|

市场调查报告书

商品编码

1404393

资料准备:市场占有率分析、产业趋势/统计、2024-2029 年成长预测Data Preparation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

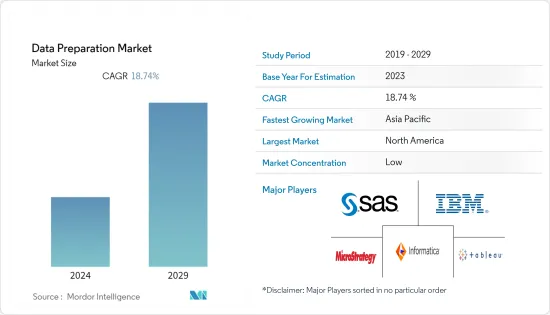

去年资料准备市场的市场规模为47.8亿美元,预计未来六年将达到135.1亿美元,预测期内复合年增长率为18.74%。

由于数位化颠覆,企业需要比以往更快的调试时间来产生有意义的见解,以便在市场中生存。因此,对分析(尤其是资料分析)的需求在组织中变得越来越普遍。随着资料来源复杂性的增加,资料分析专业人士和企业需要协助推动洞察。这极大地推动了组织中资料准备的需求。

主要亮点

- 自动化和云端技术在企业和企业中的快速采用导致了资料的产生和云端资料流量。据Cisco称,全球IP资料流量预计将达到每月333Exabyte。特别是对于大型内容服务提供者 (CSP) 而言,资料流量已从点对点 (P2P) 檔案共用转向影片内容传送。

- 资料量的大幅增加导致资料和资料分析的快速普及。因此,企业需要比以往更快的洞察力才能保持竞争力,尤其是在越来越多的产业面临数位颠覆的情况下。因此,分析在整个企业中普遍存在,智慧源自于越来越多样化的资料来源。这样,资料准备市场变得更加活跃。

- 此外,最终用户公司不断发展并变得更加以资料为中心,以保持竞争力。当今的企业收集前所未有的大量资料来做出资讯的决策、了解业务趋势并提高效率。为了帮助员工将资料转化为行动,公司正迅速转向资料准备工具,从而推动市场成长。

- 此外,市场领先的公司正在将人工智慧 (AI) 和机器学习 (ML) 等先进技术与资料准备相结合,以读取、解释和扁平化复杂的资料结构。这些因素进一步推动了对资料准备解决方案的需求。

- COVID-19 的普及加速了资料准备工具的采用。例如,IBM Cognos Analytics 是一个人工智慧驱动的商业智慧平台,支援从发现到营运的整个分析週期。人工智慧辅助的资料准备让您可以在几分钟内清理和合併资料来源。

资料准备市场趋势

IT/通讯领域预计将占据较大市场占有率

- 世界各地的电信和IT公司正在产生大量资料,创造了资料金矿。缺乏对非结构化和结构化资料的可操作分析来更深入地了解客户行为,以及即时分析资料偏好和服务使用模式的需求不断增长,这促使这些公司采用资料分析,从而间接影响市场成长。

- 此外,高度发展和竞争激烈的通讯业在处理大量资料集(例如客户、网路和呼叫资料)方面发挥关键作用。此外,为了在这样的竞争环境中取得成功,电讯业参与者正在大力采用资料准备解决方案,这些解决方案可以创造业务考察,帮助他们获得超越竞争的优势。

- 资料解决方案可协助 IT 和电讯业推动探索性分析、提高分析师工作效率并改善组织的资料使用。通讯习惯处理大量客户资料,但现代资料的复杂性提出了新的挑战。

- 此外,资料流量的快速成长也推动了IT和通讯业对资料准备的需求。例如,根据Cisco的资料,到 2022 年,全球行动资料流量预计将达到每月 77.5Exabyte。

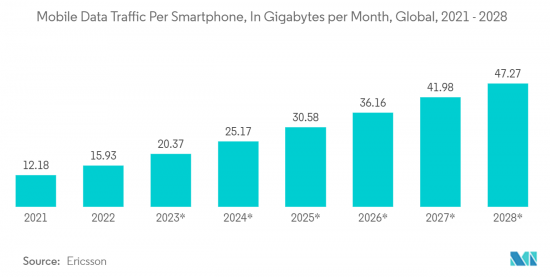

- 此外,根据爱立信的数据,到2022年,全球智慧型手机平均每月使用15.93GB行动资料,高于2021年的12.18GB。此外,到 2028 年,这一数字预计将达到 47.27 GB。

- 此外,像 IBM 公司这样的市场供应商已经帮助许多领先的通讯业资料分析供应商重组了他们的市场衡量产品。这项工作包括重组资料整合流程、开发新的自订使用者介面以及自动化工作流程。此外,将机器学习解决方案与资料准备工具整合正在占领市场。

预计北美将占据最大的市场占有率

- 北美将在预测期内实现成长,主要是由于对云端基础、资料分析和麵向资料的解决方案的大量投资、新技术和新兴技术的早期采用以及该地区存在大量重要的资料准备市场供应商预计将在受调查的市场中占据相当大的份额。

- 此外,过去几年资料的数量和复杂性使得资料准备对于全部区域面临激烈竞争的各种技术先进的最终用户行业至关重要。我们不断发展并变得更加以资料为中心克服挑战。

- 许多当地计画和研究人员正在利用资料科学来获得更好的见解。资料准备解决方案可以帮助您抓住这些机会,轻鬆存取各种资料并增强视觉化。例如,根据美国资料统计局的资料,到 2026 年,对经验丰富、消息灵通的资讯科学家的需求预计将增加 27.9%。

- 此外,随着云端服务的普及,该地区的公司越来越多地寻求可以部署在云端中的资料准备解决方案。在资料准备解决方案中越来越多地使用人工智慧和机器学习等先进技术,加上企业对灵活部署的资料准备工具解决方案的需求不断增长,将推动该地区资料准备市场在预测期内的成长。被形成。

资料准备产业概述

资料准备市场竞争激烈,市场上有多家主要参与者。然而,随着云端领域技术创新的进步和资料准备技术的进步,大多数公司正在增加其市场份额并开拓新兴国家的新市场。此外,供应商正在积极寻求联盟、合併和收购,以增加其在市场上的影响力。

2022 年 11 月,Qlik 宣布推出企业整合平台即服务 Qlik Cloud Data Integration,透过将所有企业应用程式和资料来源连接到云端的即时资料整合结构来支援企业资料策略。这个新的资料整合平台将资料准备和编目功能结合在一个地方,使企业能够准备资料以进行即时分析。

2022 年 6 月,分析自动化公司 Alteryx, Inc. 宣布收购 Trifacta。这家屡获殊荣的云端公司利用可扩展的资料管理和机器学习来使资料分析更快、更直观。透过收购 Trifactor,该公司打算利用其先进的云端平台帮助客户建立更强大的资料管道,并提供更重要的分析和准备功能。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争公司之间敌对关係的强度

- COVID-19 市场影响评估

第五章市场动态

- 市场驱动因素

- 对自助资料创建工具的需求

- 对资料分析的需求不断增长

- 市场挑战

- 引进网路保险难度高、高成本

第六章市场区隔

- 按配置

- 本地

- 云端基础

- 按公司规模

- 中小企业 (SME)

- 大公司

- 按行业分类

- BFSI

- 卫生保健

- 零售

- 製造业

- 资讯科技/通讯

- 其他行业

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东/非洲

第七章竞争形势

- 公司简介

- Informatica LLC

- IBM Corporation

- SAS Institute Inc.

- Microstrategy Inc.

- Tableau Software, LLC(Salesforce.com Inc.)

- SAP SE

- Alteryx Inc.

- Rapid Insight Inc.

- Unifi Software Inc.

- Qlik Technologies Inc. QlikTech International AB

- Paxata Inc.

- ClearStory Data Inc.

- Oracle Corporation

第八章投资分析

第9章 市场的未来

The data preparation market was valued at USD 4.78 billion last year and is expected to reach USD 13.51 billion in the next six years, registering a CAGR of 18.74% over the forecast period. Due to digital disruption, companies are demanding faster debugging time to generate meaningful insights than ever to sustain in the market. As a result, the analytics requirement, particularly data analytics, is becoming pervasive among organizations. Data analytics professionals and companies need help driving insights owing to the rising complexities in procuring data. This significantly drives the demand for data preparation among organizations.

Key Highlights

- The rapid adoption of automation and cloud technologies across enterprises and businesses resulted in tremendous data generation and cloud data traffic. According to Cisco Systems, the global IP data traffic is anticipated to reach 333 exabytes per month. There is a significant shift in data traffic from P2P (peer-to-peer) file sharing to video content delivery, especially in large content service providers (CSPs).

- This significant increase in the volume of data has resulted in the swift proliferation of data and data analytics. Therefore, businesses are demanding faster time to insight than ever to remain competitive, particularly as more industries face digital disruption. As a result, analytics is becoming more pervasive across enterprises, and wisdom is derived from more significant numbers of diverse data sources. Thus, in turn, driving the data preparation market.

- Moreover, various end-user companies are constantly evolving and becoming more data-centric to stay ahead of the competition. Companies today gather unprecedented amounts of data that they want to use to make informed decisions, spot business trends, and increase efficiency. To help employees turn data into action, organizations are rapidly shifting towards data preparation tools, thus driving the market's growth.

- Further, leading market players are integrating advanced technologies, such as artificial intelligence (AI) and machine learning (ML), with data preparation to read, interpret, and flatten complex data structures. Such factors further boost the demand for data preparation solutions.

- The spread of COVID-19 accelerated the adoption of data preparation tools. For instance, IBM Cognos Analytics is an AI-fueled business intelligence platform that supports the entire analytics cycle, from discovery to operationalization. It cleanses and combines data sources in minutes with AI-assisted data preparation.

Data Preparation Market Trends

IT and Telecom Segment is Expected to Hold a Significant Market Share

- Telecom and IT companies worldwide are creating a data gold mine as they generate plenty of data. The lack of practical analysis of unstructured and structured data to get more profound insights into customer behavior and the growing need to analyze their preferences and service usage patterns in real-time motivates these companies to adopt data analytics, indirectly impacting the market's growth.

- Further, in the highly evolving and competitive industry, the telecommunication industry plays a significant role in handling massive data sets of customers, network, and call data. Further, to thrive in such a competitive environment, the telecom industry players are significantly adopting data preparation solutions to create helpful business insights to stay ahead of the competitors.

- Data solutions help the IT and telecom industry to empower exploratory analytics, increase analyst productivity, and improve organizational data usage. While telecommunications providers are used to dealing with large volumes of customer data, the considerable complexity of modern-day data is a new challenge.

- In addition, the exponential growth in data traffic also drives the demand for data preparation in the IT and telecom industry. For instance, according to the data from Cisco Systems, by 2022, mobile data traffic worldwide is expected to reach 77.5 exabytes per month.

- Moreover, as per Ericsson, In 2022, smartphones across the globe used an average of 15.93 gigabytes of mobile data per month, up from 12.18 gigabytes in 2021. Additionally, the figure is expected to reach 47.27 gigabytes by 2028.

- Moreover, market vendors like IBM Corporation have helped many leading telecom industry data analytics providers re-engineer their market measurement products. The effort included restructuring data integration processes, developing new custom user interfaces, and making workflow automation. Further, integrating the ML solution with data preparation tools is gaining the market.

North America is Expected to Hold the Largest Market Share

- North America is expected to have a significant share in the market studied during the forecast period, mainly due to high investments in cloud-based, data analytics, and data-oriented solutions, early adoption of new and emerging technologies, and a large number of significant data preparation market vendors in the region.

- Moreover, the volume and complexity of data in the past few years have only made data preparation essential for various technologically advanced end-user industries across the region, which are constantly evolving and becoming more data-centric to keep themselves ahead of the fierce competition.

- Many regional programs and researchers use data science for better insights. Data preparation solutions can penetrate this opportunity and help them easily access extensive data and enhance visualization. For instance, according to the US Bureau of Labor Statistics data, demand for experienced and informed data scientists will likely increase by 27.9% by 2026.

- In addition, with the growing popularity of cloud services, enterprises in the region are increasingly looking for data preparation solutions that can be deployed in the cloud. The increasing use of advanced technologies such as AI and ML in data preparation solutions, coupled with the ever-increasing demand from enterprises for data preparation tool solutions that are flexible in terms of deployment, will shape the future of the growth of the data preparation market in the region over the forecast period.

Data Preparation Industry Overview

The data preparation market is highly competitive and consists of several significant players across the market space. However, with the growing innovation across the cloud segment and the advancement across the data preparation technique, most companies are increasing their market presence, thereby tapping into new markets of emerging economies. Moreover, the market vendors are indulging in partnership, merger, and acquisition activities to enhance their market presence.

In November 2022, Qlik launched its Enterprise Integration Platform as a Service Qlik Cloud Data Integration to fuel enterprise data strategies through a real-time data integration fabric that connects all enterprise applications and data sources to the cloud. The new data integration platform joins data preparation and cataloging capabilities in one place, enabling enterprises to ready their data in real-time for analysis.

In June 2022, Alteryx, Inc., the Analytics Automation company, announced the acquisition of Trifacta. This award-winning cloud company leverages scalable data management and machine learning to make data analytics faster and more intuitive. By acquiring Trifacta, the company intends to use its advanced cloud platform to help customers build a more robust data pipeline with more significant profiling and preparation capabilities.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHT

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Assessment of COVID-19 Impact on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Demand for Self-service Data Preparation Tools

- 5.1.2 Increasing Demand for Data Analytics

- 5.2 Market Challenges

- 5.2.1 Difficulties in Implementing Cyber Insurance and High Costs

6 MARKET SEGMENTATION

- 6.1 By Deployment

- 6.1.1 On-premise

- 6.1.2 Cloud-based

- 6.2 By Enterprise Size

- 6.2.1 Small and Medium Enterprises (SMEs)

- 6.2.2 Large Enterprises

- 6.3 By End-user Vertical

- 6.3.1 BFSI

- 6.3.2 Healthcare

- 6.3.3 Retail

- 6.3.4 Manufacturing

- 6.3.5 IT and Telecommunication

- 6.3.6 Other End-user Verticals

- 6.4 By Geography

- 6.4.1 North America

- 6.4.2 Europe

- 6.4.3 Asia-Pacific

- 6.4.4 Latin America

- 6.4.5 Middle East & Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Informatica LLC

- 7.1.2 IBM Corporation

- 7.1.3 SAS Institute Inc.

- 7.1.4 Microstrategy Inc.

- 7.1.5 Tableau Software, LLC (Salesforce.com Inc.)

- 7.1.6 SAP SE

- 7.1.7 Alteryx Inc.

- 7.1.8 Rapid Insight Inc.

- 7.1.9 Unifi Software Inc.

- 7.1.10 Qlik Technologies Inc. QlikTech International AB

- 7.1.11 Paxata Inc.

- 7.1.12 ClearStory Data Inc.

- 7.1.13 Oracle Corporation