|

市场调查报告书

商品编码

1406064

氟介面活性剂-市场占有率分析、产业趋势与统计、2024年至2029年成长预测Fluorosurfactant - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

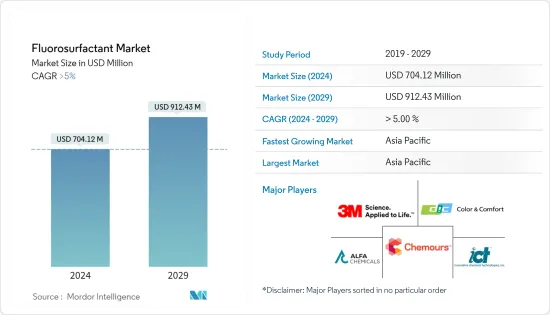

氟化介面活性剂市场规模预计2024年为7.0412亿美元,预计到2029年将达到9.1243亿美元,预测期内(2024-2029年)复合年增长率为5,预计增长超过%。

介面活性剂市场受到了 COVID-19 大流行的负面影响,由于油漆、被覆剂和清洁剂行业由于遏制措施和经济中断而被迫放慢生产,生产和运输放缓。目前市场正从疫情中恢復。预计2022年市场将达到疫情前水准并持续稳定成长。

由于油漆和涂料行业的需求不断增加,介面活性剂市场预计在预测期内将成长。

另一方面,与烃基和硅基介面活性剂相比,价格较高阻碍了市场成长。

此外,介面活性剂因其对腐蚀性化学品的高稳定性、高介电强度等而被用于电子涂料,预计将在预测期内创造市场机会。

亚太地区在全球整体市场中占据主导地位,其中消费量最高的国家是中国、印度和日本。

介面活性剂的市场趋势

油漆和涂料行业的需求不断增加

- 介面活性剂是具有疏水部分和亲水部分的两双亲性分子。疏水尾部是碳氟化合物,亲水部分根据电荷进行表征。

- 介面活性剂通常称为介面活性剂,可降低液体和气体之间、液体和固体之间或两个不混溶相之间的表面张力。这降低了漆膜的表面张力,从而获得更光滑、更好的漆面。

- 介面活性剂可改善颜料和基材的润湿性和流平性,提供较长的开放时间。由于氟的电负性高,且氟与碳原子之间的键非常稳定,因此氟基界面介面活性剂比其他介面活性剂更稳定,适用于各种条件,是优选的,很少见。

- 根据美国人口普查局的数据,2022 年私人建筑价值为 14,342 亿美元,比 2021 年的 12,795 亿美元增长 11.7%。 2022年住宅建设支出为8,991亿美元,比2021年的7,937亿美元成长13.3%。因此,建设活动的扩张预计将推动市场成长。

- 此外,过去30年中国油漆和涂料行业的销售成长领先世界其他地区。由于建设活动的增加,这一时期的快速都市化将国内建筑涂料行业推向了新的高度。

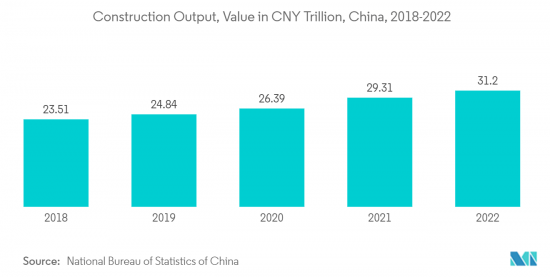

- 根据中国国家统计局的数据,中国的建筑产值将于 2022 年达到峰值,达到约 31.2 兆元(约 4.61 兆美元)。结果,这些因素往往会增加市场需求。

- 此外,德国拥有欧洲最大的建筑业。中国建设产业持续温和成长,主要得益于新建住宅建设项目数量的增加。该国拥有欧洲大陆最大的建筑存量,预计这一趋势在可预见的未来将持续下去。德国的目标是到 2050 年拥有近乎气候中立的建筑群,作为转型为永续能源系统的一部分。

- 由于上述因素,预计市场在预测期内将快速成长。

亚太地区主导市场

- 由于中国、印度和日本等国家的需求不断增加,预计亚太地区将在预测期内主导介面活性剂市场。

- 介面活性剂广泛应用于油漆和涂料行业。亚太地区建筑和施工对油漆和涂料的需求不断增长预计将推动市场发展。

- 在电子商务和办公空间需求增加的推动下,中国拥有庞大的建筑业。正因为如此,中国的商业建设不断增加。例如,中国是购物中心建设的领先国家之一。中国约有4,000家购物中心,预计到2025年还将开幕7,000家。这支持了预测期内的市场成长。

- 此外,印度正在扩大其商业部门。该国正在进行多个计划。例如,价值9亿美元的CommerzIII商业办公室综合大楼于2022年第一季动工。该计划涉及在孟买戈尔冈建造一座43层的商业办公综合体,允许占地面积为2,60,128平方公尺。该计划预计将于 2027 年第四季完成,为预测期内的市场成长做出贡献。

- 除了油漆和涂料外,介面活性剂也广泛应用于石油和天然气领域。印度石油和天然气部预计,2022年该国石油产品产量将超过2.543亿吨,比2021年的2.335亿吨增加8%以上。预计这将支持市场成长。

- 所有上述因素预计将在预测期内推动亚太地区介面活性剂市场的成长。

介面活性剂产业概况

介面活性剂市场因其性质而部分分散。研究市场中的主要企业(排名不分先后)包括 3M、Innovative Chemical Technologies、DIC CORPORATION、The Chemours Company、Alfa Chemicals 等。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第一章简介

- 调查先决条件

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场动态

- 促进因素

- 油漆和涂料行业的需求不断增加

- 扩大介面活性剂在油田的使用

- 其他司机

- 抑制因素

- 与其他介面活性剂相比价格高

- 其他阻碍因素

- 产业价值链分析

- 波特五力分析

- 供应商的议价能力

- 买方议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章市场区隔(市场规模)

- 类型

- 阴离子

- 阳离子

- 非离子型

- 双性恋

- 目的

- 油漆/被覆剂

- 清洁剂/清洗剂

- 油和气

- 阻燃剂

- 黏剂

- 其他应用(汽车、电子等)

- 地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 欧洲其他地区

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东/非洲

- 沙乌地阿拉伯

- 南非

- 其他中东/非洲

- 亚太地区

第六章竞争形势

- 併购、合资、联盟、协议

- 市场占有率(%)**/排名分析

- 主要企业策略

- 公司简介

- 3M

- Alfa Chemicals

- CYTONIX

- DIC CORPORATION

- DYNAX

- Innovative Chemical Technologies

- MAFLON SpA

- Merck KGaA

- TCI EUROPE NV

- The Chemours Company

第七章 市场机会及未来趋势

- 电子领域介面活性剂的使用增加

- 其他机会

The Fluorosurfactant Market size is estimated at USD 704.12 million in 2024, and is expected to reach USD 912.43 million by 2029, growing at a CAGR of greater than 5% during the forecast period (2024-2029).

The fluorosurfactant market was negatively impacted by the COVID-19 pandemic as there was a slowdown in production and mobility wherein industries, such as paints and coatings, detergents, etc., were forced to delay their production due to containment measures and economic disruptions. Currently, the market has recovered from the pandemic. The market reached pre-pandemic levels in 2022 and is expected to grow steadily in the future.

The fluorosurfactant market is expected to grow during the forecast period owing to the increasing demand from the paints and coatings industry.

On the flip side, higher price when compared to hydrocarbon and silicone-based surfactants, is hindering the market growth.

Further, the use of fluorosurfactants in electronic coatings, owing to their high stability to aggressive chemicals, high dielectric strength, etc., is predicted to generate a market opportunity during the forecast period.

Asia-Pacific region dominates the market across the globe, with the largest consumption from countries such as China, India, and Japan.

Fluorosurfactant Market Trends

Growing Demand from the Paints and Coatings Industry

- Fluorosurfactants are amphiphilic molecules that have hydrophobic and hydrophilic parts. The hydrophobic tail is a fluorocarbon, and the hydrophilic part is characterized based on charge.

- Surfactants, often called surface-active agents, lower the surface tension between a liquid and a gas, or between a liquid and a solid, or between two immiscible phases. This lowers the surface tension of a coating, thus offering a smoother and excellent finish.

- Fluorosurfactant improves pigment and substrate wetting and leveling characteristics and provides high open time. Because of the high electronegativity of fluorine and the highly stable bond between fluorine and carbon atoms, fluorosurfactants are more stable, suitable for various conditions, and are more favored than other surfactants.

- In the United States, according to the US Census Bureau, the value of private construction in 2022 stood at USD 1,434.2 billion, 11.7% higher than USD 1,279.5 billion in 2021. Residential construction spending in 2022 was USD 899.1 billion, up 13.3% from USD 793.7 billion in 2021. Thus, the growing construction activities are anticipated to fuel the market growth.

- Further, China's paints and coating industry has outperformed the rest of the world in terms of volume growth over the last 30 years. Rapid urbanization during this time has boosted the domestic architectural coating sector to new heights owing to increasing construction activities.

- According to the National Bureau of Statistics of China, China's construction output peaked in 2022 at a value of about CNY 31.20 (~USD 4.61 trillion). As a result, these factors tend to increase the market demand.

- Moreover, Germany has the largest construction industry in Europe. The country's construction industry has been growing slowly, which is majorly driven by the increasing number of new residential construction activities. The country is home to the continent's largest building stock and is expected to continue in the foreseeable future. Germany aims to have an almost climate-neutral building stock by 2050 as part of its ongoing transition to a sustainable energy system.

- Owing to all the factors mentioned above, its market is expected to grow rapidly over the forecast period.

Asia-Pacific Region to Dominate the Market

- Asia-Pacific region is expected to dominate the market for fluorosurfactants during the forecast period due to an increase in demand from countries like China, India, and Japan.

- Fluorosurfactants are widely used in the paints and coatings industry. The increase in demand for paints and coatings in building and construction in the Asia-Pacific region is expected to drive the market.

- China hosts a vast construction sector owing to the rising demand from e-commerce, office space requirements, etc. This has resulted in increased commercial construction in China. For example, China is one of the leading countries concerning the construction of shopping centers. China has almost 4,000 shopping centers, while 7,000 more are estimated to be open by 2025. Thereby supporting the market growth during the forecast period.

- Furthermore, India is expanding its commercial sector. Several projects have been going on in the country. For instance, the CommerzIII Commercial Office Complex construction worth USD 900 million started in Q1 2022. The project involves the construction of a 43-story commercial office complex with a permissible floor area of 2,60,128 square meters in Goregaon, Mumbai. The project is expected to be completed in Q4 2027, thus benefitting the market growth during the forecast period.

- Apart from paints and coatings, fluorosurfactants are widely used in the oil and gas sector. According to the Ministry of Petroleum and Natural Gas (India), the production volume of petroleum products in the country was more than 254.3 million metric tons in 2022, reflecting an increase of more than 8% compared to 233.5 million metric tons in 2021. This, in turn, is likely to support the market growth.

- All the factors mentioned above are likely to fuel the growth of the Asia-Pacific fluorosurfactants market over the forecast period.

Fluorosurfactant Industry Overview

The fluorosurfactant market is partially fragmented in nature. The major players in the studied market (not in any particular order) include 3M, Innovative Chemical Technologies, DIC CORPORATION, The Chemours Company, and Alfa Chemicals, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Demand From the Paints and Coatings Industry

- 4.1.2 Increasing Application of Flurosurfactants in Oil Field

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Higher Price Compared to Other Surfactants

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Type

- 5.1.1 Anionic

- 5.1.2 Cationic

- 5.1.3 Non-ionic

- 5.1.4 Amphoteric

- 5.2 Application

- 5.2.1 Paints and Coatings

- 5.2.2 Detergents and Cleaning Agents

- 5.2.3 Oil and Gas

- 5.2.4 Flame Retardants

- 5.2.5 Adhesives

- 5.2.6 Other Applications (Automotive, Electronics, etc.)

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 3M

- 6.4.2 Alfa Chemicals

- 6.4.3 CYTONIX

- 6.4.4 DIC CORPORATION

- 6.4.5 DYNAX

- 6.4.6 Innovative Chemical Technologies

- 6.4.7 MAFLON S.p.A.

- 6.4.8 Merck KGaA

- 6.4.9 TCI EUROPE N.V.

- 6.4.10 The Chemours Company

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Rising Use of Fluorosurfactants in Electronics Sector

- 7.2 Other Opportunities

氟表面活性剂:全球市场份额和排名、总收入和需求预测(2025-2031年)

氟表面活性剂:全球市场份额和排名、总收入和需求预测(2025-2031年) 氟表面活性剂市场规模、份额、成长分析(按类型、应用和地区)- 2025-2032 年产业预测

氟表面活性剂市场规模、份额、成长分析(按类型、应用和地区)- 2025-2032 年产业预测 氟界面活性剂市场按类型、最终用途产业、应用、离子类型、形态和分销管道划分-2025-2032年全球预测

氟界面活性剂市场按类型、最终用途产业、应用、离子类型、形态和分销管道划分-2025-2032年全球预测 氟界面活性剂市场-全球产业规模、份额、趋势、机会及预测(按类型、应用、地区和竞争细分,2020-2030 年)

氟界面活性剂市场-全球产业规模、份额、趋势、机会及预测(按类型、应用、地区和竞争细分,2020-2030 年) 全球氟表面活性剂市场规模(按类型、应用、地区、范围和预测)

全球氟表面活性剂市场规模(按类型、应用、地区、范围和预测) 含氟界面活性剂市场规模、份额、趋势分析报告:按类型、应用、地区、细分市场预测,2024-2030

含氟界面活性剂市场规模、份额、趋势分析报告:按类型、应用、地区、细分市场预测,2024-2030 含氟界面活性剂市场 - 按类型(阴离子、非阴离子、阳离子、两性)、应用(粘合剂和密封剂、油漆和涂料、聚合物分散体、消防泡沫),2024 - 2032 年

含氟界面活性剂市场 - 按类型(阴离子、非阴离子、阳离子、两性)、应用(粘合剂和密封剂、油漆和涂料、聚合物分散体、消防泡沫),2024 - 2032 年