|

市场调查报告书

商品编码

1406093

肼:市场占有率分析、产业趋势与统计、2024年至2029年成长预测Hydrazine - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

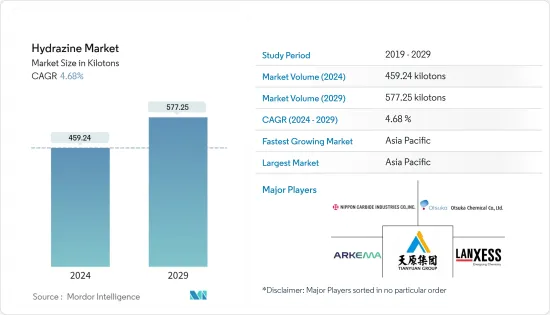

联氨市场规模预计到2024年为459.24 Kt,预计到2029年将达到577.25 Kt,在预测期内(2024-2029年)复合年增长率为4.68%。

COVID-19 大流行对市场产生了负面影响,生产和运输放缓,农化行业和其他行业由于遏制措施和经济中断而被迫推迟生产。目前市场正从疫情中恢復。预计2022年市场将达到疫情前水准并持续稳定成长。

主要亮点

- 推动市场的主要因素是农化和製药业需求的增加。

- 另一方面,肼的高毒性(例如,它会导致皮肤烧烫伤、眼睛损伤等)阻碍了市场成长。

- 在燃料电池中使用肼作为氢的替代品预计将为市场成长提供各种机会。

- 亚太地区主导全球市场,其中中国和印度等国家的消费量最高。

联氨市场趋势

製药业的需求不断增加

- 肼在多种药物应用中用作前驱物。例如,硫酸肼用于治疗癌症和治疗与恶病质相关的虚弱。

- 此外,异烟肼是一种用于治疗结核病的抗生素,是用肼製备的。根据世界卫生组织 (WHO) 的数据,六个亚洲国家的结核病患者人数最多:印度 (27%)、中国 (9%)、印尼 (8%)、菲律宾 (6%) 和巴基斯坦 (6%)。 %).),孟加拉国(4%)。

- 目前,全球製药业受到技术创新及其对世界人口健康的正面影响的推动。该行业在过去几年中取得了可观的成长。

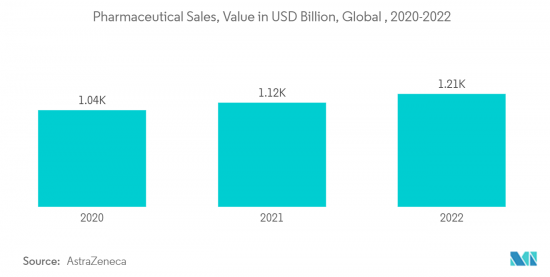

- 根据Astra Zeneca,2022年全球药品销售额为12,140亿美元,与前一年同期比较增8.4%。

- 美国、中国、印度和德国是世界上最大的製药工业国。根据药物成分公约(CPHI),美国仍是全球最大的药品市场,占全球药品支出的41%。

- 美国是大型製药、生物製药和药物开发公司的所在地,也是技术创新中心。多年的研发投资已为该行业开发治疗方法和疫苗做好了准备。此外,据Astra Zeneca称,到 2022 年,美国将占全球药品销售额的 49.8%。

- 因此,由于上述因素,预计市场在预测期内将大幅成长。

亚太地区主导市场

- 由于製药和农化行业的扩张,预计亚太地区在预测期内将成为肼的最大市场。

- 中国的医药工业也是世界上最大的工业之一。该国生产学名药、治疗药物、原料药和中药。

- 中国政府实施「健康中国2030」策略,大力开拓医疗健康产业,目标是到2030年将市场规模增加到2.4兆美元。

- 此外,2023年8月,中国国务院发布了旨在改善外商投资营商环境的24条指导意见,重点关注中国医疗保健和生物製药行业的发展。

- 此外,印度的製药业也在显着成长。根据印度投资局报告,预计2024年印度医药产业市场规模将达650亿美元,到2030年进一步达到1,300亿美元。因此,该地区的 PVP 市场预计将会成长。

- 此外,肼也被用作许多农药的前体,包括化学肥料、杀虫剂、荷尔蒙和植物生长调节剂(PGR),可保护植物和土壤、提高产量、维持和改善植物生长过程。

- 根据印度化学和化学肥料部预计,2022年印度农药产量将达29.9万吨,较2021年增加17%以上。因此,在预测期内促进了市场成长。

- 因此,上述因素显示亚太地区市场农化和製药业的成长将对预测期内的研究市场产生正面影响。

联氨行业概况

联氨市场较为分散。调查市场主要企业(排名不分先后)包括朗盛、日本碳化物工业株式会社、大冢化学、阿科玛、宜宾天元集团等。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 调查先决条件

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场动态

- 促进因素

- 农药需求增加

- 扩大在製药业的应用

- 其他司机

- 抑制因素

- 肼的高毒性

- 其他阻碍因素

- 价值链分析

- 波特五力分析

- 供应商的议价能力

- 买方议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章市场区隔(市场规模)

- 类型

- 水合肼

- 硝酸肼

- 硫酸肼

- 其他类型(如碳酸肼)

- 目的

- 缓蚀剂

- 霹雳

- 火箭燃料

- 医药原料

- 农药前驱

- 发泡

- 其他用途(发泡、推进剂等)

- 最终用户产业

- 药品

- 农药

- 工业的

- 其他最终用户产业(例如水处理)

- 地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 义大利

- 法国

- 欧洲其他地区

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东/非洲

- 沙乌地阿拉伯

- 南非

- 其他中东/非洲

- 亚太地区

第六章 竞争形势

- 併购、合资、联盟、协议

- 市场占有率(%)**/排名分析

- 主要企业策略

- 公司简介

- ACURO ORGANICS LIMITED

- Arkema

- Arrow Fine Chemicals

- BroadPharm

- Innova Corporate

- LANXESS

- MERU CHEM PVT.LTD.

- NIPPON CARBIDE INDUSTRIES CO. INC.

- Otsuka Chemical Co.,Ltd

- Tokyo Chemical Industry Co., Ltd.

- Yibin Tianyuan Group

第七章 市场机会及未来趋势

- 肼作为燃料电池中氢的替代品

- 其他机会

The Hydrazine Market size is estimated at 459.24 kilotons in 2024, and is expected to reach 577.25 kilotons by 2029, growing at a CAGR of 4.68% during the forecast period (2024-2029).

The market was negatively impacted by the COVID-19 pandemic as there was a slowdown in production and mobility, wherein agrochemical and other industries were forced to delay their production due to containment measures and economic disruptions. Currently, the market has recovered from the pandemic. The market reached pre-pandemic levels in 2022 and is expected to grow steadily in the future.

Key Highlights

- The major factor driving the market studied is the increasing demand from the agrochemical and pharmaceutical sectors.

- On the flip side, the highly toxic nature of hydrazine (such as it can cause skin burns, eye damage, etc.) is hindering the growth of the market.

- The use of hydrazine as an alternative to hydrogen in fuel cells is expected to offer various opportunities for the growth of the market.

- Asia-Pacific dominates the market across the world, with the largest consumption from countries such as China and India.

Hydrazine Market Trends

Increasing Demand from Pharmaceutical Sector

- Hydrazine is used as a precursor in several pharmaceutical applications. For example, hydrazine sulfate is used in the treatment of cancer and as a treatment for body wasting associated with cachexia disease.

- Further, Isoniazid, an antibiotic for the treatment of Tuberculosis, is prepared using hydrazine. According to the World Health Organization (WHO), the greatest number of Tuberculosis patients was found in six Asian countries, namely, India (27%), China (9%), Indonesia (8%), the Philippines (6%), Pakistan (6%), and Bangladesh (4%).

- The global pharmaceutical industry is currently driven by innovations and positive implications for the global population's health. The industry has been witnessing decent growth over the past several years.

- According to AstraZeneca, the global pharmaceutical sales in 2022 were USD 1,214 billion, representing a growth of 8.4% compared to the previous year.

- The United States, China, India, and Germany are the largest pharmaceutical industries in the world. CPHI (Convention on Pharmaceutical Ingredients) states that the United States remains the world's largest pharmaceutical market, accounting for 41% of global pharmaceutical spending.

- The United States is home to large pharmaceutical and biopharmaceutical companies, drug developers, and a center of innovation. Owing to years of investment in research and development, the industry is prepared to develop therapeutics and vaccines. Further, according to AstraZeneca, in 2022, the United States had 49.8% of global pharmaceutical sales.

- Therefore, owing to the above-mentioned factors, the market is expected to grow significantly during the forecast period.

Asia-Pacific to Dominate the Market

- The Asia-Pacific region is expected to account for the largest market for hydrazine during the forecast period owing to expanding pharmaceuticals and agrochemical industries.

- The pharmaceutical industry in China is also one of the largest in the world. The country produces generics, therapeutic medicines, active pharmaceutical ingredients, and traditional Chinese medicine.

- The government in China has implemented the "Healthy China 2030" initiative for developing the healthcare industry, which aims for the market to reach a value of USD 2.4 trillion by 2030.

- Furthermore, in August 2023, China's State Council released a 24-point list of guidelines aiming to improve the business environment for foreign investment which focuses on advancing Chinese healthcare and biopharma sectors.

- Further, in India, the pharmaceutical sector is also growing significantly. According to a report by Invest India, the pharmaceutical industry in India is anticipated to reach a market value of USD 65 billion by the year 2024, with further growth projected to reach USD 130 billion by 2030. Therefore, the PVP market is expected to rise in the region.

- Moreover, hydrazine is used as a precursor to many agrochemicals, involving fertilizers, pesticides, hormones, and plant growth regulators (PGR) that enable plant and soil protection, improve yield, and maintain and improve the growth process of plants.

- According to the Ministry of Chemicals and fertilizers (India), the pesticide production volume in 2022 accounted for 299 thousand metric tons in India, reflecting an increase of more than 17% compared to 2021. Thus boosting the market growth during the forecast period.

- Therefore, the above-mentioned factors indicate a positive influence of the growing agrochemical and pharmaceutical industry in the Asia-Pacific market on the studied market over the forecast period.

Hydrazine Industry Overview

The hydrazine market is fragmented in nature. The major players in the studied market (not in any particular order) include LANXESS, NIPPON CARBIDE INDUSTRIES CO. INC., Otsuka Chemical Co.,Ltd., Arkema, and Yibin Tianyuan Group, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand from Agrochemicals

- 4.1.2 Growing Applications in Pharmaceutical Industry

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Highly Toxic Nature of Hydrazine

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Type

- 5.1.1 Hydrazine Hydrate

- 5.1.2 Hydrazine Nitrate

- 5.1.3 Hydrazine Sulfate

- 5.1.4 Other Types (Hydrazine Carbonate, etc.)

- 5.2 Application

- 5.2.1 Corrosion Inhibitor

- 5.2.2 Explosives

- 5.2.3 Rocket Fuel

- 5.2.4 Medicinal Ingredients

- 5.2.5 Precursor to Pesticides

- 5.2.6 Blowing Agent

- 5.2.7 Other Applications (Foaming Agent, Propellants, etc.)

- 5.3 End-user Industry

- 5.3.1 Pharmaceuticals

- 5.3.2 Agrochemicals

- 5.3.3 Industrial

- 5.3.4 Other End-user Industries (Water Treatment, etc.)

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 Italy

- 5.4.3.4 France

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 ACURO ORGANICS LIMITED

- 6.4.2 Arkema

- 6.4.3 Arrow Fine Chemicals

- 6.4.4 BroadPharm

- 6.4.5 Innova Corporate

- 6.4.6 LANXESS

- 6.4.7 MERU CHEM PVT.LTD.

- 6.4.8 NIPPON CARBIDE INDUSTRIES CO. INC.

- 6.4.9 Otsuka Chemical Co.,Ltd

- 6.4.10 Tokyo Chemical Industry Co., Ltd.

- 6.4.11 Yibin Tianyuan Group

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Hydrazine as an Alternative to Hydrogen in Fuel Cells

- 7.2 Other Opportunities