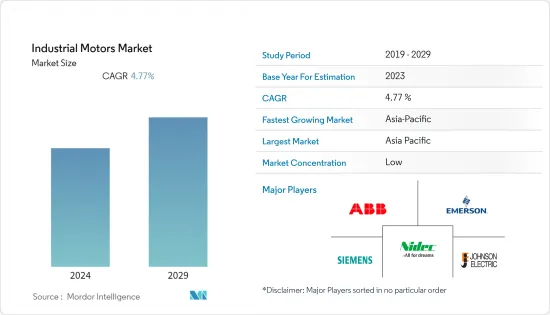

预计2024年工业马达市场规模为212.9亿美元,2029年将达281.7亿美元,预测期内复合年增长率为4.77%。

新兴市场产业部门的扩张、先进机械和自动化的普及正在支持市场成长。

主要亮点

- 电机是工业生产的重要动力。设计和开发工业马达的全新先进方法包括对准、马达监控、连接、测试、节省成本和时间等要素,同时提高安全性。节能马达和智慧型驱动器还可以提高效率和性能,同时使故障排除更加容易。

- 对工业 4.0 的日益关注主要推动了工业电机市场的发展。工业自动化正在推动多个地区製造业生产力的提高,预计需求强劲。根据工业能源加速器的数据,多个产业消耗的全部电能中近 70% 是由世界各地安装的数百万台电动马达使用的。这些趋势推动了对提高工业马达能效的创新的需求。

- 此外,产业参与者正专注于扩大製造业务,进一步推动市场成长。例如,2022年7月,三菱电机向其子公司Mitsubishi Electric India Pvt. Ltd.投资约31亿日元(20,753,139美元)或2180万欧元(23,078,570美元),在印度建设新工厂,并宣布将提供资金来建构其他活动计划于2023年12月开始,新工厂将生产逆变器和其他工厂自动化(FA)控制系统产品,以增强公司满足印度强劲需求的能力。这些案例可能为该地区研究市场的成长提供良好的前景。

- 在工业应用中,AC马达通常更可靠并且需要更少的维护。AC马达不需要换向器、电刷或滑环,因此不存在经常磨损的零件。这使得交流马达非常适合不易接近、可以连续运作或长时间无人监管的应用。此外,重要的市场趋势之一是开拓具有高功率重量比的工业马达。由于大型电动存在便携性和高能耗的问题,一些製造商正在开发高功率重量比的电动。

- 然而,工业马达的高安装和维护成本等挑战正在影响所研究市场的成长,特别是在价格敏感的新兴市场。

- 研究市场宏观经济因素的影响也更大,因为工业部门的投资很大程度上受到製成品市场需求、地区总体经济状况和地缘政治局势等因素的影响。因此,预计这些因素将继续在确定预测期内研究市场的成长轨迹方面发挥关键作用。

工业马达市场趋势

低压占较大市场占有率

- 低压马达的行业标准差异很大。一些製造商更改了低压马达的分类。根据 IEC 600038 标准(国际电工委员会),所有额定功率电压不超过 1000 伏特的马达被视为低电压 (LV)。

- 与市场上的其他马达相比,低压引擎在多个行业中具有广泛的应用。低压马达的典型应用包括中游和下游石油和天然气、水、污水、食品以及食品和食品和饮料产业。

- 多功能低压马达采用经济实惠的标准设计,易于安装和快速启动,具有高生产率、高可靠性、更高的安全性和高效的电力使用。低压电机也可以设计用于没有专门开发的引擎的应用。欧盟委员会的生态设计法规最近透过实施和建立 IEC(国际电工委员会)定义的国际效率等级 (IE) 来解决低压电机问题。这些规定使 IE3 成为最低标准,使 IE5 成为独特的超高级额定功率,其中还包括具有变速驱动器的马达。

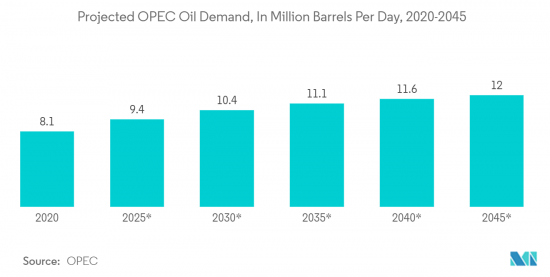

- 此外,由于油价上涨,石油和天然气行业对低压马达的强劲需求预计将在预测期内恢復。例如,根据OPEC的数据,到2045年,OPEC国家的石油需求预计将从810万桶/日增加到1,200万桶/日。鑑于这些趋势,各公司正在专注于为石油和天然气行业开发低压马达解决方案,以抓住新的成长机会。

亚太地区正在经历显着成长

- 製造业是亚太地区尤其是中国经济的支柱之一,正经历快速转型。这一重大转变使该国处于市场领先地位。在过去的二十年里,中国製造商的能力已从生产低成本产品发展到生产更复杂的产品,但强大的工业机械和马达仍然至关重要。

- 智慧製造措施预计也将推动工业马达在该国的采用。根据工业和资讯化部介绍,中国政府已启动多个智慧製造试点计划。 「十三五」规划目标是到2025年建立智慧型製造体系,完成重点产业转型。由于这些倡议,汽车製造商正在扩大其在中国的製造设施,为预测期内的工业马达需求提供了积极的前景。

- 其他国家也出现了类似的趋势。例如,2022年10月,印度政府宣布将透过国际竞标竞标探勘开发42个油气田。印度打算在2025年将其石油和天然气勘探和生产面积增加一倍,达到50万平方公里,到2030年增加到100万平方公里,增加国内产量,减少对进口燃料的依赖。我是。这为石油和天然气行业的工业电机需求创造了良好的前景。工业马达在上游石油和天然气产业中发挥重要作用,广泛用于驱动泵浦和压缩机系统等设备。

- 此外,在跨国公司寻求向中国境外扩张的投资增加的推动下,东南亚工业部门近年来也取得了显着发展。泰国、马来西亚和印尼等国家正迅速崛起为该地区的主要工业国家,预计将有利于预测期内东南亚研究市场的成长。

工业马达产业概况

工业电机市场包括ABB集团、西门子股份公司、艾默生电气有限公司和Johnson Electric。虽然透过创新获得永续的竞争优势是可能的,但企业在市场竞争中脱颖而出变得越来越困难。供应商高度集中,买家可以从众多供应商中进行选择。儘管市场上的参与者多种多样,但拥有高标准、高品质和全球影响力的参与者仍然屈指可数。

2023年7月,Electrified Automation推出了新系列电动马达。这种新的马达架构旨在为寻求可靠且响应迅速的供应链的OEM最大限度地提高自动化和大量生产潜力。此外,新型 EA 193 系列永磁电动支援从工业到两轮公路式的广泛应用。

2023年6月,ABB开发出新一代AMI 5800 NEMA模组化感应电动机。 AMI 5800 马达旨在为泵浦、风扇、压缩机、挤出机、输送机和破碎机等要求严苛的应用提供可靠性和能源效率,可提供高达1750 HP 的功率,是采矿、化学石油和天然气的理想选择,它具有高度可自订性和模组化,适用于多种行业的应用,包括传统发电、水泥和金属等。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买家/消费者的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争公司之间敌对关係的强度

- 宏观趋势对工业马达市场的影响

第五章市场动态

- 市场驱动因素

- 政府法规对能源效率的需求

- 越来越多地转向智慧电机

- 市场挑战

- 便携性问题

- 购买新设备和升级现有设备的初始投资较高

第六章市场区隔

- 依马达类型

- 交流 (AC) 电机

- 直流 (DC) 电机

- 其他马达(伺服马达和电子换向器马达(EC马达)

- 按电压

- 高电压

- 中压

- 低电压

- 按最终用户

- 油和气

- 发电

- 矿业/金属

- 用水和污水管理

- 化工/石化

- 离散製造

- 其他最终用户

- 按地区

- 北美洲

- 美国

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 欧洲其他地区

- 亚太地区

- 中国

- 日本

- 印度

- 其他亚太地区

- 拉丁美洲

- 巴西

- 阿根廷

- 其他拉丁美洲

- 中东/非洲

- 沙乌地阿拉伯

- 南非

- 其他中东/非洲

- 北美洲

第七章竞争形势

- 公司简介

- ABB Ltd.

- Emerson Electric Co.

- Siemens

- Nidec Industrial Solutions

- Johnson Electric Holdings Limited

- Arc Systems Inc.

- Ametek Inc.

- Toshiba Electronic Devices and Storage Corporation

- Wolong Industrial Motors

- Allen-Bradly Co. LLC(Rockwell Automation Inc.)

- Maxon Motor AG

- Franklin Electric Co. Inc.

- Fuji Electric Co. Ltd

- ATB Austria Antriebstechnik AG

- Menzel Elektromotoren GmbH

第八章投资分析

第9章市场的未来

The Industrial Motors Market size is estimated at USD 21.29 billion in 2024 and is expected to reach USD 28.17 billion by 2029, registering a CAGR of 4.77% during the forecast period. The expanding footprint of the industrial sector across developing regions, along with the growing penetration of advanced machinery and automation, supports the studied market's growth.

Key Highlights

- Motors are the significant driving force of industrial production. The new and advanced approaches for designing and developing industrial motors include factors like alignment, motor monitoring, connections, testing, and saving costs and time while improving safety and security. Energy-saving motors and intelligent drives also boost efficiency and performance while facilitating troubleshooting.

- The growing focus on Industry 4.0 primarily drives the market for industrial motors. Industrial automation drives the manufacturing sector toward more productivity in several regions, expecting to show strong demand. According to Industrial Energy Accelerator, nearly 70% of all electrical energy consumed by several industries is used by the millions of electrical motors installed globally. Such trends drive the demand for innovations in industrial motor technology to make them energy efficient.

- The industry players also focus on expanding their manufacturing operations, further supporting the market growth. For instance, in July 2022, Mitsubishi Electric Corporation revealed that it would fund the construction of a new factory in India by investing roughly JPY 3.1 billion (USD 20753139), or EUR 21.8 million (USD 23078570), in its subsidiary Mitsubishi Electric India Pvt. Ltd. The new facility, whose activities are scheduled to begin in December 2023, will likely produce inverters and other factory automation (FA) control system goods, enhancing the company's capacity to satisfy India's booming demand. Such an instance will create a favorable outlook for the growth of the studied market in the region.

- In Industrial applications, AC motors are generally more reliable with low maintenance requirements, and the bearing life frequently limits the service life of AC motors. Since the motors do not need commutators, brushes, or slip rings, they don't have parts that wear out regularly. This factor makes the motors ideal for applications that are not easily accessible, continuously available to operate, or will work without supervision for long periods. Furthermore, one critical trend in the market is the development of high power-to-weight ratio industrial motors. Several manufacturers are developing electric motors with a high power-to-weight ratio, as large electric motors have portability and high energy consumption issues.

- However, factors such as the higher installation and maintenance cost of industrial motors challenge the growth of the studied market, especially in developing markets, wherein price sensitivity is higher.

- The impact of macroeconomic factors is also on the higher side in the studied market, as investments in the industrial sector are largely influenced by factors such as the market demand for manufactured products, the general economic condition of the region, and the geopolitical situation. Hence, during the forecast period, these factors are anticipated to continue to play a pivotal role in determining the growth trajectory of the studied market.

Industrial Motors Market Trends

Low Voltage to Hold Significant Market Share

- The industry standards for low-voltage motors vary broadly. Several manufacturers have different motor classifications that are considered low-voltage motors. According to the IEC 600038 standard (International Electrotechnical Commission's), any motor rating up to 1000 volts is regarded as a low voltage (LV).

- Compared to other motors in the market, low-voltage engines have a wide range of applications across multiple industries. Some of the primary applications of low-voltage motors are in the mid-stream and downstream oil and gas, water, wastewater, food, and beverage industries, etc.

- Multi-purpose low voltage motors provide simple installation and quick start and have an affordable standardized design with high productivity, high reliability, increased safety, and very efficient electricity use. Low-voltage motors can also be designed for applications without a specially developed engine. The European Commission Ecodesign Regulation recently addressed this for low-voltage motors by enforcing and establishing (IE) International Efficiency classes defined by the IEC (International Electrotechnical Commission). It set IE3 as the minimum standard and IE5 as a unique ultra-premium rating, including motors with variable-speed drives.

- Additionally, over the forecast period, rising oil prices are expected to create a strong rebound demand for LV motors from the oil and gas industry. For instance, according to OPEC, crude oil demand in the OPEC member countries is anticipated to grow from 8.1 million barrels per day to 12 million barrels per day by 2045. Considering such trends, companies are now focusing on developing low-voltage motor solutions for the oil and gas sector to grab emerging opportunities, creating a favorable outlook for the growth of the studied market.

Asia-Pacific to Witness Significant Growth

- Manufacturing is one of the pillars of several countries of the Asia Pacific region, specifically of the Chinese economy, and is undergoing a rapid transformation. This large-scale transformation has put the country in a leading position in the market. Over the last two decades, Chinese manufacturers have evolved their capabilities from producing low-cost goods to creating more advanced products, wherein competent industrial machinery and motors remain pivotal.

- The adoption of industrial motors in the country is also expected to be driven by smart manufacturing initiatives. According to the Ministry of Industry and Information Technology, the Chinese government initiated several smart manufacturing pilot projects. As per the 13th five-year plan, the country aims to establish its intelligent manufacturing system and complete the critical industry transformation by 2025. As a result of such initiatives, automakers have been expanding their manufacturing facilities in China, creating a favorable outlook for the demand for industrial motors during the forecast period.

- A similar trend has been observed across other countries. For instance, the government of India, in October 2022, announced that it put up 42 oil and gas blocks for exploration and development through international competitive bidding. India will more than double the area under investigation and production of oil and gas to 0.5 million square kilometers by 2025 and 1 million sq. km. by 2030, intending to raise domestic output and cut reliance on imported fuel, thus creating a favorable outlook for demand for industrial motors in the oil and gas industry as industrial motors play a vital role in the upstream of the oil and gas industry and are widely used to drive equipment such as pump and compressor systems.

- Furthermore, in recent years, the industrial sector in Southeast Asia has also flourished significantly, driven by the growing investment by MNCs exploring destinations outside China. Countries such as Thailand, Malaysia, and Indonesia are fast emerging among the leading industrialized economies in the region, which is anticipated to favor the studied market's growth in Southeast Asia during the forecast period.

Industrial Motors Industry Overview

The industrial motor market is moving towards a fragmented stage, owing to the presence of a large number of companies, such as the ABB Group, Siemens AG, Emerson Electric Co. Inc., and Johnson Electric. Through innovation, sustainable competitive advantage can be attained, but it has become increasingly challenging for firms to differentiate themselves from market competition. Because the concentration of suppliers is high, buyers can choose among different vendors. Although the market comprises various players, a handful of them are still prominent for their high standards, excellent quality, and global reach.

In July 2023, Electrified Automation launched a new range of electric motors. The new motor architecture is designed to maximize the potential of automation and high-volume production for OEMs looking for a reliable, responsive supply chain. Furthermore, the new EA 193 Series permanent magnet electric motors will support a range of applications from industrial to two-wheel-on-road.

In June 2023, ABB developed the new generation AMI 5800 NEMA modular induction motor. Designed to offer reliability and energy efficiency in demanding applications such as pumps, fans, compressors, extruders, conveyors, and crushers, the AMI 5800 motor's power output of up to 1750 HP offers the capability of a high degree of customization and modularity to suit applications in a wide range of industries including mining, chemical oil and gas, conventional power generation, and cement and metals.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers/Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Impact of Macro Trends on the Industrial Motors Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Demand for Energy Efficiency Owing to Government Regulations

- 5.1.2 Growing Shift towards Smart Motors

- 5.2 Market Challenges

- 5.2.1 Portability Issues

- 5.2.2 High Initial Investment for Procuring New Equipment and Upgrading Existing Equipment

6 MARKET SEGMENTATION

- 6.1 By Type of Motor

- 6.1.1 Alternating Current (AC) Motors

- 6.1.2 Direct Current (DC) Motor

- 6.1.3 Other Types of Motors (Servo and Electronically Commutated Motors (EC))

- 6.2 By Voltage

- 6.2.1 High Voltage

- 6.2.2 Medium Voltage

- 6.2.3 Low Voltage

- 6.3 By End User

- 6.3.1 Oil and Gas

- 6.3.2 Power Generation

- 6.3.3 Mining and Metals

- 6.3.4 Water and Wastewater Management

- 6.3.5 Chemicals and Petrochemicals

- 6.3.6 Discrete Manufacturing

- 6.3.7 Other End Users

- 6.4 By Geography

- 6.4.1 North America

- 6.4.1.1 United States

- 6.4.1.2 Canada

- 6.4.2 Europe

- 6.4.2.1 United Kingdom

- 6.4.2.2 Germany

- 6.4.2.3 France

- 6.4.2.4 Rest of Europe

- 6.4.3 Asia-Pacific

- 6.4.3.1 China

- 6.4.3.2 Japan

- 6.4.3.3 India

- 6.4.3.4 Rest of Asia-Pacific

- 6.4.4 Latin America

- 6.4.4.1 Brazil

- 6.4.4.2 Argentina

- 6.4.4.3 Rest of Latin America

- 6.4.5 Middle East and Africa

- 6.4.5.1 Saudi Arabia

- 6.4.5.2 South Africa

- 6.4.5.3 Rest of Middle East and Africa

- 6.4.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 ABB Ltd.

- 7.1.2 Emerson Electric Co.

- 7.1.3 Siemens

- 7.1.4 Nidec Industrial Solutions

- 7.1.5 Johnson Electric Holdings Limited

- 7.1.6 Arc Systems Inc.

- 7.1.7 Ametek Inc.

- 7.1.8 Toshiba Electronic Devices and Storage Corporation

- 7.1.9 Wolong Industrial Motors

- 7.1.10 Allen - Bradly Co. LLC (Rockwell Automation Inc.)

- 7.1.11 Maxon Motor AG

- 7.1.12 Franklin Electric Co. Inc.

- 7.1.13 Fuji Electric Co. Ltd

- 7.1.14 ATB Austria Antriebstechnik AG

- 7.1.15 Menzel Elektromotoren GmbH

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

工业马达市场:按类型、组件、电压、输出功率、应用分类 - 2025-2030 年全球预测

工业马达市场:按类型、组件、电压、输出功率、应用分类 - 2025-2030 年全球预测 2024-2032 年按马达类型(交流马达、直流马达等)、电压、最终用户和地区分類的工业马达市场报告

2024-2032 年按马达类型(交流马达、直流马达等)、电压、最终用户和地区分類的工业马达市场报告 工业马达市场,按产品类型、电压、应用、最终用户、国家和地区 - 2024-2032 年行业分析、市场规模、市场份额和预测

工业马达市场,按产品类型、电压、应用、最终用户、国家和地区 - 2024-2032 年行业分析、市场规模、市场份额和预测 全球工业马达市场 - 2024年至2029年预测

全球工业马达市场 - 2024年至2029年预测 2030 年工业马达市场预测:按产品类型、相位、电压、效率、额定功率、最终用户和地区进行的全球分析

2030 年工业马达市场预测:按产品类型、相位、电压、效率、额定功率、最终用户和地区进行的全球分析 工业电机市场:按电机类型、电压、最终用户、地区 - 规模、份额、展望、机会分析,2023-2030 年

工业电机市场:按电机类型、电压、最终用户、地区 - 规模、份额、展望、机会分析,2023-2030 年