|

市场调查报告书

商品编码

1403953

金属盖瓶盖:市场占有率分析、产业趋势与统计、2024-2029 年成长预测Metal Caps & Closures - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

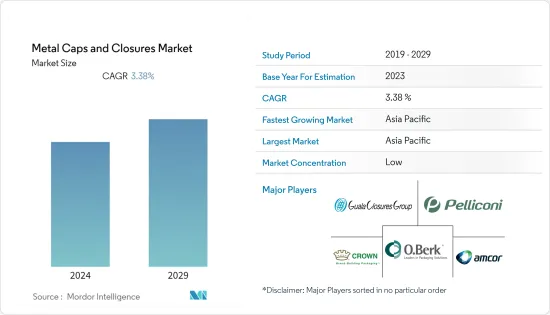

全球金属瓶盖市场规模预计未来五年将从上一年的 229.9 亿美元成长至 271.4 亿美元,预测期内复合年增长率为 3.38%。

金属盖和封闭件提供刚性和稳定性,同时向市场上的消费者展示良好的产品形象。

主要亮点

- 由于食品和饮料的增加,预计金属瓶盖市场将在预测期内迅速扩张。对酒精饮料、啤酒、麵包、家禽/鱼、已调理食品、乳製品等的需求正在增加。此外,由于塑胶法规的限制,软性饮料包装供应商更喜欢使用金属皇冠盖进行饮料包装,这推动了市场成长。

- 对使用环保产品的日益关注正在推动金属盖子与封口装置的采用。儘管塑胶瓶盖对金属瓶盖构成高度威胁,但塑胶瓶盖市场正面临环境问题的高度威胁。这为金属盖和封闭件创造了机会。近年来,一些公司已经用金属取代了塑胶瓶盖和瓶盖。

- 此外,金属盖子与封口装置可以印上标誌和其他设计,透过推广独特的品牌来增加需求。此外,自适应皇冠盖由独特的金属製成,与螺纹瓶颈结合时可提供最佳的配合。皇冠盖价格合理、功能强大、易于使用、快速使用,并提供真正的防篡改保护。

- 金属盖和封闭件也常用于製药业,因为它们是无菌的并且通常由多层材料製成。业界最常用的金属盖由钢和铝製成。此外,铝材有多种材质,包括普通铝材、压花铝材、彩色铝材和天然铝材。结果,可以根据消费者的需求提供药物包装。儿童用、付加和老年瓶盖市场预计将受到快速扩张的製药业和鼓励製造商生产优质瓶盖和瓶盖的监管改革的推动。

- 然而,其他由塑胶、木材等製成的封闭系统的存在预计将成为抑制因素,并在预测期内挑战金属封闭件市场的成长。

- 食品和饮料行业在金属盖子与封口装置市场中占有主要份额,由于该行业属于必需品类别,因此在 COVID-19 大流行期间见证了巨大的需求。特别是对包装食品、肉类、蔬菜和水果的需求不断增加。随着市场同时进一步适应当前情况,消费行为无疑将在预测期内继续改变。因此,从需求面来看,Covid-19之后金属盖子与封口装置市场的未来看起来很有希望。

金属盖瓶盖市场趋势

製药应用提供成长潜力

- 金属盖子与封口装置主要用于製药领域,因为它们是无菌的并且通常由层状材料组成。该领域主要使用钢製和铝製金属盖。铝也是高度可客製化的,包括本色、彩色、素色和压花选项。这样,药品包装就可以依照消费者的需求来供应。

- 药品销售和生产的快速成长以及监管变化预计将进一步有利于儿童用、付加和老年用药,从而在预测期内推动市场发展。世界卫生组织(WHO)估计,全世界销售的药品中有三分之一是非法的。假药风险的增加催生了对高效防伪解决方案的需求,并推动了防伪瓶盖的采用。

- 由于橡胶瓶盖容易污染药品,製药业越来越多采用铝瓶盖。污染源合成橡胶体容器的封闭部件。可能的污染物包括微生物、内毒素和化学物质。 2022 财年,166 个製造地发生了 912 起药品召回事件,为过去五年来的最高数量。

- 资料显示,这些召回最大的缺陷仍然是 CDER 每年报告的现行良好生产规范 (CGMP) 偏差。大多数召回产品是由于仓库的温度控制和储存问题造成的。报告强调,此类情况可能会导致产品劣化,并对保存期限、安全性和功效产生负面影响。

- 此外,由于现行的使用法规,糖浆瓶产业对金属盖和密封件的需求可能会面临一些挑战。草药(HMP)最近变得越来越重要,并广泛用于预防和治疗各种疾病。

亚太地区成长最快

- 由于中国和印度这两个人口大国的存在,亚太地区预计将成长最快。在这两个国家,可支配收入的增加预计将抵消金属盖子与封口装置市场的成长。

- 印度的饮料业(包括酒类)是最多元化的产业之一。该行业深受与天气相关的广大地区的影响。因此,容纳饮料、实现运输并保护其免受机械应力和材料损失的包装功能变得至关重要。根据北欧银行的研究,印度2020年的酒精消费量为48.6亿公升。预计2024年将达62.1亿升。

- 中国的烈酒市场不断扩大,对包装解决方案的需求很高。这些销售对于中国饮料包装製造商来说是一个巨大的机会。外国投资者认识到此类细分市场的巨大潜力。此外,来自中国的酒精饮料进口额的增加正在推动饮料瓶盖和瓶盖市场的发展。中国海关资料显示,2022年10月最新公布的资料显示,7月至9月,中国向北韩出口了价值近300万美元的葡萄酒和酒精饮料。

- 在消费者对永续性意识不断增强以及各相关人员兴趣日益浓厚的推动下,永续饮料包装趋势在东南亚正在加速发展。一些製造商选择用更永续的材料代替塑胶。

- 包装食品和食品和饮料的需求显着增加,以及瓶盖和密封件在长期保持包装消耗品新鲜方面发挥的重要作用,可能会提振这些地区的市场。

金属盖子与封口装置产业概览

由于国际供应商的存在,全球金属盖子与封口装置市场高度分散且竞争激烈。该市场的主要企业包括 Crown Holdings、O.Berk Company、Guala Closures SPA 和 Amcor PLC。市场在产品差异化、产品组合和定价方面竞争激烈。对付加瓶盖和砸道机的需求不断增长,将增加金属盖和瓶盖在各个领域的使用,特别是在製药和饮料领域。

2022 年 7 月,各类瓶子瓶盖製造商 Guala Closures 收购了位于维琴察的豪华瓶盖专家 Labrenta。此次收购对于 Guala Closures 来说非常重要,扩大了其在奢侈品领域的影响力,并有助于使其成为该行业的全球领导者。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场洞察

- 市场概况

- 产业价值链分析

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争公司之间的敌对关係

第五章市场动态

- 市场驱动因素

- 由于对永续包装材料的需求不断增长,饮料消费量增加

- 与其他封闭材料相比具有优越的性能

- 市场抑制因素

- 其他类型封闭材料的采用率较高

第六章市场区隔

- 依材料类型

- 铝

- 钢

- 锡

- 按闭合类型

- 皇冠帽

- 螺丝帽

- 扭曲金属帽

- 其他瓶盖(易开盖、ROPP金属盖)

- 按最终用户产业

- 食品

- 饮料

- 有酒精的饮品

- 非酒精性

- 药品

- 个人护理

- 其他最终用户产业

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东/非洲

第七章竞争形势

- 公司简介

- Crown Holdings Inc.

- O.Berk Company

- Guala Closures SPA

- Pelliconi & C. SpA

- Nippon Closures Co. Ltd

- Silgan White Cap LLC

- Sks Bottle & Packaging Inc.

- Amcor PLC

- Qorpak(Berlin Packaging)

- Alameda Packaging LLC

- Closure Systems International Inc(CSI)

第八章投资分析

第9章市场的未来

The Global Metal Caps And Closures market size is expected to grow from USD 22.99 billion in the previous year to USD 27.14 billion in the next five years, registering a CAGR of 3.38% during the forecast period. Metal caps and closures provide rigidity and stability while portraying a superior product image to the consumers in the market.

Key Highlights

- The market for metal caps and closures is predicted to expand rapidly during the forecast period due to the increased demand for food and beverages. There is a rising demand for alcoholic drinks, beer, bread, poultry and fish, ready-to-eat meals, dairy goods, etc. Moreover, due to plastic regulations, soft drink packaging vendors prefer metal crown caps for beverage packaging, driving the market growth.

- The growing concerns regarding the usage of environment-friendly products have boosted the adoption of metal caps and closures. Though plastic-based caps pose a high threat to metal caps, the plastic caps market is witnessing high threats regarding environmental problems. This has been creating the opportunity for metal caps and closures. Several companies in recent years have been replacing their plastic-based caps and closures with metal.

- Further, metal caps and closures can be branded with logos or other designs, increasing demand for them by promoting the distinctive brand. Moreover, the adaptable crown caps are composed of a unique metal that gives the optimum fit when combined with a threaded bottleneck. Crown caps are reasonably priced, very functional, simple to use, allow for high-speed application, and provide genuine tamper protection.

- Metal caps and closures are also often utilized in the pharmaceutical industry since they are sterile and typically made of multilayer materials. The most common metal caps used in the industry are comprised of steel and aluminum. Additionally, aluminum is made in various variations, including plain or embossed, colored, or natural. As a result, pharmaceutical packaging may be provided in accordance with consumer demand. The market for child-resistant, value-added, and senior-friendly closures is expected to be driven by the rapidly expanding pharmaceutical industry as well as regulatory reforms, which have encouraged manufacturers to produce superior-quality caps and closures.

- However, the presence of other closure systems made of plastics, wood, etc., is expected to act as a restraint and challenge the growth of the metal closures market over the forecast period.

- The food and beverage industry, with a major share in the metal caps and closures market, witnessed huge demand amidst the COVID-19 pandemic as the industry fell under the essential commodity. There was an increasing demand for packaged food products, meat, vegetables, and fruits, among others. Consumer behavior was to undoubtedly continue to change in the forecast period as the market simultaneously acclimated more to the current scenario. Thus, the post-COVID-19 future for the metal caps and closures market looks promising in terms of demand.

Metal Caps & Closures Market Trends

Pharmaceutical Application Offers Potential Growth

- Metal caps and closures are predominantly used in the pharmaceutical sector as they are sterile and are generally composed of layered material. Metals caps made of steel and aluminum are mostly used in the sector. Besides, aluminum can be highly customizable: natural or colored, plain or embossed. Thus, pharmaceutical packaging can be supplied according to the consumers' needs.

- The rapidly growing pharmaceutical sales and production and the regulatory changes further favor child-resistant, value-added, and senior-friendly closures, which are anticipated to drive the market in the foreseen period. The World Health Organization (WHO) estimated that one-third of all medicines sold worldwide are illegitimate. The increasing risks from falsified drugs are creating the need for efficient anti-counterfeiting solutions, boosting the adoption of anti-counterfeiting closures.

- The adaptation of aluminum closures in the pharmaceutical industry is on the rise, as its rubber counterparts tend to contaminate the drugs. The contamination is attributable to elastomeric container closure components. Possible contaminants include microorganisms, endotoxins, and chemicals. In the fiscal year 2022, 912 drug recalls were generated by 166 manufacturing sites, marking the highest number of recalls in the past five years.

- The data indicates that the largest defect group for these recalls remains current good manufacturing practice (CGMP) deviations, as reported in previous years by CDER. The majority of the products were recalled due to issues with temperature control and storage in warehouses. The report highlights the fact that these conditions can cause degradation of the product, leading to a negative impact on its shelf-life, safety, or effectiveness.

- Further, the demand for metal caps and closures may witness a few challenges in the syrup bottle sector owing to the regulations prevailing in their usage. Herbal medicinal products (HMP) have recently gained importance and are extensively used to prevent and treat various ailments.

Asia-Pacific to Witness the Fastest Growth

- Asia-Pacific is expected to witness the fastest growth because of the presence of two highly populated countries, i.e., China and India. In these two countries, the increase in disposable income will supplement the growth of the metal caps and closures market.

- The Indian beverage sector, consisting of alcohol, is one of the most diverse sectors. The industry is highly influenced by the country's vast geography associated with the weather. With it comes the imperative of packaging function to contain beverages, enabling transportation, and protecting beverages against mechanical stress and material loss. According to a study performed by Banco do Nordeste, alcohol consumption in India was 4.86 billion liters in 2020. The consumption is expected to reach 6.21 billion liters in 2024.

- China's spirits market is expanding continuously, leading to a high demand for packaging solutions. Such turnover represents an enormous opportunity for domestic producers in Chinese beverage packaging. Foreign investors have recognized the huge potential of such a market segment. Moreover, the growing import value of alcoholic drinks from China has boosted the market for caps and closures for beverages. Recent data published in October 2022 showed that China exported nearly USD 3 million of wine and liquor to North Korea from July to September, according to Chinese customs data.

- The trend for sustainable beverage packaging is accelerating in Southeast Asia, buoyed by greater consumer awareness of sustainability and increased focus by various stakeholders, with governments incentivizing a shift towards a circular economy and manufacturers focusing on recycling, packaging reduction, and the adoption of more sustainable packaging alternatives. Some manufacturers are opting to replace plastics with more sustainable materials.

- The vast rise in the demand for packaged foods and beverages and the critical role played by caps and closures in keeping packaged consumables fresh for extended periods are likely to boost the market in these regions.

Metal Caps & Closures Industry Overview

The global metal caps and closures market is highly fragmented and competitive due to the presence of international vendors. Some of the key players in this market are Crown Holdings, O.Berk Company, Guala Closures S.P.A., and Amcor P.L.C., amongst others. Intense competition prevails in the market in terms of product differentiation, portfolio, and pricing. The rising demand for value-added closures and tamper resistance properties will augment the usage of metal caps and closures in various segments, primarily pharmaceuticals and beverages.

In July 2022, Guala Closures, a company that produced closures for various types of bottles, acquired Labrenta, a high-end closure specialist based in Vicenza. This acquisition was crucial for Guala Closures as it helped the company expand its reach in the luxury segment, thus making it a world leader in the industry.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitutes

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Consumption of Beverages with a Rising Need for Sustainable Packaging Materials

- 5.1.2 Superior Properties Compared to Other Closure Materials

- 5.2 Market Restraints

- 5.2.1 High Adoption Rate of Other Types of Closure Materials

6 MARKET SEGMENTATION

- 6.1 By Material Type

- 6.1.1 Aluminium

- 6.1.2 Steel

- 6.1.3 Tin

- 6.2 By Closures Type

- 6.2.1 Crown Caps

- 6.2.2 Screw Caps

- 6.2.3 Twist Metal Caps

- 6.2.4 Other Closures Types (Easy Open Ends, ROPP Metal Caps)

- 6.3 By End-User Industry

- 6.3.1 Food

- 6.3.2 Beverages

- 6.3.2.1 Alcoholic

- 6.3.2.2 Non-Alcoholic

- 6.3.3 Pharmaceuticals

- 6.3.4 Personal Care

- 6.3.5 Other End-User Industries

- 6.4 By Geography

- 6.4.1 North America

- 6.4.2 Europe

- 6.4.3 Asia-Pacific

- 6.4.4 Latin America

- 6.4.5 Middle East and Africa

7 Competitive Landscape

- 7.1 Company Profiles

- 7.1.1 Crown Holdings Inc.

- 7.1.2 O.Berk Company

- 7.1.3 Guala Closures S.P.A.

- 7.1.4 Pelliconi & C. SpA

- 7.1.5 Nippon Closures Co. Ltd

- 7.1.6 Silgan White Cap LLC

- 7.1.7 Sks Bottle & Packaging Inc.

- 7.1.8 Amcor PLC

- 7.1.9 Qorpak (Berlin Packaging)

- 7.1.10 Alameda Packaging LLC

- 7.1.11 Closure Systems International Inc (CSI)