|

市场调查报告书

商品编码

1404432

乙烯醋酸乙烯酯 (EVA) -市场占有率分析、产业趋势与统计、2024-2029 年成长预测Ethylene Vinyl Acetate (EVA) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

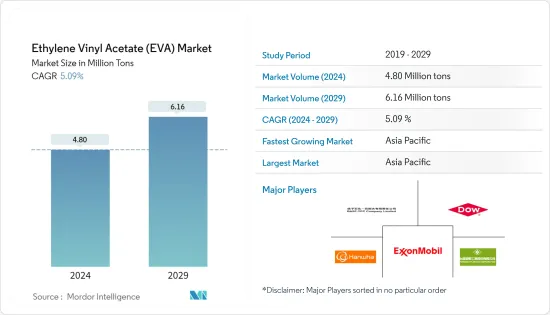

乙烯醋酸乙烯酯市场规模预计到2024年为480万吨,预计到2029年将达到616万吨,在预测期内(2024-2029年)复合年增长率为5.09%。

COVID-19 大流行影响了 2020 年的市场。这导致国际旅行禁令、零售店关闭以及许多最终用户群体的销售、购买和使用减少。然而,2021年和2022年乙烯醋酸乙烯(EVA)的需求增加。

主要亮点

- 短期内,包装产业和农业应用对乙烯醋酸乙烯酯(EVA)需求的增加预计将推动市场发展。

- 相反,替代品威胁的增加预计将阻碍市场成长。

- 对光伏(太阳能电池)封装的需求不断增长预计将在预测期内为市场提供成长机会。

- 预计亚太地区将主导市场,并可能在预测期内保持最高的复合年增长率。这是因为该地区的经济带动了市场,导致人们消费能力的增强。

乙烯醋酸乙烯酯市场趋势

薄膜应用主导市场

- 乙烯醋酸乙烯酯是一种共聚物树脂,在透过平晶粒挤出之前加热并充分混合后会形成 EVA 薄膜。该薄膜有白色、透明和多种其他颜色可供选择,并提供光滑、不粘的表面光洁度。 EVA 薄膜通常夹在两片塑胶或玻璃片之间作为中间层。

- 当EVA薄膜使用率较低时,用于冷冻食品包装(EVA 6%)、麵包袋(EVA 2%)、冰袋(EVA 4%)等。此外,EVA 含量高达 20% 的薄膜还可用于低熔点/全批次封装袋等应用。同样,在太阳能电池板中,高达 33% 的 EVA 薄膜被用作面板的黏合层。

- 鑑于关键应用领域对EVA薄膜的需求不断增加,一些主要的EVA薄膜製造商正在加大对扩产计划的投资。主要进展包括:

- 2023年2月,中国最大的光电模组EVA薄膜供应商SVECK宣布,决定投资约13.6亿元人民币(约2.03亿美元)进行扩产计划。新厂将在中国江苏省盐城市分两期建设,年产能将达4.2亿平方公尺。第一阶段计画于2023年第三季开始商业运营,年产能1.2亿平方公尺,共有16条生产线。阶段将再部署40条生产线,总产能达3亿平方公尺。 SVECK预计透过该计划每年将额外产生34亿元人民币(约5亿美元)的收益。

- 2022年6月,全球大型公司的EVA薄膜製造商杭州第一应用材料公司宣布,决定投资2.26亿美元扩大在越南的EVA薄膜产能。该公司计划在越南建造新的製造地,并支持推出年产能约2.5亿平方公尺的高效能太阳能电池EVA薄膜计划。该计划预计将在未来三年内实现商业化。

- 非食品应用、太阳能电池封装和太阳能板对 EVA 薄膜的需求不断增长,预计将在预测期内加强 EVA 薄膜市场。

亚太地区主导市场

- 亚太市场是最大的乙烯醋酸乙烯酯(EVA)市场。由于中国和印度的强劲需求(主要用于黏剂和包装产业),预计在预测期内仍将是最大的市场。

- 乙烯醋酸乙烯酯共聚物 (EVA) 是包装应用中常用的树脂,可取代聚氯乙烯。 EVA 共聚物不需要硬化剂或塑化剂,无味。由于其相对于传统包装塑胶的优势,EVA在包装领域的使用量大幅增加。

- 中国包装产业预计将成长。据政府预测,该产业预计将实现近6.8%的成长率。中国政府发布的报告预计,到2025年,该产业价值将达到2兆元(约2,900亿美元)。中国食品工业位居世界前列,其成长预计将对 EVA 市场产生影响。

- 由于其减震性能,EVA 也越来越多地应用于鞋类、曲棍球垫片、武术手套和其他运动器材。

- 亚运会由亚洲奥林匹克理事会(OCA)主办,将于2023年9月23日至10月8日在杭州举行。亚运会通常吸引全部区域。收入增加、健康意识增强、体育专业化水平提高以及都市区健身选择多样化等因素预计将推动对运动服和休閒服的需求。

- 中国鞋业由14,400多家企业组成。中国是世界上最大的鞋类生产国。中国占鞋类出口的50%以上。 2022年,鞋子出口量将超过90亿双。

- 印度拥有世界上最大的包装工业之一。由于出口增加以及微波炉、零食和冷冻食品等食品行业客製化包装的使用增加,预计预测期内将实现稳定成长。

- 根据印度包装工业协会(PIAI)预测,印度包装产业在预测期内预计将成长 22%。印度包装市场预计到 2025 年复合年增长率为 26.7%,达到 2,048.1 亿美元。因此,该地区的EVA市场预计将成长。

- 根据贸易、工业、消费者事务、食品、公共分配和纺织品联盟部长表示,由于政府和产业的努力,印度有潜力成为鞋类和皮革领域的世界领导者。例如,由于与阿拉伯联合大公国签订自由贸易协定(FTA),皮革业预计将成长,2022年11月出口量将成长64%。

- 印度是世界第二大鞋类和皮革服饰生产国,拥有约 30 亿平方英尺的製革厂。此外,2021 年,该中心通过了 170 亿印度卢比(2.058 亿美元)的支出,用于将于 2021 年至 2026 年实施的印度鞋类和皮革发展计画 (IFLDP)。

- 所有上述因素预计将在预测期内增加调查市场的需求。

乙烯醋酸乙烯酯产业概况

全球乙烯醋酸乙烯酯市场已与占据重要全球市场占有率的主要企业部分整合。研究市场的主要企业包括(排名不分先后)埃克森美孚、韩华解决方案、陶氏化学、台塑公司、BASF扬子石化有限公司等。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第一章简介

- 调查先决条件

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场动态

- 促进因素

- 包装产业的需求不断增加

- 农业应用需求增加

- 抑制因素

- 替代品的威胁日益增大

- 产业价值链分析

- 波特五力分析

- 供应商的议价能力

- 交付的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章市场区隔(市场规模(基于数量))

- 年级

- 低密度

- 中等密度

- 高密度

- 目的

- 电影

- 黏剂

- 发泡体

- 太阳能电池封装

- 其他用途

- 地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 欧洲其他地区

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东/非洲

- 沙乌地阿拉伯

- 南非

- 中东和非洲其他地区

- 亚太地区

第六章竞争形势

- 併购、合资、联盟、协议

- 市场占有率(%)**/排名分析

- 主要企业策略

- 公司简介

- Arlanxeo

- Asia Polymer Corporation

- Basf-ypc Company Limited

- Benson Polymers

- Braskem

- Celanese Corporation

- China Petrochemical Corporation

- Clariant

- Dow

- Exxonmobil Corporation

- Formosa Plastics Corporation

- Hanwha Solutions

- Hd Hyundai Oilbank Co.

- Innospec

- Jiangsu Sailboat Petrochemical Co. Ltd

- Levima Advanced Materials Corporation

- LG Chem

- Lyondellbasell Industries Holdings BV

- Repsol

- Sinochem Holdings Corporation Ltd

- Sipchem Company

- Sumitomo Chemical Co. Ltd

- Zhejiang Petroleum & Chemical Co. Ltd

第七章 市场机会及未来趋势

- 对太阳能电池封装的需求增加

The Ethylene Vinyl Acetate Market size is estimated at 4.80 Million tons in 2024, and is expected to reach 6.16 Million tons by 2029, growing at a CAGR of 5.09% during the forecast period (2024-2029).

The COVID-19 pandemic impacted the market in 2020. As a result, international travel bans and retail business closures, sales, purchases, and usage fell across many end-user segments. However, the demand for ethylene-vinyl acetate (EVA) increased in 2021 and 2022.

Key Highlights

- Over the short term, the growing demand for ethylene-vinyl acetate (EVA) from the packaging industry and agricultural applications is expected to drive the market.

- Conversely, the increasing threat of substitutes is expected to hinder the market's growth.

- The increasing demand for photovoltaic (PV) solar cell encapsulants is expected to offer growth opportunities for the market during the forecast period.

- Asia-Pacific is expected to dominate the market and is likely to witness the highest CAGR during the forecast period as the economies in the region are driving the market, leading to increased spending capacities among the people.

Ethylene Vinyl Acetate Market Trends

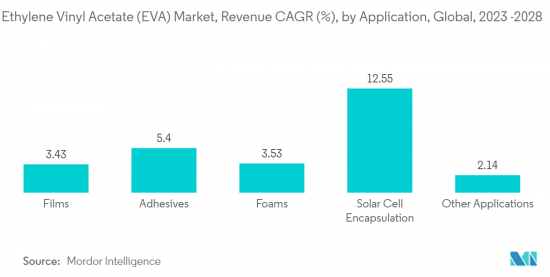

Films Application to Dominate the Market

- Ethylene Vinyl Acetate is a copolymer resin that, when heated and mixed thoroughly before being extruded through a flat die, forms EVA films. These films are available in white, clear, and other different colors and provide a non-sticky and smooth surface finish. EVA films are generally sandwiched between two plastic or glass sheet pieces as an interlayer.

- In lower percentages, EVA films have been used for frozen food packaging (at 6% EVA), bread bags (at 2% EVA), and ice bags (at 4% EVA), as it helps provide enhanced sealability for such applications. Further, in higher percentages, with up to 20% EVA, these films are used in applications involving low melt/total batch inclusion bags. Similarly, in solar panels, films with up to 33% EVA are used as a bonding layer for these panels.

- Some of the key manufacturers of EVA films have been increasingly investing in production expansion projects in view of the growing demand for EVA films in critical applications. Some of the key developments include:

- In February 2023, SVECK, one of the largest suppliers of EVA films for PV modules in China, announced its decision to invest around CNY 1.36 billion (~USD 203 million) into its production expansion project. The new factory will be built in two phases, in Yancheng, China's Jiangsu, at a planned annual capacity of 420 million square meters. The first phase is expected to begin commercial operations by Q3 2023, with an annual capacity of 120 million square meters spread across 16 production lines. The second phase will deploy an additional 40 production lines with a total capacity of 300 million square meters. SVECK has projected an additional annual revenue of CNY 3.4 billion (~USD 500 million) through this project.

- In June 2022, Hangzhou First Applied Material Co., Ltd., another leading manufacturer of EVA films across the globe, announced its decision to invest USD 226 million into the expansion of its EVA film production capacity in Vietnam. The company intends to build a new manufacturing base in Vietnam to support the launch of its EVA film project specifically designed for high-efficiency solar cells, with an annual output of around 250 million square meters. The project is expected to be commercialized in the next three years.

- The rising demand for EVA films in non-food applications, photovoltaic encapsulations, and solar panels is anticipated to strengthen the EVA films market during the forecast period.

Asia-Pacific to Dominate the Market

- The Asia-Pacific market is the largest ethylene vinyl acetate (EVA) market. It is also expected to remain the largest market during the forecast period, owing to the major demand from China and India, mainly for the adhesive and packaging industry applications.

- Ethylene vinyl acetate copolymers (EVA) are commonly used in packaging applications, replacing polyvinyl chloride as the most used resin. EVA copolymers require no curing or plasticizer and have no odor. The use of EVA in the packaging sector is increasing tremendously, owing to its advantages over the conventional packaging plastics used.

- The Chinese packaging industry is expected to grow. As projected by the government, the industry is expected to achieve a growth rate of nearly 6.8%. The report published by the Chinese government foresees the industry achieving a valuation of CNY 2 trillion, equivalent to approximately USD 290 billion, by the year 2025. The growing Chinese food industry, which ranks among the largest globally, is expected to affect the EVA market.

- EVA is also increasingly used in footwear, hockey pads, martial arts gloves, and other sports goods due to its shock absorber properties.

- The Asian Games will take place in Hangzhou from September 23 to October 8, 2023, per the Olympic Council of Asia (OCA). The Asian Games generally attract more than 10,000 athletes across the region. Factors such as rising income, increased health awareness, the growing level of sports specialization, and the diversity of urban fitness options are expected to boost the demand for sportswear and recreational wear.

- China's footwear industry consists of over 14,400 businesses. China is the largest footwear producer in the world. China accounts for over 50% of the exports of footwear. The country exported more than 9,000 million pairs of shoes in 2022.

- India has a huge packaging industry in the world. The country is expected to witness consistent growth during the forecast period, owing to the rise of customized packaging in the food segment, like microwave, snack, and frozen foods, along with increasing exports.

- According to the Packaging Industry Association of India (PIAI), the Indian packaging industry is expected to grow at 22% during the forecast period. The Indian packaging market is expected to reach USD 204.81 billion by 2025, registering a CAGR of 26.7% till 2025. Therefore, the EVA market is expected to grow in the region.

- According to the Union Minister for Trade Industries, Consumer Affairs, Food, and Public Distribution and Textiles, India has the potential to become a world leader in the footwear and leather sector due to government and industry efforts. For instance, the leather industry is expected to grow, owing to a free trade agreement (FTA) with the United Arab Emirates, which saw exports increase by 64% in November 2022.

- India is the second largest producer of footwear and leather garments, boasting nearly 3 billion sq. ft of tanneries worldwide. In addition, in 2021, the Center passed an expenditure of INR 1,700 crore (USD 205.8 million) to the Indian Footwear and Leather Development Program (IFLDP) for implementation from 2021 to 2026.

- All the aforementioned factors are expected to boost the demand for the market studied during the forecast period.

Ethylene Vinyl Acetate Industry Overview

The global ethylene-vinyl acetate market is partially consolidated, with top-level players accounting for a sizeable global market share. The key players in the market studied (not in any particular order) include Exxon Mobil Corporation, Hanwha Solutions, Dow, Formosa Plastics Corporation, and BASF-YPC Limited.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Demand from the Packaging Industry

- 4.1.2 Rising Demand from Agricultural Applications

- 4.2 Restraints

- 4.2.1 Increasing Threat of Substitutes

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buters

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Grade

- 5.1.1 Low Density

- 5.1.2 Medium Density

- 5.1.3 High Density

- 5.2 Application

- 5.2.1 Films

- 5.2.2 Adhesives

- 5.2.3 Foams

- 5.2.4 Solar Cell Encapsulation

- 5.2.5 Other Applications

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East & Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East & Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Arlanxeo

- 6.4.2 Asia Polymer Corporation

- 6.4.3 Basf-ypc Company Limited

- 6.4.4 Benson Polymers

- 6.4.5 Braskem

- 6.4.6 Celanese Corporation

- 6.4.7 China Petrochemical Corporation

- 6.4.8 Clariant

- 6.4.9 Dow

- 6.4.10 Exxonmobil Corporation

- 6.4.11 Formosa Plastics Corporation

- 6.4.12 Hanwha Solutions

- 6.4.13 Hd Hyundai Oilbank Co.

- 6.4.14 Innospec

- 6.4.15 Jiangsu Sailboat Petrochemical Co. Ltd

- 6.4.16 Levima Advanced Materials Corporation

- 6.4.17 LG Chem

- 6.4.18 Lyondellbasell Industries Holdings BV

- 6.4.19 Repsol

- 6.4.20 Sinochem Holdings Corporation Ltd

- 6.4.21 Sipchem Company

- 6.4.22 Sumitomo Chemical Co. Ltd

- 6.4.23 Zhejiang Petroleum & Chemical Co. Ltd

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Demand for Photovoltaic (PV) Solar Cell Encapsulants