|

市场调查报告书

商品编码

1406099

聚脲:市场占有率分析、产业趋势与统计、2024年至2029年成长预测Polyurea - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

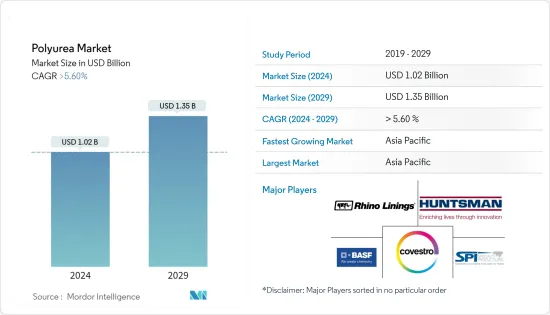

聚脲市场规模预计到2024年为10.2亿美元,预计到2029年将达到13.5亿美元,在预测期内(2024-2029年)复合年增长率将超过5.60%,预计将会如此。

由于 COVID-19 大流行,市场受到生产和流动性放缓的负面影响,因为汽车、建筑等行业因遏制措施和经济中断而被迫推迟生产。目前市场正从疫情中恢復。预计2022年市场将达到疫情前水准并持续稳定成长。

推动市场的关键因素之一是建设产业对聚脲的需求不断增长。

然而,聚脲原料价格的波动预计将阻碍市场成长。

聚脲在食品工业和饮用水应用中的使用不断增加,这可能对未来几年的市场来说是个好兆头。

预计亚太地区将主导市场,其中中国和印度等国家的消费量最高。

聚脲市场趋势

建设产业对聚脲的需求不断增长

- 聚脲是异氰酸酯组分与合成树脂共混物的反应产物经由高级聚合而获得的一类合成橡胶。

- 聚脲是保护管道免受腐蚀和外部影响的理想选择,可应用于钢製和发泡聚氨酯管道隔热材料。

- 聚脲具有对钢材和混凝土隔热的能力及其高耐用性,因此结构安全,可以使用多年而无需维修。

- 亚太地区拥有世界上最大的建筑业,由于中国和印度住宅建筑市场的不断扩大,预计亚太地区的住宅成长最快。

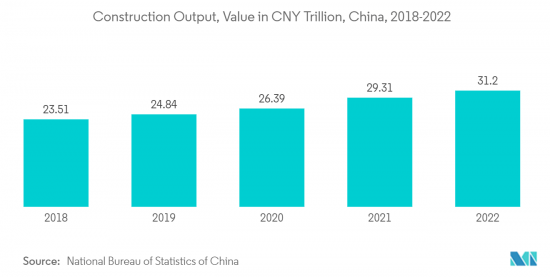

- 根据国家统计局的数据,中国的建筑产值将于2022年达到峰值,达到约31.2兆元(4.61兆美元)。结果,这些因素往往会增加市场需求。

- 印度正在扩大其商业部门。该国正在进行多个计划。例如,2022年第一季,价值9亿美元的CommerzIII商业办公综合体开工。该计划将在孟买戈尔冈建造一座43层的商业综合体。该计划预计将于 2027 年第四季完成,为预测期内的市场成长做出贡献。

- 此外,在美国,根据美国人口普查局的数据,2022年私人建筑价值为14,342亿美元,比2021年的12,795亿美元增长11.7%。 2022年住宅建设支出为8,991亿美元,比2021年的7,937亿美元成长13.3%,支撑市场成长。

- 德国也是欧洲最大的建筑业。该国的建筑业继续温和增长,主要是由于新住宅建设项目数量的增加。该国拥有欧洲大陆最大的建筑存量,预计这一趋势在可预见的未来将持续下去。作为向永续能源系统转型的一部分,德国的目标是到 2050 年使其建筑接近气候中和。

- 因此,由于上述因素,预测期内建设产业聚脲的应用很可能成为主导。

亚太地区主导市场

- 预计亚太地区将在预测期内主导聚脲市场。随着中国和印度等开发中国家的人口成长、汽车产业和建设活动的成长,对聚脲的需求预计将推动该地区的聚脲需求。

- 最大的聚脲生产国是亚太地区。聚脲生产的领导公司包括BASF股份公司、科思创股份公司和亨斯曼国际有限责任公司。

- 印度政府的目标是使汽车製造业成为「印度製造」计画的关键驱动力,预计将推动市场成长。根据印度汽车工业商协会(SIAM)统计,2022年印度小客车销售量为379万辆,较2021年小客车成长约23%。

- 在2023-2024年预算中,印度财政部长宣布拨款27亿印度卢比(约33.9亿美元)来促进住宅建设。这一分配比前上年度增加了近10%。预计这将大大推动住宅建设。

- 该地区建筑业的成长将显着提振市场。中国政府正致力于增加全国建筑业的投资,以促进整体经济成长。例如,近期增加基础建设融资的措施包括提高政策性银行贷款比例1,200亿美元。政府也考虑透过特别债券安排向地方政府提供约2,200亿美元的资金,为基础建设提供资金。

- 在日本,根据国土交通省的数据,2022年将建造约859,500套住宅,与前一年同期比较增加0.4%。

- 由于上述因素,亚太地区聚脲市场预计在研究期间将显着成长。

聚脲行业概况

聚脲市场部分整合。研究市场的主要企业(排名不分先后)包括BASF SE、Huntsman International LLC、Covestro AG、Rhino Linings Corporation、Specialty Products Inc.等。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 调查先决条件

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场动态

- 促进因素

- 建设产业对聚脲的需求不断增长

- 汽车产业的需求不断增加

- 其他司机

- 抑制因素

- 原物料价格波动

- 其他阻碍因素

- 产业价值链分析

- 波特五力分析

- 供应商的议价能力

- 买方议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章市场区隔(市场规模)

- 化学结构

- 芳香

- 脂肪族的

- 类型

- 热聚脲

- 冷聚脲

- 产品

- 衬垫

- 涂层

- 密封剂

- 最终用户产业

- 建造

- 油漆/涂料

- 车

- 工业

- 船运

- 其他最终用户产业(例如运输)

- 地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 欧洲其他地区

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东/非洲

- 沙乌地阿拉伯

- 南非

- 其他中东/非洲

- 亚太地区

第六章 竞争形势

- 併购、合资、联盟、协议

- 市场占有率(%)**/排名分析

- 主要企业策略

- 公司简介

- Armorthane

- CITADEL FLOORS

- Covestro AG

- Dorf Ketal

- Elastothane

- Huntsman International LLC

- Lonza

- Rhino Linings Corporation

- SATYEN POLYMERS PVT. LTD.(TEVO)

- Speciality Products Inc.

- Teknos Group

第七章 市场机会及未来趋势

- 聚脲在食品工业和饮用水应用的使用增加

- 其他机会

The Polyurea Market size is estimated at USD 1.02 billion in 2024, and is expected to reach USD 1.35 billion by 2029, growing at a CAGR of greater than 5.60% during the forecast period (2024-2029).

The market was negatively impacted by the COVID-19 pandemic as there was a slowdown in production and mobility wherein industries, such as automotive, construction, etc., were forced to delay their production due to containment measures and economic disruptions. Currently, the market has recovered from the pandemic. The market reached pre-pandemic levels in 2022 and is expected to grow steadily in the future.

One of the main factors driving the market is the growing demand for polyurea from the construction industry.

However, volatility in the raw material price of polyurea is expected to hinder the growth of the market studied.

The increasing use of polyurea in the food industry and drinking water application is likely to act as an opportunity for the market studied in the coming years.

The Asia-Pacific region is expected to dominate the market with the largest consumption from countries such as China and India.

Polyurea Market Trends

Growing Demand for Polyurea from the Construction Industry

- Polyurea is a kind of elastomer that results from the reaction product of an isocyanate component and synthetic resin blend through advanced development polymerization.

- Polyurea is ideal for protecting pipes and pipelines against corrosion and external influences and can be applied to both steel and polyurethane foam, which is the thermal insulation of the pipeline.

- The ability of polyurea to insulate both steel and concrete and high durability allows for secure structures without the need for renovation for many years.

- The construction sector in the Asia-Pacific region is the largest in the world, and the highest growth for housing is expected to be registered in the Asia-Pacific region, owing to the expanding housing construction markets in China and India.

- Also, according to the National Bureau of Statistics of China, China's construction output peaked in 2022 at a value of about CNY 31.20 (USD 4.61 trillion). As a result, these factors tend to increase the market demand.

- India is expanding its commercial sector. Several projects have been going on in the country. For instance, the CommerzIII Commercial Office Complex construction worth USD 900 million started in Q1 2022. The project involves the construction of a 43-story commercial office in Goregaon, Mumbai. The project is expected to be completed in Q4 2027, thus benefitting the market growth during the forecast period.

- Further, in the United States, according to the US Census Bureau, the value of private construction in 2022 stood at USD 1,434.2 billion, 11.7% higher than the USD 1,279.5 billion in 2021. Residential construction spending in 2022 was USD 899.1 billion, up 13.3% from USD 793.7 billion in 2021, thus supporting the market growth.

- In addition, Germany has the largest construction industry in Europe. The country's construction industry has been growing slowly, which is majorly driven by the increasing number of new residential construction activities. The country is home to the continent's largest building stock and is expected to continue in the foreseeable future. Germany aims to have an almost climate-neutral building stock by 2050 as part of its ongoing transition to a sustainable energy system.

- Hence, owing to the above-mentioned factors, the application of polyurea from the construction industry is likely to dominate during the forecast period.

The Asia-Pacific Region to Dominate the Market

- The Asia-Pacific region is expected to dominate the market for polyurea during the forecast period. The rising demand for polyurea, along with the growing population, automotive sector, and construction activities in developing countries like China and India, is expected to drive the demand for polyurea in this region.

- The largest producers of polyurea are located in the Asia-Pacific region. Some of the leading companies in the production of polyurea are BASF SE, Covestro AG, Huntsman International LLC, and others.

- The Indian government aims to make automobile manufacturing the main driver of the 'Make in India' initiative, which is anticipated to enhance the growth of the market studied. According to the Society of Indian Automobile Manufacturers (SIAM), a total of 3.79 million passenger vehicles were sold in India in 2022, witnessing a growth rate of around 23% compared to the passenger vehicles sold in the year 2021.

- In the budget 2023-2024, the Indian finance minister announced an allocation of INR 2.7 lakh crore (~USD 3.39 billion) for boosting housing construction. This allocation increased by nearly 10% as compared to the previous year. This will provide a significant boost to housing construction.

- The market is significantly boosted by the growing construction sector in the region. The Chinese government is focusing on enhancing investments across the construction sector in the country to boost overall economic growth. For instance, recent moves to increase financing for infrastructure construction include a USD 120 billion increase in the lending ratio of policy banks. The government is also considering allowing local governments to spend up to about USD 220 billion of the special bond quota through which local governments fund infrastructure construction.

- In Japan, according to the Ministry of Land, Infrastructure, Transport, and Tourism (MLIT) Japan, in 2022, approximately 859.5 thousand housing developments were initiated in Japan, which represented an increase of 0.4% compared to the previous year.

- Owing to the above-mentioned factors, the market for polyurea in the Asia-Pacific region is projected to grow significantly during the study period.

Polyurea Industry Overview

The polyurea market is partially consolidated in nature. The major players in the studied market (not in any particular order) include BASF SE, Huntsman International LLC, Covestro AG, Rhino Linings Corporation, and Speciality Products Inc., among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Demand of Polyurea from Construction Industry

- 4.1.2 Growing Demand from Automotive Sector

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Volatility in Raw Material Price

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Chemical Structure

- 5.1.1 Aromatic

- 5.1.2 Aliphatic

- 5.2 Type

- 5.2.1 Hot Polyurea

- 5.2.2 Cold Polyurea

- 5.3 Product

- 5.3.1 Lining

- 5.3.2 Coating

- 5.3.3 Sealants

- 5.4 End-user Industry

- 5.4.1 Construction

- 5.4.2 Paints and Coatings

- 5.4.3 Automotive

- 5.4.4 Industrial

- 5.4.5 Maritime

- 5.4.6 Other End-user Industries (Transportation, Etc.)

- 5.5 Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle East and Africa

- 5.5.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers & Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share(%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Armorthane

- 6.4.2 CITADEL FLOORS

- 6.4.3 Covestro AG

- 6.4.4 Dorf Ketal

- 6.4.5 Elastothane

- 6.4.6 Huntsman International LLC

- 6.4.7 Lonza

- 6.4.8 Rhino Linings Corporation

- 6.4.9 SATYEN POLYMERS PVT. LTD. (TEVO)

- 6.4.10 Speciality Products Inc.

- 6.4.11 Teknos Group

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Use of Polyurea in Food Industry and Drinking Water Application

- 7.2 Other Opportunities

聚脲市场按产品类型、技术类型、应用、最终用户产业和分销管道划分-2025-2032 年全球预测

聚脲市场按产品类型、技术类型、应用、最终用户产业和分销管道划分-2025-2032 年全球预测 聚脲市场依原料、产品类型、最终用途产业及地区划分

聚脲市场依原料、产品类型、最终用途产业及地区划分 聚脲的全球市场:市场规模·占有率·趋势,产业分析 (各原料·各产品·各用途·各地区),未来预测 (2025年~2034年)

聚脲的全球市场:市场规模·占有率·趋势,产业分析 (各原料·各产品·各用途·各地区),未来预测 (2025年~2034年) 全球聚脲市场规模研究,依原料(芳香族、脂肪族)、产品(涂料、衬里、黏合剂和密封剂)、应用(建筑、工业、运输)以及 2022-2032 年区域预测

全球聚脲市场规模研究,依原料(芳香族、脂肪族)、产品(涂料、衬里、黏合剂和密封剂)、应用(建筑、工业、运输)以及 2022-2032 年区域预测 2024-2028年全球聚脲市场

2024-2028年全球聚脲市场 聚脲市场规模、份额、趋势分析报告:依原料、产品、应用、地区、细分市场预测,2024-2030

聚脲市场规模、份额、趋势分析报告:依原料、产品、应用、地区、细分市场预测,2024-2030