|

市场调查报告书

商品编码

1404498

FPGA(现场可程式闸阵列):2024-2029 年市场占有率分析、产业趋势与统计、成长预测Field Programmable Gate Array (FPGA) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

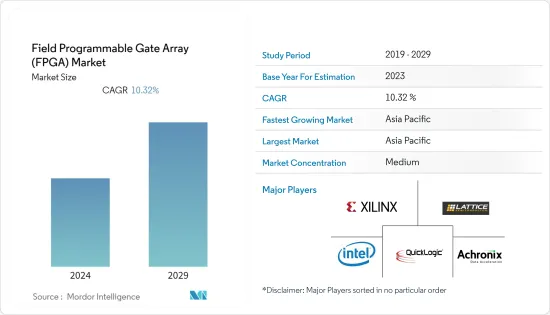

FPGA(现场可程式闸阵列)市场上年度为69亿美元,预计未来五年将达到124.4亿美元,复合年增长率为10.32%。

资料中心和高效能运算的高度部署预计将在预测期内推动 FPGA 需求。例如, 资料年 3 月,NTT 计划未来三个月在印度推出 6 个资料中心,另外 3 个正在建设中。 NTT India MD Sharad Sanghi 表示,这些资料中心近 70% 的相同容量已被预留。该公司计划在 6 月底前再推出 6 个资料中心,使印度运作的资料中心总数达到 11 个。

主要亮点

- FPGA(现场可程式闸阵列)包含具有可程式硬体结构的电路。与 ASIC 和 GPU 不同,FPGA 晶片内的电路不是硬蚀刻的,可以根据需要重新编程。这项特性使 FPGA 成为 ASIC 的合适替代品,因为 ASIC 需要较长的开发时间和大量的设计和製造投资。

- FPGA 在科技产业中用于机器学习和深度学习。微软研究院展示了过去十年来在 FPGA 上使用人工智慧的首批使用案例之一,作为该公司加速网路搜寻努力的一部分。 FPGA 结合了可编程性、速度和弹性,可提供高效能,而无需开发客製化专用积体电路 (自订) 的高成本和复杂性。 FPGA 也用于微软的搜寻引擎Bing,展示了 FPGA 在深度学习应用上的实用性。据该公司称,Bing 使用 FPGA 来加速搜寻排名,实现吞吐量提高 50%。

- 此外,FPGA 还支援整合 AI 的硬体定制,并且可以透过程式设计提供类似 ASIC 和 GPU 的行为。 FPGA 的可重新配置和可重新编程特性使其非常适合快速发展的人工智慧领域,使设计人员能够快速测试演算法并将其快速推向市场。与 ASIC 相比,高功耗限制了市场成长。能源效率一直是各行业关注的重点。电子设备产业一直在寻找低功耗的设备。 FPGA 功耗较高,程式设计师无法控制功耗优化。

- 此外,5G 网路基础设施技术开发的成长和进步、FPGA 在各个最终用户产业中的使用不断增加是推动所研究的市场成长的一些因素。例如,2022年6月,爱立信在德克萨斯州投资超1亿美元建设节能5G智慧工厂。该工厂展示了由 5G 连接支援的创新技术,包括自主机器人和扩增实境(AR) 培训。

- 此外,市场上的各个参与者都在不断投资最新技术来开发创新产品。例如,2023 年 1 月,FPGA新兴企业Rapid Silicon 筹集了 1,500 万美元,将其首款晶片推向市场。本轮资金筹措将用于投资 Rapid Silicon 的产品系列,帮助推出低端 FPGA 领域的优质产品,并巩固公司将开放原始码软体应用于商业应用的势头。

- 由于 COVID-19大流行,政府、企业和学术机构对资料中心、人工智慧和机器学习的需求激增。这种成长对 FPGA 需求产生了正面影响。预计在预测期内将保持相同的速度,有助于普及FPGA 在各个最终用户产业中的影响力和重要性。

FPGA(现场可程式闸阵列)市场趋势

物联网需求的增加预计将推动市场成长

- 并行执行是 FPGA 的关键优势,因为多个感测器(例如湿度和温度检测器)检测器处于活动状态。 FPGA 对于物联网来说非常节能,因为无需花时间循环或暂停延迟。根据《2022 年物联网现况》报告,全球连网物联网设备将增加 18%,达到 144 亿台。到 2025 年,这一数字预计将超过 300 亿,平均每人拥有近 4 个连网物联网设备。

- 预计在预测期内,物联网的需求将进一步增加,这意味着对半导体和其他组件的需求增加。根据SEMI预测,到2025年,物联网设备所需的半导体和感测器规模预计将达到1,142亿美元。

- 随着物联网设备的快速增加,建构物联网设备的晶片需求预计也会在预测期内上升。加上晶片小型化,降低消费量成为製造商的首要任务。

- 根据爱立信的数据,2022 年短距离物联网连接设备的销售额为 139.39 亿美元,广域物联网连接设备的销售额为 26.96 亿美元。此外,预计到2026年将分别达到206.49亿美元和58.85亿美元。

- 物联网有望成为产生重大创新、推广新商业模式并以多种方式加强全球社会的主要驱动力。市场开拓供应商正在开发 FPGA 并将其整合到物联网设备和解决方案中。例如,Intel Stratix 10 等英特尔 FPGA 解决方案由于其固有的软体和硬体可编程性,可实现可扩展性和弹性,以满足物联网要求。

亚太地区预计将占据主要市场占有率

- 亚太地区是 FPGA 产业参与者的重要地区。在亚太地区,中国、印度、韩国和台湾等许多国家的消费性电子产业在过去几年中出现了显着成长。因此,该地区的 FPGA 需求被视为一个影响点。

- 根据SEMI(半导体设备与材料国际)的数据,中国在半导体设备的支出最多,其次是韩国、台湾和日本。此外,预计中国大陆今年仍将是半导体製造设备的最大支出国,而台湾地区预计将在 2024 年重返榜首。此外,中国政府鼓励国家龙头企业和顶尖数位公司发展国内半导体製造能力,以恢復中国对海外半导体需求的依赖平衡。这些努力可能会进一步提振半导体市场并推动对 FPGA 的需求。

- 此外,冠状病毒引发的居家趋势大流行推动对半导体晶片的需求。例如,根据WSTS预测,2023年亚太地区半导体产业收入预计将达到4,119.7亿美元。这些趋势正在鼓励主要半导体製造商进入亚太市场。例如,市场上最着名的参与者之一 ASML 最近在台南开设了一个独特的、最先进的培训设施。

- 同样,2022年11月,日月光半导体工程(ASE)宣布将投资3亿美元扩大马来西亚生产基地。此外,中国国务院《国家积体电路产业发展指南》提出了2030年在半导体所有领域成为全球领导者的目标。

- 此外,「中国製造2025」计画支持获取有关先进半导体製造的知识,这是中国未来经济和社会的关键要素。此外,该国最近在医疗保健领域投资了 5,740 亿美元,这可能会进一步推动所研究的市场成长。

- 此外,5G 的采用在网路和装置领域都在蓬勃发展。根据爱立信移动的报告,5G用户预计比4G早两年达到10亿。主要因素包括中国比4G更早进行5G,设备由多个供应商及时提供。近年来,中国通讯业经历了快速发展,预计这种情况将持续到2025年。人口、通讯服务和智慧型手机使用的成长正在刺激该行业的发展。中国的市场开拓大部分以优质连结和内容服务为主。

- 中国正在为FPGA市场的扩张铺路。由于其作为国际家用电子电器製造商的重要地位,该国的需求正在增长。中国是全球最大的製造地,生产全球36%的电子产品,包括智慧型手机、电脑、云端伺服器和通讯基础设施,成为全球电子供应链中最重要的节点。人工智慧在中国的普及,为中国电力市场带来了新的开拓。智慧家庭和物联网 (IoT) 可能是 FPGA 製造商未来十年的主要发展方向。

FPGA(现场可程式化闸阵列)产业概述

FPGA(现场可程式闸阵列)市场较为分散。市场参与企业正在采取联盟和收购等策略来加强其产品供应并获得永续的竞争优势。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场洞察

- 市场概况

- 产业价值链分析

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 竞争公司之间的敌对关係

- 替代品的威胁

- 宏观经济走势对产业的影响

第五章市场动态

- 市场驱动因素

- 物联网需求增加

- 市场抑制因素

- 与 ASIC 相比功耗较高

第六章市场区隔

- 按配置

- 高阶FPGA

- 中端 FPGA/低阶 FPGA

- 依架构

- 基于SRAM的FPGA

- 基于耐熔熔丝的 FPGA

- 基于快闪记忆体的FPGA

- 按最终用户产业

- 资讯科技/通讯

- 消费性电子产品

- 车

- 工业的

- 军事/航太

- 其他的

- 按地区

- 北美洲

- 美国

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 其他欧洲国家

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 其他亚太地区

- 拉丁美洲

- 巴西

- 阿根廷

- 墨西哥

- 其他拉丁美洲

- 中东/非洲

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 南非

- 其他中东/非洲

- 北美洲

第七章竞争形势

- 公司简介

- Xilinx Inc.

- Lattice Semiconductor Corporation

- Quicklogic Corporation

- Intel Corporation

- Achronix Semiconductor Corporation

- GOWIN Semiconductor Corporation

- Microchip Technology Incorporated

- Efinix Inc.

第八章供应商市场占有率分析

第九章投资分析

第10章市场的未来

The Field Programmable Gate Array (FPGA) Market was valued at USD 6.9 billion in the previous year and is expected to grow at a CAGR of 10.32%, reaching USD 12.44 billion by the next five years. High deployment of data centers and high-performance computing is expected to propel the demand for the FPGA in the forecasted period. For instance, in March 2023, NTT intends to launch six data centers in India over the next three months, with three more in the works. Almost 70 percent of the identical capacity in these data centers has already been booked, according to NTT India MD Sharad Sanghi. The company will launch six additional data centers by the end of June, bringing its total number of operating data centers in the country to 11.

Key Highlights

- Field programmable gate arrays (FPGAs) incorporate circuits with a programmable hardware fabric. Unlike ASICs or graphics processing units (GPUs), the circuitry inside an FPGA chip is not hard etched; it can be reprogrammed as required. This capability makes FPGAs a suitable alternative to ASICs, which need a long development time and a significant investment to design and fabricate.

- FPGAs are used in the technology industry for machine learning and deep learning. Microsoft Research displayed one of the first use cases of AI on FPGAs in the last decade as part of the company's efforts to speed up web searches. FPGAs provide a combination of programmability, speed, and flexibility, delivering performance without high cost and complexity to develop custom application-specific integrated circuits (ASICs). Microsoft's Bing search engine also uses FPGAs in production, indicating their value for deep learning applications. According to the company, Bing realized a 50% increase in throughput using FPGAs to accelerate search ranking.

- In addition, FPGAs deliver hardware customization with integrated AI and can be programmed to provide behavior like an ASIC or a GPU. The reconfigurable, reprogrammable nature of an FPGA makes itself well suited for a rapidly evolving AI landscape, enabling designers to test algorithms quickly and get to market fast. High Power Consumption Compared to ASIC restraining the market growth. Energy efficiency has always been a significant concern across various industries. Industries incorporating electronic devices always seek low-power-consuming devices. In FPGAs, power consumption is higher, and programmers do not have any control over power optimization.

- Furthermore, growth and advancement in technology development for 5G networking infrastructure and an increase in the use of FPGA in various end-user industries are some of the factors driving the studied market growth. For instance, in June 2022, Ericsson invested over USD 100 million in its energy-efficient 5G smart factory in Texas, where the equipment powering 5G networks across the United States is constructed. The factory showcases innovation powered by 5G connectivity, with abilities such as autonomous robots, augmented reality training, and many more.

- In addition, various players in the market are continuously investing in the latest technology to develop innovative products. For instance, in January 2023, FPGA startup Rapid Silicon landed USD 15 million to bring its first chip to market. The round of funding will be used to invest in Rapid Silicon's product portfolio, support its premier low-end FPGA product launch, and build on the company's momentum in adopting open-source software for commercial applications.

- The demand for data centers, artificial intelligence, and machine learning across government, enterprises, and academic entities is witnessing exponential growth due to the COVID-19 pandemic. This growth has positively impacted the need for FPGAs. It is predicted to maintain the same pace in the forecasted period, helping spread the impact and significance of FPGAs in various end-user industries.

Field Programmable Gate Array (FPGA) Market Trends

Increasing Demand for IoT is Expected to Drive the Market Growth

- Parallel execution is a crucial benefit of FPGAs, as several sensors, like humidity and temperature detectors, operate constantly. Since no time is required to be spent on looping and pausing for the delay, FPGAs are more power-efficient for IoT. According to the State of the IoT 2022 report, connected IoT devices are increasing by 18% to 14.4 billion globally. By 2025, this number is predicted to be over 30 billion, nearly 4 IoT devices per person on average.

- The demand for IoT is anticipated to increase even further during the forecast period, which signifies a boost in demand for semiconductors and other components. According to SEMI, the size of the semiconductor and sensor needed for IoT devices is expected to reach USD 114.2 billion by 2025.

- With the rapid increase in the number of IoT devices, chip requirement for building IoT instruments is also expected to rise during the forecast period. Reducing energy consumption, combined with the miniaturization of chips, will be prioritized by manufacturers.

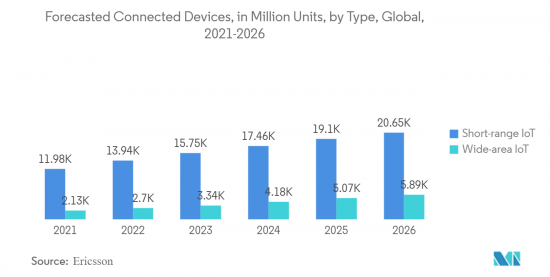

- According to Ericsson, short-range IoT-connected devices recorded USD 13,939 million, and wide-area IoT-connected instruments recorded USD 2,696 million in 2022. Further, it is anticipated to reach USD 20,649 million and USD 5,885 million in 2026.

- IoT promises to be a major driving force that would create significant innovation, facilitate new business models, and enhance global society in multiple ways. Market vendors develop FPGAs to integrate them into IoT devices and solutions. For instance, Intel FPGA solutions, such as Intel Stratix 10, allow scalability and flexibility to address IoT requirements with inherent software and hardware programmability.

Asia Pacific is Expected to Hold Significant Market Share

- The Asia Pacific is a significant region for the players operating in the FPGA industry. Within the Asia Pacific, many nations, including China, India, South Korea, Taiwan, and others, have seen an enormous increase in the consumer electronics industry in the past few years. As a result, the FPGA demand in the area is seen as an influence point.

- According to the Semiconductor Equipment and Material International (SEMI), China is a significant spender on semiconductor equipment, followed by South Korea, Taiwan, and Japan. Furthermore, China is expected to maintain the top position in semiconductor equipment spending this year, while Taiwan is anticipated to regain the lead in 2024. In addition, the Chinese government encouraged its national champions and top digital enterprises to develop their domestic semiconductor manufacturing capacities to rebalance China's reliance on overseas semiconductor demand. Such an initiative may further boost the semiconductor market, propelling the demand for FPGA.

- Furthermore, the stay-at-home trend spurred by the coronavirus pandemic continues to drive the demand for semiconductor chips. For instance, according to WSTS, the estimated semiconductor industry revenue in the Asia Pacific region will reach USD 411.97 billion in 2023. Such trends encourage leading semiconductor manufacturers to enter the Asia Pacific market. For instance, ASML, one of the most prominent players in the market, recently opened a unique state-of-the-art training facility in Tainan.

- Similarly, in November 2022, Advanced Semiconductor Engineering (ASE) announced a USD 300 million investment to expand its production site in Malaysia. Moreover, China's State Council's "National Integrated Circuit Industry Development Guidelines" set the aim of becoming a global player in all semiconductor industry segments by 2030.

- In addition, the Made in China 2025 initiative supports achieving knowledge about advanced semiconductor manufacturing as a critical component of China's future economy and society. In addition, the country recently spent USD 574 billion in the healthcare sector, which may further drive the studied market growth.

- Furthermore, 5G adoption is rising in momentum for both the network and device domains. According to the report, Ericson Mobility 5G subscriptions are predicted to reach 1 b, two years earlier than 4G. Key factors include China's earlier engagement with 5G, compared to 4G, and the timely availability of instruments from several vendors. The Chinese telecom sector experienced rapid evolution in recent years, which is expected to continue until 2025. Increased population, communication services, and smartphone use fuel the industry's development. Premium connectivity and content services in China account for the majority of the market development in the country.

- China is paving the way for the FPGA market to expand. The country's demand is extending due to its significant position as the international manufacturer of consumer electronics gadgets. China is the world's largest manufacturing hub, producing 36% of the world's electronics, including smartphones, computers, cloud servers, and telecom infrastructure, establishing the country as the global electronics supply chain's most important node. The popularity of AI in China opened up a new development potential for the Chinese consumer electronics market. Smart homes and IoT (Internet of Things) will likely be significant development potential for manufacturers of FPGA in the next decade.

Field Programmable Gate Array (FPGA) Industry Overview

The Field Programmable Gate Array (FPGA) Market is moderately fragmented with the presence of major players like Xilinx Inc., Lattice Semiconductor Corporation, Quicklogic Corporation, Intel Corporation, and Achronix Semiconductor Corporation. Players in the market are adopting strategies such as partnerships and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

- December 2022- Lattice announced its first devices based on this latest platform, Lattice Avant-E FPGAs, which are developed to solve critical customer challenges at the Edge by combining class-leading energy efficiency, size, and performance with an optimized characteristic set tailored to the requirements of edge applications like data processing and AI.

- February 2022- QuickLogic Corporation announced that its PolarPro 3 family of low-power, SRAM-based FPGAs was available to solve semiconductor supply availability challenges. This favorably flexible family features power consumption lower than 55uA and a tiny footprint in small packages and die options.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Intensity of Competitive Rivalry

- 4.3.5 Threat of Substitutes

- 4.4 Impact of Macro Economic trends on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Demand for IoT

- 5.2 Market Restraints

- 5.2.1 High Power Consumption Compared to ASIC

6 MARKET SEGMENTATION

- 6.1 By Configuration

- 6.1.1 High-end FPGA

- 6.1.2 Mid-range FPGA/Low-end FPGA

- 6.2 By Architecture

- 6.2.1 SRAM-based FPGA

- 6.2.2 Anti-fuse Based FPGA

- 6.2.3 Flash-based FPGA

- 6.3 By End-user Industry

- 6.3.1 IT and Telecommunication

- 6.3.2 Consumer Electronics

- 6.3.3 Automotive

- 6.3.4 Industrial

- 6.3.5 Military and Aerospace

- 6.3.6 Other End-user Industries

- 6.4 By Geography

- 6.4.1 North America

- 6.4.1.1 United States

- 6.4.1.2 Canada

- 6.4.2 Europe

- 6.4.2.1 Germany

- 6.4.2.2 United Kingdom

- 6.4.2.3 France

- 6.4.2.4 Rest of Europe

- 6.4.3 Asia Pacific

- 6.4.3.1 China

- 6.4.3.2 Japan

- 6.4.3.3 India

- 6.4.3.4 South Korea

- 6.4.3.5 Rest of the Asia Pacific

- 6.4.4 Latin America

- 6.4.4.1 Brazil

- 6.4.4.2 Argentina

- 6.4.4.3 Mexico

- 6.4.4.4 Rest of Latin America

- 6.4.5 Middle East and Africa

- 6.4.5.1 United Arab Emirates

- 6.4.5.2 Saudi Arabia

- 6.4.5.3 South Africa

- 6.4.5.4 Rest of Middle East and Africa

- 6.4.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Xilinx Inc.

- 7.1.2 Lattice Semiconductor Corporation

- 7.1.3 Quicklogic Corporation

- 7.1.4 Intel Corporation

- 7.1.5 Achronix Semiconductor Corporation

- 7.1.6 GOWIN Semiconductor Corporation

- 7.1.7 Microchip Technology Incorporated

- 7.1.8 Efinix Inc.

8 VENDOR MARKET SHARE ANALYSIS

9 INVESTMENT ANALYSIS

10 FUTURE OF THE MARKET

嵌入式FPGA(现场可程式闸阵列)2024 年全球市场报告

嵌入式FPGA(现场可程式闸阵列)2024 年全球市场报告 2024-2032 年按架构、配置、最终用途产业和地区分類的现场可程式闸阵列市场报告

2024-2032 年按架构、配置、最终用途产业和地区分類的现场可程式闸阵列市场报告 嵌入式 FPGA (eFPGA) 市场,按技术、按应用、按国家和地区划分 - 2024-2032 年行业分析、市场规模、市场份额和预测

嵌入式 FPGA (eFPGA) 市场,按技术、按应用、按国家和地区划分 - 2024-2032 年行业分析、市场规模、市场份额和预测 2024 年现场可程式闸阵列全球市场报告

2024 年现场可程式闸阵列全球市场报告 FPGA 市场报告:2030 年趋势、预测与竞争分析

FPGA 市场报告:2030 年趋势、预测与竞争分析 嵌入式 FPGA 市场报告:2030 年趋势、预测与竞争分析

嵌入式 FPGA 市场报告:2030 年趋势、预测与竞争分析 现场可程式闸阵列(FPGA) 市场报告:2030 年趋势、预测与竞争分析

现场可程式闸阵列(FPGA) 市场报告:2030 年趋势、预测与竞争分析 FPGA(现场可程式闸阵列)市场、份额、市场规模、趋势、产业分析报告:按类型、技术、应用、地区、细分市场预测,2024-2032 年

FPGA(现场可程式闸阵列)市场、份额、市场规模、趋势、产业分析报告:按类型、技术、应用、地区、细分市场预测,2024-2032 年 现场可程式闸阵列市场:按配置、架构、类型、製程节点和最终用户划分 - 2024-2030 年全球预测

现场可程式闸阵列市场:按配置、架构、类型、製程节点和最终用户划分 - 2024-2030 年全球预测 全球FPGA市场(~2029):配置(低端FPGA、中端FGA、高阶FPGA)、技术(SRAM、快闪记忆体、抗熔丝)、节点尺寸(16 nm、20-90 nm、90 nm以上) , 产业(通讯、资料中心与计算、汽车)/按地区

全球FPGA市场(~2029):配置(低端FPGA、中端FGA、高阶FPGA)、技术(SRAM、快闪记忆体、抗熔丝)、节点尺寸(16 nm、20-90 nm、90 nm以上) , 产业(通讯、资料中心与计算、汽车)/按地区