|

市场调查报告书

商品编码

1404401

聚氨酯添加剂(PU添加剂):市场占有率分析、产业趋势/统计、成长预测,2024-2029Polyurethane Additives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

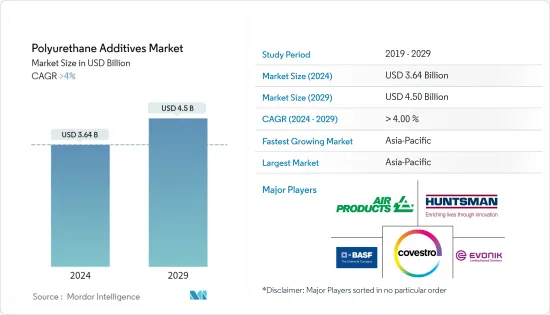

聚氨酯添加剂(PU添加剂)市场规模预计2024年为36.4亿美元,预计到2029年将达到45亿美元,在预测期内(2024-2029年)复合年增长率为4%,预计将进一步增长。

市场受到 COVID-19大流行的负面影响。由于遏制措施和经济混乱迫使该行业推迟生产,生产和流动性放缓。目前市场正从疫情中恢復。预计2022年市场将达到疫情前水准并持续稳定成长。

主要亮点

- 建设产业对聚氨酯的需求不断增长可能会推动添加剂的消费。最大的应用之一是使用硬质 PU 泡棉作为墙壁和屋顶隔热材料、隔热板以及门窗周围的间隙填充材。这将推动市场成长。

- 另一方面,替代添加剂也可用于与 PU 添加剂相同的应用。例如,有机硅添加剂和丙烯酸类添加剂都是PU泡棉的有效添加剂。

- 对更具创新性和成本效益的添加剂的需求不断增长预计将成为未来几年市场的机会。

- 亚太地区占比重最大,预计在预测期内成长率最高。

聚氨酯添加剂市场趋势

汽车产业需求增加

- 汽车产业是PU材料多样化应用的最佳例子之一。几乎所有类型的 PU 产品都用于汽车最终用户产业。

- 软质PU发泡体用于座椅、头枕、扶手、暖通空调和其他汽车内装系统、客机、火车、巴士等。 PU 涂层为您的汽车外装提供高光泽度、耐用性、防刮擦性和耐腐蚀性。 PU 涂层也用于挡风玻璃和窗户嵌装玻璃,以增加强度并提供防雾保护。

- PU合成橡胶可防止轮胎刺穿,也可用于避震器等模製部件。热塑性 PU 材料用于製造许多汽车零件,例如外装外饰板、行李箱衬里、防锁死煞车系统、正时皮带和燃油管路。 PU合成橡胶的独特性能专门用于垫圈、O 形环和其他密封件。

- 座椅是PU在汽车产业最大的应用领域。许多汽车座椅製造商正在寻求使用生物基多元醇的产品。然而,在全球大部分聚氨酯市场,「绿色」聚氨酯的市场渗透率仍处于起步阶段。

- 在全球整体,超过 90% 的汽车是使用单组份 PU 密封胶将挡风玻璃和后玻璃黏合在一起生产的。汽车产业是反应射出成型(RIM) PU 零件最大的最终用户产业。 RIM 用于最大限度地吸收车辆挡泥板、保险桿和扰流板的衝击力,而不会增加重量或体积。

- 根据国际汽车製造商组织 (OICA) 的数据,2022 年全球汽车产量约为 8,502 万辆。这个数字比去年增加了约6%。到2022年,中国、日本和德国将成为最大的汽车和商用车生产国,推动PU添加剂市场的发展。

- 然而,随着对汽油和柴油车环境污染的担忧加剧,电动车产量预计将在未来五年内恢復。这可能会在预测期内提振受调查市场的需求。

- 2023 年 8 月,总部位于密西根州的全球科技公司 Altair 和汽车研究中心 (CAR) 评选马瑞利为内装产品聚氨酯泡沫轻量化未来类别 2023 年 Enlighten 奖得主。

- 此外,全球电动车市场正在显着扩张,这有利于所研究的市场。例如,2022年,全球销售了约1,050万辆纯电动车(BEV)和插电式混合电动车(PHEV),与前一年的677万辆相比成长了55%。

- 所有上述因素预计将在预测期内推动市场。

中国可望主导亚太地区

- 在亚太地区,中国是GDP最大的经济体。 2022年中国GDP产值将占世界经济的7.73%,GDP成长速度与前一年同期比较3%。

- 中国是世界上最大的经济体之一,其建筑业的成长速度几乎超过了所有其他行业。 2022年,建筑业占中国国内生产总值约6.9%,中国建筑业增加付加比与前一年同期比较增长约5.5%。

- 中国家具製造业的快速成长很大程度上得益于国内需求的增加以及海外市场的大量需求。

- 2022年,中国将占全球家具产量的近53%。国内需求的增加和对欧洲国家的出口进一步增加了产量。

- 根据OICA统计,自2009年以来,中国一直是全球最大的汽车製造国和汽车市场。中国年汽车产量占全球汽车产量的32%以上,超过欧盟、美国和日本的总和。

- 然而,电动车在该国的普及预计将在未来几年推动聚氨酯添加剂的需求。中国政府计画在2025年引进至少5,000辆燃料电池电动车,到2030年引进100万辆。政府推广电动车、混合和燃料电池汽车的使用预计将在预测期内推动市场研究。

- 这些因素预计将增加该国对聚氨酯添加剂的需求。

聚氨酯添加剂产业概况

聚氨酯添加剂市场因其性质而部分分散。主要参与者(排名不分先后)包括赢创工业股份公司、空气产品公司、科思创股份公司、亨斯曼国际有限责任公司和BASF股份公司。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第一章简介

- 调查先决条件

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场动态

- 促进因素

- 建设产业对聚氨酯的需求增加

- 汽车产业需求增加

- 对永续聚氨酯产品的需求不断增长

- 抑制因素

- 替代添加剂的可得性

- 严格的政府法规

- 产业价值链分析

- 波特五力分析

- 供应商的议价能力

- 买方议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章市场区隔(市场规模:以金额为准)

- 类型

- 发泡

- 催化剂

- 阻燃剂

- 介面活性剂

- 其他(填料、乳化剂、交联剂)

- 目的

- 黏剂/密封剂

- 涂层

- 软质模製泡沫

- 硬质泡沫

- 其他(合成橡胶、纤维、复合材料、医疗设备)

- 地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 东南亚国协

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 义大利

- 法国

- 其他欧洲国家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东/非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲

- 亚太地区

第六章竞争形势

- 併购、合资、联盟、协议

- 市场占有率(%)/排名分析

- 主要企业策略

- 公司简介

- Air Products Inc.

- Covestro AG

- BASF SE

- Dow

- GEO Specialty Chemicals Inc.

- Huntsman International LLC

- Eastman Chemical Company

- Evonik Industries AG

- Momentive Performance Materials Inc.

- KAO Corporation

- Specialty Products Inc.

- Tosoh Corporation

第七章 市场机会及未来趋势

- 对创新且具有成本效益的添加剂的需求不断增长

- 其他机会

The Polyurethane Additives Market size is estimated at USD 3.64 billion in 2024, and is expected to reach USD 4.5 billion by 2029, growing at a CAGR of greater than 4% during the forecast period (2024-2029).

The market was negatively impacted by the COVID-19 pandemic as there was a slowdown in production and mobility wherein industries were forced to delay their production due to containment measures and economic disruptions. Currently, the market has recovered from the pandemic. The market reached pre-pandemic levels in 2022 and is expected to grow steadily in the future.

Key Highlights

- The rising demand for polyurethane in the construction industry will likely propel additives' consumption. One of the largest applications is the use of rigid PU foam as wall and roof insulation, insulated panels, and gap fillers for the space around doors and windows. Thereby augmenting the market's growth.

- On the flip side, the alternative additives can be used in some of the same applications as PU additives. For example, silicon additives and acrylic additives are both effective additives against PU foams.

- The increasing demand for more innovative and cost-effective additives is projected to act as an opportunity for the market in the future.

- The Asia-Pacific region is expected to account for the largest share and register the highest growth rate over the forecast period.

Polyurethane Additives Market Trends

Increasing Demand from the Automotive Industry

- The automotive industry provides one of the best examples of the diverse applications of PU materials. Nearly every type of PU product is used in the automotive end-user industry.

- Flexible PU foams are used in seating, headrests, armrests, HVAC, and other interior systems for automotive, like in airliners, trains, and buses. PU coatings provide a vehicle's exterior with high gloss, durability, scratch resistance, and corrosion resistance. PU coatings are also used for glazing windshields and windows, increasing strength and providing fog resistance.

- PU elastomers protect against tire punctures and are used in other molded components, such as shock absorbers. Thermoplastic PU materials are used to manufacture many automotive parts, including exterior body parts, trunk liners, anti-lock brake systems, timing belts, and fuel lines. The unique properties of PU elastomers contribute to their exclusive usage in gaskets, O-rings, and other seals.

- Seating is the largest application of PU in the automotive industry. Many automotive seating manufacturers demand products made with bio-based polyols. However, the market penetration of "green" PU is still emerging in most global PU markets.

- Globally, more than 90% of automobiles are produced with bonded windshields and rear windows using one-component PU sealants. The automotive industry is the largest end-user industry for reaction injection molding (RIM) PU parts. RIM is used to maximize the shock absorption of vehicle fenders, bumpers, and spoilers without adding weight or bulk.

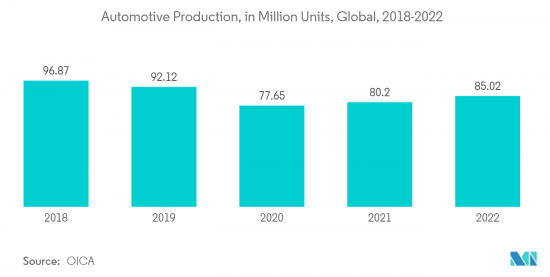

- In 2022, according to the Organisation Internationale des Constructeurs d'Automobiles (OICA), around 85.02 million motor vehicles were produced worldwide. This figure translates into an increase of around 6% compared with the previous year. China, Japan, and Germany were the largest producers of cars and commercial vehicles in 2022, which is driving the PU additive market.

- However, with growing concerns about environmental pollution from petrol- and diesel-based vehicles, the production of electric vehicles is expected to pick up over the next five years. This is likely to drive the demand in the market studied over the forecast period.

- In August 2023, Global technology company Altair and the Center for Automotive Research (CAR), both based in Michigan, named Marelli as the 2023 Enlighten award winner in the Future of Lightweighting category for its polyurethane foam for interior products.

- Further, the global electric vehicle market is expanding significantly, which is benefitting the market studied. For instance, in 2022, around 10.5 million units of battery electric vehicles (BEVs) and plug-in hybrid electric vehicles (PHEVs) were sold across the globe, witnessing a growth rate of 55% compared to 6.77 million units sold in the previous year.

- All the factors above are expected to drive the market during the forecast period.

China is Expected to Dominate the Asia-Pacific Region

- In Asia-Pacific, China is the largest economy in terms of GDP. The GDP value of China represents 7.73% of the world economy in 2022 and has a 3% GDP growth compared to the previous year.

- China is one of the largest countries in the world, where the construction sector dominates almost all other sectors in growth. In 2022, the construction industry accounted for around 6.9% of China's gross domestic product, and the value added to the Chinese construction industry increased by about 5.5% compared to the previous year.

- The rapid growth of the furniture manufacturing industry in the country is majorly fueled by the increasing domestic demand, coupled with significant demand from the foreign market.

- China accounted for almost 53% of the global furniture production in 2022. The production was further increased rapidly due to the increase in domestic demand and exports to European countries.

- According to the OICA, China remains the world's largest automotive manufacturing country and automotive market since 2009. Annual vehicle production in China accounted for more than 32% of worldwide vehicle production, which exceeds that of the European Union or that of the United States and Japan combined.

- However, the popularity of electric vehicles in the country is expected to propel the demand for PU additives in the coming years. The Chinese government plans to have a minimum of 5,000 fuel-cell electric vehicles by 2025 and 1 million by 2030. The government promoting the use of electric, hybrid, and fuel-cell electric vehicles is expected to drive the market studied during the forecast period.

- Such factors are expected to increase the demand for polyurethane additives in the country.

Polyurethane Additives Industry Overview

The polyurethane additives market is partially fragmented in nature. The major players (not in any particular order) include Evonik Industries AG, Air Products Inc., Covestro AG, Huntsman International LLC, and BASF SE. among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Rising Demand for Polyurethane in the Construction Industry

- 4.1.2 Increasing Demand from the Automotive Industry

- 4.1.3 Growing demand for sustainable Polyurethane products

- 4.2 Restraints

- 4.2.1 Availability of Alternative Additives

- 4.2.2 Stringent Government Regulations

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Type

- 5.1.1 Blowing Agents

- 5.1.2 Catalysts

- 5.1.3 Flame Retardants

- 5.1.4 Surfactants

- 5.1.5 Other Additives( Filler, Emulsifiers, and Crosslinking Additives)

- 5.2 Application

- 5.2.1 Adhesives and Sealants

- 5.2.2 Coatings

- 5.2.3 Flexible Molded Foams

- 5.2.4 Rigid Foams

- 5.2.5 Other Applications (Elastomers, Fibers, Composites, and Medical Devices)

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Air Products Inc.

- 6.4.2 Covestro AG

- 6.4.3 BASF SE

- 6.4.4 Dow

- 6.4.5 GEO Specialty Chemicals Inc.

- 6.4.6 Huntsman International LLC

- 6.4.7 Eastman Chemical Company

- 6.4.8 Evonik Industries AG

- 6.4.9 Momentive Performance Materials Inc.

- 6.4.10 KAO Corporation

- 6.4.11 Specialty Products Inc.

- 6.4.12 Tosoh Corporation

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Demand for More Innovative and Cost-effective Additives

- 7.2 Other Opportunities

聚氨酯添加剂市场:按类型、应用和最终用途划分 - 2024-2030 年全球预测

聚氨酯添加剂市场:按类型、应用和最终用途划分 - 2024-2030 年全球预测 聚氨酯添加剂市场 - 2018-2028 年全球产业规模、份额、趋势、机会和预测,按类型、最终用户、地区和竞争细分

聚氨酯添加剂市场 - 2018-2028 年全球产业规模、份额、趋势、机会和预测,按类型、最终用户、地区和竞争细分 聚氨酯(PU)用添加剂的全球市场

聚氨酯(PU)用添加剂的全球市场