|

市场调查报告书

商品编码

1405722

汽车边缘运算 -市场占有率分析、产业趋势与统计、2024-2029 年成长预测Edge Computing In Automotive - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

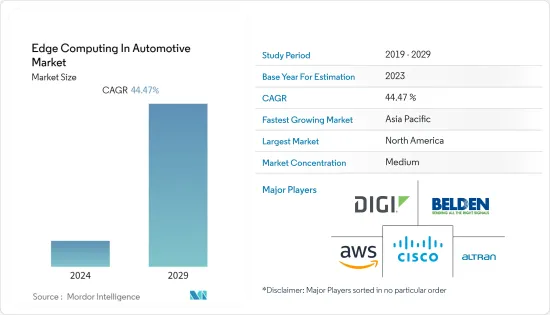

汽车边缘运算市场目前市场规模为14.3亿美元,预计未来五年将成长至90.1亿美元,预测期内复合年增长率为44.47%。

自动驾驶汽车和联网汽车基础设施的发展,以及对提高边缘运算解决方案效率的轻量级框架和系统的需求,预计将为边缘运算供应商创造丰富的机会。

主要亮点

- 汽车行业的公司开始透过实施各种技术创新来追求新的性能和生产力水平,包括感测器、其他资料生成和收集设备以及分析工具。传统上,资料管理和分析是在云端或资料中心完成的。然而,随着智慧製造和智慧城市等网路相关技术和措施的日益普及,这种情况似乎正在改变。

- 为了让连网型汽车提供预期价值,需要能够即时合成这些资料的设备。边缘运算是一种处理 IoT(物联网)设备产生的资料的方法。在边缘,收集的资料在源头进行审查。

- 此外,以更快的速度处理配备各种感测器的工业连网型和连网汽车产生的越来越多的资料是一个问题,而5G应用将以低延迟和高可靠性解决此类问题,从而轻鬆卸载一些资料。此处理需要云端基础的伺服器,从而最大限度地降低复杂性。

- 此外,单一所有者的生态系统不存在「全球」边界,由大量必须透过网路协作的个人管理,这使得生态系统更加脆弱。您的基础设施的某些部分可能会受到高度局部的攻击,并产生局部影响。

- COVID-19 大流行对 5G 和多接入边缘运算 (MEC) 部署产生了积极影响,因为企业将服务速度和低延迟作为差异化因素制定了策略。网路和运算的更紧密整合以支援次世代应用程式是未来的挑战。

汽车边缘运算市场趋势

物联网的普及正在推动汽车边缘运算市场的成长

- 物联网技术正在克服製造业的劳动力短缺问题。对于越来越多的企业来说,机器人化等工业4.0技术的使用正成为日常业务的一部分。

- 使用边缘网路上的物联网设备收集和传输资料的机器人可以比使用云端基础的设计更快地检测异常并消除低效率。此类系统由于其分散式设计而更具弹性,并且还保证了更高水准的执行时间生产力。

- 5G 营运将加速物联网在汽车产业的日益普及,这主要得益于低延迟和网路切片功能。很大一部分工业IoT服务供应商和聚合商现在提供支援 5G 的网路选项,并预计在未来几年内整合边缘运算来处理大量资料。

- 边缘运算的潜力正在改变工业製造。未来几十年,边缘运算应用将从根本上改变製造业,因为它们可以提高效率和产量,同时降低成本。这可能会与新一代智慧型物联网边缘设备结合来实现。预计这将对预测期内的市场成长产生积极影响。

- 此外,企业采用云端主要是因为其弹性、扩充性和成本效益,这有助于在所研究的市场中提高车辆功能。

北美占最大市场占有率

- 北美占据最大的市场占有率,由于该地区的消费者和商业部门依赖物联网设备,预计在整个预测期内将保持其主导地位。该地区越来越多地采用云端技术并走向技术化。该地区还正在经历自动驾驶汽车等创新概念的市场开拓,预计这将在未来几年推动该地区的市场成长。

- 此外,由于边缘运算供应商数量庞大以及北美公司对利用 5G 等新技术的接受程度不断提高,该地区将在预测期内占据最大的市场。

- 2022 年 3 月,联邦机动车辆安全监管机构为无人驾驶汽车的开发和使用开了绿灯,无人驾驶汽车没有方向盘或踏板等手动控制装置。

- 5G技术仍处于实验阶段。不过,希望未来能结出硕果。例如,在美国,AT&T和Verizon正在进行现场测试。其中一些得到了企业合作伙伴的支持,例如美国最大的行动电话网站营运商 Crown Castle 以及边缘运算专家 VaporIO 的投资者。

汽车边缘运算概述

汽车市场边缘运算的竞争非常激烈,多家主要公司纷纷进入该市场。目前,占据大部分市场占有率的大公司寥寥无几,份额最大的是新兴市场,主要是北美和欧洲。在日本和中国等新兴市场,市场高度混乱,区域和本地经销商占据主导地位。国际参与者已经意识到潜在商机的巨大性,并逐渐建立供应网络并透过併购进入这些非结构化市场。

2023 年 1 月,百通宣布推出单对乙太网路 (SPE) 连接产品组合,旨在优化乙太网路连接在恶劣环境(包括工业和运输业务)中的潜力。 SPE 产品组合包括用于洁净区域连接的 IP20 级 PCB 插孔、插线和电线组,以及用于可靠现场设备工业乙太网连接的 IP65/IP67 级圆形 M8/M12插线、电线组和电线组。包含插座。

2022 年 11 月,Belden Inc. 宣布推出网路安全、强化和部署简单性解决方案,包括 Hirschmann GDME 重型阀门连接器和 Belden HorizonTM 边缘编配平台。该平台管理的软体能够安全地存取远端设备,同时保持 OT 设备和应用程式的安全且轻鬆的部署、连接和管理。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场洞察

- 市场概况

- 价值链/供应链分析

- 产业吸引力-波特五力分析

- 买家/消费者的议价能力

- 供应商的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争公司之间敌对关係的强度

第五章市场动态

- 市场驱动因素

- 物联网的采用率提高

- 资料量和网路流量呈指数级增长

- 市场抑制因素

- 初始基础建设投资

- 隐私和安全问题

第六章市场区隔

- 按用途

- 连网型汽车

- 交通管理

- 智慧城市

- 运输/物流

- 其他用途

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 世界其他地区

第七章 竞争形势

- 公司简介

- Altran Inc

- Belden Inc.

- Digi International Inc.

- Cisco Systems, Inc.

- Amazon Web Services(AWS), Inc.

- General Electric Company

- Hewlett Packard Enterprise Development LP

- Huawei Technologies Co., Ltd.

- Litmus Automation

- Azion Technologies Ltd.

第八章投资分析

第九章 市场机会及未来趋势

The Edge Computing in Automotive Market is valued at 1.43 billion in the current year and is expected to register a CAGR of 44.47% during the forecast period to become 9.01 billion by the next five years. The evolution of autonomous vehicles and connected car infrastructure and the requirement for lightweight frameworks and systems to heighten the efficiency of edge computing solutions are anticipated to generate abundant opportunities for edge computing vendors.

Key Highlights

- Enterprises across automotive are beginning to drive new levels of performance and productivity by deploying different technological innovations, like sensors and other data-producing and collecting devices, along with analysis tools. Traditionally, data management and analysis are performed in the cloud or data centers. However, the scenario seems to be changing with the increasing penetration of network-related technologies and initiatives, such as smart manufacturing and smart cities.

- For connected cars to give the value they are expected to, there is a device that can concoct this data in real time. Edge computing is the method of processing data from IoT (Internet of Things) devices where it is generated. With the edge, the data being gathered gets examined right at the source.

- Moreover, processing increasing amounts of data at a faster pace, generated by industrial robots and connected cars equipped with various sensors, is problematic, and 5G applications are solving such issues with their low latency and high reliability, making it easier to offload part of this processing need to edge or cloud-based servers, thus, minimizing the complexity.

- Additionally, the absence of a "global" border and an ecosystem with a single owner that is governed by numerous individuals who must cooperate through networks makes it even more vulnerable. A piece of the infrastructure may be under the control of highly localized attacks with localized impact.

- The COVID-19 pandemic positively affected the 5G and multi-access edge computing (MEC) deployments as businesses strategized service speed and low latency as key differentiators. Tight integration of network and compute to support next-generation apps is the way forward.

Edge Computing In Automotive Market Trends

Rising Adoption of IOT to Witness the Growth Edge Computing in Automotive Market

- IoT technologies are overcoming the labor shortage in the manufacturing sector. For more organizations, using Industry 4.0 technologies, like robotization, is part of day-to-day operations.

- Robots collecting and transferring data using IoT devices on an edge network can detect anomalies and eliminate inefficiencies far faster than they could use a cloud-based design. Such a system is substantially more resilient due to its distributed design, which also ensures higher levels of uptime productivity.

- The growing use of IoT in the automotive industry is accelerated by 5G operations, principally fueled by lower latency and network slicing capabilities. A sizable portion of industrial IoT service providers and aggregators currently offer 5 G-enabled network options, which are anticipated to incorporate edge computing over the next few years to handle the massive volume of data.

- Due to the potential of edge computing, industrial manufacturing is transforming. In the upcoming decades, edge computing applications will radically alter manufacturing to increase efficiency and production while lowering costs. This would be accomplished by combining them with a new generation of intelligent IoT edge devices. Over the projected period, this is expected to have a favorable effect on the market's growth.

- Furthermore, the adoption of the cloud in enterprises is primarily due to flexibility, scalability, and cost-effectiveness, which can help the advancement of vehicle capabilities in the studied market.

North America Occupies the Largest Market Share

- North America has accounted for the largest market share and is projected to maintain dominance throughout the forecast years as the consumer and business sectors in the region rely on IoT devices. Higher cloud adoption in the region contributes to the continued transition toward technology. The development of innovative concepts, such as autonomous cars, within the area is also expected to propel regional market growth in the years to come.

- Additionally, the region is anticipated to represent the largest market during the forecast period due to a significant number of edge computing suppliers and the growing acceptance of technology among North American businesses for utilizing new technologies, such as 5G.

- In March 2022, Federal vehicle safety regulators gave the go-ahead for developing and using driverless cars without manual controls like steering wheels or pedals.

- 5G technology is still in the testing stage. However, it is hoped that it will be fruitful in the future. For example, AT&T and Verizon conduct field tests in the United States. Some are backed by corporate partners, such as Crown Castle, the largest US mobile phone website operator and an investor in his Vapor IO, an edge computing specialist.

Edge Computing In Automotive Industry Overview

Edge computing in the automotive market is moderately competitive and consists of several major players. Few major companies today hold a disproportionate amount of the market share, which continues to be significant in all developed nations, particularly in North America and Europe. The market is highly disorganized in developing nations like Japan and China, where regional or local sellers predominate. International players are gradually creating supply networks and entering these unstructured marketplaces through mergers and acquisitions as they become aware of the significant potential opportunities.

In January 2023, Belden introduced its Single Pair Ethernet (SPE) portfolio of connectivity products designed to optimize Ethernet connection possibilities in harsh environments, including industrial and transportation operations. The SPE portfolio includes IP20-rated PCB jack, patch cords, and cord sets for clean-area connections and IP65/IP67-rated circular M8/M12 patch cords, cord sets, and receptacles for reliable field device industrial ethernet connections.

In November 2022 - Belden Inc. announced the launch of solutions for network security, ruggedization, and simplified deployment, including the Hirschmann GDME Heavy-Duty Valve Connectors and the Belden HorizonTM edge orchestration platform. The platform manages software that allows secure access to remote equipment while sustaining secure and easy deployment, connection, and management of OT devices and applications.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Value Chain / Supply Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Buyers/Consumers

- 4.3.2 Bargaining Power of Suppliers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rising Adoption of IOT

- 5.1.2 Exponentially Growing Data Volumes And Network Traffic

- 5.2 Market Restraints

- 5.2.1 Initial Capital Expenditure For Infrastructure

- 5.2.2 Privacy and Security Concerns

6 MARKET SEGMENTATION

- 6.1 By Application

- 6.1.1 Connected Cars

- 6.1.2 Traffic Management

- 6.1.3 Smart Cities

- 6.1.4 Transportation & Logistics

- 6.1.5 Other Applications

- 6.2 By Geography

- 6.2.1 North America

- 6.2.2 Europe

- 6.2.3 Asia-Pacific

- 6.2.4 Rest of the World

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Altran Inc

- 7.1.2 Belden Inc.

- 7.1.3 Digi International Inc.

- 7.1.4 Cisco Systems, Inc.

- 7.1.5 Amazon Web Services (AWS), Inc.

- 7.1.6 General Electric Company

- 7.1.7 Hewlett Packard Enterprise Development LP

- 7.1.8 Huawei Technologies Co., Ltd.

- 7.1.9 Litmus Automation

- 7.1.10 Azion Technologies Ltd.

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS

全球边缘人工智慧软体市场:按产品、按资料模式、按技术、按最终用途、按地区 - 预测到 2030 年

全球边缘人工智慧软体市场:按产品、按资料模式、按技术、按最终用途、按地区 - 预测到 2030 年 人工智慧边缘运算市场:按组件、资料来源、应用程式和最终用户划分 - 2025-2030 年全球预测

人工智慧边缘运算市场:按组件、资料来源、应用程式和最终用户划分 - 2025-2030 年全球预测 边缘安全市场:按组件、部署类型、组织规模、产业划分 - 2025-2030 年全球预测

边缘安全市场:按组件、部署类型、组织规模、产业划分 - 2025-2030 年全球预测 边缘运算市场:按组件、应用和最终用途划分 - 2025-2030 年全球预测

边缘运算市场:按组件、应用和最终用途划分 - 2025-2030 年全球预测 2024-2028年全球AI边缘运算市场

2024-2028年全球AI边缘运算市场 自动驾驶汽车市场的全球边缘运算 - 2024-2031

自动驾驶汽车市场的全球边缘运算 - 2024-2031 全球超大规模运算市场

全球超大规模运算市场 医疗保健边缘运算市场 - 全球产业规模、份额、趋势、机会和预测,细分、按组件、按应用、按组织规模、按地区、按竞争,2019-2029F

医疗保健边缘运算市场 - 全球产业规模、份额、趋势、机会和预测,细分、按组件、按应用、按组织规模、按地区、按竞争,2019-2029F 医疗保健边缘运算市场:按组件、应用程式和最终用户划分 - 2025-2030 年全球预测

医疗保健边缘运算市场:按组件、应用程式和最终用户划分 - 2025-2030 年全球预测 多接入边缘运算市场:按技术、产业划分 - 2025-2030 年全球预测

多接入边缘运算市场:按技术、产业划分 - 2025-2030 年全球预测