|

市场调查报告书

商品编码

1404458

球阀:市场占有率分析、产业趋势与统计、2024-2029 年成长预测Ball Valve - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

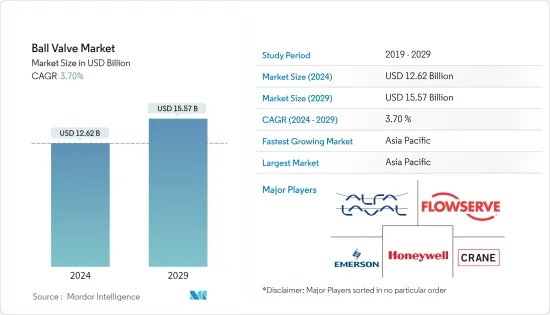

球阀市场规模预计到2024年为126.2亿美元,预计到2029年将达到155.7亿美元,在市场估计和预测期间(2024-2029年)复合年增长率为3.70%。

石油和天然气需求的大幅成长被视为促进球阀市场成长的关键因素之一。此外,快速的工业化和都市化也是支撑新兴市场开拓的重要因素。

主要亮点

- 球阀本质上是直角迴转驱动阀,其提供强制关闭的能力使其适用于工业应用中的清洁气体、压缩空气和液体服务。然而,当用于泥浆服务时,必须采取措施防止碎片堆积。此外,这些阀门非常坚固,非常适合需要简单开/关操作的应用。它还非常耐用,无论使用多少次都保持稳定的性能。

- 球阀是石油和天然气生产设备中应用最广泛的流体隔离阀。这些阀门也用于为熔炉供应的燃气系统。这些应用使得产油地区和具有大量精製能力的地区成为产品供应商有吸引力的目标。此外,由于此类工厂将在竞标浮动的基础上开发,因此与此类解决方案提供商合作的市场供应商预计将拥有竞争优势。

- 在所有类型的材料中,不銹钢因其高耐腐蚀性而获得并预计将继续获得重要性。由于阀门经常打开和关闭,腐蚀会导致严重的问题。这些阀门可以使食品加工厂受益,并且可以在更恶劣的水类型中保持更好的性能。不銹钢阀门比黄铜等其他材料具有更高的压力额定功率,这一事实进一步促进了不銹钢阀门的采用。

- 此外,根据阀口和阀座的数量,提供不同类型的球阀(例如单向、双向和多向),并补充了它们的工业应用。这些阀门按照高压管道和低压管道等分类製造,进一步扩大了使用案例范围。多家供应商不断投资创新新产品,这是推动市场的主要因素之一。

- 阀门技术的进步,包括智慧阀门的出现以及自动化和控制系统的结合,正在为市场带来新的前景。日益增长的环境问题和监管要求推动了对环保和节能阀门的需求。提供具有最小排放、低洩漏率和能源效率的节能球阀的製造商可以满足对永续解决方案不断增长的需求。

- 球阀通常采用较大直径,因为蝶阀等替代阀门类型往往具有较小且较弱的阀桿。在空间限制和结构负荷至关重要的情况下,例如海上钻探平臺和浮式生产储油卸油设备(FPSO),使用者会选择球阀的替代品。此外,流量控制的精度有限对所研究市场的成长构成了挑战。

- COVID-19 的影响因供应商而异,一些供应商为食品业提供球阀并提供服务,而其他供应商仅为石油和天然气行业提供服务。参与食品加工的供应商受疫情影响较小,因为食品相关产品的生产被视为基本服务,而且这些设施正在加班以满足需求。然而,随着大流行引发的限制几乎取消并且各行业已恢復全面营运能力,预计所研究的市场将在预测期内出现向上增长。

球阀市场趋势

食品加工业可能有重要的应用

- 食品加工产业是球阀重要应用的一个值得注意的领域。产品填充过程需要保持稳定的流量,因此球阀成为重要组件。该行业使用两种类型的阀门:直接接触材料的阀门和用于水和蒸汽等公共产业服务的阀门。在这两种情况下,阀门都必须符合多项行业法规,特别是那些与食品材料接触的行业法规。这对製造商获得监管部门批准提出了重大挑战,并且必须设计符合严格行业标准的阀门。

- 球阀在控制和维持大体积、温度和压力方面非常有效。在食品和饮料领域,卫生级球阀用于连接和调节输送管道,由于其材质为不銹钢,保证了所输送流体的纯净、稳定性和品质。卫生级阀门也易于消毒和清洗,促进卫生。随着各种供应商不断推出产品,市场预计将会成长。

- 例如,2022 年 11 月,致动阀和设备控制製造商 Valworx 最近推出了一系列适合部署在食品和饮料製造领域的新卫生球阀。这些球阀具有突出的位置指示器,并且与 Namur 和 ISO 安装相容。阀门有二通阀和三通阀,尺寸从 0.5 英吋到 4 英吋不等。新系列阀门符合 FDA、USD A 和 3-A 标准。

- 不銹钢因其广泛的耐腐蚀性而日益被认为是一种重要材料,这是食品加工领域的关键问题。当暴露于更具腐蚀性的水成分时,这些阀门也表现出卓越的耐用性,为食品加工厂提供了显着的优势。此外,与黄铜等替代材料相比,不銹钢阀门具有更高的压力额定功率。例如,典型的 1 英吋黄铜球阀的额定功率等级为 600 PSI,而相同尺寸的标准不銹钢球阀的压力额定功率为 1000 PSI。这项特性使其特别适合食品加工产业的高压应用。

- 世界各地都市化不断提高,对包装食品的需求显着增加。生活方式的改变,特别是在都市区,也导致包装和加工食品的需求增加。为了确保粮食安全并实现自给自足的目标,各国正在透过监管改革和建立经济特区等努力来发展食品加工业。例如,2022年6月,新兴国家宣布提供3.75亿美元资金支持美国肉类和家禽加工厂计划。这些因素可能会产生对食品业广泛使用的球阀的需求。

- 其他国家也观察到了这种有利于市场成长的情况。根据工业和国内贸易促进部的报告,到 2022 年,印度食品加工产业的拟议投资价值为 1,203.7 亿印度卢比(14.7 亿美元)。印度食品加工工业部正在努力鼓励整个价值链的投资,包括实施 PLI 计划,到 2026-27 年将食品加工能力扩大近 3,000 亿印度卢比(36 亿美元)。创造额外的直接和间接就业机会。这些倡议预计将为球阀提供重要机会。

预计北美将占据主要市场占有率

- 北美是球阀的主要市场,石油和天然气、电力、食品和包装以及化学品等多个行业对球阀的需求量很大。美国和加拿大显示出巨大的需求,工业自动化的快速整合进一步推动了这一需求。这一趋势预计将刺激该地区球阀市场的需求。

- 在北美地区,对智慧型球阀的需求不断增加。该地区的主要行业正在转向球阀,球阀结合了处理器和网路功能,以补充透过中央控制站协调的先进监控技术。製程工业中越来越多地采用自动化进一步强化了这种需求趋势。

- 与加拿大相比,美国在区域需求成长中发挥关键作用。在美国,几乎每个最终用户领域的需求都在成长,主要是石油和天然气、精製和发电。能源消费量的增加是这些产业需求成长的主要驱动力。例如,根据EIA的数据,2022年美国即时能源消耗总量约为102.92兆BTU,其中石油消费量约为31%。

- 此外,对石油和天然气以及其他石油产品的需求不断增加也鼓励石油生产商增加产量并开拓新油田,预计这将推动所研究市场的进一步成长。例如,2022年11月,加拿大能源承包协会(CAOEC)宣布,预计2023年加拿大将钻探约6,409口井,比2022年增加约15%。

- 随着该地区人口的增长以及各行业消费量预计将增加,预计该地区可能会安装新的水处理设施,以满足对球阀的需求。一个着名的例子是纽约州官员在 2022 年 9 月宣布,他们已拨款超过 2.32 亿美元用于七个城市的用水和污水基础设施计划。纽约州环境设施公司提供资金和低成本融资方案,以促进水基础设施计划,累积支出超过 7.63 亿美元。这些建立处理厂的投资必然会增加对球阀的需求。

- 球阀用于调节压力和流量。其防漏性能是一个显着的特性,在处理液体的化学工业中特别有利。 2022年7月,BASF宣布了计划的最终投资决定,旨在将其位于路易斯安那州阿森松教区的化学製造综合体的产能提高一倍。该扩建计划历时七年多,总资本投资超过 10 亿美元,使该公司能够满足北美地区建筑、电器、道路运输和汽车等多个行业对其产品不断增长的需求。 。 变得。

球阀产业概况

球阀市场分散,由多个参与企业组成,但目前没有一个集团占据较大份额。每家公司都进行併购以提高其产品的专业化。由于其广泛的消费者基础,该市场被视为利润丰厚的投资机会。主要市场参与企业包括福斯公司、阿法拉伐、克瑞公司和霍尼韦尔国际公司。

2022 年 11 月,克林格流体控制推出了更坚固的球阀「Monoball KHO」。该公司表示,该阀门具有铸造精良的外壳,比其前身能够吸收更多的力。此外,这些阀门有多种型号可供选择,螺纹和法兰也可根据客户要求量身定制。

2022 年 11 月,丹佛斯宣布推出适用于无油系统的新排放解决方案。据该公司称,这些新型止回阀和截止阀结合了阻尼喷嘴止回阀、截止阀和扩散器功能,以满足应用需求。此外,系统的分离式停止和止回功能可实现快速存取并提高密封可靠性,并且锁定环设计可防止球阀意外关闭。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争公司之间的敌对关係

- 产业价值链分析

- COVID-19 对市场的影响

第五章市场动态

- 市场驱动因素

- 各国工业化进展

- 对製程安全的需求不断增长

- 市场挑战

- 因阀门维修而停机

第六章市场区隔

- 按材料(定性分析)

- 铸铁

- 钢

- 合金底座

- 其他材料

- 按最终用户产业

- 油和气

- 化学

- 水/污水

- 电力

- 食品和饮料

- 製药

- 其他最终用户产业

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东/非洲

第七章竞争形势

- 公司简介

- ALFA LAVAL

- CIRCOR International Inc.

- Crane Co.

- Castel SRL

- Sanhua USA

- Curtiss-Wright Corporation

- Danfoss A/S

- Emerson Electric Co

- Georg Fischer Ltd

- Flowserve Corporation

- Hitachi Ltd

- Honeywell International Inc.

- KITZ Corporation

- Mueller Water Products Inc

第八章投资分析

第九章 市场未来展望

The Ball Valve Market size is estimated at USD 12.62 billion in 2024, and is expected to reach USD 15.57 billion by 2029, growing at a CAGR of 3.70% during the forecast period (2024-2029).

A significant rise in the demand for oil and gas is expected to be one of the significant factors contributing to the ball valve market growth. Additionally, rapid industrialization and urbanization are other essential factors supporting the development of the studied market.

Key Highlights

- The ball valve is essentially a valve that requires a quarter-turn to operate and is well-suited for clean gas-compressed air and liquid service in industrial applications, owing to its ability to provide a secure shutoff. However, when used for slurry service, measures must be taken to prevent the accumulation of debris. Furthermore, these valves are incredibly robust and highly suitable for applications requiring a simple on/off action. They're also highly durable and maintain consistent performance even after many use cycles.

- Ball valves are the most widely adopted fluid shutoff valves among oil and gas production facilities. These valves are also used in fuel gas systems feeding furnaces. Such applications make the oil-producing regions and regions with huge oil refining capacities attractive targets for the product vendors. Furthermore, as such plants are developed on tender floatation, the market vendors with partnerships and collaborations with such solution providers are expected to have a competitive advantage.

- Among all the types of materials, stainless steel is gaining and is expected to witness importance since they are more corrosion-resistant. Because valves open and close frequently, corrosion can cause significant issues. These valves hold up much better to harsher water types, which can benefit food processing plants. The fact that stainless steel valves also have a higher pressure rating than other materials, such as brass, further drives their adoption.

- Furthermore, the availability of ball valves in different variants, such as unidirectional, bidirectional, or multi-directional, depending on valve ports and the valve seat number, also complements their industrial adoption. These valves are also manufactured based on the classification for high-pressure or low-pressure pipelines, further expanding their use cases. Several vendors are constantly investing in innovative new products, which is acting as one of the major factors driving the market.

- The advancements in valve technology, including the emergence of smart valves and the incorporation of automation and control systems, present fresh prospects in the market. The rising environmental concerns and regulatory mandates fuel the need for eco-friendly and energy-efficient valves. Manufacturers who provide ball valves with minimized emissions, low leakage rates, and enhanced energy efficiency can seize the expanding demand for sustainable solutions.

- Ball valves are commonly employed in larger bore sizes, as alternative valve types like butterfly valves tend to have smaller and weaker stems. In situations where space constraints and structural load are paramount, such as offshore drilling platforms and floating production storage and offloading (FPSOs), users opt for alternatives to ball valves. Furthermore, the limited precision in flow rate control poses a challenge to the growth of the examined market.

- The impact of COVID-19 was different on the vendors since some offer and service ball valves for the food industry, while others offer only for the oil and gas sector. The pandemic less impacted vendors catering to food processing since the manufacturing of food-related items was deemed an essential service, and those facilities worked extra hours to fulfill the demand. However, with the pandemic-led restriction almost removed from everywhere and industries returning to their full-scale operational capabilities, the studied market is expected to experience upward growth during the forecast period.

Ball Valve Market Trends

Food Processing Industry Expected to Have Significant Applications

- The food processing industry is a notable sector where ball valves find significant application. The process of product fillings necessitates the maintenance of a regulated flow, making ball valves an essential component. The valves employed in the industry are of two types: those that come in direct contact with the material and those used in utility services such as water and steam. In both cases, the valves must comply with several industry regulations, particularly those that come in contact with food material. This presents a considerable challenge for manufacturers to obtain regulatory approvals, requiring them to design valves that meet stringent industry standards.

- Ball valves are highly efficient in controlling and maintaining high volume, temperature, and pressure. In the food and beverage sector, sanitary ball valves are utilized to connect and regulate conveyance pipes, ensuring the purity, stability, and quality of fluids during transport due to their stainless steel construction. Sanitary valves are also easy to disinfect and clean, promoting hygiene. The market is expected to grow due to continuous product launches by various vendors.

- For instance, in November 2022, Valworx, a producer of actuated valves and equipment controls, recently introduced a novel range of hygienic ball valves suitable for deployment in the food and beverage manufacturing sector. These ball valves are equipped with a conspicuous position indicator and are compatible with Namur and ISO mountings. The valves are obtainable in two- and three-way configurations and available in various sizes ranging from 0.5 to 4 inches. The new line of valves conforms to the FDA, USDA, and 3-A standards.

- Stainless steel is increasingly recognized as a crucial material due to its extensive resistance to corrosion, a significant concern in the food processing sector. These valves have also demonstrated exceptional durability when exposed to more aggressive water compositions, offering notable advantages to food processing plants. Moreover, stainless steel valves possess a higher pressure rating compared to alternative materials like brass. For instance, a typical 1-inch brass ball valve may have a pressure rating of 600 PSI, whereas a standard stainless steel ball valve of the same size would likely have a pressure rating of 1000 PSI. This characteristic renders them particularly suitable for high-pressure applications within the food processing industry.

- The growing urbanization rate across various parts of the world significantly enhances the demand for packaged food. Changing lifestyles, especially in urban areas, also contribute to the ever-increasing demand for packaged and processed foods. To ensure food security and achieve self-sufficiency goals, various countries are making efforts such as making regulatory changes and developing special economic zones to develop food processing industries; for instance, in June 2022, USDA announced a fund of USD 375 million in support for meat and poultry processing plant projects in the United States. Such factors will create the demand for the ball valves for their extensive usage in the food industry.

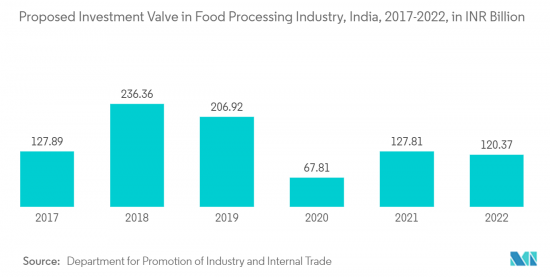

- A favorable scenario for the growth of the studied market has also been observed in other countries. The Department for Promotion of Industry and Internal Trade reported that the proposed investment in the food processing sector in India was valued at INR 120.37 billion (USD 1.47 billion) in 2022. Efforts are being taken to encourage investments across the entire value chain by the Indian Ministry of Food Processing Industries, including the implementation of the PLI scheme, which is expected to expand food processing capacity by nearly INR 30,000 crore (USD 3.6 billion) and create additional direct and indirect employment by the year 2026-27. Such initiatives are expected to offer significant opportunities for the ball valves.

North America is Expected to hold a Significant Market Share

- North America stands as a prominent market for ball valves, boasting substantial demand across diverse industries such as oil and gas, electricity, food and packaging, and chemicals. Both the United States and Canada exhibit immense demand, further fueled by the swift integration of industrial automation. The projected trend is expected to stimulate the market demand for ball valves in the region.

- North American area is witnessing a growing requirement for intelligent ball valves. Prominent regional industries are transitioning towards ball valves that incorporate processors and networking capabilities to complement advanced monitoring technology, which is coordinated through a central control station. The increased adoption of automation in process industries further reinforces this demand trend.

- The United States assumes a pivotal role in augmenting regional demand in contrast to Canada. The nation experiences a growing demand across nearly all end-user sectors, particularly in oil and gas, refining, and power generation. Higher energy consumption is the primary factor behind the higher demand across these sectors. For instance, according to EIA, total immediate energy consumption in the United States in 2022 was about 102.92 quadrillions Btu, of which petroleum consumption was about 31 percent.

- Furthermore, higher demand for oil & gas and other petroleum products also drives oil producers to increase their production and explore new oil extraction sites, which are expected to help the studied market grow further. For instance, in November 2022, the Canadian Association of Energy Contractors (CAOEC) announced that in 2023, it expects about 6,409 wells to be drilled in Canada, an approximately 15 percent increase from 2022.

- It is expected that new water treatment facilities will likely be set up in the region to feed the demand for ball valves as a result of an anticipated increase in regional population and increased water consumption across different sectors. A notable example is the recent announcement by New York State officials in September 2022, wherein they allocated over USD 232 million for water and sewer infrastructure projects in seven municipalities. The New York State Environmental Facilities Corporation granted funds and offered low-cost financing packages to facilitate water infrastructure initiatives with a cumulative expenditure exceeding USD 763 million. These investments in establishing treatment plants will inevitably augment the need for ball valves.

- Ball valves are utilized to regulate pressure and flow. Their leak-proof nature is a notable attribute that renders them highly advantageous, particularly in the chemical industry involving liquids. In July of 2022, BASF declared its final investment decision on a project worth USD 780 million, aimed at doubling the production capacity of its chemical manufacturing complex in Ascension Parish, Louisiana. The expansion project, which spans over seven years and represents a combined capital investment of over USD 1 billion, will enable the company In order to meet the growing demand for its products in a variety of sectors, such as construction, appliances, road haulage, and automobiles throughout North America.

Ball Valve Industry Overview

The ball valve market is fragmented and consists of several players, with no group currently holding a major share in the market. The companies are engaging in mergers and acquisitions to increase their expertise in the product. The market is viewed as a lucrative investment opportunity due to its wide consumer base. Some key market players include Flowserve Corporation, Alfa Laval, Crane Co., Honeywell International Inc., etc.

In November 2022, Klinger Fluid Control launched a more robust ball valve, Monoball KHO. According to the company, this valve has a neatly cast housing that can absorb even more force than the previous model. Furthermore, these valves are available in various models and with threads or flanges that can be adapted to customer requirements.

In November 2022, Danfoss launched its new discharge solution for oil-free systems. According to the company, these new check and stop valves incorporate a damped nozzle check valve, stop valves, and diffuser function to address the application requirements. Furthermore, the decoupled stop and check functions of the system allow fast access and improve the reliability of sealing, while the lock ring design prevents unintentional ball valve closes.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Industrialization in Various Countries

- 5.1.2 Growing Demand for ProcessSafety

- 5.2 Market Challenges

- 5.2.1 Downtime Due to Repairing of Valves

6 MARKET SEGMENTATION

- 6.1 By Material (Qualitative Analysis)

- 6.1.1 Cast Iron

- 6.1.2 Steel

- 6.1.3 Alloy Based

- 6.1.4 Other Materials

- 6.2 By End-User Industry

- 6.2.1 Oil and Gas

- 6.2.2 Chemicals

- 6.2.3 Water and Waste Water

- 6.2.4 Power

- 6.2.5 Food and Beverage

- 6.2.6 Pharmaceutical

- 6.2.7 Other End-User Industries

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia-Pacific

- 6.3.4 Latin America

- 6.3.5 Middle East & Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 ALFA LAVAL

- 7.1.2 CIRCOR International Inc.

- 7.1.3 Crane Co.

- 7.1.4 Castel SRL

- 7.1.5 Sanhua USA

- 7.1.6 Curtiss-Wright Corporation

- 7.1.7 Danfoss A/S

- 7.1.8 Emerson Electric Co

- 7.1.9 Georg Fischer Ltd

- 7.1.10 Flowserve Corporation

- 7.1.11 Hitachi Ltd

- 7.1.12 Honeywell International Inc.

- 7.1.13 KITZ Corporation

- 7.1.14 Mueller Water Products Inc

8 INVESTMENT ANALYSIS

9 FUTURE OUTLOOK OF THE MARKET

医用气体和设备市场:按产品、供应型态、应用和最终用途 - 全球预测 2024-2030

医用气体和设备市场:按产品、供应型态、应用和最终用途 - 全球预测 2024-2030 球阀市场:按类型、材质、尺寸、行业划分 - 2024-2030 年全球预测

球阀市场:按类型、材质、尺寸、行业划分 - 2024-2030 年全球预测 2024-2032 年按气体类型、应用、最终用户和地区分類的医用气体市场报告

2024-2032 年按气体类型、应用、最终用户和地区分類的医用气体市场报告 医用气体和设备市场 - 2024年至2029年预测

医用气体和设备市场 - 2024年至2029年预测 全球医用气体和设备市场规模、份额、成长分析(按类型、按应用) - 按行业预测,2024-2031 年

全球医用气体和设备市场规模、份额、成长分析(按类型、按应用) - 按行业预测,2024-2031 年 2024 年球阀世界市场报告

2024 年球阀世界市场报告 全球医用气体和设备市场:2024 年

全球医用气体和设备市场:2024 年 医用气体压力调整器 - 全球市场的考察,竞争情形,市场预测(2030年)

医用气体压力调整器 - 全球市场的考察,竞争情形,市场预测(2030年) 陶瓷球阀市场报告:2030 年趋势、预测与竞争分析

陶瓷球阀市场报告:2030 年趋势、预测与竞争分析 医用气体市场、份额、规模、趋势、行业分析报告:按产品、按应用、按最终用途、按地区、按细分市场、预测,2024-2032 年

医用气体市场、份额、规模、趋势、行业分析报告:按产品、按应用、按最终用途、按地区、按细分市场、预测,2024-2032 年